Revisiting Grüss’s inequality: covariance bounds, QDE but not QD copulas, and central moments

Martín Egozcue

Department of Economics, University of Montevideo,

Montevideo 11600, Uruguay,

and

Accounting and Finance Department, Norte Construcciones,

Punta del Este,

Maldonado 20100, Uruguay. E-mail: megozcue@correo.um.edu.uy

Luis Fuentes García

Departamento de Métodos Matemáticos e de Representación,

Escola Técnica Superior de Enxeñeiros de Camiños, Canais e Portos,

Universidade da Coruña, 15001 A Coruña, Spain. E-mail: lfuentes@udc.es

Wing-Keung Wong

Department of Economics and the Institute for Computational Mathematics,

Hong Kong Baptist University, Kowloon Tong, Hong Kong.

E-mail: awong@hkbu.edu.hk

Ričardas Zitikis111Corresponding author. Tel: 519-432-7370; Fax: 519-661-3813; E-mail: zitikis@stats.uwo.ca

Department of Statistical and Actuarial Sciences, University of Western Ontario, London, Ontario N6A 5B7, Canada. E-mail: zitikis@stats.uwo.ca

Abstract

Since the pioneering work of Gerhard Grüss dating back to 1935, Grüss’s inequality and, more generally, Grüss-type bounds for covariances have fascinated researchers and found numerous applications in areas such as economics, insurance, reliability, and, more generally, decision making under uncertainly. Grüss-type bounds for covariances have been established mainly under most general dependence structures, meaning no restrictions on the dependence structure between the two underlying random variables. Recent work in the area has revealed a potential for improving Grüss-type bounds, including the original Grüss’s bound, assuming dependence structures such as quadrant dependence (QD). In this paper we demonstrate that the relatively little explored notion of ‘quadrant dependence in expectation’ (QDE) is ideally suited in the context of bounding covariances, especially those that appear in the aforementioned areas of application. We explore this research avenue in detail, establish general Grüss-type bounds, and illustrate them with newly constructed examples of bivariate distributions, which are not QD but, nevertheless, are QDE. The examples rely on specially devised copulas. We supplement the examples with results concerning general copulas and their convex combinations. In the process of deriving Grüss-type bounds, we also establish new bounds for central moments, whose optimality is demonstrated.

Keywords and phrases: Grüss’s inequality, covariance bound, Hoeffding representation, Cuadras representation, quadrant dependence, quadrant dependence in expectation, copula, convex combination, Archimedean copula, Fréchet copula, Farlie-Gumbel-Morgenstern copula, central moments, Edmundson-Madansky bound.

1 Introduction

The covariance, say between two random variables and , has played pivotal roles in numerous areas such as economics, finance, insurance, statistics, and, more generally, in decision making under uncertainty. For details on specific applications with references to many works in the areas that have greatly influenced our current research, we refer to Broll et al. [1], Egozcue et al. [9], [10], Furman and Zitikis [14], [15], [16], Zitikis [38]. A number of mathematics problems, especially those related to the theory of functions, have also been successfully tackled with the aid of covariance-type considerations (see, e.g., Dragomir and Agarwal [5], Dragomir and Diamond [6], Furman and Zitikis [12], [13], Izumino and Pečarić [25], Izumino et al. [26]). Solutions to problems in these areas often rely on determining the sign of covariances as well as on establishing their lower and upper bounds.

The random variables and are often unobservable but are known to be transformations (also called distortions) of some observable random variables and ; that is, and for some functions . Consequently, the covariance becomes of interest. In a large number of applications, only one of the two random variables is distorted. In this paper we concentrate on this case, thus restricting ourselves to an in-depth analysis of the covariance

| (1.1) |

If compared to the more general covariance , this reduction of generality plays a significant role in providing us with additional technical tools, including the notion of ‘quadrant dependence in expectation’ (QDE) to be defined in Section 3 below, and thus in turn allows us to establish deeper results than those available in the literature under, say, the notion of quadrant dependence (QD). In applications where covariance (1.1) emerges, the distortion function might be, for example, a utility or value function (see, e.g., Broll et al. [1], Egozcue et al. [9], [10], and references therein), some insurance-premium loading function (see, e.g., Furman and Zitikis [14], [15], [16]; Sendov et al. [34], and references therein).

When estimating covariance (1.1), perhaps most naturally that comes first into our mind is the Cauchy-Schwarz inequality

| (1.2) |

where is the variance (i.e., ) of the random variable . Furthermore, assuming that there are finite intervals and such that and almost surely, from bound (1.2) we immediately obtain Grüss’s [23] inequality

| (1.3) |

(see, e.g., Zitikis [38] for details and references). Inequalities (1.2) and (1.3) hold irrespectively of the dependence structure between and , which implies that the inequalities also hold under the ‘worst possible’ dependence scenario, which is associated with the strongest dependence structure between and , arising when almost surely. It is under this scenario that the optimality of the Grüss’s bound has been established in the literature, and we refer to, e.g., Dragomir [4], [7], Mitrinović et al. [31], Steele [35], and Zitikis [38] for further notes, examples, and references on the topic.

When the random variables and are independent, which in particular happens when the underlying random variables and are such, then the covariance is zero. Hence, knowing how much and in what sense the random variables and are dependent plays a significant role when investigating the magnitude of the covariance and its sign, among other properties. This line of research has been advocated by Zitikis [38] and Egozcue et al. [9], who have employed the notion of quadrant dependence to be defined rigorously in Section 3 below.

We conclude this section with a guide through the rest of this paper. In Section 2, we first show how the assumption of bivariate normality leads, via the well-known Stein’s Lemma, towards a Grüss-type covariance bound. We then extend this bivariate normal case into the formulation of a general Grüss-type covariance bound, which we aim at establishing in various situations throughout the current paper. In Section 3, we recall definitions of QD and QDE and their counterparts for copulas, and also relate these notions of dependence to Grüss-type covariance bounds. In Section 3 we also establish general results concerning convex mixtures of negative quadrant dependent (NQD) and positive quadrant dependent (PQD) copulas that provide a basis for constructing bivariate distributions which are QDE but not QD. We devote Section 4 to constructing several illustrative examples of copulas which are QDE but not QD; as far as we are aware of, these examples are the first ones in the literature. In Section 5, we establish QDE-based Grüss-type bounds for covariance (1.1), discuss their optimality and highlight the importance of having tight bounds for central moments of random variables. We investigate the latter bounds in great detail in Section 6. Since the QDE notion of dependence also naturally leads towards regression-based considerations, in Section 7 we establish regression-based Grüss-type bounds for covariance (1.1).

2 Formulation of the problem

Applications often suggest models for but it may not be feasible to assume models for the pair because the distortion function may change depending on, say, investor, insurer, etc. For this reason it is desirable to separate the underlying stochastic model, which is based on , from the class of distortion functions .

Stein [36] noted that if the pair follows the bivariate normal distribution and the function is differentiable, then

| (2.1) |

This equation, frequently known as Stein’s Lemma, separates the dependence structure from the distortion function . For extensions and generalizations of this result, we refer to Furman and Zitikis [14], [15], [16], [17], and references therein. In particular, it has been observed that equation (2.1) is a direct consequence of the following one

| (2.2) |

which separates the dependence structure of from the distortion function but does not require the differentiability of .

Now we rewrite equation (2.2) in the form

| (2.3) |

which we call to be of the ‘Grüss form’ for reasons to be made clear below (Problem 2.1 below), where is the Pearson correlation coefficient between and , and is a ‘Grüss factor’ defined by

Note that the Grüss factor does not depend on the bivariate distribution of except that it depends on the cumulative distribution functions (cdf) and of the underlying random variables and , respectively, and also on the distortion function . By the Cauchy-Schwarz inequality, does not exceed the product of the standard deviations and , which do not exceed and , respectively, under what we call the ‘Grüss condition’:

-

•

There are two finite intervals and such that and almost surely.

Hence, under the Grüss condition, we have that does not exceed the right-hand side of bound (1.3), and we thus have that

| (2.4) |

Since does not exceed , bound (2.4) implies Grüss’s bound (1.3) irrespectively of the dependence structure between and . When these two random variables are independent, then the right-hand side of bound (1.3) is zero. This demonstrates the pivotal role of the dependence structure when sharpening Grüss’s bound.

Reflecting upon the notes above, we next put forward a general formulation of the problem that we shall tackle from various angles throughout this paper.

Problem 2.1

We are interested in establishing bounds of the form

| (2.5) |

where

-

•

is a ‘dependence coefficient’, which must be equal to when the random variables and are independent, and should not depend on the distortion function ;

-

•

is a ‘Grüss factor’, which should not depend on the dependence structure between and but may depend on and the cdf’s and of and , respectively.

Throughout the paper we assume that the distortion function is of bounded variation, meaning that it can be written as the difference of two non-decreasing functions . The corresponding function is defined by the equation . When is differentiable, then . Furthermore, we use for the indicator function of statement which is equal to when the statement is true and otherwise. Hence, in particular, for any random variable and any real number ,

is a random variable that takes on the value when and otherwise. We shall frequently view as a random function of . In our following considerations, we shall also use the sign-function, , which takes on three values: when , when , and when .

3 QD and QDE random variables and copulas

One of the most fundamental equations that we utilize in the present paper is the Cuadras-Hoeffding representation

| (3.1) |

of the covariance between the transformed random variables and . The representation has been established by Cuadras [2] assuming, naturally and necessarily, that the expectations of , , and are well-defined and finite. Covariance representation (3.1) generalizes the classical Hoeffding’s [24] representation established in the case and (see also Sen [33]). The importance of representation (3.1) in our context is that it achieves a separation of the dependence structure present in from the distortion functions and . Hence, in particular, the positive quadrant-dependence (definition follows) implies that , and the negative quadrant-dependence implies that . These are, of course, well-known facts (Lehmann [28]).

Definition 3.1 (Lehmann [28])

Two random variables and are positively (resp. negatively) quadrant dependent if (resp. ) for all . We abbreviate this as PQD (resp. NQD), and when it is not important to specify whether the two random variables are PQD or NQD, then we simply say that they are quadrant dependent (QD).

As a special case of representation (3.1) we have the following one:

| (3.2) |

Note that the inner integral on the right-hand side of equation (3.2) is equal to , and so representation (3.2) becomes

| (3.3) |

The integrand on the right-hand side of equation (3.3) is related to the following definition.

Definition 3.2 (Kowalczyk and Pleszczynska [27])

A random variable is positively (resp. negatively) quadrant dependent in expectation on a random variable if (resp. ) for all . We abbreviate this as is PQDE (resp. NQDE) on , and when it is not important to specify whether these two random variables are PQDE or NQDE, then we simply say that is quadrant dependent in expectation (QDE) on .

QDE is not a stronger notion than QD, which follows from the already noted but not explicitly written equation:

| (3.4) |

For discussions and hints on potential applications of this notion of dependence, we refer to Kowalczyk and Pleszczynska [27], Wright [37], and references therein. One would actually expect that QDE is a weaker notion than QD, which means that there must be pairs which are QDE (i.e., either NQDE or PQDE) but not QD (i.e, neither NQD nor PQD). Our search of the literature has not, however, revealed examples that would formally confirm this non-equivalence of QDE and QD. Hence, we next present general results pointing in the direction of non-equivalence, and we shall use them in Section 4 as our guide when constructing specific examples of bivariate distributions that are QDE but not QD.

The main tool that we are going to employ is the notion of copula, which is a surface defined on the square and such that is equal to , where and are the cdf’s of and , respectively. Hence, in particular, we have the equation

| (3.5) |

When the random variables and have uniform (marginal) distributions, then we denote them by and , respectively. In turn, we have the following reformulations of Definitions 3.1 and 3.2 in terms of the copula , which is connected to the bivariate distribution of via the equation

Namely, and are PQD (resp. NQD) if (resp. ) for all , and is PQDE (resp. NQDE) on if (resp. ) for all , where , that is (cf. equation (3.5)),

In general, we have the following QD and QDE definitions for copulas.

Definition 3.3

Copula is PQD (resp. NQD) if (resp. ) for all . The copula is QD if it is either NQD or PQD.

Definition 3.4

Copula is PQDE (resp. NQDE) if (resp. ) for all . The copula is QDE if it is either NQDE or PQDE.

Note 3.1

In Definition 3.4 it would be more precise to say that is PQDE (resp. NQDE) on if (resp. ) for all . Analogously, is QDE on if is either NQDE or PQDE on . We avoid this pedantry by always considering the ‘first variable’ to be (N/P)QDE on the ‘second variable’.

Hence, the problem that we are interested in at the moment is whether there are any copulas that are QDE (i.e., either NQDE or PQDE) but not QD (i.e, neither NQD nor PQD). The following two general theorems are fundamental in solving this problem, with illustrative examples provided in Section 4.

Theorem 3.1

Let and be NQD and PQD copulas, respectively. Denote their convex combination by with parameter . Suppose that the surface

| (3.6) |

is not constant on . Then there exist such that , , and , and such that the copula is:

-

•

NQD for ;

-

•

neither NQD nor PQD for ;

-

•

PQD for ;

-

•

NQDE if and only if (it could be that );

-

•

neither NQDE nor PQDE for (it could be that , in which case the interval is empty);

-

•

PQDE if and only if (it could be that ).

Proof. Let and . We have the following facts:

-

1.

and .

-

2.

(similarly ) is a closed subspace of . Namely, if for all and , then for all .

-

3.

(similarly ) is a connected space. Namely, if , then for any is a convex combination of and , and so it is NQD.

-

4.

and are closed intervals (it follows from 2 and 3).

-

5.

. We prove this by contradiction. Suppose that there exists . Then is NQD and PQD. This implies that for all . Hence, function (3.6) is equal to the constant ; a contradiction.

In view of the above facts we have that and with , and the first three statements of Theorem 3.1 follow. In a similar way, but working with the function

| (3.7) |

we establish the other three statements of Theorem 3.1. Note that NQD (PQD) implies NQDE (PQDE), and so we must have and . This completes the proof of Theorem 3.1.

Note 3.2

If we have , then there are values such that the copula is neither NQD nor PQD, but it is NQDE. Similarly, if we have , then there are values such that the copula is neither NQD nor PQD, but it is PQDE.

Theorem 3.2

Proof. We have that for all . Thus, the copula is both PQDE and NQDE. By the previous theorem, we have that . Since , and , we deduce that or . Consider these two cases separately: 1) if , then for any the copula is neither NQD nor PQD, but it is NQDE, and 2) if , then for any the copula is neither NQD nor PQD, but it is PQDE. This completes the proof of Theorem 3.2.

4 Examples of QDE copulas which are not QD

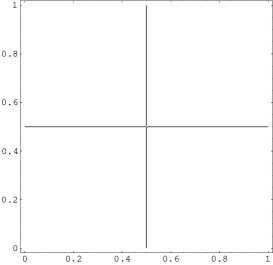

Here we give three examples of QDE copulas that are not QD. In the first two examples we choose NQD and PQD copulas such that their convex combinations are not QD but, nevertheless, are QDE. The third example is based on a copula which is not QD but, under an appropriate choice of marginal distributions, produces a bivariate distribution that is not QD but, nevertheless, is QDE. These three examples open up broad avenues for constructing QDE copulas that are not QD, using a myriad of existing copulas whose QD-type properties have been documented in the literature (e.g., Nelsen [32]). For discussions concerning copulas in the context of actuarial, financial, and other applications, we refer to, for example, Denuit et al. [3], Genest and Favre [18], Genest et al. [19], McNeil et al. [29], and references therein.

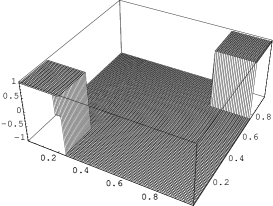

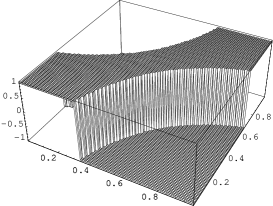

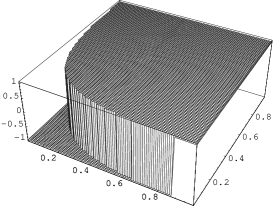

Example 4.1

The Fréchet lower-bound (FL) copula

is NQD, and the Fréchet upper-bound (FU) copula

is PQD. Both are defined on the unit square . Let be the convex combination of the two Fréchet copulas (cf. McNeil et al. [29]):

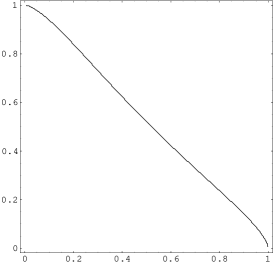

| (4.1) |

where . We see from Figure 4.1

that the copula is neither PQD nor NQD. To check whether is QDE (i.e., either PQDE or NQDE), we calculate the integral

| (4.2) |

Hence, for all if and only if , meaning that the copula is NQDE. Likewise, for all if and only if , meaning that is PQDE. Hence, for example, when , then is neither PQD nor NQD but it is NQDE. Likewise, when , then is neither PQD nor NQD but it is PQDE. This concludes Example 4.1.

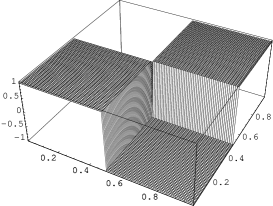

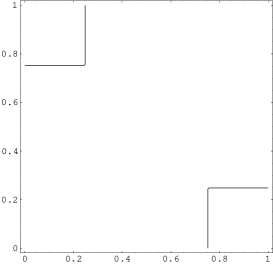

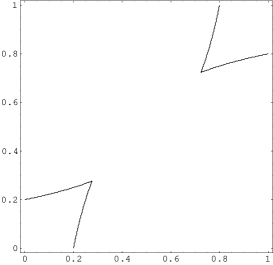

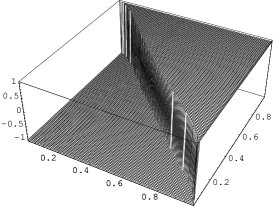

Example 4.2

Here we first choose the Farlie-Gumbel-Morgenstern (FGM) copula

with ; we set the parameter to throughout this example to make the FGM copula NQD. Next we choose the already noted Fréchet upper-bound copula , which is PQD. Let be a parameter, and let be the convex combination of the above two copulas:

| (4.3) |

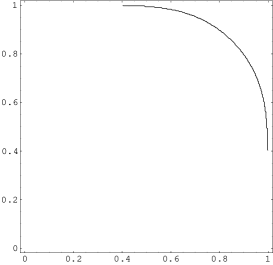

We have that

| (4.6) |

Hence, for only those that are between (cf. equation (4.6)) the zero-curve

from above, and the zero-curve

from below. We illustrate the two curves in Figure 4.2.

Note that the curves intersect in the interior of the square only when and touch each other at one point when . As to the PQDE or NQDE, we calculate the integral

| (4.7) |

Hence, for all meaning that is NQDE if and only if , and for all meaning that is PQDE if and only if . This concludes Example 4.2.

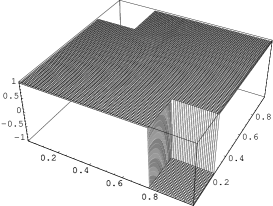

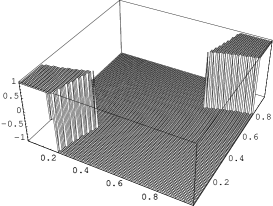

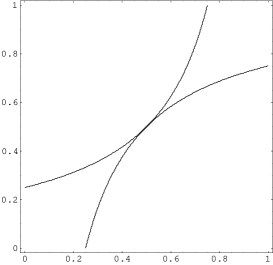

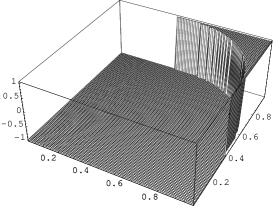

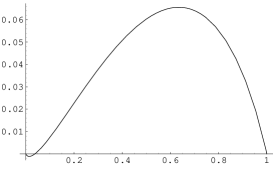

Example 4.3

We model the pair using the following Archimedean copula (Genest and MacKay [21], [22]; Genest and Ghoudi [20]; see also Nelsen [32] for additional information and references)

where is parameter. The copula is not QD. The zero-curve , which separates the NQD region from the PQD region, is given by

depicted in Figure 4.3.

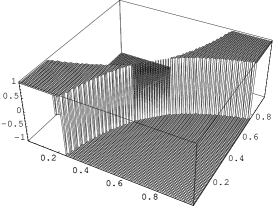

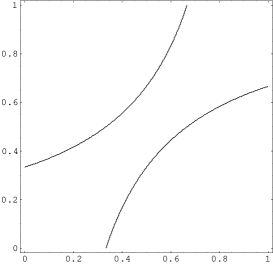

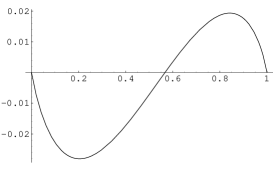

Concerning the QDE property, we want to know if and when the function defined by the formula

is positive or negative. Our experimental analysis has revealed that this function is negative for some and positive for other , and this applies to every . For an illustration, we have produced Figure 4.4.

This implies that for the purpose of constructing QDE pairs of random variables we cannot choose both marginal cdf’s uniform. Hence, we choose only the first marginal cdf (i.e., that of ) uniform. Since the second marginal cdf (i.e., that of ) cannot be uniform, nor any other continuous cdf, we construct a discrete cdf or, equivalently, a discrete random variable in such a way that is PQDE on .

First we note that, for every ,

-

•

is positive for some and negative for some other , thus violating the QD property.

To verify this non-QD property rigorously, we first rewrite the copula as with the notation

For every fixed and when , then we have . Thus, in a neighbourhood of . From this we deduce that when for some . In a neighbourhood of , we have that is equal to , which is a differentiable function. The partial derivative at the point is negative. Hence, the function is decreasing in a neghbourhood of . When , then we have and thus . Hence, the function or, equivalently, is positive in a neighbourhood to the left of . This establishes the property formulated under the bullet above.

Next, in view of the equation

| (4.8) |

we construct such that its support is in an interval and

-

•

for every , we have , thus assuring that the PQDE property holds, provided that takes only on values in the interval .

The construction of the aforementioned is as follows. We choose a set of points such that and . Define the cdf by the formula

where are real numbers. In other words, the random variable takes on the values with the probabilities . Note that the range of the cdf is the set . By construction, for all . Hence, in order to verify that for all real , we are only left to check that for , but this holds because and .

In summary, we have constructed a pair such that for all , that is, is PQDE on , but the pair is not QD, that is, it is neither PQD nor NQD. This concludes Example 4.3.

5 QDE-based Grüss-type covariance bounds

From the previous two sections we know that the set of QDE random pairs is larger than the set of QD pairs. In this sense, establishing Grüss-type covariance bounds under the QDE assumption would be an extension of those established under the QD assumption. We explore such QDE-based results in the current section. In what follows, we use the notation

The next theorem, whose proof is a consequence of equation (3.3), utilizes the QDE notion and establishes a sharper bound than Grüss’s original bound (1.3).

Theorem 5.1

For every pair such that , we have the bound

| (5.1) |

where the QDE-based dependence coefficient is

with the supremum taken over all such that , that is, over the support of the random variable , and where the QDE-based Grüss factor is

Before discussing properties of the QDE-based dependence coefficient and Grüss’s factor, we first show that bound (5.1) implies Grüss’s bound (1.3).

Statement 5.1

Proof. Since , we only need to show that

| (5.2) |

Since does not exceed and is equal to outside the support of , and since almost surely, we have that does not exceed . Furthermore, since almost surely, then (see, e.g., Zitikis [38], p. 16) does not exceed . Hence, bound (5.2) holds.

The dependence coefficient is always in the interval . It takes on the value when and are independent. Furthermore, the coefficient achieves its upper bound , as seen from the following statement.

Statement 5.2

The dependence coefficient achieves its upper bound .

Proof. Given , let be the random variable defined by the equation

where

-

•

the number is any but fixed, and

-

•

the random variable , independent of , takes on the two values with same probabilities .

The expectation is equal to . The absolute value is equal to . The covariance is equal to . Hence, .

The magnitude of the coefficient depends on the dependence structure between and , as well as on the marginal cdf’s of the two random variables. For example, in the case of independent and , we have . Less trivial and thus more interesting examples follow.

Example 5.1

Consider the convex combination of the lower and upper Fréchet copulas as defined by equation (4.1). Both and have uniform distributions on the interval , and thus

| (5.3) |

where the function is defined by

Furthermore, since with given by equation (4.2), we have that

| (5.4) |

Recall that . The QDE-based Grüss factor is

| (5.5) |

In the special case when and , we have that

| (5.6) | ||||

| (5.7) |

Bound (5.1) therefore implies that

| (5.8) |

whereas the exact calculation using, for example, the equation and formula (4.2) gives the value

| (5.9) |

This concludes Example 5.1.

Example 5.2

Consider the convex combination of the Farlie-Gumbel-Morgenstern and upper-Fréchet copulas as defined by equation (4.3). Just like in the previous example, both and have uniform distributions on the interval . Thus, equations (5.3) hold in the current case as well. The covariance is, however, different: it is equal to given by equation (4.7). Hence, the QDE-based dependence coefficient is

| (5.10) |

Recall that . Note that the QDE-based Grüss factor is unaffected by the change of the dependence structure and therefore has the same expression as in previous Example 5.1 (see eq. (5.5)). In the special case when , from the above formulas we have that

| (5.11) |

Bound (5.1) therefore implies that

| (5.12) |

whereas the exact calculation using the equation and formula (4.7) gives the value

| (5.13) |

This concludes Example 5.2.

6 Estimating the QDE-based Grüss factor

In Example 5.1 we calculated the QDE-based Grüss factor in the case of uniform random variables and . In Statement 5.1 we estimated under the Grüss condition on and . In the current section we develop general results that aid in establishing tight upper bounds for the QDE-based (general) Grüss factor . Specifically, upon expressing the quantities and by the formulas

and

where the mean , the cdf of , and the function

we see that estimating relies on tight bounds for the central moment as well as on the function . Interestingly, as we shall see from Theorem 6.1 below, which is the main result of this section, tight upper bounds for the central moment also crucially rely on the function .

Theorem 6.1

Let be a random variable with support in . Then, for every , we have that

| (6.1) |

Consequently, with the notation , we have that

| (6.2) |

Furthermore, when , we have that

| (6.3) |

The maximum of the function is achieved at a unique point in the interval and thus, by symmetry, also at the point in the interval . The point is such that, when ,

| (6.4) |

Note 6.1

Note 6.2

When , then , which plays a crucial role in deriving the Grüss bound. Formulas for for the integers are given in Table 6.1

along with the corresponding values of . By symmetry, the maximum is also achieved at the point . However, throughout this paper we use to denote the only existing point in the interval such that

(We refer to the proof of Theorem 6.1 for the existence and uniqueness of .) When becomes large, expressions for and become unwieldy, due to the fact that is a certain solution to a polynomial equation of a high degree, for which explicit solutions are not known to the best of our knowledge. For this reason, in Table 6.1 we have provided only numerical values of and for the integers .

Note 6.3

We next present a few results under additional assumptions on . For example, if we have more precise information about the location of the mean than just (see, e.g., Zitikis [38] for a related discussion), then the following corollary to Theorem 6.1 holds.

Corollary 6.1

Let be a random variable with support in , and let be a sub-interval of such that . Then for every we have that

| (6.8) |

Proof. Bound (6.8) follows from equation (6.10) and the bound (cf. bound (6.1))

where

This concludes the proof of Corollary 6.1.

In some situations the random variable might be symmetric, in which case we have the following proposition.

Proposition 6.1

Let be symmetric with support in . Then, for every ,

| (6.9) |

Proof. Denote . The random variable has support in and its mean is . Hence,

| (6.10) |

Since is symmetric (around its mean ), and the mean is in the interval , we have that does not exceed . Hence, the right-hand side of equation (6.10) does not exceed . This concludes the proof of Proposition 6.1.

Proof of Theorem 6.1. Edmundson [11] proved that if is a convex function and is a random variable with support in , then

| (6.11) |

where is the mean of . This result was subsequently extended by Madansky [30] and is nowadays known as the Edmundson-Madansky inequality. Since the function is convex for every , the Edmundson-Madansky inequality gives bound (6.1). Bound (6.2) follows trivially. Statement (6.3) follows from the fact that and the bound

| (6.12) |

which holds for every as we shall next prove. We start with the upper bound and show that, for every ,

| (6.13) |

Since , we only need to check bound (6.13) for . With the notation we have that

On the interval , the function achieves its maximum at the point , and so we have that

| (6.14) |

On the other hand, the function is increasing on the interval , and so it achieves its maximum at the point , thus giving the bound

| (6.15) |

To establish the lower bound of (6.12), we first note that , and thus . Since the function achieves its maximum on the interval at the point , bound implies the lower bound of (6.13). This completes the proof of the two bounds of (6.12).

To prove that when , we show that

| (6.16) |

where is defined by equation (6.7). The lower bound of (6.16) is obvious when . Hence, from now on we consider the case . We want to find those that maximize the function . We check that holds if and only if

| (6.17) |

The left-hand side of equation (6.17) is non-negative for all , whereas the right-hand side is non-negative only when . This implies that if we find a point such that the function is maximized, then the point must be such that , thus implying the left-hand bound of (6.16).

Both sides of equation (6.17) are increasing functions on the interval . Both sides are equal to at the end point . Hence, the existence and uniqueness of is equivalent to showing that the two functions intersect only once on the interval , but if they do not intersect, then we have . We determine this by checking if the ratio

| (6.18) |

crosses the horizontal line only once, provided that it crosses at all. Note that and . Furthermore, the derivative is always positive on the interval when . Hence, the function achieves its maximum at the end point , implying that when . When , then the derivative is positive on , negative on , and vanishes at , where

| (6.19) |

Since and , we therefore conclude that when , then the function is increasing on the interval with the initial value , and then, once it reaches its maximum at the point , becomes decreasing on the interval with the final value . Since the final value is , we conclude that the function has crossed the horizontal line exactly once. The crossing point is because it maximizes the function . This proves Theorem 6.1.

7 Regression-based covariance bounds

In this section, we look at the covariance from a slightly different angle. First, we write the equation

| (7.1) |

where

which is the centered regression function. The right-hand side of equation (7.1) complicates the problem by introducing an additional distortion function but it also simplifies the problem by reducing the pair to . Nevertheless, the following theorem, whose proof is based on an application of Hölder’s inequality on the right-hand side of equation (7.1), offers a sharper bound than Grüss’s bound (1.3) by utilizing a regression-based dependence coefficient

We shall discuss properties of the coefficient later in this section.

Theorem 7.1

For every pair such that , we have the bound

| (7.2) |

where

| (7.3) |

is the regression-based Grüss factor of the bound.

Statement 7.1

Proof. Since , we only need to show that

| (7.4) |

Since almost surely, then (see, e.g., Zitikis [38], p. 16) does not exceed . Likewise, when almost surely, then does not exceed . Bound (7.4) follows.

We next discuss properties of the regression-based dependence coefficient . Note first that the coefficient is always in the interval . Furthermore, when and are independent, then , and when almost surely, then .

When the pair follows the bivariate normal distribution, then the centered regression function takes on the form

| (7.5) |

and we therefore have the equation

In particular, when , since and , we have that the regression-based dependence coefficient is equal to the Pearson correlation coefficient . Furthermore, an application of equation (7.5) on the right-hand side of equation (7.1) gives equation (2.2), which, assuming that is differentiable, in turn gives equation (2.1).

Acknowledgements

The four authors have been supported by the research grant FRG1/10-11/012 from Hong Kong Baptist University (HKBU) under the title “The Covariance Sign of Transformed Random Variables with Applications to Economics, Finance and Insurance”. The authors also gratefully acknowledge their partial research support by the Agencia Nacional de Investigación e Innovación (ANII) of Uruguay, the Research Grants Council (RGC) of Hong Kong, and the Natural Sciences and Engineering Research Council (NSERC) of Canada.

References

- [1] Broll, U., Egozcue, M., Wong, W.K. and Zitikis, R., Prospect theory, indifference curves, and hedging risks. Applied Mathematics Research Express 2010 (2010) 142–153.

- [2] Cuadras, C.M., On the covariance between functions. Journal of Multivariate Analysis 81 (2002) 19–27.

- [3] Denuit, M., Dhaene, J., Goovaerts, M. and Kaas, R., Actuarial Theory for Dependent Risks: Measures, Orders and Models. Wiley, Chichester, 2005.

- [4] Dragomir, S.S., A generalization of Grüss’s inequality in inner product spaces and applications. Journal of Mathematical Analysis and Applications 237 (1999) 74–82.

- [5] Dragomir, S.S. and Agarwal, R.P., Some inequalities and their application for estimating the moments of guessing mappings. Mathematical and Computer Modelling 34 (2001) 441–468.

- [6] Dragomir, S.S. and Diamond, N.T., A discrete Grüss type inequality and applications for the moments of random variables and guessing mappings. In: Stochastic Analysis and Applications. Vol. 3, Nova Science Publishers, New York, 2003, pp. 21–35.

- [7] Dragomir, S.S., Advances in Inequalities of the Schwarz, Gr ss and Bessel Type in Inner Product Spaces. Nova Science, New York, 2005.

- [8] Egozcue, M., Fuentes Garcia, L., and Wong, W.K., On some covariance inequalities for monotonic and non-monotonic functions. Journal of Inequalities in Pure and Applied Mathematics 10, Article 75 (2009) 7 pages.

- [9] Egozcue, M., Fuentes García, L., Wong, W.K. and Zitikis, R., Grüss-type bounds for the covariance of transformed random variables. Journal of Inequalities and Applications 2010 (2010) Article ID 619423, 10 pages.

-

[10]

Egozcue, M., Fuentes García, L., Wong, W.K. and Zitikis, R.,

The covariance sign of transformed random variables with applications to economics and finance.

IMA Journal of Management Mathematics (2010), to appear. Available on-line at:

http://imaman.oxfordjournals.org/content/early/2010/09/07/imaman.dpq012 - [11] Edmundson, H.P., Bounds on the expectation of a convex function of a random variable. Technical report, The RAND Corporation, Paper P-982, Santa Monica, California, 1957.

- [12] Furman, E. and Zitikis, R., Monotonicity of ratios involving incomplete gamma functions with actuarial applications. Journal of Inequalities in Pure and Applied Mathematics 9 (2008), Article 61, 6 pages.

- [13] Furman, E. and Zitikis, R., A monotonicity property of the composition of regularized and inverted-regularized gamma functions with applications. Journal of Mathematical Analysis and Applications 348 (2008) 971–976.

- [14] Furman, E. and Zitikis, R., Weighted premium calculation principles. Insurance: Mathematics and Economics 42 (2008) 459–465.

- [15] Furman, E. and Zitikis, R., Weighted risk capital allocations. Insurance: Mathematics and Economics 43 (2008) 263–269.

- [16] Furman, E. and Zitikis, R., Weighted pricing functionals with applications to insurance: an overview. North American Actuarial Journal 13 (2009) 1–14.

- [17] Furman, E. and Zitikis, R., General Stein-type covariance decompositions with applications to insurance and finance. ASTIN Bulletin 40 (2010) 369–375.

- [18] Genest, C. and Favre, A.-C., Everything you always wanted to know about copula modeling but were afraid to ask. Journal of Hydrologic Engineering 12 (2007) 347–368.

- [19] Genest, C., Gendron, M. and Bourdeau-Brien, M., The advent of copulas in finance. European Journal of Finance 15 (2009) 609–618.

- [20] Genest, C. and Ghoudi, K., Une famille de lois bidimensionnelles insolite. Comptes Rendus de l’Académie des Sciences de Paris 318, Series I (1994) 351–354.

- [21] Genest, C. and MacKay, R.J., Copules archimédiennes et familles de lois bidimensionnelles dont les marges sont données. Canadian Journal of Statistics 14 (1986) 145–159.

- [22] Genest, C. and MacKay, R.J., The joy of copulas: bivariate distributions with uniform marginals. American Statistician 40 (1986) 280–283.

- [23] Grüss, G., Über das maximum des absoluten betrages von . Mathematische Zeitschrift 39 (1935) 215–226.

- [24] Hoeffding, W., Masstabinvariante korrelationstheorie, Schriften des Matematischen Instituts für Angewandte Matematik der Universität Berlin 5 (1940) 181–233.

- [25] Izumino, S. and Pečarić, J.E., Some extensions of Gruss’ inequality and its applications. Nihonkai Mathematical Journal 13 (2002) 159–166.

- [26] Izumino, S., Pečarić, J.E. and Tepeš, B., A Grüss-type inequality and its applications. Journal of Inequalities and Applications 2005 (2005) 277–288.

- [27] Kowalczyk, T. and Pleszczynska, E., Monotonic dependence functions of bivariate distributions. Annals of Statistics 5 (1977) 1221-1227.

- [28] Lehmann, E.L., Some concepts of dependence. Annals of Mathematical Statistics 37 (1966) 1137–1153.

- [29] McNeil, A.J., Frey, R. and Embrechts, P., Quantitative Risk Management: Concepts, Techniques, and Tools. Princeton University Press, Princeton, 2005.

- [30] Madansky, A., Bounds on the expectation of a convex function of a multivariate random variable. Annals of Mathematical Statistics 30 (1959) 743–746.

- [31] Mitrinović, D., Pečarić, J.E. and Fink, A.M., Classical and New Inequalities in Analysis, Kluwer, Dordrecht, 1993.

- [32] Nelsen, R.B., An Introduction to Copulas. (Second Edition.) Springer, New York, 2006.

- [33] Sen, P.K., The impact of Wassily Hoeffding’s research on nonparametric. In: Collected Works of Wassily Hoeffding, N.I. Fisher and P.K. Sen (eds.), Springer, New York, 1994, pp. 29–55.

- [34] Sendov, H.S., Wang, Y. and Zitikis, R., Log-supermodularity of weight functions and the loading monotonicity of weighted insurance premiums. Insurance: Mathematics and Economics (2010), under revision. Available at SSRN: http://ssrn.com/abstract=1660809; and also at arXiv: http://arxiv.org/abs/1008.3427

- [35] Steele, J.M., The Cauchy-Schwarz Master Class: An Introduction to the Art of Mathematical Inequalities. Cambridge University Press, Cambridge, 2004.

- [36] Stein, C.M., Estimation of the mean of a multivariate normal distribution. In: Proceedings of Prague Symposium on Asymptotic Statistics (ed. J. Hajek), pp. 345–381, Prague, Charles University, 1973.

- [37] Wright, R., Expectation dependence of random variables, with an application in portfolio theory. Theory and Decision 22 (1987) 111–124.

- [38] Zitikis, R., Grüss’s inequality, its probabilistics interpretation, and a sharper bound. Journal of Mathematical Inequalities 3 (2009) 15–20.