The price impact of order book events

Abstract

We study the price impact of order book events - limit orders, market orders and cancelations - using the NYSE TAQ data for 50 U.S. stocks. We show that, over short time intervals, price changes are mainly driven by the order flow imbalance, defined as the imbalance between supply and demand at the best bid and ask prices. Our study reveals a linear relation between order flow imbalance and price changes, with a slope inversely proportional to the market depth. These results are shown to be robust to seasonality effects, and stable across time scales and across stocks. We argue that this linear price impact model, together with a scaling argument, implies the empirically observed “square-root” relation between price changes and trading volume. However, the relation between price changes and trade volume is found to be noisy and less robust than the one based on order flow imbalance.

1 Introduction

The availability of high-frequency records of trades and quotes has stimulated an extensive empirical and theoretical literature on the relation between order flow, liquidity and price movements in order-driven markets. A particularly important issue for applications is the impact of orders on prices: the optimal liquidation of a large block of shares, given a fixed time horizon, crucially involves assumptions on price impact (see Bertsimas and Lo [6], Almgren and Chriss [2], Obizhaeva and Wang [35]).

Various models for price impact have been proposed in the literature but there is little agreement on how to model it [7]. In the empirical literature, price impact has been described by various authors as linear, non-linear, square root, virtual, mechanical, temporary, instantaneous, permanent or transient. The only consensus seems to be the intuitive notion that imbalance between supply and demand moves prices.

The empirical literature on price impact has primarily focused on trades. One approach is to study the impact of “parent orders” gradually executed over time using proprietary data (see Engle et. al [14], Almgren et. al [3]). Alternatively, empirical studies on public data [16, 18, 20, 28, 29, 43, 38, 39] have investigated the relation between the direction and sizes of trades and price changes and typically conclude that the price impact of trades is an increasing, concave (“square root”) function of their size. This focus on trades leaves out the information in quotes, which provide a more detailed picture of price formation [15], and raises a natural question: is volume of trades truly the best explanatory variable for price movements in markets where many quote events can happen between two trades?

Understanding the price impact of orders is also important from a theoretical perspective, in the context of optimal order execution. Huberman and Stanzl [25] show that there are arbitrage opportunities if the effect of trades on prices is permanent and the impact is non-linear; Gatheral [19] extends this analysis by showing that if the price impact function is non-linear, impact needs to decay in a particular way to exclude arbitrage. Bouchaud et al. [9] associated the decay of price impact of trades with limit orders, arguing that there is a “delicate interplay between two opposite tendencies: strongly correlated market orders that lead to super-diffusion (or persistence), and mean reverting limit orders that lead to sub-diffusion (or anti-persistence)”. This insight implies that looking solely at trades, without including the effect of limit orders amounts to ignoring an important part of the price formation mechanism.

There is ample evidence that limit orders play an important role in determining price dynamics. Arriving limit orders significantly reduce the impact of trades [44] and the concave shape of the price impact function changes depending on the contemporaneous limit order arrivals [41]. The outstanding limit orders (also known as market depth) significantly affect the impact of an individual trade ([30]) and low depth is associated with large price changes [45, 17]. Hasbrouck and Seppi [22] use depth as one of the factors that determine price impact. The emphasis in these studies remains, however, on trades and there are few empirical studies that focus on limit orders from the outset. Notable exceptions are Engle & Lunde [15], Hautsch and Huang [23] who perform an impulse-response analysis of limit and market orders, Hopman [24] who analyzes the impact of different order categories over 30 minute intervals and Bouchaud et al. [12] who examine the impact of market orders, limit orders and cancelations at the level of individual events.

1.1 Summary

We conduct in this study an empirical investigation of the impact of order book events –market orders, limit orders and cancelations– on equity prices. Although previous studies give a relatively complex description of this impact, we argue that, in fact, their impact on price dynamics may be modeled parsimoniously through a single variable, the order flow imbalance (OFI), which represents the net order flow at the bid and ask and tracks changes in the size of the bid and ask queues by

-

•

increasing every time the bid size increases, the ask size decreases or the bid/ask prices increase

-

•

decreases every time the bid size decreases, the ask size increases or the bid/ask prices decrease.

Interestingly, this variable treats a market sell and a cancel buy of the same size as equivalent, since they have the same effect on the size of the bid queue. We find that this aggregate variable explains mid-price changes over short time scales in a linear fashion, for a large sample of stocks, with an average of 65%. The resulting price impact model relates prices, trades, limit orders and cancelations in a simple way: it is linear, requires the estimation of a single parameter and it is robust across stocks and across timescales.

The slope of this relation, which we call the price impact coefficient, exhibits intraday seasonality in line with known intraday patterns observed in spreads, market depth and price volatility [1, 4, 31, 34] which have been explained in terms of intraday shifts in information asymmetry [33] or informativeness of trades [21]. Motivated by a stylized model of the order book, we relate the intraday changes in the price impact coefficient to variations in market depth and show that price impact is inversely proportional to the depth of the order book. This allows us to explain intraday patterns in price impact and price volatility using only observable quantities - the order flow imbalance and the market depth, as opposed to unobservable parameters previously invoked in the literature, such as information asymmetry or informativeness of trades.

The intuition that “it takes volume to move prices”, though widely confirmed by empirical studies [27], is not easy to explain theoretically (see [37, Chapter 6.2]). In Section 4, we show that our price impact model, together with a scaling argument, leads to an apparent “square root” relation between price changes and trade volume, similar to some findings in the empirical literature [11, 40]. However, we argue that this relation is not robust and is a statistical artifact due to the aggregation of data.

1.2 Outline

The article is structured as follows. In Section 2, motivated by a stylized model of the order book, we specify a parsimonious model that links stock price changes, order flow imbalance and market depth. Section 3 describes the trades and quotes data and estimation results for our model. There, we also show how intraday patterns in depth and order flow imbalance generate intraday patterns in price impact and price volatility. In Section 4 we discuss the role of trading volume as an explanatory variable and show that order flow imbalance is more effective in explaining price moves than variables based on trades. We also derive a scaling relation between order flow imbalance and traded volume and show how the “square-root” price impact of volume follows from our model. We present our conclusions in Section 5.

2 A model for the price impact of orders

2.1 Variables

We focus on ‘Level I order book’: the limit orders sitting at the best bid and ask. Every observation of the bid and the ask consists of the bid price , the size of the bid queue (in number of shares), the ask price and the size of the ask queue (in number of shares):

![[Uncaptioned image]](/html/1011.6402/assets/BBO.png)

The bid price and size represent the demand for a stock, while the ask price and size represent the supply. We enumerate these observations by and compare with . Between two such observations, only one of the following events can occur:

-

•

or signifying an increase in demand

-

•

or signifying a decrease in demand

-

•

or signifying an increase in supply

-

•

or signifying a decrease in supply

We define the variable which measures the contribution of the th event to the size of bid and ask queues:

Note that if increases but remains the same, we assign , representing the size that was added at the bid. If decreases, we also assign , representing the size that was removed from the bid, whether due to a market sell or cancel buy order. If increases, we let , representing the size of a price-improving limit order. If decreases, we let , representing the size that was removed, whether due to a market order or a cancellation. The same classification is done for events on the ask side, with signs reversed.

Events affecting the order book occur at random times , and we define to be the number of events during . We define the order flow imbalance over time intervals as a sum of individual event contributions over these intervals:

where and are the index of the first and the index of the last event in the interval . The order flow imbalance is a measure of supply/demand imbalance, which encompasses trades, limit orders and cancelations. Whereas previous studies [10, 20, 22, 29, 38, 43] focused on measures of “trade imbalance”111Hopman [24] computes the supply/demand imbalance based on limit orders and trades, but not cancelations., using orders provides a more natural way of measuring supply and demand.

We also consider mid-price changes (in number of ticks) over the same time grid:

where is the mid-quote price at time and is the tick size (equal to 1 cent in our data).

2.2 A stylized model of the order book

Consider first a stylized model of the order book in which

-

1.

the number of shares at each price level beyond the best bid/ask is equal to .

-

2.

limit orders arrivals and cancelations occur only at the best bid/ask.

We will show that under these assumptions a linear relation holds between order flow imbalance and price changes. Consider three scenarios, when only market buy orders, limit buy orders or limit sell cancels happen over some time interval :

-

•

Market sell orders remove shares from the bid.

![[Uncaptioned image]](/html/1011.6402/assets/market.png)

-

•

Market sell orders remove shares from the bid, while limit buy orders add shares to the bid.

![[Uncaptioned image]](/html/1011.6402/assets/limit.png)

-

•

Market sell orders and limit buy cancels remove shares from the bid, while limit buy orders add shares to the bid.

![[Uncaptioned image]](/html/1011.6402/assets/cancel.png)

The three variables , and for the ask can be defined analogously. Under the above assumptions, the impact of order book events at the bid (ask) side of the book is additive and only depends on their net effect on the bid (ask) queue size:

Similarly, for the ask:

These relations are remarkably simple - they involve no parameters and incorporate the effects of all order book events on bid and ask prices. Although the following analysis can be carried for the bid and the ask prices separately, we take their average (the mid-price) to simplify the analysis:

Note that the above is equivalent (up to truncation) to

| (1) |

where and is the truncation error. This expression for is obtained from its definition by grouping individual order contrubutions by their types (limit buys, market sells, etc).

2.3 Model specification

In reality, order books have complex dynamics and the relation (1) will only hold in a statistical sense. For example, limit orders and cancelations occur at all levels of the order book. The distribution of depth across price levels often has humps, gaps and is itself a separate object of study [39, 46]. Moreover, the depth is subject to important intraday fluctuations. Finally, there may be hidden orders in the book which are not reported in the data [5]. With these considerations, we suggest the following relation:

| (2) |

where is the price impact coefficient and is a noise term due to the influence of deeper levels of the order book and rounding errors. Our earlier discussion suggests that the price impact coefficient is inversely related to market depth, which is itself subject to intraday fluctuations. We define a measure of depth by averaging the bid/ask queue sizes over intervals :

We therefore specify the following relation between the price impact coefficient in the time interval and our measure of market depth as:

| (3) |

where are constants and is a noise term. Note that the stylized model exposed above corresponds to .

The specification (2-3) may be regarded as a model of the instantaneous price impact over a short time interval . An order, submitted at , has a contribution and joins the aggregate order flow imbalance . If the order goes in the same direction as the majority of the orders (), it reinforces the concurrent order flow imbalance and can affect the price. If the order goes against the concurrent order flow imbalance (), it is compensated by other orders and may have an instantaneous impact of zero. In our model all events (including trades) have a linear price impact, equal to on average. Their realized impact, however, depends on the rest of the orders that arrive during the same time interval.

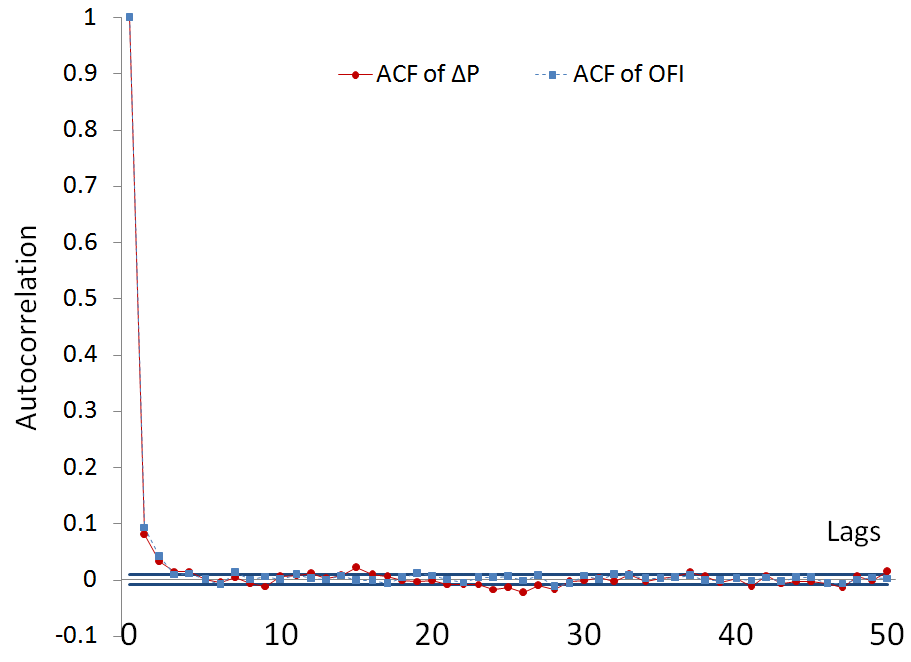

The idea that the concurrent limit order activity can make a difference in terms of trades’ impact was demonstrated by Stephens et al. [41], where authors show that the shape of the price impact function essentially depends on the contemporaneous limit order activity. Our approach can also be related to the model proposed by Bouchaud et al. [12]. where order book events have a linear impact on prices, which depends on their signs and types222Note that in our case all order book events have the same average impact, equal to , regardless of their type. As shown in [12], average impacts of different event types are empirically very similar, allowing to reasonably approximate them with a single number.. The major difference of our models lies in the aggregation across time and events. As argued in [12], order book events have complicated auto- and cross-correlation structures on the timescale of individual events, which typically vanish after 10 seconds. In our data the autocorrelations at a timescale of 10 seconds are small and quickly vanish as well (ACF plots for a representative stock are shown on Figure 1). Finally, Hasbrouck and Seppi [22] propose a model similar to (2, 3) for explaining the price impact of trades. Although their focus is on trades, they also allow the price impact coefficient to depend on contemporaneous liquidity factors and change through time.

However, the linear equation (2) is quite different from models of price impact that consider only the size of trades [18, 20, 29, 43, 38, 39]. Instead of modeling price impact of trades as a (nonlinear) function of trade size, we show that the price impact of all events (including trades) is a linear function of their size after events are aggregated into a single imbalance variable. In Section 4 we will argue that, first, the effect of trades on prices is adequately captured by the order flow imbalance and, second, that if one leaves out all events except trades, the relation 2 leads to an apparent concave relation between price changes and trade volume.

The next section provides an overview of the estimation results for our model.

3 Estimation and results

3.1 The trades and quotes (TAQ) data

Our data set consists of one calendar month (April, 2010) of trades and quotes (TAQ) data for 50 stocks. The stocks were selected by a random number generator from the S&P 500 constituents. The S&P 500 composition for that month was obtained from Compustat and the data for individual stocks was obtained from the TAQ consolidated quotes and TAQ consolidated trades databases. The data were obtained through Wharton Research Data Services (WRDS).

Consolidated quotes contains all changes in queue sizes at the best bid and ask. For each stock, a data update consists of a timestamp (rounded to the nearest second), bid price, bid size, ask price, ask size and exchange flag. Consolidated trades (or market orders) consist of a timestamp, a price and a size. These two data sets are often referred to as Level 1 data, as opposed to Level 2 data, which also includes quote updates deeper in the book.

Our reason for using TAQ data rather than Level 2 order book data, is that it is far more accessible, yet contains all events in the top order book (best bid and ask updates). We demonstrate that Level 1 TAQ data can be successfully used to study limit orders and we hope that more empirical studies of that subject will follow. We note that the ratio of the number of quote updates to the number trades is roughly 40 to 1 in our data. Many empirical studies have focused exclusively on trades rather than quotes, but the sheer ratio in the size of these data sets is a good indicator that more information may be conveyed by the quotes than by trades.

Using a procedure described in detail in the appendix, we aggregate all quote updates to estimate the National Best Bid and Offer sizes and prices (NBBO) at each quote update. Instead of aggregating all exchanges in this fashion, one may also simply filter by the exchange flag and study one exchange at the time. Focussing on one exchange at a time yields similar results.

We use a uniform grid in time with a timescale seconds to compute the price changes and the order flow imbalances. To test the robustness of our findings to the choice of the basic timescale, we repeated our calculations on a subsample of stocks for different values of , ranging from 10 quote updates (usually less than half of a second in our data) up to 10 minutes. The fit of our model generally increases with , but the rest of the results stays the same. Time aggregation serves two purposes: first, it alleviates the issue of data discreteness and second, it mitigates the errors due to the trade matching algorithm (described in the Appendix).

3.2 Empirical findings

We assume that the price impact coefficient is constant over each half-hour interval and estimate the model by ordinary least squares regression in each half-hour subsample for each stock:

| (4) |

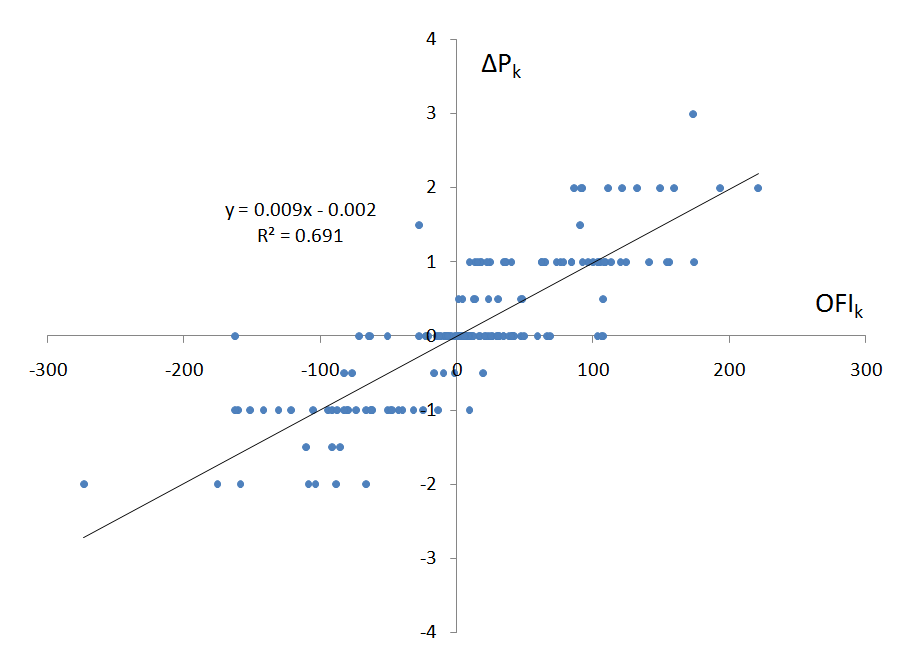

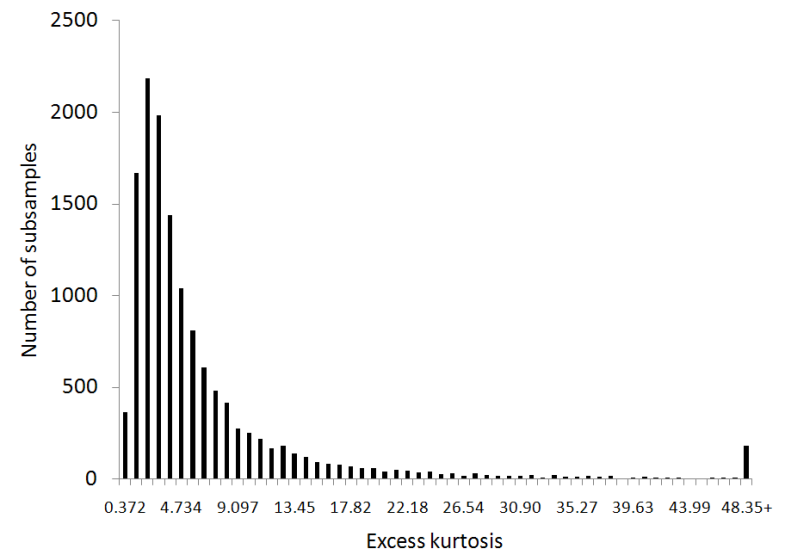

Figure 2 presents a scatter plot of against for one of the half-hour subsamples. Table 2 reports regression outputs, averaged across time for each stock. This table provides strong evidence of a linear relation between order flow imbalance and price changes. The goodness of fit is surprisingly high for all of the stocks, suggesting that the model (2) performs well regardless of stock-specific features333 We note that includes the contributions of price-changing order book events, leading to a possible tautology in the regression (4). This problem is inherent to all price impact modeling, because the explanatory variables (events or trades) can directly cause price changes. To test that the high in our regressions is not due to this tautology, we estimated (4) on a subsample of stocks, excluding the price-changing events from . With this change the declined, but remained in the 35%-60% region.. In addition to the high quality of fits, the regression coefficient is virtually always statistically significant (at a 95% level of the z-test), while the intercept is mostly insignificant. Figure 3 represents the histogram of excess kurtosis values of the residuals across subsamples: the relatively low level of kurtosis shows that the residuals are not predominantly associated with large price changes. Since the regression residuals demonstrate heteroscedasticity, we used White’s heteroscedasticity-consistent standard errors for the z-test. To check for higher order/nonlinear dependence we add a quadratic term to the regression. The increase in , from 65% to 68% on average, is barely noticeable and the coefficient is statistically insignificant in most samples.

Table 1. Descriptive statistics Name Ticker Price Daily Number of Number of Average Maximum Best quote volume, best quote trades Spread, spread, depth, shares updates cents cents shares Advanced Micro Devices AMD 9.61 20872996 417204 6687 1 1 1035 Apollo Group APOL 62.92 1949337 172942 4095 2 5 15 American Express AXP 45.21 8678723 559701 7748 1 24 79 Autozone AZO 179.03 243197 43682 1081 9 35 7 Bank of America BAC 18.43 164550168 1529395 15008 1 1 3208 Becton Dickinson BDX 78.07 1130362 61029 2968 2 5 15 Bank of New York Mellon BK 31.77 6310701 285619 5518 1 1 122 Boston Scientific BSX 7.13 25746787 309441 6768 1 1 2965 Peabody Energy corp BTU 47.14 5210642 298616 7267 1 3 29 Caterpillar CAT 67.20 6664891 392499 8224 1 2 38 Chubb CB 52.22 1951618 149010 3601 1 2 43 Carnival CCL 40.16 4275911 215427 5503 1 2 53 Cincinnati Financial CINF 29.41 688914 51373 1528 1 2 42 CME Group CME 322.83 418955 38504 1412 31 103 5 Coach COH 41.91 3126469 176795 4458 1 2 41 ConocoPhillips COP 56.09 9644544 426614 8621 1 2 84 Coventry Health Care CVH 24.16 1157022 79305 2213 1 2 38 Denbury Resources DNR 17.88 5737740 263173 4643 1 1 186 Devon Energy DVN 66.98 3260982 177006 5805 2 4 18 Equifax EFX 35.34 799505 62957 1945 1 3 39 Eaton ETN 78.53 1757136 67989 3580 2 6 13 Fiserv FISV 52.56 1038311 58304 2208 1 3 20 Hasbro HAS 39.48 1322037 86040 2672 1 2 34 HCP HCP 32.63 2872521 213045 4357 1 2 48 Starwood Hotels HOT 50.59 3164807 150252 5106 2 4 22 Kohl’s KSS 56.88 3064821 128196 4936 1 3 27 L-3 Communications LLL 94.64 670937 72818 2141 2 6 9 Lockheed Martin LMT 84.14 1416072 88254 3333 2 5 15 Macy’s M 23.40 8324639 491756 6469 1 1 176 Marriott MAR 34.45 5014098 238190 5499 1 2 65 McAfee MFE 40.04 2469324 109073 3561 1 2 40 McGraw-Hill MHP 34.90 1954576 102389 3261 1 2 42 Medco Health Solutions MHS 63.22 2798098 109382 4680 1 3 25 Merck MRK 36.03 13930842 448748 7997 1 1 231 Marathon Oil MRO 32.33 5035354 341408 5522 1 1 143 MeadWestvaco MWV 26.96 1035547 92825 2312 1 3 37 Newmont Mining NEM 53.43 5673718 435295 7717 1 2 38 Omnicom OMC 41.17 3357585 150800 4359 1 2 65 MetroPCS Communications PCS 7.53 4424560 107967 2901 1 1 523 Pultegroup PHM 11.80 6834683 262420 4604 1 1 319 PerkinElmer PKI 23.98 1268774 78114 2127 1 2 72 Ryder System R 44.01 631889 47422 2085 2 5 11 Reynolds American RAI 54.44 773387 56236 2076 1 4 22 Schlumberger SLB 67.94 9476060 440839 10286 1 2 39 Teco Energy TE 16.52 1070815 70318 1807 1 1 148 Time Warner Cable TWC 53.21 1770234 88286 3554 2 3 22 Whirlpool WHR 97.73 1424264 134152 3348 4 9 10 Windstream WIN 11.03 2508830 104887 2937 1 1 798 Watson Pharmaceuticals WPI 42.51 895967 63094 2024 1 3 29 XTO Energy XTO 48.13 7219436 612804 5040 1 7 225 Grand mean 51.75 7512376 223232 4552 2 6 227

Table 1 presents the average mid-price, daily transaction volume, daily number of best quote updates, daily number of trades, spread and the depth at the best bid and ask for 50 randomly chosen U.S. stocks. All values are calculated from the filtered data, that consists of 21 trading day during April, 2010.

Table 2. Relation between price changes and order flow imbalance. Ticker Average results Hypothesis testing AMD -0.0032 -0.17 0.0008 9.96 1.4E-07 0.68 64% 0% 98% 22% APOL 0.0038 0.10 0.0555 10.32 -2.2E-04 -1.17 63% 12% 91% 4% AXP 0.0019 0.08 0.0082 13.87 -3.8E-06 -0.88 69% 11% 100% 5% AZO 0.0101 0.33 0.1619 6.39 -9.3E-04 -0.89 47% 23% 97% 3% BAC -0.0018 -0.09 0.0002 18.36 1.9E-09 0.01 79% 1% 100% 8% BDX -0.0008 -0.06 0.0536 10.08 -1.1E-04 -0.38 63% 9% 100% 8% BK -0.0078 -0.19 0.0069 14.97 -4.0E-06 -0.57 74% 3% 100% 6% BSX 0.0000 -0.01 0.0003 6.12 7.8E-08 1.14 58% 0% 81% 22% BTU 0.0048 0.12 0.0242 14.51 -3.5E-05 -1.26 72% 11% 100% 3% CAT 0.0147 0.23 0.0194 14.85 -1.9E-05 -1.13 71% 12% 99% 3% CB -0.0086 -0.07 0.0191 11.97 -3.5E-07 0.00 64% 5% 100% 8% CCL -0.0067 -0.18 0.0140 13.88 -1.2E-05 -0.64 70% 3% 99% 7% CINF -0.0030 -0.02 0.0260 10.73 -7.0E-06 0.27 70% 1% 98% 16% CME 0.0506 0.05 0.6262 4.98 -7.2E-03 -0.99 35% 15% 94% 2% COH -0.0221 -0.45 0.0179 12.75 -1.7E-05 -0.77 69% 2% 100% 3% COP -0.0008 0.06 0.0084 12.50 -5.8E-06 -1.17 68% 10% 100% 3% CVH -0.0034 -0.06 0.0217 10.83 7.6E-06 0.20 65% 3% 99% 10% DNR -0.0008 -0.04 0.0045 12.76 -1.3E-07 0.19 69% 1% 99% 13% DVN 0.0112 0.18 0.0370 11.48 -1.0E-04 -1.59 65% 17% 97% 0% EFX -0.0032 -0.04 0.0222 8.71 6.4E-05 0.64 56% 1% 98% 18% ETN -0.0076 0.05 0.0712 10.51 -2.3E-04 -1.14 65% 14% 98% 1% FISV -0.0002 0.06 0.0397 10.42 -2.3E-05 -0.19 63% 4% 100% 8% HAS -0.0031 -0.02 0.0222 11.45 4.7E-06 0.21 67% 3% 100% 16% HCP -0.0078 -0.17 0.0150 13.60 -1.4E-05 -0.46 67% 2% 100% 6% HOT -0.0012 0.05 0.0345 12.64 -7.2E-05 -1.21 68% 10% 99% 2% KSS -0.0030 -0.04 0.0317 13.82 -5.4E-05 -0.80 71% 10% 98% 3% LLL 0.0160 0.32 0.1000 11.76 -3.8E-04 -0.75 67% 14% 96% 3% LMT 0.0006 0.00 0.0520 13.58 -1.2E-04 -0.98 72% 14% 100% 1% M -0.0010 0.04 0.0043 15.82 8.8E-08 0.13 75% 0% 100% 12% MAR -0.0039 -0.02 0.0121 14.61 -4.1E-06 -0.23 71% 3% 100% 4% MFE 0.0087 0.16 0.0205 12.72 -3.8E-05 -0.38 68% 7% 100% 7% MHP -0.0073 -0.13 0.0211 11.62 5.8E-06 0.14 68% 2% 99% 11% MHS -0.0055 -0.16 0.0334 11.70 -8.3E-05 -1.10 66% 9% 99% 3% MRK -0.0065 -0.20 0.0032 12.53 -5.4E-07 -0.38 69% 1% 100% 8% MRO 0.0018 0.07 0.0058 13.67 -3.6E-07 0.22 69% 5% 100% 13% MWV -0.0011 0.01 0.0205 11.79 -1.7E-05 -0.25 68% 3% 100% 7% NEM -0.0102 -0.22 0.0170 13.81 -1.9E-05 -1.36 71% 8% 100% 2% OMC -0.0099 -0.28 0.0144 11.88 -4.5E-06 -0.01 65% 2% 99% 13% PCS -0.0006 -0.03 0.0015 5.21 1.8E-06 1.01 53% 0% 79% 24% PHM 0.0006 0.03 0.0027 10.33 8.4E-07 0.55 66% 1% 98% 21% PKI -0.0004 -0.03 0.0102 7.25 4.1E-05 1.10 53% 2% 94% 29% R 0.0006 0.03 0.0667 10.14 3.7E-05 0.01 63% 8% 98% 10% RAI -0.0070 -0.10 0.0396 10.40 2.6E-05 0.01 66% 5% 100% 11% SLB -0.0077 -0.15 0.0198 16.76 -1.8E-05 -1.15 76% 7% 100% 1% TE 0.0011 0.05 0.0049 6.66 1.4E-05 1.45 54% 2% 86% 30% TWC -0.0130 -0.13 0.0384 11.80 -5.6E-05 -0.44 64% 8% 99% 5% WHR 0.0628 0.63 0.1278 10.26 -3.3E-04 -0.80 65% 22% 97% 4% WIN -0.0004 -0.03 0.0009 3.12 1.5E-06 0.76 44% 1% 60% 15% WPI -0.0090 -0.21 0.0270 10.47 2.9E-05 0.28 66% 3% 98% 14% XTO -0.0088 -0.18 0.0029 13.28 2.7E-07 0.30 65% 0% 100% 18% Average 0.0002 -0.02 0.0398 11.47 -2.0E-04 -0.28 65% 6% 97% 9%

Table 2 presents a cross-section of results (averaged across time) for the regressions: ,

,

where are the 10-second mid-price changes and are the contemporaneous order flow imbalances. These regressions were estimated using 273 half-hour subsamples (indexed by ) for each stock and their outputs were averaged across subsamples. Each subsample typically contains about 180 observations (indexed by ). The t-statistics were computed using White’s standard errors. For brevity, we report the , the average and the average only for the first regression (with a single term). There is almost no difference between averages of estimates and and the in two regressions. The last three columns report the percentage of samples where the coefficient(s) passed the z-test at the 5% significance level.

Next, we estimate the parameters and in (3). For each stock, we first obtain fit via a loglinear regression:

| (5) |

Then, using , we estimate in a linear regression:

| (6) |

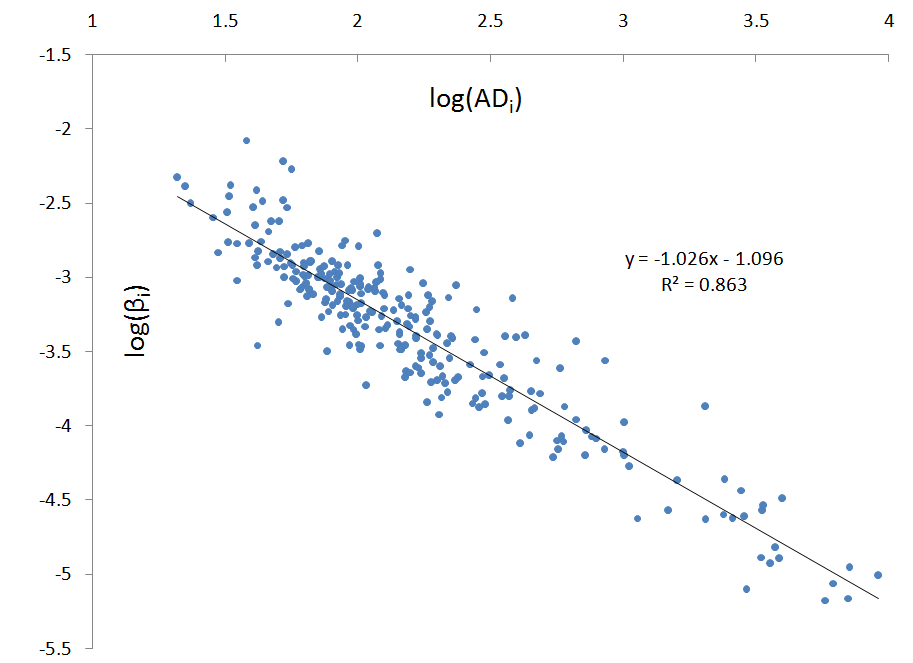

Both regressions are estimated using ordinary least squares. The results are presented in Table 3: the quality of these fits convincingly demonstrates that the instantaneous price impact (measured by ) is inversely related to market depth. There are three stocks with bad fits (namely APOL, AZO and CME) and we note that they also have wide spreads and low values of depth. It is possible that for these stocks other factors, such as the presence of hidden orders and depth beyond the best price levels the order book may dominate the instantaneous price impact. The intercept is highly statistically significant (being an estimate of parameter ) and , which is included to absorb the means, is mostly insignificant. Since the residuals of these regressions appear to be autocorrelated, the t-statistics and confidence intervals in Table 3 are computed with Newey-West standard errors. Coinciding with our intuition for (1), estimates are very close to 1 across stocks and the hypothesis cannot be rejected for 35 out of 50 stocks. The restricted model (with ) also demonstrates a good quality of fit, making this a good approximation. However, the coefficient is generally different from in (1). Lower values of mean that mid-prices are (on average) more resilient to the incoming orders than indicated by (which is only a rough measure of market depth). In summary, appears to be a good approximation for most of the stocks and only the constant needs to be calibrated to the data. The general case of regression (5) is illustrated on Figure 4 by a scatter plot for a representative stock.

Table 3. Relation between the price impact coefficient and market depth. Ticker Parameter estimates 5% confidence intervals Fit measures AMD 0.23 0.94 27.74 23.11 0.22 0.25 0.86 1.02 78% 86% 86% APOL 0.27 0.36 4.43 1.05 0.15 0.39 -0.32 1.04 2% 30% 31% AXP 0.14 0.83 13.95 26.48 0.12 0.16 0.77 0.89 84% 76% 76% AZO 0.39 0.67 5.48 5.10 0.25 0.53 0.41 0.92 13% 17% 16% BAC 0.27 0.96 25.27 19.74 0.25 0.29 0.90 1.03 76% 87% 87% BDX 0.38 1.04 22.83 18.64 0.35 0.41 0.93 1.15 71% 68% 68% BK 0.21 0.92 17.52 54.54 0.19 0.24 0.88 0.95 93% 91% 90% BSX 0.35 0.98 14.98 24.55 0.31 0.40 0.90 1.05 73% 81% 81% BTU 0.42 1.12 40.90 36.77 0.40 0.44 1.06 1.18 87% 83% 83% CAT 0.29 0.96 21.70 16.87 0.27 0.32 0.85 1.07 87% 83% 83% CB 0.32 1.02 27.08 49.61 0.30 0.34 0.98 1.06 92% 89% 89% CCL 0.26 0.96 24.36 37.55 0.24 0.29 0.91 1.01 87% 83% 83% CINF 0.31 0.97 20.05 47.39 0.28 0.34 0.93 1.01 92% 88% 88% CME 1.27 0.50 2.55 1.99 0.29 2.24 0.01 0.99 2% 4% 3% COH 0.37 1.05 15.29 36.65 0.32 0.43 0.98 1.12 77% 75% 75% COP 0.13 0.80 8.52 15.95 0.10 0.16 0.70 0.89 75% 66% 66% CVH 0.32 1.03 26.50 37.51 0.29 0.34 0.98 1.08 89% 89% 89% DNR 0.23 0.96 32.44 40.90 0.22 0.24 0.92 1.01 91% 89% 89% DVN 0.26 0.91 13.50 16.66 0.22 0.30 0.80 1.02 45% 56% 56% EFX 0.30 0.99 20.16 26.13 0.27 0.33 0.92 1.07 84% 79% 79% ETN 0.45 1.07 11.51 17.34 0.38 0.53 0.95 1.19 60% 56% 56% FISV 0.34 1.01 23.35 30.70 0.31 0.36 0.94 1.07 84% 77% 77% HAS 0.32 1.00 26.36 46.00 0.30 0.34 0.96 1.05 89% 83% 83% HCP 0.19 0.89 22.93 51.27 0.17 0.21 0.86 0.93 94% 90% 90% HOT 0.44 1.12 19.53 26.59 0.40 0.48 1.04 1.20 82% 80% 79% KSS 0.39 1.05 24.40 33.17 0.36 0.42 0.99 1.11 85% 78% 78% LLL 0.43 1.01 13.21 14.45 0.37 0.50 0.87 1.14 51% 58% 58% LMT 0.50 1.14 7.31 13.49 0.37 0.64 0.98 1.31 60% 52% 52% M 0.19 0.90 37.41 57.39 0.18 0.20 0.87 0.93 94% 92% 92% MAR 0.28 0.98 22.58 50.20 0.25 0.30 0.94 1.02 92% 88% 88% MFE 0.31 1.01 20.28 46.20 0.28 0.34 0.96 1.05 91% 86% 86% MHP 0.27 0.94 19.60 33.62 0.24 0.30 0.89 1.00 82% 74% 74% MHS 0.53 1.16 17.03 34.25 0.47 0.59 1.10 1.23 85% 81% 80% MRK 0.13 0.81 18.07 32.20 0.11 0.14 0.76 0.86 87% 81% 81% MRO 0.23 0.94 35.54 49.68 0.21 0.24 0.91 0.98 94% 93% 93% MWV 0.32 1.05 28.07 37.81 0.30 0.34 1.00 1.10 90% 85% 85% NEM 0.26 0.98 18.79 25.97 0.23 0.28 0.91 1.05 81% 77% 77% OMC 0.30 0.96 29.47 17.76 0.28 0.32 0.85 1.06 83% 85% 85% PCS 0.30 1.02 21.27 18.73 0.27 0.33 0.90 1.14 53% 82% 82% PHM 0.28 0.98 36.43 35.12 0.26 0.29 0.93 1.04 86% 90% 90% PKI 0.30 1.07 26.59 38.35 0.28 0.32 1.00 1.13 82% 88% 87% R 0.37 1.02 18.51 15.76 0.33 0.41 0.90 1.15 57% 58% 58% RAI 0.35 1.03 24.94 40.46 0.32 0.38 0.98 1.08 86% 76% 76% SLB 0.35 1.06 18.98 40.60 0.31 0.38 1.01 1.12 91% 88% 88% TE 0.21 1.00 16.18 24.28 0.18 0.24 0.92 1.09 70% 86% 86% TWC 0.37 1.04 17.70 15.96 0.33 0.42 0.91 1.16 72% 79% 79% WHR 0.78 1.18 9.24 11.54 0.61 0.94 0.98 1.38 44% 43% 42% WIN 5.81 1.60 16.09 11.70 5.11 6.52 1.33 1.87 28% 71% 71% WPI 0.27 0.92 19.33 28.99 0.24 0.30 0.86 0.98 78% 76% 76% XTO 0.31 1.04 30.85 39.51 0.29 0.33 0.98 1.09 89% 91% 91% Grand mean 0.45 0.98 20.74 29.53 0.38 0.52 0.88 1.08 74% 75% 75%

Table 3 presents the results of regressions: ,

, where is the price impact coefficient for the -th half-hour subsample and is the average market depth for that subsample. These regressions were estimated for each of the 50 stocks, using 273 estimates of for that stock, obtained from (4). The second regression uses estimates obtained from the first regression. The t-statistics and the confidence intervals were computed using Newey-West standard errors. Confidence intervals are built with normal critical values. The last three columns provide three alternative fit measures - the of the linear regression (5), the squared correlation between and fitted values and the squared correlation between and .

3.3 Intraday patterns

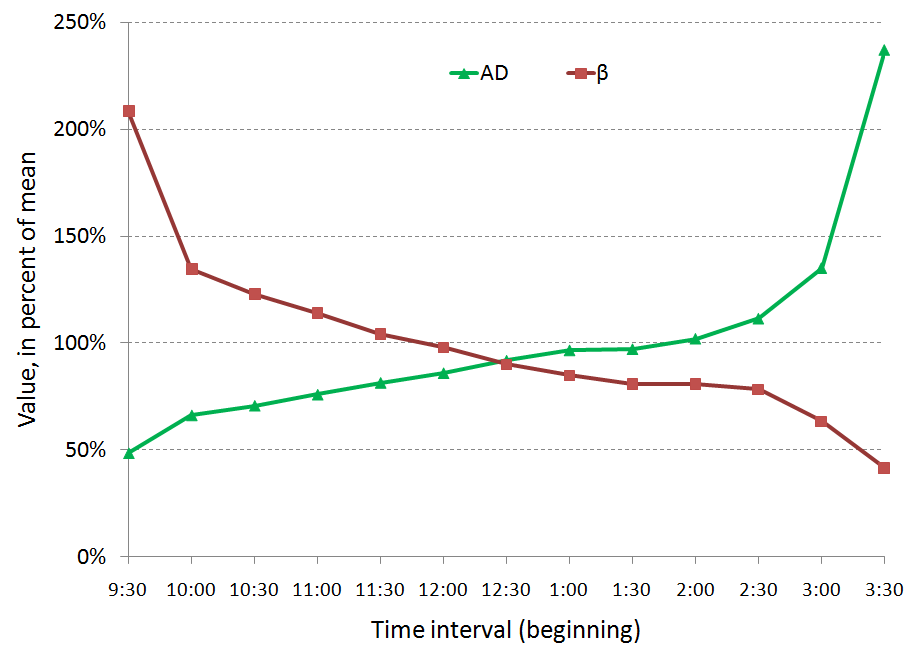

The link that we established between the price impact and the market depth has an important implication. Since the market depth follows a predictable pattern of intraday seasonality ([1], [31]), the price impact coefficient must also have a predictable intraday pattern. To demonstrate it, we averaged for each stock and each half-hour interval across days, resulting in the intraday seasonality pattern for that stock, normalized these values by the average of that stock and averaged the normalized seasonality patterns across stocks. The same procedure was repeated for and the results are shown on Figure 5.

Near the market open, depth is two times lower than it is on average, indicating that the order book is relatively shallow. In a shallow market, the incoming orders can easily affect the mid-price and the price impact coefficient is two times higher near the market open than on average. Moreover, price impact is five times higher at the market open compared to the market close.

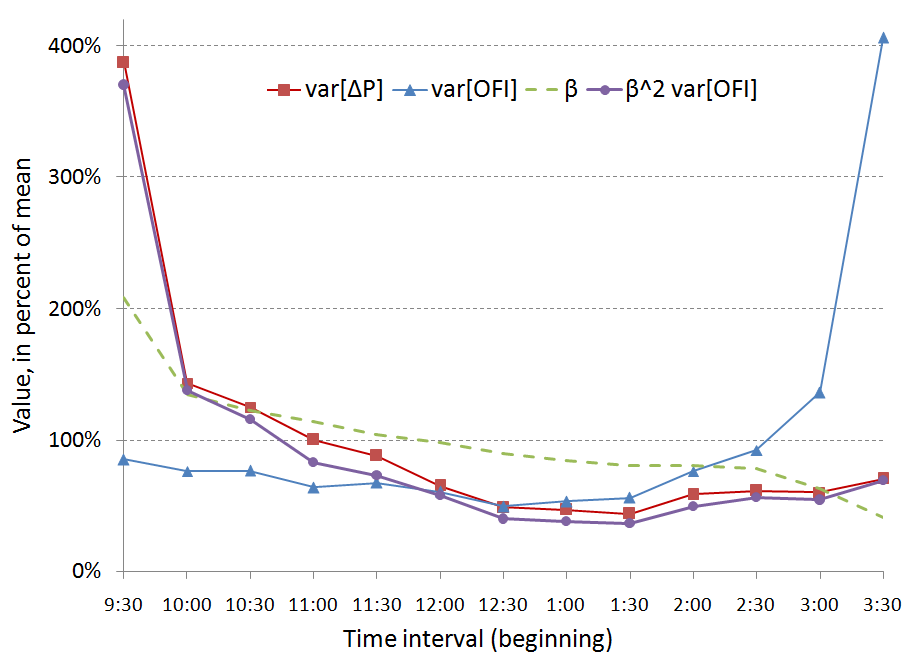

The intraday pattern in price impact can be used to explain the intraday patterns in price volatility, observed by many researchers ([1], [4], [21], [33]). Similarly to the price impact coefficient and the market depth, we computed the intraday patterns in variances of and , using half-hour subsamples (indexed by ). Taking the variance on both sides of equation (2) demonstrates the link between , and :

| (7) |

The average patterns are plotted on Figure 6. Notice that the price volatility has a sharp peak near the market open, while the volatility of order flow imbalance has a peak near the market close. This peak is, however, offset by a low price impact, which gradually declines throughout the day. For the -th half-hour interval, the equation (7) implies that which is demonstrated on Figure 6444 was computed from the average patterns of and .

The intraday pattern in price variance was explained by Madhavan et al. [33] in terms of a structural model. They argued that the volatility is higher in the morning because of the higher inflow of both public and private information. Similarly, Hasbrouck [21] argued that the peak of price volatility at market open is mostly due to higher intensity of public information. Both studies agree that the impact of trades is larger in the morning. Our model contributes to this discussion by explaining the peak of price volatility using tangible quantities, rather than unobservable parameters. We also argue that the price impact of trades and the information asymmetry may be, in fact, two sides of the same coin.

First, we associate the higher volatility of order flow imbalance at market the open and close with a higher rate of trading, that is, higher inflow of public and private information. Second, if the bid-ask spread is small (it is mostly equal to 1 cent in our data), limit order traders may avoid being “picked off” only by lowering the number of submitted orders, reducing the depth. Therefore, if limit order traders are aware of information asymmetry in the morning, the low depth may simply indicate this asymmetry. In our model, low depth also implies a higher price impact, making the information advantages harder to realize at the market open.

4 Price impact of trades

4.1 Trade imbalance vs order flow imbalance

The previous section discussed the linear relation between price changes and - our measure of supply/demand imbalance. However, little has been said about trade imbalances, which are widely used in the academic literature [10, 20, 22, 24, 29, 38] and in practice [43]. The aim of this section is to compare the price impact of trades and order flow imbalance and show that the (nonlinear) price impact of trade volume may be derived from our linear model for the price impact of order flow.

For convenience we will call ‘buy trade’ a transaction initiated by a market buy order and ‘sell trade’ a transaction initiated by a market sell order. We define the trade imbalance during a time interval as the difference between volumes of buy and sell trades during that interval:

Here, is the size of a buyer-initiated trade that occurs at the -th quote; if no buy trade occurs at that quote. Similarly, is the size of a sell trade that occurs at the -th quote or zero. The procedure that matches trades with quotes and classifies them as buys or sells is described in the Appendix.

To compare the explanatory power of trade and order flow imbalances with respect to price changes, we perform the following regressions:

| (8a) | |||

| (8b) | |||

| (8c) | |||

The regressions are estimated separately for every half-hour subsample of data (indexed by ). If the effect of trades is included in the order flow imbalance, the coefficients in (8c) must be indistinguishable from zero. We note that regressions (8a-8c) contain only the linear terms, because we found no evidence of non-linear price impacts in our data (for neither nor ). The average results of these regressions are presented in Panel A of Table 4. Clearly, when and are taken individually, each of them has a statistically significant influence on price changes. Comparing the two we observe that explains price changes better than - the average for order flow imbalance is 65% compared to 32% for the trade imbalance. When two variables are used together to explain price changes, the dependence on trade imbalance becomes questionable. The average t-statistic of decreases by a factor of four and the coefficients are statistically significant in only 31% of subsamples. However, the dependence on remains convincingly strong.

Our findings show that:

-

1.

The order flow imbalance explains price movements better than the imbalance of trades.

-

2.

The effect of trade imbalance is adequately included in , a more general measure of supply/demand imbalance.

Table 4. Comparison of order flow imbalance and trade imbalance. Panel A: Detailed results for changes in mid prices Ticker Order flow imbalance Trade imbalance Both covariates AMD 64% 9.96 98% 382 39% 4.15 86% 140 67% 6.49 1.26 93% 34% 214 APOL 63% 10.32 91% 396 30% 4.14 84% 83 66% 8.00 1.09 89% 26% 211 AXP 69% 13.87 100% 449 34% 4.72 83% 101 71% 10.05 1.50 100% 44% 241 AZO 47% 6.39 97% 179 30% 4.09 90% 87 54% 5.02 2.34 96% 68% 118 BAC 79% 18.36 100% 774 45% 6.31 96% 157 80% 12.55 0.72 99% 19% 397 BDX 63% 10.08 100% 362 28% 4.02 82% 79 65% 7.88 1.23 97% 34% 195 BK 74% 14.97 100% 610 36% 4.58 81% 117 75% 10.68 0.68 99% 17% 313 BSX 58% 6.12 81% 338 31% 2.57 54% 106 62% 4.51 0.57 73% 12% 189 BTU 72% 14.51 100% 527 35% 5.21 88% 103 74% 10.90 1.31 99% 32% 277 CAT 71% 14.85 99% 498 33% 5.01 86% 94 72% 11.27 1.28 99% 38% 262 CB 64% 11.97 100% 378 33% 4.66 88% 102 66% 8.42 1.34 99% 37% 202 CCL 70% 13.88 99% 478 32% 4.55 85% 93 71% 10.50 0.98 99% 26% 247 CINF 70% 10.73 98% 552 39% 4.26 87% 141 72% 7.17 1.01 96% 27% 297 CME 35% 4.98 94% 112 24% 3.39 75% 63 44% 4.10 2.18 92% 59% 78 COH 69% 12.75 100% 457 29% 3.91 82% 80 70% 10.06 0.87 100% 22% 238 COP 68% 12.50 100% 450 35% 4.92 84% 107 70% 9.19 1.42 100% 40% 240 CVH 65% 10.83 99% 418 35% 4.10 84% 114 67% 7.30 1.01 97% 25% 222 DNR 69% 12.76 99% 471 32% 3.98 81% 101 70% 9.29 1.01 97% 24% 246 DVN 65% 11.48 97% 414 33% 4.83 88% 96 68% 8.58 1.70 93% 48% 226 EFX 56% 8.71 98% 289 31% 3.72 80% 101 60% 6.21 1.64 96% 43% 167 ETN 65% 10.51 98% 389 25% 3.59 71% 69 67% 8.66 1.04 98% 29% 209 FISV 63% 10.42 100% 380 28% 3.79 81% 79 65% 8.12 0.88 100% 25% 201 HAS 67% 11.45 100% 427 32% 4.04 84% 97 68% 8.53 0.89 100% 24% 223 HCP 67% 13.60 100% 417 31% 4.43 82% 91 68% 10.01 1.05 100% 32% 217 HOT 68% 12.64 99% 438 27% 3.86 77% 74 70% 9.94 1.17 99% 29% 231 KSS 71% 13.82 98% 525 31% 4.43 81% 91 72% 10.83 0.94 97% 25% 274 LLL 67% 11.76 96% 485 36% 5.07 90% 117 70% 8.58 1.63 94% 44% 270 LMT 72% 13.58 100% 516 35% 4.89 90% 105 73% 10.19 1.50 99% 40% 277 M 75% 15.82 100% 640 35% 4.41 84% 108 76% 11.38 0.97 100% 26% 330 MAR 71% 14.61 100% 498 34% 4.77 89% 105 72% 10.45 1.05 100% 27% 258 MFE 68% 12.72 100% 463 31% 4.17 82% 93 69% 9.06 0.73 99% 18% 239 MHP 68% 11.62 99% 489 31% 3.85 84% 96 70% 8.92 0.77 98% 19% 257 MHS 66% 11.70 99% 414 28% 4.03 77% 80 68% 9.10 1.11 99% 27% 218 MRK 69% 12.53 100% 451 31% 4.08 82% 93 70% 9.20 0.76 100% 20% 235 MRO 69% 13.67 100% 465 35% 4.66 89% 104 70% 9.73 0.91 100% 24% 241 MWV 68% 11.79 100% 452 34% 4.37 86% 102 69% 8.63 0.80 100% 24% 237 NEM 71% 13.81 100% 490 34% 4.99 81% 100 72% 10.24 1.53 99% 43% 260 OMC 65% 11.88 99% 411 30% 4.14 85% 88 67% 8.99 0.96 99% 24% 216 PCS 53% 5.21 79% 297 35% 2.68 59% 169 58% 3.44 0.86 71% 20% 195 PHM 66% 10.33 98% 416 35% 3.87 84% 115 68% 7.28 0.95 93% 29% 224 PKI 53% 7.25 94% 263 28% 3.03 70% 89 57% 5.39 1.24 88% 32% 148 R 63% 10.14 98% 352 27% 3.92 86% 71 65% 8.07 1.20 97% 30% 188 RAI 66% 10.40 100% 422 36% 4.67 89% 111 68% 7.52 1.11 99% 31% 224 SLB 76% 16.76 100% 644 32% 4.54 79% 94 77% 13.02 1.24 100% 36% 336 TE 54% 6.66 86% 301 37% 3.27 67% 175 60% 4.34 1.32 79% 29% 200 TWC 64% 11.80 99% 377 31% 4.26 77% 93 66% 8.46 1.34 99% 37% 201 WHR 65% 10.26 97% 394 29% 4.29 88% 85 67% 8.17 1.43 96% 39% 217 WIN 44% 3.12 60% 243 41% 2.68 54% 249 58% 1.78 1.39 42% 29% 206 WPI 66% 10.47 98% 437 32% 3.91 83% 100 68% 7.82 1.05 97% 30% 232 XTO 65% 13.28 100% 399 21% 3.05 63% 54 66% 10.72 1.05 100% 27% 209 Grand mean 65% 11.47 97% 429 32% 4.18 81% 103 67% 8.49 1.16 95% 31% 231 Panel B: Average results for changes in transaction prices trades 14% 15.74 98% 464 1% 2.69 63% 26 15% 14.17 -2.58 98% 54% 245 trades 38% 19.42 98% 753 8% 4.50 75% 113 39% 16.85 -0.20 98% 9% 379 trades 51% 17.78 98% 655 13% 4.55 75% 100 51% 14.97 0.57 98% 9% 329

Table 4 presents the average results of regressions: ,

,

, where are the 10-second mid-price changes (Panel A) or changes in trade prices between trades (Panel B), are the contemporaneous order flow imbalances and are the contemporaneous trade imbalances. For Panel A, these regressions were estimated using 273 half-hour subsamples (indexed by ) for each stock and their outputs were averaged across subsamples. Each subsample typically contains about 180 observations (indexed by ). For Panel B, data was pooled across half-hour subsamples, resulting in 13 subsamples for each stock. The t-statistics were computed using White’s standard errors. For each of three regressions, Table 4 reports the average , the average t-statistic of the coefficient(s), the percentage of samples where the coefficient(s) passed the z-test at the 5% significance level and the F-statistic of the regression. The outputs for Panel B were averaged across stocks.

As a robustness check, we repeated regressions (8a-8c) with differences between transaction prices instead of differences in mid-prices . This time price differences were computed in trade time as for trades. The average results across five stocks, picked at random555The stocks tickers were BDX, CB, MHS, PHM and PKI. We computed price changes for trades to mitigate the possible issues with trade and quote alignment in the TAQ data and we correspondingly computed order flow imbalances and trade imbalances during the time intervals between 2, 5 or 10 consecutive trades. To ensure that there is an ample amount of data for each regression, we pooled data across days for each stock and each time interval. are presented in Panel B of Table 4. Our findings for transaction prices are essentially the same as for mid prices - explains price changes better than . Moreover, the effect of trades on prices seems to be captured by the order flow imbalance. The variable becomes statistically insignificant when used together with in the regression and the increase in from adding as an extra regressor is not economically significant.

Interestingly, we found that the relation between and is concave in some samples, and similarly for and . We estimated regressions (8a) and (8b) for transaction price changes with additional quadratic terms (respectively, ) and found that they are significant in nearly half of the samples with t-statistics of -2.8 on average (-2.3 for ). Sampling data at special times (trade times) may introduce biases to the right side of the regression. One possible explanation is that traders submit their orders when they expect their impact to be minimal, leading to a concave (sublinear) impact. Supporting this idea of sampling biases, we found that when mid-prices are sampled at trade times, the price impact of is again concave in some samples. On another hand, when we regressed last trade prices sampled at 1-minute frequency on , we observed the concave price impact once again. This suggests that using either trade times or trade prices may lead to non-linear price impact. However the quadratic term in our regressions is insignificant in about half of the samples and marginally significant in the the other half of the data.

4.2 Does volume move the prices?

The relation between price changes and volume is empirically confirmed by many authors (see [27] for a review). Recently, traded volume became an important metric for order execution algorithms - these algorithms often attempt to match a certain percentage of the total traded volume to reduce the price impact. However, it remains unclear whether the traded volume truly determines the magnitude of price moves and whether it is a good metric for price impact. Casting doubt on this assertion, Jones et al. [26] showed that the relation between the daily volatility and the daily volume is essentially due to the number of trades and not the volume per se (also see [Chan2000] for the discussion).

We extend this result in two ways. First, we show that even when prices are driven by order flow imbalance, an apparent (concave) dependence on traded volume may emerge as an artifact due to data aggregation. Second, we empirically confirm that the price-volume relation is an indirect one - it becomes statistically insignificant after accounting for the order flow imbalance.

The volume traded during a time interval is:

where is the size of any trade (either buy or sell) if it occurs at the -th quote or zero otherwise. Comparing this definition with the definition of we note that both quantities are sums of random variables. As the aggregation window becomes progressively larger, the behavior of these sums (under certain assumptions) will be governed by the Law of Large Numbers and the Central Limit Theorem. We consider a time interval and denote by the number of order book events during that time interval. We also denote by and , respectively, the order flow imbalance and the traded volume during . The following proposition shows a link between and as grows.

Proposition 1.

Assume that

-

1.

Order book events accumulate over time at some average rate :

-

2.

are i.i.d. random variables with a finite variance ,

-

3.

are i.i.d. random variables with a finite mean , where is the proportion of order book events that correspond to trades and is the mean trade size.

| (9) |

where is a standard normal random variable and denotes convergence in distribution.

Proof: First, we apply the law of large numbers to the traded volume. Assumption (1) ensures that as :

| (10) |

Second, event contributions have a finite variance and, under our assumptions, we can apply the classical central limit theorem to the order flow imbalance:

| (11) |

where is a standard normal random variable. Although the denominator is random, it goes to infinity by assumption (1) and Anscombe’s lemma ensures that we can use such a normalization in the central limit theorem [13, Lemma 2.5.8]. Since the square root function is continuous, the convergence in (10) takes place almost-surely and the limit in (10) is deterministic, we can combine (10) and (11) in the following way:

| (12) |

If the time interval includes a large enough number of order book events and trades, the above limit argument implies a noisy scaling relation between order flow imbalance and the square root of traded volume:

| (13) |

where and are constants and . Now, assume that it holds not just for the first interval, but for every time interval of large enough length , regardless of its index . Then, (13) can be substituted into our model (2), to yield:

| (14) |

where is a slope coefficient and is a noise term due to scaling. Due to the scaling approximation, the slope in (14) is a random normal variable: . For every time interval the ratio is a different draw from the distribution, leading to a different in each case. This additional randomness makes this model considerably less robust than (2) and we do not recommend to use it.

Equation (14) shows that even if prices are driven by the order flow imbalance (i.e. even if ), there will be a noisy square-root relation between the price changes and the traded volume. However, if the assumptions of Proposition 1 do not hold (e.g. are strongly dependent or have infinite variance), the price-volume relation may have a different exponent. A variety of exponents have been observed in the relation between prices changes and trade sizes [8], suggesting the following model:

| (15) |

To estimate the exponent , we put and in (15) and fit a logarithmic regression to every half-hour subsample, indexed by :

| (16) |

Based on Proposition 1, we expect the price-volume relation to be indirect (i.e. come through ) and noisy. To empirically confirm this, we compare the following three regressions:

| (17a) | |||

| (17b) | |||

| (17c) | |||

These regressions are estimated for every half-hour subsample with the exponents pre-estimated by (16). The averages of and their standard deviation for each stock are presented on the left panel in Table 5. The exponent varies considerably across stocks and time, but is generally below 1/2 in our data. The average results of regressions (17a-17c) for each stock are presented on the middle and right panels. We observe that explains the magnitude of price moves better than . Although both variables appear to be statistically significant when taken individually, only remains significant in the multiple regression. Thus, the dependence between the magnitude of price moves and the traded volume is mostly due to correlation between and . Interestingly, the number of trades variable (suggested in [26]) is also statistically significant on a stand-alone basis, but becomes insignificant when added to (17c) as a third variable.

5 Conclusion

We have introduced order flow imbalance, a variable that cumulates the sizes of order book events, treating the contributions of market, limit and cancel orders equally, and provided empirical and theoretical evidence for a linear relation between high-frequency price changes and order flow imbalance for individual stocks. We have shown that this linear model is robust across stocks and the impact coefficient is inversely proportional to market depth. These relations suggest that prices respond to changes in the supply and demand for shares at the best quotes, and that the impact coefficient fluctuates with the amount of liquidity provision, or depth, in the market. Moreover, we have demonstrated that order flow imbalance is a stronger driver of high-frequency price changes than standard measures of trade imbalance. Trades seem to carry little to no information about price changes after the simultaneous order flow imbalance is taken into account. If trades do not help to explain price changes after controlling for the order flow imbalance, it is highly possible that the relation between price changes and traded volume simply capture the noisy scaling relation between these variables.

Overall, these findings seem to give an intuitive picture of the price impact of order book events, which is somewhat simpler than the one conveyed by previous studies.

Table 5. Comparison of traded volume and order flow imbalance. Ticker Avg Stdev Order flow imbalance Traded volume Both covariates AMD 0.06 0.08 63% 10.3 99% 356 14% 4.5 83% 34 63% 9.4 1.1 99% 35% 182 APOL 0.24 0.08 53% 8.3 90% 258 25% 6.8 99% 63 57% 6.9 2.9 89% 84% 144 AXP 0.16 0.08 55% 10.5 100% 249 20% 6.6 100% 48 57% 9.0 2.8 100% 81% 133 AZO 0.43 0.22 39% 5.5 96% 131 32% 5.3 100% 93 50% 4.3 3.6 94% 96% 98 BAC 0.09 0.08 73% 16.3 100% 560 24% 5.6 83% 61 74% 13.9 1.2 96% 35% 285 BDX 0.26 0.10 55% 8.4 99% 261 27% 6.3 100% 71 58% 6.7 2.9 98% 84% 147 BK 0.11 0.07 68% 13.1 100% 437 19% 6.6 97% 46 68% 11.5 2.0 99% 58% 225 BSX -0.17 2.41 68% 8.4 100% 486 14% 3.3 95% 33 69% 8.0 0.1 97% 12% 246 BTU 0.24 0.07 58% 10.5 99% 283 23% 6.8 99% 57 60% 8.9 2.4 99% 78% 151 CAT 0.22 0.07 56% 10.4 98% 250 19% 6.0 98% 44 57% 8.9 2.1 98% 63% 131 CB 0.19 0.09 56% 10.1 99% 261 23% 6.4 99% 58 58% 8.2 2.6 99% 74% 141 CCL 0.14 0.07 60% 11.3 100% 309 19% 6.6 99% 45 62% 9.9 2.4 99% 74% 162 CINF 0.13 0.12 67% 10.6 99% 505 30% 6.1 98% 85 69% 8.7 2.0 99% 55% 268 CME 0.49 0.24 28% 4.1 94% 78 30% 4.8 99% 83 42% 3.2 3.6 86% 94% 71 COH 0.19 0.07 60% 10.4 99% 299 22% 6.5 99% 52 61% 8.9 2.2 98% 69% 157 COP 0.16 0.07 56% 9.8 100% 277 20% 6.0 96% 49 58% 8.4 2.4 100% 70% 145 CVH 0.18 0.10 62% 10.2 100% 352 27% 5.9 99% 72 64% 8.2 2.2 100% 70% 189 DNR 0.08 0.07 64% 12.0 99% 376 17% 6.3 95% 38 65% 10.7 1.8 99% 55% 193 DVN 0.26 0.07 52% 8.6 93% 236 24% 6.7 100% 59 55% 7.1 2.9 91% 81% 131 EFX 0.20 0.11 52% 8.1 99% 241 26% 5.4 99% 69 56% 6.4 2.7 97% 75% 137 ETN 0.26 0.10 55% 8.2 97% 252 27% 6.4 99% 70 58% 6.8 2.9 96% 83% 142 FISV 0.19 0.11 57% 9.1 100% 284 25% 5.9 100% 65 59% 7.3 2.2 99% 66% 153 HAS 0.20 0.09 61% 10.1 100% 328 26% 6.2 100% 67 63% 8.2 2.3 100% 73% 175 HCP 0.14 0.07 57% 11.1 100% 268 21% 7.0 99% 50 59% 9.3 2.7 100% 79% 143 HOT 0.23 0.08 57% 9.7 98% 263 24% 6.9 100% 60 60% 8.2 3.0 98% 85% 145 KSS 0.24 0.08 60% 10.8 97% 318 25% 6.6 99% 61 62% 9.0 2.4 97% 74% 169 LLL 0.33 0.12 58% 9.4 94% 323 34% 6.9 100% 101 63% 7.1 3.0 91% 86% 188 LMT 0.28 0.09 61% 10.7 99% 327 31% 7.3 100% 85 64% 8.4 2.9 99% 84% 182 M 0.11 0.07 69% 13.9 100% 463 20% 6.3 99% 46 69% 12.2 2.0 100% 60% 238 MAR 0.15 0.07 61% 12.3 100% 324 21% 6.9 99% 50 62% 10.4 2.4 100% 71% 170 MFE 0.16 0.09 60% 10.9 99% 318 24% 7.1 98% 62 62% 8.8 2.5 99% 71% 170 MHP 0.20 0.10 62% 10.2 99% 377 25% 5.9 99% 62 64% 8.5 1.9 99% 55% 199 MHS 0.23 0.08 56% 9.2 99% 258 24% 6.6 100% 58 58% 7.7 2.6 98% 77% 139 MRK 0.10 0.07 62% 11.0 100% 330 17% 5.4 99% 40 63% 9.8 1.8 100% 55% 170 MRO 0.09 0.06 61% 11.8 100% 333 16% 6.3 95% 36 63% 10.6 2.0 100% 54% 172 MWV 0.18 0.10 62% 10.3 100% 330 28% 6.7 100% 75 64% 8.2 2.4 100% 74% 180 NEM 0.20 0.07 56% 9.9 99% 253 20% 6.1 99% 47 58% 8.6 2.5 99% 75% 135 OMC 0.15 0.09 57% 10.1 99% 286 20% 6.4 98% 48 59% 8.6 2.4 98% 73% 151 PCS 0.11 0.18 62% 7.1 96% 411 18% 3.7 97% 54 63% 6.5 0.7 93% 20% 214 PHM 0.07 0.08 64% 10.2 100% 384 15% 5.5 90% 34 65% 9.4 1.2 99% 40% 195 PKI 0.11 0.11 55% 7.8 99% 266 20% 4.8 97% 47 57% 6.7 1.8 98% 53% 141 R 0.27 0.11 56% 8.6 98% 259 28% 6.0 100% 74 59% 6.9 2.9 97% 85% 147 RAI 0.25 0.10 61% 9.2 99% 334 28% 5.7 100% 73 63% 7.6 2.4 99% 71% 182 SLB 0.24 0.07 62% 12.0 99% 330 19% 5.5 98% 46 63% 10.6 1.7 99% 51% 171 TE 0.09 1.69 60% 8.0 98% 371 18% 4.4 85% 48 61% 7.2 1.3 98% 39% 196 TWC 0.25 0.10 55% 9.7 99% 253 27% 6.6 100% 73 58% 7.6 3.0 99% 81% 142 WHR 0.34 0.11 56% 8.2 97% 272 29% 6.3 100% 78 59% 6.6 2.9 95% 86% 156 WIN 0.06 0.26 48% 3.9 79% 340 10% 2.8 50% 34 49% 3.7 0.6 79% 29% 179 WPI 0.22 0.10 61% 9.6 98% 361 28% 5.8 100% 75 64% 7.7 2.2 98% 71% 196 XTO 0.08 0.06 53% 10.9 100% 238 15% 6.5 100% 32 55% 9.6 2.7 100% 78% 125 Grand mean 0.18 0.18 58% 9.8 98% 313 23% 6.0 97% 58 61% 8.3 2.3 97% 67% 168

Table 5 presents the average results of regressions: ,

,

, where are the 10-second mid-price changes, are the contemporaneous order flow imbalances and are the contemporaneous trade volumes. The exponents were estimated in each subsample beforehand using a logarithmic regression: . These regressions were estimated using 273 half-hour subsamples (indexed by ) for each stock and their outputs were averaged across subsamples. Each subsample typically contains about 180 observations (indexed by ). The t-statistics were computed using White’s standard errors. For each of three regressions, Table 5 reports the average , the average t-statistic of the coefficient(s), the percentage of samples where the coefficient(s) passed the z-sest at the 5% significance level and the F-statistic of the regression.

References

- [1] H. Ahn, K. Bae, and K. Chan, Limit orders, depth, and volatility: evidence from the stock exchange of Hong Kong, Journal of Finance, 56 (2001), pp. 767–788.

- [2] R. Almgren and N. Chriss, Optimal execution of portfolio transactions, Journal of Risk, 3 (2000), pp. 5–39.

- [3] R. Almgren, C. Thum, E. Hauptmann, and H. Li, Direct estimation of equity market impact, Journal of Risk, 18 (2005), p. 57.

- [4] T. Andersen and T. Bollerslev, Deutsche mark - dollar volatility: intraday activity patterns, macroeconomic announcements, and longer run dependencies, Journal of Finance, 53 (1998), p. 219.

- [5] M. Avellaneda, S. Stoikov, and J. Reed, Forecasting prices from level-I quotes in the presence of hidden liquidity. Working paper, 2010.

- [6] D. Bertsimas and A. Lo, Optimal control of execution costs, Journal of Financial Markets, 1 (1998), pp. 1–50.

- [7] J.-P. Bouchaud, Encyclopedia of Quantitative Finance, Wiley, 2010, ch. Price Impact.

- [8] J.-P. Bouchaud, D. Farmer, and F. Lillo, Handbook of financial markets: dynamics and evolution, Elsevier: Academic Press, 2009, ch. How markets slowly digest changes in supply and demand.

- [9] J.-P. Bouchaud, Y. Gefen, M. Potters, and M. Wyart, Fluctuations and response in financial markets: the subtle nature of ’random’ price changes, Quantitative Finance, 4 (2004), p. 176.

- [10] T. Chordia, R. Roll, and A. Subrahmanyam, Liquidity and market efficiency, Journal of Financial Economics, 87 (2008), p. 249.

- [11] P. K. Clark, A subordinated stochastic process model with finite variance for speculative price, Econometrica, 41 (1973), pp. 135–155.

- [12] Z. Eisler, J.-P. Bouchaud, and J. Kockelkoren, The price impact of order book events: market orders, limit orders and cancellations, Quantitative Finance Papers 0904.0900, arXiv.org, Apr. 2009.

- [13] P. Embrechts, C. Kluppelberg, and T. Mikosch, Modelling extremal events for insurance and finance, Springer, 1997.

- [14] R. Engle, R. Ferstenberg, and J. Russel, Measuring and modeling execution cost and risk. NYU Working Paper No. FIN-06-044, 2006.

- [15] R. Engle and A. Lunde, Trades and quotes: a bivariate point process, Journal of Financial Econometrics, 1 (2003), pp. 159–188.

- [16] M. Evans and R. Lyons, Order flow and exchange rate dynamics, Journal of Political Economy, 110 (2002), p. 170.

- [17] J. D. Farmer, L. Gillemot, F. Lillo, S. Mike, and A. Sen, What really causes large price changes?, Quantitative Finance, 4 (2004), pp. 383–397.

- [18] X. Gabaix, P. Gopikrishnan, V. Plerou, and H. Stanley, A theory of power-law distributions in financial market fluctuations, Nature, 423 (2003), p. 267.

- [19] J. Gatheral, No-dynamic-arbitrage and market impact, Quantitative Finance, 10 (2010), p. 749.

- [20] J. Hasbrouck, Measuring the information content of stock trades, Journal of Finance, 46 (1991), pp. 179–207.

- [21] , The summary informativeness of stock trades: An econometric analysis, Review of Financial Studies, 4 (1991), p. 571.

- [22] J. Hasbrouck and D. Seppi, Common factors in prices, order flows and liquidity, Journal of Finance and Economics, 59 (2001), p. 383.

- [23] N. Hautsch and R. Huang, The market impact of a limit order. SFB 649 Discussion Papers, 2009.

- [24] C. Hopman, Do supply and demand drive stock prices?, Quantitative Finance, 7 (2007), pp. 37–53.

- [25] G. Huberman and W. Stanzl, Price manipulation and quasi-arbitrage, Econometrica, 72 (2004), pp. 1247–1275.

- [26] C. Jones, G. Kaul, and M. Lipson, Transactions, volume, and volatility, Review of Financial Studies, 7 (1994), pp. 631–651.

- [27] J. Karpoff, The relation between price changes and trading volume: A survey, Journal of Financial and Quantitative Analysis, 22 (1987), p. 109.

- [28] D. Keim and A. Madhavan, The upstairs market for large-block transactions: Analysis and measurement of price effects, Review of Economic Studies, 9 (1996), p. 1.

- [29] A. Kempf and O. Korn, Market depth and order size, Journal of Financial Markets, 2 (1999), p. 29.

- [30] P. Knez and M. Ready, Estimating the profits from trading strategies, Review of Financial Studies, 9 (1996), p. 1121.

- [31] C. Lee, B. Mucklow, and M. Ready, Spreads, depths, and the impact of earnings information: an intraday analysis, Review of Financial Studies, 6 (1993), pp. 345–374.

- [32] C. Lee and M. Ready, Inferring trade direction from intraday data, Journal of Finance, 46 (1991), pp. 733–746.

- [33] A. Madhavan, M. Richardson, and M. Roomans, Why do security prices change? a transaction-level analysis of nyse stocks, Review of Financial Studies, 10 (1997), p. 1035.

- [34] T. McInish and R. Wood, An analysis of intraday patterns in bid/ask spreads for nyse stocks, Journal of Finance, 47 (1992), pp. 753–764.

- [35] A. Obizhaeva and J. Wang, Optimal trading strategy and supply/demand dynamics. NBER Working Papers, No 11444, 2005.

- [36] E. Odders-White, On the occurrence and consequences of inaccurate trade classification, Journal of Financial Markets, 3 (2000), pp. 259–286.

- [37] M. O’Hara, Market Microstructure Theory, Wiley, 1998.

- [38] V. Plerou, P. Gopikrishnan, X. Gabaix, and H. Stanley, Quantifying stock-price response to demand fluctuations, Physical Review E, 66 (2002), p. 027104.

- [39] M. Potters and J. Bouchaud, More statistical properties of order books and price impact, Physica A, 324 (2003), p. 133 140.

- [40] G. Richardson, S. E. Sefcik, and R. Thompson, A test of dividend irrelevance using vol? ume reaction to a change in dividend polic, Journal of Financial Economics, 17 (1986), pp. 313–333.

- [41] C. Stephens, H. Waelbroeck, and A. Mendoza, Relating market impact to aggregate order flow: the role of supply and demand in explaining concavity and order flow dynamics. Working Paper Series, 11 2009.

- [42] E. Theissen, A test of the accuracy of the lee/ready trade classification algorithm, Journal of International Financial Markets, Institutions and Money, 11 (2001), pp. 147–165.

- [43] N. Torre and M. Ferrari, The Market Impact Model, BARRA, 1997.

- [44] P. Weber and B. Rosenow, Order book approach to price impact, Quantitative Finance, 5 (2005), pp. 357–364.

- [45] P. Weber and B. Rosenow, Large stock price changes: volume or liquidity?, Quantitative Finance, 6 (2006), p. 7.

- [46] I. Zovko and J. D. Farmer, The power of patience: A behavioral regularity in limit order placement, Quantitative Finance, 2 (2002), pp. 387–392.

Appendix A Appendix: TAQ data processing

Quotes data were filtered as follows:

-

1.

Timestamp [9:30 am, 4:00 pm].

-

2.

Bid, ask, bid size, ask size are positive.

-

3.

Quote mode

Trades data were filtered as follows:

-

1.

Timestamp [9:30 am, 4:00 pm].

-

2.

Price and size are positive.

-

3.

Correction indicator .

-

4.

Condition

From the filtered quotes data we construct the National Best Bid and Offer (NBBO) quotes. This is done by scanning through the filtered quotes data, while maintaining a matrix with the best quotes for every exchange. When a new entry is read, we check the exchange flag of that entry and update the corresponding row in the exchange matrix. Using this matrix, the NBBO prices are computed at each entry as the highest bid and the lowest ask across all exchanges. The NBBO sizes are simply the sums of all sizes at the NBBO bid and ask across all exchanges.

After the NBBO quotes are computed, we applied a simple quote test to the NBBO quotes and the filtered trades data. This test matches trades with NBBO quotes and computes the direction of matched trades. A trade is matched with a quote, if:

-

1.

Trade is not inside the spread, i.e.

-

(a)

Trade price NBBO ask: in this case the trade is considered to be a buy trade.

-

(b)

Trade price NBBO bid: in this case the trade is considered to be a sell trade.

-

(a)

-

2.

Trade date quote date.

-

3.

Trade timestamp [quote timestamp, quote timestamp + 1 second].

-

4.

If the above conditions allow to match a trade with several quotes, it is matched with the earliest quote.

There are other routines to estimate trade direction, including the tick test and the Lee-Ready rule [32]. Although the latter is used quite frequently, there seems to be no compelling evidence of superiority of either of these heuristics [36, 42]. To test the robustness of our findings to the choice of a trade direction test, we compared our results on a subsample of data, applying alternatively the tick test or the quote test and it led to virtually the same results.

Finally, we removed observations with extremely high bid-ask spreads. To apply this filter coherently across stocks, we computed for each stock the 95-th percentile of its bid-ask spread distribution and removed the 5% of that stock’s quotes with the spreads above that percentile.