Predictor-dependent shrinkage for linear regression via partial factor modeling

Abstract

In prediction problems with more predictors than observations, it can sometimes be helpful to use a joint probability model, , rather than a purely conditional model, , where is a scalar response variable and is a vector of predictors. This approach is motivated by the fact that in many situations the marginal predictor distribution can provide useful information about the parameter values governing the conditional regression. However, under very mild misspecification, this marginal distribution can also lead conditional inferences astray. Here, we explore these ideas in the context of linear factor models, to understand how they play out in a familiar setting. The resulting Bayesian model performs well across a wide range of covariance structures, on real and simulated data.

1 Introduction

Consider regressing a scalar response on a vector of predictors , when the number of independent replications, , is much smaller than the number of predictors, . Assume that the goal is to provide reliable predictions along with associated confidence statements. This paper focuses on the following question: assuming that we know the form of the conditional distribution , how should the marginal distribution of the predictors inform our estimates of ?

Within a Bayesian framework one may pass information through a joint sampling model (Liang et al., 2007). In the setting, a parsimonious assumption is that the covariation among the elements of and between and can be captured by a lower dimensional set of latent variables, which we denote by . Generically this may be expressed as

| (1) |

where . This structure describes conditional independence of and , given .

While natural, this approach presents an often overlooked modeling challenge. Because the sampling distribution for is of much higher dimension than the regression model, posterior inference on the latent factors is liable to be overwhelmingly determined by this marginal distribution, essentially ignoring . When is chosen inadequately small, it may be mistakenly inferred that the response is entirely uncorrelated with the predictors. The joint likelihood is dominated by , even if our practical goal is to use to predict . An analogous problem in principal component regression is well known; the least eigenvalue scenario is when the response is associated strongly only with the least important principal component (Hotelling, 1957; Cox, 1968; Jolliffe, 1982).

There are two common tactics for dealing with this problem. The first is simply to use a conditional model. This approach has the virtue of limiting the number of free parameters one must interpret and compute with. It has the drawback that information about must be incorporated into the regression with no accompanying reliability assessment. For example, in singular value regression, one takes the top left singular vectors of the design matrix as the predictors. Such procedures do not propagate uncertainty about this choice of into predictions and confidence regions.

The second approach is to place a prior on , including it in a full Bayesian model, thus allowing inference on . Though this approach inherently propagates uncertainty about , specifying a prior over that respects the goal of prediction within the framework of the joint distribution is nontrivial (see example 2, section 2.2).

To fix ideas, this paper studies the above issues in a Normal linear regression setting, where

| (2) |

As our marginal predictor model we study a Bayesian factor model West (2003),

| (3) |

Without loss of generality we assume throughout that our response and predictor variables are centered at zero.

In the next section, we demonstrate the challenges of prior specification in this setting, in terms of obtaining a satisfactory conditional regression. Rather than tackling this prior specification head on, our solution is to construct a hierarchical model which is centred at the Bayesian factor regression model. Permitting deviations from this model safeguards inference against sensitivity to the choice of the number of factors included in the model, sidestepping the intrinsic sensitivity to prior specification.

Section four compares our method to common alternatives, such as ridge regression, partial least squares, principal component regression (Hastie et al., 2001) and least angle regression (Efron et al., 2004) on real and simulated data. Principal components, partial least squares and least angle regression all explicitly incorporate features of the observed predictor space when making predictions, while ridge regression does not, a distinction which is further discussed in Section 3.2. Section five considers extensions to variable selection and subspace estimation.

2 The effect of on factor model regression

2.1 Bayesian linear factor models

We briefly provide details of a typical Bayesian linear factor model. Any multivariate Normal distribution may be written in factor form as in (3). The matrix is a real-valued matrix and is diagonal. The matrix is referred to as a loadings matrix, the elements of are referred to as idiosyncratic variances, and the are called factor scores. Conditional on and , the elements of each observation are independent. Integrating over , we see

| (4) |

When this form is unrestricted in that any positive definite matrix can be written as (4). We say that a positive definite matrix admits a -factor form if it can be written in factor form where . Note that has full rank whenever the idiosyncratic variances are strictly positive, while , which encodes the covariance structure, may have much lower rank.

If we further assume that the predictors influence the response only through the -dimensional latent variable , we arrive at the Bayesian factor regression model of West (2003):

| (5) |

As the norm of goes to zero, this model recovers singular value regression. Here is a row vector; effectively it is an additional row of the loadings matrix ( and ).

Factor models have been a topic of research for over a century, with increased recent interest spurred by the ready availability of computational implementations. A seminal reference is Spearman (1904); Press (1982) and Bartholomew (1987) are key modern references. Bayesian factor models for continuous data have been developed by many authors, including Geweke and Zhou (1996) and Aguilar and West (2000). A thorough bibliography can be found in (Lopes, 2003). Notable applications include finance (Aguilar and West, 2000; Fama and French, 1993, 1992; Fan et al., 2008; Bai, 2003; Chamberlain, 1983; Chamberlain and Rothschild, 1983; Lopes and Carvalho, 2007) and gene expression studies (Merl et al., 2009; Lucas et al., ; Carvalho et al., 2008). The area continues to see new methodological developments focusing on a variety of issues: prior specification (Ghosh and Dunson, 2009), model selection (Lopes and West, 2004; Bhattacharya and Dunson, 2010) and identification Fruhwirth-Schnatter and Lopes (2009). In this work we highlight the use of factor models for prediction.

2.2 The effects of misspecifying

If is chosen too small, model inferences can be unreliable as a trivial consequence of misspecification. Less appreciated, however, is that minute misspecifications in terms of overall model fit can drastically impair the suitability of the regression induced by the joint model. The following two examples demonstrate that the evidence provided by the data may be indifferent between two factor models which differ only by the presence of one factor, even though the larger model is strongly preferred by some prediction criterion. In the first example this can be observed analytically; the second example demonstrates this effect via simulation.

-

Example

Consider returns on petroleum in the United States and in Europe and assume we are interested in estimating the spread for trading purposes. Let , where and is the price in the U.S. and in Europe, respectively, so that we want to predict . If we consider the correlation matrix, the first principal component will be given by with variance while the second component is with variance where is the correlation between the two prices. For near one, a regression based on only the first principal component will discard all the relevant information, because the second principal component is the one of interest (Forzani, 2006).

We see that the bias incurred by throwing away the second principal component is much bigger than the reduction in variance incurred by its elimination.

In the bivariate case, this discrepancy may seem inconsequential. But with even a moderate number of predictors, deciding whether or not to add an additional factor can be difficult, as the next example illustrates.

-

Example

Consider the 10-dimensional two-factor Gaussian model with loadings matrix

(6) and idiosyncratic variances for all . Now consider the one-factor model that is closest in KL-divergence to this model, with loadings matrix

(7) and idiosyncratic variances given by the vector

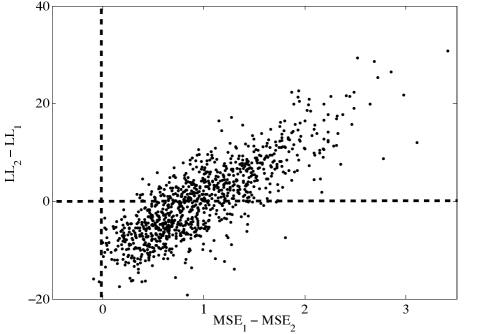

Observe that the one-factor loadings matrix is very nearly equal to the first factor of , but that the idiosyncratic variances are notably different. In particular, consider the problem of using the one-factor approximation to predict future observations of the dimension of , which does not load on the first factor (similar to the first example). The true idiosyncratic variance is , but the approximate model has , suggesting that prediction on this dimension will be inaccurate. However, as measured by the joint likelihood, the one factor model is an excellent approximation. These mismatched conclusions are reflected in the following graph, which plots the difference in mean-squared prediction error between the two models against the difference in log-likelihood; each point represents a realization of 10 observations. Above zero on the vertical axis favors the true model, while below zero favors the one-factor approximation. The horizontal axis represents approximation loss due to the missing factor. The average likelihood ratio is approximately one, while prediction performance is always worse with the smaller model.

Figure 1: Points denote realizations from the true two-factor model. For points above the dashed horizontal line the likelihood ratio favors the true model. The distance to the right of the dashed vertical line measures how much worse than the true model the one-factor approximation did in terms of predicting . Model selection based on the full likelihood favors the larger model half the time, while model selection based on predictive fit favors the larger model nearly always.

More importantly, this discrepancy does not fade as we collect more data. With only 10 observations, the likelihood ratio favors the true model only 47% of the time; with 100 observations this number creeps up to 51% and at 1000 observations it stays at 51%. By the likelihood criterion the two models are virtually identical. However, in terms of predicting , the one-factor approximation is literally useless: the conditional and marginal variances are virtually identical.

Thus we see that relying on a prior distribution to correctly chose between a one- versus two-factor model is a difficult task: the prior would have to be strong enough to overwhelm more than a thousand observations worth of evidence which favors the wrong model about half the time.

It may be instructive for some readers to understand this phenomenon from a matrix decomposition point of view, by defining to be the optimal value of the Frisch problem (Frisch, 1934):

| (8) |

with a fixed covariance matrix and the optimization performed over , the diagonal idiosyncratic variance matrix; denotes positive semi-definite. This rank minimization problem is known to be NP-hard (Vandenberghe and Boyd, 1996); this means, intuitively, that the minimum rank is very sensitive to small changes in . This hardness implies, conversely, that for unknown of fixed rank and unknown , there exist matrices which we may approximate arbitrarily closely as , although .

By contrast, a cross-validation approach would uncover the predictive superiority of the two-factor model directly. While a joint distribution allows one to borrow information from the marginal predictor distribution, which may be useful for prediction, using an unmodified high dimensional joint distribution subjugates the prediction task to the potentially more difficult task of high dimensional model selection. These difficulties persist even with the use of sophisticated nonparametric model selection priors for factor models (Bhattacharya and Dunson, 2010), because the trouble lies not with any particular prior, but rather with the assumption that the latent factors explain all of the variability in both and .

In the next section we surmount the difficulty directly, by relaxing the assumption that the latent factors capturing the predictor covariance are also sufficient for predicting the response. n letting be inferred, if the priors over all of the parameters of the model are not carefully chosen.

3 Partial factor regression

3.1 Specification

Our new model – referred to here as the partial factor model – circumvents the prior specification difficulties described in the previous section by positing a lower-dimensional covariance structure for the predictors, but permitting the relationship between the predictors and the response to be linear in up to dimensions. This is achieved by using the following covariance structure for the joint Normal distribution:

| (9) |

The difference between (5) and (9) is that in (9) is not required to equal . The matrix is still a matrix with so that the predictor covariance matrix is constrained to the form, but, the full covariance matrix is not simultaneously restricted. This way, the response can depend on directions in predictor space which are not dominant directions of variability, but inference and prediction still benefit from this structural regularization of .

Just as crucially, the prior on may be conditioned on . Specifically, we may suggest, via the prior, that higher variance directions in predictor space are more apt to be predictive of the response. But, unlike principal component regression or factor models, the prior furnishes this bias as a hint rather than a rigid assumption; hints are important in settings.

The hierarchical specification arises from the jointly Normal distribution between , , and the latent factors, which have covariance:

| (10) |

From this covariance, the conditional moments of the response can be expressed as:

| (11) | |||||

| (12) |

A natural prior for , conditional on , and might be

implying that a priori the error piece plays no role in the regression. A reasonable choice of independent Normal prior on would be

because the scale of the factors are set to have unit variance. All together, the model may be expressed as

| (13) |

The conditional regression parameters now borrow information from the marginal distribution via the prior – we have centered the regression at the pure factor model. However, the data may steer us away from this assumption. By decoupling the predictor distribution from the conditional distribution, prior specification on the potentially ultra-high dimensional predictor space does not affect our lower dimensional regression in counterproductive ways. At the same time, the hierarchical prior on the regression parameters facilitates the borrowing of information that is necessary in the setting.

3.2 A conditional distribution view

Note that the prior on , marginalizing over , is

| (14) |

Because ,

| (15) |

In other words, the partial factor model is a special case of the following hierarchical model:

| (16) |

where is restricted to have -factor form. Note that conditional on this is simply a conjugate Normal-Inverse-Gamma prior on the regression parameters:

| (17) |

with . This observation permits easy comparison to two other common linear regression priors. Taking the prior covariance matrix to be gives the well-known ridge estimator:

| (18) |

where is the (generalized) least-squares estimator

(where denotes the Moore-Penrose pseudo-inverse (Golub and Van Loan, 1996) of ). Similarly, Zellner’s -prior (Zellner, 1986; Liang et al., 2008) takes yielding the estimator

| (19) |

To appreciate the benefit of using (16), consider the usual rationale behind the ridge regression prior versus that of the -prior . It is straightforward to show that the ridge estimator downweights the contribution of the directions in (observed) predictor space with lower sample variance, from which one may argue that (Hastie et al., 2001):

ridge regression protects against the potentially high variance of gradients estimated in the short directions. The implicit assumption is that the response will tend to vary most in the directions of high variance in the inputs.

The -prior, by contrast, shrinks more in directions of high sample variance in the predictor space a priori, which has the net effect of shrinking the orthogonal directions of the design space equally regardless of whether the directions are long or short. This reflects the substantive belief that higher variance directions in predictor space need not influence the response variable more than the directions of lower variance.

However, this story conflates the observed design space with the pattern of stochastic covariation characterizing the random predictor variable. It would be more desirable to realize the benefit of regularizing estimates in directions of low sample variance, while not over-regularizing regions of predictor space with weak stochastic covariance structure. Teasing apart these two aspects of the problem can be done by conditioning on and separately, exactly as (16) does.

We may observe this teasing-apart effect directly from the form of the estimator under (16). Assuming for simplicity that , and let and . Then

| (20) | |||||

| (21) |

where is chosen a priori and determines the prior mean of the regression coefficients. Because and are never identical, we still get shrinkage in different directions, thus combatting the “high variance of gradients estimated in short directions” while not having to assume that any direction in predictor space is more or less important a priori.

In this light, we see that ridge regression is motivated by a mathematical fact about regularization, while the -prior is motivated by a substantive belief regarding the influence of the predictor variables on the response (namely, symmetry). The partial factor model can be understood as using to learn about and then using this information when trying to learn .

Moreover, Zellner’s -prior may be interpreted as a crude approximation to this idea – rather than as a misguided regularization tool that shrinks the impact of reliably measured covariates more than unreliable ones. The crucial distinction is whether or not the predictors are taken to be fixed or stochastic. For example, Maruyama and George (2010) advocate “more shrinkage on higher variance estimates” and construct a prior on which involves , much like the -prior, but which amplifies the effect of ridge regression in that it results in more shrinkage in observed directions of low sample variance. However, in the case of stochastic predictors, one must distinguish between and , as we have seen in (20). The partial factor model, which centres the conditional regression at a low-dimensional factor model, actually recovers the -prior-esque (16). However, the -factor structure imposed on by the partial factor model provides a much improved estimator of over the naive sample covariance estimate that appears in the -prior.

It is further instructive to consider the case where is given. Here, the difference between (16) and ridge regression amounts to placing an independent prior on the regression coefficients associated with the de-correlated predictors as opposed to those corresponding to the original – possibly correlated – predictors. To see the equivalence, let , where is the Cholesky decomposition of the covariance matrix so that

| (22) |

Then an independent prior on this regression implies

as in (16) above.

This simple observation raises interesting questions about the role of “sparsity” in linear regression models with stochastic predictors. Indeed, believing it plausible that some of the regression coefficients are identically zero is incompatible with the assumption that the same is true of the coefficients in the de-correlated predictor space (for arbitrary covariances).

3.3 Efficient approximation

Sampling from the posterior distribution of the partial factor model may be achieved via standard Markov chain Monte Carlo methods. In particular, a Gibbs sampler for the ordinary factor model provides an excellent proposal distribution for a Metropolis-Hastings update for many of the parameters. This approach provides measures of posterior uncertainty over all parameters, up to Monte Carlo error. This approach is slow, however, owing to the need to compute the determinant of a -dimensional matrix in computing the acceptance ratio. For the purpose of prediction, the following approximation, which we call partial factor regression, proves useful.

Partial factor regression applies ridge regression to an augmented design matrix with elements

| (23) |

mimicking the expression in (11). Two regularization parameters, and , are then selected by cross-validation, corresponding to the respective regression coefficients on the latent factors and the residuals; these are analgous to and in (13) . Point estimates are obtained for as the posterior mean of (3) using a Gibbs sampling implementation. Partial factor ridge regression may be written as

| (24) |

where the expectation in the last line is taken over the posterior derived from model (3).

This approach ignores the impact of on learning these parameters under the partial factor model; however, this contribution should be minor by the arguments of Section two, turning a model flaw in the factor modeling context into a computational shortcut in the partial factor setting. This step of the procedure may be done ahead of time and using as much marginal predictor data as is available, to better estimate . Aside from this preprocessing, the model fitting is exactly ridge regression using the augmented design matrix.

Moreover, this expression of the partial factor idea makes transparent where gains may be achieved over other methods – by decomposing the regularization component into two separate pieces, one concerned with the marginal stochastic structure of the predictors and the other dealing directly with the conditional regression model.

Viewed from this perspective, the partial factor model is an instantiation of the manifold regularization approach of Belkin et al. (2006), but motivated by an underlying generative model; is the “intrinsic” penalty parameter and is an additional “ambient” penalty parameter. The key insight underlying the partial factor model is precisely that these two components may be decoupled, even in the simple venerable linear model.

4 Performance comparisons

4.1 Simulation study

This section considers the improvement the partial factor model can bring over standard Bayesian alternatives: the conjugate linear model with an independent “ridge prior” (with unknown ridge parameter) and the Bayesian factor regression model. We observe via simulation studies that the partial factor model protects against the case where the response loads on a comparatively weak factor. The partial factor model is most frequently the best performing model (modally optimal), and it is also the best model on average (mean optimal) in unfavorable low signal-to-noise regimes and nearly so in the high signal-to-noise case. In summary, the partial factor model predicts nearly as well as the conjugate linear model and factor models when those models perform well, but it does much better than those models in cases where they do poorly. This profile is consistent with results of the multiple-shrinkage principal component regression model of George and Oman (1996), which has a similar motivation – seeking to mimic principal component regression but to protect against the least-eigenvalue scenario – but is not derived from a joint sampling model.

For this simulation study, let and . Of the fifty observations, observations are labeled with a corresponding value. Across 150 data sets, the remaining 15 unlabeled values were predicted using the posterior mean imputed value.

The data was generated according to the following recipe.

-

1.

Draw .

-

2.

Generate a matrix of size with independent standard Normal random variables.

-

3.

Generate a diagonal matrix with elements drawn from a half-Cauchy distribution.

-

4.

Set the true loadings matrix where the norm is the Frobenius norm.

-

5.

The elements of are drawn independently as folded-t random variables with 5 degrees of freedom and scale parameter 0.1.

-

6.

Lastly, was drawn by first drawing a folded-t scale parameter and then drawing a mean zero random variable with corresponding scale.

We consider two scenarios. In the first, the elements of and are ordered so that the highest absolute value of corresponds to the highest absolute value of , the second highest corresponds to the second highest, etc. This is a favorable case for the assumptions of ridge regression and factor models in that the response depends most on the directions of highest variability in predictor space. For the second case the elements of and are arranged in reverse, the smallest absolute value of is associated with the largest absolute value of . In this case the highly informative directions in predictor space are least informative of the response in terms of variation explained.

| Case One. | |||

|---|---|---|---|

| Method | % best | mean relative error | scaled MSE |

| PFR | 36 | .37 | 1.06 |

| NIG | 19 | .48 | 1 |

| BFR | 29 | 7.27 | 1.89 |

| Case Two. | |||

| Method | |||

| PFR | 43 | .27 | 1 |

| NIG | 17 | .45 | 1.04 |

| BFR | 30 | 3.87 | 1.32 |

To compare the average behavior of these methods on a wide range of data we may look at the paired hold out error on each of the sets. We record the frequency that each method was the best performing method, the average relative error (the average of the ratio of the squared error of the method to the minimum squared error over the three methods), and also the overall mean square error. The first measure records how often we should expect a method to be the best method to use on a randomly selected data set, so that higher numbers are better. The second column reflects how far off, on average, a given method performs relative to the best method for a given data set; smaller numbers are better. The final column gives the average error relative to the best overall method; numbers nearer to one are better.

We observe that in the favorable setting the pure factor model is quite often the best model of the four, as shown in the first column. However, we notice also that when it is not the best, it performs, on average, much worse than the best method, as shown in the second column. This is the impact of the bias. Next, we note that while ridge regression moderately outperforms the partial factor model in terms of overall mean squared error, we see that on average partial factor regression is closer to the best performing model. Relatedly, it is the partial factor model that is most often the best model.

In the unfavorable setting, results unambiguously favor the partial factor model. In this setting, as expected, the partial factor model outperforms ridge regression by all three measures. Again, the pure factor model is crippled by its too-strong bias.

4.2 Real data examples

In this section, we extend our comparisons to additional methods and to the case of real data. We compare partial factor regression to four other methods: principal component regression (PCR), partial least squares (PLS), least-angle regression (Efron et al., 2004) (LARS), and ridge regression (RR). We observe the same pattern of robust prediction performance as in the simulation study. Partial factor regression shows itself to be the best or nearly the best among the methods considered in terms of out-of-sample mean squared prediction error.

Five real data sets in the regime are analyzed; the data are available from the R packages pls (Mevik and Wehrens, 2007), chemometrics (Varmuza and Filzmoser, 2009), and mixOmics (Cao et al., 2009).

nutrimouse: the hepatic fatty-acid concentrations of 40 mice are regressed upon the expression of 120 liver cell genes.

cereal: the starch content of 15 cereals is regressed upon 145 different wavelengths of NIR spectra.

yarn: the yarn density of 28 polyethylene terephthalate (PET) yarns is regressed upon 268 wavelenths of NIR spectra.

gasoline: the octane numbers of 60 gasoline samples are regressed upon 401 wavelengths of NIR spectra.

multidrug: an ATP-binding cassette transporter (ABC3A) is regressed upon the the activity of 853 drugs for 60 different human cell lines.

To test the methods, each of the data sets is split into training and test samples, with 75% of the observations used for training. Each model is then fit using the training data, with tuning parameters chosen by ten-fold cross validation on only the training data. Out-of-sample predictive performance on the holdout data is measured by sum of squared prediction error (SSE).

Average out-of-sample error

| Data set | PFR | RR | PLS | LARS | PCR | ||

|---|---|---|---|---|---|---|---|

| nutrimouse | 40 | 100 | 435.0 (4%) | 418.72 | 448.3 (7%) | 502.3 (20%) | 454.2 (8%) |

| cereal | 15 | 120 | 44.4 | 49.5 (11%) | 51.2 (15%) | 69.0 (55%) | 54.3 (22%) |

| yarn | 28 | 145 | 0.16 | 0.47 (194%) | 0.47 (194%) | 0.39 (144%) | 0.58 (263%) |

| gasoline | 60 | 269 | 0.68 | 0.79 (16%) | 0.86 (27%) | 1.04 (52%) | 0.80 (18%) |

| multidrug | 60 | 401 | 167.6 (6%) | 158.8 | 159.9 (1%) | 198.1 (25%) | 167.8 (6%) |

As shown in table 2, the partial factor model outperforms all models on three of the five data sets. In the other two data sets, the nutrimouse and multidrug examples, the factor structure was weak, requiring to account for the variation in the predictor space. In these cases, the extra variance of learning two tuning parameters does not pay dividends and ridge regression narrowly comes out on top. Even so, partial factor regression is never much worse than the best. In cases where the predictor space can be described well by low dimensional (linear) structure, partial factor regression out-performs methods such as principal component regression, which require that this same structure account for all of the variability in the response.

Note that these data were selected because they are publicly available and fall within the regime that is most germane to our comparisons.

5 Variable selection and subspace dimension estimation

5.1 Sparsity priors for variable selection

In this and the next section, it is convenient to work with a reparametrized form of the partial factor model, defining

| (25) |

and using the equivalent independent prior

| (26) |

Note that represents a pure factor model, and that this prior is independent of the other parameters. The revised expression for our (latent) regression becomes

| (27) |

If , predictor appears in the regression of only via its dependence on the latent factors. Further, if we assume that is not identically zero so that has some relation to the latent factors, then we see that if (so that dimension does not load on any of the factors) and , then necessarily. That is, if is not related to any of the latent factors governing the predictor covariance and additionally is not idiosyncratically correlated with via , then does not feature in our regression. The reverse need not hold; the net effect of on can appear insignificant if has a direct effect on the response, but is positively correlated with variables having the opposite effect.

Partial factor regression helps distinguish between these two scenarios, because the framework permits sparsity to be incorporated in each of three separate locations, with the following easy interpretations.

-

1.

Does variable load on latent factor ? ( versus )

-

2.

Does depend on the residual of element ; is important for predicting above and beyond the impact of the latent factors? ( versus )

-

3.

Does depend on latent factor ? ( versus )

This decomposition avoids the unsatisfactory choice of having to decide which of two variables should be in a model if they are very highly correlated with one another and associated with the response. Rather it allows one to consider the common effect of two such variables in the form of a latent factor, and then to consider separately if both or neither should enter into the model residually via the parameter . Earlier work has keyed on to the idea that covariance regularization is useful for variable selection problems (Jeng and Daye, 2010); here these intuitive decompositions follow directly from the generative structure of the partial factor model.

Such a variable selection framework may be implemented with the usual variable selection point-mass priors on , and . Previous work incorporated such priors for the elements of (Carvalho et al., 2008). Alternatively, shrinkage priors may and thresholding may be used to achieve a similar effect.

5.2 Subspace dimension estimation

In the case of multivariate Normal random variables, a factor decomposition of the covariance matrix, in combination with point mass priors as described above, admits a ready characterization of the dimension reduction subspace (Cook, 2007; Cook and Forzani, 2008; Wu et al., 2010) with respect to the response . A dimension reduction subspace is the span of a projection of the predictors which is sufficient to characterize the conditional distribution of the response.

In the factor model setting, we can calculate the dimension of this subspace as follows (Mao et al., 2010). Let denote the nonzero elements of in the partial factor parameterization. Denote by the corresponding columns of and likewise let denote the remaining columns. Then, if , the conditional distribution of given can be characterized purely in terms of

| (28) |

where , showing that enters this distribution only via . Thus, the rank of is the dimension of the reduced subspace, as long as we have a pure factor model. We have already seen, however, that while a covariance matrix may be relatively well approximated by a small number of factors, these factors alone may not span the dimension reduction subspace, so that is estimated to be approximately zero and is biased upward.

Accordingly, we estimate , the posterior probability that the sufficient subspace is less than . Further, by monitoring the number of nonzero elements of in our sampling chain, we can estimate the sufficient dimension, conditional on it being less than . This approach may be thought of as partitioning our prior hypotheses as

| (29) |

The prior probabilities assigned to these hypotheses are induced via priors on and ; grouping many individual hypotheses into the aggregate permits easier control of the contribution of the prior, which can be critical to inference when .

6 Conclusions

In the setting, inference and prediction may sometimes be improved by making structural simplifications to the statistical model. In a Bayesian framework this can be accomplished by positing lower dimensional latent variables which govern the joint distribution between predictors and the response variable. An inherent downside to this approach is that it requires specifying a high dimensional joint sampling distribution and the associated priors. Due to the high dimensionality this task is difficult, particularly with respect to appropriately modulating the implied degree of regularization of any given conditional regression.

The partial factor model addresses this difficulty by reparametrizing the joint sampling model using a compositional representation, allowing the conditional regression to be handled independently of the marginal predictor distribution. Specifically, this formulation of the joint distribution realizes borrowing of information via a hierarchical prior rather than through a fixed structure imposed upon the joint distribution.

Here we have examined the simplified setting of a joint Normal distribution. However, the idea of utilizing a compositional representation in conjunction with a hierarchical prior can be profitably extended to many joint distributions. In particular, one may specify the joint distribution directly, building in borrowing of information by design. For example, the form of the conditional moment for the partial factor model suggests the following nonlinear generalization:

| (30) |

where perhaps and denote smooth functions to be inferred from the data. Here, the smoothness assumptions for and could be different; specifically the prior on could be conditioned on properties of . More generally, the partial factor model is a special case of models of the form:

| (31) | |||||

| (32) |

where generically denotes parameters governing the joint distribution. In the partial factor model and . The conditional model depends on both and , but the presence of in the model leads to a more flexible regression, while the hierarchical prior (32) still borrows information from the predictor variables via .

Such models alleviate the burden of having to get the high dimensional distribution just right in all of its many details. As such, it represents a robust method for fashioning data-driven prior distributions for regression models.

References

- Aguilar and West [2000] O. Aguilar and M. West. Bayesian dynamic factor models and variance matrix discounting for portfolio allocation. Journal of Business and Economic Statistics, 18:338–357, 2000.

- Bai [2003] J. Bai. Inferential theory for factor models of large dimensions. Econometrica, 71:135–171, 2003.

- Bartholomew [1987] D. Bartholomew. Latent variable models and factor analysis. Charles Griffin, 1987.

- Belkin et al. [2006] M. Belkin, P. Niyogi, and V. Sindhwani. Manifold regularization: A geometric framework for learning from labeled and unlabeled examples. Journal Of Machine Learning Research, 7:2399–2434, 2006.

- Bhattacharya and Dunson [2010] A. Bhattacharya and D. B. Dunson. Sparse Bayesian infinite factor models. Biometrika, 2010.

- Cao et al. [2009] K.-A. L. Cao, I. Gonzalez, and S. Dejean. integrOmics: an R package to unravel relationships between two omics data sets. Bioinformatics, 25(21):2855–2856, 2009.

- Carvalho et al. [2008] C. M. Carvalho, J. Lucas, Q. Wang, J. Nevins, and M. West. High-dimensional sparse factor modelling: Applications in gene expression genomics. Journal of the American Statistical Association, 103(484):1438–1456, December 2008.

- Chamberlain [1983] G. Chamberlain. Funds, factors and diversification in arbitrage pricing theory. Econometrica, 51:1305–1323, 1983.

- Chamberlain and Rothschild [1983] G. Chamberlain and M. Rothschild. Arbitrage, factor structure and mean-variance analysis on large asset markets. Econometrica, 51:1281–1304, 1983.

- Cook [2007] R. D. Cook. Fisher lecture: Dimension reduction in regression. Statistical Science, 22(1):1–26, 2007.

- Cook and Forzani [2008] R. D. Cook and L. Forzani. Principal fitted components for dimension reduction in regression. Statistical Science, 23(4):485–501, 2008.

- Cox [1968] D. Cox. Notes on some aspects of regression analysis. Journal of the Royal Statistical Society Series A, 131:265–279, 1968.

- Efron et al. [2004] B. Efron, T. Hastie, I. Johnstone, and R. Tibshirani. Least angle regression. The Annals of Statistics, 32(2):407–499, 2004.

- Fama and French [1992] E. Fama and K. French. The cross-section of expected stock returns. Journal of Finance, 47:427–465, 1992.

- Fama and French [1993] E. Fama and K. French. Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33:3–56, 1993.

- Fan et al. [2008] J. Fan, Y. Fan, and J. Lv. High dimensional covariance matrix estimation using a factor model. Journal of Econometrics, 147:186–197, 2008.

- Forzani [2006] L. Forzani. Principal component analysis: A conditional point of view. December 2006.

- Frisch [1934] R. Frisch. Statistical confluence analysis by means of complete regression systems. Technical Report 5, University of Oslo, Economic Institute, 1934.

- Fruhwirth-Schnatter and Lopes [2009] S. Fruhwirth-Schnatter and H. Lopes. Parsimonious bayesian factor analysis. Technical report, University of Chicago Booth School of Business, 2009.

- George and Oman [1996] E. I. George and S. D. Oman. Multiple-shrinkage principal component regression. Journal of the Royal Statistical Society Series D (The Statistician), 45(1):111–124, 1996.

- Geweke and Zhou [1996] J. Geweke and G. Zhou. Measuring the pricing error of the arbitrage pricing theory. The Review of Financial Studies, 9:557–587, 1996.

- Ghosh and Dunson [2009] J. Ghosh and D. B. Dunson. Default prior distributions and efficient posterior computation in Bayesian factor analysis. Journal of Computational and Graphical Statistics, 18(2):306–320, June 2009.

- Golub and Van Loan [1996] G. Golub and C. Van Loan. Matrix Computations. Johns Hopkins University Press, 1996.

- Hastie et al. [2001] T. Hastie, R. Tibshirani, and J. Friedman. The Elements of Statistical Learning. Springer Series in Statistics. Springer, 2001.

- Hotelling [1957] H. Hotelling. The relationship of the newer multivariate statistical methods to factor analysis. British Journal of Statistical Psychology, 10:69–79, 1957.

- Jeng and Daye [2010] X. J. Jeng and Z. J. Daye. Sparse covariance thresholding for high-dimensional variable selection. Statistica Sinica, 2010.

- Jolliffe [1982] I. T. Jolliffe. A note on the use of principal components in regression. Journal of the Royal Statistical Society, Series C, 31(3):300–303, 1982.

- Liang et al. [2007] F. Liang, S. Mukherjee, and M. West. The use of unlabeled data in predictive modeling. Statistical Science, 22(2):189–205, 2007.

- Liang et al. [2008] F. Liang, R. Paulo, G. Molina, M. A. Clyde, and J. O. Berger. Mixtures of g priors for bayesian variable selection. Journal of the American Statistical Association, 103:410–423, March 2008. URL http://ideas.repec.org/a/bes/jnlasa/v103y2008mmarchp410-423.html.

- Lopes [2003] H. Lopes. Factor models: An annotated bibliography. Bulletin of the International Society for Bayesian Analysis, 2003.

- Lopes and Carvalho [2007] H. Lopes and C. M. Carvalho. Factor stochastic volatility with time varying loadings and Markov switching regimes. Journal of Statistical Planning and Inference, 137(10):3082–3091, October 2007.

- Lopes and West [2004] H. Lopes and M. West. Bayesian model assessment in factor analysis. Statistica Sinica, 14:41–67, 2004.

- [33] J. Lucas, C. Carvalho, Q. Wang, A. Bild, J. Nevins, M. West, K. A. Do, P. Müller, and M. Vannucci. Sparse Statistical Modelling in Gene Expression Genomics, chapter 1, pages 155–176. Bayesian inference for gene expression and proteomics. Cambridge University Press.

- Mao et al. [2010] K. Mao, F. Liang, and S. Mukherjee. Supervised dimension reduction using Bayesian mixture modeling. In Proceedings of the 13th International Conference on Artificial Intelligence and Statistics, 2010.

- Maruyama and George [2010] Y. Maruyama and E. I. George. gBF: A fully bayes factor with a generalized -prior. Technical report, University of Tokyo, 2010.

- Merl et al. [2009] D. Merl, J. L.-Y. Chen, J.-T. Chi, and M. West. An integrative analysis of cancer gene expression studies using Bayesian latent factor modeling. Annals of Applied Statistics, 3(4):1675–1694, 2009.

- Mevik and Wehrens [2007] B. H. Mevik and R. Wehrens. The pls package: Principal component and partial least squares regression in R. Journal of Statistical Software, 18(2):1–24, January 2007.

- Press [1982] S. Press. Applied Multivariate Analysis: Using Bayesian and Frequentist Methods of Inference (2nd edition). New York: Krieger, 1982.

- Spearman [1904] C. Spearman. General intelligence, objectively determined and measured. American Journal of Psychology, 15:201–293, 1904.

- Vandenberghe and Boyd [1996] L. Vandenberghe and S. Boyd. Semidefinite programming. SIAM, 38(1):49–95, March 1996.

- Varmuza and Filzmoser [2009] K. Varmuza and P. Filzmoser. Introduction to Multivariate Statistical Analysis in Chemometrics. CRC Press, 2009.

- West [2003] M. West. Bayesian factor regression models in the “large p, small n” paradigm. In J. M. Bernardo, M. Bayarri, J. Berger, A. Dawid, D. Heckerman, A. Smith, and M. West, editors, Bayesian Statistics 7, pages 723–732. Oxford University Press, 2003.

- Wu et al. [2010] Q. Wu, J. Guinney, M. Maggioni, and S. Mukherjee. Learning gradients: Predictive models that infer geometry and statistical dependence. Journal Of Machine Learning Research, 11:2175–2198, August 2010.

- Zellner [1986] A. Zellner. On assessing prior distributions and Bayesian regression analysis with -prior distributions. In Bayesian Inference and Decision Techniques: Essays in Honor of Bruno de Finetti, pages 233–243. Elsevier, 1986.