Cross-Correlations between Volume Change and Price Change

Abstract

In finance, one usually deals not with prices but with growth rates , defined as the difference in logarithm between two consecutive prices. Here we consider not the trading volume, but rather the volume growth rate , the difference in logarithm between two consecutive values of trading volume. To this end, we use several methods to analyze the properties of volume changes , and their relationship to price changes . We analyze daily recordings of the S&P 500 index over the 59-year period 1950–2009, and find power-law cross-correlations between and using detrended cross-correlation analysis (DCCA). We introduce a joint stochastic process that models these cross-correlations. Motivated by the relationship between and , we estimate the tail exponent of the probability density function for both the S&P 500 index as well as the collection of 1819 constituents of the New York Stock Exchange Composite index on 17 July 2009. As a new method to estimate , we calculate the time intervals between events where . We demonstrate that , the average of , obeys . We find . Furthermore, by aggregating all values of 28 global financial indices, we also observe an approximate inverse cubic law.

There is a saying on Wall Street that “It takes volume to move stock prices.” A number of studies have analyzed the relationship between price changes and the trading volume in financial markets Ying ; Crou ; Clark ; Epps ; Rogalski ; Cornell ; Tauc ; Gram ; Karp ; Lamo90 ; Gall ; tauch96 ; Gabaix ; Gabaix06x . Some of these studies Ying ; Clark ; Epps ; Rogalski ; Cornell have found a positive relationship between price change and the trading volume. In order to explain this relationship, Clarke assumed that the daily price change is the sum of a random number of uncorrelated intraday price changes Clark , so predicted that the variance of the daily price change is proportional to the average number of daily transactions. If the number of transactions is proportional to the trading volume, then the trading volume is proportional to the variance of the daily price change.

The cumulative distribution function (cdf) of the absolute logarithmic price change obeys a power law

| (1) |

It is believed Lux96 ; Gopi98 ; Gopi99 ; Plerou99 that (“inverse cubic law”), outside the range characterizing a Lévy distribution Mand63 ; Plerou99 . A parallel analysis of , the volume traded, yields a power law Gopi00 ; Plerou07xx ; Racz09 ; Plerou09reply ; Gopi01 ; Kert05 ; kertesz ; Farm04 ; Plerou04xx

| (2) |

To our knowledge, the logarithmic volume change— and its relation to the logarithmic price change —has not been analyzed, and this analysis is our focus here.

I Data Analyzed

-

A.

We analyze the S&P500 index recorded daily over the 59-year period January 1950 – July 2009 (14,981 total data points).

-

B.

We also analyze 1819 New York Stock Exchange (NYSE) Composite members comprising this index on 17 July 2009, recorded at one-day intervals (6,794,830 total data points). Both data sets are taken from http://finance.yahoo.com. Different companies comprising the NYSE Composite index have time series of different lengths. The average time series length is 3,735 data points, the shortest time series is 10 data points, while the longest is 11,966 data points. If the data display scale independence, then the same scaling law should hold for different time periods.

-

C.

We also analyze 28 worldwide financial indices from http://finance.yahoo.com recorded daily.

-

(i)

11 European indices (ATX, BEL20, CAC 40, DAX, AEX General, OSE All Share, MIBTel, Madrid General, Stockholm General, Swiss Market, FTSE 100),

-

(ii)

12 Asian indices (All Ordinaries, Shanghai Composite, Hang Seng, BSE 30, Jakarta Composite, KLSE Composite, Nikkei 225, NZSE 50, Straits Times, Seoul Composite, Taiwan Weighted, TA-100), and

-

(iii)

5 American and Latin American indices (MerVal, Bovespa, S&P TSX Composite, IPC, S&P500 Index).

-

(i)

For each of the 1819 companies and 28 indices, we calculate over the time interval of one day the logarithmic change in price ,

| (3) |

and also the logarithmic change in trading volume Ausloos ,

| (4) |

For each of the 3694 time series, we also calculate the absolute values and and define the “price volatility” Liu99 and “volume volatility,” respectively,

| (5) |

and

| (6) |

where and are the respective standard deviations.

II Methods

Recently, several papers have studied the return intervals between consecutive price fluctuations above a volatility threshold . The pdf of return intervals scales with the mean return interval as Yama05 ; Wang06 ; Wang08

| (7) |

where is a stretched exponential. Similar scaling was found for intratrading times (case in Ref. Ivanov04 . In this paper we analyze either (i) separate indices or (ii) aggregated data mimicking the market as a whole. In case (i), e.g., the S&P500 index for any , we calculate all the values between consecutive index fluctuations and calculate the average return interval . In case (ii), we estimate average market behavior, e.g., by analyzing all the 500 members of the S&P500 index. For each and each company we calculate all values and their average.

For any given value of in order to improve statistics, we aggregate all the values in one data set and calculate . If the pdf of large volatilities is asymptotically power-law distributed, , and , we propose a novel estimator which relates the mean return intervals with , where is calculated for both case (i) and case (ii). Since on average there is one volatility above threshold for every volatilities, then

| (8) |

For both case (i) and case (ii), we calculate for varying , and obtain an estimate for through the relationship

| (9) |

We compare our estimate for in the above procedure with the value obtained from , using an alternative method of Hill Hill . If the pdf follows a power law , we estimate the power-law exponent by sorting the normalized returns by their size, , with the result Hill

| (10) |

where is the number of tail data points. We employ the criterion that does not exceed 10% of the sample size which to a good extent ensures that the sample is restricted to the tail part of the pdf Pagan96 .

A new method based on detrended covariance, detrended cross-correlations analysis (DCCA), has recently been proposed PRL08 . To quantify power-law cross-correlations in non-stationary time series, consider two long-range cross-correlated time series and of equal length , and compute two integrated signals and , where . We divide the entire time series into overlapping boxes, each containing values. For both time series, in each box that starts at and ends at , define the “local trend” to be the ordinate of a linear least-squares fit. We define the “detrended walk” as the difference between the original walk and the local trend.

Next calculate the covariance of the residuals in each box . Calculate the detrended covariance by summing over all overlapping boxes of size ,

| (11) |

If cross-correlations decay as a power law, the corresponding detrended covariances are either always positive or always negative, and the square root of the detrended covariance grows with time window as

| (12) |

where is the cross-correlation exponent. If, however, the detrended covariance oscillates around zero as a function of the time scale , there are no long-range cross-correlations.

When only one random walk is analyzed (), the detrended covariance reduces to the detrended variance

| (13) |

used in the DFA method CKP .

III Results of Analysis

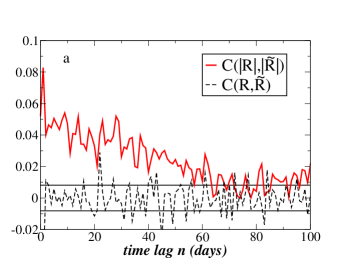

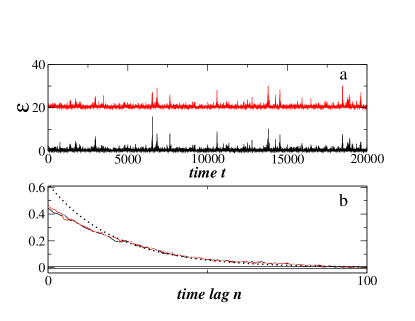

We first investigate the daily closing values of the S&P500 index adjusted for stock splits together with their trading volumes. In Fig. 1(a), we show the cross-correlation function between and and the cross-correlation function between and . The solid lines are 95% confidence interval for the autocorrelations of an i.i.d. process. The cross-correlation function between and is practically negligible and stays within the 95% confidence interval. On the contrary, the cross-correlation function between and is significantly different than zero at the 5% level for more than 50 time lags.

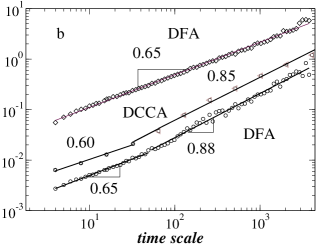

In Fig. 1(b) we find, by using the DFA method CKP ; DFA1 , that not only Engle ; Liu99 , but also exhibit power-law auto-correlations. As an indicator that there is an association between and , we note that during market crashes large changes in price are associated with large changes in market volume. To confirm co-movement between and , in Fig. 1(b) we demonstrate that and are power-law cross-correlated with the DCCA cross-correlation exponent (see Methods section) close to the DFA exponent CKP ; DFA1 corresponding to . Thus, we find the cross-correlations between and not only at zero time scale , but for a large range of time scales.

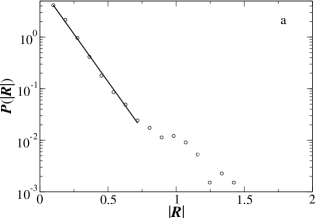

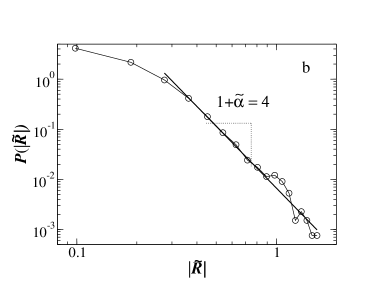

Having analyzed cross-correlations between corresponding (absolute) changes in prices and volumes, we now investigate the pdf of the absolute value of of Eq. (4). In order to test whether exponential or power-law functional form fits better the data, in Figs. 2(a) and (b) we show the pdf in both linear-log and log-log plot. In Fig. 2(a) we see that the tail substantially deviates from the central part of pdf which we fit by exponential function. In Fig. 2(b) we find that the tails of the pdf can be well described by a power law with exponent , which supports an inverse cubic law—virtually the same as found for average stock price returns Lux96 ; Gopi98 ; Gopi99 , and individual companies Plerou99 .

In order to justify the previous finding, we employ two additional methods. First, we introduce a new method [described in Methods by Eqs. (8) and (9)] for a single financial index. We analyze the probability that a trading volume change has an absolute value larger than a given threshold, . We analyze the time series of the S&P500 index for 14,922 data points. First, we define different thresholds, ranging from to . For each , we calculate the mean return interval, . In Fig. 2(c) we find that and follow the power law of Eq. (9), where . We note that the better is the power law relation between and in Fig. 2(c), the better is the power-law approximation for the tail of the pdf . In order to confirm our finding that follows a power law where obtained in Fig. 2(a) and 2(b), we also apply a third method, the Hill estimator Hill , to a single time series of the SP500 index. We obtain consistent with the results in Fig. 2(a) and 2(b).

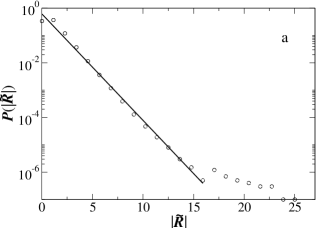

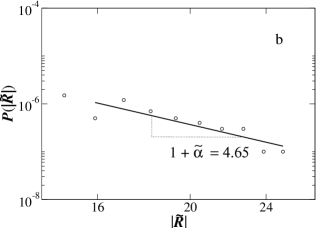

Next, by using the procedure described in case (ii) of Methods, we analyze 1,819 different time series of Eq. (4), each representing one of the 1,819 members of the NYSE Composite index. For each company, we calculate the normalized volatility of trading volume changes of each company (see Eq. (6)). In Figs. 3(a) and (b) we show the pdf in both linear-log and log-log plot. In Fig. 3(a) we see that the broad central region of the pdf, from 2 up to 15 , is fit by an exponential function. However, the far tail deviates from the exponential fit. In Fig. 3(b) we find that the tails of the pdf from 15 to up to 25 , are described by a power law with exponent .

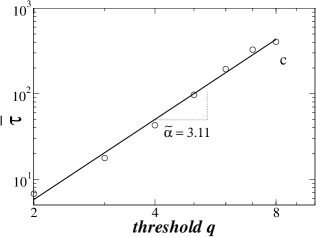

Then, by employing the method described by Eqs. (8) and (9) we define different thresholds, , ranging from to (different range than in Fig. 3(a)). We choose the lowest equal to 2 since we employ the criterion that does not exceed 10% of the sample size Pagan96 . For each , and each company, we calculate the time series of return intervals, . For a given , we then collect all the values obtained from all companies in one unique data set — mimicking the market as a whole — and calculate the average return interval, . In Fig. 3(c) we find that and follow an approximate inverse cubic law of Eq. (9), where . Our method is sensitive to data insufficiency, so we show the results only up to 8 . Clearly, this method gives the value for the market as a whole, not the values for particular companies. By joining all the normalized volatilities obtained from 1,819 time series in one unique data set, we estimate Hill’s exponent of Eq. (10), , consistent with the value of exponent obtained using the method of Eqs. (8) and (9).

In the previous analysis we consider time series of the companies comprising the NYSE Composite index of different lengths (from 10 to 11,966 data points). In order to prove that the Hill exponent of Eq. (10) is not affected by the shortest time series, next we analyze only the time series longer than 3,000 data points (1,128 firms in total). For the Hill exponent we obtain , that is the value practically the same as the one we obtained when short time series were considered as well.

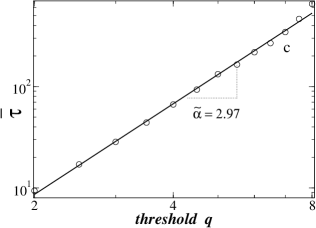

We perform the method of Hill Hill , and the method of Eqs. (8) and (9), also for the 500 members of the S&P500 index comprising the index in July 2009. There are in total data points for of Eq. (6). For the thresholds, , ranging from to , we find that and follow for this range an approximate inverse cubic law of Eq. (9), where . We estimate the Hill exponent of Eq. (10) to be , with the lowest .

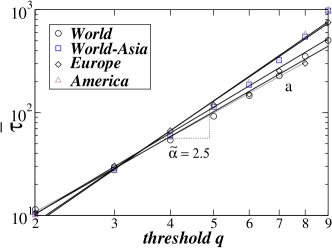

In order to find what is the functional form for trading-volume changes at the world level, we analyze 28 worldwide financial indices using the procedure described in Methods [case(ii)]. For each , and for each of the 28 indices, we calculate the values for the return interval . Then for a given , we collect all the values obtained for all indices and calculate the average return interval . In Fig. 4(a), we find a functional dependence between and which can be approximated by a power law with exponent . We also calculate vs. for different levels of financial aggregation.

Finally, in addition to trading-volume changes, we employ for stock price changes our procedure for identifying power-law behavior in the pdf tails described in Methods [case (ii)]. The pdf of stock price changes, calculated for an “average” stock, is believed to follow where , as empirically found for wide range of different stock markets Lux96 ; Gopi99 .

Next we test whether this law holds more generally. To this end, we analyze the absolute values of price changes, [see Eq. (3)], for five different levels of financial aggregation: (i) Europe, (ii) Asia, (iii) North and South America, (iv) the world without the USA, and (v) the entire world. For each level of aggregation, we find that the average return interval .

IV Model

In order to model long-range cross-correlations between and , we introduce a new joint process for price changes

| (14) |

| (15) |

and for trading-volume changes

| (16) |

| (17) |

If , Eqs. (14)–(17) reduce to two separate processes of Ref. Boll . Here and are two i.i.d. stochastic processes each chosen as Gaussian distribution with zero mean and unit variance. In order to fit two time series, we define free parameters , , , , , , , , which we assume to be positive Boll . The process of Eqs. (14)–(17) is based on the generalized autoregressive conditional heteroscedasticity (GARCH) process (obtained from Eqs. (14)-(15) when ) introduced to simulate long-range auto-correlations through . The GARCH process also generates the power-law tails as often found in empirical data [see Lux96 ; Gopi98 ; Gopi99 ; Plerou99 , and also Fig. 2(b)]. In the process of Eqs. (14)–(17) we obtain cross-correlations since time-dependent standard deviation for price changes depends not only on its past values (through and ), but also on past values of trading-volume errors (). Similarly, for trading-volume changes depends not only on its past values (through and ), but also on past values of price errors ().

For the joint stochastic process of Eqs. (14)-(17) with , , , we show in Fig. 5(a) the cross-correlated time series of Eqs. (15) and (17). In Fig. 5(b) we show the auto-correlation function for and the cross-correlation function which practically overlap due to the choice of parameters.

If stationarity is assumed, we calculate the expectation of Eq. (15) and (17) and since, e.g., , we obtain , and similarly . So, stationarity generally assumes that as found for the GARCH process Boll . However, for the choice of parameters in the previous paragraph for which stationarity assumes that . This result explains why the persistence of variance measured by should become negligible in the presence of volume in the GARCH process Lamo90 . In order to have finite , we must assume .

It is also possible to consider IGARCH and FIGARCH processes with joint processes for price and volume change, a potential avenue for future research Boll2 .

V Summary

In order to investigate possible relations between price changes and volume changes, we analyze the properties of , the logarithmic volume change. We hypothesize that the underlying processes for logarithmic price change and logarithmic volume change are similar. Consequently, we use the traditional methods that are used to analyze changes in trading price to analyze changes in trading volume. Two major empirical findings are:

(i) we analyze a well-known U.S. financial index, the S&P500 index over the 59-year period 1950-2009, and find power-law cross-correlations between and . We find no cross-correlations between and .

(ii) we demonstrate that, at different levels of aggregation, ranging from the S&P500 index, to aggregation of different world-wide financial indices, approximately follows the same cubic law as . Also, we find that the central region of the pdf, , follows an exponential function as reported for annually recorded variables, such as GDP Lee ; PRE08 , company sales Michael , and stock prices EPL09 .

In addition to empirical findings, we offer two theoretical results:

(i) to estimate the tail exponent for the pdf of , we develop an estimator which relates of the cdf to the average return interval between two consecutive volatilities above a threshold Yama05 .

(ii) we introduce a joint stochastic process for modeling simultaneously and , which generates the cross-correlations between and . We also provide conditions for stationarity.

Acknowledgements.

We thank NSF and the Ministry of Science of Croatia for financial support.References

- (1) Ying C C (1966) Stock market prices and volume of sales. Econometrica 34:676–685.

- (2) Crouch R L (1970) The Volume of Transactions and Price Changes on the New York Stock Exchange. Financial Analysts Journal 26:104–109.

- (3) Clark P K (1973) A subordinate stochastic process model with finite variance for speculative prices. Econometrica 41:135–155.

- (4) Epps T W, Epps M L (1976) The stochastic dependence of security price changes and transaction volumes: Implications for the mixture-of-distribution hypothesis. Econometrica 44:305–321.

- (5) Rogalski R J (1978) The dependence of prices and volume. Review of economics and statistics 60:268–274.

- (6) Cornell B (1981) The relationship between volume and price variability in future markets. Journal of Futures Markets 1:303–316.

- (7) Tauchen G, Pitts M (1983) The Price Variability-Volume Relationship on Speculative Markets. Econometrica 51:485–505.

- (8) Grammaticos T, Saunders A (1986) Futures Price Variability: A Test of Maturity and Volume Effects, Journal of Business 59:319–330.

- (9) Karpoff J (1987) The relation Between Price Changes and Trading Volume. Journal of Financial and Quantitative Analysis 22:109–126.

- (10) Lamoureux C G, Lastrapes W D (1990) Heteroskedasticity in Stock Return Data: Volume Versus GARCH Effects. Journal of Finance 45:221–229.

- (11) Gallant A R et al. (1992) Stock Prices and Volume. Review of Financial Studies 5:199–242.

- (12) Tauchen G (1996) Volume, Volatility, and Leverage: A Dynamic Analysis, Journal of Econometrics 74:177–208.

- (13) Gabaix X et al. (2003) A theory of power-law distributions in financial market fluctuations. Nature 423:267–270.

- (14) Gabaix X et al. (2006) Institutional investors and stock market volatility. Quarterly Journal of Economics 121:461–504.

- (15) Lux (1996) The stable Paretian hypothesis and the frequency of large returns: an examination of mayor German stocks. Applied Financial Economics 6:463–475.

- (16) Gopikrishnan P et al. (1998) Inverse cubic law for the probability distribution of stock price variations. European Physical Journal B: Rapid Communications 3:139–140.

- (17) Gopikrishnan P et al. (1999) Scaling of the Distributions of fluctuations of financial market indices. Phys. Rev. E 60:5305–5316.

- (18) Plerou V et al. (1999) Scaling of the distributions of price fluctuations of individual companies. Phys. Rev. E 60:6519–6529.

- (19) Mandelbrot B (1963) The variation of certain speculative prices. Journal of Business 26:394–419.

- (20) Gopikrishnan P et al. (2000) Statistical properties of share volume traded in financial markets. Phys. Rev. E 62:R4493–R4496.

- (21) Plerou V, Stanley HE (2007) Tests of scaling and universality of the distributions of trade size and share volume: Evidence from three distinct markets. Phys. Rev. E 76:046109.

- (22) Rácz E et al. (2009) Comment on “Tests of scaling and universality of the distributions of trade size and share volume: Evidence from three distinct markets”. Phys. Rev. E 79:068101.

- (23) Plerou V, Stanley HE (2009) Reply to “Comment on ‘Tests of scaling and universality of the distributions of trade size and share volume: Evidence from three distinct markets”’. Phys. Rev. E 79:068102.

- (24) Gopikrishnan P et al. (2001) Price fluctuations, market activity and trading volume. Quantitative Finance 1:262–270.

- (25) Eisler Z, Kertesz J (2005) Size matters: some stylized facts of the stock market revisited. European Physical Journal B 51:145–154.

- (26) Eisler Z, Kertesz J (2006) Scaling theory of temporal correlations and size-dependent fluctuations in the traded value of stocks. Phys. Rev. E 73:046109.

- (27) Farmer J D and Lillo F (2004) On the origin of power law tails in price fluctuations. Quantitative Finance 3:C7–C11.

- (28) Plerou V et al. (2004) On the Origins of Power-Law Fluctuations in Stock Prices. Quantitative Finance 4:C11–C15.

- (29) Ausloos M, Ivanova K (2002) Mechanistic approach to generalized technical analysis of share prices and stock market indices. Eur. Phys. J. B 27:177-187.

- (30) Liu Y et al. (1999) The statistical properties of the volatility of price fluctuations. Phys. Rev. E 60:1390–1400.

- (31) Yamasaki K et al. (2005) Scaling and Memory in Volatility Return Intervals in Stock and Currency Markets. Proc. Natl. Acad. Sci. USA 102:9424–9248.

- (32) Wang F et al. (2006) Scaling and memory of intraday volatility return intervals in stock market. Phys. Rev. E 73:026117.

- (33) Wang F et al. (2008) Indication of multiscaling in the volatility return intervals of stock markets. Phys. Rev. E 77:016109.

- (34) Ivanov P Ch et al. (2004) Common scaling patterns in intratrade times of U.S. Stocks. Phys. Rev. E 69:056107.

- (35) Hill B M (1975) A simple general approach to inference about the tail of a distribution. Ann. Stat. 3:1163–1174.

- (36) Pagan A (1996) The econometrics of financial markets. Journal of Empirical Finance 3:15–102.

- (37) Podobnik B, Stanley H E (2008) Detrended cross-correlation analysis: A new method for analyzing two nonstationary time series. Physical Review Letters 100:084102.

- (38) Peng C K et al. (1994) Mosaic Organization of DNA Nucleotides. Phys. Rev. E 49:1685–1689.

- (39) Hu K et al. (2001) Effect of trends on detrended fluctuation analysis. Phys. Rev. E 64:011114.

- (40) Ding Z et al. (1993) A long memory property of stock market returns and a new model. Journal of Empirical Finance 1:83–106.

- (41) Bollerslev T (1986) Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31:307–327.

- (42) Lee Y et al. (1998) Universal features in the growth dynamics of complex organizations. Phys. Rev. Lett. 81:3275–3278.

- (43) Podobnik B et al. (2008) Size-dependent standard deviation for growth rates: Empirical results and theoretical modeling. Phys. Rev. E 77:056102.

- (44) Stanley M H R et al. (1996) Scaling behavior in the growth of companies. Nature 379:804–806.

- (45) Podobnik B, Horvatic D, Petersen A M, and Stanley H E (2009) Quantitative relations between risk, return and firm size. Europhys. Lett. 85:50003.

- (46) Bollerslev T, Mikkelsen H O (1996) Modeling and pricing long memory in stock market volatility. Journal of Econometrics 73:151–184.