Juri Hinzlabel=e1]mathj@nus.edu.sg

[Alex Novikovlabel=e2]Alex.Novikov@uts.edu.au

[Department of Mathematics, National University of Singapore,

2 Science Drive, 117543 Singapore.

Department of Mathematical Sciences,

University of Technology Sydney, PO Box 123,

Broadway, NSW 2007, Australia.

(2010; 7 2008; 9 2009)

Abstract

Tackling climate change is at the top of many agendas. In this context,

emission trading schemes

are considered as promising

tools. The regulatory framework for an emission trading scheme introduces a

market for emission allowances and creates

a need for risk management by appropriate financial contracts.

In this work, we address logical principles underlying their valuation.

emission derivatives,

environmental risk,

doi:

10.3150/09-BEJ242

keywords:

††volume: 16††issue: 4

and

1 Introduction

The generic principle of an emission trading scheme is based on the

so-called ‘cap-and-trade’ mechanism.

In this framework, an authority allocates

fully tradable

credits among responsible institutions. At pre-settled compliance dates,

each source must have enough allowances

to cover all of its recorded emissions, or be subject to penalties.

A mandatory cap-and-trade system involves its participants

in a risky business with an obvious need for risk management. That is,

certificate trading

is usually accompanied by a secondary market

for emission-related futures, including a rapidly growing variety of their

derivatives.

Their pricing is addressed in this work.

Our contribution focuses on a methodology between equilibrium and risk-neutral

approaches. Due to the complexity of emissions markets,

risk-neutral dynamics must be addressed in terms of explanatory variables,

viewed as proxies of fundamental quantities.

Thus, we utilize equilibrium analysis to explain the role of

fundamentals in

risk-neutral allowance price formation. Thereby, the key issue is

a feedback relation between allowance prices and abatement activity.

Namely, we demonstrate that

any increase in allowance

price causes market participants to enforce emission saving in order to

sell their allowances. Hence,

an increasing allowance price encourages a supply of certificates and

lowers the probability of non-compliance, which

tends to bring down their prices.

Apparently, the correct description of this feedback is the key to

derivatives pricing.

The present work focuses on this issue. On this account, our contribution

goes beyond any risk-neutral approach to modeling of emission-related

assets suggested in the existing literature to date.

2 Emissions markets

The literature on this subject is enormous: it encompass

hundreds of books and papers.

For this reason, we focus only on those market models which are

relevant in the present approach.

Economic theory of allowance trading can be traced back to [8] and [14],

whose authors proposed a market model for the public environmental goods described by tradable permits.

Dynamic allowance trading is addressed in [7, 22, 16, 11, 17, 21, 13]

and in the literature cited therein.

Empirical evidence from existing markets is discussed in

[9]. This paper suggests economic

implications and hints at several ways to model spot and futures

allowance prices, whose detailed interrelations are investigated in

[23] and

[24].

Econometric modeling is addressed in

[1], where characteristic properties for financial time

series are observed for prices of emission allowances from

the mandatory European Scheme EU ETS. Furthermore, a Markov switch and AR–GARCH

models are suggested. The work [15] also considers

tail behavior and the heteroscedastic dynamics in the returns of

emission allowance prices.

Dynamic price equilibrium and optimal market design are

investigated in

[2]. Based on this approach, [3] discusses the

price formation

for goods whose production is affected by emission regulations. In this

setting, an equilibrium analysis

confirms the existence of the so-called ‘windfall profits’ (see [19]) and provides

quantitative tools to analyze alternative market designs.

Pricing of options was addressed only recently. The paper [6] discusses an endogenous emission

permit price dynamics within equilibrium setting and elaborates on

valuation of European option on emission allowances.

The paper [18] and the dissertation [25] deal with

the the risk-neutral allowance price formation

within EU ETS. Here, utilizing equilibrium properties, the price

evolution is

treated in terms of marginal abatement costs and optimal stochastic control.

Also, the work [5] is devoted to option pricing

within EU ETS.

The authors suppose that the drift of allowance spot prices is related

to a hidden variable

which describes the overall market position in allowance contracts and

they make use of

filtering techniques to derive option price formulas which reflect

specific allowance

banking regulations, valid in the EU ETS. Finally, the recent work

[4] presents an approach

where emission certificate futures are modeled in terms of

deterministic time change applied to a certain class of interval-valued

diffusion processes.

The present work brings aspects of risk-aversion into the line of

research followed in [18, 3]

and [2], which we briefly sketch now. Within a stochastic model of an emissions market, a so-called

central planer problem is introduced and discussed in

[18]. Under additional assumptions, the authors formulate

this problem in terms of continuous-time stochastic

optimization.

Furthermore, they provide economic arguments justifying

why optimal control solutions correspond to an equilibrium of the

emissions market.

Interpreting the allowance certificate price as the marginal abatement

costs, particular explicit solutions

are discussed and yield a dynamic stochastic model for allowance price

evolution.

The work [2] starts from the opposite direction. In

a discrete-time

framework, the Radner equilibrium of an emissions market is introduced

and constructed

via a solution of the central planer problem.

The work [3] yields an extension: in a

slightly different setting,

it is proved that any market equilibrium is reached by this

methodology. Thus, results from [18, 2] and [3] show that a

quantitative analysis of emissions markets is tractable in terms of

stochastic control theory. However, this connection

is valid only if risk aversion is neglected, in other words, under the

assumption that each agent possesses a linear utility function.

Losing sight of risk aversion comes at the costs of

unrealistic results. Among other singularities, it turns out that the

equilibrium allowance price follows

a martingale (with respect to objective measure!) with the consequence

that allowance trading can be

arbitrary, only the final position must be adjusted accordingly.

This work resolves all of these problems. Starting from the

no-arbitrage property which is satisfied in an equilibrium of a

market with risk-averse players,

we show that the risk-neutral allowance price dynamics exhibits the

above feedback property,

which we formalize as a fixed point equation, discussing its solution.

We show that for such a risk-averse setting, our fixed point equation

plays the same role as

the central planer optimal control problem for the non-risk-averse

situation. Namely, it provides a

methodology to describe the market equilibrium in terms of aggregated quantities.

However, this description is valid only from the viewpoint of the

so-called risk neutral dynamics, not being suitable

for discussing all interesting problems. Still,

derivatives valuation

is naturally addressed in, and can be obtained in, this setting.

3 Mathematical model

Let be a filtered

probability space.

Assume that is deterministic and agree that all processes

considered in this work are

adapted to . Write and

to denote, respectively, conditional expectation and conditional

distribution with respect to .

Consider a market with a finite number of the agents confronted

with emission reduction.

Emission dynamics.

For each agent

, introduce the stochastic process

with the interpretation that

describes the total pollution of the agent which is

emitted within the time

interval

in the case of the so-called ‘business-as-usual’ scenario (where no

abatement measure is applied).

Although each agent is considered as a potential producer, purely

financial institutions

are also covered with this approach by setting emissions to zero, that

is, for .

Abatement.

Consider the opportunity to reduce emissions. Each agent

can decide at any time to reduce its emissions

within by pollutant units.

We suppose that each abatement level is possible, ranging from no

reduction to full reduction.

Hence, we assume that holds for all

.

Abatement costs. We

assume that the cost of abatement is a random function of the reduced

volume. The randomness

is due to uncertainty in prices (of fuel) and is observable at the

corresponding time. Thus, if

the agent decides at time on reduction of

their own emissions by units, then

it causes costs , where given

(1)

Since emission savings cannot exceed the business-as-usual emission,

the abatement activity is feasible if

(2)

Following abatement policy , the agent

accumulates

at the compliance date the total terminal costs

(3)

Abatement volume.

For later use, let us introduce, for each , and ,

the abatement volume as

(4)

which is well defined since, under the assumptions (1),

the minimum of the function on

is attained at the unique point.

The reader may imagine as the total reduction volume which is available within in the

situation

at a price which is less than or equal to (measured in currency

unit per pollutant unit).

A straightforward proof shows that (1) ensures that

(5)

For later use, we

introduce the cumulative abatement volume function

(6)

Obviously, stands for the total abatement in the

market, which is available from

all measures in the situation whose price is less than or

equal to .

Allowance trading.

Suppose that, at any time , credits can be

exchanged between agents by trading at the spot price .

Denote by the change at time in allowance

number held

by agent . That is, given the allowance prices ,

the position changes yield costs

(7)

Penalty payment.

The total pollution of the agent can be expressed as a difference

of the cumulative business-as-usual emission less the entire reduction.

As mentioned above,

a penalty is being paid at maturity for each

unit of pollutant, which is

not covered by allowances.

Considering the total change in the allowance position effected by trading, the

loss of the agent resulting from potential penalty payment is

(8)

where

(9)

Remark 1.

Our stylized scheme deals with stand-alone emission trading mechanisms.

In the real world,

cap-and-trade systems operate on multi-period scales, where unused allowances

can be carried out (banked) into next period. Further period

interconnections may include

a transfer of future allocation from the next into the present period

(borrowing) and,

in the case of non-compliance, a withdrawal of an appropriate number of

credits from the

next period allocation in addition to penalty payment. To complete the complexity,

let us mention that different emissions markets could be interconnected

by acceptance of foreign certificates in the national scheme.

Emission trading in multi-period settings is addressed in, among

others, [4] and

[5]. Mathematically, it reduces to the

specification of a more complex

penalty mechanism than that presented above. For this reason, we have

decided to focus on the stand-alone

allowance market to analyze quantitative methods in the simplest situation

before tackling multi-scale systems (such as the second period of EU ETS).

Recording uncertainty.

In what follows, we also need to take into account uncertainty in the

emission recording.

It is convenient to subtract these recording errors from the initial

allocation. Hence, we

interpret as the credits allocated to the agent less

emissions which

become known with certainty only at time . With this interpretation,

stands

for allowances effectively available for compliance and is modeled by

an -measurable random variable. For later use, let us

agree that

the distribution of

, conditioned on

, possesses almost surely no point masses,

which implies that

(10)

Admissible policies.

Since maximally possible reduction cannot exceed emission, wehave (2).

Let us define the space of feasible trading

and abatement strategies of the

agent by

(11)

Individual wealth.

In view of

(3), (7) and (8), the

revenue of the agent following admissible

policy equals

Risk aversion. To face risk preferences, suppose that attitudes

of the agents are

described by utility functions

which are continuous, strictly increasing and concave.

Consider the utility functional

which is assumed to be defined for each random variable where the

expectation is finite or .

Given allowance price process , the agent

behaves rationally,

maximizing

by an appropriate choice

of their own policy .

Market equilibrium.

Following standard theory, a realistic market state is described by the

so-called equilibrium –

a situation where the allowance price, positions and abatement measures

are such that each agent is satisfied by their own policy and,

at the same time, natural restrictions are fulfilled. In our framework,

an appropriate notion of equilibrium

is given as follows.

Definition 1.

The process

is called an equilibrium allowance price process if, for each

,

there exists

such that is finite

and

[(ii)]

(i)

the cumulative changes in positions are in zero net supply,

that is,

(13)

(ii)

each agent is satisfied by their own policy, in

the sense that

(14)

The existence of emissions market equilibrium is addressed in [2] and [3],

under the assumption of a linear utility function and in a slightly

different setting.

However, although equilibrium modeling in the spirit of these

contributions is appropriate

to investigate important questions of

optimal market design, it

has little to offer to the problem of derivatives valuation.

With the present approach, we intend to establish a reduced-form model

which describes the evolution of emission-related assets

from a risk-neutral perspective.

We obtain a realistic picture

by incorporating three essential assumptions into a risk-neutral model.

These assumptions are shown to be direct consequences of an equilibrium

situation:

[(b)]

(a)

There is no arbitrage since, in equilibrium, any profitable strategy

would immediately be followed by all agents.

This would instantaneously

change prices and exhaust any arbitrage opportunity.

(b)

The allowance trading instantaneously triggers all abatement measures

whose costs are below allowance price. The explanation here is that if

an agent possess a technology

with lower reduction costs than the present allowance price, then it is

optimal for that agent to immediately reduce

pollution and take profit from selling allowances.

(c)

There are only two final outcomes for allowance price. Either the

terminal allowance price drops to zero

or it approaches the penalty level.

The reason is that at maturity, the price must vanish if there is an

excess in allowances, whereas in the

case of their shortage, the price will rise, reaching penalty.

We believe that in reality, an exact coincidence of allowance demand

and supply

occurs with zero probability and can be neglected.

Let us formalize the above assertions (a), (b) and (c).

Proposition 1.

Suppose that is an equilibrium allowance price

and for are the corresponding

equilibrium abatement policies.

[(b)]

(a)

There exists

a measure which is equivalent to such that

follows a -martingale.

The terminal value of the allowance price is given by

(16)

Before we proceed with the proof, let us emphasize that this result can

serve as a starting point for risk-neutral modeling. The above

proposition states that at equilibrium, the allowance price process

follows a martingale with respect to an equivalent measure whose terminal value is

obviously depending on intermediate values through

abatement volume function for

.

The surprising and far-reaching consequence is that, from a

risk-neutral perspective, only cumulative

market quantities are relevant. To see this, define the overall

allowance shortage

(17)

which would appear in the market without any emission penalty.

Further, recall from (4)

and (6) the cumulative abatement functions

to express the risk-neutral certificate price dynamics

in terms of the following feedback equation:

Although individual market attributes and actions of the different

agents seem to be irrelevant in this picture,

the reader should notice that this picture appears only from the

risk-neutral viewpoint. In line with standard aggregation theorems, the

equilibrium market state heavily depends on, and is determined by,

market architecture, rules, risk attitudes

and uncertainty. However, once equilibrium is reached and all arbitrage

opportunities are

exhausted, asset dynamics can be considered under risk-neutral measure.

With respect to this measure, market evolution appears as if it were driven

by cumulative quantities only.

With this in mind, let us formulate the problem of the

reduced-form modeling as

follows:

(18)

Note that this formulation serves as a guideline for martingale modeling

since price-dependent abatement volume can be estimated from

market data,

whereas potential allowance shortage

can be modeled in terms of total allowance allocation and demand

fluctuations on goods whose

production causes the pollution. Finally, we shall emphasize a natural

passage to continuous time.

(19)

{pf*}

Proof of Proposition 1

(a) According to the first fundamental theorem of asset pricing (see

[10]), it suffices to verify that if

is an equilibrium allowance price process, then there is no arbitrage

for allowance trading. Let us follow an

indirect proof, supposing that is an allowance

trading arbitrage, meaning that

(20)

Now, we verify that in the presence of arbitrage, no equilibrium can

exist since each agent can change their own policy

to an improved strategy satisfying

(21)

The improvement is achieved by incorporating arbitrage into their own allowance trading as follows:

with appropriate definitions . Indeed, the

revenue improvement from allowance trading is

which we combine with (20) to see that there is no

optimality since

where the transformed trading strategy is given by

Obviously, is a maximizer to the

original problem

if and only if

, where is a

maximizer to the transformed problem

(23)

The last line in the calculation

(24)

shows that if is a maximizer to (23), then must satisfy

for ,

which proves (15).

(c) This assertion is proved by an argument identical to that given in

[2].

4 Reduced-form modeling

In what follows, we propose a solution to the problem of risk-neutral

allowance price modeling (18).

Below, we prove that under the assumptions given above ((10), in particular, is essential),

the problem (18) possess a solution. Moreover, we

show how to obtain the

martingale .

It turns out that

the martingale closed by plays a crucial role, so

we introduce

For later use, let us also define its increments as

Following the intuition that the equilibrium allowance price should be

uniquely determined by the

present time and the general market situation, we express a candidate

for allowance price as

(25)

with hypothetic functionals

(26)

applied to

(27)

According to (18),

this approach yields an obvious definition for :

(28)

Note that, given functionals (26),

the price process is indeed well defined by recursive

application of (27) and (25):

(29)

(31)

Generated by this recursion, the process

follows a martingale if, for all and almost

all , the following holds:

Indeed, we have

In other words, it is sufficient to ensure that

(32)

In the remainder of this section, we will show

that the functionals (26) are recursively obtained as

the unique solution to (4), starting

with from (28). First, let us prepare an

auxiliary result dealing with the solution to (4)

where no conditional information needs to be considered.

Lemma 1.

Given

(33)

(34)

(35)

suppose that the random variable satisfies

(36)

is continuous.

For each , introduce the function given by

The following assertions then hold:

[(iii)]

(i)

for each , there exists a unique with ;

(ii)

the root of is obtained as a

limit in the standard

bisection method

(38)

started at , ;

(iii)

the mapping , is non-decreasing and continuous.

Proof.

(i) For each , the function

is continuous due to (1) and the continuity (33) of .

Thus, the existence of a root follows from

the intermediate value theorem because of

(39)

The uniqueness of the root is ensured by the strict monotonic increase

of . To verify this, observe that

(35) and (33) imply that

the subtrahend

in (1)

is non-increasing, whereas the minuend is strictly

increasing in .

[

(ii)] The bisection algorithm is properly initialized because of (39).

Standard arguments ensure its convergence to the root.

(iii)

To show the monotonic increase of ,

suppose that . Then (35) ensures that for each ,

giving for all , which

implies that .

Now, let us turn to the continuity.

If , then there exists with

. Due to the strict monotonic increase of

, we obtain .

If is a sequence with

, then according to

(1),

(40)

Hence, there exists such that holds for all .

Thus, we obtain

(41)

Since is arbitrarily small and , due to (i),

this implication shows that is continuous on

each point with

.

A similar argument yields

(42)

Again, since is arbitrary, we obtain the continuity of

on each point with

.

If , then the continuity of on follows by the combination of (41) and (42).

∎

Let us now turn to the conditioned version of Lemma 1. Supposing the

existence of the regular -conditioned distribution

,

the proof reproduces the arguments of the previous lemma with

appropriate notational changes due to

conditioning on

the event . However, a useful insight is that the

approximating points ,

of the bisection algorithm turn out to be dependent on and

in a -measurable

way, which shows that the functional under discussion,

, is also -measurable, being the limit

of the sequence of measurable

functions.

Lemma 2.

Suppose that for ,

(43)

(44)

(45)

(46)

Given a regular version of the -conditioned

distribution , assume that the random variable satisfies

(47)

The following assertions then hold:

[(ii)]

(i)

there exists a unique

-measurable -valued satisfying

(48)

(ii)

the mapping , is non-decreasing and continuous

for all .

Proof.

(i) As in the proof of the Lemma 1, we obtain the

unique root of the function

By the

bisection method,

started at , .

Since

each bisection point is

-measurable, which shows that

for ,

the pointwise limit of

the bisection sequence is also -measurable.

By construction, the equality

holds for all and , whose right-hand

side is nothing but

the right-hand side of ((i)) for each .

(ii) The proof is obtained from (iii) of the previous lemma by replacing

, , and

by ,,

and , respectively, with appropriate

notational adaptations according to the conditioning on .

∎

Finally, we address a solution to (18) in the last

point of the following proposition.

Proposition 2.

Consider

under the model assumption (10) and the cumulative

abatement volume functions

from (6)

under (1) and (4).

[(ii)]

(i)

Given measure , there exist functionals

(49)

which fulfill, for all ,

(50)

(51)

(ii)

There exists a -martingale

which satisfies

(52)

Proof.

(i) In this proof, we repeatedly make use of Lemma 2.

Let us start

with and verify that the assumptions of this

lemma are satisfied. Due to continuity (3) of the

abatement function, we have

(33).

The properties

(45) and (46) hold for , by

definition (50).

To show (2), we utilize the specific form of :

(53)

Note that, due to (10), there are almost surely no

point masses in the distribution of

conditioned on (with respect , since ).

That is, (53) is continuous for each

, as required in (2). Hence, (i)

of Lemma 2 yields the functional

satisfying (51) (with ), as required.

To proceed by induction, we emphasize that (ii)

of Lemma 2 ensures that is non-decreasing and continuous for

all . That is, for the next step, , the

assumption (46)

on is automatically satisfied. Moreover, (2) now follows, due to the continuity of ,

from the pointwise convergence

dominated by , which holds

for each with .

That is, all assumptions of Lemma 2 are also fulfilled

for . Proceeding recursively

for , we obtain with (49), (50) and

(51).

(ii) As suggested by (29)–(31), we define, for all

,

The process generated in this way obeys the

terminal condition (52), in view of

(50).

To show the -martingale

property of ,

we calculate, for ,

for almost

all ,

where the penultimate equality follows from (51).

∎

5 Applications

Let us elaborate on the computational feasibility of our reduced-form modeling.

For illustrative

purposes, we focus on the simplest case of martingales with independent

increments and deterministic abatement functions.

We assume that:

(54)

(55)

Under these assumptions, the randomness enters the allowance price

through the present up-to-day emissions only. More precisely,

(54) ensures that

(56)

Let us verify this assertion.

For , (56) holds, by definition (50).

For , we proceed inductively as follows: by

construction, is the unique solution to

(57)

where, in the last equality, we have utilized the fact that ,

due to the independence (54),

and the fact that does not depend on , by the

the induction assumption.

Obviously, the fixed point from (57) also does not depend on .

For numerical calculation, we rely on the one-dimensional least-squares

Monte Carlo method,

which is applicable in our case of martingales with independent

increments. Although this setting is relatively

restrictive, it covers a sufficiently rich class of martingales. For

instance, important cases

of information shocks leading to allowance price jumps can be easily

addressed under this approach when

is modeled as an

appropriately sampled, centered Poisson process. In this case, fixed

point equations can be

treated analytically. We do not follow this path in favor of numerical methods,

which deserve particular attention due to the complexity of emissions

markets. In particular,

extensions of Monte Carlo methods to the multidimensional setting (see

[20])

seem to be appropriate. A preliminary analysis shows that assuming the

existence of a global Markovian

state process allows independence to be weakened to conditional

independence, which leads to

multidimensional Monte Carlo, in the sense of [20],

since the state process gives additional dimensions.

We now focus on computational aspects.

From (56), it follows that is a

-measurable random variable.

Thus, in the equality (51), the

condition can be replaced by the condition :

(58)

We shall treat this relation as a fixed point equation for the

Borel-measurable function and attempt to obtain a solution

in the limit of iterations

(59)

started at . (Note that, given and , the equation (59)

indeed defines

a Borel function by the factorization of the

-measurable random variable on the right-hand side of

(59).)

For numerical calculation of conditional expectations, we suggest using

the least-squares Monte Carlo method.

To explain the principle of the least-squares

Monte Carlo approach (see [12] and [20])

in more detail, we abstract from the concrete situation (59) and consider

where are -valued and independent with

respect to and is a bounded Borel function on .

Under these assumptions, the function

is obtained as

for -almost all ,

where are image measures of under

and , respectively.

An equivalent condition defining is the orthogonality

(60)

where is a measure which is equivalent to and

stands for a set of functions

which are square-integrable with respect to , whose

linear space is dense in . The idea of the

least-squares Monte Carlo method is to relax,

for computational tractability, the principle (5) to

(61)

with a finite set of basis functions

and an appropriate sample

chosen such that

the combination

of the Dirac measures approximates the distribution

(for instance, being realizations of

independent -distributed random

variables). The solution

to the weakened problem (5) is given in terms of

(62)

as follows:

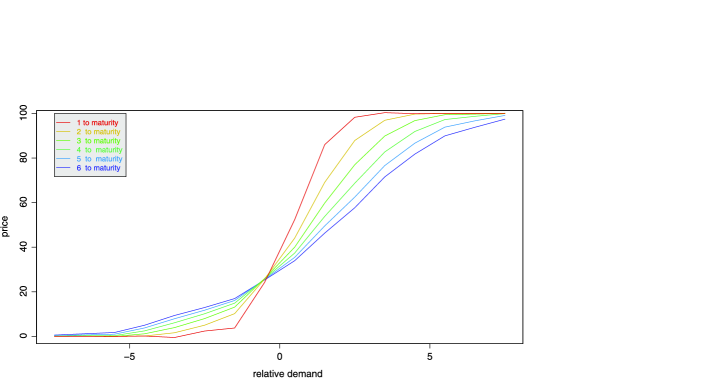

Figure 1: The functions for , from the

least-squares Monte Carlo method.

We now formulate an algorithm for the approximate calculation of (58) in which the conditional

expectation is replaced by the least-squares Monte Carlo projection. To

ease notation, let us suppose

that are identically distributed (in

addition to their independence (54)).

{APMCM*}

1.

Initialization.

Given sample

describing the distribution of

and a set of basis functions on ,

define as in (5).

Set for all and

proceed in the next step with .

2.

Iteration. Define and proceed

in the next step with .

[(2b)]

(2a)

Calculate .

(2b)

Determine a solution to

.

(2c)

Define .

(2d)

If , then

put and continue with step

2a).

If , then set .

If , go to step 2, otherwise finish.

{example*}

To illustrate allowance price calculation via the Monte Carlo method,

we consider the following

numerical example. Suppose that the penalty

is set at

and that the martingale increments

are independent, identically Normally

distributed. Note that by an appropriate choice of the

emission measurement scale, the standard deviation can always be

normalized, thus we have assumed that

each is -distributed. Further,

consider the

basis consisting of piecewise linear hut functions

where the peaks are chosen

to be equidistant with the distance

. For numerical illustration,

we set and . Further, the sample for the Monte Carlo method is generated

with outcomes. For , we followed a natural

choice, taking realizations of

independent -distributed random variables.

However, since

the distribution of is not known in advance, an appropriate

candidate for

seems to be the uniform distribution concentrated on the

interval which is relevant for calculations.

That is, the outcomes are constructed by

equidistant sampling of ,

ranging from to . For

the cumulative volume function , we observed a fast and stable convergence

which gave a reasonable outcome within a few iterations. The resulting

functions are depicted in Figure 1.

Let us outline a valuation procedure for a European call on emission

allowance price.

{VECMCM*}

1.

Given basis functions and a sample

which approximates ,

determine in terms of basis coefficients

using the above

least-squares Monte Carlo

algorithm.

2.

Given maturity time of the European

call, determine its pay-off

.

Calculate least-squares projections, recursively processing for as follows:

[(b)]

(a)

put ;

(b)

obtain as solution to ;

(c)

set ;

(d)

if , then finish, otherwise set and return

to (a).

3.

Given recent allowance price , calculate the state variable

as solution to

.

4.

Plug in the state variable and into function to obtain the price of the European call as

as .

Let us conclude this section by sketching core ideas on continuous-time

modeling.

Our analysis shows that the risk-neutral allowance price evolution

must be described by

a martingale whose

terminal value is digital and depends on the intermediate values (see

(19)).

Suppose that the compliance period

is given by an interval , such that all relevant

random evolutions are described by adapted stochastic processes on

(63)

where represents the spot martingale measure.

Given a random variable and appropriate non-decreasing and

continuous abatement functions

indexed by , we follow

an analogy to discrete time and consider

solutions to

(64)

Our results from the discrete-time setting suggest that if

(65)

then a solution to (64) should be expected in

the functional form

with an appropriate deterministic function

(66)

and a state process given by

To illustrate how such an approach allows one to guess a solution,

assume that

To ensure the martingale property of

,

apply the Itô formula

and claim the function as a solution on to

(68)

with boundary condition

(69)

justified by the

digital terminal allowance price.

Having obtained in this way, we construct the state process

as the solution to the stochastic differential equation

(70)

and then determine

(71)

Finally, this process must be verified in order to solve (64).

6 Conclusion

This article explains the logical principles underlying risk-neutral

modeling of emission certificate

price evolution.

We show that within a

realistic situation of risk-averse market players,

there is no connection between social optimality and market

equilibrium, but there is a

useful feedback relation characterizing

risk-neutral allowance price dynamics.

Expressing this result in terms of fixed point equations on the level

of martingales,

we address the existence of its solution and elaborate on its

algorithmic tractability.

Furthermore, we suggest an extension of these concepts to continuous time

and show that promising results can be obtained using

diffusion processes. Here, emission allowances and their options

can be described in terms of standard partial differential equations.

Although option pricing in this framework seems to be appealing,

we believe that it is not

superior to our Monte Carlo method since the latter can be used in high

dimensions and, more importantly,

in the presence of jumps

in the martingale . This is particularly

important to describe price shocks,

which may result from possible discontinuities in the information flow.

Acknowledgements

The authors would like to thank the referees

for insightful remarks

and comments which helped us to improve this work.

References

[1]

Benz, E. and Trueck, S. (2008).

Modeling the price dynamics of co2 emission allowances.

Energy Economics31 4–15.

[2]

Carmona, R., Fehr, F. and Hinz, J. (2009).

Optimal stochastic control and carbon price formation.

SIAM J. Control Optim.48 2168–2190.

MR2520324

[3]

Carmona, R., Fehr, F., Hinz, J. and Porchet, A. (2010).

Market designs for emissions trading schemes.

SIAM Review. To appear.

[4]

Carmona, R. and Hinz, J. (2009).

Risk neutral modeling of emission allowance prices and option

valuation.

Technical report, Princeton Univ.

[5]

Cetin, U. and Verschuere, M. (2009).

Pricing and hedging in carbon emissions markets.

Int. J. Theor. Appl. Finance12 949–967.

[6]

Chesney, M. and Taschini, L. (2008).

The endogenous price dynamics of the emission allowances: An

application to co2 option pricing.

Technical report.

[7]

Cronshaw, M. and Kruse, J.B. (1996).

Regulated firms in pollution permit markets with banking.

Journal of Regulatory Economics9 179–189.

[8]

Dales, J.H. (1968).

Pollution, Property and Prices. Toronto:

Univ. Toronto Press.

[9]

Daskalakis, G., Psychoyios, D. and Markellos, R.N. (2009).

Modeling co2 emission allowance prices and derivatives: Evidence from

the European Trading Scheme. Journal of Banking and Finance33

1230–1241.

[10]

Kabanov, Y.M. and Stricker, C. (2001).

A teachers’ note on no-arbitrage criteria.

Lecture Notes Math.1775 149–152.

MR1837282

[11]

Leiby, P. and Rubin, J. (2001).

Intertemporal permit trading for the control of greenhouse gas

emissions.

Environmental and Resource Economics19 229–256.

[12]

Longstaff, F. and Schwartz, E. (2001).

Valuing american options by simulation: A simple least-squares

approach.

Review of Financial Studies14 113–147.

[13]

Maeda, A. (2004).

Impact of banking and forward contracts on tradable permit markets.

Environmental Economics and Policy Studies6 81–102.

[14]

Montgomer, W.D. (1972).

Markets in licenses and efficient pollution control programs.

Journal of Econom. Theory5 395–418.

MR0443849

[15]

Paolella, M.S. and Taschini, L. (2008).

An econometric analysis of emissions trading allowances.

Journal of Banking and Finance32 2022–2032.

[16]

Rubin, J. (1996).

A model of intertemporal emission trading, banking and borrowing.

Journal of Environmental Economics and Management31 269–286.

[17]

Schennach, S.M. (2000).

The economics of pollution permit banking in the context of title iv

of the 1990 clean air act amendments.

Journal of Environmental Economics and Management40 189–210.

[18]

Seifert, J. Uhrig-Homburg, M. and Wagner, M. (2008).

Dynamic behavior of co2 spot prices.

Journal of Environmental Economics and Management56

180–194.

[19]

Sijm, J., Neuhoff, K. and Chen, Y. (2006).

Co2 cost pass-through and windfall profits in the power.

Climate Policy6 49–72.

[20]

Stentoft, L. (2004).

Convergence of the least squares monte carlo approach to american

option valuation.

Management Science50 576–611.

[21]

Stevens, B. and Rose, A. (2002).

A dynamic analysis of the marketable permits approach to global

warming policy: A comparison of spatial and temporal flexibility.

Journal of Environmental Economics and Management44

45–69.

[22]

Tietenberg, T. (1985).

Emissions Trading: An Exercise in Reforming Pollution Policy.

Boston: Resources for the Future.

[23]

Uhrig-Homburg, M. and Wagner, M. (2008).

Derivatives instruments in the EU emissions trading scheme, and

early market perspective.

Energy and Environment19 635–655.

[24]

Uhrig-Homburg, M. and Wagner, M. (2009).

Futures price dynamics of cO2 emissions certificates: An empirical

analysis.

Journal of Derivatives17 73–88.

[25]

Wagner, M. (2006).

co2-Emissionszertifikate, Preismodellierung und

Derivatebewertung.

Ph.D. thesis, Universität Karlsruhe.