Do price and volatility jump together?

Abstract

We consider a process , which is observed on a finite time interval , at discrete times This process is an Itô semimartingale with stochastic volatility . Assuming that has jumps on , we derive tests to decide whether the volatility process has jumps occurring simultaneously with the jumps of . There are two different families of tests for the two possible null hypotheses (common jumps or disjoint jumps). They have a prescribed asymptotic level as the mesh goes to . We show on some simulations that these tests perform reasonably well even in the finite sample case, and we also put them in use on S&P 500 index data.

doi:

10.1214/09-AAP654keywords:

[class=AMS] .keywords:

.and

1 Introduction.

Financial asset prices have two well-documented salient features: their volatility changes over time and their trajectories can exhibit large discontinuities. Both features have nontrivial implications for risk modeling and management as the underlying asset itself is no longer sufficient to span all the available risks in it and derivatives (written on it) are typically needed. Of central importance then becomes the relationship between the price jumps and volatility. For example, if the volatility is driven by a single (Markov) diffusion process, then one can separate the management of volatility and jump risks by using first at-the-money options for the former and then out-of-the-money options for the latter. But such a simple separate management of these two risks will obviously not work if the price jumps are associated with simultaneous discontinuous changes in the level of volatility. Empirical evidence in TT based on the behavior of close-to-maturity options written on the stock market index suggest that this indeed might be the case. And this is exactly what we try to investigate in this paper: are price jumps accompanied by jumps in volatility?

The link between price and volatility jumps is intrinsically associated with the observed path, and therefore we develop tests that are, as much as possible, independent from the underlying model. More specifically, we suppose that we have discrete observations from an arbitrary Itô semimartingale (typically the log-price) at times for where the time span will stay fixed and the length of the high-frequency intervals . Under such a sampling scheme, we propose tests that determine the common arrival, or not, of the price and volatility jumps on the discretely-observed path over .

The test statistics that we construct can be intuitively described as follows. First, we identify the high-frequency price increments containing jumps as those being higher in absolute value than a truncation level which goes to zero at a certain (known) rate. Then, for the set of identified jump times we construct left and right local volatility estimators from the neighboring high-frequency price increments. Our statistics are simple sums of certain functions of the identified jumps and the associated left and right volatility estimators. Then the tests we develop are based on the different limit behavior of these statistics on the sets of common and disjoint arrival of the price and volatility jumps.

While the results in the paper are derived for general functions measuring the distance between the left and right volatility, there is one specific choice which is particularly attractive for our testing purposes, and we use it in our applications. This function corresponds to the log-likelihood ratio test for deciding whether two independent samples of i.i.d. zero-mean normal variables have the same variance. The link with our analysis comes from the fact that the leading terms in the asymptotic expansions of the left and right local volatility estimators are (close to) sample averages of squared increments of a Brownian motion multiplied by the volatility level straight before and after the price jump time. The “local Gaussianity” of the high-frequency increments has been also used in MZ in a different context, that is, for constructing various integrated measures of volatility in a continuous setting. Unlike MZ , however, our analysis is for processes with jumps.

Finally, our results can be related to JT in which we propose tests for deciding the common arrival of jumps for two discretely observed processes. The major difference with that paper is that here one of the processes, namely the volatility, is not directly observed, and it has to be estimated from the price increments first. This has nontrivial consequences, as it is essentially the error associated with measuring the volatility that determines the asymptotic behavior of our statistics, and it can significantly slow down their rate of converge. The intrinsic nonsymmetric nature of the price and volatility is reflected in our construction of the tests here, and this makes the statistical problem very different from the one analyzed in JT .

The paper is organized as follows. Section 2 introduces our setup and states the assumptions to be used in the rest of the paper. In Section 3 we propose statistics constructed from the high-frequency data to measure the simultaneous arrival of price and volatility jumps. In this section we also derive central limit theorems associated with the statistics. Section 4 constructs our tests using the statistics of Section 3. Section 5 contains Monte Carlo evidence for the performance of the tests, while Section 6 applies our tests to real financial data. Proofs are in Section 8.

2 Setting and assumptions.

We suppose throughout that our underlying process is an Itô semimartingale on a filtered space . This means that it can be written as

where is a standard Brownian motion, and is a Poisson random measure on , with an auxiliary measurable space, on the space and the predictable compensator (or intensity measure) of is for some given -finite measure on . We write for the volatility process. The processes and should be progressively measurable and should be a predictable function on . We refer to JS for all unexplained, but classical, notation.

We need some assumptions on , and below .

Assumption (H-).

(a) The process is locally bounded.

(b) The process is càdlàg, and neither nor vanish.

(c) We have , for a locally bounded process and a (nonrandom) function satisfying .

When this is little more than being an Itô semimartingale, except for the fact that and do not vanish. When it requires further that the jumps are -summable, and the bigger is, the weaker is the assumption. When (H-) holds, then the jumps of have finite activity.

Next, we make an assumption on the local behavior of . We want to accommodate two extreme cases: one is when is itself an Itô semimartingale (a quite usual assumption for stochastic volatility models), and one is when it is the sum of finitely many jumps plus a continuous process having pathwise some Hölder continuity property such as a fractional Brownian motion. So we present an assumption which may look complicated but is satisfied by all models used so far and implies that is càdlàg. In this assumption, is in , and the bigger it is, the stronger is the assumption.

Assumption (K-).

We have , where is a function on , and and are two adapted processes with the following properties:

(a) The process is an Itô semimartingale satisfying (H-) when whereas when it satisfies (H-), and its continuous martingale part vanishes.

(b) The process satisfies, for some locally bounded process ,

| (2) |

3 Limit theorems for functionals of jumps and volatility.

Our aim is to decide whether we have jumps of and occurring at the same times, and for this we make use of the following processes where is the jump size at time of any càdlàg process :

| (3) |

Here, is a function on where . The derivatives of , when they exist, are denoted by and , for . The general idea will be to choose a function which, for example, is nonnegative and if and only if ; then on the set where the two processes and have common jumps within the time interval , and elsewhere.

The process is not directly observable because we only observe for . Consequently, we “approximate” it by an observable process which we presently describe. We need some notation. For any process we set

| (4) |

We choose two sequences and which serve as cutoff level and window size at stage : we must have but more slowly than , and but more slowly than . To this end it is convenient to choose two exponents and such that, for some constant ,

| (5) |

The next variables serve as “local estimators” of the volatility:

| (6) |

Note that (b) of Assumption (H-) implies that a.s. for all , so a.s. and we can set

| (7) |

The aim of this section is to describe the asymptotic behavior of those observable processes .

3.1 The law of large numbers.

Here we describe under which conditions on we have . Basically, this requires that be continuous, plus some additional conditions. However, we want to apply the result when, for example, has the form , where , and such an is of course not continuous: so the desired convergence does not take place, unless with probability there is no jump of with size or . This is why we introduce the following family of subsets :

| (8) |

Theorem 3.1

Assume Assumption (H-) for some and Assumption (K-) and (5), and let be a Borel function on which is continuous at each point of for some . The processes converge in probability, for the Skorokhod topology, to , as soon as one of the following three sets of hypotheses is satisfied:

(a) for for some ;

(b) we have ;

(c) we have if for some .

3.2 The central limit theorems.

The above consistency result is not enough for us, and we need a central limit theorem (CLT) associated with it. Moreover, in view of the statistical applications given later, we need a joint CLT for the process and for the similar process obtained by substituting with for some integer .

The test function should satisfy some smoothness conditions in connection with the index in Assumption (H-) and involves another index as well. Namely, we suppose that there exist and such that:

(recall that any contains for some ). When the last condition is empty. When the second condition is empty.

We need some additional notation. Let be an auxiliary space endowed with four sequences , , and of independent variables. We introduce the following extension of :

Any variable or process defined on or will be extended to in the usual way, without change of notation. We consider an arbitrary sequence of positive stopping times on which exhausts the jumps of : this means that if and , and that for each the set is contained in .

Below we assume Assumption (H-), and satisfies (3.2). Then the formulas

| (10) |

define two càdlàg adapted processes and on the extended filtered space where is the smallest filtration which contains and such that the variables are -measurable. Moreover, conditionally on , these two processes are independent, with the same (conditional) laws, and are centered Gaussian martingales (hence with independent increments) and with the conditional variances

| (11) | |||

| (12) |

Moreover, if we modify the exhausting sequence we accordingly modify and , but we do not change their -conditional laws which is the only relevant property of for the stable convergence in law below (all these facts are proved, in a slightly different form, in JSEMSTAT ; we refer to JS for the stable convergence in law).

Theorem 3.2

Assume Assumption (H-) for some and Assumption (K-) and (5) with

| (13) |

Let satisfy (3.2) with when and otherwise, and let be an integer.

If either , or for for some , the two-dimensional processes

| (14) |

converge stably in law to the process in the Skorokhod sense.

In (ii) above we do not state the “functional convergence” (stably in law), although it is probably true. For the tests we are after in the paper, we need only the finite-dimensional convergence of the above theorem.

Our second CLT is about the case when the limiting process in the first CLT vanishes. Another normalization is then needed, and also stronger smoothness assumptions on . Namely, we assume (3.2) and

Of course, the limit in Theorem 3.2 may vanish under various circumstances, but for us it is enough to consider the rather simple situation where there is a Borel set and some such that

Then obviously on the set on which, for all , we have whenever . When the set is the set where and have no common jumps on .

When satisfies (3.2), and with a given integer , the formulas

| (18) |

define two càdlàg adapted processes and on the extended filtered space . Moreover, conditionally on , the pair is a process with independent increments and finite variation on compact intervals, and with the conditional means,

| (19) | |||

| (20) |

Here again, if we modify the exhausting sequence we accordingly modify and , but we do not change their -conditional laws.

Theorem 3.3

Assume Assumption (H-) for some and Assumption (K-) and (5) with

| (21) |

Let satisfy (3.2) for some , and (3.2) for when and some otherwise.

If either , or for for some , the two-dimensional variables converge stably in law, in restriction to the set , to the variable .

The same holds when , provided and satisfy

| (22) |

4 Construction of the tests.

4.1 Preliminaries.

Now we are ready to construct our tests using the limit results of the previous section. The overall interval on which the process is observed, at times , is . In our tests the processes and will not play a symmetrical role, mainly because is observed, whereas is not.

Although our main concern is to test for common jumps, irrespective of their sizes, it might be useful to test also whether there are jumps of with size in a subset of , occurring at the same time as jumps of : for example, or (positive or negative jumps of of size bigger than only), or (jumps of of size bigger than ).

We thus pick a subset satisfying the first part of (3.2), and we are interested in the following two disjoint sets:

The subscripts “” and “” stand for “joint” jumps and “disjoint” jumps. One could also specify a subset in which the jumps of lie, but it requires more sophisticated CLTs than Theorems 3.1 and 3.2, and we will not consider this case here. Note that is contained in the set of Theorem 3.3.

Next, we recall that testing a null hypothesis “we are in a subset ” of , against the alternative “we are in a subset ,” with of course , amounts to finding a critical (rejection) region at stage . The asymptotic size and asymptotic power for this sequence of critical regions are the following numbers:

In all forthcoming tests, we fix a priori two sequences and satisfying (5): typically and where are constants. Some restrictions on and will also be made, depending on the test at hand.

Finally, similar to the tests for deciding whether price and volatility jump together or not which we develop here, one can use the limit results of Section 3 to derive various other tests about the relationship between jumps in and its volatility. Examples include: (1) testing whether all jumps in are associated with volatility jumps and (2) testing whether jumps in of given sign always lead to positive (negative) volatility jumps.

4.2 Testing the null hypothesis “no common jump.”

Here we take the null hypothesis to be “ and have no common jump” with jump size of in , that is, , for like in (3.2).

4.2.1 General family of tests.

The idea is to use the variable of (3) and its approximations for a suitable function , namely

| (25) | |||

| (26) | |||

| (27) |

and where . These ensure that satisfies (3.2), (3.2) and (3.2). It also implicitly implies conditions on the set , since and is on , whose complement is finite.

By Theorem 3.1, we have the following convergence:

| (28) |

So in order to test the null hypothesis , it is natural at stage to take a critical region of the form for some (possibly random) . In order to determine in such a way that the asymptotic level of the test be some , we make use of Theorem 3.3, which says that, in restriction to the set , the variables converge stably in law to , as defined by (18). Conditionally on , this variable is a weighted chi-square variable, with mean given by (3.2).

One simple, not very efficient, way to derive test with a prescribed level makes use of Bienaymé–Chebyshev inequality, plus the fact that by Theorem 3.1 again we can approximate the variable by where

| (29) |

satisfies all the requirements of that theorem. At this point, the critical region is taken to be

| (30) |

and the following is straightforward:

Theorem 4.1

The actual asymptotic size of this test is usually much lower than , because Bienaymé–Chebyshev is a crude approximation. However we can use a Monte Carlo simulation to better fit the size, in the spirit of JT : we take a sequence , and we simulate independent variables and of independent variables, for and . Then, with the observed values of , hence of the variables as well, we set

Next, we consider the order statistics of these simulated variables, that is, such that , and we take as our critical region the following:

| (32) |

Theorem 4.2

4.2.2 A leading example.

Here we specialize to be either or for some positive , and in the first case we will need ; that is, our process has finite activity jumps. In both cases, we end up using a finite number of jumps of (jumps of size higher than a fixed value are almost surely of finite number); therefore we consider with . Since for this choice is discontinuous at , we need [recall (8)] in order for (3.2) to be satisfied. Of course, is unknown, but in the typical case when the Lévy measure of has no atom, and thus any works. Otherwise, we can replace by a function which is very close to this. Practically this should make no significant difference, and therefore we stick to the indicator function, with . When we set .

A natural choice for the function is the following:

| (33) |

This choice corresponds to the log-likelihood ratio test for testing that two independent samples of i.i.d. zero-mean normal variables have the same variance. The link with our testing comes from the fact that around a jump time the high-frequency increments of are “approximately” i.i.d. normal.

With this choice of , our test for common jumps becomes essentially pivotal, that is, the limiting distribution of the test statistics depends only on the number of jumps and is thus straightforward to implement. To see this, note that in this case (18) writes as

| (34) |

Conditionally on , this variable has the same law as a chi-square variable with degrees of freedom where . The variable is not observable. However, we have

| (35) |

and since these are integer-valued variables we even have .

Therefore, denoting by the -quantile of a chi-square variable with degrees of freedom, that is, the number such that , we may take the following critical region at stage :

| (36) |

Theorem 4.3

Note that for constructing the critical region in (36), we need only the critical values of a chi-square variable , and thus there is no need for simulation.

4.3 Testing the null hypothesis, “common jump.”

Now we take the null hypothesis to be “ and have common jumps” with sizes in for , that is, , for like in (3.2). We take an integer and a function satisfying (4.2.1), and introduce the statistics

| (37) |

If we combine Theorems 3.1 and 3.3, we first obtain

| (38) |

where stands for the stable convergence in law; for the second convergence we must assume that satisfies (21), and is implicitly depending on ; note that the pair has -conditionally a density, implying a.s.

To determine the asymptotic level of a test based upon , we make use of Theorem 3.2 which by way of the delta method shows that, in restriction to the set , the variables converge stably in law to . The limit is -conditionally centered Gaussian with variance [recall (3.2)]. Hence, if

we deduce that, in restriction to the set , the variables converge stably in law to a standard normal variable, under (15), of course.

Then we may take the following critical region at stage , where denotes the symmetric -quantile of an variable , that is, .

| (40) |

Theorem 4.4

There is no statement about the asymptotic power for the alternative which is any case is not equal to . Indeed, on , the variables converge stably in law to some limit (easily constructed from , and also the variable associated with the function ) as soon as satisfies the assumption of Theorem 3.3. The variable is a.s. nonvanishing, and the asymptotic power of our test is

This quantity cannot be computed explicitly and may be close to , as simulations show later on.

To avoid this power problem, we can “truncate” the estimated variance : let be a sequence of positive numbers (possibly random, but of course depending only on the observations at stage ), such that and , and set

Since converges to a positive finite limit on , we have and this truncation has no effect on the behavior of our standardized statistics under the null, and we take the following critical region:

| (41) |

Theorem 4.5

4.4 Practical aspects.

The construction of the tests involves several choices to be made by the user. The first one is about the functions and in (4.2.1). A good choice seems to be for some and as given by (33). However this works only when (H-) holds (a serious restriction indeed), or when , and in the latter case we only test for common jumps when the size of the jumps of is bigger than . Then the user can perform the testing for various levels of . In addition, if jumps of certain size in are more important, can be replaced with an appropriate weighting function for the jumps of different size. Finally, if the user wants to check cojumping, including the very “small” jumps in , then a good choice is to take and where is a function with bounded first and second derivatives, and and and when .

The second choice in implementing the tests is about the sequences and . Here we face a natural tradeoff between efficiency and robustness. and should satisfy (13) or (21) when , and (15) or (22) otherwise, depending on which test is performed. These conditions depend on the a priori unknown numbers and in Assumptions (H-) and (K-). The higher the and the lower the are, the stricter the conditions are, and the lower the rate at which can grow, that is, the slower the rate at which converges. Intuitively, high makes it difficult to distinguish the many small jumps from the Brownian increments, while low means volatility is very “active” over short intervals and that makes estimation from neighboring increments “noisier.”

Most stochastic volatility models imply that is an Itô semimartingale and therefore . If in addition we assume that , that is, jumps are of finite variation, then we can choose and arbitrarily close to , which is the optimal choice. Alternatively, if we are willing to assume only that for some , then we can write the conditions on and with respect to and pick and so that they are fulfilled. One should emphasize that and only give an order of magnitude, and the concrete choice of and when one is faced with a set of data and thus with and given is always a difficult question: in the Monte Carlo study we provide some guidance on that.

The last choice to be made, for the second test, is choosing the integer . Under the null the normalized asymptotic -conditional variance of takes the form where does not depend on . The minimum of for is achieved at . At the same time the effect of changing under the alternative hypothesis is unclear and in general depends on the particular realization. For that reason we suggest to take and we do so in our numerical applications without further mention. Some Monte Carlo experiments (not reported here) with provide further support for this choice.

5 Monte Carlo study.

In this section we check the performance of our tests on simulated data. We work with the stochastic volatility model

| (42) | |||||

where and are two independent Brownian motions; the (finite activity) Poisson measures and are independent with compensators for and and . This two-factor volatility structure is found to fit high-frequency financial data very well in T09 (see also references therein). The above cited study finds the continuous volatility factor to be very persistent, while the discontinuous one to be transient. This is reflected in our choice of the parameter values of and in the Monte Carlo settings, in an effort to make them realistically plausible for financial applications. In Table 1 we report the parameter values for all cases considered. In all of them the variance of the jumps in is fixed and its share in the total price variation is in the range , which is similar to one estimated from real financial data (see, e.g., HT ). Scenarios with a higher number of jumps imply that the jumps are of smaller size. The different parameter settings differ in the average number of jumps, their sizes, whether jumps are present in the volatility and whether they arrive together with the jumps in or not. The cases labeled with and are draws from the set , while the cases labeled with and are draws from the set . To ensure the latter, we discard simulations from scenarios on which there is no common price and volatility jumps. The behavior of the tests on the discarded simulation draws is exactly as on the simulations from scenarios .

| Parameters | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Case | ||||||||||||

| I-c | 0.02 | 0.4 | 0.04 | 0.5 | 1 | 0 | 0 | 0.5 | 0.1 | 1.0420 | ||

| II-c | 0.02 | 0.4 | 0.04 | 0.5 | 1 | 0 | 0 | 1.0 | 0.1 | 0.7197 | ||

| III-c | 0.02 | 0.4 | 0.04 | 0.5 | 1 | 0 | 0 | 4.0 | 0.1 | 0.3275 | ||

| I-d | 0.02 | 0.4 | 0.04 | 0.5 | 1 | 0 | 1 | 0.5 | 0.1 | 1.0420 | 0.04 | 0.7600 |

| II-d | 0.02 | 0.4 | 0.04 | 0.5 | 1 | 0 | 1 | 1.0 | 0.1 | 0.7197 | 0.04 | 0.3600 |

| III-d | 0.02 | 0.4 | 0.04 | 0.5 | 1 | 0 | 1 | 4.0 | 0.1 | 0.3275 | 0.04 | 0.0600 |

| I-j | 0.02 | 0.4 | 0.04 | 0.5 | 1 | 1 | 0 | 0.5 | 0.1 | 1.0420 | 0.04 | 0.7600 |

| II-j | 0.02 | 0.4 | 0.04 | 0.5 | 1 | 1 | 0 | 1.0 | 0.1 | 0.7197 | 0.04 | 0.3600 |

| III-j | 0.02 | 0.4 | 0.04 | 0.5 | 1 | 1 | 0 | 4.0 | 0.1 | 0.3275 | 0.04 | 0.0600 |

| I-m | 0.00 | 0.0 | 0.00 | 0.5 | 1 | 1 | 1 | 0.5 | 0.1 | 1.0420 | 0.04 | 0.7600 |

| II-m | 0.00 | 0.0 | 0.00 | 0.5 | 1 | 1 | 1 | 1.0 | 0.1 | 0.7197 | 0.04 | 0.3600 |

| III-m | 0.00 | 0.0 | 0.00 | 0.5 | 1 | 1 | 1 | 4.0 | 0.1 | 0.3275 | 0.04 | 0.0600 |

In the simulated model we have (H-) and (K-), so we use the tests based on and given by (33), and . Throughout, time is measured in days, and the observation length is five days, that is, , which constitutes one business week. We simulate days, that is, Monte Carlo replications. On each day we consider sampling , or times, corresponding approximately to sampling every minutes, seconds or second for a trading day of hours or equivalently to sampling every minutes, seconds or seconds for a trading day of hours. Finally, for the calculation of the local volatility estimators we use a window . Our choice for the truncation parameters and determining is and , respectively, where denotes the bi-power variation over the day BS1 , BS4 . This choice of the truncation level reflects the time-variation in the volatility.

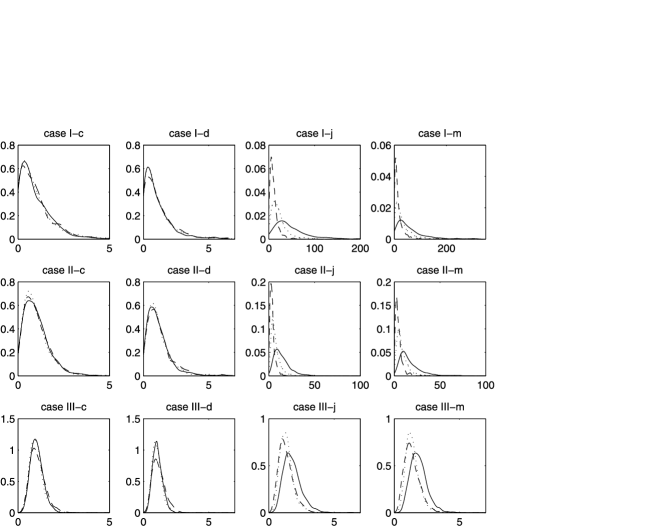

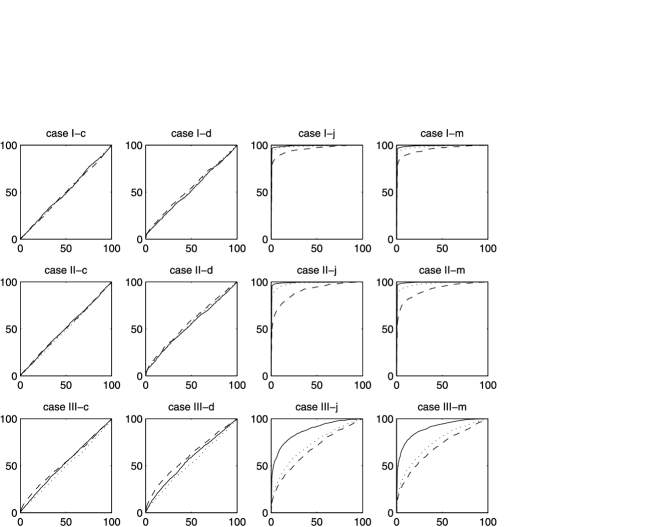

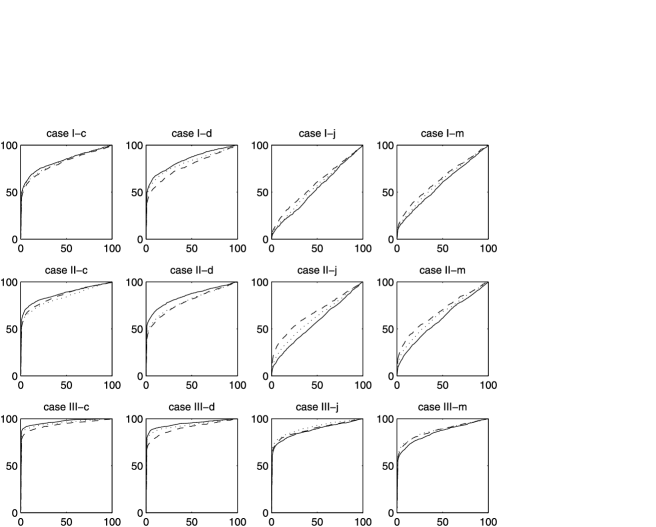

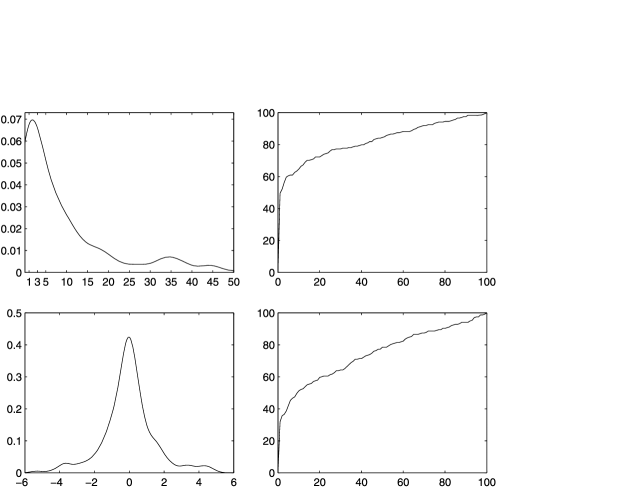

Figure 1 shows kernel density estimates of , and Figure 2 shows the size and power of the test for disjoint jumps. Overall the test behaves as prescribed by our asymptotic results. Not surprisingly, the size of the jumps have the strongest finite sample effect: the last row of Figure 2, corresponding to the scenarios with the smallest on average jumps, shows that for we have slight overrejection when the null is true (cases and ) and lower power when the alternative is true (cases and ). The size distortion disappears and the power converges to as we increase the sampling frequency.

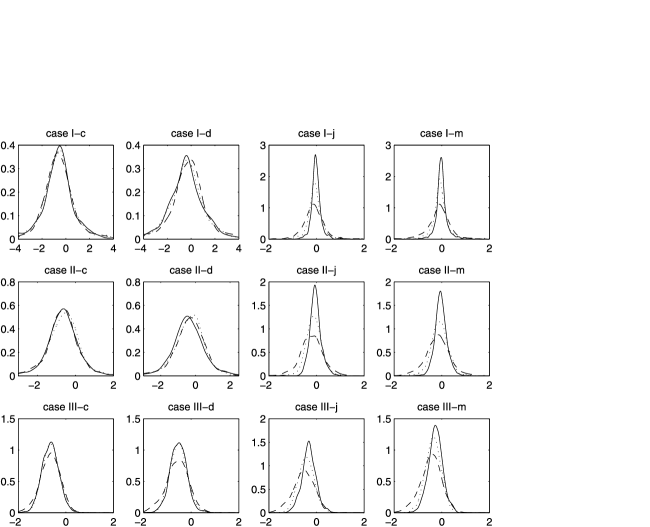

Turning to the test for common jumps, Figure 3 shows kernel density estimates of . The statistics are centered around on the samples in (cases and ), as predicted from our theoretical results. The distribution of on these samples becomes more concentrated around the true value of as we increase the frequency. On the other hand, on the samples in (cases and ), the statistics are centered around , and its distribution remains nearly unchanged across the different sampling frequencies (because for those samples converge to a random variable and not a constant).

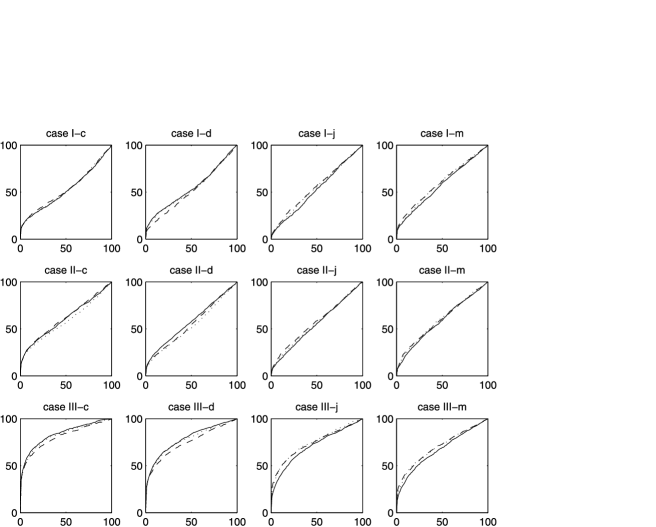

Figure 4 shows the size and power of the test for common jumps when we standardize by . The test has overall good size with the only exception being the cases with high intensity of arrival of small size jumps (last row of the figure), for which even for we have somewhat significant overrejection. On the other hand, from the first two columns of Figure 4 we can see that, when using , the test has essentially no power against the considered alternatives. The lack of power is explained after Theorem 4.4.

We next performed the test with rejection region of (41), corresponding to the truncated variance , and we have taken where is given by (35). The choice of reflects the fact that on , is distributed approximately as . The results of the test with the truncated asymptotic variance are reported on Figure 5. The power against all alternatives improves in all cases, as seen from the first two columns of the figure. The cost of this is finite sample overrejection in the scenarios of frequent small jumps, that is, the last row on Figure 5. The overrejection for cases III-j and III-m is quite big.

Overall, we conclude that the test for disjoint jumps performs well in finite samples and has relatively good power. The test for common jumps should be always performed using the truncated variance , and it can significantly overreject the null in the case of jumps of small size. Finally, as confirmed by the Monte Carlo, using coarser sampling frequencies in performing the tests leads to larger errors in estimating the left and right volatility. Therefore, our ability to distinguish small price and volatility jumps worsens in such cases. As a result, on coarser frequencies the tests will perform worse (i.e., weaker power against alternatives and possible size distortions) when jumps are small, for example, case III in our Monte Carlo, and there will be little effect when jumps are bigger, for example, cases I and II considered here.

6 Empirical application.

Before going to the empirical application, let us mention a crucial point. Our construction of the tests assumes that the stochastic process is observed without error, and the Monte Carlo in the previous section is conducted in this way. In financial applications at very high frequencies, for example, seconds, the presence of microstructure noise in the prices is nonnegligible. If, for example, we have an i.i.d. noise, say with a continuous bounded density , then converges in probability to for all : so obviously our test statistics behave in a very different way than in our theorems for their limiting behavior in probability, not to mention the CLTs. Intuitively, the microstructure noise will tend to bias downwards the estimated difference between left and right volatility, that is, a bias in favor of no common price and volatility jumps hypothesis.

There seem to be two ways to get around the problem of microstructure noise. One is to use a coarser frequency at which the microstructure noise is considered as being negligible. Given our conclusions from the Monte Carlo, this way will inevitably sacrifice somewhat the performance of the tests when very small jumps are involved. An alternative is to develop tests which are robust against the noise, like using a pre-averaging preliminary procedure for our local volatility estimators, but this will inevitably lead to a further decrease in the rates of convergence. Furthermore such an extension of our tests, while building on the theoretical results here, asks for a significantly more involved mathematical approach which goes beyond the scope of the current paper and is thus left for future work.

In our empirical application we use one minute S&P 500 index futures data. The S&P 500 index futures contract is one of the most liquid financial instruments, and thus the microstructure noise should be of little concern at the selected one minute frequency. The sample period is from January 1997 till June 2007 and has 2593 trading days. We aggregate the data into business weeks (a total of 552) and perform the tests over these periods. Our choice for is with given by (33), and we report results for various truncation sizes . The choice of , and is done exactly as in the Monte Carlo study above.

| Rejection rate | |||||

|---|---|---|---|---|---|

| # of weeks with jumps | Null | Null | |||

| Jump size | |||||

| any size | 238 | ||||

| 0.2% | 163 | ||||

| 0.3% | 96 | ||||

| 0.4% | 56 | ||||

[]Note: the test for common jumps is based on in (41).

Table 2 reports the rejection rates of the two tests (for the conventional and significance levels) for various levels of the truncation size , while Figure 6 plots the kernel density estimate of the test statistics together with rejection curves of the two tests for the case of . The results suggest very strongly that the jumps in the level of the S&P 500 index are accompanied by jumps in its volatility. This is further confirmed from Table 3 in which we report the percentage of weeks in which both tests suggest the observed path is in , , or disagree. Based on the results in Table 3 for the weeks in which the S&P 500 index jumps: (1) in approximately of them there is strong evidence for common price and volatility jumps, (2) in around of them there is evidence for disjoint jumps and (3) for the rest of the weeks the tests are inconclusive. Given our Monte Carlo study, this last part of the sample can be explained with a lot of small jumps for which detecting common or disjoint arrival needs even higher frequencies.

7 Conclusion.

In this paper we derive tests for deciding whether jumps in a stochastic process are accompanied by simultaneous jumps in its volatility using only high-frequency data of the process. Our application of the tests to S&P 500

=270pt Accept Reject Accept Reject \sv@tabnotetext[]Note: numbers based on the two tests with significance level and truncation level . The test for common jumps is based on in (41).

index data indicates that most stock market jumps are associated with volatility jumps as well.

8 Proofs.

8.1 Preliminaries.

Under Assumptions (H-) and (K-), both and are Itô semimartingales, with (2) for , and has a similar representation, in which (up to “augmenting” the Poisson measure ) it is no restriction to assume that the Poisson measure is the same. That is, we can write

where is another standard Brownian motion, independent of . Moreover we have , where we can always take the same process than in Assumption (H-) for , as we may do for the process showing in (2). Note also that

By a well-known localization procedure (see, e.g., JSEMSTAT ) it is enough to prove all theorems of Section 3, hence also of Section 4, when in addition to the relevant Assumptions (H-) and (K-) we have

| (45) | |||

for some constant . This additional assumption will be supposed throughout. In the sequel, is a constant which varies from line to line and may depend on above and also on and on the function in (H-), and is written if it depends on an additional parameter .

Under (8.1), we can write as , where

| (46) | |||||

We also need a long series of additional notation. For each integer we denote by the successive jump times of the counting (Poisson) process . We relabel the two-parameter sequence as a single sequence , which clearly exhausts the jumps of .

When we denote by the set of all ’s such that for some and . We set and

We have

| (47) |

When we also set

Note that , , , and . When , we can also define those quantities when , in which case , , , and .

8.2 Estimates.

We proceed here by recalling or proving a number of useful estimates. As said before, we always assume Assumptions (H-) and (K-) and (8.1). Mostly, these estimates are conditional with respect to a possibly larger filtration than . So we fix , and denote by and the restrictions of the measure to the sets and , respectively. These are two independent Poisson measures, independent of and as well. We denote by the -field generated by the measure , and by the smallest filtration containing and such that contains .

We set which is also the union of the graphs of the stopping times for . Then we define the process

Due to the independence of , , and , the processes and and the measure are still Wiener processes and a Poisson random measure, relative to the filtration . Hence and are Itô semimartingales, with the same form as in (8.1) (we can replace and by and its deterministic compensator because of the presence of ) and relative to the filtration . In the same way is still of the form (8.1), driven by , and (instead of ), relative to [and up to replacing by , which is still bounded].

1. Estimates on .

2. Estimates on .

The following classical estimates use (8.1) and . Below, and and is an integer, possibly random but -measurable, and we have

| (53) |

Next, we also have for ,

| (54) |

These estimates hold when as well [in which case and is not random, and ]. In particular, in this case we deduce

| (55) |

Next, with any measurable subset of we consider the increasing process . This process is infinite for all if , and otherwise is a Lévy process, and known estimates on Lévy processes yield for all ,

| (56) |

[Since is bounded, when the right-hand side above is smaller than .] Since , we deduce (for not random)

| (57) |

3. Estimates on .

Below, is a nonrandom integer. First (55) yields

| (58) |

We need also estimates on the difference for suitable times . If is a -measurable positive finite time and an -measurable random integer, the sets

are -measurable, and we have

Lemma 8.1.

Assume Assumptions (H-) and (K-) and (8.1). Let or , and assume (5) with also

Then there is a sequence such that, for and any -measurable variables and as above, we have

| (60) | |||

and also

Moreover, as soon as , and under (5) only, we have

We will prove, for example, the second claims of (8.1), (57) and (8.1) (the first ones are slightly easier). On the set the variable is equal to the variable associated in the same way with the process .

The following estimate, for all , , , is straightforward:

This will be applied with and and [so ], and and such that , and when : using Hölder’s inequality, we deduce from (8.2) and (54) and the boundedness of , and after some calculation, that in this case

for any , on the set , because .

Next, we write , and we apply (51) and (8.2) and either Hölder’s inequality plus the boundedness of , or successive conditioning, to get, for and as above,

These estimates, together with the definition of and , yield

on the set , where . Then (5) and a proper choice of show that for , under (56), and as soon as . This in particular gives the second part of (8.1).

8.3 The stable convergence of .

From now on, the integer is fixed. The aim of this subsection is to prove the following stable convergence:

Proposition 8.2.

Step 1. It is enough to prove the convergence of any finite sub-family of indices . In other words, instead of considering the infinite sequence indexed by in (63) and (8.2), we can fix an arbitrarily large integer and consider the families indexed by . All smaller than are in some , and we consider the set on which for any and any we have and . Obviously, as .

Now we will apply Lemma 8.1 with for , and : then and are -measurable, and the set is included into both and . Since , we deduce from this lemma that

Step 2. Now we set

By (8.3), we are left to prove that the variables stably converge in law to . Taking into account that is independent of , this amounts to proving

| (67) |

where is any bounded -measurable variable, and is continuous bounded.

In fact, if denotes the smallest filtration to which is adapted and such that , each is -measurable. So, up to substituting with above, it is clearly enough to prove (67) when is -measurable.

Step 3. We introduce some further notation: first the set , which is a random -measurable set, and second the processes

[those are well defined because is a -Brownian motion]. The -fields generated by and all variables increase with , and . Therefore it is enough to prove (67) when is -measurable for some : to see this, let be -measurable; set ; if (67) holds for each , it also holds for because in .

The set of Step 1 is -measurable, hence -measurable for all . Since it is enough to prove that for any bounded -measurable variable ,

| (68) |

Step 4. We introduce a double sequence of i.i.d. variables on some auxiliary probability space. Then, define the variables

Observe that in restriction to the set the variable involves increments of which are different for different values of , and are increments of the process above, which is independent of . Therefore if is fixed, for any and in restriction to the -measurable set , the -conditional distribution of the variable of (8.3) is exactly the law of

This means that the left-hand side of (68) for is equal to .

8.4 Proof of Theorem 3.1.

1. As stated before, we assume Assumptions (H-) and (K-) and (8.1). If and and , we have

| (69) | |||

| (70) | |||

| (71) | |||

| (72) |

The sum defining has a bounded number of summands, as varies. We also have for ,

[use (8.2) and for the second property]. We have by (8) and is continuous on . Since and on [use (8.1) with ], the th summand in converges to in probability. Therefore we have the following convergence in probability for the Skorokhod topology:

| (74) |

2. Next, we show the result in case (a). Pick . Since , for any we have for all , on a set whose probability goes to . On we have for all , because of the property of , which also implies identically. Then the result readily follows from (74).

3. Next, we show the result in case (b). The notation (8.1) is also valid for , and (74) holds for (the right-hand side is a finite sum) and . Since , it follows from the second part of (8.2) (which also holds with when ) that , which is smaller than if . So Borel–Cantelli lemma yields that, for each , we have for all , hence for , when is large enough. We then conclude as above.

4. It remains to consider the case (c). First, as soon as (recall that is bounded). Since a.s. for all , whereas when differs from all for , we deduce from the dominated convergence theorem that a.s., locally uniformly in time as . Therefore by (74) it remains to prove that for all ,

| (75) |

On the one hand, as in the previous step we deduce from (8.2) and from that, if , we have and for all , when is large enough. On the other hand, our assumption on yields that if and , then as soon as . Hence for any given , and outside a set satisfying as , we have for all , where

Therefore we are left to show that for all ,

| (76) |

8.5 Proof of Theorem 3.2.

Step 1. We use the notation (8.4) of the previous proof when we deal with and write instead and when we deal with . We also use , as defined in (74), and

and is the same with instead of . We have

where

We also set

Step 2. In this step we prove that

| (78) | |||

(stable functional convergence in law) where and are as described in (10), except that the sum is taken over the only. By Proposition 8.2, we have

note the normalization in is by . Hence proving (8.5) shows that for each we have

| (79) |

in restriction to each set . We will prove, for example, the first property. We have and (47) and (8.4), implying that the set converges in probability to the set . Therefore it is enough to show that

The sequences are bounded in probability and a.s., so (3.2) and Taylor’s formula yield

So in fact it is enough to prove that

| (80) | |||

Since a.s. and the two sequences and are tight in , the first part of (3.2) yields that (8.5) will hold if . Therefore (8.5) follows from the facts that and that the sequence is bounded in probability, the latter coming, for example, from Lemma 8.5 of JSEMSTAT . This ends the proof of (8.5), hence of (8.5).

Step 3. Here we prove (i). Suppose first that for for some , and take . As in the previous theorem we then have and and , whereas for all on a set having . The result follows from (8.5).

Next we assume . Again as in the previous proof, we argue with : we have and and , whereas for all on a set having . Then the result follows as before.

Step 4. Now we assume . By (3.2) and the boundedness of , we have

as soon as . This goes to a.s. as because of Assumption (H-), and it follows that (convergence in probability, locally uniformly in time). In the same way, we have . Therefore, it remains to prove that for all ,

| (81) |

and the same for . We will prove (81) only. Observe that, with the simplifying notation and , we have , where and, with ,

In view of (47) we are thus left to prove the existence of sets and satisfying for all ,

| (82) |

such that, for and , respectively,

| (83) | |||||

| (84) |

Step 5. In this step we prove (83). In view of the second part of (3.2) and of and (8.1) we have when ,

Moreover, we have the following estimate, for all possibly random but -measurable:

| (85) |

Since the set satisfies (82), and on this set we have . Then (83) for readily follows from (85) and the property [see (15)].

Now we consider the case . We have . The successive integers in are -measurable, and the number of them is a Poisson variable independent of the ’s and with some parameter (exploding with ). Then , and (83) for holds with .

Step 6. In this step we prove (84) for . The sets

| (86) |

satisfy the first part of (82) because and [use (8.2) for this]. When , (3.2) yields that on the set and for all where

Then it remains to prove that (84) holds for and .

Apply (8.1) with and or [so ] to get

| (87) |

Moreover (8.2) gives . Then by successive conditioning we obtain . Since as we deduce (84).

Step 7. Now we prove (84) for with . We suppose that , so and (3.2) yields that where

So it is enough to prove (84) for . The case is simple: the process is predictable; hence

where the last inequality comes from (51) with and . Then (84) for follows because by (15).

Step 8. Now we start proving (84) for . Set

If , we deduce from (3.2) and the boundedness of that

Therefore

Taking (15) into consideration, we deduce that

and thus we are left to prove (84) for .

Step 9. In this auxiliary step we fix , and also some [this is possible by (15)]. We write and we suppose that is big enough for having . We complement notation (8.1) with

| (88) | |||||

First, is a Poisson process with parameter ; hence

| (89) |

Second, upon observing that (because ) and when and if , that

| (90) |

This applied with and Markov’s inequality yield

| (91) |

Next, on the set , we have and , and also for all , except when for a single value of for which (whose absolute value may be smaller or greater than ). In other words, on we have

The following estimate, when and for some (this will be the bound of the process ) and with and , is easy to prove, upon using (3.2):

Therefore, on the set again we have

| (92) |

The process satisfies the same estimate as in (54), hence since ,

| (93) |

On the other hand, we can apply (90) with and the Cauchy–Schwarz inequality to obtain . We also have [see before (56) for this notation], and is -measurable. Therefore, in view of (56) applied with the power and Hölder’s inequality, and upon applying , and with the notation , we see that

Hence by (92) and (93), we deduce

| (94) |

8.6 Proof of Theorem 3.3.

Step 1. We assume Assumptions (H-) and (K-) and (8.1). Recalling (2) and (8.1), we set , and define by (2) with instead of . This process satisfies Assumption (H-) as well, and coincides with on the interval , in restriction to the set . Hence the variables and and and are the same on , whether computed using or . So it is enough to prove the result for the process . Or, in other words, we can assume throughout that

| (95) |

We use the same arguments as in the previous proof, and the same notation, except that the variable of (8.5) should be replaced by

and the same for with instead of .

Step 2. In this step we prove that

| (96) |

where and are as in (18), except that the sum is taken over the only. By Proposition 8.2, we have

so proving (8.5) shows that for each and on each set we have

| (97) |

We prove only the first property, which [like in Theorem 3.2; note that here by (3.2) and (95)] amounts to the convergence of

to in probability. Upon using again (3.2) and (95), we deduce from Taylor’s formula and the tightness of the sequences that, on the set which has probability , the variables

go to in probability. Hence the first part of (97) will follow if we show

This is proved exactly as (8.5), except that here we use the property .

Step 3. The proof of (i) follows from (96) in exactly the same way as in Step 3 of the proof of Theorem 3.2.

Step 4. Now we start proving (ii), so . We can suppose that contains a neighborhood of ; otherwise we are in the second situation of case (i). Hence we may take in (3.2) such that also . Similar to (3.2), and by the boundedness of and (3.2), we have if ,

This goes to a.s. as because of Assumption (H-), so , and also . Then it remains to prove that for all ,

| (98) |

and the same for . We will prove (98) only.

Because of our assumptions we have here . Then, in view of definition (8.4), and since the sets of (86) satisfy (82), it is enough to prove that

| (99) |

where

On , when , for all we have and also when further . Then, using (3.2) and a Taylor expansion around , and since for all , we see that

where

Hence we are left to prove that, for , we have

| (100) |

Step 5. On the one hand, successive conditioning, plus the third estimate in (8.2) with , plus (8.1) with and , yield . Then (100) for follows. For we will prove the stronger statement, for large enough,

| (101) |

Therefore, we fix below.

First, suppose that . Then , and since and when [recall and (95)], we have , where

Then exactly as in Step 7 of Theorem 3.2, and using (51) with instead of , we obtain . Then (101) holds for , hence for , by (22).

It remains to consider the case . We take , and we use the notation and (8.5), which we complement as follows:

so , and we associate the variables

It is thus enough to prove (101) when . First, we have , and thus by (51) we get , which equals , and (101) for holds by (22). Next, (8.2) applied with instead of implies that for any we have (use again ). Then by (51) and Hölder’s inequality we see that for any . Then again, upon taking close to , we have (101) for .

8.7 Proof of the results on the tests.

Proof of Theorem 4.1 Theorems 3.1 and 3.3 yield that, in restriction to , the variables converge stably to a positive variable which, conditionally on , has mean . Hence if and with given by (30), we have , which is smaller than because , and the result for the asymptotic level follows. Since on the set by Theorem 3.1, the asymptotic power is clearly . {pf*}Proof of Theorem 4.2 We will be very sketchy here. By localization we may assume (8.1).

First, we can suppose that the simulated variables are defined on our auxiliary space , so that the ’s are defined on the extension . Then we can reproduce the proof of Theorem 4.4 of JT to obtain that, if are -measurable variables, we have

| (102) |

The only slightly different point is that we need here . This does not follow from (58), but it does from (8.1) applied with , because by hypothesis (8.1) holds.

Then, using (102) and that on the set , we can reproduce the proof of Theorem 5.1, Part (c), of JT , and we obtain the claim about the asymptotic level. In the course of this proof it is also shown that -conditionally the variables converge in law to the unique variable such that , from which follows.

Finally on . This and , yields that . Hence the asymptotic power equals . {pf*}Proof of Theorem 4.3 The proof is the same as for Theorem 4.1, with the following changes: we now have because converges stably in law on to a chi-square variable with degrees of freedom, independent of , and for large enough. This gives that the asymptotic level is , and for the asymptotic power we use the fact that and on the set . {pf*}Proof of Theorem 4.4 The result readily follows from the stable convergence in law of to a standard normal. {pf*}Proof of Theorem 4.5 Since for all large enough, on the set , only the claim about the power needs a proof. Now, , and we have the second part of (38) on ; that the asymptotic power equals is now obvious.

Acknowledgments.

We would like to thank Tim Bollerslev for providing us with the high-frequency data and an anonymous referee for careful reading and constructive comments on the paper.

References

- (1) {barticle}[auto:SpringerTagBib—2009-01-14—16:51:27] \bauthor\bsnmBarndorff-Nielsen, \bfnmO. E.\binitsO. E. and \bauthor\bsnmShephard, \bfnmN.\binitsN. (\byear2004). \btitlePower and bipower variation with stochastic volatility and jumps. \bjournalJournal of Financial Econometrics \bvolume2 \bpages1–37. \biddoi=10.1093/jjfinec/nbh001 \endbibitem

- (2) {barticle}[vtex] \bauthor\bsnmBarndorff-Nielsen, \bfnmO. E.\binitsO. E. and \bauthor\bsnmShephard, \bfnmN.\binitsN. (\byear2006). \btitleEconometrics of testing for jumps in financial economics using bipower variation. \bjournalJournal of Financial Econometrics \bvolume4 \bpages1–30. \endbibitem

- (3) {barticle}[auto:SpringerTagBib—2009-01-14—16:51:27] \bauthor\bsnmHuang, \bfnmX.\binitsX. and \bauthor\bsnmTauchen, \bfnmG.\binitsG. (\byear2006). \btitleThe relative contribution of jumps to total price variance. \bjournalJournal of Financial Econometrics \bvolume4 \bpages456–499. \endbibitem

- (4) {bbook}[mr] \bauthor\bsnmJacod, \bfnmJean\binitsJ. and \bauthor\bsnmShiryaev, \bfnmAlbert N.\binitsA. N. (\byear2003). \btitleLimit Theorems for Stochastic Processes, \bedition2nd ed. \bseriesGrundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences] \bvolume288. \bpublisherSpringer, \baddressBerlin. \bidmr=1943877 \endbibitem

- (5) {bmisc}[auto:SpringerTagBib—2009-01-14—16:51:27] \bauthor\bsnmJacod, \bfnmJ.\binitsJ. (\byear2007). \bhowpublishedStatistics and High-Frequency Data. SEMSTAT Course in La Manga. To appear. \endbibitem

- (6) {barticle}[vtex] \bauthor\bsnmJacod, \bfnmJean\binitsJ. and \bauthor\bsnmTodorov, \bfnmViktor\binitsV. (\byear2009). \btitleTesting for common arrivals of jumps for discretely observed multidimensional processes. \bjournalAnn. Statist. \bvolume37 \bpages1792–1838. \biddoi=10.1214/08-AOS624, mr=2533472 \endbibitem

- (7) {barticle}[vtex] \bauthor\bsnmMykland, \bfnmP.\binitsP. and \bauthor\bsnmZhang, \bfnmL.\binitsL. (\byear2009). \btitleInference for continuous semimartingales observed at high frequency. \bjournalEconometrica \bvolume77 \bpages1403–1455. \endbibitem

- (8) {barticle}[vtex] \bauthor\bsnmTodorov, \bfnmV.\binitsV. (\byear2010). \btitleVariance risk-premium dynamics: The role of jumps. \bjournalThe Review of Financial Studies \bvolume23 \bpages345–383. \endbibitem

- (9) {bmisc}[vtex] \bauthor\bsnmTodorov, \bfnmV.\binitsV. and \bauthor\bsnmTauchen, \bfnmG.\binitsG. (\byear2009). \bhowpublishedVolatility jumps. Preprint, Northwestern Univ. \endbibitem