Dynamic Coherent Acceptability Indices and their

Applications to Finance

††thanks: TRB and IC acknowledge support from the NSF grant DMS-0908099. The authors would like to thank the anonymous referees and the editors for their helpful comments and suggestions which improved greatly the final manuscript.

Illinois Institute of Technology

10 West 32nd Str, Bld E1, Room 208

Chicago, IL 60616-3793

First circulated: October 21, 2010

Current version:

)

Abstract

In this paper we present a theoretical framework for studying coherent acceptability indices in a dynamic setup. We study dynamic coherent acceptability indices and dynamic coherent risk measures, and we establish a duality between them. We derive a representation theorem for dynamic coherent risk measures in terms of so called dynamically consistent sequence of sets of probability measures. Based on these results, we give a specific construction of dynamic coherent acceptability indices. We also provide examples of dynamic coherent acceptability indices, both abstract and also some that generalize selected classical financial measures of portfolio performance.

Keywords:

dynamic coherent acceptability index, dynamic measures of performance, dynamic coherent risk measures,

dynamically consistent sequence of sets of probability measures, time consistency, dynamic GLR, dynamic RAROC

MSC2010: 91B30, 60G30, 91B06

1 Introduction

Individual and institutional investors are typically concerned with finding satisfactory balance between reward and risk associated with an investment process. Various measures have been developed to quantify this balance. Such measures are typically referred to as performance measures or measures of performance (MOP). Recently, Cherny and Madan [13] originated an effort to provide a mathematical framework to study these measures in a unified way. The present paper contributes to this effort.

One of the most popular MOPs is the Sharpe Ratio (SR) introduced in [30]. SR is expressed as a ratio of expected excess return to standard deviation, and thus in financial applications it measures expected excess return of a portfolio in units of portfolio’s standard deviation. SR has been used as a classical tool to rank portfolios according to their “reward-to-risk” characteristics.

Using standard deviation to quantify risk is considered to be the major drawback of Sharpe Ratio. The reason of course is that positive returns also contribute to this measure of risk. To eliminate this unwanted feature other ratio-types MOPs were proposed, such as Sortino Ratio (SOR) [31] and Gain Loss Ratio (GLR) [6]. These MOPs focus on downside risk only. A popular generalization of SR is provided by the Risk Adjusted Return on Capital (RAROC), which is constructed as a ratio of mean excess return to some selected measure of risk.

All the MOPs mentioned above share some common desirable features: they are unit-less, they are increasing functions of reward and decreasing functions of risk; moreover, according to these MOPs diversification of a portfolio improves its performance. This observation prompts a natural desire to study MOPs in a unified mathematical framework.111There exists a vast literature that studies measures of risk in a general mathematical framework. As already mentioned, such a study was recently originated in [13]. We shall recall the main results of that paper in Section 2 below. The study of [13] was done in static, one-time period setup. Cherny and Madan coined the term Acceptability Index (AI) as a mathematical terminology for MOPs. Our goal is to elevate the mathematical framework for studying AIs to dynamical, multi-period setup, where cash flows are considered as random processes, and one needs to assess their acceptability consistently in time. In particular, we are concerned not just with the total cumulative terminal value of the cashflow as seen from the initial time of the investment process, but also with all remaining cumulative cashflows between each intermediate time and the terminal time of the investment process.

Thus, in a sense, our program is analogous to the one of those researchers (cf. [5, 7, 9, 10, 11, 14, 18, 26, 28, 25, 23, 29, 33, 17, 32]) who are studying dynamic risk measures. Moreover, as it will be seen later in the paper, there is a duality relationship between dynamic (coherent) acceptability indices and dynamic (coherent) risk measures in the sense of Section 4.

The paper is organized as follows:

In Section 2 we summarize the main results of [13]. This is done for the convenience of the reader, but also in order to give the flavor of the duality between acceptability indices and risk measures, that will be generalized to the dynamic framework in the subsequent sections. In Section 3 we present the definition of a dynamic coherent acceptability index (DCAI). We devote some time to discussion of the properties of DCAI from the definition, putting special emphasis on discussion of various forms of the dynamic consistency property.

Section 4 first introduces the concept of the dynamic coherent risk measure (DCRM), specific for our needs, and then proceeds to study the duality between families of such measures and DCAI. In the process, we discuss the dynamic consistency property of a DCRM, and we relate our findings to the results from existing literature.

In Section 5 we provide characterization of a DCRM in terms of so called dynamically consistent sequence of sets of probability measures, thereby providing an additional perspective at DCAIs.

Section 6 is dedicated to discussion of some abstract examples of dynamic MOPs, as well as some specific examples of dynamic MOPs derived form the classical ones, such as GLR and RAROC. In particular, we show that dynamic version of GLR is a DCAI, whereas the dynamic version of RAROC is not.

2 Static Acceptability Indices

In this section, we will briefly review the theory of static acceptability indices developed in [13].

Let be a probability space and denote by the space of all bounded random variables on . The random variable can be regarded as discounted terminal cash flow of a zero-cost self-financed portfolio. By definition, an acceptability index is a map . The value should be understood as the degree of acceptability of a cash flow ; in a sense, it represents a measure of efficiency of the cash flow. A larger index indicates better performance, with for being an ‘arbitrage opportunity’; in particular, if the cash flow is strictly positive, then

Acceptability index as such is a too broad concept, and it may not fulfill certain practically desirable properties. That is why, Cherny and Madan [13] focused their attention on a more specific concept of the coherent acceptability index.

Definition 2.1.

An acceptability index is called coherent if the following properties are satisfied:

-

(S1)

Monotonicity. If , then ;

-

(S2)

Scale invariance. For every and ;

-

(S3)

Quasi-concavity. If , then for all ;

-

(S4)

Fatou property. If for all , and , as , in probability, then .

The above properties have natural financial interpretation. For example, (S1) states that if dominates – almost surely,222In the present paper we shall make a standing assumption that is finite and that is strictly positive. Thus, our statements regarding relations between random variables will hold point-wise. In particular, will mean that dominates for every then is acceptable at least at the same level as is; (S2) implies that cash flows with the same direction of trade have the same level of acceptance. Quasi-concavity (S3) implies that a diversified portfolio performs at higher level than its components; to see this, it is enough to take . Fatou property (S4) is a technical continuity property, which is used for constructing the duality between coherent acceptability indices and coherent risk measures.

It can be shown that Sharpe Ratio, defined as , where is the standard deviation of and is the (constant) interest rate, does not satisfy the monotonicity property (S1), and hence it is not a coherent acceptability index. The Gain Loss Ratio, given by if , and zero otherwise, is a coherent acceptability index. Other measures of performance such as RAROC, AIT, AIW, AIMIN, AIMAX, AIMINMAX, AIMAXMIN etc, have been also studied in [13]. Moreover, in [13] the authors proved the following representation theorem:

Theorem 2.2.

A map , unbounded from above, is a coherent acceptability index if and only if there exists a family of sets of probability measures, such that for and admits the following representation

| (2.1) |

where and .

Thus, any Coherent Acceptability Index (CAI) can be characterized by an increasing family of sets of probability measures. This family of probability measures can be seen as generalized scenarios as described in [4], or set of supporting kernels as discussed in [13]. Moreover, there is a strong relationship between CAI and Coherent Risk Measures (CRM), a concept introduced by Artzner, Delbaen, Eber, Heath [3, 4].

Definition 2.3.

A function is called coherent risk measure if the following properties are satisfied:

-

(R1)

Monotonicity. If , then ;

-

(R2)

Positive homogeneity. , for every and ;

-

(R3)

Translation property. , for every and ;

-

(R4)

Subadditivity. , for every .

Traditional Value at Risk , while very popular, it is not a coherent risk measure since it lacks the subadditivity property (R4), which corresponds to the diversification property in finance. In contrast, the Tail Value at Risk (also called Tail Conditional Expectation), defined as , where and is the set of probability measures absolutely continuous with respect to such that , is a CRM. So is the Weighted Value at Risk, , where is a probability measure on . The following representation theorem is established in [4] for finite , and generalized to a general probability space in [16, 8]:

Theorem 2.4.

A function is a coherent risk measure if and only if

| (2.2) |

for a certain set of probability measures absolutely continuous with respect to .

Note that by (2.1) and the above theorem, every CAI can be characterized in terms of an increasing family of coherent risk measures.

The theory of static risk measures has been explored and extended by many researchers; to mention just a few of them: Föllmer and Schied [19, 20] and Frittelli and Rosazza Gianin [22] generalized the concept of coherent risk measures to convex and monetary risk measures; Cheridito and Li [12] studied generalized measures on Orlicz Hearts, law-invariant risk measures have been investigated by Kusuoka [27] and Frittelli and Rosazza Gianin [24]; for a systematic discussion on static risk measures we refer reader to the monographs by Delbaen [15] and Föllmer and Schied [21, Chapter 4].

3 Dynamic Coherent Acceptability Indices

As it has been already stated, the dynamic acceptability indices are meant to assess performance of a cash-flow accounting for newly acquired information when time progresses. Of course, one may attempt to use for this purpose a sequence of static (one-period) acceptability indices. However, by doing this one may end up with a sequence of measurements that are not consistent in time, in the sense to be explained below (cf. property D7). The motivation for developing a theory of DCAIs, as presented in this paper, was to create a systematic mathematical framework to provide performance measurements consistently in time.

Let be a finite underlying probability space, and let be a finite set of time instants. We assume that is of full support. We endow the underlying probability space with a filtration . For each and , there exists a partition of , say , that generates .

A cash flow, also called dividend process, denoted as , is any real valued random process adapted to the filtration . We denote by the set of all cash flows. In addition, we denote by the set of all probability measures that are absolutely continuous with respect to , and by the set of all probability measures equivalent to . Also, will denote a generic constant, and will denote a generic random variable. Finally, a standing (financial type) assumption, which we make without loss of generality, is that the interest rates are zero.

Definition 3.1.

A dynamic coherent acceptability index is a function that satisfies the following properties:

-

(D1)

Adaptiveness. For any and , is -measurable;

-

(D2)

Independence of the past. For any and , if there exists such that for all , then ;

-

(D3)

Monotonicity. For any and , if for all and , then for all ;

-

(D4)

Scale invariance. for all and ;

-

(D5)

Quasi-concavity. If and for some , , , and , then for all ;

-

(D6)

Translation invariance. for every , , , and every -measurable random variable ;

-

(D7)

Dynamic consistency. For any and , if for all , and there exists a non-negative -measurable random variable such that for all , then for all .

Property (D1) is a natural property in a dynamic setup and it assumes that a DCAI is adapted to the same information flow as is any cash flow .

(D2) postulates that in the dynamic context the current measurement of performance of a cash flow only accounts for future payoffs. To decide, at any given point of time, whether one should hold on to a position generating the cash flow , one may want to compare the measurement of the performance of the future payoffs (provided by DCAI at this point of time) to already known past payoffs.

Properties (D3)-(D5) are naturally inherited from the static case (cf. Section 2).

Translation invariance (D6) implies that if a known dividend is added to at time (today), or at any future time , then all such adjusted cashflows are accepted today at the same level.

Dynamic consistency (D7) is the property in the dynamic setup which relates the values of the index between two consecutive days in a consistent manner. It can be interpreted from financial point of view as follows: if a portfolio has a nonnegative cashflow today, then we accept this portfolio today at least at the same level as we would accept it tomorrow; similarly, if the today’s cashflow is nonpositive the acceptance level today can not be larger than the level of acceptance tomorrow.

For technical reasons, which will become clear later, we assume that for every DCAI , and for every and , there exist two portfolios such that and . We shall say that DAI is normalized.

Note that normalization will exclude the degenerate examples of acceptability indices such as a constant index over all states, times, and portfolios. Moreover, one can show that a normalized index gets value infinity for every strictly positive cashflow and value zero if the cashflow is strictly negative:

where, for any and , for and zero otherwise.

For normalized DCAI we have equivalent forms of Property (D7). In fact, one can show that under normalization, the set of properties (D1)–(D7) is equivalent to either the set (D1)–(D7-I) or the set (D1)–(D7-II), where

-

(D7-I) For a given and , if for all , and there exists a non-negative -measurable random variable such that for all , then for all .

-

(D7-II) For a given and , if for all , then

for all .

Finally we want to mention that (D3) and (D7) can be equivalently replaced in the definition of DCAI by the following two properties:

-

(D3-I) For , if there exists such that for all , then ;

-

(D7-III) For , if there exist and a non-negative -measurable random variable , such that and , then .

4 Characterization of Dynamic CAI by a family of Dynamic CRMs

As mentioned in Section 2, there is a strong relationship between coherent acceptability indices and coherent risk measures. In fact, as seen from Theorem 2.2 and Theorem 2.4, any CAI can be represented in terms of a family of coherent risk measures :

| (4.1) |

Looking at (4.1) one might think that a natural approach to constructing a DCAI would be to use this representation but to replace the static coherent risk measures in (4.1) by their dynamic counterpart. The representation (4.8) that we derive below shows that this is indeed the case. The delicate issue however is, what family of dynamic coherent risk measures should be used. It turns out that in order to produce a DCAI satisfying a financially acceptable set of dynamic properties, one needs to use a carefully crafted family of dynamic coherent risk measures. In this section we introduce such a family of dynamic coherent risk measures and we compare our definition of coherent dynamic risk measures with analogous ones that have been already studied in the literature.

4.1 Definition of dynamic coherent risk measure

Definition 4.1.

Dynamic coherent risk measure is a function that satisfies the following properties:

-

(A1)

Adaptiveness. is -measurable for all and ;

-

(A2)

Independence of the past. If for some , , and and for all , then ;

-

(A3)

Monotonicity. If for some and , and for all and , then for all ;

-

(A4)

Homogeneity. for all , and ;

-

(A5)

Subadditivity. for all , , and ;

-

(A6)

Translation invariance. for every , , -measurable random variable , and all ;

-

(A7)

Dynamic consistency.

for every , and .

We want to mention that our definition of DCRM differs from the definition given in previous studies essentially only by the dynamic consistency property. For sake of completeness, we will present here how property (A7) relates to other forms of dynamic consistency of risk measures (for processes).

-

(A7-I) If , and for some , and , then ;

-

(A7-II) for all times and positions .

-

(A7-III) for all ,

-

(A7-IV) for all ,

-

(A7-V) if , and for some and , then .

Property (A7-I) is the dynamic consistency property for DCRM defined by Riedel [28]. Property (A7-II) is the version of the dynamic programming principle (also called recursiveness), introduced in Cheridito, Delbaen and Kupper [11], adapted to the setup of our paper, that is, it is stated in terms of dividend processes rather than value process as in [11]. Properties (A7-I) and (A7-II) are equivalent, and they are also sometimes called strong dynamic consistency property. To the best of our knowledge, properties (A7-III) and (A7-IV) were first introduced in the context of random processes in Acciaio, Föllmer and Penner [1], and they were called acceptance and rejection consistency, respectively. In the same paper, Acciaio, Föllmer and Penner introduced condition (A7-V) and they called it weakly acceptance consistent.

For corresponding definitions in case of random variables rather than random processes we refer to the survey paper by Acciaio and Penner [2] and references therein.

It easy to show that the dynamic consistency condition (A7) is stronger than (A7-V), and it is weaker than (A7-I) or (A7-II). Also note that since conditions (A7-II) and (A7-III) taken together are equivalent to (A7-II), then, taken together they imply (A7). However, the inverse implication is not necessarily true.

We conclude this subsection with the following result.

Proposition 4.2.

If is a dynamic coherent risk measure, then , for all , , and .

Proof.

Given some fixed and , denote by . Then, by translation invariance (A6) of , we deduce

| (4.2) |

for all . In particular, for , we have . Hence, by (A4)-homogeneity of , it follows that , for all . Combining this with (4.2) we get , and consequently , for arbitrary positive . Thus, we conclude that , and hence . With this, by (4.2), the proposition follows. ∎

Note that, in particular, , for all .

4.2 Duality between DCAI and DCRM

We start this section with several definitions that will be used in the main results derived here.

Definition 4.3.

A family of dynamic coherent risk measures is called increasing if , for all , , and .

Definition 4.4.

A dynamic acceptability index is called right-continuous if , for all , , and .

Definition 4.5.

A family of dynamic coherent risk measures is called left-continuous at , if , for all , , and .

Theorem 4.6.

Assume that is a normalized dynamic coherent acceptability index. Then, the set of functions , defined by

| (4.3) |

for all , and , is an increasing, left-continuous family of dynamic coherent risk measures.

Proof.

First we will show that defined by (4.3) is well-defined. Since is normalized, for all , , there exist two finite constants and such that

for all . Hence, for every , the set is not empty, and . From here we conclude that infimum from (4.3) is finite, and hence is well-defined.

Next we will show that , satisfies properties (A1)-(A7). By (D1)-adaptiveness and (D2)-independence of the past of , property (A1) and (A2) for , follow immediately.

Assume that and are such that for all and . Then for , and and by (D3), monotonicity of

| (4.4) |

for all and . From here, we deduce the following inclusion

Taking infimum of both sets, follows. Similarly, the homogeneity of follows from the scale invariance of .

Next we show that satisfies . Let , and , and let us take such that

Then, by (D5), quasi-concavity of , we have

and therefore by (D4), scale invariance of , we get . This implies that . Hence,

| (4.5) |

Note that the above inequality holds true for all and . By taking infimum in (4.5), first with respect to , and then with respect to , we have, , and hence is checked.

Now we will show that satisfies (A6), translation invariance. Fix an , , and an -measurable random variable . Denote by the unique element of partition of such that . This yields that the cash-flows and agree on the set , and for all times . Then, for any constant , we have

By (D2), independence of the past of , we have

Since is -measurable, by (D6), translation invariance of , we have

Combining the above with (4.3), we deduce

Since is arbitrarily chosen in , we obtain , for all , and (A6) is checked.

Next we will show that satisfies , dynamic consistency. Assume that , and are fixed, and denote by and . Then , for all and for any . Due to the finiteness of the probability space , there exists a number , such that , for all . By (D2), independent of the past of , we have

for all . Since, , then, by (D7)

Consequently, since is a constant, by (D6)

for all and . By the definition of , we get

for all and . Hence, , or equivalently . Similarly, one can show that

and thus (A7) is established.

All the above imply that is a DCRM for every .

Monotonicity of with respect to follows immediately from (4.3) and the inclusion

Finally, we will show that is left-continuous. Let be any positive number. Then,

| (4.6) |

If the above inequality holds strictly, then there exists a constant such that,

| (4.7) |

Note that is an non-decreasing function with respect to . Therefore, the second inequality in (4.7) implies that, , for all . Hence, by (D3), monotonicity of , , for all , and thus . On the other hand, by the first inequality in (4.7), we deduce that, Contradiction. Therefore, we should have strict equality in (4.6).

This completes the proof. ∎

Next Theorem shows the representation of a DCAI in terms of a family of DCRMs.

Theorem 4.7.

Assume that is an increasing family of dynamic coherent risk measures. Then the function defined as follows,

| (4.8) |

for , and , is a normalized, right-continuous, dynamic coherent acceptability index. Here, we assume .

Proof.

Note that the assumption guarantees that from (4.8) is well-defined and takes values in .

In the following, we will prove that defined in (4.8) satisfies properties (D1)–(D7).

(D1) - adaptiveness, (D2) - independence of the past, (D4) - scale invariance, and (D6) - translation invariance follow immediately from the definition of , and from adaptiveness (A1), independence of the past (A2), homogeneity (A4) and translation invariance (A6) of , respectively.

Let , , and assume that for all , and . By (A3), monotonicity of , we have

| (4.9) |

Note that, for any , we have , which combined with (4.9) implies . Therefore,

By taking supremum of both sides, (D3) follows.

Next we will prove that is quasi-concave. For given , and , if are such that , then, by definition (4.8) of , and monotonicity of in , we conclude that for any ,

By (A4), homogeneity of , we note that for any and ,

From here, by (A5), subadditivity of , we get

for any . Hence , and thus, by definition (4.8) of , we have, . This yields quasi-concavity of .

Assume that , and is an -measurable random variable. By (4.8) and (A6), we get

for all and . Hence, satisfies property (A6).

Now, let us show that satisfies dynamic consistency property (D7). Assume that , and are such that for all , and there exists a non-negative -measurable random variable such that for all . By definition (4.8)

for all . Let us fix an , and denote by . There exists a such that . From the above inequality, we conclude that for all

Then, for all and , , which consequently implies that

| (4.10) |

Also note that , for any . By monotonicity of with respect to , we have . Due to the finiteness of , (4.10) implies that , for all . Using (A7), dynamic consistency of , we get the following

Equivalently,

| (4.11) |

for all , and .

If , for some , then there exists a constant such that

This implies that , that contradicts with (4.11). Therefore,

and by (4.8), we have

| (4.12) |

By similar arguments, one can show that

| (4.13) |

Since was arbitrarily chosen, by (4.12) and (4.13), we finally conclude that,

Thus (A7) is checked.

Let us show that is right-continuous. Given and , we have

for any constant . Taking the supremum of both sides, and then the limit of the right hand side as , we get

| (4.14) |

If the above inequality holds strictly, then there exists such that

| (4.15) |

The second inequality implies that

By monotonicity of , we deduce that . Since the last inequality holds true for all , we have that , that contradicts with first strict inequality in (4.15). Therefore, we have equality in (4.14). Using this equality, and (A6), translation invariance of , we write

and right continuity of is established.

Finally, we will prove that is normalized. Given a fixed , consider the following cash-positions

Recall that . By (4.8) and (A6), we have

Similarly, one can show that .

The proof is complete.

∎

We conclude this section with the main result that provides a representation of a DCAI in terms of a family of DCRMs, and vise versa, a representation of DCRM in terms of a DCAI.

Theorem 4.8.

-

(i)

If is a normalized, right-continuous, dynamic coherent acceptability index, then there exists a left-continuous and increasing family of dynamic coherent risk measures

, such that(4.16) -

(ii)

If is a left-continuous and increasing family of dynamic coherent risk measures, then there exists a right-continuous and normalized dynamic coherent acceptability index such that,

Here we assume that and .

Proof.

(i) For every , define as follows,

| (4.17) |

for all , and . By theorem 4.6, is an increasing, left-continuous, family of dynamic coherent risk measures. We will show that

for all and .

For any , , and , we have

By (4.17) , and hence,

Since the above inequality holds true for all , we conclude that

Similarly, one can show that .

(ii) Define the function as follows,

| (4.18) |

for all , and . By theorem (4.7), is a right-continuous and normalized dynamic coherent acceptability index. Finally, one can check that

for all , and . ∎

5 Special Construction of DCAIs

It is known, that a dynamic coherent risk measure has a representation similar to (2.2). One of the important discoveries done in the process of robust representation of dynamic risk measures, similar to (2.2), was that due to dynamic consistency property (A7), the set of probability measures has to posses some additional features, which depend on how the dynamic consistency property (A7) is formulated. A set of probability measures having such additional features is referred to as a dynamically consistent set of probability measures (or, for short, a consistent set of probability measures).

In Section 5.1 we present our version of the concept of dynamically consistent set of probability measures, as well as some non-trivial examples of such sets. It is seen that our concept is different from the ones previously studied in the literature. Its form and properties have been dictated by the goal of using it in the context of robust representation of our DCAI.

In Section 5.2 we prove the representation theorem for DCRM in terms of consistent sets of probability measures. We conclude this section with representation theorem for DCAIs in terms of families of sequences of dynamically consistent sets of probability measures.

5.1 Dynamically consistent sequence of sets of probability measures

In this section we shall discuss the concept of dynamically consistent sequence of sets of probability measures.

In what follows we denote by the set of all absolutely continuous probability measures with respect to the underlying probability , and will stand for the set of all equivalent probability measures with respect to . Recall that our standing assumption is that has full support. Note that in this case, due to the finiteness of , the set consists of all probability measures on , and also coincides with the set of all probability measures on of full support.

Definition 5.1.

A sequence of sets of probability measures , with , is called dynamically consistent with respect to the filtration , if the following inequalities hold true

| (5.1) |

for every , , and every random variable .

Definition 5.2.

A set of probability measures is called consistent with respect to filtration , if the following equality holds true

| (5.2) |

for every , and every random variable .

Proposition 5.3.

If a set of probability measures is consistent, then with , is dynamically consistent.

Proof.

If is strongly consistent, then, for every -measurable random variable , and , we have

| (5.3) |

Since is a constant, then, for each , we have,

Therefore,

The last equality together with (5.3) imply

Finally note that for any set of probability measures , we have

| (5.4) |

for every , , and every random variable . ∎

The rest of the subsection is dedicated to examples of dynamically consistent sequences of sets of probability measures.

Example 5.4.

Singleton set , with , is clearly strongly consistent. By Proposition 5.3 the constant sequence is dynamically consistent. For simplicity of writing, we will denote this sequence by .

Example 5.5.

It is not hard to show that

This implies that the set of all equivalent probability measures with respective to , is consistent. Hence, the constant sequence is dynamically consistent.

Example 5.6.

Let be a real number. The following set of probability measures

is consistent.

First note that

for every and -measurable bounded random variable . Next we will show that the converse inequality also holds true and hence, by definition, is consistent. Towards this end, assume that , is an -measurable random variable, and ; all arbitrary but fixed in what follows. For convenience, we denote by the set of partition such that . Note that .

Pick up arbitrarily probability measures from , and denote them by , , . Some of them are allowed to be the same. We will construct a new probability measure based on the above set of probabilities. For any , , and we put

Note that , , , is a partition of , and hence is well-defined, and since all probability measures in are of full support, is finite for all . It is also easy to show that , and thus is a probability measure.

Next we will prove that . On any set , we have

Thus, , and by tower property, for all , we also have . Consequently, we get

| (5.5) |

On the other hand, for any , we have,

Since , we have that , and thus . This implies that . Hence, , and therefore,

Since the above holds true for any , we have that

By similar arguments as above, inductively, one can show that

for any . Combining this with (5.5), we conclude that .

Next let us evaluate . Consider a new random variable , defined as follows:

Then, for any , we can deduce that

| (5.6) |

For convenience, we put . Note that

Hence,

By the definition of , we note that

Then,

From here, using the fact that , we conclude that

Since , we have that . Consequently, the following inequality holds true

By (5.6), it follows that

from which we continue

and since, this is true for all , we have

Summing both sides of the last inequality over , we have

or equivalently,

This concludes the proof that is consistent.

Remark 5.7.

It is easy to show that for any ,

In particular, , for any and . Different probabilities in can be regarded as different opinions about the distribution of cash-flows; the above inequality provides an upper bound of these probabilities in terms of the underlying probability .

Example 5.8.

By similar arguments as in previous examples, one can show that the set of probability measures defined as follows

is a consistent set of probability measures.

Example 5.9.

In this example we construct a dynamically consistent sequence of sets probability measures that is not constant sequence of consistent sets of probability measures.

Let , be a sequence of probability measures in such that , for . Consider the following sequence of sets of probability measures . It is easy to show that

| (5.7) |

This implies that is a dynamically consistent sequence of sets of probabilities measures. Clearly it is not a constant sequence.

5.2 Representation Theorem of DCRM

In this section we will present a representation theorem for dynamic coherent risk measures in terms of dynamically consistent set of probabilities. These results combined with the results from Section 4.2 about duality between DCAI and DCRM will lead to a representation theorem for dynamic coherent acceptability indices.

Theorem 5.10 (Representation Theorem for DCRM).

A function is a dynamic coherent risk measure if and only if there exists a dynamically consistent family of sets of probabilities such that,

| (5.8) |

Proof.

Sufficiency. It is not hard to show that defined in (5.8) is a dynamic coherent risk measure. (A1)-(A6) are checked similarly as in existing literature (see for instance [28]), and for interest of saving space we will not check them here. We will show only that (A7), dynamic consistency, is satisfied.

Since is dynamically consistent, we have,

for any , and .

Similarly, one can show that , for every . Thus (A7) is satisfied.

Necessity. The set will be constructed explicitly. Fix a time . Recall that denotes the partition of that corresponds to . Also, we will denote by the partition of generated by , for some future time . Thus . Assume that is fixed for some , and define the following probability space with,

and for each .

Let us denote by the set of all random variables on . There exists a one-to-one correspondence between and the set . The map can be defined as follows: for any , put

| (5.9) |

and vise versa, for any , define

| (5.10) |

for , , and .

Consider the following map with,

| (5.11) |

We claim that is a static coherent risk measure, i.e. satisfies the properties (R1)-(R4) of Definition 2.3. Indeed, for any , such that , we have, , for all and . Then, by (A3), the monotonicity of , we get , for . Therefore, by (5.11), , i.e. satisfies (R1).

Note that for all and , by (5.9), we have,

for all and . From here, by (5.11) and using homogeneity of , the homogeneity (R2) of follows.

Next we will show that satisfies (R3). For all and , by (5.9), we have,

for all and . Therefore, by (5.11) and (A6), translation invariance of , we deduce

for all .

To show that satisfies (R4), consider an . By (5.9) , for all and , and therefore, by (5.11) and (A5), subadditivity of , we obtain

From all the above, we conclude that is a static coherent risk measure. By Theorem 2.4, representation of static coherent risk measures, there exists , a set of absolutely continuous probability measures with respect to on , such that

By (5.11), we have,

| (5.12) |

Since there is one-to-one map between and , for any , we also can write

| (5.13) |

Fix a time , and denote by the process . By (A6)-translation invariance and (A2)-independence of the past of , it follows that , . Hence, by (5.13),

| (5.14) |

Note that . Thus, (5.14) implies

Similarly, one can show that . Thus we derive that

and consequently

This yields that

| (5.15) |

For any , define as follows

It is straightforward to show that is a probability measure on for every .

For all , we can derive,

Hence, by (5.13), we have

| (5.16) |

Since satisfies (A6) and (A7), we deduce that

Thus, (5.13) and (5.16) imply,

Since the above equality holds true for all , it also holds true for . Hence, we have

| (5.17) |

On the other hand, by (5.10), one gets

Thus,

| (5.18) |

By (5.17) and (5.18) we conclude that

and hence

| (5.19) |

for all , and . Therefore, we can rewrite (5.16) as follows,

| (5.20) |

for all , and .

To summarize, for every , we constructed a set of probability measures on . Having these sets, we define as follows:

where stands for cardinality of the set .

By direct evaluations, one can show that , is a set of probability measure on .

Next we will show that (5.8) is fulfilled. Note that, for all ,

If , then there exists such that

| (5.21) |

However, for constructed by , as previously proved,

that contradicts (5.21). By the same arguments, one can show that the inequality

can not hold true, and thus, we conclude that

and by (5.20),

To complete the proof we need to show that is a dynamically consistent sequence of sets of probability measures. Recall that by (A7), dynamic consistency of ,

| (5.22) |

for all and . Using this, we get

for any and . Consequently, we obtain

| (5.23) |

Similarly, by (5.22)

and hence

| (5.24) |

This completes the proof. ∎

Remark 5.11.

An interesting question is whether the sequence appearing in the representation (5.8) can be replaced with a constant sequence of sets of probability measures. The question is motivated by the following observation:

First note that

for any set of probability measures , the following inequality holds true

| (5.25) |

for every , , and every random variable . Thus, if the set additionally satisfies the following weak consistency condition

| (5.26) |

then the constant sequence , is dynamically consistent. Observe that in Example 6.2 we indeed have that

where . Note however that satisfies consistency condition (5.2) which is stronger than (5.26).

5.3 Representation of DCAIs

Having derived a representation theorem for dynamic coherent risk measures in terms of sets of probability measures, and having derived the duality between DCRM and DCAI we can present the final results of this paper: duality between DCAI and sets of probability measures.

Definition 5.12.

A family of sequences of sets of probability measures

is called increasing

if , for all and .

Theorem 5.13.

Assume that is an increasing family of dynamically consistent sequences of sets of probability measures. Then, the function defined as follows,

| (5.27) |

is a normalized and right-continuous dynamic coherent acceptability index.

Theorem 5.14.

If is a normalized and right-continuous dynamic coherent acceptability index, then there exists a family of dynamically consistent sequences of sets of probability measures such that

Here we adopt the usual convention that and .

Remark 5.15.

We want to mention that the static AI is a particular case of the DCAI developed in this paper and corresponds to . Same is true for the representation theorem for static AI in terms of family of sets of probability measures.

6 Examples

Theorem 5.13, besides being a fundamental theoretical result, can serve as basis for construction of DCAIs by means of constructing increasing sequences of dynamic sets of probability measures. Using this idea, we present here some abstract, non-trivial, examples of DCAIs.

Example 6.1.

Dynamic upper-limit ratio.

Assume that is an increasing function.

Define as follows,

and let . Note that , where , is defined in Example 5.6, and thus is dynamically consistent for any . Also observe that monotonicity of implies monotonicity of with respect to . Hence, by Theorem 5.13,

is a normalized and right-continuous dynamic coherent acceptability index. We call it dynamic upper-limit ratio.

Example 6.2.

Dynamic lower-limit ratio.

Similarly, using Example 5.8, we consider

, for some increasing, non-negative function .

Then, is dynamically consistent,

and by Theorem 5.13, the function defined by (5.27)

with , is a normalized and right-continuous dynamic coherent acceptability index.

We call it dynamic lower-limit ratio.

Example 6.3.

(Continuation of Example 5.9)

In Example 5.9 we constructed a non-constant dynamically consistent sequence of sets of probability measures. In view of (5.7) the corresponding family of risk measures satisfies

The point that we are making here is that the infimum over a time dependent set can be replaced by the infimum over time independent set (see also Remark 5.11 in this regard).

Example 6.4.

Dynamic Gain Loss Ratio.

Gain Loss Ratio (GLR) is a typical return-to-risk type of performance measure, very popular among practitioners. We recall that it is defined as the ratio of expectation of positive returns to expectation of negative returns:

, if , and zero otherwise.

As shown in [13], GLR is a (static) coherent acceptability measure.

Here we present a dynamic version of GLR, denoted by dGLR, and defined as follows:

| (6.1) |

where and . Note that taking , dGLR becomes the static GLR.

We argue that dGLR is a normalized and right-continuous dynamic coherent acceptability index. Indeed, since and , we have that dGLR is normalized. Right-continuity follows from linearity of expectation and continuity of function . Adaptiveness (D1), and independence of the past (D2) of dGLR follow directly from the definition. Monotonicity (D3), scale invariance (D4), and quasi-concavity (D5) are verified as in static case with expectation replaced by conditional expectation (for details see [13]).

Since , and , for all , (D6), translation invariance, follows.

Finally we will prove that dGLR satisfies (D7), dynamic consistency property. Assume that is an -measurable random variable, and such that and . Assume that , and . By definition of dGLR, we have, , and since , we have

which implies that . If or , then clearly .

Similarly, one can show that if , and , then .

Thus, we conclude that dGLR is a DCAI.

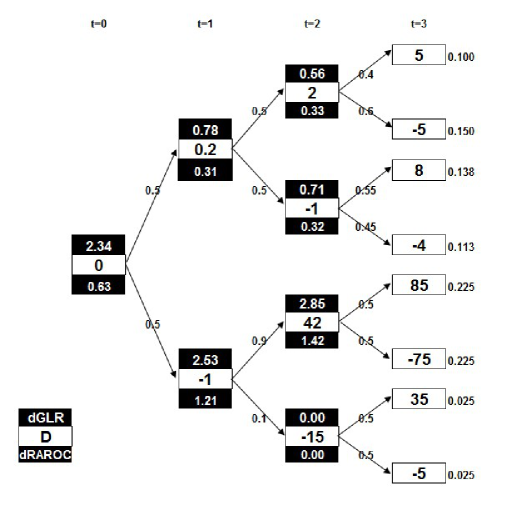

Example 6.5 (Counterexample).

Taking into account the general form of a dynamic acceptability index (cf. (5.27)), and the general form of a static one (cf. (2.1)), the natural question arises: is it possible to dynamize a static coherent acceptability index by taking the appropriate ‘conditional quantity’ of the cumulative future cash-flow? For example, to dynamize GLR, we consider the static GLR, and replaced in it the expectation with conditional expectation, and the terminal value with future cumulative cash-flow. However, this procedure is not valid in general. The natural extension of static Risk Adjusted Return on Capital (RAROC) to a dynamic setup has the following form:

with convention if .

As it is seen from Figure 1, which represents a numerical example, dRAROC does not satisfy property (D7), dynamic consistency. In this example, we consider . Assume that the states are labeled from top to bottom . Note that, , i.e. positive cashflow at time and state , but , as well as . Thus dRAROC does not satisfy (D7) and hence it is not a DCAI.

For comparison reasons, we also present in Figure 1 the values of dGLR, which is a DCAI.

References

- [1] B. Acciaio, H. Föllmer, and I. Penner, Risk assessment for uncertain cash flows: Model ambiguity, discounting ambiguity, and the role of bubbles, preprint (2010).

- [2] B. Acciaio and I. Penner, Dynamic risk measures, preprint (2010).

- [3] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath, Thinking coherently, Risk 10 (1997), 68–71.

- [4] , Coherent measures of risk, Math. Finance 9 (1999), no. 3, 203–228.

- [5] P. Artzner, F. Delbaen, J.-M. Eber, D. Heath, and H. Ku, Coherent multiperiod risk adjusted values and bellman’s principle, Ann. Oper. Res. 152 (2007), 5–22.

- [6] A. Bernardo and O. Ledoit, Gain, loss, and asset pricing, Journal of Political Economy 108 (2000), 144–172.

- [7] J. Bion-Nadal, Time consistent dynamic risk processes, Stochastic Process. Appl. 119 (2009), no. 2, 633–654.

- [8] P. Carr, H. Geman, and D.B. Madan, Pricing and hedging in incomplete markets, J. Fin. Econ. 62 (2001), no. 1, 131–167.

- [9] P. Cheridito, F. Delbaen, and M. Kupper, Coherent and convex monetary risk measures for bounded càdlàg processes, Stochastic Process. Appl. 112 (2004), no. 1, 1–22.

- [10] , Coherent and convex monetary risk measures for unbounded càdlàg processes, Finance Stoch. 9 (2005), no. 3, 369–387.

- [11] , Dynamic monetary risk measures for bounded discrete-time processes, Electron. J. Probab. 11 (2006), no. 3, 57–106.

- [12] P. Cheridito and T. Li, Risk measures on Orlicz hearts, Math. Finance 19 (2009), no. 2, 189–214.

- [13] A.S. Cherny and D.B. Madan, New measures for performance evaluation, The Review of Financial Studies 22 (2009), no. 7, 2571–2606.

- [14] J. Cvitanic and I. Karatzas, On dynamic meaures of risk, Finance Stoch. 3 (1999), no. 4, 451–482.

- [15] F. Delbaen, Coherent risk measures, Scuola Normale Superiore, 2000.

- [16] , Coherent risk measures on general probability spaces, Advances in finance and stochastics, Springer, 2002, pp. 1–37.

- [17] F. Delbaen, S. Peng, and E. Rosazza Gianin, Representation of the penalty term of dynamic concave utilities, Finance and Stochastics 14 (2010), 449–472, 10.1007/s00780-009-0119-7.

- [18] K. Detlefsen and G. Scandolo, Conditional and dynamic convex risk measures, Finance Stoch. 9 (2005), no. 4, 539–561.

- [19] H. Föllmer and A. Schied, Convex measures of risk and trading constraints, Finance Stoch. 6 (2002), no. 4, 429–447.

- [20] , Robust preferences and convex measures of risk, Advances in finance and stochastics, Springer, 2002, pp. 39–56.

- [21] H. Föllmer and A. Schied, Stochastic finance, extended ed., de Gruyter Studies in Mathematics, vol. 27, Walter de Gruyter & Co., Berlin, 2004, An introduction in discrete time.

- [22] M. Frittelli and E. Rosazza Gianin, Putting order in risk measures, Journal of Banking and Finance 26 (2002), 1473–1486.

- [23] , Dynamic convex measures, 2004, pp. 227–248.

- [24] , Law invariant dynamic convex measures, 2005, pp. 227–248.

- [25] M. Frittelli and G. Scandolo, Risk measures and capital requirements for processes, Math. Finance 16 (2006), no. 4, 589–612.

- [26] A. Jobert and L.C.G. Rogers, Valuations and dynamic convex risk measures, Math. Finance 18 (2008), no. 1, 1–22.

- [27] S. Kusuoka, On law invariant coherent risk measures, Advances in mathematical economics, Vol. 3, Adv. Math. Econ., vol. 3, Springer, 2001, pp. 83–95.

- [28] F. Riedel, Dynamic coherent risk measures, Stochastic Process. Appl. 112 (2004), no. 2, 185–200.

- [29] B. Roorda, J.M. Schumacher, and J. Engwerda, Coherent acceptability measures in multiperiod models, Math. Finance 15 (2005), no. 4, 589–612.

- [30] W.F. Sharpe, Mutual fund performance, Journal of Business 39 (1966), 119–139.

- [31] F.A. Sortino and L.N. Price, Performance measurement in a downside risk framework, The Journal of Investing 3 (1994), no. 3, 59–64.

- [32] S. Tutsch, Update rules for convex risk measures, Quant. Finance 8 (2008), no. 8, 833–843.

- [33] S. Weber, Distribution-invariant risk measures, information, and dynamic consistency, Math. Finance 16 (2006), no. 2, 419–441.