American Step-Up and Step-Down Default Swaps under Lévy Models*

Abstract.

This paper studies the valuation of a class of default swaps with the embedded option to switch to a different premium and notional principal anytime prior to a credit event. These are early exercisable contracts that give the protection buyer or seller the right to step-up, step-down, or cancel the swap position. The pricing problem is formulated under a structural credit risk model based on Lévy processes. This leads to the analytic and numerical studies of several optimal stopping problems subject to early termination due to default. In a general spectrally negative Lévy model, we rigorously derive the optimal exercise strategy. This allows for instant computation of the credit spread under various specifications. Numerical examples are provided to examine the impacts of default risk and contractual features on the credit spread and exercise strategy.

.

Keywords: optimal stopping; credit default swaps; step-up and step-down options; Lévy processes; scale functions

JEL Classification: G13, G33, D81, C61

Mathematics Subject Classification (2010): 60G51 91B25 91B70

1. Introduction

Credit default swaps (CDSs) are among the most liquid and widely used instruments for managing and transferring credit risks. Despite the recent market turbulence, their market size still exceeds US$30 trillions111According to the ISDA Market Survey, the total CDS outstanding volume in 2009 is US$30,428 billions.. In a standard single-name CDS, the protection buyer pays a pre-specified periodic premium (the CDS spread) to the protection seller to cover the loss of the face value of an asset if the reference entity defaults before expiration. The contract stipulates that both the buyer and seller have to commit to their respective positions until the default time or expiration date. To modify the initial CDS exposure in the future, one common way is to acquire appropriate positions later from the market, but it is subject to credit spread fluctuations and market illiquidity, especially during adverse market conditions.

To provide additional flexibility to investors, credit default swaptions and other derivatives on CDSs have emerged. For instance, the payer (receiver) default swaption is a European option that gives the holder the right to buy (sell) protection at a pre-specified strike spread at expiry, given that default has not occurred. Otherwise, the swaption is knocked out. See, for example, [25]. By appropriately combining a default swaption with a vanilla CDS position, one can create a callable or putable default swap. A callable (putable) CDS allows the protection buyer (seller) to terminate the contract at some fixed future date. Hence, as described here, the callable/putable CDSs are in fact cancellable CDSs. Typically, the callable feature is paid for through incremental premium on top of the standard CDS spread, so selling a callable CDS can enhance the yield from the seller’s perspective.

In this paper, we consider a class of default swaps embedded with an option for the investor (protection buyer or seller) to adjust the premium and notional amount once for a pre-specified fee prior to default. Specifically, these non-standard contracts equip the standard default swaps with the early exercisable rights such as (i) the step-up option that allows the investor to increase the protection and premium at exercise, and (ii) the step-down option to reduce the protection and premium. By definition, these contracts are indeed generalized versions of the callable and putable CDSs mentioned above, and thus are more flexible credit risk management tools. Henceforth, we shall use the more general meaning of the terminology callable and putable default swaps, rather than limiting them to cancellable CDSs.

The main contribution of our paper is to determine the credit spread for these default swaps under a Lévy model, and analyze the optimal strategy for the buyer or seller to exercise the step-up/down option. Specifically, we model the default time as the first passage time of a Lévy process representing some underlying asset value. We decompose the default swap with step-up/down option into a combination of an American-style credit default swaption and a vanilla default swap. From the investor’s perspective, this gives rise to an optimal stopping problem subject to possible sudden early termination from default risk. Our formulation is based on a general Lévy process, and then we solve analytically for a general spectrally negative Lévy process. By employing the scale function and other properties of Lévy processes, we derive analytic characterization for the optimal exercising strategy. This in turn allows for a highly efficient computation of the credit spread for these contracts. We provide a series of numerical examples to illustrate the credit spread behavior and optimal exercising strategy under various contract specifications and scenarios.

We adopt a Lévy-based structural credit risk model that extends the original approach introduced by Black and Cox [10] where the asset value follows a geometric Brownian motion. Other structural default models based on Lévy and other jump processes can also be found in [12, 22, 44]. To our best knowledge, the valuation of American step-up and step-down default swaps has not been studied elsewhere. For Lévy-based pricing models for other credit derivatives, such as European credit default swaptions and collateralized debt obligations (CDOs), we highlight [3, 17, 27], among others.

Lévy processes have been widely applied in derivatives pricing. Some well-known examples of Lévy pricing models include the variance gamma (VG) model [36], the normal inverse Gaussian (NIG) model [7], the CGMY model [14] as well as a number of jump diffusion models (see [29, 37]). In this paper, instead of focusing on a particular type of Lévy process, we consider a general class of Lévy processes with only negative jumps. This is called the spectrally negative Lévy process and has been drawing much attention recently, as a generalization of the classical Cramér-Lundberg and other compound-Poisson type processes. A number of fluctuation identities can be expressed in terms of the scale function and are used in a number of applications. We refer the reader to [1, 5] for derivatives pricing, [32] for optimal capital structure, [8, 9] for stochastic games, [6, 31, 35] for optimal dividend problem, and [19] for optimal timing of capital reinforcement. For a comprehensive account, see [30].

A key part of our analysis focuses on a non-standard American option subject to default risk (see Proposition 2.1). We discuss both the perpetual and finite-maturity cases. The former is related to some existing work on perpetual early exercisable options under various Lévy models, for example [2, 5, 11, 34, 38]. The infinite horizon nature provides significant convenience for analysis and sometimes leads to explicit solutions. Working under a general spectrally negative Lévy model, we provide analytic results for the timing strategies and contract values. For numerical examples, we select the phase-type (and hyperexponential) fitting approach by Egami and Yamazaki [18] to illustrate the cases when the process is a mixture of Brownian motion and a compound Poisson process with Pareto-distributed jumps. We then apply our formulation and results to study the finite-maturity case. For finite-maturity American options under Lévy models, the pricing problem typically requires numerical solutions to the underlying partial integral differential equation (PIDE), or other simulation methods; see, among others, [4, 24, 26]. In our paper, we illustrate how to approximate the finite-maturity case using our analytical solutions to the perpetual case.

The rest of the paper is organized as follows. In Section 2, we formulate the default swap valuation problems under a general Lévy model. In Section 3, we focus on the spectrally negative Lévy model and provide a complete solution and detailed analysis. Section 4 provides the numerical results. In Section 5, we apply the results to the finite-maturity case. Section 6 concludes the paper and presents some extensions of our model. Most proofs are included in the Appendix.

2. Problem Overview

Let be a complete probability space, where is the risk-neutral measure used for pricing. We assume there exists a Lévy process , and denote by the filtration generated by . The value of the reference entity (a company stock or other assets) is assumed to evolve according to an exponential Lévy process , . Following the Black-Cox [10] structural approach, the default event is triggered by crossing a lower level , so the default time is given by the first passage time: . Without loss of generality, we can take by shifting the initial value . Henceforth, we shall work with the default time:

where we assume . Throughout this paper, we denote by the probability law and the expectation under which .

2.1. Credit Default Swaps and Swaptions

In preparation for default swaps with step-up/down options, let us start with the basic concepts of credit default swaps and swaptions. Under a -year CDS on a unit face value, the protection buyer pays a constant premium payment $ continuously over time until default time or maturity , whichever comes first. If default occurs before , the buyer will receive the default payment at time , where is the assumed constant recovery rate (typically 40%). From the buyer’s perspective, the expected discounted payoff is given by

| (2.1) |

where is the positive constant risk-free interest rate. The quantity can be viewed as the market price for the buyer to enter (or long) a CDS with an agreed premium , default payment and maturity . On the opposite side of the trade, the protection seller’s expected cash flow is .

In standard practice, the CDS spread is determined at inception such that , yielding zero expected cash flows for both parties. Direct calculations show that the credit spread can be expressed as

| (2.2) |

For most Lévy models, due to the lack of explicit formulas, the computation of the CDS spread is based on simulation or other approximation methods (see, for example, [12]). Alternatively, one can consider the perpetual case as an approximation and to obtain analytic or explicit bounds. This is a popular approach adopted for equity derivatives, especially American options, for which the finite-maturity contracts do not admit closed-form solutions while the perpetual versions often do (see [11, 34, 38] for some examples under Lévy models).

To illustrate, we set and express the buyer’s CDS price as

| (2.3) | ||||

where

| (2.4) |

The seller’s CDS price is . Solving yields the credit spread:

| (2.5) |

Therefore, the credit spread calculation reduces to computing the Laplace transform , which admits an explicit analytic formula under some well-known Lévy models (see (3.5) below for the spectrally negative case). It is clear from (2.5) that the CDS spread scales linearly in : .

Next, we introduce a perpetual American payer and receiver default swaptions, which give the holder the right to, respectively, buy and sell protection on a perpetual CDS with default payment at a pre-specified spread for the strike price upon exercise. If default occurs prior to exercise, then the swaption is knocked out and becomes worthless. The payer and receiver swaption holder is required to pay an upfront fee, which is given by respectively

| (2.6) | ||||

| (2.7) |

where

| (2.8) |

is the set of all -stopping times smaller than or equal to the default time. The two price functions are related by

| (2.9) |

In summary, is the payer default swaption price when , and it is the receiver default swaption price when .

Remark 2.1.

We remark that the perpetual American payer and receiver default swaptions introduced above are non-standard option contracts, but they bear similarity to the traditional European-style default swaptions. In Section 5, we will discuss the finite-maturity version of these contracts.

2.2. American Callable Step-Up and Step-Down Default Swaps

Next, we consider a default swap contract with an embedded option that permits the protection buyer to change the face value and premium once for a fee. We discuss the perpetual case here, and the finite-maturity case in Section 5. Beginning from initiation, the buyer pays a premium for a protection of a unit face value. At any time prior to default, the buyer can select a time to switch to a new contract with a new premium and face value for a fee . The default payment then changes from to after the exercise time . Here, , and are constant non-negative parameters pre-specified at time zero. The buyer’s maximal expected cash flow is given by

| (2.10) | |||

with defined in (2.8).

This formulation covers default swaps with the following provisions:

-

(1)

Step-up Option: if and , then the buyer is allowed to increase the coverage once from to by paying the fee and a higher premium thereafter.

-

(2)

Step-down Option: when and , then the buyer can reduce the coverage once from to by paying the fee and a reduced premium thereafter.

-

(3)

Cancellation Right: as a special case of the step-down option with , the resulting contract allows the buyer to terminate the default swap at time .

In addition, the perpetual vanilla CDS corresponds to the case with , and , and the CDS spread is given by (2.5). We ignore the contract specifications with since they would mean paying more (less) premium in exchange for a reduced (increased) protection after exercise. In summary, we study the valuation of the (perpetual) American callable step-up/down default swaps. For any fixed parameters , the value is referred to as the buyer’s price, so the seller’s price is . The credit spread is determined from the equation so that no cash transaction occurs at inception.

In preparation for our solution procedure, we first provide a useful representation of the buyer’s value . Define

| (2.11) |

Here, and hold for a step-down default swap and and for a step-up default swap.

Proposition 2.1.

Proof.

First, by a rearrangement of integrals, the expression inside the expectation in (2.10) becomes

since implies by the definition of . Because the last two terms do not depend on , we can rewrite the buyer’s value function as

| (2.13) |

Here, the last two terms in fact constitute . Next, using the fact for every and the strong Markov property of at time , we rewrite the first term as

| (2.14) |

with

| (2.15) |

Since and a.s. on , it follows from (2.14) that . Therefore, it is never optimal to exercise at any if . Consequently, we can replace with in (2.14). As a result, with , the function is indeed the price of a perpetual American payer (receiver) default swaption written on the buyer’s (seller’s) CDS price with strike . This implies that , and therefore (2.12) follows.∎

The decomposition (2.12) in Proposition 2.1 yields a static replication of the American callable step-up/down default swap. To this end, one may also verify the result by a no-arbitrage argument. We summarize the buyer’s and seller’s positions in the American callable step-up/down default swaps in Table 1. As we shall discuss in Section 5 below, this also holds for the finite-maturity case.

As an illustrative example, let us consider the step-up case where the premium and protection are doubled after exercise, i.e. and . For any candidate exercise time , the observable market prevailing vanilla CDS spread is given by in (2.5), and by definition. Hence, if at , then , and the buyer will not exercise. This is intuitive because the buyer is better off giving up the step-up option and doubling his protection by entering a separate CDS at the lower market spread at time .

2.3. The American Putable Step-Up and Step-Down Default Swaps

Applying the ideas from the previous subsection, we formulate the pricing problem for the perpetual American putable step-up/down default swaps. These default swaps allow the protection seller (and not the buyer) to change the protection premium and default payment for a fee anytime prior to default. Let and be the initial premium and default payment. The seller may select a time to switch to a new premium and default payment for a switching fee . The seller’s maximal expected cash flow is

| (2.16) | ||||

In particular, we will study the American putable default swap with a step-up option (i.e. and ) or step-down option (i.e. and ). Again, the credit spread is chosen so that the seller’s value function is zero, i.e. .

Following the procedure in the proof of Proposition 2.1 or by a no-arbitrage argument, we can simplify the seller’s value as follows:

Proposition 2.2.

| Default Swap Types | Protection Buyer’s Position: | Protection Seller’s Position: |

|---|---|---|

| a vanilla CDS and | a vanilla CDS and | |

| Callable Step-Up | an American payer default swaption | an American payer default swaption |

| Callable Step-Down | an American receiver default swaption | an American receiver default swaption |

| Putable Step-Up | an American receiver default swaption | an American receiver default swaption |

| Putable Step-Down | an American payer default swaption | an American payer default swaption |

We summarize the buyer’s and seller’s positions in the American putable step-up/down default swaps in Table 1. To gain intuition on the seller’s exercise decision, let us look at the step-down case where and . Recall that is decreasing in and for any stopping time . If the market prevailing CDS spread is at some , then the seller’s default swaption payoff is . The seller will not exercise at since the protection of can be purchased from a separate CDS at the lower prevailing spread .

2.4. Symmetry Between Callable and Putable Default Swaps

By Propositions 2.1 and 2.2, along with (2.9), we observe the following “put-call parity” and symmetry identities:

The first equality means a long position in an American callable step-up (step-down) default swap and a short position in an American putable step-down (step-up) default swap result in a double long position in a vanilla CDS. From the second equality, a long position in both an American callable step-up (step-down) default swap and an American putable step-down (step-up) default swap yields a double long position in an American payer (receiver) default swaption. As we see in Section 5, this also holds for the finite-maturity case.

Furthermore, according to (2.12) and (2.17), the optimal exercise times for and are determined from and which depend on the triplet but not directly on and . Consequently, by (2.9), the same optimal exercising strategy applies for both

-

(1)

the protection buyer of an American callable default swap with a step-up (step-down) option with , and

-

(2)

the protection seller of an American putable default swap with a step-down (step-up) option with .

This observation means that it suffices to solve for two cases instead of four. Specifically, we shall solve for (i) the buyer’s callable step-down case in (2.12) and (ii) the seller’s putable step-down case in (2.17), both with and . In view of (2.14) and the proof of Proposition 2.1, this amounts to solving the following optimal stopping problems:

| (2.18) | ||||

| (2.19) |

where and

| (2.20) | ||||

| (2.21) |

for . Here, and are computed using formula (2.3).

By inspecting (2.18), it follows from (2.20) that if . Financially, this means that the fee to be paid exceeds the maximum benefit of stepping down, i.e. perpetual annuity with premium . It is clear that choosing is optimal and the protection buyer will never exercise the step-down option. Hence, we only need to study the non-trivial case with the condition

| (2.22) |

For (2.19), we have if because is decreasing in on . Again, this means that is automatically optimal for the protection seller. Therefore, we shall focus on the case with which also implies

| (2.23) |

The intuition behind this is that the fee should not exceed the reduction in liability.

.

2.5. Solution Methods via Continuous and Smooth Fit

We conclude this section by describing our solution procedure for the optimal stopping problems under a general Lévy model. In the next section, we shall focus on the spectrally negative Lévy model and derive an analytical solution.

For our first problem (2.18), the protection buyer has an incentive to step-down when default is less likely, or equivalently when is sufficiently high. Following this intuition, we denote the threshold strategy

| (2.24) |

Clearly, . The corresponding expected payoff is given by

| (2.25) |

Note that for . Sometimes it is more intuitive to consider the difference

One common solution approach for many optimal stopping problems is continuous and smooth fit (see [39, 41, 42, 43]). Applying to our problem, it involves two main steps:

-

(a)

obtain that satisfies the continuous or smooth fit condition: or , and

-

(b)

verify the optimality of by showing (i) for and (ii) the process , , is a supermartingale.

To this end, an analytical expression for or would be useful.

Lemma 2.1.

Fix . The function is given by

| (2.26) |

where and .

As we shall see in Section 3, the functions and can be computed via the scale functions for a spectrally negative Lévy model; see (3.4) below.

In our second problem (2.19), the protection seller tends to exercise the step-down option when default is likely, or equivalently when is sufficiently small. Suppose the seller exercises at the first time reaches or goes below some fixed threshold ; namely,

Then, the corresponding expected payoff is given by

Again, we denote the difference between continuation and exercise by for .

For this problem, the continuous and smooth fit solution approach is to

-

(a)

obtain that satisfies the continuous or smooth fit condition: or , and

-

(b)

verify the optimality of by showing (i) for and (ii) the process , , is a supermartingale.

This method requires some expression for , which is summarized as follows:

Lemma 2.2.

Fix . The function is given by

| (2.27) |

where

| (2.28) |

3. Solution Methods under the Spectrally Negative Lévy Model

We proceed to solve the optimal stopping problems and in (2.18) and (2.19) for spectrally negative Lévy processes. Our main results are Theorems 3.1 and 3.2 which provide the optimal solutions for and , respectively. In turn, the American callable/putable step-up/down default swap can be immediately priced in view of Propositions 2.1 and 2.2.

3.1. The Spectrally Negative Lévy Process and Scale Function

Let be a spectrally negative Lévy process with the Laplace exponent

| (3.1) |

where , is called the Gaussian coefficient, and is a measure on such that and

See, e.g. Theorem 1.6 of [30]. The risk neutral condition requires that so that the discounted value of the reference entity is a -martingale. By Lemma 2.12 of [30], if further we have

| (3.2) |

then the Laplace exponent can be expressed as

where . Recall that the process has paths of bounded variation if and only if and (3.2) holds. A special example is a compound Poisson process with , where is the finite rate of jumps. We ignore the negative subordinator case ( decreasing a.s.). This means that we require to be strictly positive when is of bounded variation.

By Theorem 8.1 of [30], for any spectrally negative Lévy process, there exists an (r-)scale function , such that on , and is characterized on by the Laplace transform:

| (3.3) |

where .

The properties of the scale function [30, Theorem 8.1] allow us to derive the analytic formulas for and from Lemma 2.1. Precisely, for ,

| (3.4) | ||||

where , . Notice that for . The Laplace transform of in (2.4) is given by

| (3.5) |

Henceforth, we assume that does not have atoms, which guarantees that is on (see [15]). Moreover, as in (8.18) of [30],

| (3.6) |

From Lemmas 4.3 and 4.4 of [32], we also summarize the behavior in the neighborhood of zero.

Lemma 3.1.

For every , we have

3.2. Callable Step-Down Default Swap

We proceed to solve for in (2.18) for the callable step-down default swap. First, we consider the expected payoff function in (2.25) with some threshold :

| (3.10) |

for . If , then , . If , then , . Applying (3.4) and (3.5) and Lemma 2.1 to the stopping value and difference function , we can express them in terms of the scale function, namely,

| (3.11) | ||||

| (3.12) |

where

| (3.13) |

Remark 3.1.

From (3.12), we observe that . This implies that continuous fit must hold for all .

To obtain the candidate optimal threshold, we consider the smooth fit condition . To this end, we compute from (3.12) the derivatives

| (3.14) | ||||

| (3.15) |

Here is continuous on and (3.15) holds at which the second derivative of exists (which holds for Lebesgue-a.e. ).

Observing from (3.13) that for and by (3.6), we deduce that is increasing in . Therefore, there exists at most one satisfying the smooth fit condition, which by (3.14) is equivalent to

| (3.16) |

If it exists, then this is our candidate optimal threshold, and is the candidate value function for (2.18).

The smooth fit condition fails if (a) , or (b) . Under each of these scenarios, we need another way to deduce the candidate optimal threshold. To this end, let us consider the derivative of with respect to . For ,

| (3.17) |

Under scenario (a), in (3.17) implies that is decreasing in for any , so we choose as our candidate optimal threshold. In this case, the buyer will stop immediately (), and the corresponding expected payoff is (see (2.25)). As we show next, is possible only when is of bounded variation.

Lemma 3.2.

We have if and only if and .

As for scenario (b), it follows from (3.17) that is increasing in for any . Therefore, we set , meaning that the buyer will never exercise (), and the corresponding expected payoff is (see (2.25)). In fact, this corresponds to the case where the payoff . To see this, we deduce from (3.17) and continuous fit in Remark 3.1 that, for any arbitrarily fixed , . Then, applying Fatou’s lemma and because a.s., we obtain , and thus . Therefore, under condition (2.22), we have already ruled out scenario (b).

To summarize, we propose the candidate value function corresponding to the candidate optimal threshold from (3.16) for , or otherwise. By direct computation using (3.10)-(3.12), the value function is

| (3.20) |

Here, on , because .

The next step is to verify the optimality of . We shall show that (i) dominates and (ii) the stochastic process

| (3.21) |

is a supermartingale.

We address the first part as follows. When , it follows from (2.25) or the arguments above that . When , is monotonically increasing and attains at . Therefore, is increasing in for by (3.17). Then, by continuous fit in Remark 3.1, for any arbitrarily fixed , taking , we have . Moreover, on by definition. Hence, we conclude that:

| (3.22) |

We now pursue the supermartingale property of the process in (3.21). Define the generator of by

for the unbounded variation case and

for the bounded variation case. The supermartingale property of is due to the following lemma (see the Appendix for a proof):

Lemma 3.3.

The function satisfies

Theorem 3.1.

3.3. Putable Step-Down Default Swap

We now turn our attention to the putable step-down default swap, which amounts to solving in (2.19) with and . Under the spectrally negative Lévy model, the function in (2.28) can be expressed explicitly by scale functions as shown in Lemma 3.4 below. This together with (3.5) expresses explicitly in (2.27), which is needed to apply continuous and smooth fit principle.

Define

| (3.23) |

It is clear that decreases monotonically in . Next, we express using and the scale function. For its proof, we refer to Lemma 4.3 of [19].

Lemma 3.4.

Fix , we have

and for .

We proceed to consider the continuous fit condition. First, it follows from (2.27) that, for every ,

| (3.24) | ||||

If is of unbounded variation, then by Lemma 3.1, and therefore continuous fit holds for every . Nevertheless, for the bounded variation case, we can apply the continuous fit condition: , which is equivalent to

| (3.25) |

For the unbounded variation case, we apply the smooth fit condition. By differentiation, we have

where (in particular, if and by Lemma 3.1). Therefore,

Consequently, the smooth fit condition, , is also equivalent to (3.25).

In summary, we look for the solution to (3.25), denoted by , which will be our candidate optimal threshold. Since is monotonically decreasing, there exists at most one that satisfies (3.25). If it does not exist, we set the threshold .

When has paths of bounded variation, we must have under assumption (2.23). Indeed, if , then it follows from (3.24) that for every . This implies that there exists such that . However, since attains the global maximum (because by (2.23)), this is a contradiction. Hence is impossible when is of bounded variation.

In the case with , we take to be our candidate optimal threshold, and the corresponding stopping time is . The candidate value function is given by

For , we can apply (3.25) to express it as

| (3.26) |

When , we consider the candidate value function defined by (see (2.21) and (2.27))

| (3.27) | ||||

for all and for every . Here is well-defined according to Lemma 3.4 since if ; see (3.25).

This implies a strategy by which the seller will delay until is arbitrarily close to zero, and exercise at a sufficiently small level . This can be realized by monitoring as it creeps downward through zero (see Section 5.3 of [30]). The seller may lose the opportunity to exercise prior to default if suddenly jumps across (below) zero. In fact, and this is strictly positive if and only if (see Exercise 7.6 of [30]). The optimality result below implies that can happen only when has a diffusion component by our assumption .

For optimality verification, we shall show (i) and (ii) , , is a supermartingale. We shall first show (i) via:

Lemma 3.5.

For every , we have

| (3.28) |

Suppose . For the unbounded variation case, we apply Lemma 3.5 for any fixed , along with the continuous fit, to obtain the inequality: , . When is of bounded variation, we observe from (3.24) that for , which implies that

| (3.29) |

This domination also holds for in the same way by its definition as a limit in (3.27) and because (3.28) holds for every . Finally for , the equality holds by definition. As a result, we conclude that

| (3.30) |

For the supermartingale property, we shall use the following result (see Appendix for a proof):

Lemma 3.6.

We have for every .

4. Numerical Examples

In this section, we numerically illustrate the investor’s optimal exercise strategy and the credit spread behaviors, where the underlying spectrally negative Lévy process is assumed to have hyperexponential jumps of the form

| (4.1) |

Here is a standard Brownian motion, is a Poisson process with arrival rate , and are i.i.d. hyperexponential random variables with density function

for some .

As discussed in [18], the scale function of the Lévy process of the form (4.1) admits analytic form and can approximate that of any spectrally negative Lévy process with a completely monotone Lévy measure. For our numerical examples, we consider the process in the form (4.1) with replaced by Pareto random variables with distribution function for . We use the approximation to its scale function computed in [18] where they adopted the hyperexponential fitting algorithm given by [21]. We refer to [18, 21] for the detailed fitting procedure and fitted parameters.

For both callable and putable default swaps, we consider the following cases:

-

•

Step-Down default swap with ,

-

•

Step-Up default swap with .

Hence, there are in total 4 cases. The model parameters are , , , and bps, unless specified otherwise. We shall adjust the values of and so that the risk-neutral condition holds.

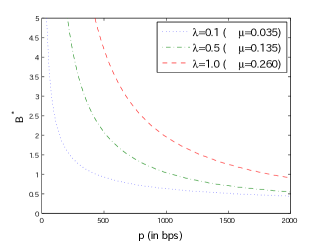

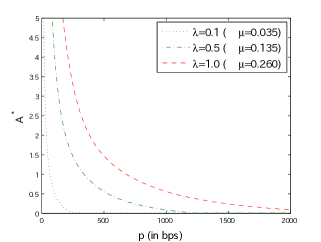

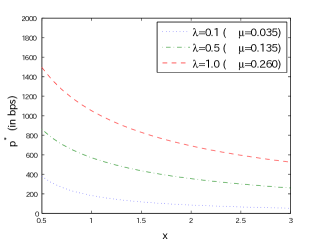

By symmetry (see Section 2.4), the optimal stopping problems for callable step-down and putable step-up default swaps are equivalent, while callable step-up and putable step-down default swaps are equivalent. Figure 3 shows the optimal thresholds for callable step-down/putable step-up default swaps and for callable step-up/putable step-down default swaps. Both and are decreasing in the premium , as is intuitive. Also, and rise as default risk increases.

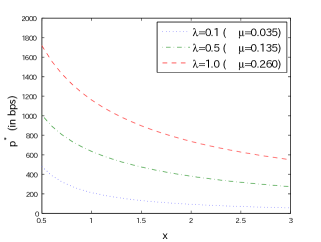

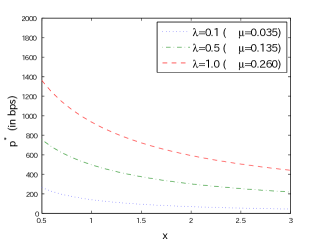

Figure 4 shows the credit spread as a function of the distance-to-default for the callable and putable step-down default swaps, with the vanilla CDS as benchmark (see (2.5)). We first compute the contract values, which are monotone in , and then determine by a bisection method. As increases, meaning lower default risk, the credit spread reduces. The callable step-down default swap spreads are naturally higher than the vanilla case due to the embedded step-down option. In contrast, the putable step-down spreads are lower than the vanilla case because the buyer is subject to the step-down exercise by the seller.

5. The Finite-maturity case

We now consider the finite-maturity case, and study how the solutions can be approximated using the results obtained in the previous sections. We first formulate the finite-maturity American callable/putable step-up/down default swaps by modifying the results in Sections 2.2 and 2.3. We then show that their value functions, optimal strategies, and credit spreads can be efficiently approximated by our analytical results on the perpetual case.

5.1. Finite-Maturity Formulation

Let be a given finite maturity and define

| (5.1) |

be the set of all stopping times smaller than or equal to . The buyer’s and seller’s maximal expected cash flows, respectively, are given by,

Here, the contract is terminated at default or maturity , whichever comes first. For the callable case, the buyer can exercise anytime (strictly) before the contract termination. Since for any , we may interpret as the event that the option expires without being exercised. When default happens before maturity (on ), the default payment is if the buyer has exercised () and is otherwise (). The interpretation for the putable case is similar.

5.2. Symmetry and Decomposition

As we shall describe below, the symmetry and decomposition we attained in Section 2 for the perpetual case can be extended to the finite-maturity case.

To see this, we can decompose the buyer’s maximal expected cash flow as

| (5.2) | ||||

where and are the same as in (2.11) and is the value of a standard finite-maturity CDS defined as in (2.1). By for every ,

with

The case for the seller is similar. Consequently, Propositions 2.1 and 2.2 can be extended to the finite-maturity case.

Proposition 5.1.

For all , we have the decomposition

| (5.3) | ||||

where

Clearly,

| (5.4) |

and Table 1 holds for the finite-maturity case as well. Moreover, “put-call parity” and symmetry identities also hold simply by replacing with . To summarize,

While these identifications are analogous to the perpetual case, the computation of the value function for the finite-maturity case (5.3) is significantly more difficult. Whereas can be computed using standard techniques such as Laplace inversion and simulation, the computation of and must involve a free-boundary problem of PIDE. Moreover, in light of the non-standard nature of our problem such as the discontinuity of the payoff function and early termination due to default, it is not clear if any standard numerical method can achieve reasonable accuracy. It is also noted that one needs to focus on a certain type of Lévy process (and its infinitesimal generator), and the results are significantly limited compared to our results on the perpetual case, which are applicable to a general spectrally negative Lévy process. For this reason, we take an analytical approach by utilizing greatly our analytical solutions for the perpetual case.

5.3. Analytical Bounds and Asymptotic Optimality

In view of the computational challenges involving and , here we discuss how these can be approximated using the analytical value functions from the perpetual case, namely, and (see (3.20), (3.26) and (3.27)).

As in the perpetual case, in order to compute the value function for all four cases (callable/putable and step-up/down), it suffices to obtain and for thanks to (5.4). As in (5.2), we have the identities:

| (5.5) | ||||

| (5.6) |

We shall first show that the function

can approximate , for , with some suitable analytical bounds.

Lemma 5.1.

For and , we have

for .

Proof.

Using (5.5) and that a.s. for any by (5.1), we write

Observing that, for any ,

| (5.7) |

and , we obtain the inequality

| (5.8) | ||||

Recall from (2.13) that

| (5.9) |

and , dominates the first expectation of the right hand side in (5.8). Hence we have the desired upper bound.

For the lower bound, by (5.9),

In view of the integrand on the right hand side, in the event the contract has not been terminated until , it is optimal to exercise at because waiting further would simply reduce the cash flow at rate . Therefore, the optimal stopping time must be in and

which gives the lower bound. ∎

Similarly, to approximate , we define

Lemma 5.2.

For and ,

for every and .

Proof.

On the other hand, because ,

| (5.10) |

Because in the integrand on the right-hand side, the payoff after is uniformly zero, we can replace with and this gives the lower bound.∎

Define the error functions

for every and . By Lemmas 5.1 and 5.2, these have bounds:

| (5.11) | ||||

| (5.12) |

for every and . If the exercise fee is set zero or sufficiently small (recall that the exercise fee is supposed to be much smaller than the change in default payment ), the bound (5.11) is expected to be small. Indeed, in light of the expectation , the discount and the indicator function keep its value small when is large and when it is small, respectively. The bound (5.12) is in comparison less tight because of the expectation on the lower bound. In the analytical proof of Lemma 5.2 (in particular (5.10)), this term cannot be removed, but is expected to be closer to its upper bound than to its lower bound in (5.12).

We shall show that the error functions vanish in the limit as which also implies that converges to the perpetual value function . We further show upon some suitable conditions that these error functions also converge to zero as and .

The first convergence result as is immediate because

Proposition 5.2.

For every fixed , as ,

-

(1)

and ,

-

(2)

and ,

-

(3)

and .

This proposition shows, for each of the callable/putable step-up/down cases, the asymptotic optimality as of the value functions and of the perpetual case; namely,

| (5.13) | ||||

| (5.14) |

as for every fixed . This also implies the effectiveness of the approximation using the strategies and . To this end, let , , and be the expected values corresponding to the strategy and . Observing that and (since implies on ), we can write

| (5.15) | ||||

Similarly, we conclude that

By (5.3) and (5.4), and can be obtained by adding/subtracting .

Proposition 5.3.

The asymptotic optimality of and holds. That is, for every ,

-

(1)

,

-

(2)

,

-

(3)

,

-

(4)

,

as .

Proof.

We now analyze the asymptotic behavior of the error functions in terms of for every fixed . In view of (5.11) and (5.12), each error bound contains the indicator function and this tends to decrease as decreases (or equivalently, as decreases). In particular, if is sufficiently small and fluctuates rapidly, these tend to vanish. The following result is immediate by the regularity of a Lévy process of unbounded variation; we refer the reader to page 142 of [30].

Proposition 5.4.

Fix and suppose is of unbounded variation. Then and as .

We now consider the limit as as an approximation for the case the maturity is small in comparison to the default time . In (5.11) and (5.12), while the error bounds do not converge to zero when , we can obtain the convergence for the case . By (3.5) and Exercise 8.5(i) of [30],

Hence, we can conclude the following limits.

Proposition 5.5.

Suppose and fix . Then,

-

(1)

as ,

-

(2)

.

5.4. Limits as and Approximation of Stopping Boundaries

The analytical bounds of the value function obtained above are certainly practical and are indeed tight depending on the chosen parameters. Next, we consider taking and also analyze the stopping boundary as a function of .

We first consider the case , or there is no exercise fee. Consider the callable case with :

for any small . Intuitively, for sufficiently small , because the movement of the process until the contract termination can be made arbitrarily small by choosing sufficient small (see (5.16) below), the investor’s strategy is constant; either waiting until contract termination () or exercising immediately (). The former gives a zero value. As for the latter case, we observe that

| (5.16) |

because, as in page 247 of Hilberink and Rogers [23],

| (5.17) |

and

where the last relation holds by (5.17). Consequently, if and only if (5.16) is positive. More precisely, let be such that

| (5.18) |

if it exists; otherwise, we set to be zero. Then the strategy to stop if and only if is asymptotically optimal as goes to zero. By symmetry, for , the strategy to stop if and only if is asymptotically optimal. As a trivial example, suppose does not have jumps (i.e. Brownian motion with drift), then and exercising immediately is optimal for while waiting until contract termination is optimal for at a time close to maturity.

The asymptotic behavior as for the case , on the other hand, is trivial. In this case, for both parties, it is never optimal to exercise at a time sufficiently close to the maturity. This is because as in (5.16) the premium payment until maturity and the default probability both converge to zero, while the exercise fee is strictly positive.

Using the asymptotic results obtained above, we now analyze the stopping boundary as a function of . The Markov property of suggests that the optimal stopping times of and admit the forms

for some deterministic functions and that map from to . Thanks to the asymptotic analysis as and obtained above, we can actually obtain the asymptotics of and as and . As , the optimal strategies for the perpetual case, and , are asymptotically optimal for and , respectively. Regarding the asymptotics as , the asymptotically optimal strategies depend on whether or . When , and are asymptotically optimal for and , respectively. When , is asymptotically optimal for both and . In summary,

-

(1)

and as ;

-

(2)

and as when ;

-

(3)

and as when .

In light of these asymptotic behaviors, Figure 5 illustrates the shapes of the stopping boundaries for the cases and . When , tends to increase as (or the time until maturity) increases while tends to decrease as increases. This is commonly observed in finite horizon optimal stopping problems; see Shiryaev and Peskir [41] for the cases of American options, sequential detection and sequential hypothesis testing. Intuitively speaking, if one has more time till maturity, he does not have to rush to exercise, and hence continuation region tends to increase (decrease) in width as the remaining time increases (decreases). We can confirm this monotonicity because by the definitions of and as in (3.25) and (5.18)

On the other hand, these monotonicities fail once an exercise fee is introduced ().

This observation is particular useful. Notice that a numerical lower bound can be attained by choosing any feasible strategy and computing its corresponding expected value via simulation. With this and the analytical upper bounds obtained above, one may obtain a tighter error bound. In particular, for the case , we can focus on the set of monotone functions and connecting / and . It is possible to approximate their shapes parametrically or non-parametrically. For a related technique where non-parametric regression is applied to approximate convex stopping regions, we refer the reader to, e.g., Section 6 of Dayanik et al. [16]. Regarding the continuity, monotonicity and smooth/continuous fit for the finite-horizon optimal stopping problem, we refer the reader to [41].

5.5. Term Structure of Credit Spreads

We now consider the credit spread that makes . We assume here that is always proportional to and set as we did in our numerical examples for some constant . Because the payoff function is monotone in , it is expected that there exists a unique value of credit spread as we have confirmed in our numerical results in Section 4 for the perpetual case. The function is potentially highly nonlinear both in terms of and . Nonetheless, we can obtain some asymptotic behaviors as and for every fixed as we describe below.

We first consider the asymptotic behavior of as as an approximation to the credit spread for a long maturity. While the convergence is not guaranteed, the credit spread of the perpetual case can be used as an approximation. The following holds immediately because both (5.13) and (5.14) hold for the case and .

Proposition 5.6.

For every ,

as .

We now consider the asymptotic behavior as . Suppose , then it is optimal never to exercise close to the maturity. Therefore, the asymptotic credit spread for all cases (callable/putable and step-up/down) is that of the standard CDS . As in (2.2), the credit spread of the standard CDS with finite-maturity is given by

As in page 247 of [23], we obtain

and this is the limit of the credit spread of our default swap as the maturity goes to zero.

The case is harder to analyze because the boundary depends on which also depends on how the premium is chosen. However, because for any and either stopping immediately or never exercising is asymptotically optimal as as we discussed in Section 5.4, the credit spread is expected to converge to either or .

6. Concluding Remarks

In summary, the incorporation of American step-up and step-down options give default swap investors the additional flexibility to manage and trade credit risks. The valuation of these contracts requires solving for the optimal timing to step-up/down for the protection buyer/seller. The perpetual nature of the contract allows us to compute analytically the investor’s optimal exercise threshold under quite general Lévy credit risk models. Using the symmetry properties between step-up and step-down contracts, we gain better intuition on various contract specifications, and drastically simplify the procedure to determine the credit spreads. The approximation for the finite-maturity case can be efficiently conducted using our analytical solutions on the perpetual case.

There are a number of avenues for future research. For instance, it would be interesting to value a default swap where both the protection buyer and seller can terminate the contract early. Then, the valuation problem can be formulated as a modified game option as introduced by Kifer [28]. In this case, we conjecture that threshold strategies will again be optimal for both parties and constitute Nash or Stackelberg equilibrium [20, 40]. Another direction for future research is to consider derivatives with multiple early exercisable step-up/down options. This is related to some optimal multiple stopping problems arising in other financial applications, such as swing options [13] and employee stock options [33].

Appendix A Proofs

A.1. Proof of Lemma 2.1

Applying the definitions of and (see (2.15)) and noting that whenever , we obtain, for every ,

A.2. Proof of Lemma 2.2

The proof follows from the same arguments for Lemma 2.1, and is thus omitted.

A.3. Proof of Lemma 3.2

A.4. Proof of Lemma 3.3

As discussed in p.228-229 of [30], for every fixed , the stochastic processes and are -martingales. Consequently, we have

| (A.1) |

With this and the definition of in (3.20), if , it follows that

| (A.2) |

Lemma A.1.

If , then we have .

Proof.

Lemma A.2.

If and , then we have .

Proof.

Suppose . Since and are continuous at by the continuous and smooth fit conditions, it follows from Lemma A.2 that , and then by (A.2) that . Suppose , we have by Lemma A.1. Now, in order to show on , it is sufficient to prove that is decreasing on . To this end, we rewrite as

where

| (A.5) |

By (A.1), for every . Furthermore, on , and hence

In order to show that this is decreasing in on , it is sufficient to show that the integrand in the right-hand side is decreasing in or equivalently is decreasing in for every fixed by noting that is a constant on .

Lemma A.3.

The function is decreasing on and is uniformly bounded below by .

Proof.

It is clear that in (A.5) is monotonically decreasing when because . Suppose . By differentiating , for , we get

A.5. Proof of Theorem 3.1

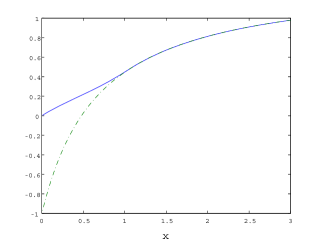

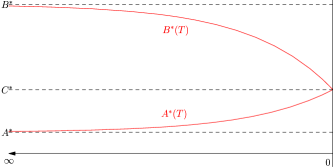

Due to the potential discontinuity and non-smoothness of the value function at zero, we need to proceed carefully. Before showing the main result, we first prove that as illustrated in Figure 1.

Suppose . Both and are both increasing in (see (2.20) and (3.20)). Since is increasing and non-negative, we must have and hence , and this is strictly positive if and only if has paths of bounded variation by Lemma 3.1. On the other hand, if (which implies is of bounded variation by Lemma 3.2), we also have because (3.17) implies that, for any , for every and .

We focus on the case it is discontinuous at (or is of bounded variation) and then address how the proof can be modified for the other case. We first construct a sequence of functions such that (1) it is continuous everywhere, (2) on and (3) pointwise for every fixed . This implies, by noting that and on , that decreases monotonically in to zero for every fixed by the monotone convergence theorem. Notice that is uniformly bounded because is. Hence, we can choose so that is also uniformly bounded for every fixed .

Suppose is the maximum difference between and . Using as the Poisson random measure for , we have by compensation formula (see, e.g., Theorem 4.4 in [30]), for every ,

| (A.6) |

Fix . By applying Ito’s formula to , we see that

| (A.7) |

is a local martingale. Suppose is the corresponding localizing sequence, namely, for given ,

where the second line makes sense by (A.6). Applying the dominated convergence theorem on the left-hand side and the monotone convergence convergence theorem on the right-hand side (here the integrands in the two expectations are positive and negative, respectively, by Lemma 3.3), we obtain again by (A.6)

Hence, (A.7) is in fact a martingale.

Now fix . By the optional sampling theorem, we have, for any , that

where the last equality holds by Lemma 3.3. Applying dominated convergence via (A.6) and because as , upon taking limits as and ,

| (A.8) |

Furthermore, the monotone convergence theorem yields the followings:

Therefore, by taking on both sides of (A.8) (note ), we have

where the last inequality follows from (3.22). This together with the fact that the stopping time corresponds to the value function completes the proof for the case is discontinuous at . For the case is continuous (unbounded variation case), the proof is simpler; the approximation via is no longer needed but the localization via is still needed because the value function fails to be at zero.

A.6. Proof of Lemma 3.5

A.7. Proof of Lemma 3.6

(1) We first show for every . Define a function by (3.26) and (3.27) but extended to the whole real line. This way, for , while does not vanish. Now fix . Using (3.26) and recalling that for every , we have

| (A.10) |

Here the generator can go into the integral because, by Lemma 3.1, is continuous when and is continuously differentiable when . On the other hand, if , then from (3.27) we derive that as above. Furthermore, it is straightforward to show that . Combining this with (A.10), we get .

References

- [1] L. Alili and A. E. Kyprianou. Some remarks on first passage of Lévy processes, the American put and pasting principles. Ann. Appl. Probab., 15(3):2062–2080, 2005.

- [2] S. Asmussen, F. Avram, and M. R. Pistorius. Russian and American put options under exponential phase-type Lévy models. Stochastic Process. Appl., 109(1):79–111, 2004.

- [3] S. Asmussen, D. Madan, and M. Pistorius. Pricing equity default swaps under an approximation to the CGMY Levy model. J. Comput. Finance, 11(2):79–93, 2007.

- [4] F. Avram, T. Chan, and M. Usabel. On the valuation of constant barrier options under spectrally one-sided exponential Lévy models and Carr’s approximation for American puts. Stochastic Process. Appl., 100:75–107, 2002.

- [5] F. Avram, A. E. Kyprianou, and M. R. Pistorius. Exit problems for spectrally negative Lévy processes and applications to (Canadized) Russian options. Ann. Appl. Probab., 14(1):215–238, 2004.

- [6] F. Avram, Z. Palmowski, and M. R. Pistorius. On the optimal dividend problem for a spectrally negative Lévy process. Ann. Appl. Probab., 17(1):156–180, 2007.

- [7] O. E. Barndorff-Nielsen. Processes of normal inverse Gaussian type. Finance Stoch., 2(1):41–68, 1998.

- [8] E. Baurdoux and A. E. Kyprianou. The McKean stochastic game driven by a spectrally negative Lévy process. Electron. J. Probab., 13:no. 8, 173–197, 2008.

- [9] E. Baurdoux and A. E. Kyprianou. The Shepp-Shiryaev stochastic game driven by a spectrally negative lévy process. Theory Probab. Appl., 53, 2009.

- [10] F. Black and J. Cox. Valuing corporate securities: Some effects of bond indenture provisions. J. Finance, 31:351–367, 1976.

- [11] S. Boyarchenko. Pricing of perpetual Bermudan options. Quant. Finance, 4:525–547, 2004.

- [12] J. Cariboni and W. Schoutens. Pricing credit default swaps under Lévy models. J. Comput. Finance, 10(4):1–21, 2007.

- [13] R. Carmona and N. Touzi. Optimal multiple stopping and valuation of swing options. Math. Finance, 18(2):239–268, April 2008.

- [14] P. Carr, H. Geman, D. B. Madan, and M. Yor. The fine structure of asset returns: An empirical investigation. J. Bus., 75(2):305–332, 2002.

- [15] T. Chan, A. Kyprianou, and M. Savov. Smoothness of scale functions for spectrally negative Lévy processes. Probab. Theory Related Fields, 150:691–708, 2011.

- [16] S. Dayanik, C. Goulding, and H. V. Poor. Bayesian sequential change diagnosis. Math. Oper. Res., 33(2):475–496, 2008.

- [17] E. Eberlein, W. Kluge, and P. J. Schönbucher. The Lévy Libor model with default risk. J. Credit Risk, 2(2):3–42, 2006.

- [18] M. Egami and K. Yamazaki. Phase-type fitting of scale functions for spectrally negative Lévy processes. Working paper. ArXiv:1005.0064, 2012.

- [19] M. Egami and K. Yamazaki. Precautionary measures for credit risk management in jump models. Stochastics, To appear.

- [20] E. Ekström and G. Peskir. Optimal stopping games for Markov processes. SIAM J. Control Optim., 47(2):684–702, 2008.

- [21] A. Feldmann and W. Whitt. Fitting mixtures of exponentials to long-tail distributions to analyze network performance models. Performance Evaluation, (31):245–279, 1998.

- [22] B. Hilberink and C. Rogers. Optimal capital structure and endogenous default. Finance Stoch., 6(2):237–263, 2002.

- [23] B. Hilberink and L. C. G. Rogers. Optimal capital structure and endogenous default. Finance Stoch., 6(2):237–263, 2002.

- [24] A. Hirsa and D. Madan. Pricing american options under variance gamma. J. Comput. Finance, 7(2), 2003.

- [25] J. Hull and A. White. The valuation of credit default swap options. J. Derivatives, 10(3):40–50, 2003.

- [26] K. Jackson, S. Jaimungal, and V. Surkov. Fourier space time stepping for option pricing with Lévy models. J. Comput. Finance, 12(2):1–29, 2008.

- [27] H. Jösson and W. Schoutens. Single name credit default swaptions meet single sided jump models. Rev. Derivatives Res., 11(1):153–169, 2008.

- [28] Y. Kifer. Game options. Finance Stoch., 4:443–463, 2000.

- [29] S. G. Kou and H. Wang. Option pricing under a double exponential jump diffusion model. Manage. Sci., 50(9):1178–1192, 2004.

- [30] A. E. Kyprianou. Introductory lectures on fluctuations of Lévy processes with applications. Universitext. Springer-Verlag, Berlin, 2006.

- [31] A. E. Kyprianou and Z. Palmowski. Distributional study of de Finetti’s dividend problem for a general Lévy insurance risk process. J. Appl. Probab., 44(2):428–448, 2007.

- [32] A. E. Kyprianou and B. A. Surya. Principles of smooth and continuous fit in the determination of endogenous bankruptcy levels. Finance Stoch., 11(1):131–152, 2007.

- [33] T. Leung and R. Sircar. Accounting for risk aversion, vesting, job termination risk and multiple exercises in valuation of employee stock options. Math. Finance, 19(1):99–128, 2009.

- [34] S. Z. Levendorski. Early exercise boundary and option prices in lévy driven models. Quant. Finance, 4(5):1469–7696, 2004.

- [35] R. L. Loeffen. On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes. Ann. Appl. Probab., 18(5):1669–1680, 2008.

- [36] D. Madan, C. P.P., and C. E.C. The variance gamma processes and option pricing. Europ. Finance Rev., 2:79–105, 1998.

- [37] R. Merton. Option pricing when underlying stock returns are discontinuous. J. Financial Econom, 3:125–144, 1976.

- [38] E. Mordecki. Optimal stopping and perpetual options for lévy processes. Finance Stoch., 4:473–493, 2002.

- [39] G. Peskir. Principles of optimal stopping and free-boundary problems, volume 68 of Lecture Notes Series (Aarhus). University of Aarhus, Department of Mathematics, Aarhus, 2001. Dissertation, University of Aarhus, Aarhus, 2002.

- [40] G. Peskir. Optimal stopping games and Nash equilibrium. Theory Probab. Appl., 53(3):558–571, 2009.

- [41] G. Peskir and A. Shiryaev. Optimal stopping and free-boundary problems. Lectures in Mathematics ETH Zürich. Birkhäuser Verlag, Basel, 2006.

- [42] G. Peskir and A. N. Shiryaev. Sequential testing problems for Poisson processes. Ann. Statist., 28(3):837–859, 2000.

- [43] G. Peskir and A. N. Shiryaev. Solving the Poisson disorder problem. In Advances in finance and stochastics, pages 295–312. Springer, Berlin, 2002.

- [44] C. Zhou. The term structure of credit spreads with jump risk. J. Banking Finance, 25:2015–2040, 2001.