2 Asymptotic portfolio loss ordering

To compare stochastic risk models with respect to extreme portfolio losses,

we introduce the asymptotic portfolio loss order .

This order relation is designed for the analysis of the asymptotic

diversification effects and the identification of models that generate

portfolio risks with stronger extremal behaviour.

Before stating the definition, some basic notation is needed.

Focusing on risks, let be a random loss vector with values in

, i.e., let positive values of the components , ,

represent losses and let negative values of represent gains

of some risky assets.

Following the intuition of diversifying a unit capital over several assets,

we restrict the set of portfolios to the unit simplex in :

|

|

|

The portfolio loss resulting from a random vector and the portfolio

is given by the scalar product of and .

In the sequel it will be denoted by .

Definition 2.1.

Let and be -dimensional random vectors.

Then is called smaller than in

asymptotic portfolio loss order, ,

if

|

|

|

(1) |

Here, is defined to be 1.

The ordering statement means that for all portfolios

the portfolio loss is asymptotically smaller .

Thus concerns only the extreme portfolio losses.

In consequence, this order relation is weaker than the (usual)

stochastic ordering of the portfolio losses:

|

|

|

(3) |

Here, for real random variables , the stochastic ordering

is defined by

|

|

|

(4) |

Some related, well-known stochastic orderings

(cf. Müller and Stoyan, 2002; Shaked and Shanthikumar, 1997)

are collected in the following list. Remind that

is called supermodular if

|

|

|

(5) |

Definition 2.3.

Let , be random vectors in . Then is said to be smaller than in

-

(a)

(increasing) convex order,

(), if for all (increasing) convex functions such that the expectations exist;

-

(b)

linear convex order, , if

for all ;

-

(c)

positive linear convex order, ,

if for all ;

-

(d)

supermodular order , if

for all supermodular functions such

that the expectations exist;

-

(e)

directionally convex order, , if

for all directionally convex, i.e., supermodular and componentwise convex functions

such that the expectations exist.

The stochastic orderings listed in Definition 2.3 are useful

for describing the risk induced by larger diffusion (convex risk) as well as

the risk induced by positive dependence

(supermodular and directionally convex).

The following implications are known to hold generally for random

vectors , in :

-

(a)

-

(b)

-

(c)

The following proposition helps to establish sufficient criteria

for in the univariate case.

To obtain multivariate results,

it can be separately applied to each portfolio loss for

.

Proposition 2.5.

Let , be real random variables and let be a real random variable independent of , .

-

(a)

If and

for some constant , then

|

|

|

(6) |

-

(b)

If , then

|

|

|

(7) |

In addition, if and are integrable and , then

|

|

|

(8) |

Moreover, if , then .

Part (a).

Since is trivial for , we

assume that .

Hence implies for all

|

|

|

|

|

|

|

|

(9) |

where

|

|

|

An obvious consequence of (9) is the inequality

|

|

|

(10) |

Since is equivalent to ,

we obtain

|

|

|

Part (b).

By the well-known coupling principle for the stochastic ordering

we may assume without loss of generality that

pointwise on the underlying probability space.

This implies

|

|

|

and, similarly,

|

|

|

In consequence we obtain (7).

From the proof of (7) it follows that the distribution functions of the products , , satisfy the cut criterion of Karlin–Novikov

(cf. Shaked and Shanthikumar, 1994, Theorem 2.A.17 and

Müller and Stoyan, 2002, Theorem 1.5.17)

Hence we obtain

|

|

|

(11) |

If , then and therefore

|

|

|

(12) |

An important class of stochastic models with various applications are

elliptical distributions,

which are natural generalizations of multivariate

normal distributions.

A random vector is called elliptically distributed,

if there exist and a matrix such that

has a representation of the form

|

|

|

(14) |

where is uniformly distributed on the Euclidean unit sphere ,

|

|

|

and is a non-negative random variable independent of .

By definition we have

|

|

|

(15) |

and in this case

|

|

|

(16) |

The matrix is unique except for a constant factor and

is also called the generalized covariance matrix of .

We denote the elliptical distribution constructed

according to (14) by ,

where is the distribution of .

A classical stochastic ordering result going back to

Anderson (1955) and Fefferman et al. (1972)

(cf. Tong, 1980, p. 70)

says that positive semidefinite ordering

of the generalized covariance matrices , defined as

|

|

|

(17) |

implies symmetric convex ordering if

the location parameter and the distribution of the radial

factor are fixed:

|

|

|

(18) |

It is also known that for elliptical random vectors

the multivariate distribution function

is increasing in for , where (see, e.g., Joe, 1997, Theorem 2.21).

The following result is concerned

with the asymptotic portfolio loss ordering for elliptical

distributions.

Theorem 2.7.

Let , be elliptically distributed

with generalized covariances . If

|

|

|

(19) |

and

|

|

|

(20) |

then

|

|

|

(21) |

Proof.

It suffices to show that for an

arbitrary portfolio .

Furthermore, without loss of generality we can assume .

For and denote

|

|

|

and

|

|

|

Then, by definition of elliptical distributions, we have

|

|

|

(22) |

Since the vectors have unit length by construction,

the random variables are orthogonal projections of

on vectors of unit length.

Symmetry arguments yield that the distribution of is independent of

and that .

Thus we have

|

|

|

with .

By assumption we have and .

Applying Proposition 2.5(a)

we obtain .

3 Multivariate regular variation: in terms of spectral measures

This section is concerned with the characterization of the asymptotic

portfolio loss order in the framework of multivariate regular

variation. The results obtained here highlight the influence of the tail

index and the spectral measure on ,

with primary focus put on dependence structures captured by .

It is shown that corresponds to a family of order relations

on the set of canonical spectral measures and that these order relations

are intimately related to the extreme risk index introduced

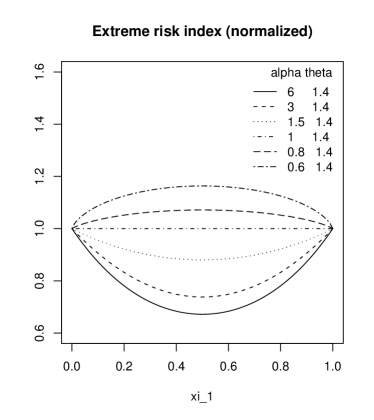

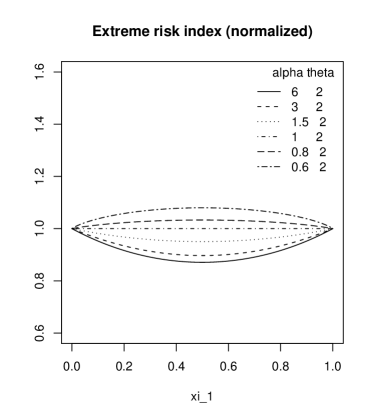

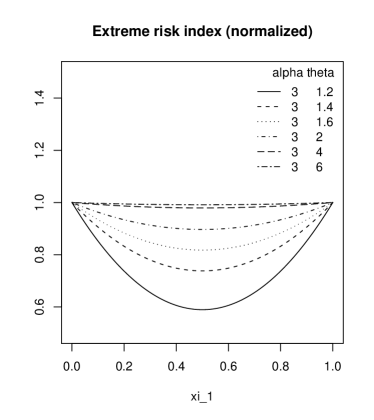

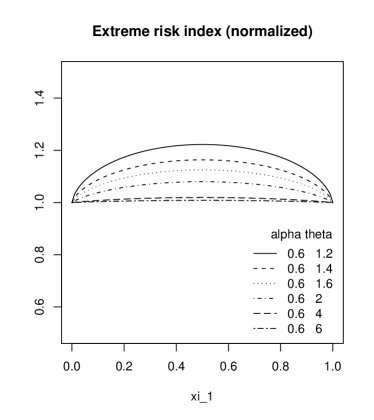

in Mainik and Rüschendorf (2010) and Mainik (2010).

The main result of this section is stated in Theorem 3.6,

providing criteria for in terms of componentwise ordering

for

and ordering of canonical spectral measures.

A particular consequence of these criteria is the

characterization of the dependence structures that

yield the best and the worst possible diversification effects for

random vectors in

(cf. Theorem 3.7 and Corollary 3.8).

Another application concerns elliptical distributions. Combining

Theorem 3.6 with results on obtained in

Theorem 2.7, we obtain ordering of the corresponding

canonical spectral measures.

Recall the notions of regular variation.

In the univariate case it can be defined separately for the lower

and the upper tail of a random variable via (13).

A random vector taking values in is called

multivariate regularly varying with tail index

if there exist a sequence and a (non-zero) Radon measure on

the Borel -field

such that and,

as ,

|

|

|

(23) |

where denotes the

vague convergence of Radon measures

and is the probability distribution of

.

It should be noted that random vectors with non-negative components

yield limit measures that are concentrated on

.

Therefore multivariate regular variation in this special case can also

be defined by vague convergence on .

Many popular distribution models are multivariate regularly varying.

In particular, according to Hult and Lindskog (2002),

multivariate regular variation of an elliptical distribution

is equivalent to the regular variation of the

radial factor and the tail index is inherited from .

Other popular examples are obtained by endowing regularly varying margins

with an appropriate copula

Wüthrich (cf. 2003); Alink et al. (cf. 2004); Barbe et al. (cf. 2006)

For a full account of technical details related to the notion of

multivariate regular variation, vague convergence, and

the Borel -fields on the punctured spaces

and

the reader is referred to Resnick (2007).

It is well known that the limit measure obtained in (23)

is unique except for a constant factor, has a singularity in the origin

in the sense that

for any ,

and exhibits the scaling property

|

|

|

(24) |

for all sets that

are bounded away from .

It is also well known that (23) implies that the random variable

with an arbitrary norm on is

univariate regularly varying with tail index .

Moreover,

the sequence can always be chosen as

|

|

|

(25) |

where is the quantile function of . The resulting limit measure

is normalized on the set by

|

|

|

(26) |

Thus, after normalizing by (26),

the scaling relation (24) yields an equivalent rewriting of

the multivariate regular variation condition (23)

in terms of weak convergence:

|

|

|

(27) |

for ,

where is the restriction of to the set .

Additionally to (23)

it is assumed that the limit measure is

non-degenerate

in the

following sense:

|

|

|

(28) |

This assumption ensures that

all asset losses are relevant for the extremes of the portfolio loss

. If (28) is satisfied in the upper tail region, i.e., if

|

|

|

(29) |

then also characterizes the asymptotic distribution

of the componentwise maxima

with

by the limit relation

|

|

|

(30) |

for .

Therefore is called

exponent measure.

For more details concerning the asymptotic distributions of maxima

the reader is referred to Resnick (1987)

and de Haan and Ferreira (2006).

Another consequence of the scaling property (24) is the

product representation of in polar coordinates

|

|

|

with respect to an arbitrary norm on .

The induced

measure necessarily satisfies

|

|

|

(31) |

with the constant factor

|

|

|

the measure on defined by

|

|

|

(32) |

and a probability measure on the unit sphere

with respect to ,

|

|

|

The measure is called

spectral measure

of or .

Since the term “spectral measure” is already used in other areas,

is also referred to as

angular measure.

In the special case of -valued random vectors it

may be convenient to reduce the domain of to

.

Although the domain of the spectral measure depends on the

norm underlying the polar coordinates, the

representation (31) is norm-independent in the following sense:

if (31) holds for some norm , then it also holds for

any other norm that is equivalent to .

The tail index is the same and the spectral measure

on the unit sphere corresponding to

is obtained from by the following transformation:

|

|

|

Finally, it should be noted that multivariate regular variation of

the loss vector is intimately related with the univariate regular variation

of portfolio losses .

As shown in Basrak et al. (2002),

multivariate regular variation of

implies existence of a portfolio vector such that

is regularly varying with tail index and any

portfolio loss satisfies

|

|

|

(33) |

This means that all portfolio losses are either regularly

varying with tail index or asymptotically negligible

compared to .

Moreover, it is also worth a remark

that for -valued random vectors

the converse implication is true in the sense that (33)

and univariate regular variation of

imply multivariate regular variation of the random vector .

This sort of Cramér-Wold theorem was established in

Basrak et al. (2002) and Boman and Lindskog (2009).

Under the assumption of multivariate regular variation of

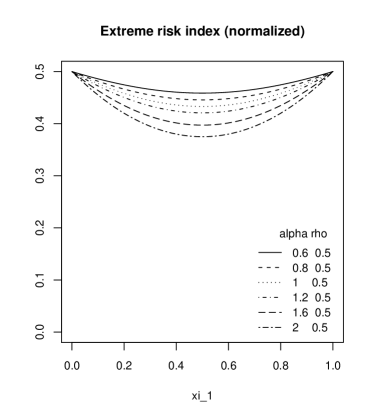

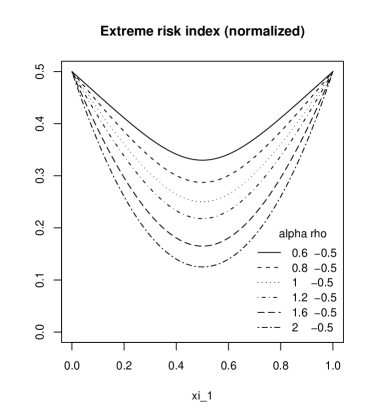

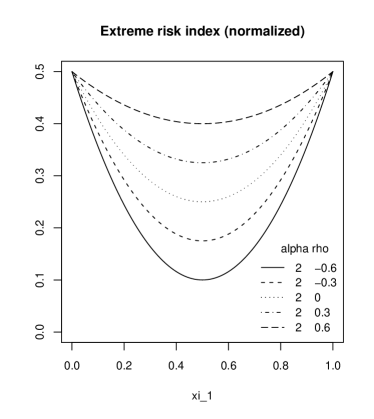

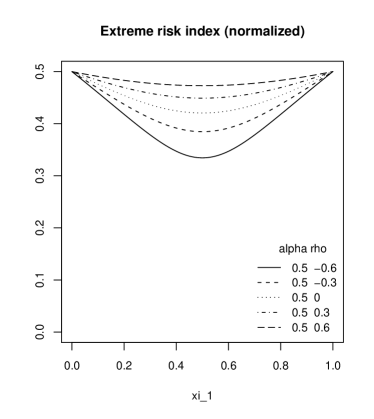

the extreme risk index

is defined as

|

|

|

(34) |

In Mainik and Rüschendorf (2010) the random vector is restricted to

and the portfolio vector is restricted to .

The general case with in and possible negative portfolio

weights, i.e., short positions, is considered in Mainik (2010).

Normalizing the exponent measure by (26),

one obtains

|

|

|

(35) |

Rewriting this representation in terms of the spectral measure

and the tail index yields

|

|

|

(36) |

Denoting the integrand by , we will write this representation

as .

The extreme risk index allows to compare the risk of different

portfolios. It is easy to see that (34) implies

|

|

|

(37) |

Thus, by construction,

ordering of the extreme risk index is related to the

asymptotic portfolio loss order .

However, designed for the comparison of different portfolio risks within one

model, the extreme risk index cannot be directly applied

to the comparison of different models.

The major problem is the standardization by in

(34). Indeed, since also depends on the

spectral measure of , criteria for in terms of

demand the specification of the limit

|

|

|

Another technical issue arises from the invariance of under

componentwise rescalings. Since the spectral measure does not exhibit

this property, ordering of spectral measures needs additional normalization

of margins that makes it consistent with . To solve these problems,

we use an alternative representation of in terms of the

so-called canonical spectral measure ,

which has standardized marginal weights.

This representation is closely related to the asymptotic risk aggregation

coefficient discussed by Barbe et al. (2006).

Furthermore, the link between the canonical spectral measure and

extreme value copulas

allows to transfer ordering results for copulas into the

setting. These results are presented in Section 4.

To reduce the problem to the essentials,

we start with the observation that is trivial for

multivariate regularly varying random vectors with different

tail indices and non-degenerate portfolio losses.

Proposition 3.1.

Let and be multivariate regularly varying on and assume that for all .

-

(a)

If

|

|

|

(38) |

then .

-

(b)

If , then .

Proof.

-

(a)

Using relation (34) we obtain

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-

(b)

Recall that multivariate regular variation of implies regular variation of with tail index . Analogously, is regularly varying with tail index . Finally, yields (38) and by (3.1) we obtain .

Thus the primary setting for studying the influence of dependence

structures on the ordering of extreme portfolio losses is the case of

random variables and with equal tail indices:

|

|

|

In the framework of multivariate regular variation, asymptotic dependence in the tail region

is characterized by the spectral measure or its canonical version .

The canonical exponent measure of is obtained from the exponent

measure as

|

|

|

with the transformation defined by

|

|

|

(39) |

where

|

|

|

(40) |

Furthermore, exhibits the scaling property

|

|

|

and, analogously to (31), has a product structure in polar

coordinates:

|

|

|

(41) |

The measure is the canonical spectral measure of .

Since and are invariant under componentwise rescalings,

the canonical spectral measure is more suitable for the

characterization of .

The following lemma provides a representation of the extreme risk index

in terms of . Note that the formulation makes use of

the componentwise product notation (2).

Proposition 3.2.

Let be multivariate regularly varying on with tail index

.

If satisfies the non-degeneracy condition (28),

then

|

|

|

(42) |

where denotes the canonical spectral measure of ,

the rescaling vector

is defined by

|

|

|

(43) |

and the function is defined as

|

|

|

(44) |

Proof.

Denote . Then, by definition of ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(45) |

It is easy to see that (40) implies

for and .

Consequently, (39) yields

|

|

|

(46) |

for and .

Applying (46) to (45), one obtains

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(47) |

Finally, consider the sets defined in (40).

It is easy to see that

|

|

|

Hence

|

|

|

|

|

|

|

|

() |

As already mentioned above, and are invariant under

rescaling of components.

Consequently, characterization of can be reduced to the case when the marginal weights in (42) are standardized by

|

|

|

(48) |

This condition will be referred to as the

balanced tails condition.

The following result shows that this condition significantly simplifies the representation (42).

Proposition 3.3.

Suppose that is multivariate regularly varying on with tail index

.

-

(a)

If has balanced tails in the sense of (48), then

|

|

|

(49) |

-

(b)

The non-degeneracy condition (28) is equivalent to

the existence of a vector

such that has balanced tails.

-

(c)

The extreme risk index of the rescaled vector obtained

in part (b) satisfies

|

|

|

(50) |

Proof.

Part (a).

Consider the integrand in the representation (42):

|

|

|

The balanced tails condition (48) implies that is

non-degenerate in the sense of (28).

Furthermore, all weights in the representation (42)

are equal:

|

|

|

|

|

|

|

|

Hence simplifies to

|

|

|

|

|

|

|

|

Part (b).

Suppose that satisfies (28). Then the sets defined in (40) satisfy for . Consequently, the random variables are regularly varying with tail index . Denoting

|

|

|

(51) |

one obtains

|

|

|

|

|

|

|

|

|

|

|

|

for . Hence, for any ,

|

|

|

|

To prove the inverse implication, suppose that has balanced tails

for some . Then the the exponent measure of

satisfies

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Since multivariate regular variation of implies for at least

one index , this yields for all .

Part (c). This is an immediate consequence of

part (a) and the invariance of canonical spectral measures

under componentwise rescaling.

Representation (49) suggests that ordering of

the normalized extreme risk indices

in the balanced tails setting can be considered

as an integral order relation

for canonical spectral measures with respect to the function class

|

|

|

(52) |

This justifies the following definition.

Definition 3.4.

Let and be canonical spectral measures on

and let .

Then the order relation is defined by

|

|

|

(53) |

The following theorem states that is in a certain sense

equivalent to the ordering of canonical spectral measures

and allows to reduce the verification of to the verification

of .

Some exemplary applications are given in Section 5.

Furthermore, given explicit representations of spectral measures or their

canonical versions,

this result allows to verify numerically, which is very

useful in practice.

Theorem 3.6.

Let and be multivariate regularly varying random vectors on with tail index and canonical spectral measures and . Further, suppose that and satisfy the balanced tails condition (48).

-

(a)

If ,

then implies .

-

(b)

If

and

,

then

is equivalent to .

Proof.

(a) Since has balanced tails, Proposition 3.3(a) yields

|

|

|

|

|

|

|

|

|

|

|

|

Analogously one obtains

|

|

|

Moreover, implies

|

|

|

(55) |

Consequently,

|

|

|

|

|

|

|

|

|

|

|

|

(56) |

|

|

|

|

due to (55) and .

(b)

By part (a), it suffices to show that

implies .

By assumption and have asymptotically equivalent tails,

|

|

|

Thus (56) yields

|

|

|

and implies .

The following result answers the question for dependence structures

corresponding to the best and the worst possible diversification effects

for multivariate regularly varying random vectors in .

According to Theorem 3.6, it suffices to find the upper and

the lower elements with respect to in the set

of all canonical spectral measures on .

It turns out that for

the best diversification effects are obtained in case of asymptotic

independence, i.e., the -maximal element is given by

|

|

|

(57) |

whereas the worst diversification effects are obtained in case of

the asymptotic comonotonicity, represented by

|

|

|

(58) |

For the situation is inverse.

Theorem 3.7.

Let be an arbitrary canonical spectral measure on and let

and be defined according to (57)

and (58). Then

-

(a)

for .

-

(b)

for .

Proof.

Let be multivariate regularly varying on with canonical spectral

measure . Without loss of generality we can assume that

satisfies the balanced tails condition (48).

Then, according to (49), we have

|

|

|

(59) |

Furthermore,

we have for .

Recall that the mapping is convex for

(cf. Mainik and Rüschendorf, 2010, Lemma 3.2).

Due to (59) this behaviour is inherited by the mapping

.

Thus for

we have for all ,

which exactly means for .

To complete the proof of part (a), note that

the normalization of canonical spectral measures yields

|

|

|

(60) |

Comparing the integrand on the right side of (60) with

the function ,

we see that

|

|

|

with

|

|

|

Thus it suffices to demonstrate that ,

which follows from , for , and

.

The inverse result for stated in (b)

follows from

the concavity of the mapping

and the inequality .

Due to Theorem 3.6, an analogue of the foregoing

result for is straightforward.

Corollary 3.8.

Let be multivariate regularly varying in with tail index

and identically

distributed margins , .

Further, let be a random vector with independent margins

, and let be a random vector with totally dependent

margins -a.s. and .

Then

-

(a)

for

-

(b)

for .

Combining Theorem 3.6 with Theorem 2.7, one obtains an

ordering result for the canonical spectral measures of multivariate regularly

varying elliptical distributions.

The notation is justified by the fact that

spectral measures of elliptical distributions depend only on the tail

index and the generalized covariance matrix .

An explicit representation of spectral densities for bivariate elliptical

distributions was obtained by Hult and Lindskog (2002).

Alternative representations that are valid for all dimensions

are given in Mainik (2010), Lemma 2.8.

Proposition 3.10.

Let and be -dimensional covariance matrices satisfying

|

|

|

(61) |

and

|

|

|

(62) |

Then

|

|

|

Proof.

Fix and consider random vectors

|

|

|

where and are square roots of the matrices and

in (62), i.e.,

|

|

|

and is an arbitrary regularly varying non-negative

random variable with tail index .

As a consequence of Theorem 2.7 one obtains .

Furthermore, invariance of under componentwise rescaling

yields for with

|

|

|

Moreover, as a particular consequence of arguments

underlying (22), one obtains

|

|

|

Hence the random vectors and satisfy the balanced tails condition (48), whereas their components are mutually ordered with respect to .

Finally, Theorem 3.6(b) and invariance of canonical spectral measures under componentwise rescalings yield

|

|

|

() |

The subsequent result extends Theorem 3.6 to random vectors that do not have balanced tails.

Theorem 3.11.

Let and be multivariate regularly varying random vectors on

with tail index

and canonical spectral measures and .

Further, assume that with

|

|

|

(63) |

for and that the vector defined by

|

|

|

(64) |

satisfies

|

|

|

(65) |

Then implies .

Proof.

According to Proposition 3.3(b), there exists

such that satisfies the balanced tails condition (48).

Furthermore, the tails of the random vector

|

|

|

with defined in (63) are also balanced. Indeed, it is easy to see that

|

|

|

for . Analogously one obtains

|

|

|

and, as a result,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

for . Hence the balanced tails condition for implies that the tails of are also balanced.

Furthermore, invariance of canonical spectral measures under

componentwise rescaling yields

|

|

|

Thus, applying Theorem 3.6(a), one obtains

|

|

|

(66) |

Since for ,

condition (66) is equivalent to

|

|

|

(67) |

Moreover, assumption (65) implies

|

|

|

(68) |

Combining this ordering statement

with (66) and (67),

one obtains

|

|

|

Finally,

invariance of with respect to componentwise rescaling yields

.

In the special case of random vectors in Theorem 3.11

can be simplified to the following result.

Corollary 3.12.

Let and be multivariate regularly varying random vectors on

with tail index and canonical

spectral measures and .

Further, suppose that

|

|

|

(69) |

Then implies .

Proof.

Assumption (69) yields that the rescaling vector

defined in (64) is an element of .

Thus and, since takes values in ,

we have

|

|

|

Similar arguments yield .

Hence condition (65) of Theorem 3.11 is satisfied.

The final result of this section is due to the indifference of

for mentioned in

Remark 3.5(a).

This special property of spectral measures on allows to reduce

to the ordering of components.

It should be noted that this result cannot be extended to the

general case of spectral measures on .

Lemma 3.13.

Let and be multivariate regularly varying on with tail

index .

Further, suppose that satisfies the non-degeneracy

condition (28) and that

for . Then .

Proof.

According to Proposition 3.3(b),

there exists such that satisfies the balanced tails

condition (48).

Furthermore, due to the invariance of under componentwise

rescaling, is equivalent to .

Thus it can be assumed without loss of generality that has balanced tails.

This yields

|

|

|

Hence the assumption for

implies for all .

Moreover, the balanced tails condition for yields

|

|

|

(70) |

Now consider the random vector and denote

|

|

|

Recall that

with

denoting the exponent

measure of and that is non-zero. This yields

even if does not satisfy the non-degeneracy condition (28).

Moreover, for , the mapping

is linear. This implies

|

|

|

(71) |

and (70) yields

|

|

|

(72) |

Hence

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

due to , (71), and (72).

4 Relations to convex and supermodular orders

As mentioned in Remark 2.4(b),

dependence orders ,

and convexity orders , ,

do not imply in general.

However, it turns out that the relationship between and

the ordering of canonical spectral measures by allows

to draw conclusions of this type

in the special case of multivariate regularly varying models.

The core result of this section is stated in Theorem 4.1.

It entails

a collection of sufficient

criteria for in terms of convex and supermodular order relations,

with particular interest paid to the

inversion of diversification effects for .

An application to copula based models is given in Proposition 4.4.

This approach was applied by Embrechts et al. (2009b)

to the ordering of risks for the portfolio vector

and for a specific family of multivariate

regularly varying models with identically distributed, non-negative margins

(cf. Example 5.2 in Section 5).

The next theorem is the core element of this section.

It generalizes the arguments of Embrechts et al. (2009b)

to multivariate regularly varying random vectors in with balanced

tails and tail index .

The case is not included for two reasons.

First, this case is partly trivial due to the indifference of

for spectral measures on (cf. Remark 3.5(a)).

Second, Karamata’s theorem used in the proof of the integrable case does not yield the desired result for random variables with tail index .

Theorem 4.1.

Let and be multivariate regularly varying on with identical

tail index . Further, assume that and satisfy

the balanced tails condition (48).

-

(a)

For let

|

|

|

(73) |

and let there exist such that with

|

|

|

(74) |

Then .

-

(b)

For suppose that and are

equivalent with respect to , i.e.,

|

|

|

(75) |

and let there exist such that with ,

|

|

|

(76) |

Then .

The proof will be given after some conclusions and remarks.

In particular, it should be noted that the relation between

and established in Theorem 3.6

immediately yields the following result.

Corollary 4.2.

-

(a)

If random vectors and satisfy conditions of Theorem 4.1(a),

then ;

-

(b)

If and satisfy conditions of Theorem 4.1(b),

then .

It should also be noted that

conditions (74) and (76) are asymptotic forms of

the increasing convex ordering

and the decreasing convex ordering ,

respectively.

The consequences can be outlined as follows.

Finally, a comment should be made upon

convex ordering of non-integrable random variables and

diversification for .

The so-called phase change at ,

i.e., the inversion of diversification effects

taking place when the tail index crosses this critical value,

demonstrates that the implications of convex ordering are essentially different

for integrable and non-integrable random variables.

Indeed, it is easy to see that if a random variable on

satisfies ,

then the only integrable convex functions of are the constant ones.

Moreover, if is restricted to and ,

then any integrable convex function of is necessarily non-increasing.

Proof of Theorem 4.1.(a)

Consider the expectations in (74).

It is easy to see that for

|

|

|

|

|

|

|

|

and, as a consequence,

|

|

|

Moreover, Proposition 3.3(a) implies

|

|

|

(77) |

and Karamata’s theorem

(cf. de Haan and Ferreira, 2006, Theorem B.1.5)

yields

|

|

|

As a result one obtains

|

|

|

and, analogously,

|

|

|

Hence (74) and (73) yield

|

|

|

|

|

|

|

|

|

|

|

|

for all , which exactly means

.

(b) Note that (75) implies

|

|

|

(78) |

and that (76) yields

|

|

|

(79) |

Furthermore, it is easy to see that any random variable in

satisfies

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This implies

|

|

|

Consequently, (79) yields

|

|

|

(80) |

where

|

|

|

|

|

|

|

|

with

|

|

|

Moreover, (78), (77), and an

analogue of (77) for yield

|

|

|

|

|

|

|

|

(81) |

Now suppose that is not satisfied,

i.e., there exists such that

.

Then (81) yields

for some and sufficiently large .

This implies

|

|

|

(82) |

for sufficiently large and all .

Moreover, regular variation of with tail index

implies .

Consequently, the integral on the right side of (82) tends to

infinity for :

|

|

|

Hence, choosing and sufficiently large, one can achieve

for any . In particular, and can be

chosen such that

|

|

|

which contradicts (80). Thus

cannot be true

and therefore it necessarily holds that .

Now let us return to the ordering criterion in terms of the supermodular

order stated in Remark 4.3. The invariance of

under non-decreasing component transformations

allows to transfer these criteria to copula models.

Furthermore, since we are interested in the ordering of the asymptotic

dependence structures represented by the canonical spectral measures,

and , we can take

any copulas that yield and as asymptotic

dependence structures.

A natural choice is given by the extreme value copulas, defined

as the copulas of simple max-stable distributions corresponding to

, i.e., the distributions

|

|

|

(83) |

where is the canonical exponent associated with

via (41). For further details on max-stable and simple max-stable

distributions we refer to Resnick (1987).

Since extreme value copulas and canonical spectral measures can be

considered as

alternative parametrizations of the same asymptotic dependence structures,

we obtain the following result.

Proposition 4.4.

Let and be canonical spectral measures on .

Further, for , let denote the copula of the

simple max-stable distribution induced by

according to (83) and (41).

Then implies

-

(a)

for ;

-

(b)

for .

Proof.

Let denote the canonical exponent measures corresponding

to and .

It is easy to see that the transformed measures

|

|

|

with and the transformation defined as

|

|

|

exhibit the scaling property with index :

|

|

|

|

Hence the transformed distributions

|

|

|

(84) |

are max-stable with exponent measures .

It is well known that max-stable distributions with identical heavy-tailed margins are multivariate regularly varying (cf. Resnick, 1987).

Moreover, the limit measure in the multivariate regular variation condition can be chosen equal to the exponential measure associated with the property of max-stability.

Consequently, the probability distributions for and are multivariate regularly varying with tail index and canonical spectral measures .

Furthermore, it is easy to see that and

have identical margins:

|

|

|

Moreover, due to the invariance of under non-decreasing marginal

transformations, implies

|

|

|

for all .

Thus an application of the ordering criteria from Remark 4.3

to and completes the proof.