Is Brownian motion necessary to model high-frequency data?

Abstract

This paper considers the problem of testing for the presence of a continuous part in a semimartingale sampled at high frequency. We provide two tests, one where the null hypothesis is that a continuous component is present, the other where the continuous component is absent, and the model is then driven by a pure jump process. When applied to high-frequency individual stock data, both tests point toward the need to include a continuous component in the model.

doi:

10.1214/09-AOS749keywords:

[class=AMS] .keywords:

.and t1Supported in part by NSF Grants DMS-05-32370 and SES-0850533. \pdfauthorYacine Ait-Sahalia, Jean Jacod

1 Introduction

This paper continues our development of statistical methods designed to assess the specification of continuous-time models sampled at high frequency. The basic framework, inherited from theoretical models in mathematical finance but also common in other fields such as physics or biology, is one where the variable of interest , in financial examples often the log of an asset price, is assumed to follow an Itô semimartingale. That semimartingale is observed on some fixed time interval at discrete regularly spaced times , with a time lag which is small.

A semimartingale can be decomposed into the sum of a drift, a continuous Brownian-driven part and a discontinuous, or jump, part. The jump part can in turn be decomposed into a sum of “small jumps” and “big jumps.” Such a process will always generate a finite number of big jumps, but it may give rise to either a finite or infinite number of small jumps, corresponding to the finite and infinite jump activity situations, respectively. In earlier work, we developed tests to determine on the basis of the observed sampled path on whether a jump part was present, whether the jumps had finite or infinite activity, and in the latter situation proposed a definition and an estimator of a “degree of jump activity” parameter.

In this paper, we tackle the last remaining question: Does the semimartingale need to have a continuous part? In other words, is the Brownian motion present at all? From a model specification standpoint, there is a natural statistical interest in distinguishing the two situations where a continuous part is included or not, on the basis of an observed sample path. When there are no jumps, or finitely many jumps, and no Brownian motion, reduces to a pure drift plus occasional jumps, and such a model is fairly unrealistic in the context of most financial data series, although it may be realistic in some other contexts. But for financial applications one can certainly consider models that consist only of a jump component, plus perhaps a drift, if that jump component is allowed to be infinitely active.

Many models in mathematical finance do not include jumps. But among those that do, the framework most often adopted consists of a jump-diffusion: these models include a drift term, a Brownian-driven continuous part and a finite activity jump part (see, e.g., balltorous83 , bates91 and merton76 ). When infinitely many jumps are included, however, there are a number of models in the literature which dispense with the Brownian motion altogether. The log-price process is then a purely discontinuous Lévy process with infinite activity jumps or, more generally, is driven by such a process (see, e.g., eberleinkeller95 , carrwu03b and madanseneta90 ).

The mathematical treatment of models relying on pure jump processes is quite different from the treatment of models where a Brownian motion is present. For instance, risk management procedures, derivative pricing and portfolio optimization are all significantly altered, so there is interest from the mathematical finance side in finding out which model is more likely to have generated the data.

For all these reasons, it is of importance to construct procedures which allow us to decide whether the Brownian motion is really here, or if it can be forgone in favor of a pure jump process. This is the aim of this paper: we will provide two tests allowing for a symmetric treatment of the two situations where the null hypothesis is that the Brownian motion is present, and where the null is that the Brownian motion is absent.

In the context of a specific parametric model, allowing for jump components of finite or infinite activity on top of a Brownian component, carrgemanmadanyor02 find that the time series of index returns are likely to be devoid of a continuous component. An alternative but related approach to testing for the presence of a Brownian motion component to the one we propose here is due to tauchentodorov . They employ the test statistic for jumps of yacjacod09a , plot its logarithm for different values of the power argument and contrast the behavior of the plot above two and below two in order to identify the presence of a Brownian component. A formal test is constructed under the null hypothesis where a continuous component is present.

The methodology that both tauchentodorov and we employ to design our respective test statistics is based on tried-and-true principles that originate in our earlier work on testing whether jumps are present yacjacod09a , whether they have finite or infinite activity yacjacod08c and on estimating the index of jump activity yacjacod09b , although, of course, exploited in a manner specific to the problem at hand. We compute power variations of the increments, suitably truncated and/or sampled at different frequencies. Exploiting the different asymptotic behavior of the variations as we vary these parameters gives us enough flexibility to accomplish our objectives. As is well known, powers below two will emphasize the continuous component of the underlying sampled process. Powers above two will conversely accentuate its jump component. The power two puts them on an equal footing. Truncating the large increments at a suitably selected cutoff level can eliminate the big jumps when needed, as was shown by mancini01 . Finally, sampling at different frequencies can let us distinguish between situations where the variations converge to a finite limit, in which case the ratio of two variation measures constructed at different frequencies will converge to one, from situations where the variations converge to either zero or diverge to infinity, in which case the ratio will typically converge to a different constant. Since these various limiting behaviors are indicative of which component of the model dominates at a particular power, they effectively allow us to distinguish between all manners of null and alternative hypotheses.

This said, the commonality of approach should not mask the fact that each situation is, in reality, mathematically quite different. By nature, certain components of the model are turned off under particular null hypotheses. For instance, when the null hypothesis is that no Brownian motion is present, as will be the case for our first test here, then jumps drive the asymptotics. As a result, the driving component of the model that matters for the asymptotic behavior of the statistic will vary with the situation and consequently the methods employed behind the scenes to obtain the desired asymptotics will vary accordingly.

The paper is organized as follows. Section 2 describes our model and the statistical problem. Our testing procedure is described in Section 3, and the next two Sections, 4 and 5, are devoted to a simulation study of the tests and an empirical implementation of our tests on high-frequency stock returns. Section 6 is devoted to technical results and to the proof of the main theorems.

2 The model

The underlying process which we observe at discrete times is a -dimensional Itô semimartingale defined on some filtered space , which means that its characteristics are absolutely continuous with respect to Lebesgue measure. is the drift, is the quadratic variation of the continuous martingale part and is the compensator of the jump measure of . In other words, we have

Here and are optional process, and is a transition measure from endowed with the predictable -field into . More customarily, one may write as

where is a standard Brownian motion. It is also possible to write the last two terms above as integrals with respect to a Poisson measure and its compensator, but we do not need this here. This is a standard setup and we refer the reader to jacodshiryaev2003 for details.

We have referred above to “small jumps” and “big jumps.” In the context of (2), they are represented, respectively, by the last two integrals. The size cutoff adopted here is arbitrary and could be replaced by any fixed a change which amounts merely to an adjustment to the drift term Note that the small jumps integral needs to be compensated by since there are potentially an infinite number of such small jumps. The large jump integral is always a finite sum; it may be compensated if desired but this is not necessary. Any compensation or lack thereof is then again absorbed by an adjustment to the drift.

We now turn to the assumptions. As usual for tests, the assumptions essentially ensure that one can compute and then estimate a significance level under the null hypothesis. So here, we need some structure for the jumps of , namely that the small jumps essentially behave like the small jumps of a stable process with some index , up to a random intensity. As noted above, when no Brownian is present, we view the realistic situation as one where there are infinitely many small jumps. When the null is that there is a Brownian motion, we need the additional assumption that the volatility process is itself an Itô semimartingale.

We would like to give tests with a prescribed asymptotic level, as , and, of course, this is more difficult when increases because then the process resembles more and more a continuous process plus a few big jumps: The qualitative behavior of the paths can become quite similar whether the Brownian motion is present or not. So, unsurprisingly, we can exhibit a test with prescribed level, for the null hypothesis where the Brownian motion is present, only when . The parameter is typically unknown (although a method for estimating in this setting is given in yacjacod09b ). On the other hand, for the null hypothesis where the Brownian motion is absent we provide a test which works under no assumption on .

With this context in mind, here is the first assumption which will be assumed throughout:

Assumption 1

(i) The drift process is locally bounded and the volatility process is càdlàg.

(ii) There are three constants and a locally bounded process , such that the Lévy measure is of the form , where

| (3) |

where , , , are nonnegative predictable processes and is predictable function (meaning -measurable, where is the predictable -field on ), satisfying

and where is a measure which is singular with respect to and satisfies

| (5) |

This assumption is identical to Assumptions 1 and 2 of yacjacod09b [with some notational changes: in that paper are called here , and the condition is not a restriction and is put here only for convenience].

For example, take a process solution of the stochastic differential equation

| (6) |

where and are càdlàg adapted processes, is -stable or tempered -stable and is any other Lévy process whose Lévy measure integrates near the origin and has an absolutely continuous part whose density is smaller than on for some (e.g., a stable process with index strictly smaller than ). Then will satisfy Assumption 1.

If this assumption is satisfied with , then almost surely the jumps have finite variation for all or equivalently, . This allows us to decompose into the sum , where

| (7) |

and where is a locally bounded process.

For clarity, we will derive the properties of both tests under the same generic Assumption 1 even though the properties of the test for the null of a Brownian present remain valid under weaker assumptions. When the null hypothesis to be tested is that the Brownian motion is present, it becomes the driving process for our test statistic and as is customary for tests or estimation problems involving a stochastic volatility, we then need an additional regularity assumption on the process:

Assumption 2

We have Assumption 1 with . Moreover the volatility process is an Itô semimartingale, that is, it can be written (necessarily in a unique way) as

| (8) |

where is a local martingale which is orthogonal to the Brownian motion , and further the compensator of the process is of the form . Moreover we suppose that: {longlist}[(ii)]

the processes and are locally bounded;

the processes and defined above are càdlàg.

3 The two tests

3.1 The hypotheses to be tested

In a semimartingale model like (2), saying that the Brownian motion is absent on the interval does not mean that there is no Brownian motion on the probability space (something which cannot be tested at all, obviously) but it means that the Brownian motion does not impact the observed process , in the sense that the corresponding stochastic integral vanishes on this interval, or equivalently for Lebesgue-almost all in , and it would be more appropriate to say that we are testing whether “the continuous martingale part of vanishes on , or not.” This is typically an -wise property: we can divide the set into two complementary subsets

| (9) |

Then almost surely on the set the integral process vanishes on , whereas it does not vanish on the complement . In what follows, we take to represent the hypothesis that the Brownian motion is present and to represent the hypothesis that the Brownian motion is not present.

In connection with Assumption 1 we consider the following set representing paths that have infinite jump activity of some index :

| (10) |

One knows that on the set the path of over has almost surely infinitely many jumps.

We are interested in testing the following two situations:

| (11) |

As discussed above, the realistic situation supposes that infinite activity jumps are present when under and so we will in fact provide testing procedures for the following two situations:

| (12) |

In the second test, requiring with under allows us to characterize precisely the properties of the statistic under this alternative (as opposed to just ). But it is not necessary for the actual implementation of the test which relies on its behavior under the null.

Finally, we recall that testing a null hypothesis “we are in a subset ” of , against the alternative “we are in a subset ,” with, of course, , amounts to finding a critical (rejection) region at stage . The asymptotic size and asymptotic power for this sequence of critical regions are the following numbers:

| (13) |

3.2 The building blocks

Before stating the results, we introduce some notation to be used throughout. We observe the increments of

| (14) |

to be distinguished from the (unobservable) jumps of the process, . In a typical application, is a log-asset price, so is the recorded log-return over units of time.

For any given cutoff level we count the number of increments of with size bigger than , that is,

| (15) |

If we also sum the th absolute power of the increments of , truncated at level , that is,

| (16) |

is what we call a “truncated power variation.” Note that in we are retaining all increments smaller than whereas in we are retaining those larger than

We take a sequence of positive numbers, which will serve as our thresholds or cutoffs for truncating the increments, and will go to as the sampling frequency increase. There will be restrictions on the rate of convergence of this sequence, expressed in the form

| (17) |

This condition becomes weaker when increases and when decreases.

In practice, when a Brownian motion is present, we will often translate values of the cutoff level in terms of a number of standard deviations of the continuous part of the semimartingale. That is, we express values of in terms of where Despite the presence of jumps, the integrated volatility in that expression can be estimated using the small increments of the process, since

| (18) |

for any and We can then vary the cutoff level to yield a number of (estimated) standard deviations of the continuous part of the semimartingale. This data-driven choice can help determine a range of reasonable values for the cutoff level and provide on a path-by-path basis an equivalent, but perhaps more intuitive, scale with which to measure the magnitude of the cutoff level .

When there is no Brownian motion under the null, a different scale needs to be used to assess the size of For example, we can translate into the percentage of the sample that is greater than the cutoff level, and therefore not included in the computation of the truncated power variations.

3.3 Testing for the presence of Brownian motion under the null

In a first case, we set the null hypothesis to be “the Brownian motion is present,” that is , against the alternative .

In order to construct a test, we seek a statistic with markedly different behavior under the null and alternative. One fairly natural idea is to consider powers less than since in the presence of Brownian motion they would be dominated by it, while in its absence they would behave quite differently. Specifically, the large number of small increments generated by a continuous component would cause a power variation of order less than to diverge to infinity. Without the Brownian motion, however, and when , the power variation converges to at exactly the same rate for the two sampling frequencies and whereas in the former case the choice of sampling frequency will influence the magnitude of the divergence. Taking a ratio will eliminate all unnecessary aspects of the problem and focus on the key aspect, that of distinguishing between the presence and absence of the Brownian motion.

Specifically, we fix a power and an integer , and we consider the test statistics, which depend on and on the terminal time and on the sequence subject to (17), as follows:

| (19) |

As will become clear below, taking ratios of power variations has the advantage of making the test statistic model-free. That is, its distribution under the null hypothesis can be assessed without the need for the extraneous estimation of the dynamics of the process in (2). Obviously, these dynamics can be quite complex with potentially jumps of various activity levels, stochastic volatility, jumps in volatility, etc. So the fact that the standardized test statistic can be computed without the need to estimate the various parts of (2) is a desirable feature. In fact, implementing the test—that is, computing the statistic in (19) and estimating its asymptotic variance—will require nothing more than the computation of various truncated power variations.

The first result is a law of large numbers (LLN) giving the probability limit of the statistic .

Theorem 1

Under Assumption 1 and if , we have

| (20) |

This result shows that, since , for the test at hand an a priori reasonable critical region is , for a sequence increasing strictly to : in this case the asymptotic power is in restriction to the set described in the second alternative above, whereas the asymptotic level depends on how fast converges to .

For a more refined version of this test, with a prescribed level , we need a central limit theorem (CLT) associated with the convergence in (20). For this we need some notation: letting and be two independent variables, we set

| (21) |

In terms of known functions, we have

| (22) |

where is Gauss’s hypergeometric function (see, e.g., Section 15.1 of abramowitzstegun ).

Then the standardized version of the CLT goes as follows (we use to denote the stable convergence in law (see, e.g., jacodshiryaev2003 for this notion); to explain the following statement, we recall that the convergence in law “in restriction to a subset ” is meaningless, but the stable convergence in law in restriction to makes sense):

Theorem 2

We are now ready to exhibit a critical region for testing vs. using with a prescribed asymptotic level . Denoting by the -quantile of , that is, where is , we set

| (25) |

Theorem 3

To perform the test we need to choose and the sequence . In practice one does not know , although it should be smaller than by Assumption 2. Hence if we are willing to assume that , although unknown, is not bigger than some prescribed , one should choose , and one may take for some and some , and the test can be done as soon as

| (27) |

To properly separate the two hypotheses it is probably wise to choose closer to than to .

Remark 1.

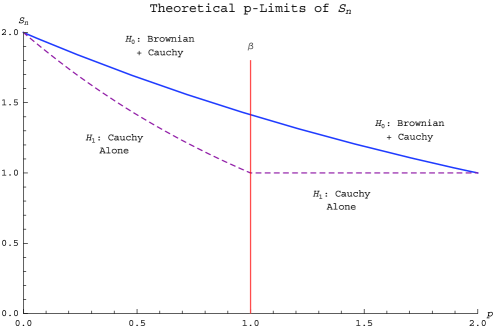

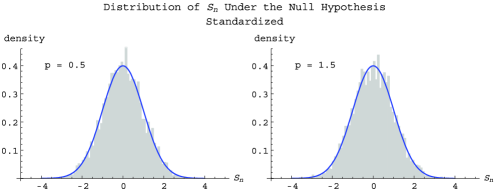

The first part of the consistency result (20) holds also for on (with basically the same proof). The second part also holds for on the set on which for all , that is, when there is no drift, whereas when there is a drift, converges to for all . When the limit of is on when , and also when when again there is no drift (and the proof is more involved). Figure 1 illustrates these various limits in the case is the sum of a Brownian martingale plus possibly a Cauchy process (with no drift).

Remark 2.

The CLT necessitates . However, more sophisticated techniques would allow us to prove the same result for all , under the additional assumption that does not vanish for , on the set (we still need , however).

Remark 3.

Despite the fact that using powers less than is the most natural way to isolate the contribution of the Brownian motion to the overall increments of the process, it is possible to design an alternative test that relies on powers greater than Instead of the statistic above, we could use the following statistic: pick and , and set

| (28) |

Under Assumption 1, converges in probability to on the set , and to on the set , as soon as . We also have a CLT under Assumption 2 and if . Under is model-free, just like is. So one can, in an obvious way, construct a test based on and which satisfies the claims of Theorem 3, under suitable conditions on the cutoff levels . However, simulations studies suggest that the statistic is not as well behaved as , and so we do not pursue its study further.

3.4 Testing for the absence of Brownian motion under the null

In a second case, we set the null hypothesis to be “the Brownian motion is absent,” that is, . Designing a test under this null is trickier because the model becomes a pure jump (plus perhaps a drift) process, and we are aiming for a test that remains model-free even for this model. That is, we are looking for a statistic whose limiting behavior under the null, despite being driven by what is now a pure jump process, does not depend on the characteristics of the pure jump process, such as its degree of activity , since those characteristics are a priori unknown.

This can be achieved as follows. We choose a real and a sequence satisfying (17) and define the test statistic

| (29) |

To understand the construction of this test statistic, recall that in a power variation of order the contributions from the Brownian and jump components are of the same order. But once the power variation is properly truncated, the Brownian motion will dominate it if it is present. And the truncation can be chosen to be sufficiently loose that it retains essentially all the increments of the Brownian motion at cutoff level and a fortiori , thereby making the ratio of the two truncated quadratic variations converge to under the alternative hypothesis. On the other hand, if the Brownian motion is not present, then the nature of the tail of jump distributions is such that the difference in cutoff levels between and remains material no matter how far we go in the tail, and the limit of that same ratio will reflect it: it will now be under assumptions made specific in the formal theorems below. Since absence of a Brownian motion is now the null hypothesis, the issue is then that this limit depends on the unknown

Canceling out that dependence is the role devoted to the ratio of the number of large increments, the ’s, in (29). The ’s are always dominated by the jump components of the model whether the Brownian motion is present or not. Their inclusion in the statistic is merely to ensure that the statistic is model-free, by effectively canceling out the dependence on the jump characteristics that emerges from the ratio of the truncated quadratic variations. Indeed, the limit of the ratio of the ’s is under both the null and alternative hypotheses. As a result, the probability limit of will be under the null, independent of .

Our first result states this precisely, establishing the limiting behavior of the statistic in terms of convergence in probability:

For a test with a prescribed level we need a standardized CLT.

Theorem 5

Hence a critical region for testing vs. is

| (33) |

Theorem 6

If we take again , the test can be performed if and

| (34) |

(always smaller than ). This requirement is constraining, because is unknown, and may typically be close to if we believe in the null hypothesis. Therefore in practice we must assume that does not exceed a given . This means that this limiting index is given a priori, and we do the test under the Assumption 1 with and , with subject to the (feasible) condition

| (35) |

These facts are not really surprising: first, by (30) we know that the statistic properly separates the two hypotheses only when is not too close to . And, second, when becomes very close to , the paths of have big jumps but also the compensated sum of small jumps looks more and more like a Brownian path, even on the set .

Remark 4.

It is possible to design an alternative statistic with similar properties but make no use of the ’s. Instead of the statistic in (29), we could use the following statistic: pick and , and set

| (36) |

Under Assumption 1, converges in probability to on the set , and to on the set , as soon as . The ratio of th power variations plays a similar role to that of the ’s, namely to cancel out the dependence of the -lim of on under the null. The fixed scaling factor allows us to use different cutoff levels for the two powers and without affecting the probability limit of the statistic. We also have a CLT if . Under is model-free, just like is, and so a test follows. But as was the case for the statistic proposed in (28), simulations studies suggest that is not as well behaved as .

Remark 5.

In Theorems 2 and 3 the rate of convergence is hidden because of the standardization, but it is , clearly optimal since there are observation altogether. In Theorems 5 and 6 the rate is , which is again “optimal” when we only use the increments bigger than [more precisely, if we were able to observe exactly all jumps of with size bigger than , this rate would be the optimal one, up to a term]. However, for those theorems we also have to choose : the smallest is, compared to , the biggest the actual rate is, but we are limited in this choice by the upper bound on . For example if we take , and due to (35), the best rate is “almost” .

4 Simulation results

We now report simulation results documenting the finite sample performance of the test statistics and . We calibrate the values to be realistic for a liquid stock trading on the NYSE, and we consider an observation length of days (one month) sampled every five seconds.

We conduct simulations to determine the small sample behavior of the two statistics and under their respective null and alternative hypotheses. The tables and graphs that follow report the results of simulations. The data generating process is the stochastic volatility model with , , , , is a compound Poisson jump process with jumps that are uniformly distributed on and . The jump process is a -stable process with , that is, a Cauchy process (which has infinite activity, and will be our model under ; this is a borderline case for the statistics under the null, nevertheless we will see that this statistic behaves well). Given the scale parameter (or equivalently ) of the stable process in simulations is calibrated to deliver different various values of the tail probability . In the various simulations’ design, we hold fixed. Therefore the tail probability parameter controls the relative scale of the jump component of the semimartingale relative to its continuous counterpart. We set such that neither of the two components of the model, and is negligible compared to the other when the hypothesis states that they should both be present. We achieve this by computing the expected percentage of the total quadratic variation attributable to jumps on a given path from the model, and set it to values that range from and

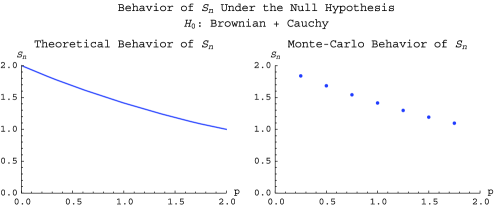

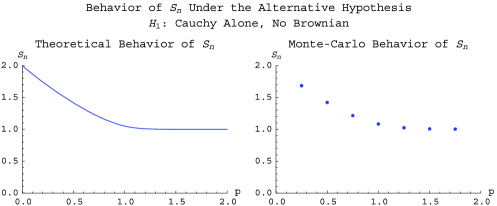

4.1 The first test

The statistic is implemented with and values of that range from to (recall Remark 2). Figure 2 compares the theoretical and Monte Carlo behavior of as a function of the power under the null hypothesis where a Brownian motion is present, in addition to a Cauchy pure jump process. Figure 3 shows the corresponding results under the alternative hypothesis, where there is no Brownian motion. The theoretical curves are computed from the expected values of the truncated power variations using the exact density of the increments at the sampling interval seconds, rather than their asymptotic limits for This introduces a slight Jensen’s inequality effect in the figure but appears to capture well the small sample behavior of the statistic.

Recall that for concreteness is expressed as a number of standard deviations of the Brownian part of : that is, the level of truncation is expressed in terms of the number of standard deviations of the continuous martingale part of the process, defined in multiples of the long-term volatility parameter : is defined by Our view of the joint choice of is that they are not independent parameters in finite sample: they are different parameters for asymptotic purposes but in finite samples the only relevant quantity is the actual resulting cutoff size . This is why we are reporting the values of the cutoffs in the form of the that would correspond to This has the advantage of providing an easily interpretable size of the cutoff compared to the size of the increments that would be expected from the Brownian component of the process: we can then think in terms of truncating at a level that corresponds to , etc., standard deviations of the continuous part of the model. Since the ultimate purpose of the truncation is either to eliminate or conserve that part, it provides an immediate and intuitively clear reference point. Of course, given and this it is possible to back this into the value of the corresponding to any for that given sample size, including the value(s) of that satisfy the required inequalities imposed by the asymptotic results. This approach would lose its effectiveness if we were primarily interested in testing the validity of the asymptotic approximation as the sample size varies, but for applications, by definition on a finite sample, it seems to us that the interpretative advantage outweighs this disadvantage.

| Sample rejection rate (%) for power | ||||||||

| Degree of truncation | Test theoretical level | 0.25 | 0.5 | 0.75 | 1.0 | 1.25 | 1.5 | 1.75 |

| 6 | 9.1 | 9.4 | 9.4 | 9.1 | 8.9 | |||

| 4.6 | 4.7 | 4.8 | 4.5 | 4.1 | ||||

| 7 | 9.7 | 9.7 | 9.8 | 9.9 | 9.8 | |||

| 5.0 | 5.0 | 5.1 | 4.9 | 4.4 | ||||

| 8 | 9.7 | 9.9 | 9.9 | 9.9 | 9.9 | |||

| 5.0 | 5.1 | 5.1 | 4.9 | 4.5 | ||||

The statistic in the plots is computed with a truncation level corresponding to . Table 1 looks at the dependence of the results on the choice of

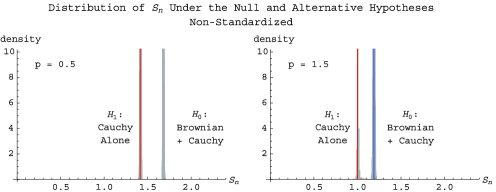

Next, we report in Figure 4 histograms of the values of the unstandardized computed under and , respectively, and with the same level of truncation . The vertical lines represent the anticipated limits of the statistic in the two situations, under and either when or when under , based on Theorem 1 and Remark 1. Since here , the two graphs with and illustrate the two situations where and

Figure 5 reports the Monte Carlo distribution of the statistic standardized according to Theorem 2, compared to the limiting distribution. Table 1 reports the Monte Carlo rejection rates of the test of vs. at the and level, using the test statistic for various levels of truncation . We find that the test behaves well, with empirical test levels close to their theoretical counterparts.

4.2 The second test

We now turn to the second problem, that of testing vs. . For this test, is implemented with a second truncation level twice as large as the first, that is, The simulation evidence suggests that the results are largely similar for values of within a range of to . Parameter values are identical to those employed for the first test. Since there is no Brownian motion under the null, the truncation level is set in terms of the percentage of observations that are excluded by the truncation. For comparison with the truncation levels employed in the first test, we report it here again in terms of a number of standard deviations for the Brownian motion using the same parameter values as under the first test’s null, or this test’s alternative hypothesis.

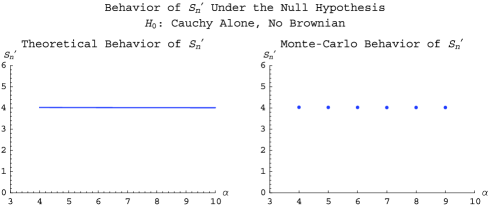

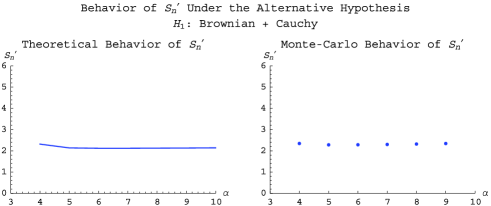

Under the null, the model is driven exclusively by the Cauchy process. Figure 6 shows the limiting value of under as a function of the truncation level comparing the theoretical limit of given in Theorem 4 (left graph) and the corresponding average value of from the Monte Carlo simulations (right graph). Figure 7 shows the corresponding values under the alternative hypothesis, where the increments of are now generated by a Brownian motion plus a Cauchy process. The theoretical limit on the left graph is computed from the expected values under the exact distribution of the increments at the sampling frequency rather than the -lim obtained in the limit where with the same remark about Jensen’s inequality applying here. We note that for small truncation levels () the interaction of the Brownian and the stable processes is material, driving the actual limit above If desired, small sample corrections for this interaction can be implemented along the same lines as in Section 5 of yacjacod09b .

The test statistic in simulations under the alternative appears to be slightly biased upwards. Quite naturally, this effect worsens as the pure jump process gets closer to a Brownian motion (for instance if instead of or ), and/or when the scale parameter of the jump process increases since that makes isolating the effect of the Brownian motion component of the model relatively more difficult.

Generally speaking, is, under its alternative, more finicky than is under either its null or alternative. The reason for this is that requires under a Goldilocks-like conjunction of factors whereby the Brownian motion component of the model is sufficiently large to drive the behavior of the ratio of truncated quadratic variations, while the jump component of the model cannot be so small as to render inaccurate the ratio of the number of increments larger than the truncation level.

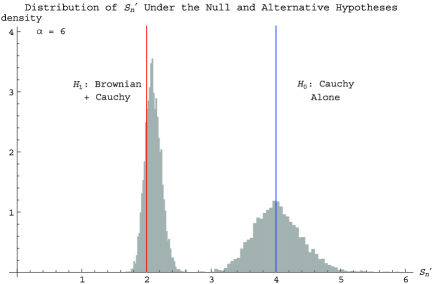

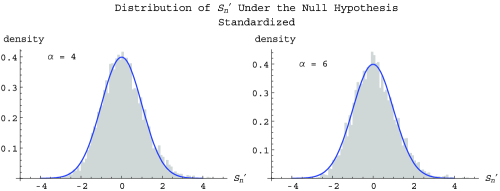

Figure 8 reports the Monte Carlo distributions of under and the vertical lines represent the theoretical limits. Under we note again that is slightly biased upwards. Fortunately, this bias is limited to so it does not adversely affect the implementation of the test per se, which is based on the behavior of under . But it can affect the interpretation of the results of the test implemented on real data, since, as we will see below, we will find empirical values of below . Figure 9 reports the Monte Carlo and asymptotic distribution of the statistic standardized under as prescribed by Theorem 5.

As said above, the histograms are computed using days (one month) sampled every five seconds. With this length of the series, the empirical distribution of the statistic is very well approximated by its asymptotic limit. Shorter time periods (such as day) tend to result in right-skewness of the Monte Carlo distribution of . We do not view the need for a longer series as a serious obstacle to the empirical implementation of the test since one would not typically expect the Brownian motion component of the model to be turned on or off on a daily basis: one would expect the market to operate in such a way that the Brownian component is either there all the time or not there at all. But if an answer is nevertheless desired on a day-by-day basis, then the first test can always be implemented, as it requires substantially shorter time spans.

=260pt Sample rejection rate (%) for truncation level Test theoretical level 10% 5%

5 Empirical results

In this section, we apply the two test statistics to real data, consisting of all transactions recorded during the year 2006 on two of the most actively traded stocks, Intel (INTC) and Microsoft (MSFT). The data source is the TAQ database. Using the correction variables in the dataset, we retain only transactions that are labeled “good trades” by the exchanges: regular trades that were not corrected, changed, or signified as cancelled or in error; and original trades which were later corrected, in which case the trade record contains the corrected data for the trade. Beyond that, no further adjustment to the raw data are made.

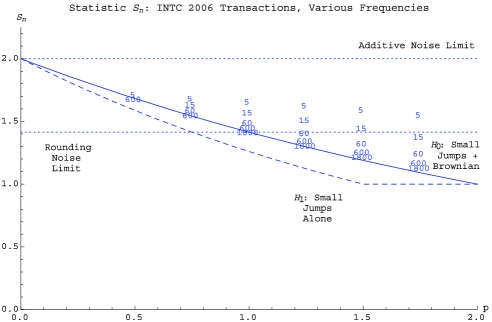

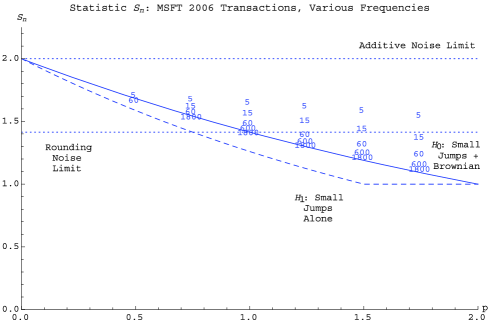

We first consider the test where the null hypothesis consists of a continuous component being present. Figures 10 and 11 show the values of the test statistic plotted for a range of values of the power for the two data series. The empirical values of are labeled on the plots with numbers representing the sampling interval employed, in seconds, with values ranging from seconds to minutes. In addition to the empirical estimates, the figures display the two limits of under the null where a Brownian is present and the alternative hypothesis where it is absent. The theoretical limits correspond to those given in Figures 2 and 3, except that the theoretical limit under (no Brownian present) is plotted for a value of , in line with the estimates of given in yacjacod09b for these data series. Quite naturally, the closer is to the closer the jump component can mimic the behavior of a Brownian motion and the harder it becomes to tell the two hypotheses apart. The limit under is independent of Also on the figures are the two limits corresponding to the situation where market microstructure noise dominates. We include the two polar cases where the noise is either of a pure additive form or of a pure rounding form.

When the observations are blurred with either an additive white noise or with noise due to rounding, the respective limits are then and . Indeed, suppose that instead of observing the exact value of we have on top of it an additive white noise, that is we observe (at stage , where the ’s are i.i.d., and independent of the process ). If we suppose that has a density which is continuous and nonvanishing at , then the noise is the leading factor in the behavior of as soon as [recall (17)]. In this case, the variables converge in probability to for some constant , and thus converges in probability to the sampling frequency ratio which is here. When the noise is pure rounding at some level , then again it is the leading factor and converges in probability to some positive limiting variable, as soon as and . Thus converges in probability to [when we have and then is not even well defined; however, here the truncation level used in practice is quite bigger than the rounding level of cent].

The values of are similar to those employed in simulations, and indexed in terms of standard deviations of the continuous martingale part of the log-price: we first estimate the volatility of the continuous part of using the small increments, those of order , and then use that estimate to form the cutoff level used in the construction of the test statistic. To account for potential time series variation in the volatility process , that procedure is implemented separately for each day and we compute the sum, for that day, of the absolute value of the increments that are smaller than the cutoff, to the appropriate power . For the full year, we then add the truncated power variations computed for each day.

The results in both Figures 10 and 11 tell a similar story. First, the empirical estimates are always on the side away from the limit under indicating that the null hypothesis of a Brownian motion present will not be rejected. Second, as the sampling frequency decreases, the empirical values get closer to the theoretical limit under For very high sampling frequencies, the results are consistent with some mixture of the noise driving the asymptotics. They then slowly settle down toward the limit corresponding to a null hypothesis of a Brownian present as the sampling frequency decreases, and the noise presumably becomes less of a factor.

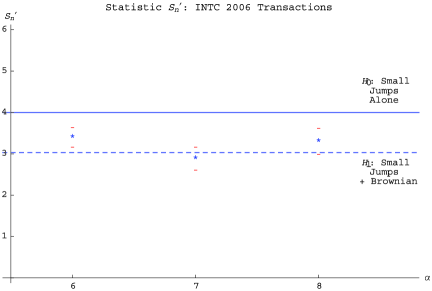

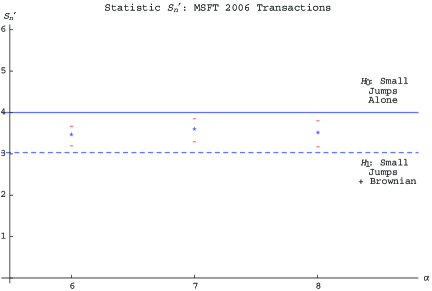

Next, we turn to the results of the second test on the same data series in Figures 12 and 13. The test statistic is implemented with with data sampled every seconds. The empirical estimates are represented by a star, with the vertical dashes representing a confidence interval. Also represented on the plots are the limits corresponding to (no Brownian) and (Brownian present). The theoretical limits correspond to those given in Figures 6 and 7, except that the theoretical limit under is plotted for a value of for the same reason as above. We find that the empirical estimates tend to be lower than the value specified by which leads to a rejection of the null hypothesis of no Brownian motion. The estimates are, however, generally higher than their expected value under consistent with the upward bias identified in simulations, the bias being more pronounced when gets closer to .

To summarize, the answer from both tests appears consistent with the presence of a continuous component in the data: using we do not reject the null of a Brownian motion present, while using we reject the null of its absence.

6 Technical results

By a standard localization procedure, we can replace the local boundedness hypotheses in our assumptions by a boundedness assumption, and also assume that the process itself, and thus the jump process , are bounded as well. That is, for all results which need Assumption 1 we may assume further that, for some constant ,

| (37) |

When we need Assumption 2 we may assume the above, together with

| (38) |

We call these reinforced Assumptions 1 or 2, and they are assumed in all the sequels instead of mere Assumptions 1 or 2, according to the case.

Recall that if , we have (7) with bounded as well. Otherwise the decomposition (7) is no longer valid, but under reinforced Assumption 1 we can always write

| (39) |

where defines a bounded process, and is a purely discontinuous martingale.

Also, below denotes a constant which may change from line to line and may depend on above.

The key to all results is clearly the behavior of the processes and . For establishing this behavior, it is convenient to introduce a few auxiliary processes, for an arbitrary cut-off level and an arbitrary process

| (40) |

6.1 Central limit theorems for the auxiliary processes

This subsection is devoted to recalling or proving some limit theorems for and for the auxiliary processes introduced in (40). First, we recall from Theorem 2.4 of jacod08 that under Assumption 1 (and even much more generally),

| (41) |

[the last property is proved when with and , but the proof works as well when (17) holds].

Lemma 1.

Suppose that is continuous, and let and and . Under Assumption 2 the two-dimensional variables

| (42) | |||

stably converge in law to a limit which is defined on an extension of and which, conditionally on , is a centered Gaussian variable with variance–covariance matrix given by

| (43) |

(The same would hold if , under the additional assumption that is bounded away from .)

Proof of Lemma 1 We can assume reinforced Assumption 2. The result will follow from Theorem 7.1 of jacodsemstat . Assumption (H) in that paper is slightly more restrictive than reinforced Assumption 2, but a close look at the proof yields that this theorem still holds in the present situation.

We apply the quoted Theorem 7.1 to the two-dimensional function on whose components are and . This function is with derivatives having polynomial growth. With the notation of that paper, variable (1) with the nontruncated variations is equal to , where

| (44) |

and is a remainder term with second component equal to , and with first component

| (45) |

By (37) we have , and hence, since there are at most summands in the definition of , we deduce that . On the other hand, the aforementioned result yields that converges stably in law to a limiting variable, which is exactly as described in the statement of the lemma.

Lemma 2.

Let , and suppose Assumption 1 and and . Then

| (46) |

Moreover, if the four-dimensional variables

| (47) |

stably converge in law to a limit which is defined on an extension of and which, conditionally on , is a centered Gaussian variable with variance–covariance matrix , where is the matrix

| (48) |

Assumption 1 here implies Assumption 6 of yacjacod08 , with the same and , and with there substituted with any number in here. Then all statements concerning are in Proposition 5 of that paper. However, we must redo the proof to obtain the joint convergence for the processes and .

Let and be the predictable compensators of and , and and . Observe that and by Assumption 1. Therefore, exactly as in the paper (and (C.23) and (C.24) in it), we see that if ,

| (49) |

The processes and are martingales, and if the brackets are given by the following formulas:

This, applied with equal to or or , and combined with the first part of (49), yield that the bracket matrix at time of the -dimensional continuous martingale converges to in probability, where is given by (48). Then as in Proposition 5 of yacjacod08 one deduces that converges stably in law to the limit described in the statement of the lemma. It remains to deduce from the second part of (49) that the difference between and the variable defined by (47) goes to in probability.

6.2 The behavior of

In this subsection we establish the behavior of for the relevant values of and for the cases not covered by (41). This is done in several lemmas.

We first observe that converges in probability to for any fixed such that . Hence there is a sequence such that converges in probability to . On the one hand as soon as . On the other hand we have as . Then the result follows.

We consider decomposition (39). In view of (41), it is enough to prove that under the conditions of the lemma we have

| (52) |

The left-hand side above is , where

With when and otherwise, we have the following inequalities, for all :

| (53) | |||

where we have used the inequality when and when . In view of (37), we have the estimates

| (54) |

(the first estimate is obvious and the second one follows from Burkholder–Davis–Gundy inequality; the third one follows from (6.25) of jacodsemstat applied to the process and with , which goes to by (17), and with as above). Then, using Hölder’s inequality and when , we deduce from (6.2) applied with and from that

We have by (17), hence , as soon as , or and . Since is arbitrary in , we deduce the result.

Lemma 5.

The proof of this lemma is similar to that of the previous one. The left-hand side of (55) is , where

Then (6.2) holds with instead of , whereas (54) is replaced by

| (56) |

(we now use (6.26) of jacodsemstat applied with and as above). Hence, using (6.2) for the pair , plus the fact that for and Hölder’s inequality, we deduce that for all and and , and with as in the previous proof,

where and and and . Since we have for large enough. When and , we have and and , and (55) will follow from for and also for when . We have because . When we have . When then if , and when we have and as soon as . So (55) is proved.

The previous lemma essentially gives the behavior of when the leading term is due to the continuous martingale part of . When this part vanishes, we have another type of behavior, which we describe now.

Lemma 6.

Let , and assume reinforced Assumption 1. {longlist}[(ii)]

If and (17) holds with we have

| (57) |

If and (17) holds with , and if , we have

| (58) |

Since the variables are the same on the set when they are computed on the basis of or on the basis of the process , it is no restriction to assume that identically.

The proof is based on the result of yacjacod08 , when identically. We have Assumption 7 of that paper with and and thus . We can then apply Lemmas 8 of that paper with the version of given at the end of Lemma 7 (because here), to obtain that for and if and for any ,

| (59) |

where

Clearly, (57) follows from (59), as soon as we can choose such that for all : this is obvious when and .

As for (58), it will also follow from (59) if we can choose as above, such that for all . This property holds for because is assumed, and for because . For , and since and do not depend on and increases with , it is enough to consider the case . Then if we let decrease strictly to , we see that , whereas and increase to and to respectively, and these quantities are strictly bigger than if is strictly smaller than and . Now, recall that one should also have , which is possible if and only if . All these conditions on are ensured if .

6.3 The behavior of

The behavior of has been exhibited in yacjacod09b , including a central limit theorem. However, here we need a joint CLT, at least on the set , for the pair , and even for this pair jointly with the similar pair with the truncation levels . For this we will use Lemma 2, and we thus need to show that the difference is negligible, after a suitable normalization. To this effect, we use the contorted way of using the aforementioned CLT for , but knowing this result it seems the shortest route toward the desired joint CLT.

Lemma 7.

Assume reinforced Assumption 1. {longlist}[(ii)]

Under (17) we have

| (60) |

If moreover and and (17) holds with , then

| (61) |

In yacjacod09b the truncation level was set as . However, it is obvious that it works with any truncation level subject to (17), with the conditions on replaced by exactly the same conditions on . With this in view, (i) follows from Proposition 1 of that paper. The proof of (ii) is much more involved, and broken into several steps.

Step (1) We write as , where and for , with

In this step we prove

| (62) |

The left-hand side above is nonnegative, with expectation , which is smaller than (see the proof of Lemma 2). Since we deduce (62).

Step (2) Let us assume for a moment that we have

| (63) |

In Proposition 2 of yacjacod09b , and upon replacing by , it is proved that under our assumptions on , and , the sequence converges in law to a limiting variable which is centered. On the other hand, Lemma 2 yields that converges in law to a limiting variable which is also centered (and, indeed, has the same law as ).

Up to taking a subsequence, assume that the pair converges in law to a pair of variables which are centered, whereas . In view of (63) it follows that converges in law to . Therefore, since by construction we must have . Since is centered, we must have a.s. In other words, for any subsequence of which converges in law, the limit is a.s. , and by a subsequence principle it follows that the original sequence goes to in law, hence in probability; this obviously implies (61).

At this stage, we are left to prove (63) which will be implied by the following:

| (64) |

for a sequence .

We recall the property (B.12) of yacjacod08 : denoting by the successive jump times of occurring after (with any fixed ), we have . This implies

Since we have . Therefore, for proving (64) it remains to show that

| (65) |

Set

We have estimate (B.15) of yacjacod08 again, with and . Thus, since on the set the process is piecewise constant and with a single jump on the interval , and the size of this jump is bigger than , we deduce

| (66) |

for any choice of the sequence decreasing to .

Finally we use estimate (61) of yacjacod09b to obtain for all

| (67) |

Of course the left-hand side of (65) is smaller than times the sum of the left-hand sides of (66) and (67). Therefore, it remains to prove that we can choose the sequence and in such a way that for , where

We have by hypothesis. Upon taking for some , this amounts to showing that one can find and such that and and . The last condition is satisfied for large enough as soon as . Then it is easy to see that the choice of is possible if and only if .

6.4 Central limit theorems for and

The previous results allow us to derive joint CLTs for the processes and , as required for Theorems 2 and 5. For the first of these two theorems, we use the following proposition which follows from Lemmas 1 and 5:

Proposition 1.

6.5 Proof of the theorems

It remains to prove the main theorems, for which we can assume the reinforced assumptions if necessary, without restriction.

First, the consistency results (20) and (30) are obvious consequences of (51), (69) and (68), plus the facts that on and on .

Second, in order to prove Theorem 2 we use Proposition 1 which, upon using the “delta method,” shows that under the stated assumptions the variables converge stably in law, in restriction to , to a variable which conditionally on is centered Gaussian with variance

With given by (24), we have by (51), and the result readily follows.

In the same way, Proposition 2 yields that converges stably in law, in restriction to , to a variable which conditionally on is centered Gaussian with variance

If is given by (5), then in restriction to by (69) and (68). This finishes the proof of Theorem 5.

Finally, for both Theorems 3 and 6, the claims concerning the asymptotic level of the tests are trivial consequences of two central limit Theorems 2 and 5. It remains to prove that the asymptotic power is in both cases. By virtue of (20) and (30), this will follow from the next two properties, under the appropriate assumptions

| (70) |

The first of these properties follows from (69), and the second one follows from (41), (50) and (68).

Acknowledgments

We are very grateful to a referee and an Associate Editor for many helpful comments.

References

- (1) Abramowitz, M. and Stegun, I. A. (1972). Handbook of Mathematical Functions. Dover, New York.

- (2) Aït-Sahalia, Y. and Jacod, J. (2008). Fisher’s information for discretely sampled Lévy processes. Econometrica 76 727–761. \MR2433480

- (3) Aït-Sahalia, Y. and Jacod, J. (2008). Testing whether jumps have finite or infinite activity. Technical report, Princeton Univ. and Univ. de Paris-6.

- (4) Aït-Sahalia, Y. and Jacod, J. (2009). Estimating the degree of activity of jumps in high frequency financial data. Ann. Statist. 37 2202–2244. \MR2543690

- (5) Aït-Sahalia, Y. and Jacod, J. (2009). Testing for jumps in a discretely observed process. Ann. Statist. 37 184–222. \MR2488349

- (6) Ball, C. A. and Torous, W. N. (1983). A simplified jump process for common stock returns. Journal of Financial and Quantitative Analysis 18 53–65.

- (7) Bates, D. S. (1991). The crash of ’87: Was it expected? The evidence from options markets. Journal of Finance 46 1009–1044.

- (8) Carr, P., Geman, H., Madan, D. B. and Yor, M. (2002). The fine structure of asset returns: An empirical investigation. Journal of Business 75 305–332.

- (9) Carr, P. and Wu, L. (2003). The finite moment log stable process and option pricing. Journal of Finance 58 753–777.

- (10) Eberlein, E. and Keller, U. (1995). Hyperbolic distributions in finance. Bernoulli 1 281–299.

- (11) Jacod, J. (2007). Statistics and high frequency data: SEMSTAT Seminar. Technical report, Univ. de Paris-6.

- (12) Jacod, J. (2008). Asymptotic properties of realized power variations and related functionals of semimartingales. Stochastic Process. Appl. 118 517–559. \MR2394762

- (13) Jacod, J. and Shiryaev, A. N. (2003). Limit Theorems for Stochastic Processes, 2nd ed. Springer, New York. \MR1943877

- (14) Madan, D. B. and Seneta, E. (1990). The Variance Gamma (V.G.) model for share market returns. Journal of Business 63 511–524.

- (15) Mancini, C. (2001). Disentangling the jumps of the diffusion in a geometric jumping Brownian motion. Giornale dell’Istituto Italiano degli Attuari LXIV 19–47.

- (16) Merton, R. C. (1976). Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics 3 125–144.

- (17) Tauchen, G. T. and Todorov, V. (2009). Activity signature functions for high-frequency data analysis. Technical report, Duke Univ. \MR2558956