Principal Regression Analysis and the index leverage effect

Abstract.

We revisit the index leverage effect, that can be decomposed into a volatility effect and a correlation effect. We investigate the latter using a matrix regression analysis, that we call ‘Principal Regression Analysis’ (PRA) and for which we provide some analytical (using Random Matrix Theory) and numerical benchmarks. We find that downward index trends increase the average correlation between stocks (as measured by the most negative eigenvalue of the conditional correlation matrix), and makes the market mode more uniform. Upward trends, on the other hand, also increase the average correlation between stocks but rotates the corresponding market mode away from uniformity. There are two time scales associated to these effects, a short one on the order of a month (20 trading days), and a longer time scale on the order of a year. We also find indications of a leverage effect for sectorial correlations as well, which reveals itself in the second and third mode of the PRA.

1. Introduction

Among the best known stylized facts of financial markets lies the so-called “leverage effect” [13, 2, 15, 9, 16, 17], a name coined by Black to describe the negative correlation between past price returns and future realized volatilities in stock markets [6]. 111While this effect holds for most markets in developed economies, Tenenbaum et al. [22] report that the situation appears to be different for markets in developing countries. It is indeed well documented that negative price returns induce increased future volatilities, an effect responsible for the observed skew on the implied volatility smile in stock option markets (see e.g. [3, 4, 11]).

However, the association, made by Black, with a true leverage effect (i.e. that when the value of a stock goes down its debt to equity ratio increases, thereby making the company riskier and more volatile), is probably misleading. In particular, the amplitude of the leverage correlation for indices is noticeably stronger than for individual stocks, which even sounds paradoxical when the index return is by definition the average of individual stock returns! The volatility of an index in fact reflects both the volatility of underlying single stocks and the average correlation between these stocks. The increased leverage effect for indices must therefore mean that both these quantities are sensitive to a downward move of the market.

The aim of the present paper is to investigate more specifically this “correlation leverage effect”, and make precise the common lore according to which correlations “jump to one” in crisis periods (see [12, 21, 14, 20] for early studies of the time evolution of the correlations in financial markets). Similar studies have appeared recently. In [1], a careful study of the average correlation between stock returns during contemporaneous upward/downward trends of the market index has confirmed that correlations are indeed stronger when the market goes down [7]. Our analyses confirm and make more precise these results, first by extending them to different markets, and second by devising and exploiting a new tool to investigate conditional correlations, that we call “principal regression analysis” (PRA). The idea here is to regress the instantaneous correlation matrix on the value of the index return (or any other conditioning variable). While the intercept of the regression gives the average correlation matrix, the regression slopes define a second symmetric (but not definite positive) matrix that can be diagonalized, leading to modes (eigenvectors) of sensitivity to the conditioning variable(s). The interpretation of these eigenvectors is particularly transparent when they coincide with those of the correlation matrix itself. The corresponding eigenvalues quantify how the whole correlation structure of stock returns is affected by the conditioning variable. The nice point about the PRA is that Random Matrix Theory (RMT) provides, as for standard PCA, a useful guide to decide whether or not these sensitivity modes are statistically meaningful (for a review on RMT, see [10]). When the conditioning variable is the past values of the index return, the conclusion of PRA is that the dominant mode is the market mode, associated to a negative eigenvalue, indeed corresponding to a correlation leverage effect. We characterize the temporal decay of this effect. Upon separating positive and negative index returns, we furthermore find that the correlation leverage effect is strongly asymmetric: whereas negative returns increase both the volatility of the underlying stocks and the average correlation between stocks, positive returns have weaker influence on these quantities (see Fig. 6 below). We furthermore find indications of a leverage effect for sectorial correlations as well, which reveals itself in the second and third modes of the PRA.

2. Data, notations and definitions

We have considered 6 pools of stocks corresponding to 6 major stock indices: SP500, BE500, Nikkei, FTSE, CAC 40 and DAX. We analyze the daily returns in a time period spanning from to . Stocks are labelled by (where depends on the market), and days by (where ). Time average will be denoted by . The return of stock between the close of day and the close of day is denoted as . We in fact understand as the demeaned return over the whole time period . We define an inverse volatility weighted index return at time as:

| (1) |

where is the average volatility of the stock over the whole time period:

| (2) |

We will further define the average instantaneous stock volatility at time as:

| (3) |

while the average instantaneous correlation between all pairs of stocks is defined as:

| (4) |

The average over time of the above two quantities will be denoted as and .

The squared index return is a rough proxy for the instantaneous index volatility. Using the above definitions and the fact that is large, it is easy to check that:

| (5) |

showing that both the average stock volatility and the average correlation contribute to the index volatility. It is therefore natural to decompose the full index leverage effect in two contributions: one coming from the dependence of the average stock volatility on the past returns of the index, and a second one describing the average correlation. We thus define a full leverage correlation function :

| (6) |

and two partial leverage correlation functions:

| (7) |

All the above leverage correlation functions are normalized to be the regression slope of the corresponding observables on the past value of the index return, for example:

| (8) |

where is some noise. (Remember that by construction, has zero mean.)

In the limit of weak correlations, the two effects are additive and one should find:

| (9) |

eliciting the contribution of the average stock volatility and of the average correlation to the full leverage correlation. The second term is responsible for the enhanced leverage effect for indices compared to single stocks.

3. Index leverage effect: A simple empirical analysis

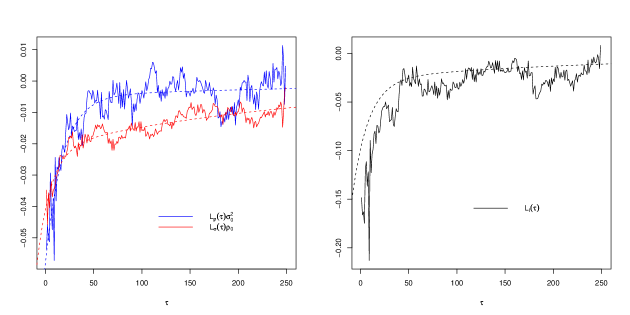

As a first stab at understanding the index leverage effect, we plot in Fig. 1 the normalized partial leverage correlation functions, , , together with the full leverage . In these plots, the data is averaged over the four indices, SP500, BE500, Nikkei and FTSE. From this figure, we draw the following conclusions:

- •

-

•

(b) the correlation effect is stronger at short times but decays faster than the volatility effect; a two time scale exponential fit of these two contributions in the range (in days) indeed leads to

(10) (11) - •

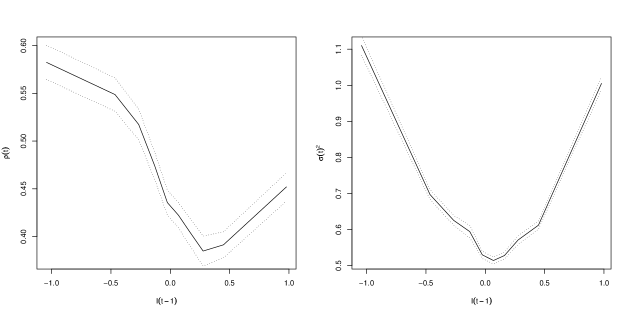

In fact, one can test directly whether linear regressions such as Eq. (8) above make sense or not, by averaging all values of corresponding to a given value of within some range. The resulting graphs are shown in Fig. 2, both for and for . One sees that whereas a linear regression for makes sense for , there is in fact perhaps a small positive slope for . For , the graph looks even more symmetric, reflecting the presence of volatility correlations on top of (assymetric) leverage correlations.

4. A more precise tool: The “Principal Regression Analysis”

The above analysis, although interesting, is oversimplified, because the structure of inter-stock correlations is described by a full correlation matrix and not by a single number , that only captures the average correlations. In order to characterize the way the correlation matrix depends on the past value of the index (or on any other conditioning variable), we propose the following: consider a given pair of stocks, , and regress the product of normalized returns on the past value of the index return, i.e. write:

| (12) |

Since has zero mean, the intercept of the regression is exactly the empirical Pearson estimate of the correlation matrix. The regression slopes define another symmetric matrix , which encodes the full information about the dependence of the correlations on past returns. More precisely, the regression leads to the following empirical determination of :

| (13) |

The aim of this section is first to discuss the information contained in , in particular its eigenvalues and eigenvectors, and second to use results from Random Matrix Theory to assess how meaningful this information is when the length of the sample, , is not very large compared to the number of stocks . Finally, we describe our empirical results on , in particular its most negative eigenvalue and eigenvectors.

4.1. Interpretation

Define to be the correlation matrix conditioned to a certain past value of , by:

| (14) |

The interpretation of the matrix is particularly simple when it commutes with the correlation matrix , i.e. when the eigenvectors of are the same as those of . In this case, the eigenvectors of are exactly the same as those of , whereas the eigenvalues are shifted as:222Note that the dependence on the lag is implied in the following formulas.

| (15) |

where are the eigenvalues of and are the associated eigenvectors (in quantum mechanics notations). When does not commute with , the structure of the eigenvectors themselves is impacted by the conditioning variable. If is small enough, standard first order perturbation theory gives back Eq. (15) for the eigenvalues and:

| (16) |

for the eigenvectors of the matrix .

As we will find below, the eigenvector corresponding to the most negative eigenvalue of turns out to be very close to the first eigenvector of (i.e. the so-called market mode, ), whereas all other eigenvalues are significantly smaller. In this case, the top eigenvalue of is to a good approximation given by:

| (17) |

where is the most negative eigenvalue of . Since can be used to define the average correlation between stocks through , the meaning of is similar to, but more precise than, the correlation leverage function defined above.

More generally, when and do not commute, one expects the “correlation leverage” to rotate the top eigenvector away from the market mode . The common lore is indeed that when markets go down, all stocks “move together”, meaning that the top eigenvector should rotate towards the uniform vector . The cosine of the angle between and is given by the scalar product , that one can compute using perturbation theory. Eq. (16) above. Assuming further that the top eigenvalue of is much larger than all the others (), one finds:

| (18) |

A measure of how strongly the top eigenvector moves towards is therefore provided by the quantity , defined as:

| (19) |

A negative means that the instantaneous market mode is closer to the uniform mode when the index goes down, since .

4.2. Results from Random Matrix Theory

When is large, the simultaneous determination – using Eq. (13) above – of the different elements of from the data points is problematic, exactly in the same way the correlation matrix is hard to measure. We thus need to provide a benchmark to compare the empirical results obtained with the noise level of the benchmark case. This will enable to separate significant effect from noise level arising from the dimensionality problem. Let be a random variable which will play the role of the conditioning variable (the past values of index returns in our context) and let be a gaussian vector of covariance matrix which should be seen as instantaneous stock returns. The will be supposed to have mean and unit variance, so that is the correlation matrix of the gaussian vector .

We begin by the case . Suppose, in addition, that there is no correlations whatsoever between the conditioning variable and the correlation , and that one forms a matrix from:

| (20) |

In the limit for finite one should find that all the elements of the matrix are zero, and therefore all its eigenvalues are zero as well. For finite , however, the matrix will have a set of non trivial eigenvalues. Random Matrix Theory offers a way to compute the statistics of these eigenvalues when and are both large, with a fixed ratio . The result depends both on the eigenvalue spectrum of the matrix and, perhaps surprisingly, on the probability distribution of the conditionning variable, . The simplest, albeit unrealistic case for applications in finance, is when is the identity matrix, i.e. there is no correlations between the . In this case, using the theory of Free Random Matrices [23], one finds that the empirical eigenvalue spectrum of , , is the solution of the following set of equations, in the limit where goes to zero: [10, 5]

| (21) | |||||

| (22) |

where is the real part of the resolvent. One can check that in the limit , and using the fact that has zero mean, the above equations boil down to:

| (23) |

i.e. all eigenvalues are zero, as they indeed should when .

The case of an arbitrary correlation matrix can also be solved completely using the above result on and the so-called -transform of the eigenvalue spectrum [23], noting that the eigenvalues of are the same as those of the product , where is a random matrix with eigenvalue spectrum . The resulting equation can in principle be solved numerically for any value of and for an arbitrary correlation matrix . The resulting theoretical eigenvalue spectrum for the matrix , assuming no correlation between the conditioning variable and the instantaneous correlation , can be compared to the empirical spectrum obtained from data using Eq. (13). Any difference between the two spectra can be interpreted as resulting from a true correlation with the conditioning variable.

In the null-hypothesis case, it is also clear that the quantity defined by:

| (24) |

must be zero when averaged over . One can compute its variance, which is found to be:

| (25) |

For large , the central limit theorem ensures that becomes Gaussian with the above variance. This result will be used below to assess whether the empirical value of (defined above) is meaningful or not.

4.3. Numerical simulations

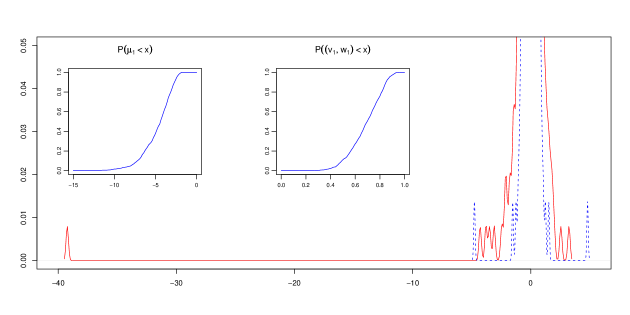

In practice, however, we found it more convenient to use direct numerical simulations rather than the above exact results. In principle, these results below could be obtained using the mathematical formalism above, but the effort required to solve numerically the equations above is larger than the one needed to make direct simulations. We measure the null-hypothesis spectrum of by choosing to be a Gaussian random variable of zero mean and unit variance, completely independent of the true returns , which we then diagonalize. The cumulative distribution of the largest negative eigenvalue in the null-hypothesis is shown in the inset. The average position of the most negative eigenvalue of in the null-hypothesis case is found to be . The average position of the second and third most negative eigenvalues in the null-hypothesis case will be denoted by and .

We have also measured the distribution of the scalar product between the corresponding top eigenvector and the top eigenvector of , . We find that even in the case where is an independent random variable, the top eigenvector of is in fact strongly correlated with , with an average scalar product equal to for the correlation matrix of the returns of the BE500 index. We find numerically that and for the BE500 index – see Fig. 3. Results for the SP500 are very similar.

4.4. Comparison with empirical data

In order to reduce the measurement noise and compare with the above numerical simulations, we have estimated using Eq. (13) with “Gaussianized” empirical index returns, obtained by first ranking the true index return from most negative to most positive, defining the rank of day , . The Gaussianized index return is then obtained as , where is the error function.

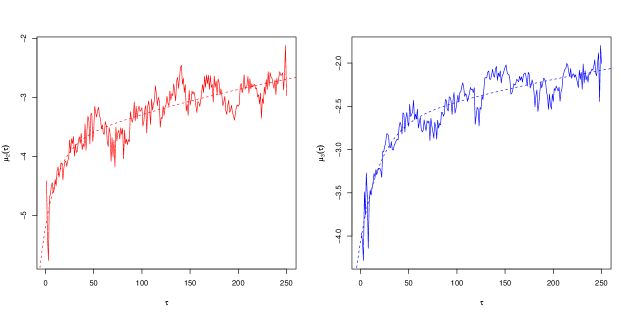

We show in Fig. 4 the evolution of , the largest (in absolute value) eigenvalue of as a function of . We find that is negative, corresponding to the correlation leverage effect (see Eq. (17)). Comparing with the null-hypothesis case, we find that remains significant at the confidence level up to . When fitting with an exponential function with two scales that saturates at the noise level determined above, we find . This reveals two time scales; a rather short one close to the one determined directly from above (see Fig. 1), and a much longer time scale on the order of a year, showing that the effect of market drops on the correlation is long lasting. The scalar product between the top eigenvectors of and globally exceeds in the whole range , whereas the null-hypothesis average value is .

We have also studied the second () and third () eigenvalues of as a function of , which are both negative and clearly beyond the noise level, and are found to decay with very similar time scales: a month and a year (see Fig. 5). The corresponding eigenvectors are found to be mostly within the subspace spanned by the second and third eigenvectors of . The financial interpretation of these eigenvalues is of an increased sectorial correlation when the market drops on top of an increase of the market correlations. Therefore, all idiosyncratic effects disappear upon market drops, while global factors become dominant.

4.5. Separating negative & positive returns

As Fig. 2 explicitely shows, the correlation depends on past index returns in a non-linear way. In fact, both negative and positive returns increase the correlations, although the effect is stronger for negative returns, which in turn leads to a non-zero linear term in the regression of on . A way to capture the parabolic shape seen in Fig. 2 would be to extend the above model to:

| (26) |

defining a new matrix that captures the symmetric effect of index returns on the correlation matrix. An alternative choice, that we adopt below, is to regress separately on negative returns and on positive returns:

| (27) | ||||

| (28) |

where and is the Dirac function. With this definition, one can rewrite the correlation matrix conditioned to a certain past value of more precisely, separating the effect of positive returns and negative returns, as follows:

| (29) |

Again, in order to reduce the measurement noise, we used “Gaussianized” empirical index returns instead of . We apply to the same analysis as above. As anticipated, the top eigenvalue of is strongly negative, whereas the top eigenvalue of is positive, but with — see Fig. 6. The projections of and onto are both very close to unity for small and gradually decay to the noise level as increases. To check the significancy of our effect, as before, we define a null-hypothesis case, introducing the matrix:

| (30) |

where the conditioning variables is independent of the (which are standard gaussian variables whose correlation matrix is as above) and distributed as where is as before a standard gaussian variable. We define further the matrix exactly as except for the fact that the conditioning variable is now distributed as . As above, will be the average positions of the first, second and third most negative eigenvalues of and will be the average positions of the first, second and third most positive eigenvalues of . Those values are all computed using numerical simulations.

We have also studied the rotation parameter for both matrices defined as:

| (31) |

The results are shown in Fig. 7. In agreement with the common lore, is negative, indicating that strongly negative index returns (below ) lead to a more uniform instantaneous market mode. On the other hand, is found to be negative as well, meaning that while strongly positive returns also tend to increase the average correlation between stocks, the instantaneous market mode rotates away from the uniform vector . The effects we are reporting are statistically significant since the root-mean square error on (defined as in Eq.(24)) in the null-hypothesis case is found to be , a factor 3 to 4 smaller than the amplitude of the empirical values of .

5. Summary & Conclusion

The aim of this paper was to revisit the index leverage effect, that can be decomposed into a volatility effect and a correlation effect. We investigated the latter in great detail using a matrix regression analysis, that we called ‘Principal Regression Analysis’ (PRA) and for which we have provided, using Random Matrix Theory and simulations, some analytical and numerical benchmarks.

Using this refined analysis, we confirm that downward index trends increase the average correlation between stocks (as measured by the top eigenvalue of the conditional correlation matrix), which in turn explains why the index leverage effect is stronger than for single stocks. Compared to the null-hypothesis benchmark, this leverage correlation effect is highly significant (see Fig. 4 and Fig. 6). We also find that large downward trends implies a more uniform future market mode (see Fig. 7, left).

Upward trends, on the other hand, also increase the average correlation between stocks (see Fig. 6, right) but large upward trends rotate the future market mode away from uniformity (see Fig. 7, right). All these effects are characterized by two ‘memory’ time scales: a ‘short’ one on the order of a month and a longer one on the order of a year. The latter long time scale could be related to the fact that the market had long cycles of booms and busts within the studied time series, during which the average correlation went down and up again.

We have also studied the correlation leverage effect on intraday data, and we find (results not shown) that while the top eigenvalue of the 15 minutes correlation matrix is nearly insensitive to the sign of the previous 15 minutes index return, a significant effect emerges when the time scale reaches one hour.

Finally, we have found indications of a leverage effect for sectorial correlations as well, which reveals itself in the second and third modes of the PRA (see Fig. 5). It would be interesting to analyze other conditional correlation matrices using the tools developed in this paper, such as for example leader-lagger effects [19, 8, 18], or the role of other macro variables such as oil, currencies or interest rates.

Acknowledgements We have benefitted from insightful comments and suggestions by Giulio Biroli, Rémy Chicheportiche, Stefano Ciliberti, Marc Potters and Vincent Vargas.

References

- [1] E. Balogh, I. Simonsen, B. Nagy, and Z. Neda. Persistent collective trend in stock markets. ArXiv e-prints, 1005.0378, 2010.

- [2] G. Bekaert and G. Wu. Asymmetric volatility and risk in equity markets. Rev. Fin. Stud., 13:1, 2000.

- [3] L. Bergomi. Smile Dynamics II. Risk, page 67, 2005.

- [4] L. Bergomi. Smile Dynamics III. Risk, page 94, 2008.

- [5] G. Biroli, J.-P. Bouchaud, and M. Potters. The Student ensemble of correlation matrices: eigenvalue spectrum and Kullback-Leibler entropy. Acta Phys. Pol. B, 38:4009, 2007.

- [6] F. Black. Proceedings of the 1976 American Statistical Association, Business and Economical Statistics Section. 1976.

- [7] L. Borland and Y. Hassid. Market panic on different time-scales. ArXiv e-prints,1010.4917, October 2010.

- [8] J.-P. Bouchaud, L. Laloux, M. A. Miceli, and M. Potters. Large dimension forecasting models and random singular value spectra. Eur. Phys. J., 201, 2007.

- [9] J.-P. Bouchaud, A. Matacz, and M. Potters. Leverage Effect in Financial Markets: The Retarded Volatility Model. Physical Review Letters, 87(22):228701–+, November 2001.

- [10] J.-P. Bouchaud and M. Potters. Financial Applications of Random Matrix Theory: a short review. ArXiv e-prints, October 2009.

- [11] S. Ciliberti, J.-P. Bouchaud, and M. Potters. Smile Dynamics: a Theory of the Implied Leverage Effect. Wilmott Journal, 1:87 94, 2009.

- [12] C.B. Erb, C.R. Harvey, and T.E. Viskanta. Forecasting International Equity Correlations. Financial Analysts Journal, 50:32–45, 1994.

- [13] L. Glosten, R. Jagannathan, and D. Runkle. Relationship between the expected value and the volatility of nominal excess return. J. Finance, 48:1779–1801, 1993.

- [14] F. Longin and B. Solnik. Is the correlation in international equity returns constant: 1960-1990. Journal of International Money and Finance, 14:3–26, 1995.

- [15] D. B. Nelson. Conditional Heteroskedasticity in Asset Returns: A New Approach. Econometrica.

- [16] J. Perelló and J. Masoliver. Random diffusion and leverage effect in financial markets. Phys. Rev. E, 67(3):037102–+, March 2003.

- [17] J. Perello, J. Masoliver, and J.-P. Bouchaud. Multiple time scales in volatility and leverage correlations: a stochastic volatility model. Applied Mathematical Finance, 11:27–50, 2004.

- [18] B. Podobnik, D. Wang, D. Horvatic, I. Grosse, and H. E. Stanley. Time-lag cross-correlations in collective phenomena. Europhysics Letters, 90, 2010.

- [19] M. Potters, J.-P. Bouchaud, and L. Laloux. Financial applications of random matrix theory : old laces and new pieces. Acta Phys. Pol. B, 36:27, 2005.

- [20] L. Ramchand and R. Susmel. Volatility and cross-correlation across major stock markets. Journal of Empirical Finance, 5:397–416, 1998.

- [21] B. Solnik, C. Boucrelle, and Y. Le Fur. International Market Correlation and Volatility. Financial Analysts Journal, 52:17–34, 1996.

- [22] J. Tenenbaum, D. Horvatic, S.C. Bajic, B. Pehlivanovic, B. Podobnik, and H.E. Stanley. Comparison between response dynamics in transition economies and developed economies. Physical Review E, 82:397–416, 2010.

- [23] A. Tulino and S. Verdù. Random Matrix Theory and Wireless Communications. Foundations and Trends in Communication and Information Theory, 1:1, 2004.