Fixed-Point Approaches to Computing Bertrand-Nash Equilibrium Prices Under Mixed-Logit Demand: A Technical Framework for Analysis and Efficient Computational Methods.

1. Introduction

Bertrand competiton has been a prominent paradigm for the empirical study of differentiated product markets for at least twenty years. Firms engaged in Bertrand competition maximize profits by choosing prices for portfolios of differentiated products, and Bertrand-Nash equilibrium prices simultaneously maximize profits for all firms. Models combining Bertrand competition with the Mixed Logit discrete choice model of consumer demand have been used to study the automotive industry, electronics, entertainment, and food products and services; see Dube et al. (2002).

Many applications of Bertrand competition rely on counterfactual experiments: exercises in which hypothetical market conditions are simulated with an estimated model. Such experiments have been used to study corporate mergers (Nevo, 2000a), novel products and services (Petrin, 2002; Goolsbee and Petrin, 2004; Beresteanu and Li, 2008), store locations (Thomadsen, 2005), and regulatory policy changes (Goldberg, 1995, 1998; Beresteanu and Li, 2008). By definition, simulating market outcomes in counterfactual experiments requires computing equilibrium prices after changing the values of exogenous variables such as the number of firms or the products offered. Numerical methods for computing equilibrium prices have not yet received a thorough treatment in the literature, which currently focuses on model specification and estimation; see Knittel and Metaxoglou (2008); Dube et al. (2008); Su and Judd (2008) for recent developments in estimation. Morrow and Skerlos (2010) fills this gap with a detailed investigation of four approaches for computing Bertrand-Nash equilibrium prices in single-period, multi-firm models with Mixed Logit demand. This working paper provides most of the technical background for that investigation.

Applying Newton’s method to some form of the first-order or “simultaneous stationarity” condition is currently the de facto approach for computing equilibrium prices; see, for example, Nevo (1997, 2000a); Petrin (2002); Smith (2004); Doraszelski and Draganska (2006); Jacobsen (2006). Newton’s method applied directly to the first-order condition may converge when started at observed prices if changes in exogenous variables have a marginal impact on equilibrium prices. However, when the changes to exogenous variables imply significant changes in product prices Newton’s method applied directly to the first-order conditions may fail to compute equilibrium prices. Furthermore analyses that do not have observed prices to use as an initial guess will require methods with greater reliability.

Morrow and Skerlos (2010) demonstrate that solving fixed-point equations equivalent to the first-order condition for equilibrium is more reliable and efficient than solving the first-order condition itself. One fixed-point equation equivalent to the first-order conditions is the BLP-markup equation popularized by Berry et al. (1995). A second fixed-point equation, here termed the -markup equation, is a novel way to write the same condition on markups. Both markup equations lead to more robust numerical methods than found with a simple application of Newton’s method to the first-order condition. Using the fixed-point expressions in this way can be considered “nonlinearly” or “analytically” pre-conditioning the first-order condition satisfied by equilibrium prices, a technique well-known in applied mathematics (Brown and Saad, 1990; Cai and Keyes, 2002).

The existence of fixed-point equations for equilibrium suggests applying fixed-point iteration (Judd, 1998) to compute equilibrium prices, instead of Newton’s method. The BLP-markup equation does not appear to be well-suited to fixed-point iteration. Example 7 in Morrow and Skerlos (2010) provides a case in which iterating on the BLP-markup equation is not necessarily locally convergent, while iterating on the -markup equation is superlinearly locally convergent. Iterating on the -markup equation also eliminates the need to solve linear systems, required to implement Newton’s method and to iterate on the BLP-markup equation. This property makes fixed-point steps based on the -markup equation very inexpensive relative to Newton steps, an essential property to obtaining fast computations from generally linearly convergent fixed-point iterations.

Besides Newton’s method and fixed-point iteration, few other practical approaches to the computation of equilibrium prices exist. Variational formulations, widely applied in economic and engineering problems (Ferris and Pang, 1997), contain many solutions that need not be equilibria of the original problem. Explicit least-square minimization or Gauss-Newton methods can also be implemented, but are computational disadvantages relative to applications of standard Newton-type methods for nonlinear systems. Some authors apply tattonement iterating on a game’s best response correspondence to compute equilibrium in prices or other strategic variables including product mix (Choi et al., 1990), product characteristics (CBO, 2003; Austin and Dinan, 2005; Bento et al., 2005), and engineering variables (Michalek et al., 2004). Tattonement, however, has three issues: it requires the iterative computation of profit-optimal prices (a special case of the problem discussed in this article), should be inefficient relative to direct methods whenever optimal strategies are coupled, and lacks the global convergence guarantees of contemporary Newton solvers. Section 5 reviews these conclusions in more detail.

2. A Technical Framework

This section describes the mathematical framework employed in Morrow and Skerlos (2010). Several key assumptions are introduced and summarized in Table 1.

| Assumption | Purpose |

|---|---|

| 2.1 | To provide a general form for utility functions |

| 2.2 | To ensure profits are bounded and vanish as prices increase without bound |

| 2.3 | To ensure the Leibniz Rule holds, validating Eqn. (9) |

| 2.4 | To ensure that is bounded. Implies the coercivity of |

| and the existence of simultaneously stationary prices. | |

| 2.5 | To ensure that is bounded. Implies the coercivity of |

| and the existence of simultaneously stationary prices. | |

| 3.1 | To ensure that the derivatives of profit vanish as prices increase without bound |

| 3.2 | To ensure the coercivity of under weaker conditions than |

| Assumption 2.4. |

2.1. Mathematical Notation

2.1.1. Sets.

Table 2 lists some important sets and the symbols used for them. denotes the natural numbers , and denotes the natural numbers up to , that is, . denotes the set of real numbers , denotes the non-negative real numbers, and denotes the extended non-negative half-line. We denote the -dimensional simplex by , and the -dimensional “pyramid” by . Hyper-rectangles in , i.e. sets of the form for some with for all , are denoted by where and . always denotes the non-negative numbers: . For other sets, we typically use calligraphic upper case letters such as “”. For any set , denotes its cardinality. For any , denotes the set .

| Symbol | Description | ||

|---|---|---|---|

| Natural numbers | |||

| Real numbers | |||

| Non-negative real numbers | |||

| Set of product indices | |||

| Set of product characteristics | |||

| Set of individual characteristics | |||

2.1.2. Symbols.

Table 3 itemizes specific symbols used in the text.

| Symbol | Description | Defined in | ||

| Products (see Section 2.2) | ||||

| number of products | ||||

| number of non-price product characteristics | ||||

| non-price characteristics of product | ||||

| price of product | ||||

| vector of all product prices | ||||

| Individual Characteristics (see Section 2.2) | ||||

| individual characteristics, including observed | ||||

| demographics and “random coefficients” | ||||

| distribution of individual characteristics | ||||

| Choice Probabilities (see Section 2.2) | ||||

| utility of product | ||||

| utility of the outside good | ||||

| [0,1] | Logit choice probability for product | Eqn. (1) | ||

| [0,1] | Mixed Logit choice probability for product | |||

| vector of Mixed Logit choice probabilities for all | ||||

| products | ||||

| Firms, Costs, Profits, and Stationarity (see Section 2.4, 2.5) | ||||

| number of firms | ||||

| indices of the products offered by firm | ||||

| (fixed) unit cost of product | ||||

| vector of all (fixed) unit costs | ||||

| expected profits for firm | Eqn. (2) | |||

| derivative of firm ’s profits, with respect to the | Eqn. (6) | |||

| price of product | ||||

| Combined Gradient of profits | Prop. 2.2, Eqn. (7) | |||

| Choice Probability Derivatives (see Sections 2.5, 2.8) | ||||

| derivative of product ’s choice probability | ||||

| with respect to the price of product | ||||

| “intra-firm” Jacobian matrix of the choice | Eqn. (8) | |||

| probability vector | ||||

| , | matrices appearing in our decomposition of | Eqn. (9), | ||

| Fixed-Point Equations (see Sections 2.7, 2.8) | ||||

| the BLP-markup function (Berry et al., 1995) | Eqn. (13) | |||

| our -markup function | Eqn. (18) | |||

Bold, un-italicized symbols (e.g., “”) denote vectors and matrices; typically we reserve lower case letters to refer to vectors and use upper case letters to refer to matrices; the vector of choice probabilities “” is an exception. Throughout we use to denote a vector of ones of the appropriate size for the context in which it appears. always denotes the identity matrix of a size appropriate for the context. For any , denotes the diagonal matrix whose diagonal is . Any vector inequalities between vectors are to be taken componentwise: for example, means for all .

Random variables are denoted with capital letters “”, with random vectors being denoted with bold capital letters (e.g., “”). While this overlaps with our notation for matrices, it should not cause any confusion. denotes a probability and denotes an expectation. denotes the essential supremum of the (measurable) function over , with respect to the measure ; see, e.g., Bartle (1966).

always denotes the natural (base ) logarithm. We use the “Big-O” notation as follows: If there exists some such that , we say ; the point is left implicit.

2.1.3. Differentiation.

Our conventions for denoting differentiation follow Munkres (1991). We use the symbol “” to denote differentiation using subscripts to invoke additional specificity. Letting , denotes the derivative of the component function with respect to the variable and is the derivative matrix of at with components . Thus for , is a row vector. If , we define the gradient as the transposed derivative: .

2.2. Consumers, Products, and Choice Probabilities

A collection of firms offer a total of products to a population of individuals (or households). Each product is defined by a price, , and a vector of product “characteristics” . Individuals are identified by a vector of characteristics from some set . These individual characteristics can include both observed demographics and “random coefficients” (Berry et al., 1995; Nevo, 2000b; Train, 2003) that characterize unobserved individual-specific heterogeneity with respect to preference for product characteristics. The relative density of individual characteristic vectors in the population is described by a probability distribution over .

An individual identified by receives the (random) utility

from purchasing product , and

for forgoing purchase of any of these products; i.e. “purchasing the outside good.” Individuals choose the “product” with maximum utility. Here is a systematic utility function, is a valuation of the no-purchase option or “outside good,” and is a random vector of i.i.d. standard extreme value variables. Section 2.3 below gives a general specification of utility functions appropriate for equilibrium pricing. The basic requirements are that is continuously differentiable and strictly decreasing in price, and without lower bound as prices increase.

Demand for each product is characterized by choice probabilities derived from (random) utility maximization. Given the distributional assumption on , the choice probabilities for an individual characterized by are those of the Logit model (Train, 2003, Chapter 3):

| (1) |

The vector denotes the vector of all product prices. Product-specific utility functions for all , defined by for all , are used in Eqn. (1) and in the following sections. The Mixed Logit choice probabilities follow from integrating over the distribution of individual characteristics (Train, 2003, Chapter 6). The vector of Mixed Logit choice probabilities for all products is denoted by .

The examples below review several instances of this choice model. Examples 1 and 2 are used in Morrow and Skerlos (2010). Example 3 illustrates the type general specifications used in estimation. Example 4 describes one kind of “simulation” of a Mixed Logit model (Train, 2003).

Example 1.

(Boyd and Mellman, 1980) Take , denoting for and . Set and for all . is defined by specifying that and are independently lognormally distributed (with appropriately chosen signs, means, and variances).

Example 2.

(Berry et al., 1995) Take , denoting for , , and . Set

for some fixed coefficient . represents income and is given a lognormal distribution, while the random coefficients are independently normally distributed with some mean and variance. Note that income () serves as an upper bound on the price an individual can pay for any product.

Example 3.

(Nevo, 2000b) Take , denoting for , , and . Again, represents income; represents a vector of observed demographic variables (which may include income); represents a vector of random coefficients: one for each product characteristic, one for price, and one for the outside good. Set

where , , , , , and are coefficients. The distribution of is estimated from available data (e.g., Census data) and is assumed to be standard independent multivariate normal. When , the coefficient on price, is positive, an individual prefers higher prices.

Example 4.

(Simulation). Take any of the examples above, and draw vectors according to the distribution . Let and define a probability measure over by for all . Then defines a simulator of the “full” Mixed Logit model with ; see Train (2003). These approximations are essential in estimation of Mixed Logit models and in computations of equilibrium prices.

2.3. Utility Specification

This section presents a generalization of the systematic utility functions used in the examples given in the text, a specification closely related to the one introduced by Caplin and Nalebuff (1991). Morrow (2008); Morrow and Skerlos (2008) use a similar specification to analyze equilibrium prices in simple Logit models.

Assumption 2.1.

For all , there exist functions and such that the systematic utility function can be written . Furthermore there exists such that satisfies, for all and -almost every (a.e.) ,

-

(a)

is continuously differentiable, strictly decreasing, and finite

-

(b)

for all , and

-

(c)

as .

is arbitrary.

Note that we have not restricted , the distribution of individual characteristics, with Assumption 2.1. Important examples of from the econometrics and marketing literature include finitely supported distributions (often empirical frequency distributions for integral observed demographic variables), standard continuous distributions (e.g. normal, lognormal and ), truncated standard continuous distributions, finite mixtures of standard continuous distributions, and independent products of any of these types of distributions. This generality allows us to address a wide variety of otherwise disparate examples with a single notation. In particular, this generality allows us to use a single framework to treat both “full” Mixed Logit models defined by some with uncountable support and simulation-based approximations to such models.

Some existing empirical specifications violate Assumption 2.1 by admiting positive price coefficients for , where has nonzero -measure. See, for example, Nevo (2000a) (Example 3) or Brownstone et al. (2000). This implies that is increasing on . If is not decreasing for -a.e. , or at least eventually decreasing for -a.e. in the sense that there are always prices large enough to ensure that is decreasing for -a.e. , then profit-optimal pricing is not a well-posed problem and finite equilibrium prices will not exist.

The variable represents an individual-specific reservation price. As in the Berry et al. (1995) model of Example 2, this reservation price is most often derived from household or individual income. Correspondingly, is often given a lognormal distribution to (roughly) fit empirical income data. In principle, this reservation price could be related to purchasing power derived from observed demographic variables other than income, or unobserved demographic variables such as family wealth. Thus we allow this reservation price to be specified as a function of all “demographic” characteristics, . Conditions (b) and (c) in Assumption 2.1 imply that the probability an individual characterized by will purchase a product is zero for any price above and vanishes as the price approaches . We set and allow, but do not require, . For example, simulation-based approximations to the Berry et al. demand model have , as can be easily checked.

Note also that Condition (c) in Assumption 2.1 ensures the continuity of at any vector of prices with some component equal to . We must require this of the Logit choice probabilities to obtain Mixed Logit choice probabilities that are continuous on for the important class of simulation-based approximations with finitely supported . Continuous Logit choice probabilities also imply continuous Mixed Logit choice probabilities, by the Dominated Convergence Theorem.

2.4. Profits

To describe the optimal pricing problems faced by each firm we use the following notation. Let denote the number of firms. For each , there exists a set of indices that corresponds to the products offered by firm . The collection of all these sets, , forms a partition of . Subsequently, in writing “” for some , we mean the unique such that . The vector refers to the vector of prices of the products offered by firm . Negative subscripts denote competitor’s variables as in, for instance, , where , is the vector of prices for products offered by all of firm ’s competitors. Firm-specific choice probability functions are denoted by .

Two additional assumptions are required to complete the definition of firms’ profits in a manner consistent with empirical applications of Bertrand competition. First, we must specify unit and fixed costs: for each product there exists a unit cost and for each firm there exists a fixed cost . Both and depend only on the collection of product characteristics chosen by the firm, and not on the quantity sold by the firm during the purchasing period for the reasons discussed below. We let denote the vector of unit costs for the products offered by firm , and denote the vector of unit costs for all products.

Second, Bertrand competition entails the following “comittment” assumption on the quantities produced (Baye and Kovenock, 2008). Let denote the (random) quantity of product that the population will demand during the purchasing period, given prices for all products . These random demands are derived from random utility maximization. We assume each firm commits to producing exactly units of each product during the purchasing period. This implies either that there are no production capacity constraints that limit a firm’s ability to meet any demands that arise during the purchase period, or that production backlogs do not affect demand.

With the commitment and constant costs assumptions, the total cost firm incurs in producing (and selling) units of product during the purchasing period are given by the random variable

Random revenues are, of course, given by . The random variable

then gives firm ’s (random) profits for the purchasing period as a function of all product prices. Following most of the theoretical and empirical literature in both marketing and economics, we assume that firms take expected profits,

| (2) |

as the metric by which they optimize their pricing decisions in this stochastic optimization problem. Here denotes the number of individuals in the population.

Eqn. (2) demonstrates that neither the total firm fixed costs nor the population size play a role in determining the prices that maximize expected profits under the assumptions described above. Henceforth we focus on the “population-normalized gross expected profits” , referred to in the text and below as simply “profits”. Firms thus solve

| (3) | maximize | |||

Before continuing with our framework, we discuss quantity-dependent costs and clarify when profits are bounded.

2.4.1. Quantity-Dependent Costs

Including costs that depend on quantities produced is certainly possible, though this should introduce extra terms into the first-order equations presented below (Eqn. (7)). Generally speaking, unit costs that depend on the quantity produced would be expressed as , and unit costs that depended on the expected quantity produced would be expressed as . If unit costs depend on the quantity produced, then product ’s unit costs for the purchasing period (i) are random and (ii) depend on prices. To see this, simply note that product ’s unit costs for the purchasing period are . Assuming quantity-dependent costs also obscures expected profits, since there are now nonlinear terms in the formula for random profits. If unit costs depend only on the expected quantity produced, then unit costs are not random but still depend on prices: . In either case the derivatives of unit costs with respect to prices should appear in the first-order conditions. This is acknowledged in the theoretical literature. As these terms have not yet been included in the empirical literature, even when costs are assumed to depend on quantities produced (Berry et al., 1995; Petrin, 2002), we focus on costs that are independent of the quantity produced.

2.4.2. Bounded and Vanishing Profits

Here we present a technical assumption that ensures that profits are not only bounded, but vanish as all prices approach .

Assumption 2.2.

For all there exists some and some satisfying

| (4) |

such that

| (5) |

for all , -a.e.

Lemma 2.1.

If Assumption 2.2 holds, then is bounded in and vanishes as .

Proof.

We use the Dominated Convergence Theorem. Eqn. (5) ensures that vanishes -a.e. as ; see also Morrow and Skerlos (2008). Eqn. (4) ensures that

is bounded as prices approach , as we now show.

The key quantities in this integral are

the terms vanish if since vanishes. We must show that these terms are bounded as . By assumption,

for all . Thus we write

By Eqn. (4), the first term is bounded. We take , without loss of generality, so that for -a.e. and the second term is bounded. ∎

We now make some remarks regarding Assumption 2.2.

Note that if then Eqn. (5) holds for any by taking . If , Eqn. (5) admits any utility function that is (eventually) concave in price.

If , then for -a.e. . Furthermore, Eqn. (4) is trivial.

To further analyze Eqn. (4), we assume . We define , where is the -valued random variable with . If for -a.e. , then we can take . Eqn. (4) can be re-written as , or equivalently . Eqn. (4) admits any with finite expectation, and even admits any with a “fat-tailed” distribution satisfying as for some . Eqn. (4) can be written .

2.5. Local Equilibrium and the Simultaneous Stationarity Conditions

Assuming that the choice probabilities are continuously differentiable in prices, at equilibrium each firm’s prices satisfy the stationarity condition

| (6) |

Combining the stationarity condition for each firm we obtain the Simultaneous Stationarity Condition, a first-order (necessary) condition for local equilibrium prices.

Proposition 2.2 (Simultaneous Stationarity Condition).

Suppose is continuously differentiable. Let denote the “combined gradient” with components where denotes the index of the firm offering product . If is a local equilibrium, then

| (7) |

where is the “intra-firm” Jacobian matrix of price derivatives of the choice probabilities defined by

| (8) |

Prices satisfying Eqn. (7) are called “simultaneously stationary.”

The matrix has previously been denoted by “” (Berry et al., 1995; Petrin, 2002; Beresteanu and Li, 2008), “” (Nevo, 2000a), and “” (Dube et al., 2002). We prefer the “” notation to emphasize the relationship of to the Jacobian matrix of the choice probabilities , while using the superscript “” to denote the intra-firm sparsity structure.

A set of simultaneously stationary prices are a local equilibrium only if every firm’s profits are locally maximized at those prices; this can be verified by confirming that every firm’s profits are locally concave (Section LABEL:SUBSECSufficiency). Note that there is no convenient condition to verify that every firm’s profits are globally maximized at a particular local equilibrium. That is, there is no convenient condition to ensure that certain prices are a proper equilibrium.

2.6. Choice Probability Derivatives

In this section we examine the price derivatives of Mixed Logit choice probabilities. In what follows, denotes the derivative of the price component of utility, , with respect to price.

Proposition 2.3.

Fix , let be given as in Assumption 2.1 for all , and suppose the Leibniz Rule holds for the Mixed Logit choice probabilities ; that is, . Then the Jacobian matrix of is given by

| (9) |

where is the diagonal matrix with diagonal entries

and is the full matrix with entries

The intra-firm price derivatives of the Mixed Logit choice probabilities are given by where if and otherwise.

Proof.

We first characterize the Logit choice probabilities. For all we have

for any and for any (because is identically zero in a neighborhood of ). Neglecting values for the moment, we observe that these formulae and the Leibniz rule generate the desired expression for the Mixed Logit choice probabilities.

We complete the proof by considering . If has -measure zero for any , then we do not need to worry about Logit choice probability derivatives at . On the other hand if has positive -measure for some , we must assume continuity of the Logit choice probability derivatives: i.e. as . Otherwise, the Logit choice probability derivative is not defined on a set of demographics with positive measure. ∎

is closely related to a familiar economic quantity. Recall that the “inclusive value,” or expected maximum utility, conditional on demographics is given by (Small and Rosen, 1981; Train, 2003)

It is easy to see that is the derivative of the “aggregate inclusive value” with respect to the price: .

Note that and are not necessarily symmetric for all . If is independent of both and , as in the case of the Boyd and Mellman (1980) model presented in Example 1 above, then (and thus ) is symmetric for all . On the other hand if is independent of and strictly monotone in , as is the case of the strictly concave in price utility from Berry et al. (1995), then if and only if .

The following assumption gives a simple, abstract condition on that guarantees the Leibniz Rule holds and defines continuously differentiable choice probabilities.

Assumption 2.3.

Let be arbitrary and define by

Assume (i) is continuous for -a.e. ; that is, as for any . (ii) is uniformly -integrable for all in some neighborhood of any ; that is, there exists some with (that may depend on and ), such that for all in some neighborhood of .

Note that under Assumption 2.1, (i) requires only that as for -a.e. .

Proposition 2.4.

If Assumption 2.3 holds, then the Leibniz Rule holds for the Mixed Logit choice probabilities which are also continuously differentiable on .

Proof.

Taking for granted that is continuous at and the differences

| (10) |

are uniformly -integrable for small enough , the Dominated Convergence Theorem implies that

This validates the Leibniz Rule. This proof is essentially that given in a general setting by (Bartle, 1966, Chapter 5, pg. 46).

To complete the proof we must validate that is continuous in and the differences in Eqn. (10) are uniformly -integrable in a neighborhood of . It is easy to see that the desired continuity follows from Assumption 2.1 and Assumption 2.3, Condition (i). Specifically, note that for and

for . Suppose . By Assumption 2.1 (a) and (b), the first two terms are continuous. By Assumption 2.1 (c),

Assumption 2.3, Condition (i) is then necessary for the continuity of for all and . Specifically if is discontinuous at , then

To prove the integrability, we first note that for all and we have . This bound is a consequence of the formula above, and is tight as varies. The mean value theorem for functions of a single real variable states that

for some such that , and thus

for -a.e. and small enough . Thus, the desired uniform -integrability follows from Assumption 2.3, Condition (ii). ∎

An “easier” bound is simply , and thus we might consider changing the statement of Proposition 2.4 to hypothesize only the uniform -integrability of the utility price derivatives. In fact, this bound can be used to validate the Leibniz Rule for the Boyd and Mellman model of Example 1 that lacks an outside good. However, this bound fails to be useful for the Berry et al. model of Example 2, since and is singular on . In empirical applications, is onto, generating a singularity somewhere in for all ; this singularity cannot be “controlled” for all by choosing the measure . In this case, a hypothesis only about the price derivatives of utility is not useful.

We close this section by stating some basic results concerning that are used below.

Lemma 2.5.

Under Assumption 2.1, and are never zero on . Thus is nonsingular for all .

Proof.

Note that is nonempty and has positive -measure, is strictly positive on , and is strictly negative on . It follows that and are nonzero. ∎

Lemma 2.6.

Let , suppose , and define

| (11) | ||||

| (12) |

These matrices are well-defined by Lemma 2.5, and have the following properties:

-

(i)

and .

-

(ii)

and .

-

(iii)

and are strictly diagonally dominant and nonsingular.

-

(iv)

and map positive vectors to positive vectors.

Proof.

-

(i)

This follows immediately from Prop. 2.3.

-

(ii)

We note that

where is the probability distribution with density, with respect to , given by

Thus has row sums

The additional assumption that plays a role in establishing this inequality because then there is always a set with on which .

-

(iii)

The inequality

is equivalent to

The claim follows.

-

(iii)

Because maps positive vectors to positive vectors, so does its power series

∎

Corollary 2.7.

and are strictly diagonally dominant and nonsingular for .

Proof.

This follows directly from Lemma 2.6, claims (i) and (iii). ∎

2.7. The BLP-Markup Equation

A prominent form of the first-order conditions Eqn. (7) is the BLP-markup equation:

| (13) |

Note that is defined for any continuously differentiable choice probabilities with nonsingular . We have shown above that this applies to certain Mixed Logit models (Section 2.6). Eqn. (13) and Corollary 2.7 show that is well-defined and continuous, at least for .

Traditionally, the BLP-markup equation (13) has been used to estimate costs assuming observed prices are in equilibrium via the formula ; see, e.g., Berry et al. (1995) or Nevo (2000a). These cost estimates form the basis of counterfactual experiments with an estimated demand model. Beresteanu and Li (2008) have recently suggested that the BLP-markup equation is also useful for computing equilibrium prices, a suggestion we explore further below. Note that the BLP-markup equation must be interpreted as a nonlinear fixed-point equation when applied to compute equilibrium prices.

We now derive several important properties of from an alternative form of Eqn. (13) based on Lemma 2.6, valid when :

| (14) |

First, Eqn. (14) proves that profit-optimal markups are positive for the class of Mixed Logit models we consider, thanks to Lemma 2.6, claim (iv).

Corollary 2.8.

Second, Eqn. (14), rather than Eqn. (13), should be used to actually compute . Recall that denotes the 2-norm condition number of the matrix (Trefethen and Bau, 1997).

Lemma 2.9.

Proof.

This follows from Lemma 2.6, claim (i), the inequality valid for any matrices and , and the formula

∎

Lemma 2.9 states that the greater the variation in aggregate absolute rate of change in inclusive values, the more poorly conditioned is relative to . Because is diagonal, and thus the same bound applies for condition numbers in norms other than the 2-norm.

Third, Eqn. (14) also provides bounds on the magnitude of values taken by :

Proof.

This follows immediately from Eqn. (14), using the triangle inequality. ∎

The upper bound suggests the following assumptions to ensure that itself is bounded:

Assumption 2.4.

Suppose there exist and such that

| (16) | ||||

| (17) |

Under simple Logit, and . Thus Eqn. (16) is akin to concavity of for all sufficiently large , and Eqn. (17) is implied by , i.e. the existence of an outside good with positive purchase probability.

Lemma 2.11.

Unfortunately some simple models do not satisfy Assumption 2.4. A simple Logit model with for some violates Eqn. (16). More generally, the Boyd and Mellman (1980) model of Example 1 does not satisfy Eqn. (16). This is most easily seen by noting that finite-sample approximations to this model have

where are the sampled price coefficients. Of course, as , , and thus .

2.8. The -Markup function

Substituting Eqn. (9) into Eqn. (7) yields the -markup equation introduced in Morrow and Skerlos (2010):

| (18) |

when is nonsingular (Section 2.6, 2.8). Thus the -markup equation is specific to Mixed Logit models, unlike the BLP-markup equation.

We observe a relationship between the maps and .

In so far as and are distinct maps, they can generate numerical methods for the computation of equilibrium prices with entirely different properties. The equation above implies that if, and only if, lies in the null space of . Thus if is full-rank, and coincide only at simultaneously stationary prices. Simple examples of Mixed Logit models can be constructed that always have . For Logit, for all and always has rank . However the analysis in Morrow and Skerlos (2008) can be used to show that and coincide only at simultaneously stationary prices.

We now explore ’s asymptotic properties.

Lemma 2.13.

Under Assumption 2.4 whenever . Moreover as .

Proof.

We simply note that

Now if , then . Thus

To prove that , note that

For all , the term in parentheses is positive. Furthermore, this term approaches as . Thus as . ∎

A slightly different assumption concerning is useful when analyzing the map.

Assumption 2.5.

Suppose

| (19) |

Lemma 2.14.

Proof.

This follows directly from the triangle inequality and the non-negativity of and for all . ∎

2.9. Existence of Simultaneously Stationary Prices

This section provides two existence results. Neither establish the existence of a local equilibrium, or the uniqueness of simultaneously stationary points. To address the existence of local equilibrium will require additional conditions to ensure that each firm’s profits are locally concave at the simultaneously stationary prices whose existence can be ensured (Morrow, 2008). Little is known about how to address the uniqueness of simultaneously stationary points. Indeed, Morrow and Skerlos (2010) provide an example of a Mixed Logit model with 9 simultaneously stationary prices, 4 of which are local equilibria and 2 of which are proper equilibria.

Assumption 2.4 ensures the existence of finite simultaneously stationary prices when .

Corollary 2.16.

Proof.

This is a direct consequence of Brouwer’s fixed-point theorem. is a continuous map that takes the compact, convex set into itself, and thus there is at least one fixed-point . ∎

To apply Corollary 2.16 to cases when , must be extended from to all of preserving the bounds (15). This is easy for many of the simulation-based approximations encountered in practice, but difficult for the general case.

We can extend this existence result using Eqn. (22) and the map.

Lemma 2.17.

Proof.

The assumed bound implies

for any and any . Consider

If Eqn. (22) holds, then

Thus for any , there exists some and with such that

Thus

In particular, if we choose we have

for all . ∎

One consequence of this lemma is that infinite prices are never an equilibrium.

Corollary 2.18.

Under the assumptions of Lemma 2.17, any profit derivative is eventually negative.

Proof.

Note that

Since is positive for all large enough , is negative for all large enough , regardless of . ∎

Another consequence of Lemma 2.17 is an alternative existence result.

Corollary 2.19.

Under the assumptions of Lemma 2.17 there exists at least one simultaneously stationary point.

Proof.

Following Morrow and Skerlos (2008), we prove this proposition using the Poincare-Hopf Theorem (Milnor, 1965). The logic is simple: We will consider the vector field on a hyper-rectangle whose critical points are simultaneously stationary; has components defined in Lemma 2.17. The Poincare-Hopf Theorem then states that the sum of the indices of all the critical points of this vector field equals one, the Euler characteristic of . Thus it is not possible that the vector field have no critical points, for then the sum of indices would be zero.

We must only prove one property of : that this vector field points outward on the boundary of the chosen hyper-rectangle. Half of this proof is Lemma 2.17, in which we prove that if with . We must also show that if with . But

∎

This proof does not need to make any claims about the number of critical points, or of their indices. If it can be shown that any critical point of cannot have a zero or negative index, then the simultaneously stationary point is unique.

3. Computational Methods

This section provides details for the four approaches to computing equilibrium prices described in Morrow and Skerlos (2010); see Table 4. Section 3.1 briefly reviews Newton’s method, followed by application of Newton’s method to solve Eqn. (7) in Section 3.2. Newton’s method applied directly to Eqn. (7) may compute “spurious” solutions with infinite prices because the combined gradient vanishes as prices increase without bound. Section 3.3 avoids this difficulty by applying Newton’s method to the two markup equations instead of Eqn. (7) itself. Section 3.4 discusses fixed-point iterations based on the BLP- and -markup equations, and Section 3.5 reviews a number of practical considerations.

| Newton Methods (NM) | ||||

| Abbr. | Method | Section | Advantage | Our Experience |

| CG-NM | Solve | 3.2 | Unreliable, slow | |

| -NM | Solve | 3.3 | Coercive | Reliable, slow |

| -NM | Solve | 3.3 | Coercive | Reliable, slow |

| Fixed-Point Iterations (FPI) | ||||

| Abbr. | Method | Section | Advantage | Our Experience |

| -FPI | Iterate | 3.4 | Easy to evaluate | Reliable, fast |

| -FPI | Iterate | 3.4 | Not convergent | |

| (a) Conclusions on behavior of these methods is based on the numerical experiments | ||||

| described in Morrow and Skerlos (2010), using a novel GMRES-Newton method with | ||||

| Levenberg-Marquardt style trust-region global convergence strategy. | ||||

3.1. Newton’s Method

Newton’s method, a classical technique to compute a zero of an arbitrary function , is now a portfolio of related approaches to solve nonlinear systems (Ortega and Rheinboldt, 1970; Kelley, 1995; Dennis and Schnabel, 1996; Judd, 1998; Kelley, 2003). Generally speaking, Newton-type methods are differentiated in two relatively independent directions: (i) the technique used to approximate the Jacobian matrices and solve for the Newton step and (ii) the technique used to enforce convergence from arbitrary initial conditions. See Dennis and Schnabel (1996), Judd (1998), or Kelley (2003) for good treatments of these issues. Choosing the right variant of Newton’s method determines the reliability and efficiency of equilibrium price computations.

Problem formulation also determines the reliability and efficiency of equilibrium price computations using Newton’s method. Scalings of the variables and function values are one prominent example of a problem transformation that improves the performance of Newton’s method (Dennis and Schnabel, 1996). Nonlinear problem preconditioning can also be important (Cai and Keyes, 2002), as the following example demonstrates.

Example 5.

Let be defined by . Iterating Newton steps converges to the unique (finite) zero only from initial conditions with . Newton’s method diverges or fails for all other starting points. Standard global convergence strategies for Newton’s method (line search, trust region methods) cannot improve this poor global convergence behavior because has unbounded level sets; see Morrow and Skerlos (2010) for details.

A simple nonlinear transformation overcomes this poor global convergence behavior. Note that where and . Because is nonsingular for all , the problems and have identical solution sets. However applying Newton’s method to the problem trivially converges in a single step from any initial condition without a global convergence strategy.

3.2. Newton’s Method on the Combined Gradient

The most direct approach to compute equilibrium prices using Newton’s method is to solve , abbreviated CG-NM in Table 4. This approach works well when the initial condition is near an equilibrium, as required by theory (Ortega and Rheinboldt, 1970; Kelley, 1995; Dennis and Schnabel, 1996). In practice, computing counterfactual equilibrium prices starting with the observed prices may exploit this local convergence if changes to exogeneous variables have a relatively small impact on equilibrium prices. On the other hand, CG-NM can be unreliable when started “far” from equilibrium.

The challenge is the tendency for the derivatives of profits to vanish as prices become large Morrow and Skerlos (2010), as demonstrated in Example 6 below.

Example 6.

Consider a simple Logit model with linear in price utility and an outside good: for some and any , and . The derivative of firm ’s profit function with respect to the price of product is

Since and both vanish as (as is easily checked), is bounded in . Thus as .

We now provide a general assumption under which as .

Assumption 3.1.

Let be defined as in Assumption 2.3. Assume: (i) as for -a.e. . (ii) There exists and such that for all .

As with Assumption 2.3 above, (i) and (ii) are essentially conditions for the Dominated Convergence Theorem.

Assumption 3.1 (i) extends Assumption 2.3 (i) to include a neighborhood of . Note that if then (i) holds if, and only if, as ; i.e. is continuous at . Thus if Assumption 3.1 (i) and Assumption 2.3 (i) are the same. If and as , then necessarily as . The converse, however, need not hold.

If , Assumption 3.1 (ii) simply says that is bounded as . This is not implied by Assumption 2.3 (ii), but is a natural extension of it.

Lemma 3.1.

Proof.

Let be any sequence converging to . Define by . The functions converge pointwise to zero and have integrals uniformly bounded by the constant . By the Dominated Convergence Theorem

∎

In other words, under Assumption 3.1 the components of vanish as the corresponding price tends to even though this may not mean that maximizes profits. Because of this, CG-NM may converge to a zero of at , or with some components equal to , that is not an equilibrium.

Note that even though the price derivatives vanish at infinity, this does not mean that infinite prices maximize profits. Nonetheless, CG-NM may converge to a zero of with some components equal to infinity that is not an equilibrium. Moreover, because the components of can vanish over some divergent sequences, standard global convergence strategies based on minimizing will not be effective ways of avoiding this behavior. As in Example 5, we must reformulate the problem to obtain reliable and efficient approaches for computing equilibrium prices.

3.3. Newton’s Method and the Markup Equations

Reliable and efficient implementations of Newton’s method are found by observing that the combined gradient, , can be written as follows:

| (20) | where | ||||||

| (21) | where |

Either or can be used to compute simultaneously stationary prices when and , respectively, are nonsingular (Morrow and Skerlos, 2010). Of course, and recast the first-order condition as a fixed-point problem: is zero if and only if the BLP-markup equation holds, and is zero if and only if the -markup equation holds.

Solving or , abbreviated -NM and -NM respectively in Table 4, requires the solution of nontrivial nonlinear systems with Newton’s method. -NM and -NM, however, are less likely to have the computational problems that CG-NM exhibits because they exploit norm-coercivity of the maps and (Morrow and Skerlos, 2010). A norm-coercive map has a norm that tends to infinity with the norm of its argument (Ortega and Rheinboldt, 1970; Harker and Pang, 1990). Globally convergent implementations of Newton’s method that decrease the value of in each step produce bounded sequences of iterates when is norm-coercive. Thus, solving the BLP- or -markup equation instead of the literal first-order condition removes the tendency for applications of Newton’s method to compute “spurious” solutions at infinity.

We now prove that the maps and are indeed coercive.

Lemma 3.2.

Proof.

Proof.

Assumption 3.2.

Suppose that and

| (22) |

Note that the limit is of a non-increasing sequence of non-negative numbers, and thus exists.

Lemma 3.4.

Assuming Eqn. (22) is equivalent to assuming that for any sequence with , .

Proof.

If Eqn. (22) holds, then for any there exists an such that

If , then there is also an such that for all . Thus

for all , and thus

Conversely, if Eqn. (22) fails, then there is a such that

for all . We can thus choose with satisfying

In other words,

for all , and thus

Hence the “sequence version” of Eqn. (22) fails, and thus by contraposition the sequence version and Eqn. (22) are identical. ∎

Proof.

Now we prove the alternative coercivity result.

Proof.

We prove the claim for ; the result for then follows from Lemma 2.15. Note that

Suppose that . By assumption,

while the second term is bounded. Thus

∎

Note that since we did not require that Eqn. (17) held, need not be bounded for and to be coercive.

3.4. Fixed-Point Iteration

In addition to applications of Newton’s method, the BLP- and -markup equations suggest applying fixed-point iteration to solve for equilibrium prices. We examine fixed-point iterations based on both equations.

3.4.1. Fixed-Point Iteration

The fixed-point iteration based on the -markup equation, here abbreviated -FPI, can efficiently compute equilibrium prices for some problems. -FPI has relatively efficient steps because no linear systems need to be solved, unlike every other method listed in Table 4. While we are not aware of a general convergence proof for -FPI, this iteration has converged reliably on test problems including the examples in Morrow and Skerlos (2010).

The first observation we make is that the -FPI steps always point in directions of “myopic gradient ascent.”

Lemma 3.7.

Let , and let denote the -FPI step. Then

Similarly, let denote the angle between and , and suppose is not simultaneously stationary. Then

Proof.

Both results follows directly from the equation where denotes the absolute value of the components of . ∎

Specifically, the -FPI steps have a positive projection onto the combined gradient, and cannot become orthogonal to the combined gradient over any sequence of non-simultaneously stationary prices that stay in .

If , and the equilibrium problem is an optimization problem, this implies -FPI has steps that point in gradient ascent directions and, when properly scaled, converge to local maximizers of profit. More specifically, -FPI cannot converge to minimizers of profits. This may generate the properties of -FPI observed in Example 10 from Morrow and Skerlos (2010).

Proof.

By Lemma 2.13, for any sufficiently large we can find some such that

If the -FPI sequence diverges, then for any such there is an such that

But then

which states that the -FPI sequence is decreasing. This is a contradiction of the hypothesis that the -FPI sequence diverges. ∎

To implement -FPI, one simply needs to iterate the assignment where Eqn. (18) defines . As shown in Table 5 below, integral approximations, rather than the actual computation of the step, drive the computational burden. Given a price vector, utilities, and utility derivatives, computing , , and for a set of samples requires floating point operations (flops), while the fixed-point step itself only requires flops. Note that computing the fixed-point step requires an equivalent amount of work as computing the combined gradient . Furthermore, because is a diagonal matrix, no serious obstacles to computing the fixed point step arise as becomes large.

3.4.2. Fixed-Point Iteration

The fixed-point iteration , abbreviated -FPI, based on the BLP-markup equation need not converge. Example 7 below, repeated from Morrow and Skerlos (2010), gives a case in which can fail to be even locally convergent.

Example 7.

Consider multi-product monopoly pricing with a simple Logit model having for some , any , and . It is well known that for a single-product firm, unique profit-maximizing prices exist (Anderson and de Palma, 1988; Milgrom and Roberts, 1990; Caplin and Nalebuff, 1991). Morrow (2008) proves that profit-optimal prices are unique for the multi-product case and even so with multiple firms even though profits are not quasi-concave (Hanson and Martin, 1996).

In this example, -FPI is not always locally convergent near , while -FPI is always superlinearly locally convergent. For an arbitrary continuously differentiable function and , is contractive on some neighborhood of in some norm if where (Ortega and Rheinboldt, 1970). We show that may hold while , where denotes the spectral radius of the matrix .

The components of the BLP-markup function are given by for all . From this formula the equation

can be derived. For valuations of the outside good, , sufficiently close to , can hold; see Morrow and Skerlos (2010) for details.

To prove the claim regarding , note that , and thus for all .

Even if the BLP-markup equation does generate a convergent fixed-point iteration, evaluating involves the solution of linear systems that grow in size with the number of products offered by the firms. The work required to evaluate using a direct method like PLU or QR factorization is , given values of , , and as approximated using simulation. The work to evaluate is only given , , and (Table 5). Generally speaking, function evaluations must be cheap for the linear convergence of fixed-point iterations to result in faster computations than the superlinearly or quadratically convergent variants of Newton’s method.

3.5. Practical Considerations

This section addresses several practical considerations.

3.5.1. Simulation

Any method for computing equilibrium prices under Mixed Logit models faces a common obstacle: the integrals that define the choice probabilities () and their derivatives () cannot be computed exactly. We employ finite-sample versions of the methods discussed below by drawing samples from the demographic distribution and applying the method to the finite-sample model thus generated. Particularly, these samples are used to compute approximate , , and ; see Table 5. These samples are kept fixed for all steps of the method and, in principle, can be generated in any way. We draw directly from the demographic distribution, although importance and quasi-random sampling (e.g., see Train (2003)) can also be employed. The Law of Large Numbers motivates this widely-used approach to econometric analysis (e.g., see McFadden (1989) and Draganska and Jain (2004)). While all numerical approaches for computing equilibrium prices described here rely on a Law of Large Numbers for simultaneously stationary prices, we do not provide a formal convergence theorem. We do provide numerical evidence that computed equilibrium prices based on the fixed-point iteration for our examples do indeed follow such a law.

3.5.2. Truncation of Low Purchase Probability Products

All of the methods we implement can be built to ignore products with excessively low choice probabilities. That is, one can ignore price updates for all products with , where is some small value (say ). Products with a choice probability this small (or smaller) need not be considered a part of the market in the price equilibrium computations. For example, Wards (2007) reports total sales of cars and light trucks during 2005 as . Particularly, 7,667,066 cars and 9,280,688 light trucks. Because expected demand is defined by , any ignores any vehicle that, as priced, is not expected to have a single customer out of the millions of customers that bought or considered buying new vehicles. There are also technical reasons for this truncation. Particularly, and become singular as , for any . Truncating avoids this non-singularity and hopefully helps conditioning.

3.5.3. Termination Conditions

We terminate all iterations with the numerical simultaneous stationarity condition where is some small number (e.g., ). Note that a standard application of Newton’s method to solve or would terminate when either

| (23) |

respectively. For example, Aguirregabiria and Vicentini (2006) use the condition . Ensuring that Eqn. (23) holds does not necessarily imply that , the strictly interpreted first-order condition.

Because

it is easy to terminate all methods, CG-NM, -NM, -NM, and -FPI, when . While this is done here to ensure consistency in our comparisons of different methods, should always be the termination condition for price equilibrium computations.

Three other standard termination conditions are used (Brown and Saad, 1990; Dennis and Schnabel, 1996). We terminate the iteration if the (relative) step length becomes too small, if a maximum number of iterations is exceeded, or if an exceptional event occurs (e.g. division by zero). These three conditions are considered “failure” as the iteration has failed to compute a numerically simultaneously stationary point in the sense of the first termination condition.

3.5.4. Second-Order Conditions.

Each method in Table 4 finds simultaneously stationary points, rather than local equilibria. Unlike in optimization, there is no a priori assurance that first-order iterative methods for equilibrium problems will converge to certain types of stationary points. Thus in computing equilibria it is vitally important to check the second-order sufficient conditions to verify that a local equilibrium has indeed been found.

In local equilibrium every firm’s profit Hessian, , should also be negative definite. The formulas given in Proposition 3.9 below provide an expression for that we use to check the second-order sufficient condition. Cholesky factorization, rather than direct approximation of the spectrum, is used to test the negative definiteness of (Golub and Loan, 1996).

3.5.5. Computational Burden

Table 5 reviews the formulae and computational burden of computing , , and .

| Quantity | Formula | flops |

|---|---|---|

| Total work to compute , , and | ||

| (a) “” here denotes element-by-element multiplication. | ||

Computing and applying Newton’s method to requires solving linear systems. We give some more details regarding these computations here. As stated above, the linear system

should be used to solve for . Note also that only the systems

for all need be solved. Of course, our condition bound applies within firms as well:

If Householder QR factorization is used to solve these systems, then computing from , , and requires flops (Table 5).

This is a significant increase in computational effort relative to computing or . The diagonal dominance of , indeed of itself, suggests that Jacobi, Gauss-Seidel, and Successive Over-Relaxation (SOR) iterations (Golub and Loan, 1996) may be a relatively efficient way to compute .

Additional work is required to compute , if this is to be used in Newton’s method. Though it requires solving a matrix-linear system of the type , the required matrix factorizations of need only be computed once to compute both and , but must be updated for each vector of prices.

3.6. Computing Jacobian Matrices for Newton’s Method

Standard “exact” or Quasi-Newton methods to solve either always or periodically require the Jacobian matrix . Using finite differences to approximate Jacobian matrices requires evaluations of the function , an unacceptable workload. In the 993 vehicle example from Morrow and Skerlos (2010), approximating once with finite differences would take roughly 993 evaluations of , when the work of less than 50 evaluations appears to sufficient to converge to equilibrium prices using the -FPI.

We recommend directly approximating using integral expressions for , , and provided below. An alternative is to use automatic differentiation, but we are skeptical that this would in fact be faster than the direct formulae provided here.

3.6.1. Jacobian of the Combined Gradient

Assuming a second application of the Leibniz Rule holds, we can derive integral expressions for the second derivatives through

Proposition 3.9.

Let be twice continuously differentiable in and suppose a second application of the Leibniz Rule holds for the Mixed Logit choice probabilities at . Set

-

(i)

Component form: Setting

we have

-

(ii)

Matrix form: Let , and be the matrices of these quantities. Also set

and

Then

(24)

Proof.

To see that this only relies on a second application of the Leibniz Rule to the choice probabilities, note that

and thus the continuous second-order differentiability of depends only on the second-order continuous differentiability of . This result is then an immediate consequence of the validity of the Leibniz Rule, if a bit tedious to derive. ∎

The validity of a second application of the Leibniz Rule to the choice probabilities is ensured by the following condition.

Proposition 3.10.

Let be such that

-

(i)

is twice continuously differentiable for all and -a.e.

-

(ii)

for all , is uniformly -integrable for all in some neighborhood of .

-

(iii)

for all ,

is uniformly -integrable for all in some neighborhood of .

Then a second application of the Leibniz Rule holds for the Mixed Logit choice probabilities, which are also continuously differentiable on .

This is proved in the same manner as Proposition 2.4.

We also observe the following.

Proposition 3.11.

If then for all .

The proof follows from the derivative formulae given above. Of course, if then as well and we have the following situation: (i) the Newton system is consistent for any and (ii) does not depend on for all . Thus, in practice one can restrict attention to the Newton step defined by the submatrix of formed by rows and columns indexed by .

The formulae above give the following expression of the profit Hessians.

Corollary 3.12.

Let be twice continuously differentiable in and suppose a second application of the Leibniz Rule holds for the Mixed Logit choice probabilities. Firm ’s profit Hessian is given by

3.6.2. The map.

For , we have where solves the linear matrix equation

Here . This is easily derived from the defining formula .

3.6.3. The map.

For , we have where can be computed using the following formula:

4. The GMRES-Newton Hookstep Method

In this section we provide some details regarding the GMRES-Newton Hookstep method employed in Morrow and Skerlos (2010). For complete details, see Morrow10b.

4.1. Inexact Newton Methods

A strong theory of “Inexact” Newton methods exists for the solution of systems of nonlinear equations when there are “many” variables. Inexact Newton steps are simply “inexact” solutions to the Newton system; that is, an inexact Newton step is any vector that satisfies

| (25) |

for some fixed (Dembo et al., 1982; Brown and Saad, 1990; Eisenstat and Walker, 1994, 1996; Pernice and Walker, 1998). The name “truncated” Newton method has also been used for the specific case when the inexactness comes from the use of iterative linear system solvers like GMRES (Saad and Schultz, 1986; Walker, 1988) or BiCGSTAB (van der Vorst, 1992; Sleijpen and Fokkema, 1993). We focus on GMRES, a particularly simple yet strong iterative method for general linear systems that has been consistently used in the context of solving nonlinear systems (Brown and Saad, 1990).

By appropriately choosing a sequence of ’s, the local asymptotic convergence rate of an inexact Newton’s method can be fully quadratic (Dembo et al., 1982; Eisenstat and Walker, 1994). Of course, taking to achieve the quadratic convergence rate will also require increasingly burdensome computations of inexact Newton steps that satisfy increasingly strict inexact Newton conditions. On the other hand, can be chosen to be a constant if a linear locally asymptotic convergence rate is suitable (Pernice and Walker, 1998).

Generally speaking there are three reasons to adopt the inexact perspective. First, direct methods like QR factorization may not be the most effective means to solve the Newton system when this system is large, because of computational burden and accumulation of roundoff errors. Instead, iterative solution methods are often used to solve linear systems with many variables; see, e.g. Trefethen and Bau (1997). Second, iterative methods like GMRES require only matrix-vector products that can be approximated with finite directional derivatives (Brown and Saad, 1990; Pernice and Walker, 1998). Thus inexact Newton’s methods can be “matrix-free”; see Section 4.3.4 below. Third, Newton steps often point in inaccurate directions when far from a solution (Pernice and Walker, 1998). Thus solving for exact Newton steps may involve wasted effort, especially when there are many variables.

matlab’s fsolve function implements a related approach using the (preconditioned) Conjugate Gradient (CG) method applied to the normal equation for the Newton system, . Use of the normal equations is required because CG is applicable only to symmetric systems (Trefethen and Bau, 1997). Note that this requires that the Jacobian is explicitly available. Although this holds for price equilibrium problems under Mixed Logit models, it can be a significant restriction for general problems. By requiring products in each step of the iterative linear solver, this approach also increases the work by flops where the solver takes steps. Finally, this approach can also be less accurate: using the normal equation squares the linear problem’s condition number, and thus risks serious degradation in solution quality (Trefethen and Bau, 1997). Pernice and Walker (1998) describe a similar approach using BiCGSTAB: the extension of CG to non-symmetric systems.

4.2. GMRES

The “Generalized Minimum Residuals” or GMRES method (Saad and Schultz, 1986) solves a linear system by using the Arnoldi process to compute an orthonormal basis of the successive Krylov subspaces and then takes approximate solutions from those subspaces having least squares residuals. See Trefethen and Bau (1997) for a good introduction to Krylov methods in general, including the Arnoldi process and GMRES. In the stage, GMRES “factors” as where is an orthonormal basis for , is an orthonormal basis for , and is upper-Hessenberg. Any vector can be written for some and thus the least-squares residual problem becomes

The orthonormal basis is typically chosen so that for some , and hence the GMRES solution where solves . This least squares problem can be solved using the QR factorization of . Furthermore this factorization can be efficiently updated in each iteration, instead of computed from scratch. Moreover the actual solution vector need not be formed until the residual is suitably small.

4.2.1. Householder GMRES

We have implemented a variant of GMRES based on Householder transformations due to Walker (1988); this is also the version implemented in matlab’s gmres code. We have verified that our implementation generates results matching matlab’s implementation. In this version of the GMRES process applied to the generic problem , Householder reflectors are used to generate the orthonormal matrices

satisfying

where is

for upper Hessenberg and . is chosen to satisfy where , and hence . The approximate solution is taken to be where solves

Again these problems can be solved cheaply by updating QR factorizations with Givens rotations. Neither the solution vector nor the residual vector be formed until GMRES converges. An efficient implementation requires flops and a matrix multiply in the iteration, so that taking iterations requires of “overhead” in addition to the work required for the matrix multiplications (using the actual Jacobians). So long as , using GMRES with the actual Jacobians is cheaper than solving for the actual Jacobian with QR. With small , as we achieve using and , the savings is quite substantial.

We note the following formulae specific to the Newton system case. For and , and so that

Moreover, for all so that

4.2.2. Preconditioning

As is well known, preconditioning is key to the effectiveness of iterative linear solvers; see Golub and Loan (1996). We have not found the linear systems in -NM or -NM to need preconditioning. However we have found the preconditioned system

| (26) |

to be very necessary for rapid solution of the Newton system in CG-NM. This preconditioner is motivated by the following relationship of the Jacobian of to the Jacobian of in equilibrium.

Lemma 4.1.

for any simultaneously stationary .

Proof.

This follows from differentiating via the product rule, recognizing that in equilibrium and . ∎

In other words, Newton’s methods applied to preconditioned as above ends up being essentially the same iteration as , close enough to equilibrium.

GMRES, if used successfully on this preconditioned system Eqn. (26), will ensure that

| (27) |

for some . This is distinct from the inexact Newton condition Eqn. (25). The following proposition gives modified tolerances for the preconditioned system to ensure satisfaction of the original system.

Proposition 4.2.

This is a consequence of the following general result, which we state without proof.

Lemma 4.3.

Let and be nonsingular. Then

| (29) |

where is given by

This implies that

Note that the preconditioned system must always be solved to a stricter tolerance than is desired for the un-preconditioned system using this bound. Additionally, computing for a generic preconditioner relies on the ability to compute .

Eqn. (29) also implies that if Eqn. (27) holds with , then

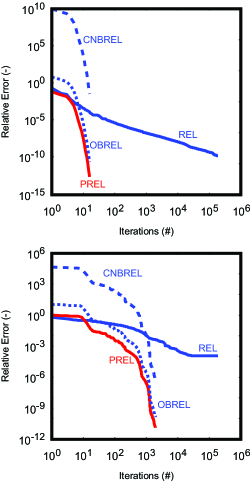

where is the (2-norm) condition number of . This equation, while the more compact representation, can also be overly conservative as clearly illustrated in Fig. 1. It is unlikely that is a tight upper bound on the multiplier in Eqn. (28). In fact, the multiplier on depends only on the norm of at a single point on the surface of the unit sphere in rather than , the maximum norm of over this entire sphere. Our examples in Fig. 1 bear this out, having condition numbers many orders of magnitude larger than the multiplier in Eqn. (28).

The power of the preconditioning is that the preconditioned system Eqn. (27) appears to be solved to a relative error of much faster than the original system can be solved to a relative error of , even though . As can be seen in Fig. 1, solving the preconditioned system to can achieve a relative error in the original system below in roughly four orders of magnitude fewer iterations than solving the original system to this same relative error for prices near equilibrium. Away from equilibrium, GMRES may not be able to solve the original system to small relative errors like at all. Thus using the original system would appear to slow, if not halt, an implementation of the inexact Newton’s method.

4.3. The GMRES Hookstep

Suitable modifications of each of the globalization strategies originally developed for “exact” Newton methods can be applied in the inexact context. Brown and Saad (1990) directly extend line search and a dogleg steps to GMRES-Newton methods. Eisenstat and Walker (1996) and Pernice and Walker (1998) apply a safeguarded backtracking line search to facilitate global convergence. More recently, Pawlowski et al. (2006, 2008) have studied dogleg steps suitable for GMRES-Newton methods in some detail. Finally Viswanath (2007) has derived an elegant version of the hookstep method suitable for GMRES-Newton methods. In contrast with the hookstep approach for the “exact” Newton method with Jacobian , Viswanath’s approach requires computing the SVD only of a matrix whose size is determined by the number of iterations taken by GMRES. For reasonable applications of GMRES, this can be far less than the size of itself. For the examples in Morrow and Skerlos (2010), the size difference is roughly two orders of magnitude: the GMRES-Newton hookstep worked with roughly instead of matrices. Thus, the GMRES-hookstep can accumulate a tremendous savings over an exact-Newton implementation of the hookstep method. Again, each of these approaches iterates until an acceptable step is found, and can, in principle, involve many additional evaluations of or fail to find an acceptable step altogether.

Here we describe an implementation of the Levenberg-Marquardt method or “hookstep” (Dennis and Schnabel, 1996) suitable for GMRES as first suggested by Viswanath (2007). See also Viswanath (2009); Viswanath and Cvitanovic (2009); Halcrow et al. (2009). First, we recall the basic structure of model trust region methods; see (Dennis and Schnabel, 1996, Chapter 6, Section 4). We then adopt this structure to the case of Krylov subspace methods, particularly GMRES. Again, see Morrow10b for a more detailed discussion of this method.

4.3.1. Model Trust Region Methods.

Trust region methods assume that for steps satisfying , the function

is an accurate local model of for suitably small steps. Note that is not the usual, quadratic model of derived from a Taylor series because (Dennis and Schnabel, 1996, pg. 149). The idea is to solve

| (30) |

The solution is given as follows: take if ; if , take where

and is the unique such that . These follow from the standard optimality conditions, or rather that the gradient must lie in the negative normal cone to at (Clarke, 1975); see (Dennis and Schnabel, 1996, Lemma 6.4.1, pg. 131).

Solving the problem above exactly generates the Levenberg-Marquardt method (Levenberg, 1944; Marquardt, 1963) or “hookstep.” By computing the SVD of we can easily solve for when (Dennis and Schnabel, 1996); see (Golub and Loan, 1996, Section 12.1, pgs. 580-583) for closely related results. Let . We can then set where

A simple single-dimensional iteration can then be used to solve for the unique such that . Morrow10b derives two globally convergent methods for this task using Newton’s method and a nonlinear local model (Dennis and Schnabel, 1996). The difficulty here is computing the SVD of , requiring flops (Golub and Loan, 1996, Chapter 5, pg. 254).

The step computed by either approach is acceptable if it generates sufficient decrease in the squared 2-norm of . Specifically, fix , , and . If

then and a the step length bound is expanded to for the next iteration. Otherwise, is chosen from and the corresponding is computed. While this process of specifying an acceptable is iterative, much of the work required to build a trial step does not need to be repeated. Specifically the SVD required for the hookstep does not change (so long as it was computed in a previous iteration) while in the doglep step the Newton and Cauchy steps remain the same. However every time the step size bound is decreased must be re-evaluated at the new trial step, with a computational burden equivalent to taking a fixed-point step.

4.3.2. Model Trust Region Methods on a Subspace

A Krylov method for solving builds approximate solutions in the successive Krylov subspaces . This has the effect of further constraining the local model problem (30) to

| (31) |

For any with orthonormal columns (generated by GMRES or not) we can set and restrict attention to the trust region problem . See (Brown and Saad, 1990, pgs. 149-150). The first-order conditions for this problem are equivalent to either

-

(i)

and

-

(ii)

or for and some .

By the definition of , (i) implies

and (ii) implies

Note that these are square problems that can be solved exactly.

4.3.3. The GMRES-Newton Hookstep

Using GMRES started at zero, and . Thus we consider the family of linear systems

defined for all .

By computing the (“thin”) Singular Value Decomposition of , where , , and , we can easily solve each such problem. See (Golub and Loan, 1996, Section 12.1, pgs. 580-583) for closely related results. Particularly,

is solved by where

Because the diagonal elements of are positive, is well defined for all . Note also that we only need the first row of , but all of , to compute .

In particular, . Invoking the full SVD of ,

for some , we can write

We thus see that solves the GMRES least squares problem

with residual . is unique: First, note that is a unit vector in the span of a single vector, say , that is orthogonal to the span of the columns of . There are only two unit vectors in this span, specifically , and thus . Thus .

It is also easy to see that

where is the first row of and for . That is, the Householder GMRES-Newton Hookstep always lies in a descent direction for the globalizing objective .

4.3.4. Directional Finite Differences

Recall that one advantage to using an iterative solver like GMRES to solve the Newton system is that only products of the type will be required to solve the Newton system for at (Brown and Saad, 1990; Pernice and Walker, 1998). Such products can be approximated by a single additional evaluation of in a “directional” finite difference (Brown and Saad, 1990; Pernice and Walker, 1998). For example, the first-order formula

requires only a single additional evaluation of per (approximate) evaluation of . Higher-order formulae requiring 2 and 4 additional evaluations of are easy to derive; see Pernice and Walker (1998). In their implementation of the GMRES method in the context of an inexact Newton method, Pernice and Walker (1998) only use higher order finite-differencing formulas at restarts. Brown and Saad (1990) provide a practical formula for computing an appropriate value of .

Since directional finite derivatives must be repeated at each step of iterative linear solvers, each step of an iterative Newton system solver using directional finite differences could be at least as expensive as a -FPI step. That is, if an iterative solver should take 100 steps to compute an inexact Newton step having small enough residual to satisfy the inexact Newton condition, then we could have equivalently taken 100, 200, and 400 -FPI steps with the first, second, and fourth order formulae available in Pernice and Walker (1998). In our examples, using GMRES regularly solves the -NM and -NM Newton systems in approximately 10 steps. This implies that each -NM and -NM step is roughly equivalent to -FPI steps.

In the Newton context, whether efficiency is ultimately gained by using directional finite differences instead of computing the Jacobian matrices and using standard matrix-vector products depends on the number of steps taken by the iterative linear solver. If GMRES takes iterations to find an inexact Newton step for , computing and using the Jacobian requires flops while using directional finite differences requires flops.