Non-asymptotic deviation inequalities for smoothed additive functionals in non-linear state-space models.

Abstract

The approximation of fixed-interval smoothing distributions is a key issue in inference for general state-space hidden Markov models (HMM). This contribution establishes non-asymptotic bounds for the Forward Filtering Backward Smoothing (FFBS) and the Forward Filtering Backward Simulation (FFBSi) estimators of fixed-interval smoothing functionals. We show that the rate of convergence of the -mean errors of both methods depends on the number of observations and the number of particles only through the ratio for additive functionals. In the case of the FFBS, this improves recent results providing bounds depending on .

1 Introduction

State-space models play a key role in statistics, engineering and econometrics; see [2, 11, 18]. Consider a process taking values in a general state-space . This hidden process can be observed only through the observation process taking values in . Statistical inference in general state-space models involves the computation of expectations of additive functionals of the form

conditionally to , where is a positive integer and are functions defined on . These smoothed additive functionals appear naturally for maximum likelihood parameter inference in hidden Markov models. The computation of the gradient of the log-likelihood function (Fisher score) or of the intermediate quantity of the Expectation Maximization algorithm involves the estimation of such smoothed functionals, see [2, Chapter and ] and [10].

Except for linear Gaussian state-spaces or for finite state-spaces, these smoothed additive functionals cannot be computed explicitly. In this paper, we consider Sequential Monte Carlo algorithms, henceforth referred to as particle methods, to approximate these quantities. These methods combine sequential importance sampling and sampling importance resampling steps to produce a set of random particles with associated importance weights to approximate the fixed-interval smoothing distributions.

The most straightforward implementation is based on the so-called path-space method. The complexity of this algorithm per time-step grows only linearly with the number of particles, see [4]. However, a well-known shortcoming of this algorithm is known in the literature as the path degeneracy; see [10] for a discussion.

Several solutions have been proposed to solve this degeneracy problem. In this paper, we consider the Forward Filtering Backward Smoothing algorithm (FFBS) and the Forward Filtering Backward Simulation algorithm (FFBSi) introduced in [9] and further developed in [12]. Both algorithms proceed in two passes. In the forward pass, a set of particles and weights is stored. In the Backward pass of the FFBS the weights are modified but the particles are kept fixed. The FFBSi draws independently different particle trajectories among all possible paths. Since they use a backward step, these algorithms are mainly adapted for batch estimation problems. However, as shown in [5], when applied to additive functionals, the FFBS algorithm can be implemented forward in time, but its complexity grows quadratically with the number of particles. As shown in [8], it is possible to implement the FFBSi with a complexity growing only linearly with the number of particles.

The control of the -norm of the deviation between the smoothed additive functional and its particle approximation has been studied recently in [5, 6]. In an unpublished paper by [6], it is shown that the FFBS estimator variance of any smoothed additive functional is upper bounded by terms depending on and only through the ratio . Furthermore, in [5], for any , a -mean error bound for smoothed functionals computed with the FFBS is established. When applied to strongly mixing kernels, this bound amounts to be of order either for

-

(i)

uniformly bounded in time general path-dependent functionals,

-

(ii)

unnormalized additive functionals (see [5, Eq. (3.8), pp. 957]).

In this paper, we establish -mean error and exponential deviation inequalities of both the FFBS and FFBSi smoothed functionals estimators. We show that, for any , the -mean error for both algorithms is upper bounded by terms depending on and only through the ratio under the strong mixing conditions for (i) and (ii). We also establish an exponential deviation inequality with the same functional dependence in and .

This paper is organized as follows. Section 2 introduces further definitions and notations and the FFBS and FFBSi algorithms. In Section 3, upper bounds for the -mean error and exponential deviation inequalities of these two algorithms are presented. In Section 4, some Monte Carlo experiments are presented to support our theoretical claims. The proofs are presented in Sections 5 and 6.

2 Framework

Let and be two general state-spaces endowed with countably generated -fields and . Let be a Markov transition kernel defined on and a family of functions defined on . It is assumed that, for any , has a density with respect to a reference measure on . For any integers and , any measurable function on , and any probability distribution on , define

| (1) |

where is a short-hand notation for . The dependence on is implicit and is dropped from the notations.

Remark 1.

Note that this equation has a simple interpretation in the particular case of hidden Markov models. Indeed, let be a probability space and a Markov chain on with transition kernel and initial distribution (which we denote ). Let be a sequence of observations on conditionally independent given and such that the conditional distribution of given has a density given by with respect to a reference measure on and set . Then, the quantity defined by (1) is the conditional expectation of given :

In its original version, the FFBS algorithm proceeds in two passes. In the forward pass, each filtering distribution , for any , is approximated using weighted samples , where is the number of observations and the number of particles: all sampled particles and weights are stored. In the backward pass of the FFBS, these importance weights are then modified (see [9, 15, 16]) while the particle positions are kept fixed. The importance weights are updated recursively backward in time to obtain an approximation of the fixed-interval smoothing distributions . The particle approximation is constructed as follows.

Forward pass

Let be i.i.d. random variables distributed according to the instrumental density and set the importance weights . The weighted sample then targets the initial filter in the sense that

is a consistent estimator of for any bounded and measurable function on .

Let now be a weighted sample targeting . We aim at computing new particles and importance weights targeting the probability distribution

. Following [17], this may be done by simulating pairs of indices and particles from the instrumental distribution:

on the product space , where are the adjustment multiplier weights and is a Markovian proposal transition kernel. In the sequel, we assume that has, for any , a density with respect to the reference measure . For any we associate to the particle its importance weight defined by:

Backward smoothing

For any probability measure on , denote by the backward smoothing kernel given, for all bounded measurable function on and for all , by:

For all and for all bounded measurable function on , may be computed recursively, backward in time, according to

2.1 The forward filtering backward smoothing algorithm

Consider the weighted samples , drawn for any in the forward pass. An approximation of the fixed-interval smoothing distribution can be obtained using

| (2) |

and starting with . Now, by definition, for all and for all bounded measurable function on ,

and inserting this expression into (2) gives the following particle approximation of the fixed-interval smoothing distribution

| (3) |

where is a bounded measurable function on ,

| (4) |

and

| (5) |

The estimator of the fixed-interval smoothing distribution might seem impractical since the cardinality of its support is . Nevertheless, for additive functionals of the form

| (6) |

where is a non negative integer and is a family of bounded measurable functions on , the complexity of the FFBS algorithm is reduced to . Furthermore, the smoothing of such functions can be computed forward in time as shown in [5]. This forward algorithm is exactly the one presented in [10] as an alternative to the use of the path-space method. Therefore, the results outlined in Section 3 hold for this method and confirm the conjecture mentioned in [10].

2.2 The forward filtering backward simulation algorithm

We now consider an algorithm whose complexity grows only linearly with the number of particles for any functional on . For any , we define

The transition probabilities defined in (4) induce an inhomogeneous Markov chain evolving backward in time as follows. At time , the random index is drawn from the set with probability proportional to . For any , the index is sampled in the set according to . The joint distribution of is therefore given, for , by

| (7) |

Thus, the FFBS estimator (3) of the fixed-interval smoothing distribution may be written as the conditional expectation

where is a bounded measurable function on . We may therefore construct an unbiased estimator of the FFBS estimator given by

| (8) |

where are paths drawn independently given according to (7) and where is a bounded measurable function on . This practical estimator was introduced in [12] (Algorithm 1, p. 158). An implementation of this estimator whose complexity grows linearly in is introduced in [8].

3 Non-asymptotic deviation inequalities

In this Section, the -mean error bounds and exponential deviation inequalities of the FFBS and FFBSi algorithms are established for additive functionals of the form (6). Our results are established under the following assumptions.

-

A1

-

(i)

There exists such that and for any , and we set .

-

(ii)

There exists such that and for any .

-

(i)

-

A2

-

(i)

For all and all , .

-

(ii)

.

-

(i)

-

A3

, and where

Assumptions AA1 and AA2 give bounds for the model and assumption AA3 for quantities related to the algorithm. AA1(i), referred to as the strong mixing condition, is crucial to derive time-uniform exponential deviation inequalities and a time-uniform bound of the variance of the marginal smoothing distribution (see [7] and [8]). For all function from a space to , is defined by:

Theorem 1.

Remark 2.

Remark 3.

The dependence on is hardly surprising. Under the stated strong mixing condition, it is known that the -norm of the marginal smoothing estimator , is uniformly bounded in time by (where depends only on , , , , and ). The dependence in instead of reflects the forgetting property of the filter and the backward smoother. As for , the estimators and become asymptotically independent as gets large, the -norm of the sum scales as the sum of a mixing sequence (see [3]).

Remark 4.

It is easy to see that the scaling in cannot in general be improved. Assume that the kernel satisfies for all . In this case, for any , the filtering distribution is

and the backward kernel is the identity kernel. Hence, the fixed-interval smoothing distribution coincides with the filtering distribution. If we assume that we apply the bootstrap filter for which and , the estimators are independent random variables corresponding to importance sampling estimators. It is easily seen that

Remark 5.

The independent case also clearly illustrates why the path-space methods are sub-optimal (see also [1] for a discussion). When applied to the independent case (for all , and ), the asymptotic variance of the path-space estimators is given in [4] by

The asymptotic variance thus increases as and hence, under the stated assumptions, the variance of the path-space methods is of order . It is believed (and proved in some specific scenarios) that the same scaling holds for path-space methods for non-degenerated Markov kernel (the result has been formally established for strongly mixing kernel under the assumption that is sufficiently close to ).

We provide below a brief outline of the main steps of the proofs (a detailed proof is given in Section 5). Following [8], the proofs rely on a decomposition of the smoothing error. For all and all bounded and measurable function on define the kernel by

The fixed-interval smoothing distribution may then be expressed, for all bounded and measurable function on , by

and this suggests to decompose the smoothing error as follows

| (9) | ||||

where we used the convention

Furthermore, for all ,

where and are two kernels on defined for all by

| (10) | ||||

| (11) |

For all we can write

and then,

| (12) |

with is a kernel on defined, for all and all bounded and measurable function on , by

where, by the same convention as above,

Two families of random variables and are now introduced to transform (12) into a suitable decomposition to compute an upper bound for the -mean error. As shown in Lemma 1, the random variables are centered given . The idea is to replace in (12) by its conditional expectation given to get a martingale difference. This conditional expectation is computed using the following intermediate result. For any measurable function on and any ,

| (13) |

Indeed,

This result, applied with the function , yields

For any , define for all bounded and measurable function on ,

| (14) | ||||

| (15) |

Using these notations, (12) can be rewritten as follows:

| (16) |

For any , the derivation of the upper bound relies on the triangle inequality:

where is defined in (6). The proof for the FFBS estimator is completed by using Proposition 1 and Proposition 2. According to (16), the smoothing error can be decomposed into a sum of two terms which are considered separately. The first one is a martingale whose -mean error is upper-bounded by as shown in Proposition 1. The second one is a sum of products, -norm of which being bounded by in Proposition 2.

The end of this section is devoted to the exponential deviation inequality for the error defined by (9). We use the decomposition of obtained in (16) leading to a similar dependence on the ratio . The martingale term is dealt with using the Azuma-Hoeffding inequality while the term needs a specific Hoeffding-type inequality for ratio of random variables.

4 Monte-Carlo Experiments

In this section, the performance of the FFBSi algorithm is evaluated through simulations and compared to the path-space method.

4.1 Linear gaussian model

Let us consider the following model:

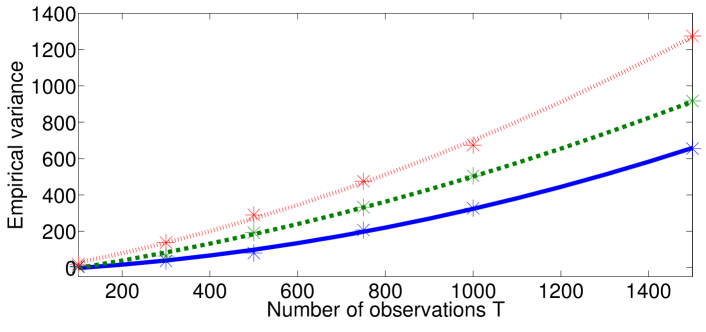

where is a zero-mean random variable with variance , and are two sequences of independent and identically distributed standard gaussian random variables (independent from ). The parameters are assumed to be known. Observations were generated using , and . Table 1 provides the empirical variance of the estimation of the unnormalized smoothed additive functional given by the path-space and the FFBSi methods over independent Monte Carlo experiments.

| Path-space | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| 300 | 500 | 750 | 1000 | 1500 | 5000 | 10000 | 15000 | 20000 | |

| 300 | 137.8 | 119.4 | 63.7 | 46.1 | 36.2 | 12.8 | 7.1 | 3.8 | 3.0 |

| 500 | 290.0 | 215.3 | 192.5 | 161.9 | 80.3 | 30.1 | 14.9 | 11.3 | 7.4 |

| 750 | 474.9 | 394.5 | 332.9 | 250.5 | 206.8 | 71.0 | 35.6 | 24.4 | 21.7 |

| 1000 | 673.7 | 593.2 | 505.1 | 483.2 | 326.4 | 116.4 | 70.8 | 37.9 | 34.6 |

| 1500 | 1274.6 | 1279.7 | 916.7 | 804.7 | 655.1 | 233.9 | 163.1 | 89.7 | 80.0 |

| FFBSi | |||||

|---|---|---|---|---|---|

| 300 | 500 | 750 | 1000 | 1500 | |

| 300 | 5.1 | 3.1 | 2.3 | 1.4 | 1.0 |

| 500 | 9.7 | 5.1 | 3.7 | 2.6 | 2.2 |

| 750 | 11.2 | 7.1 | 4.9 | 3.7 | 2.6 |

| 1000 | 16.5 | 10.5 | 6.7 | 5.1 | 3.4 |

| 1500 | 25.6 | 14.1 | 7.8 | 6.8 | 5.1 |

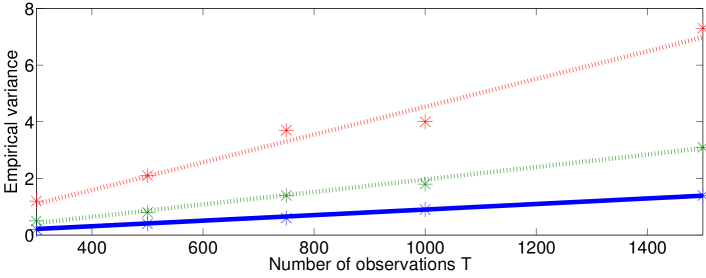

We display in Figure 1 the empirical variance for different values of as a function of for both estimators. These estimates are represented by dots and a linear regression (resp. quadratic regression) is also provided for the FFBSi algorithm (resp. for the path-space method).

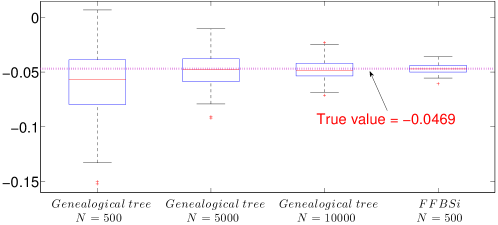

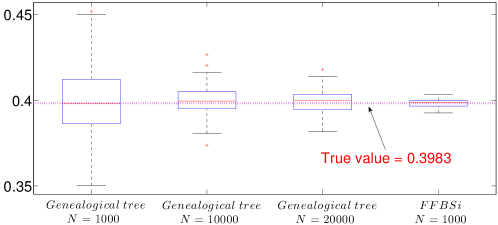

In Figure 2 the FFBSi algorithm is compared to the path-space method to compute the smoothed value of the empirical mean . For the purpose of comparison, this quantity is computed using the Kalman smoother. We display in Figure 2 the box and whisker plots of the estimations obtained with independent Monte Carlo experiments. The FFBSi algorithm clearly outperforms the other method for comparable computational costs. In Table 2, the mean CPU times over the runs of the two methods are given as a function of the number of particles (for and ).

| FFBSi | Path-space method | ||||

|---|---|---|---|---|---|

| 500 | 500 | 5000 | 10000 | ||

| CPU time (s) | 4.87 | 0.24 | 2.47 | 4.65 | |

| FFBSi | Path-space method | ||||

|---|---|---|---|---|---|

| 1000 | 1000 | 10000 | 20000 | ||

| CPU time (s) | 16.5 | 0.9 | 8.5 | 17.2 | |

4.2 Stochastic Volatility Model

Stochastic volatility models (SVM) have been introduced to provide better ways of modeling financial time series data than ARCH/GARCH models ([14]). We consider the elementary SVM model introduced by [14]:

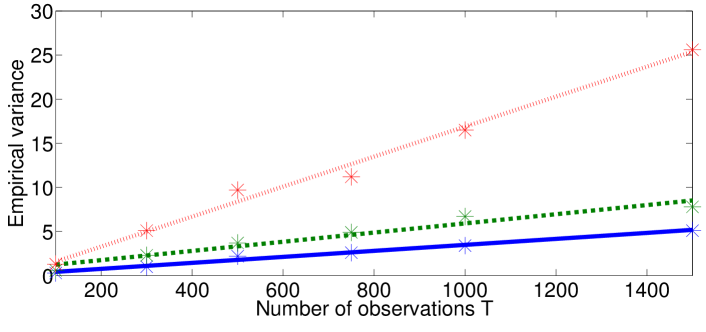

where is a zero-mean random variable with variance , and are two sequences of independent and identically distributed standard gaussian random variables (independent from ). This model was used to generate simulated data with parameters assumed to be known in the following experiments. The empirical variance of the estimation of given by the path-space and the FFBSi methods over independent Monte Carlo experiments is displayed in Table 3.

| Path-space method | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| 300 | 500 | 750 | 1000 | 1500 | 5000 | 10000 | 15000 | 20000 | |

| 300 | 52.7 | 33.7 | 22.0 | 17.8 | 12.3 | 3.8 | 2.0 | 1.4 | 1.2 |

| 500 | 116.3 | 84.8 | 64.8 | 53.5 | 30.7 | 11.4 | 6.8 | 4.1 | 2.8 |

| 750 | 184.7 | 187.6 | 134.2 | 120.0 | 65.8 | 29.1 | 12.8 | 7.3 | 7.7 |

| 1000 | 307.7 | 240.4 | 244.7 | 182.8 | 133.2 | 43.6 | 24.5 | 15.6 | 11.6 |

| 1500 | 512.1 | 487.5 | 445.5 | 359.9 | 249.5 | 90.9 | 52.0 | 32.6 | 29.3 |

| FFBSi | |||||

|---|---|---|---|---|---|

| 300 | 500 | 750 | 1000 | 1500 | |

| 300 | 1.2 | 0.6 | 0.5 | 0.4 | 0.2 |

| 500 | 2.1 | 1.2 | 0.8 | 0.6 | 0.4 |

| 750 | 3.7 | 1.8 | 1.4 | 0.9 | 0.6 |

| 1000 | 4.0 | 2.7 | 1.8 | 1.3 | 0.9 |

| 1500 | 7.3 | 3.8 | 3.1 | 1.6 | 1.4 |

We display in Figure 3 the empirical variance for different values of as a function of for both estimators.

5 Proof of Theorem 1

We preface the proof of Proposition 1 by the following Lemma:

Lemma 1.

Proof.

Proposition 1.

Proof.

Since is a is a forward martingale difference and , Burkholder’s inequality (see [13, Theorem 2.10, page 23]) states the existence of a constant depending only on such that:

Moreover, by application of the last statement of Lemma 1(iii),

and thus,

where . By the Minkowski inequality,

| (20) |

Since for any the random variables are conditionally independent and centered conditionally to , using again the Burkholder and the Jensen inequalities we obtain

| (21) |

where the last inequality comes from (18). Finally, by (20) and (5) we get

By the Holder inequality, we have

which yields

We obtain similarly

which concludes the proof. ∎

Proposition 2.

Proof.

The proof of Theorem 1 is now concluded for the FFBS estimator and we can proceed to the proof for the FFBSi estimator. We preface the proof of Theorem 1 for the FFBSi estimator by the following Lemma. We first define the backward filtration by

Lemma 2.

Proof.

According to Section 2.2, for all , is an inhomogeneous Markov chain evolving backward in time with backward kernel . For any , we have

The RHS of this equation is the difference between two expectations started with two different initial distributions. Under AA1(i), the backward kernel satisfies the uniform Doeblin condition,

and the proof is completed by the exponential forgetting of the backward kernel (see [2, 7]). The proof of (ii) follows exactly the same lines. ∎

To compute an upper-bound for the -mean error of the FFBSi algorithm, we may define the difference between the FFBS and the FFBSi estimators:

| (25) |

Proof of Theorem 1 for the FFBSi estimator.

The difference between the FFBS and the FFBSi estimators, , defined in (25), can be written

where

For all and all , the random variable is -measurable and so that can be seen as the increment of a backward martingale. Hence, since , using the Burkholder inequality (see [13, Theorem 2.10, page 23]), there exists a constant (depending only on , , , , and ) such that:

| (26) |

Then, since the random variables are conditionally independent and centered conditionally to , using the Burkholder inequality once again implies:

| (27) |

Furthermore, according to Lemma 2(i),

| (28) |

Putting (26), (27) and (28) together leads to

Using the Holder inequality as in the proof of Proposition 1 yields

and the proof of Theorem 1 for the FFBSi estimator is derived from the triangle inequality:

6 Proof of Theorem 2

We preface the proof of the Theorem by showing that the martingale term of the error (which is defined by (9)) satisfies an exponential deviation inequality in the following Proposition.

Proposition 3.

Proof.

According to the definition of given in (14), we can write

where for all and , is defined by

and is bounded by (see (18))

Furthermore, we define the filtration , for all and , by:

with the convention . Then, according to Lemma 1, is martingale increment for the filtration and the Azuma-Hoeffding inequality completes the proof. ∎

Proposition 4.

Proof.

In order to apply Lemma 4 in the appendix, we first need to find an exponential deviation inequality for which is done by using the decomposition given in (23). First, the ratio is dealt with through Lemma 3 in the appendix by defining

Assumption AA1(ii) and AA3 shows that and (18) shows that . Therefore, Condition (I) of Lemma 3 is satisfied. The bounds and the Hoeffding inequality lead to

establishing Condition (ii) in Lemma 3. Finally, Lemma 1(i) and the Hoeffding inequality imply that

Lemma 3 therefore yields

Then is dealt with by using again the Hoeffding inequality and the bounds , where :

Finally, has been shown in (24) to be bounded by a constant depending only on , , , and : so that

where

Therefore,

The proof of (30) is finally completed by applying Lemma 4 with

∎

Proof of Theorem 2 for the FFBS estimator.

Proof of Theorem 2 for the FFBSi estimator.

We recall the decomposition used in the proof of Theorem 1 for the FFBSi estimator:

where is defined by (25). Since are measurable and centered conditionally to using the same steps as in the proof of Proposition 3, we get

where is defined by (17). The proof is finally completed by writing

and by using Theorem 2 for the FFBS estimator. ∎

Appendix A Technical results

Lemma 3.

Assume that , , and are random variables defined on the same probability space such that there exist positive constants , , , and satisfying

-

(i)

, -a.s. and , -a.s.,

-

(ii)

For all and all , ,

-

(iii)

For all and all , .

Then,

Proof.

See [8, Lemma 4]. ∎

Lemma 4.

For , let be random variables. Assume that there exists a constants and for all , there exists a constant such that and all

Then, for all and all , we have

where

Proof.

By the Bienayme-Tchebychev inequality, we have

| (31) |

It remains to bound the expectation in the RHS of (31) by . First, by the Minkowski inequality,

Moreover, for , can be bounded by

Finally,

∎

References

- [1] M. Briers, A. Doucet, and S. Maskell. Smoothing algorithms for state-space models. Annals Institute Statistical Mathematics, 62(1):61–89, 2010.

- [2] O. Cappé, E. Moulines, and T. Rydén. Inference in Hidden Markov Models. Springer, 2005.

- [3] J. Davidson. Stochastic limit theory. Oxford university press, 1997.

- [4] P. Del Moral. Feynman-Kac Formulae. Genealogical and Interacting Particle Systems with Applications. Springer, 2004.

- [5] P. Del Moral, A. Doucet, and S. Singh. A Backward Particle Interpretation of Feynman-Kac Formulae. ESAIM M2AN, 44(5):947–975, 2010.

- [6] P. Del Moral, A. Doucet, and S.S. Singh. Forward smoothing using sequential monte carlo. Technical report, arXiv:1012.5390v1, 2010.

- [7] P. Del Moral and A. Guionnet. On the stability of interacting processes with applications to filtering and genetic algorithms. Annales de l’Institut Henri Poincaré, 37:155–194, 2001.

- [8] R. Douc, A. Garivier, E. Moulines, and J. Olsson. Sequential Monte Carlo smoothing for general state space hidden Markov models. Ann. Appl. Probab., 21(6):2109–2145, 2011.

- [9] A. Doucet, S. Godsill, and C. Andrieu. On sequential Monte-Carlo sampling methods for Bayesian filtering. Stat. Comput., 10:197–208, 2000.

- [10] A. Doucet, G. Poyiadjis, and S.S. Singh. Particle approximations of the score and observed information matrix in state-space models with application to parameter estimation. Biometrika, 98(1):65–80, 2011.

- [11] J. Durbin and S. J. Koopman. Time series analysis of non-Gaussian observations based on state space models from both classical and Bayesian perspectives. J. Roy. Statist. Soc. B, 62:3–29, 2000.

- [12] S. J. Godsill, A. Doucet, and M. West. Monte Carlo smoothing for non-linear time series. J. Am. Statist. Assoc., 50:438–449, 2004.

- [13] P. Hall and C. C. Heyde. Martingale Limit Theory and its Application. Academic Press, New York, London, 1980.

- [14] J. Hull and A. White. The pricing of options on assets with stochastic volatilities. J. Finance, 42:281–300, 1987.

- [15] M. Hürzeler and H. R. Künsch. Monte Carlo approximations for general state-space models. J. Comput. Graph. Statist., 7:175–193, 1998.

- [16] G. Kitagawa. Monte-Carlo filter and smoother for non-Gaussian nonlinear state space models. J. Comput. Graph. Statist., 1:1–25, 1996.

- [17] M. K. Pitt and N. Shephard. Filtering via simulation: Auxiliary particle filters. J. Am. Statist. Assoc., 94(446):590–599, 1999.

- [18] M. West and J. Harrison. Bayesian Forecasting and Dynamic Models. Springer, 1989.