Hermitian and non-Hermitian covariance estimators for multivariate Gaussian and non-Gaussian assets from random matrix theory

Abstract

The random matrix theory method of planar Gaussian diagrammatic expansion is applied to find the mean spectral density of the Hermitian equal-time and non-Hermitian time-lagged cross-covariance estimators, firstly in the form of master equations for the most general multivariate Gaussian system, secondly for seven particular toy models of the true covariance function. For the simplest one of these models, the existing result is shown to be incorrect and the right one is presented, moreover its generalizations are accomplished to the exponentially-weighted moving average estimator as well as two non-Gaussian distributions, Student t and free Lévy. The paper revolves around applications to financial complex systems, and the results constitute a sensitive probe of the true correlations present there.

pacs:

02.50.Cw (Probability theory), 05.40.Ca (Noise)I Introduction

An important problem in various fields of science featuring systems of a large number of time-dependent objects is to unravel correlations between these objects, either at the same or at distinct time moments (Sec. I.1.1). This knowledge may be gained from the past realized values of the correlations, although it is obscured by a measurement noise caused by an insufficient amount of information in any such time series (Sec. I.1.2). This paper discusses how to account for this noise in applications to models of complex systems which exhibit properties such as sectors of increased cross-correlations (Sec. I.2.1) or vector autoregression type of temporal dynamics (Sec. I.2.2).

Often in the below discussion the reference point will be financial markets—systems which are very complex, relevant for everyday life, accessible to empirical study and with the underlying mechanisms full of question marks—however, the results are beneficial for all kinds of complex systems, such as in brain science KwapienDrozdzIoannides2000 or meteorology MayyaAmritkar2006 .

I.1 Gaussian covariance functions and their historical estimation

I.1.1 Gaussian covariance functions

Random matrix theory approach to complex systems. Consider a system of real variables (labeled by ), and each one of them is observed throughout consecutive time moments (separated by some time ); let the value of object at time be denoted by , all of which constitute an matrix . For such a large complex system, a standard approach is to replace complexity by randomness, i.e., assume that is a random matrix, endowed with some joint probability density function (JPDF) , and investigate its statistical properties (here: the mean density of its eigenvalues), which then should help understand some of the generic features of the underlying complex system. Since there are two discrete dimensions here—spatial and temporal—random matrix theory (RMT) is a natural framework for doing that.

Gaussian approximation. In most of the paper is chosen Gaussian of zero mean. This is an important restriction because the density of eigenvalues is not universal, i.e., it depends on the specific form of . Even worse, for complex financial systems this JPDF is typically far from Gaussian (cf. App. A for an introduction to non-Gaussian effects on financial markets).

The Gaussian approximation is dictated by analytical difficulties—it leads to complicated solutions yet much more tractable than in a non-Gaussian case—hence, it is a natural place to begin the analysis. Furthermore, it does provide a basis for non-Gaussian extensions, e.g., to the Student t-distribution through random volatility models, in which one considers the variances to be random variables (cf. App. A.2 for an introduction and Sec. III.2.7 for an application), or to the free Lévy distribution through free probability calculus (cf. Secs. II.3.3, III.2.8).

Covariance functions. A real multivariate Gaussian distribution of zero mean is fully described by a two-point covariance function,

| (1) |

where the brackets stand for the averaging over . The attention in the literature has been mainly on the equal-time () covariances, described by an real symmetric matrix , where stationarity (independence of ) has been assumed. This paper revolves around a more involved object, the time-lagged () covariances, described by an real time-dependent matrix , obeying , where translational symmetry in time (over the considered period ) has again been assumed.

I.1.2 Measurement noise

Unbiased estimators. A basic way to experimentally measure the above covariance matrices for a given complex system is to take a historical time series of some length of the values , compute the realized covariances or , and average them over the past time moments —this results in unbiased estimators which in the matrix notation read

| (2a) | ||||

| (2b) | ||||

Weighted estimators and the EWMA. Other choices are also in use, e.g., ``weighted estimators'' in which the past realized returns are multiplied by some real and positive weights , (i) the smaller the older the data (i.e., this sequence increases with ) which reflects the fact that older measurements are less relevant for today estimation of the covariance, and (ii) obeying the sum rule to make this case consistent with [(2a), (2b)]. Denoting , this prescription is equivalent to , i.e.,

| (3a) | ||||

| (3b) | ||||

In yet other words, this is equivalent to the standard estimators [(2a), (2b)] with a modified true covariance, .

A typical example is the ``exponentially-weighted moving average'' (EWMA),

| (4) |

with just one parameter, , defining the exponential suppression of the older data with the characteristic time . Estimator [(3a), (4)] (with ) is widespread in financial industry through the RiskMetrics 1994 methodology of risk assessment RiskMetrics1996 ; MinaXiao2001 .

Measurement noise and thermodynamic limit. A fundamental obstacle for practical usage of the estimators is that a description by a finite time series will necessarily incur inaccuracies—since time series of length (i.e., quantities) are used to estimate the independent elements of the ``true'' covariance matrix, the error committed (the ``noise-to-signal ratio'') will be governed by the ``rectangularity ratio'' of , . In other words, and are consistent estimators of and , respectively, i.e., they tend to the true values as (i.e., for large compared to , which is a standard limit in statistics). On the other hand, a more practically relevant regime is when both and are large and of comparable magnitude—such as several hundred financial assets sampled daily over a few years—which is modeled by the ``thermodynamic limit,'' being a standard limit in RMT,

| (5) |

In this case, the estimators reproduce the true values of the covariances but with additional marring with the ``measurement noise,'' the more pronounced the larger .

One might immediately propose to further and further increase the observation frequency (i.e., decrease , i.e., increase , i.e., decrease ) in order to suppress the noise, but unfortunately this procedure is limited by the Epps effect (cf. the end of App. A.2.2)—the very object one is measuring, the covariance matrix, changes with the observation frequency above its certain level.

Remark that the thermodynamic limit should be combined with the following limits:

(i) The RMT methods used in this paper are valid only provided that

| (6) |

Otherwise, finite-size effects would become relevant, as illustrated in Fig. 7 (a).

(ii) For the EWMA estimators [(3a), (3b)], one should additionally take

| (7) |

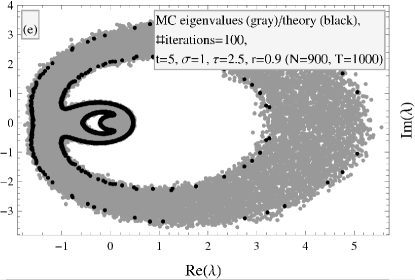

since then the characteristic time stretches over the scale of the entire time series. Unfortunately, the limits (6) and (7) are incompatible with each other due to , thus the theoretical results will reproduce Monte Carlo simulations with some discrepancy, albeit not very big, especially well inside the bulk [cf. Fig. 3 (a)].

Noise cleaning of the equal-time covariance estimator. A basic way to observe the measurement noise is by comparing the eigenvalues of the equal-time covariance matrix and its estimator . They are important because they represent uncorrelated causes (``principal components,'' ``explicative factors'') for the correlations of the objects at the same moment of time (the temporal index will thus be skipped below); indeed, diagonalizing the (symmetric and positive-definite) matrix , , yields a linear decomposition, , into uncorrelated factors of variances given by the eigenvalues, . This procedure is known as the ``principal component analysis'' (PCA). A financial interpretation is that the eigenvectors describe uncorrelated portfolios (investments of part of one's wealth into asset ) while the corresponding eigenvalues quantify their risks (this is important for the Markowitz risk assessment method Markowitz1952 ).

The simplest situation is , in which case the mean spectrum of the estimator (which is known as the ``Wishart random matrix'' Wishart1928 ) is given by the famous ``Marčenko-Pastur (MP) distribution'' MarcenkoPastur1967 (cf. App. C.1 for derivation). In other words, the single eigenvalue is ``smeared'' by the measurement noise over the interval , where , with a density (235).

In the seminal papers LalouxCizeauBouchaudPotters1999 ; PlerouGopikrishnanRosenowAmaralStanley1999 (the results below come from LalouxCizeauBouchaudPotters1999 ; cf. Fig. 1 there), the empirical spectral density of the estimator derived from financial returns of the S&P500 index, sampled over days (i.e., ), has been fitted by the MP distribution. A fit with happened to well describe most of the spectrum, except two regions, comprised of c.a. of the eigenvalues: (i) One small peak around a very big eigenvalue (c.a. times larger than ). (ii) Several well-separated peaks just above . Moreover, the eigenvector , which represents an approximately equal investment in all the assets—a very risky portfolio, depending on the behavior of the market as a whole, and thus called the ``market mode.'' In the first approximation, , i.e., just one factor, the market, governs the behavior of all the assets. Furthermore, the eigenvectors corresponding to the intermediate peaks describe portfolios of strongly correlated assets from industrial sectors. To summarize, the bulk of the spectrum may be thought to represent a pure noise, whereas the spikes which leak out of it carry relevant information about the true structure of equal-time correlations.

This use of the MP distribution for discerning the true information from noise has led to a number of ``cleaning schemes'' devised to construct a covariance matrix which better reflects experimental data. For instance, in the ``eigenvalue clipping'' method LalouxCizeauPottersBouchaud2000 , consists of the empirical eigenvalues lying above and their eigenvectors, while the eigenvalues below the upper MP edge, supposedly originating purely from the measurement noise, are all replaced by a common value such that the trace of the covariance matrix is unaltered. This scheme has been argued BouchaudPotters2009 to slightly outperform classical cleaning methods such as the ``shrinkage algorithm'' LedoitWolf2004 .

These discoveries commenced a series of applications of RMT to econophysics. In particular, an important research program is to construct more realistic ``priors'' which—unlike the trivial case above—already incorporate some features of the market, then perform the PCA of the estimator , and compare it with empirical data. More generally, one should assume a certain JPDF , dependent on parameters which describe some aspects of the market dynamics, and compare the spectra of both estimators and with empirical data, thereby assessing the parameters of the selected JPDF. In particular, quite naturally, it will be demonstrated that true correlations between different assets but at the same moment of time are more visible in the spectrum of , while becomes very useful for investigating true time-lagged correlations. In the next Sec. I.2, a few such forms of the JPDF used in this paper will be introduced.

I.2 Models of spatial and temporal correlations

As explained above, a basic approach to distinguishing relevant information about the true correlations in a given complex system from the measurement noise inevitably present in any covariance estimator is by comparing the empirical spectrum of an estimator with its theoretical spectrum obtained from the assumption of no correlations; any difference between the two results then from the true correlations. This is Toy Model 1 (Sec. III.2) below. A more advanced version of this program is to assume a certain parametric form of the true correlations, compute the theoretical spectrum of an estimator and compare it with an experiment—this has a potential to more accurately determine the parameters of the system. This Section introduces two important classes of models of the true correlations which will be used for this purpose in the paper.

I.2.1 Industrial sectors

Factor models. In order to construct a prior which would reflect the spike structure visible in the spectrum of , a simple way is through the ``factor models'' [``factor component analysis'' (FCA)].

For instance, a ``one-factor model'' [``market model,'' ``capital asset pricing model'' (CAPM)] Sharpe1964 , sufficient to describe the market mode, assumes that each asset (the temporal index is omitted here) follows a certain factor (the ``market''; a random variable with volatility ) with strength (the ``market beta''), i.e., , where the (the ``idiosyncratic noises,'' with volatilities of comparable magnitude) are uncorrelated with and each other. The cross-covariance matrix reads, , and indeed has one large () eigenvalue plus a sea of small ones.

More generally, a ``-factor model'' Noh2000 ; PappPafkaNowakKondor2005 ; BrinnerConnor2008 further supposes that the idiosyncratic noises depend on hidden factors, corresponding to the industrial sectors, , where the industrial factors and the new idiosyncratic noises have volatilities and , respectively, and are all uncorrelated. The spectrum of the cross-covariance matrix, , may be shown to contain not only the market mode but also the sectorial modes.

Other constructions along these lines exist, e.g., the ``hierarchically-nested factor models'' TumminelloLilloMantegna2007 . Regardless of the model, if the assets are Gaussian and there are no temporal correlations, the matrix can simply be considered diagonal, with an appropriate structure of its eigenvalues.

Power-law-distributed . Another model of has been suggested BouchaudPotters2009 to even better reflect the coexistence of small and large industrial sectors BurdaJurkiewicz2004 ; MalevergneSornette2004 —a hierarchical, power-law distribution of the sector sizes Marsili2002 ,

| (8) |

[this is the density of eigenvalues of defined in (186); it is normalized and yields ], which is described by two parameters, a slope and the smallest sector size [ is the Heaviside theta (step) function].

In BouchaudPotters2009 (cf. Fig. 2 there), U.S. stocks has been observed over days (i.e., ), and shown that the empirical spectrum of , after removing the market mode, is very well fitted with the Wishart distribution with (8), where and .

I.2.2 Vector autoregression models

VAR. A simple yet profound model for the evolution of statistical variables e.g. in macro-economy (cf. the European Central Bank's ``Smets-Wouters model'' SmetsWouters2002 ) or in finances (cf. the ``linear causal influence models'' PottersBouchaudLaloux2005 ) is ``vector autoregression'' (VAR) in which the value of any variable depends linearly on the values of some other variables in some previous times, plus an idiosyncratic noise (the ``error term'') which, in anticipation of the applications below, is chosen complex Gaussian of zero mean and the nonzero covariance ,

| (9) |

[The summation over time is assumed to stretch from , i.e., this is far from the beginning of the dynamics. The ``influence kernel'' .] This recurrence equation can be readily solved,

| (10) |

where certain constraints must be imposed on the kernel to make this sum convergent (to be specified below on simplified examples). Consequently, the variables are complex Gaussian of zero mean and the covariance function translationally symmetric in time (i.e., dependent on ) which reads

| (11) |

SVAR(1). In this paper only quite drastically simplified versions of the VAR model will be considered: (i) The temporal dependence in (9) is only on the previous moment, , for some matrix [this is abbreviated VAR(1)]. (ii) The covariance function of the error terms is trivial in the temporal sector, ; moreover, the spatial covariance matrix will be assumed diagonal, [this is called ``structural VAR'' (SVAR)]. Under these circumstances, the covariance function decays exponentially with the time lag,

| (12) |

where for short, .

diagonal. The matrix will first be chosen diagonal, , which means that there is no correlation between different variables. Then , where for short, , and there must be for all . Hence, the covariance function becomes

| (13) |

i.e., it is diagonal with each term consisting of a distinct (i) proportionality factor ; (ii) exponential decay with the time lag governed by ; (iii) sinusoidal modulation with the time lag governed by (however, the will henceforth be always assumed real, so no oscillations).

Three versions of this model will be investigated in this article: (i) all the equal to each other and equal to each other (Toy Model 3, Sec. III.4); (ii) all the equal to each other but arbitrary (Toy Model 4a, Sec. III.5.1); (iii) arbitrary and (Toy Model 4b, Sec. III.5.2).

with a market mode. In order to incorporate correlations between different variables, a more involved non-diagonal structure of is required. For instance, to account for the market mode (cf. Sec. I.2.1), one may assume 111This model has been suggested to me by Zdzisław Burda, and initially analyzed with Zdzisław Burda, Giacomo Livan and Artur Świech. that there is one asset (the ``market'') which depends only on itself, , while any other asset depends on the market and on itself, , for , where the beta coefficients , , are identical for all the assets. Consequently, the nonzero matrix elements of read, , , , for (i.e., the diagonal and first column). The covariance function thus becomes

| (14a) | |||

| (14b) | |||

| (14e) | |||

| (14f) | |||

| (14i) | |||

| (14j) | |||

for and (i.e., five distinct matrix entries; the first row and column interchange upon ). It has the following (time-dependent) eigenvalues: (i) an -fold degenerate eigenvalue,

| (15) |

describing the self-interaction of the assets; (ii) two eigenvalues solving the quadratic equation

| (16) |

[one of them is large as ], describing the interactions of the market with itself and individual assets with the market. This is the content of Toy Model 4c, initially analyzed in Sec. III.5.3.

II Master equations

II.1 Outline

II.1.1 Random matrix models

| Case 1 [(19a), (19b)] | Case 2 (41) | Case 3 (73) | Case 2 + 3 (83) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| , | , | ||||||||

| Gaussian | free Lévy | free Lévy, | |||||||

| ETCE | [(25a), (25b), (27a), (27b), (28), (22)] | (48) (recalculation) | [(51a), (51b)] | (53) | [(77a)-(78b), (28), (22)] | — | — | ||

| TLCE | [(33a)-(33h), (35e), (35j), (28), (22)] | [(54e)-(55j), (35e), (35j), (28), (22)] | (71), borderline: [(72a), (72b)] | (65), borderline: [(66a), (66b)] | [(69a), (69b)] | (LABEL:eq:Case2A1TLCELevyEq02) | [(79a)-(82), (28), (22)] | [(95a)-(95c), (90a), (90b), (88), (94a), (94b), (92), (99)] | [(103a)-(104)] |

The goal of this article is a basic study of the covariance estimators [(2a), (2b)] and [(3a), (3b)]. Actually, a few more assumptions about them will be made (without changing the notation) which do not influence the end results at the leading order in the thermodynamic limit [(5), (6)], but which greatly simplify the calculations: (i) The returns are complex instead of real. (ii) The indices in the Kronecker delta in the delay matrix (2b) are understood modulo , i.e., it is unitary. (iii) The normalization in (2b) is replaced by . Points (ii) and (iii) are easily justified by ; an explanation concerning the crucial point (i) is offered in Sec. II.2.3. To summarize, the following two random matrix models are investigated:

(i) The (Hermitian) ``equal-time covariance estimator'' (ETCE),

| (17) |

(ii) The (non-Hermitian) ``time-lagged covariance estimator'' (TLCE),

| (18) |

[An even more general model (29), which encompasses the weighted TLCE (3b), is also touched upon in Secs. II.2.2 and II.3.2.]

In these definitions, the return matrix consists of complex Gaussian random numbers of zero mean and the covariance function of the form,

| (19a) | ||||

| (19b) | ||||

II.1.2 Mean spectral density

Basic quantities. One quantity only will be calculated for the ETCE and TLCE—their ``mean spectral density'' (MSD) [(186), (203)]. It is introduced in App. B.1.1 (Hermitian case) and App. B.2.1 (non-Hermitian case), where it is also encoded in the form of more convenient objects—the Green function [(188), (LABEL:eq:NonHolomorphicGreenFunctionDefinition)] or the -transform [(189), (208)].

Master equations for various true covariances. The rest of this Section is devoted to deriving the ``master equations'' obeyed by these objects for several cases of the true covariance function (19a): (i) Case 1: Arbitrary (Sec. II.2). (ii) Case 2: Factorized (Sec. II.3). (iii) Case 3: Translationally symmetric in time (Sec. II.4). (iv) Case 2 + 3: Factorized and translationally symmetric in time (Sec. II.5).

All these results are summarized in Tab. 1. They are new discoveries except for the ETCE in Case 2 (Sec. II.3.1), which is presented for (i) completeness; (ii) comparison of the derivation process with the TLCE in the same case (Sec. II.3.2); (iii) an extension to the free Lévy distribution of the returns (in Sec. II.3.1 for the ETCE, then in Sec. II.3.3 for the TLCE).

Application to toy models. These general equations are subsequently (Sec. III) solved for four specific Toy Models (1, 2a, 2b, 3) of the true covariance function, and commented on for three other more involved Toy Models (4a, 4b, 4c); they have already been mentioned in Sec. I.2. Also, it is explained how they can be a basis for extensions to non-Gaussian probability distributions of the returns: Student (Sec. III.2.7) and free Lévy (Sec. III.2.8), as well as the EWMA estimator (Sec. III.2.6).

Techniques of derivation. The method used to obtain the master equations is the planar diagrammatic expansion and Dyson-Schwinger (DS) equations. All its necessary concepts are introduced in a self-contained way in App. B.1.2 (Hermitian case) and App. B.2.2 (non-Hermitian case). Occasionally (Sec. II.3.3), the ``-transform conjecture''—a mathematical hypothesis relating the eigenvalues and singular values of a non-Hermitian random matrix whose mean spectrum possesses rotational symmetry around zero—is alternatively used which greatly simplifies calculations for the relevant models.

Universality issues. Remark also that the MSD is not universal—it depends on the particular probability distribution of the returns, and not only on the symmetries of the problem—but nonetheless it is useful in applications e.g. to finances (cf. Sec. I.1.2). However, for the models with a rotationally symmetric mean spectrum, a universal form-factor is proposed and tested (Secs. III.2.4 and III.3.1) which describes the steep decline of the MSD close to the borderline of its domain.

II.2 Case 1: True covariances arbitrary

In this Section, the general structure of the true covariance function [(19a), (19b)] is assumed, and the technique of Secs. B.1.2 and B.2.2 applied to the ETCE and TLCE [actually, its generalization (29)], respectively.

II.2.1 Equal-time covariance estimator

Step 0: Prior to that, remark that is a product of two Gaussian random matrices, and (the factor could be split between the two terms in a different way, but with such a choice, they are of the same large- order), while the method is used most easily just to Gaussian matrices. To remove this obstacle, a linearization procedure has been proposed GudowskaNowakJanikJurkiewiczNowak2003 , which introduces the larger matrix,

| (20) |

Its basic property is that upon squaring,

| (21) |

it yields a block-diagonal matrix with the blocks being the two possible products of the two terms in question, which means that has the same non-zero eigenvalues as , counted twice (i.e., ), plus zero modes. In other words, the spectrum of consists of -valued square roots of the eigenvalues of , plus zero modes. This translates into a close relationship between the holomorphic -transforms of the two random matrices,

| (22) |

The cost of this linearization is the increase in the dimension of the matrix from to . The four blocks of (and of analogous matrices henceforth) will be denoted by , , , (from left to right and top to bottom), according to their dimensions. For instance, for the Green function matrix (187),

| (23) |

and similarly for the self-energy matrix (cf. the discussion of the 1LI diagrams in App. B.1.2).

Step 1: The nonzero matrix elements of are all Gaussian random numbers of zero mean, hence the full information about them is encoded in the propagators, and the nonzero ones are directly inferred from (19a) to be

| (24) |

Step 2: Knowing the propagators, one may explicitly write the second DS equation (198),

| (25a) | ||||

| (25b) | ||||

and .

Step 3: Since the nonzero blocks of the self-energy matrix lie on its diagonal [(25a), (25b)],

| (26) |

the first DS equation (197) implies that the Green function matrix is also block-diagonal, with and

| (27a) | ||||

| (27b) | ||||

One may say that the first set of DS equations decouples into a spatial and temporal sector; of course, the two sectors are coupled by the second set of DS equations [(25a), (25b)].

Step 4: Eqs. [(25a), (25b), (27a), (27b)] are the master equations for the four matrices, , , , . Their explicit solution may be attempted if the true covariance function has been specified—six examples will be analyzed in Sec. III. Once the two blocks of the Green function matrix are found, adding their traces yields the holomorphic Green function (188) of ,

| (28) |

which is then easily related to the holomorphic Green function of the estimator [(22), (189)], and thereby to its MSD (193).

II.2.2 Generalized time-lagged covariance estimator

Consider the following generalization of the TLCE,

| (29) |

where and are arbitrary constant Hermitian or non-Hermitian matrices (of dimensions and , respectively). [Setting and reduces to .]

Step 0: Before that, the matrix product in (29) should be linearized in order to obtain a Gaussian random matrix,

| (30) |

Analogously to the Hermitian case, the nonholomorphic -transforms of the original and linearized matrices remain in the simple relationship (22), so it is enough to consider only the latter.

Step 1: The non-Hermitian procedure differs from its Hermitian counterpart essentially by one step, which is ``duplication'' [(209)-(211)] of the random matrix in question. Combining the notation from Step 0 of Sec. II.2.1 and (211), the Green function matrix [(209), (210)] will have the block structure

| (31) |

and similarly for the self-energy matrix.

Step 2: The propagators (covariances) of the returns (19a) allow to easily deduce the propagators of the duplicated version (210) of ,

| (32a) | ||||

| (32b) | ||||

| (32c) | ||||

| (32d) | ||||

As explained, since the random matrix in question is Gaussian of zero mean, these propagators carry the entire information about it.

Step 3: The second set of DS equations (198) acquires thus the form,

| (33a) | ||||

| (33b) | ||||

| (33c) | ||||

| (33d) | ||||

| (33e) | ||||

| (33f) | ||||

| (33g) | ||||

| (33h) | ||||

with the remaining blocks of the self-energy matrix zero.

Step 4: The block structure of the self-energy matrix which emerges from [(33a)-(33h)] is such that each of its main four blocks (holomorphic-holomorphic, etc.) is block-diagonal,

| (34) |

and owing to it, the first set of DS equations (197) may be rewritten as two matrix equations (of dimensions and , respectively),

| (35e) | ||||

| (35j) | ||||

Analogously to the Hermitian case [(27a)-(27b)], the first set of DS equations decouples into a spatial and temporal sector.

Step 5: As in the Hermitian case, the nonholomorphic Green function (LABEL:eq:NonHolomorphicGreenFunctionDefinition) of is given by (28), which can a priori be calculated once the master equations [(33a)-(33h), (35e), (35j)] have been solved. Using (22) and [(208), (206)] leads then to the nonholomorphic Green function and MSD of .

As explained in App. B.2.1, another interesting part of the duplicated Green function matrix [(209)-(211)] is the order parameter—the negated product of the normalized traces of its off-diagonal blocks (216),

| (36) |

Recall that it necessarily is a real and nonnegative number, which zeroes only on the borderline of the mean spectral domain, (and ) (217), thus providing a way for its analytical determination.

II.2.3 Complex instead of real assets do not influence the leading order

An argument will now be given why complex instead of real assets lead to much simpler models and yet do not change the end results at the leading order in the thermodynamic limit (5), as anticipated in Sec. II.1.1. Of course, the microscopic properties for these two classes are altogether different, however, they are not the subject of this article; for an advanced calculation of some of such properties for a Wishart matrix with real entries, cf. e.g. RecherKieburgGuhr2010-1 ; RecherKieburgGuhr2010-2 . The proof will be given only for , since for the ETCE it has already been presented in BurdaJurkiewiczWaclaw2005-1 , albeit in a less general setting of the true covariance function factorized (Case 2 below)—it has been demonstrated that all the moments of the ETCE are identical at the leading order for complex or real assets.

If the random variables were real, with the most general structure of the propagator (1), then in addition to [(32a)-(32d)], there would be six nontrivial propagators of , namely between its blocks: and , and , as well as the self-propagators of , , , , e.g.,

| (37) |

etc. This would lead to eight additional nontrivial blocks in the self-energy matrix, those which are zero in (34), e.g.,

| (38) |

etc. In other words, the solutions of all our models would become significantly harder.

However, these new blocks (38) are one order of smaller than [(33a)-(33h)], i.e., may be neglected in the thermodynamic limit. Indeed, if one follows the summation indices in (38), , and treats it like matrix multiplication, one finds that is like one matrix entry of the resulting product, i.e., of order . On the other hand, in e.g. (33a) one has one matrix entry through the summation over , plus a trace from ; this trace contributes an order of , hence is of order .

For instance, in the simplest case of , (the TLCE) and (no correlations; this is Toy Model 1 below, Sec. III.2) and for real assets, the eight entries [(33a)-(33h)] of the self-energy matrix are identical as in the complex case and read

| (39a) | ||||

| (39b) | ||||

| (39c) | ||||

| (39d) | ||||

| (39e) | ||||

| (39f) | ||||

| (39g) | ||||

| (39h) | ||||

however, the eight other entries (38) are now nonzero,

| (40a) | ||||

| (40b) | ||||

| (40c) | ||||

| (40d) | ||||

| (40e) | ||||

| (40f) | ||||

| (40g) | ||||

| (40h) | ||||

but it is clear that they are one order of smaller than the other entries, and thus irrelevant in the thermodynamic limit.

II.3 Case 2: True covariances factorized

In this Section, a special form of the true covariance function (19a) is investigated—factorized into a spatial and temporal part,

| (41) |

where and are some constant Hermitian matrices of dimensions and , respectively, describing the decoupled spatial and temporal covariances. (Note the convention about the indices of .)

II.3.1 Equal-time covariance estimator

Planar diagrammatics derivation. For the ETCE, the second set of DS equations [(25a), (25b)] takes on the form

| (42a) | ||||

| (42b) | ||||

where for short,

| (43a) | ||||

| (43b) | ||||

In other words, the matrix structure of the self-energy blocks is discovered—they are proportional to or , respectively, with unknown proportionality constants , , which depend on the blocks of the Green function matrix, and this by multiplying these blocks by or , respectively, and taking the traces normalized by .

Plugging [(42a), (42b)] into the first set of DS equations [(27a), (27b)], and using the definition of the holomorphic Green function matrix (187), one obtains

| (44a) | ||||

| (44b) | ||||

Now, one should combine Eqs. [(44a), (44b)] with the definitions of , [(43a), (43b)] in a twofold way:

Firstly, insert the former into the latter, then use the definitions of the holomorphic Green function (188) and -transform (189), which allow to rewrite , and analogously in the spatial sector. This yields two scalar equations for two scalar unknowns , ,

| (45) |

Secondly, take the traces of [(44a), (44b)] and substitute into [(28), (22)], using also (45). This implies that the holomorphic -transform of the ETCE is expressed through , as

| (46) |

The master equations [(45), (46)] may be rewritten in an even more concise way by exploiting the notion of the ``holomorphic -transform'' which for any Hermitian random matrix is the functional inverse of the holomorphic -transform,

| (47) |

This quickly leads to one simple equation for ,

| (48) |

It is the only master equation presented in this paper which has already been known (cf. e.g. BurdaJurkiewiczWaclaw2005-1 ; BurdaGorlichJaroszJurkiewicz2004 ).

Free probability derivation. Equation (48) can also be derived in another even simpler way BurdaJaroszJurkiewiczNowakPappZahed2010 , based on free probability theory of Voiculescu and Speicher VoiculescuDykemaNica1992 ; Speicher1994 . Even though this derivation is already known, it will now be sketched because of three reasons: (i) It is based on an application of the multiplication law (49) to a product of two Hermitian matrices, a procedure which may a priori not be valid. For the ETCE, it does work. However, an analogous reasoning may be applied to the TLCE as well and it is quite surprising to discover that it yields a wrong result, albeit only slightly (cf. Sec. II.3.3). (ii) It can easily be adjusted to the situation of the returns distributed according to the free Lévy law, which is a model of a non-Gaussian behavior of financial assets (cf. App. A.1.4). However, this extension has been accomplished BurdaJurkiewiczNowakPappZahed2004 only for , and the free Lévy distribution with zero skewness. Therefore, it will in what follows be worked out for arbitrary , and the Lévy parameters , , (except the case with ). (iii) This result will in turn constitute a basis for a derivation of the master equation for the TLCE and free Lévy assets (cf. Sec. II.3.3).

In order to rederive (48), recall the ``multiplication law'' of free probability. If and are two free unitary random matrices (``freeness'' is a generalization of the notion of statistical independence to noncommuting objects; here it may be thought of simply as independence), then the MSD of their product is obtained by multiplying their -transforms,

| (49) |

This formula may be generalized to matrices other than unitary, although caution must then be exercised. For instance, it may be applied to Hermitian matrices, even though their product is generically non-Hermitian. It does works for certain models such as in BurdaJaroszLivanNowakSwiech2010 ; BurdaJaroszLivanNowakSwiech2011 or the below derivation, however, Sec. II.3.3 contains a counterexample. (Cf. the end of App. A.1.4 for the free probability addition law in the Hermitian world, and the end of App. B.2.1 in the non-Hermitian world.)

Now if the true covariance function of the returns is factorized (41), they can be recast as , where the new returns are IID of variance . Combining cyclic shifts of terms with the multiplication law (49) allows then to relate the ETCE for the original returns to the ETCE for the IID returns ,

| (50a) | ||||

| (50b) | ||||

Finally, inserting , which readily follows from the MP holomorphic Green function (234), reproduces the master equation (48).

Generalization to free Lévy returns. In the free Lévy instead of Gaussian world, formula (50b) remains intact [actually, (50a) will be used; also, the normalization is rather , cf. (171)], only a new expression for needs to be worked out.

It can be accomplished by the ``projector trick'' BurdaJaroszJurkiewiczNowakPappZahed2010 , which is to define a rectangular (; assume here ) free Lévy random matrix as the projection with of a square () free Lévy Hermitian matrix . This implies , in which changing cyclicly the order of terms and using the multiplication law (49) (again for a pair of Hermitian matrices; it works this time as well) yields .

Secondly, simple algebra applied to the definition (208) yields . Now, for in the upper half-plane, follows from (LABEL:eq:LevyStableDistributionCharacteristicFunction), while from the same equation only with .

Combining these results leads to the following set of two master equations for two complex unknowns, and auxiliary ,

| (51a) | |||

| (51b) | |||

where for short,

| (52) |

II.3.2 Generalized time-lagged covariance estimator

For (29), one is able to follow the steps in the above planar diagrammatics derivation to a certain extent, recognizing similar structures, however, a reduction to a single equation like (48) is yet to be accomplished.

Really, the only manageable simplification so far is to write the second set of DS equations [(33a)-(33h)] in a form analogous to [(42a), (42b), (43a), (43b)],

| (54e) | ||||

| (54j) | ||||

where

| (55e) | ||||

| (55j) | ||||

These along with the first set of DS equations [(35e), (35j)] form a set of master equations in the considered case.

In order to compare them with their ETCE counterparts, define

| (56) |

and recall (210), plus analogously in the spatial sector. Then, [(35e), (35j)] combined with [(54e), (54j)] read

| (57c) | ||||

| (57f) | ||||

while the definitions [(55e), (55j)] become

| (58c) | ||||

| (58f) | ||||

One recognizes now similarities between [(54e), (54j)] and [(42a), (42b)], [(57c), (57f)] and [(44a), (44b)], [(58c), (58f)] and [(43a), (43b)].

A way to reduce these master equations to a simple single equation like (48) for the ETCE has unfortunately not been found. The reason may essentially be traced back to the fact that the block trace (212)—unlike the usual trace—does not exhibit the cyclic property; this obscures a way to write an analog of Eq. (46), which relates the spectral information about the estimator to the constant matrices , . In other words, just as (48) utilizes the notion of the holomorphic -transform (47) (of the Hermitian matrices and ), one would expect the desired simplification to be possible only once a proper definition of the -transform for non-Hermitian matrices has been found, which is not yet the case (cf. BurdaJanikNowak2011 for recent progress in this direction).

II.3.3 Rotational symmetry

Rotational symmetry of the MSD. There is an important property, often encountered throughout this paper, which the MSD of a non-Hermitian random matrix (e.g., the TLCE) may possess—rotational symmetry around zero, i.e., dependence only on

| (59) |

in which case it is sufficient to consider just its radial part,

| (60) |

-transform conjecture. In such a situation, a very helpful tool is the following hypothesis which has been put forth and extensively tested in BurdaJaroszLivanNowakSwiech2010 ; BurdaJaroszLivanNowakSwiech2011 ; Jarosz2011-01 ; Jarosz2012-01 :

(i) For any non-Hermitian random matrix model whose nonholomorphic -transform (and therefore, the MSD) is rotationally symmetric around zero,

| (61) |

one may invert (61) functionally,

| (62) |

which is named the ``rotationally symmetric non-holomorphic -transform.''

(ii) For the Hermitian random matrix , the holomorphic -transform is the functional inverse of the holomorphic -transform (47).

(iii) The -transform conjecture claims that these two quantities are related through

| (63) |

It is useful because often one of the models, or , is more tractable than the other (concerning computation of the MSD), and therefore Eq. (63) gains access to that more complicated model.

Relationship between the TLCE and ETCE assuming the rotational symmetry. A general procedure to discern whether the MSD of the TLCE for a given true covariance function has the rotational symmetry will not be attempted in this work. Potential implications of this property will nonetheless be analyzed and two specific examples outlined.

Application of the above hypothesis to the TLCE requires caution concerning the order of terms:

Firstly, introduce the random matrix , which differs from only by the order of terms and dimension; consequently, their nonholomorphic -transforms relate as .

Secondly, assume the rotational symmetry around zero (to be verified a posteriori), and write the rotationally symmetric non-holomorphic -transform (62), .

Thirdly, consider the Hermitian random matrix , where . The -transform conjecture (63) reads . On the other hand, changing the order of the constituents and using the unitarity of , one finds .

Fourthly, recall .

Fifthly, changing again the order of terms, , where is the ETCE (17).

Collecting all the above formulae leads to an equation which relates the -transforms of the TLCE and ETCE,

| (64) |

[The expression under the square root is always nonnegative, cf. the discussion below. The sign, reflecting the two possible square roots, is irrelevant.]

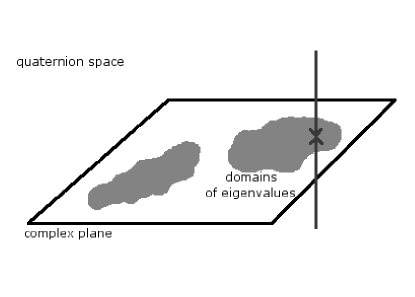

Single ring conjecture. Another hypothesis for non-Hermitian random matrices with the rotational symmetry (61) has been proposed Jarosz2011-01 ; Jarosz2012-01 —which may be regarded as an extension of the ``Feinberg-Zee single ring theorem'' FeinbergZee1997-02 ; FeinbergScalettarZee2001 ; Feinberg2006 ; GuionnetKrishnapurZeitouni2009 —that their mean spectral domain is either a ring or an annulus; the radii of the enclosing circles are denoted by and . Assuming this is true, for the TLCE, it is a general caveat that on the external circle and on the internal one, where the latter exists only for . Indeed, on the borderline, the nonholomorphic and holomorphic -transforms coincide. But the only holomorphic function compatible with the rotational symmetry (i.e., depending on ) is a constant, . Moreover, it is known from RMT that in the external outside (i.e., containing ), the holomorphic Green function must behave as , for —which implies . On the other hand, in the internal outside (i.e., containing ), the value of is related to the zero modes: The MSD (206) reads, , where the representation of the complex Dirac delta (204) has been used. Now, zero modes appear in the spectrum of the TLCE only if , and their number is , i.e., their density, ; indeed, the matrices and have the same nonzero eigenvalues, while the larger one has additionally zero modes. This implies in the internal outside, which exists only for . To summarize, is a smooth function of which monotonically grows from at to at .

Example 1: Trivial temporal covariances. It will be proven (cf. Sec. II.5.3) that the MSD of the TLCE certainly exhibits the rotational symmetry in the case of the true covariance function factorized (41) with arbitrary and . The master equation for the holomorphic -transform of the ETCE (48) becomes then , therefore Eq. (64) turns into a complex equation for two real unknowns, and auxiliary ,

| (65) |

Remark that if has a finite number of distinct eigenvalues, this can be recast as a set of polynomial equations (cf. Toy Models 1 and 2a below). For with an infinite number of distinct eigenvalues, this is typically more complicated (cf. Toy Model 2b).

The radii of the circles enclosing the mean spectral domain are obtained from (65) by expanding it around, respectively, or if also , which both are consistent with assuming an expansion around . The external one is given by the first and second moments of (190b), while the internal one by its holomorphic - and -transforms,

| (66a) | ||||

| (66b) | ||||

[Remark that (66b) may be recast in a shorter but perhaps less useful way, .]

Example 1—a surprisingly wrong derivation using the multiplication law. Before proceeding to a second example of a rotationally-symmetric TLCE, recall that the master equation (48) has been rederived (cf. the middle part of Sec. II.3.1) using the free probability multiplication law (49) by relating (50b) the ETCE for true covariances factorized into , (41) to the ETCE for IID returns. One may therefore ask whether the master equation (65) could be obtained in a similar fashion by relating the TLCE with the spatial covariance matrix to the TLCE for IID returns (which is Toy Model 1 below). The derivation should start from and proceed as

| (67a) | ||||

| (generally incorrect!). | ||||

Now the rotationally-symmetric nonholomorphic -transform of is given by functionally inverting (LABEL:eq:TM1TLCEEq02), which leads to the following equation

| (68) |

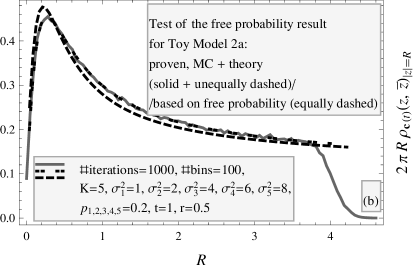

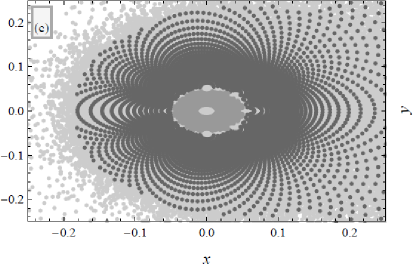

It is surprising to discover that it is different from Eq. (65). It seems that the only place the above derivation may have failed is the application of the multiplication law to a product of two Hermitian matrices, as explained in Sec. II.3.1. It is even more surprising to find out that the right and wrong master equations produce solutions with only a very slight difference in the MSD; Figure 7 (b) confirms the agreement of Monte Carlo simulations with Eq. (65) and their disagreement, albeit very small, with Eq. (68).

Example 1—generalization to free Lévy returns. Another point is to recall that the master equation (48) for the ETCE for factorized true covariances (41) has been generalized (cf. the last part of Sec. II.3.1) to the situation of free Lévy returns [(51a), (51b)]. These formulae [with , i.e., ] can be combined with (64) to yield a set of two master equations for the nonholomorphic -transform of the TLCE for arbitrary in the free Lévy case,

| (69a) | |||

| (69b) | |||

where real and complex are auxiliary unknowns.

In particular, for zero skewness, Eq. (69a) is trivially satisfied with , while Eq. (69b) becomes

| (70) |

Further setting and brings it back to the Gaussian result (65).

A derivation of the values of the external and internal radii of the borderline of the mean spectral domain will not be presented in full generality, just commented on for special values of the parameters in Sec. III.2.8.

Example 2: Trivial spatial covariances and diagonal temporal covariances. Another situation when the rotational symmetry is apparent from an inspection of Monte Carlo data is the factorized covariance function (41) with and arbitrary diagonal . The master equations for the TLCE [(54e)-(55j), (35e), (35j)] happen to be very cumbersome [especially the matrix inversion in (35j)], therefore a proof will not be offered, rather the assumption will be made and numerically verified a posteriori. Since Eq. (48) becomes , Eq. (64) turns again into a complex equation for two real unknowns, and auxiliary ,

| (71) |

Recall that this equation holds conjecturally for diagonal, not arbitrary.

The radii of the enclosing circles are found in an analogous way as above to be

| (72a) | ||||

| (72b) | ||||

where the negative moments are defined analogously to (190b) but with negative powers, and remark a different placement of the factors in (72a) as compared to (66a).

One could also directly generalize Eq. (71) to the free Lévy case; the result is not needed in this article and will not be presented.

II.4 Case 3: True covariances translationally symmetric in time

Another interesting special form of the true covariance function (19a) is when its dependence on time is translationally symmetric,

| (73) |

Note that the right-hand side may be treated as a time-dependent matrix, ; it obeys .

II.4.1 Fourier transformation

Since the thermodynamic limit (5) is assumed, it proves very convenient—especially with the symmetry (73) present in the system—to encode all the matrices (; assume that the temporal matrix indices range from to ) by their Fourier transforms. Namely, instead of any such matrix , use

| (74) |

where , which conversely reads,

| (75) |

Remark that in particular, the Kronecker delta is mapped to the Dirac delta , while the matrix multiplication translates into the integration .

If a matrix satisfies , where is some function of time, then its Fourier transform is proportional to the Dirac delta, , with

| (76a) | ||||

| (76b) | ||||

In particular, matrix multiplication is simply the multiplication of these reduced Fourier transforms, . This language of Fourier transforms for matrices will henceforth always be used provided that the temporal translational symmetry (73) holds.

Remark finally that in a situation when the entries themselves depend on , the above procedure may not work. This is the case e.g. for the EWMA estimators [(3a), (3b), (4)] in the limit (7), to which a different method needs to be applied, namely Eq. (71) based on the rotational symmetry of the MSD (cf. Sec. III.2.6).

II.4.2 Equal-time covariance estimator

The general master equations for the ETCE [(25a), (25b), (27a), (27b)] will now be written in the situation (73) in the Fourier language.

The second set of DS equations acquires the form,

| (77a) | ||||

| (77b) | ||||

while in the first set of DS equations, the spatial sector is unchanged and the temporal sector is Fourier-transformed, becoming a scalar equation,

| (78a) | ||||

| (78b) | ||||

Finding a solution to [(77a), (77b), (78a), (78b)] may be attempted once [and thus (76a); it is Hermitian for any ] is known.

II.4.3 Time-lagged covariance estimator

Consider now the TLCE [not the more general random matrix (29), since arbitrary , may break the translational symmetry in time].

II.5 Time-lagged covariance estimator for Case 2 + 3: True covariances factorized and translationally symmetric in time

Recall that in the case of factorized true covariances (41), the master equations for the ETCE have been simplified to a single equation (48) (cf. Sec. II.3.1), which has not been accomplished for the TLCE (cf. Sec. II.3.2). Some simplification becomes however possible if in addition the temporal translational symmetry (73) is assumed,

| (83) |

II.5.1 Arbitrary and

Firstly, the temporal sector of the second set of DS equations [(80a)-(80d)] acquires the form

| (84a) | ||||

| (84b) | ||||

| (84c) | ||||

| (84d) | ||||

where the information about the model is now encoded in four complex parameters,

| (85a) | ||||

| (85b) | ||||

| (85c) | ||||

| (85d) | ||||

Notice that the definition of the Green function matrix [(209), (210)] implies ; it will moreover be shown [cf. Eq. (100)] that

| (86) |

where only on the borderline of the mean spectral domain (101). Hence, there really is one complex and one real unknown.

Secondly, substitute [(84a)-(84d)] into the temporal sector of the first set of DS equations (81o),

| (87) |

where (82),

| (88) |

Thirdly, knowing (the Fourier transforms of) the temporal blocks of the Green function matrix [(LABEL:eq:Case2Plus3TLCEEq03), (88)], one may compute the spatial blocks of the self-energy matrix [(79a)-(79d)],

| (89a) | ||||

| (89b) | ||||

| (89c) | ||||

| (89d) | ||||

where for short,

| (90a) | ||||

| (90b) | ||||

(Note, , while is real.) Remark that the matrix structure of the spatial blocks of the self-energy matrix is discovered—they are all proportional to .

Fourthly, thanks to this proportionality, calculating the spatial blocks of the Green function matrix (81f) only requires inverting a matrix,

| (91a) | ||||

| (91b) | ||||

| (91c) | ||||

| (91d) | ||||

where for short,

| (92) |

(Here all the matrices commute, so they may be treated as numbers.)

Finally, in order to obtain a set of equations for the basic unknowns, , the results [(91a)-(91d)] should be plugged back into the definitions [(85a)-(85d)], which yields

| (93a) | ||||

| (93b) | ||||

| (93c) | ||||

| (93d) | ||||

where for short,

| (94a) | ||||

| (94b) | ||||

Note that , , , all depend—generically in a very complicated way—on the unknowns .

Nonholomorphic solution. As a general caveat (cf. App. B.2), the master equations [(93a)-(93d)] will have a nonholomorphic solution—valid inside the mean spectral domain, , and describing the MSD there—and a holomorphic one—for the outside of the domain, whose matching with the nonholomorphic solution provides the equation of the borderline of the domain.

In the nonholomorphic sector, there must necessarily be [cf. the discussion around Eqs. (100), (101)]. Simplifying [(93a)-(93d)] accordingly yields

| (95a) | ||||

| (95b) | ||||

| (95c) | ||||

Once are found from [(95a)-(95c)]—which, as mentioned, seems to be a formidable task—the nonholomorphic Green function of the linearized estimator (30) is given by an analog of (28), with the respective traces calculated from (91a) and (LABEL:eq:Case2Plus3TLCEEq03),

| (96a) | ||||

| (96b) | ||||

where for short,

| (97a) | ||||

| (97b) | ||||

These quantities can be expressed through , and , , respectively, by using and ,

| (98a) | ||||

| (98b) | ||||

Inserting [(98a), (98b)] into [(96a), (96b)], and then into the analog of (28), using also (208), and finally into the analog of (22)—we express the desired nonholomorphic -transform of the TLCE (in the argument ) through ,

| (99) |

Eqs. [(95a)-(95c), (90a), (90b), (88), (94a), (94b), (92), (99)] thus conclude the derivation of the master equations under the considered circumstances (83).

Holomorphic solution. One may also evaluate the order parameter [(216), (36)] inside the mean spectral domain by using the identities (LABEL:eq:Case2Plus3TLCEEq03) (its off-diagonal equations) and [(91b), (91c)],

| (100) |

where for short, . Since the left-hand side is real and nonnegative, and so is the bracket on the right-hand side—so must be (86). Therefore, the equation of the borderline (217) reads

| (101) |

II.5.2 Trivial and arbitrary

As a first subcase, suppose

| (102) |

Then, the spatial traces [(94a), (94b)] greatly simplify, and so do the master equations [(95a)-(95c)], becoming , and . Moreover, (99) turns into (here it proves simpler to use the nonholomorphic Green function instead of the -transform) . Collecting all these results (and changing the argument to ) yields the final set of master equations,

| (103a) | ||||

| (103b) | ||||

where for short,

| (104) |

where the unknowns are: complex and real and nonnegative , with . Notice that there generically is no rotational symmetry here.

II.5.3 Arbitrary and trivial

As a second subcase, suppose on the contrary,

| (105) |

Recall that the master equation in this situation has already been derived (65) using the -transform conjecture; now it will be rigorously proven.

Nonholomorphic master equations. Immediately, , and the integrals [(90a), (90b)] can be performed explicitly: Introducing a new variable

| (106) |

[notice that the dependence on is lost—this subcase is independent of the value of the time lag, of course as long as , cf. Fig. 7 (a)], and applying the method of residues—the integration requires finding roots of a quadratic polynomial in ,

| (107) |

which leads to

| (108a) | ||||

| (108b) | ||||

| (108c) | ||||

where for short,

| (109) |

[The two roots of (107) obey , hence, one of them lies inside the centered unit circle , and one outside it; only the interior one contributes to the integrals.]

Consequently, Eq. (95c) implies , , with . The other two master equations [(95a), (95b)], turn finally into two real equations for two real unknowns , ,

| (110a) | ||||

| (110b) | ||||

where substituting the results [(108a)-(108c)] into (92) yields

| (111) |

and recall that in this notation Eq. (109) reads

| (112) |

Once these equations [(110a)-(112)] are solved (after specifying the true spatial covariance matrix ), then the nonholomorphic -transform (99) is expressed through , as

| (113) |

In [(110a)-(113)] the argument has already been changed from to . Moreover, all these identities depend only on the radius , so the rotational symmetry has been demonstrated. Conversely, one may say that deviations from rotational symmetry in the MSD of the TLCE point toward nontrivial true temporal covariances.

Nonholomorphic master equations—a simpler form. The above master equations can be considerably simplified. One should start from rewriting and [i.e., the left-hand sides of (110a), (110b) with (111)] in the language of the holomorphic -transform of , which is done by factorizing ,

| (114a) | ||||

| (114b) | ||||

This leads to

| (115a) | ||||

| (115b) | ||||

which is supplemented by [(112), (113)]. Using these last three equations, one expresses , , through , , and substitutes them into (115a), which finally yields a concise complex equation (65) for two real unknowns, and auxiliary .

Borderline of the mean spectral domain. It will now be proven that is a ring for and an annulus for , with the radii [(66a), (66b)]. To find the borderline, the original form of the master equations is more convenient, in which one should set (101). To begin with, Eq. (112) becomes , which inserted into Eq. (113) confirms the two possible values that the nonholomorphic -transform of the TLCE may acquire on the borderline, or . Furthermore, manipulating Eqs. [(110a), (110b), (111)] with leads to two solutions:

(i) External circle: If (which corresponds to ), the master equations become

| (116a) | ||||

| (116b) | ||||

which reproduces (66a).

III Toy Models

III.1 Outline

| TM 1 | TM 2 | TM 3 | TM 4 (comments) | |||||||||

| Gaussian | EWMA | Student | free Lévy | TM 2a | TM 2b | TM 4a | TM 4b | TM 4c | ||||

| Ver. 1 | Ver. 2 | |||||||||||

| ETCE | Sec. | C.1 | — | — | — | — | C.2 | — | C.3 | III.5.1 | III.5.2 | III.5.3 |

| MSD | (235) | — | — | — | — | (236) | — | (LABEL:eq:TM3ETCEEq02) | [(158a), (158b)] | (162) | (166) | |

| Fig. | — | — | — | — | — | 23 | — | 24 | 15 | 17 | 19 | |

| TLCE | Sec. | [III.2.2, III.2.3, III.2.4] | III.2.6 | III.2.7 | III.2.8 | III.3.1 | III.3.2 | III.4 | III.5.1 | III.5.2 | III.5.3 | |

| MSD | [(122), (121b)-(121d)] | [(71), (126)] | (128) | [(71), (129)] | [(131a), (131b)] or (LABEL:eq:TM1TLCELevyEq02) | [(65), (134)] | [(65), (137)] | [(145a)-(147)] | [(95a)-(95c), (90a), (90b), (88), (94a), (94b), (92), (157)] | [(79a)-(82), (160)] | [(79a)-(82), (164a)-(164d)] | |

| [(119a), (119b)] | [(127a), (127b)] | [(130c), (130d)] | [(135)-(136b)] | [(138)-(141)] | [(149a)-(150b)], [(153)-(156b)] () | |||||||

| Fig. | 1 | 3 | 4 (a) | 4 (b) | 5 | 6 | 8 | [11, 12, 13, 14] | 16 | 18 | 20 | |

III.1.1 Toy Models 1, 2a, 2b, 3

In this Section, the general master equations developed in Sec. II (and summarized in Tab. 1)—which are a gateway to the MSD [(186), (203)] of the ETCE (17) and TLCE (18) for arbitrary complex Gaussian assets—are applied to three specific models of the true covariance function (19a) which are designed to approximate certain aspects of the real-world financial markets and other complex multivariate systems, according to the introduction in Sec. I.2:

(i) Toy Model 1 (Sec. III.2): The assets are IID. This is the simplest case; nevertheless, it is useful as the ``null hypothesis'' (cf. Sec. I.1.2), i.e., any discrepancy between the spectra derived from experimental data and from this model signifies genuine correlations present in the system.

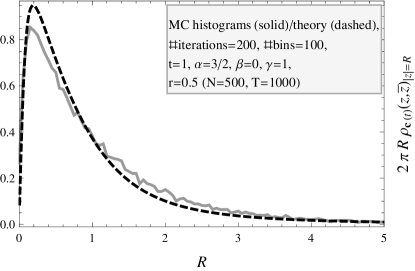

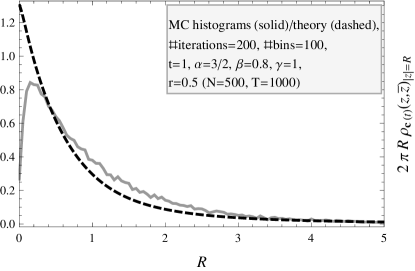

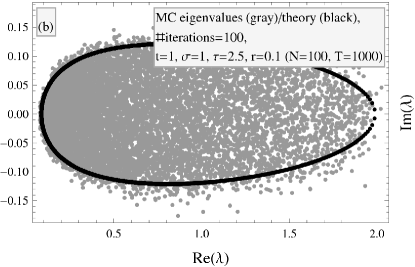

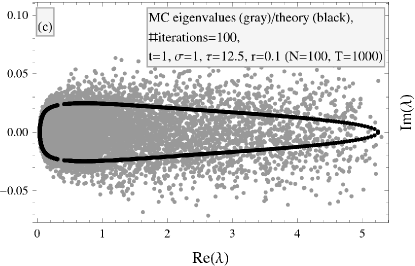

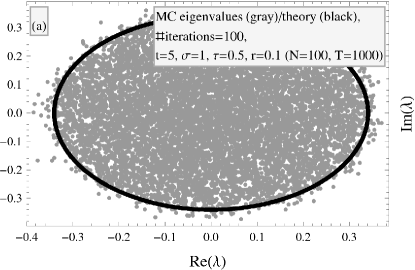

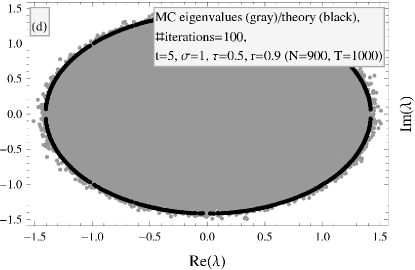

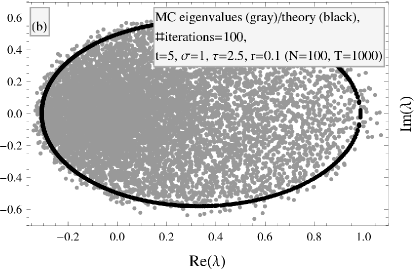

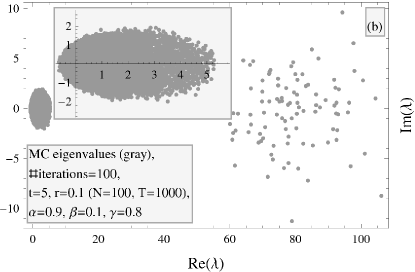

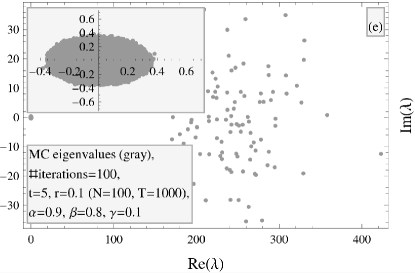

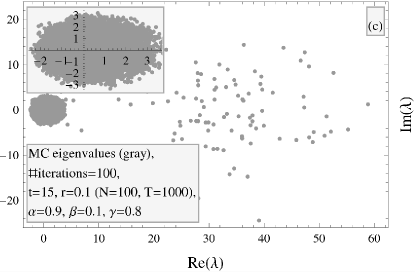

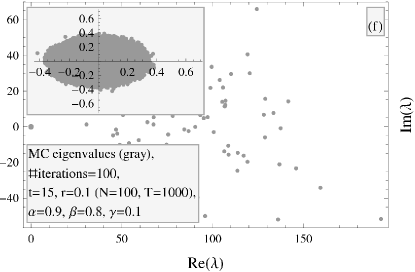

The MSD of the TLCE has first been calculated in BielyThurner2006 ; ThurnerBiely2007 , but their formula is demonstrated to be wrong (Sec. III.2.5), and the right one is presented (Secs. [III.2.2, III.2.3, III.2.4]); it is noteworthy that the only analytical result to date concerning the spectrum of the TLCE was incorrect—it reveals how involved the subject is.

This result is generalized to the EWMA estimator for Gaussian assets (Sec. III.2.6), as well as the standard estimator for two models of non-Gaussian behavior of the returns: Student (Sec. III.2.7; it comes in two versions: with a common random volatility and IID temporal random volatilities) and free Lévy (Sec. III.2.8) distributions.

(ii) Toy Model 2 (Sec. III.3): The assets have arbitrary variances but no temporal correlations; they come in two versions (cf. Sec. I.2.1): either a finite number of variance sectors (Toy Model 2a, Sec. III.3.1), or variances distributed according to a power law with a lower cutoff (Toy Model 2b, Sec. III.3.2). This and the following models signify another than the null hypothesis approach which is to build more and more realistic toy models, comparing them to data, thereby verifying their validity and assessing their parameters.

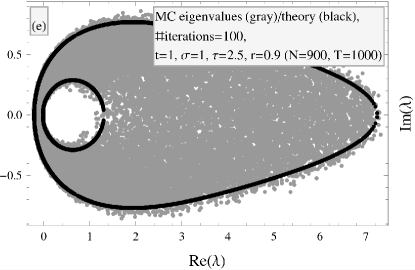

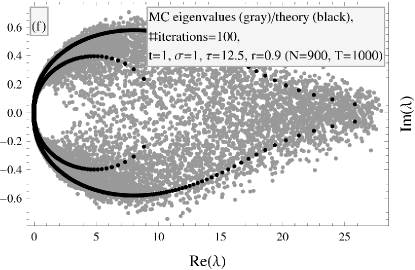

III.1.2 Toy Models 4a, 4b, 4c

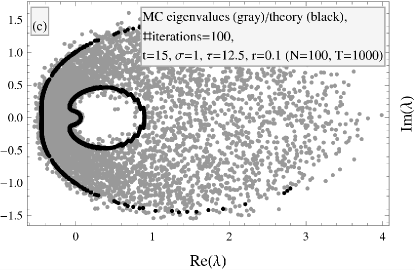

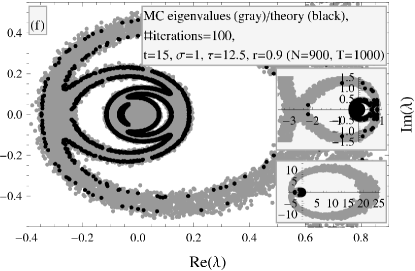

Two reflections naturally arise after analyzing the above models—firstly, they are still quite far away from financial reality; secondly, the analytical derivations of the MSD are already increasingly complicated. Consequently, it is a valid research program to both construct more realistic toy models and to enhance the techniques presented in this paper (especially on the numerics side) to be capable of handling such models. Even though the second part is beyond the scope of this article, three more models are announced and initially analyzed (i.e., the pertinent master equations are explicitly written down or commented on, and the Monte Carlo simulations are presented; Sec. III.5)—in contrast to the above examples, they are mixes of both the spatial and temporal correlations from Toy Models 2a and 3, being more advanced examples of the SVAR() class:

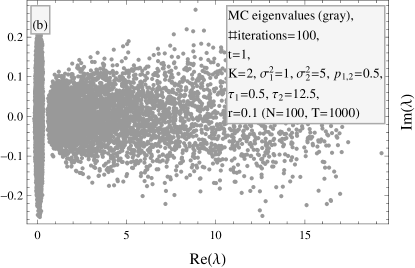

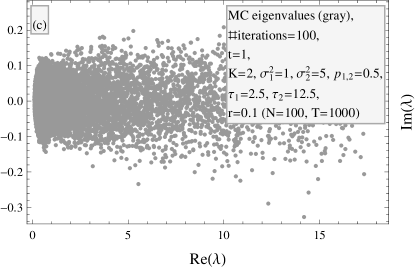

(i) Toy Model 4a (Sec. III.5.1): There is a number of variance sectors and exponentially-decaying autocorrelations identical for all the variables.

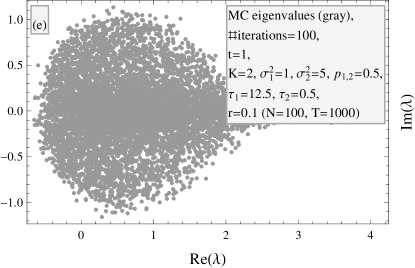

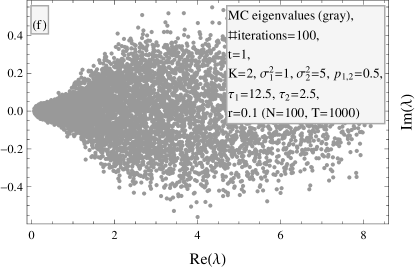

(ii) Toy Model 4b (Sec. III.5.2): There is a number of variance sectors and exponentially-decaying autocorrelations different for each sector.

(iii) Toy Model 4c (Sec. III.5.3): A SVAR() model with a simple nondiagonal covariance function originating from the market mode.

For these examples also the ETCE is analyzed because for models 4b and 4c the true spatial and temporal correlations are not factorized, unlike in the remaining cases, which causes the need to use the new master equations developed in Sec. II.2.

The main results obtained for the above six models are summarized in Tab. 2.

III.2 Toy Model 1 (null hypothesis): Uncorrelated Gaussian/Student/free Lévy assets and standard/EWMA estimator

III.2.1 Definition

III.2.2 Borderline of the mean spectral domain

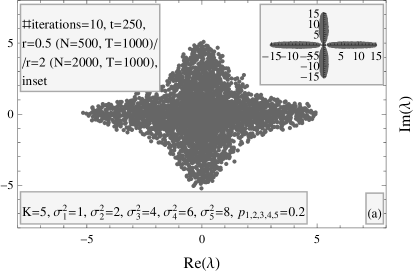

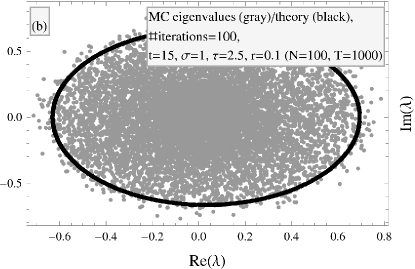

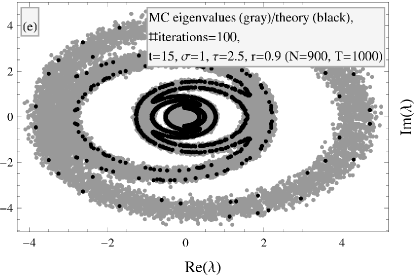

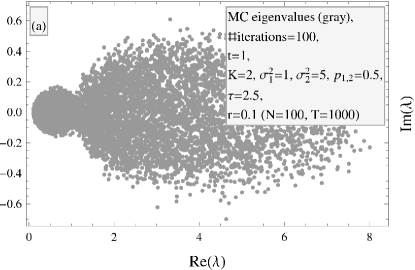

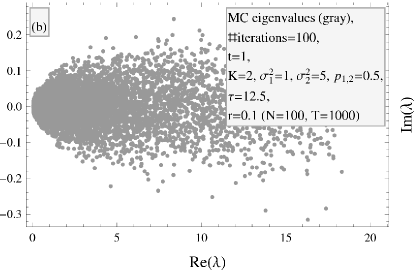

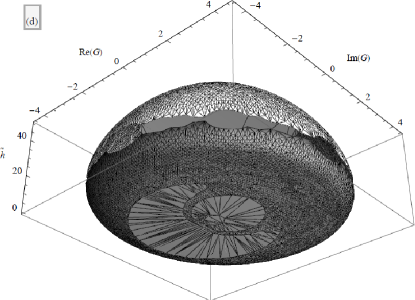

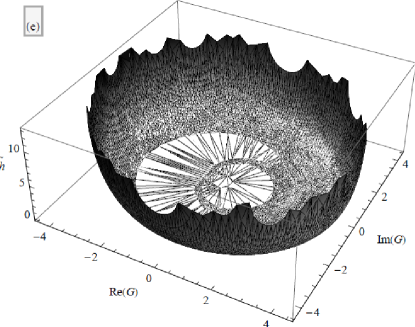

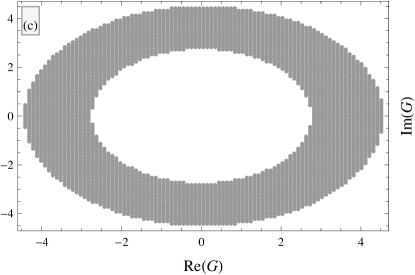

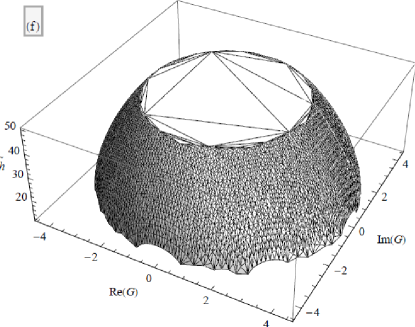

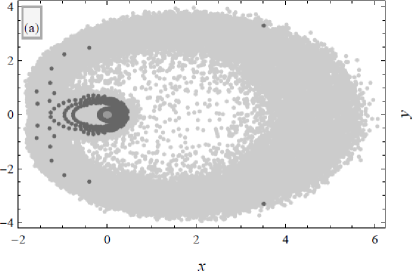

For the TLCE, the considered structure of the true covariance function falls under the discussion in Secs. II.5.3 and II.3.3. The mean spectral domain is either a disk (for ) or an annulus (for ), with the radii of the enclosing circles [(66a), (66b)],

| (119a) | ||||

| (119b) | ||||

(One easily checks that for all .)

III.2.3 Mean spectral density

The relevant master equation is (65) with , and elimination of leads to a cubic polynomial equation for the nonholomorphic -transform, ,

| (120) |

where for short, , and . The rotational symmetry around zero is evident. Once is found from (LABEL:eq:TM1TLCEEq02), the (rescaled) radial MSD (60). Actually, this relationship allows to write a depressed cubic equation directly for the MSD,

| (121a) | ||||

| (121b) | ||||

| (121c) | ||||

| (121d) | ||||

One may check that the discriminant of (121a) is always negative, i.e., it has one real root which is the desired MSD,

| (122) |

where for short, and , and two redundant complex conjugate roots. Recall also that this case is independent of the time lag [cf. (106)]. This is the time-lagged counterpart of the MP distribution (235) (cf. App. C.1).

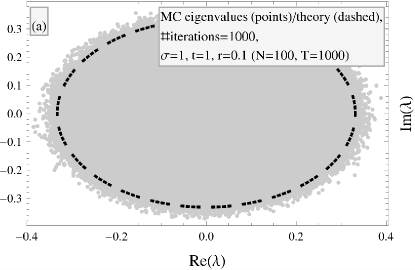

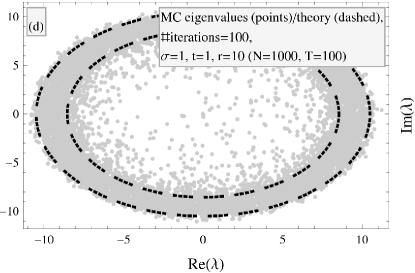

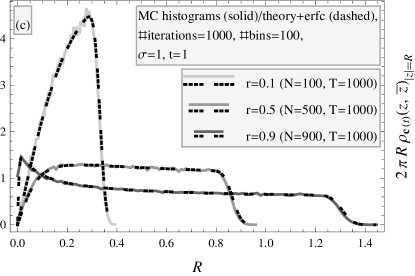

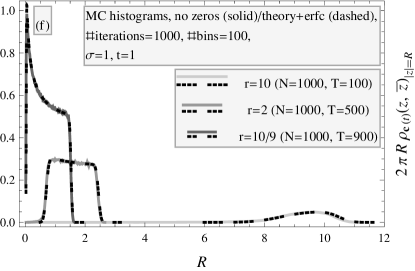

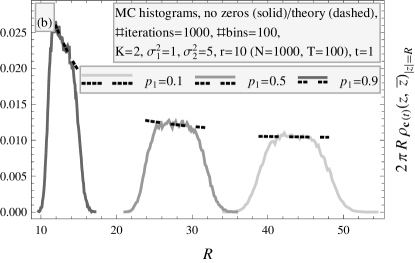

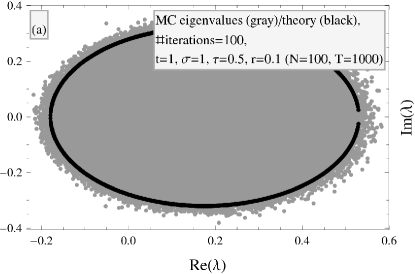

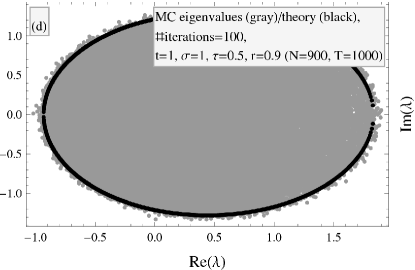

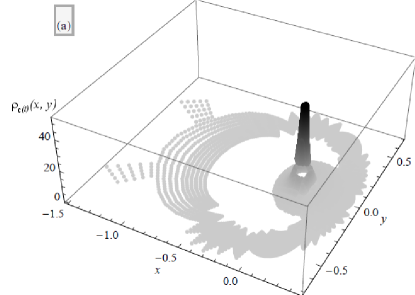

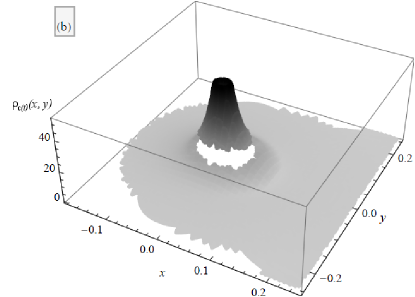

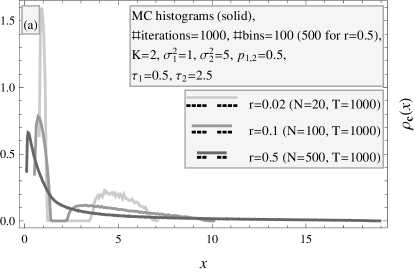

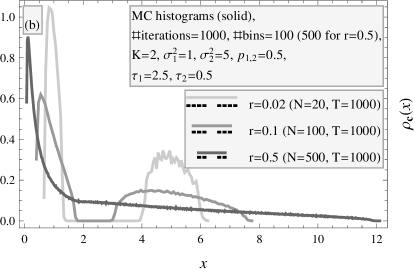

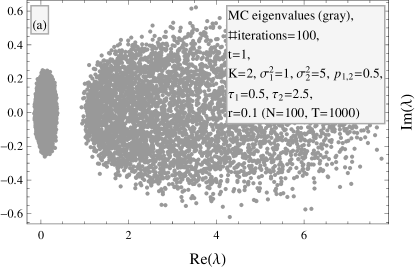

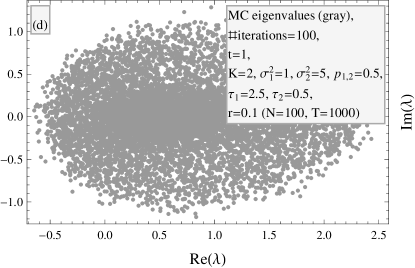

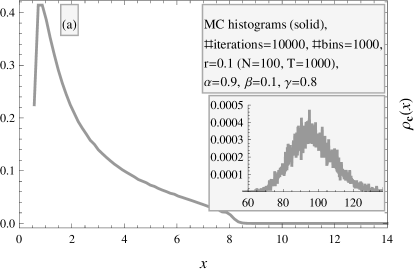

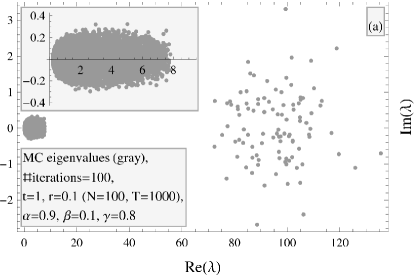

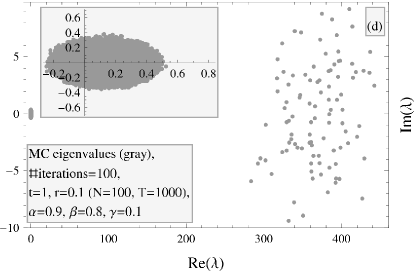

Figures 1 [(a), (d)] depict, respectively for or , the numerically-generated eigenvalues of the TLCE and the theoretical borderline(s) [(119a)-(119b)], which are seen to accurately enclose the mean spectrum, with an exception of a small number of eigenvalues leaking out (this being a finite-size effect). In Figs. 1 [(b), (e)], formula (122) is shown to precisely reproduce the histograms of (the absolute values of) these numerical eigenvalues, respectively for or , again except the vicinity of the borderline(s), to which a finite-size reasoning needs to be applied.

III.2.4 Universal erfc scaling

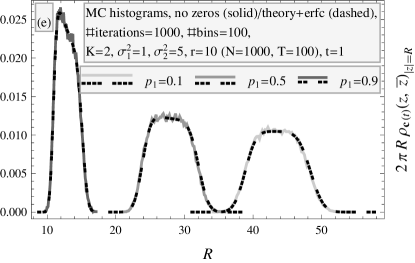

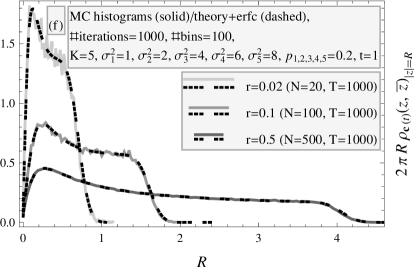

As explained in App. B.1.2, the method of planar diagrammatic expansion employed in this paper works for infinite matrix dimensions (5). However, for any non-Hermitian random matrix model (of dimensions ) whose MSD exhibits rotational symmetry around zero (cf. Sec. II.3.3) there has been put forward the ``erfc conjecture'' BurdaJaroszLivanNowakSwiech2010 ; BurdaJaroszLivanNowakSwiech2011 ; Jarosz2011-01 ; Jarosz2012-01 which claims that the universal finite-size behavior of the MSD close to the borderline of the domain (i.e., as it seems, always a ring or an annulus) is obtained simply by multiplying the density with the following form-factor,

| (123) |

for each circle (one or two) which constitutes the borderline. Moreover, the sign is for the external borderline and for the internal one; is a parameter (one for each circle) depending on a particular model, whose derivation will not be attempted (this requires genuinely finite-size techniques), but its value adjusted by fitting to Monte Carlo data; finally, is the complementary error function.

This universal form-factor has been first calculated for the Ginibre unitary ensemble (220) ForresterHonner1999 ; Kanzieper2005 (cf. also KhoruzhenkoSommers2009 ), then for a product of two rectangular Gaussian random matrices with IID entries KanzieperSingh2010 ; in both cases, the mean spectral domain is a disk, and the parameter has been analytically determined. Inspired by this performance, the result has been conjectured and tested numerically for a product of an arbitrary number of rectangular Gaussian matrices BurdaJaroszLivanNowakSwiech2010 ; BurdaJaroszLivanNowakSwiech2011 (one borderline), as well as a weighted sum of unitary random matrices from the Dyson circular unitary ensemble (CUE) Jarosz2011-01 (one or two borderlines), or an arbitrary product of these last two models Jarosz2012-01 (one or two borderlines).

In Fig. 1 [(c), (f)], numerical tests of this hypothesis are presented, with excellent agreement; in particular, the steep decline of the MSD close to the borderline(s) is reproduced.

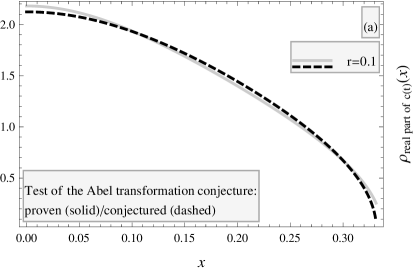

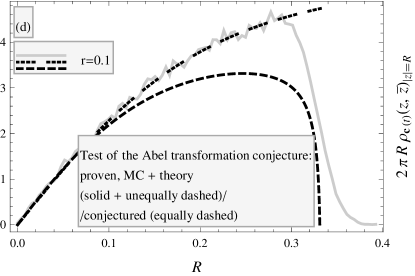

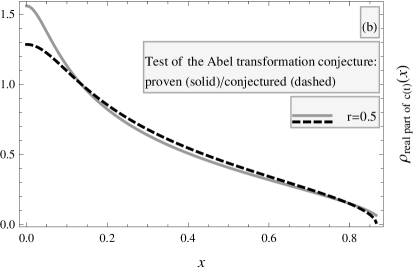

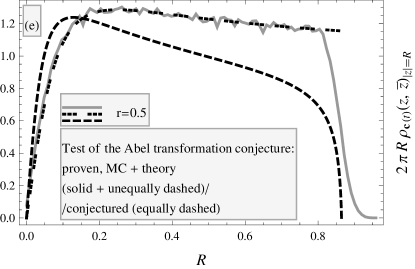

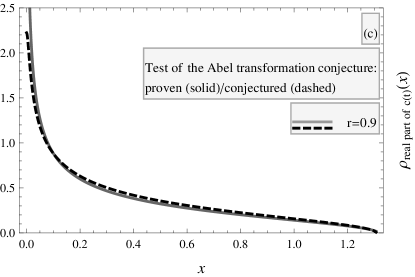

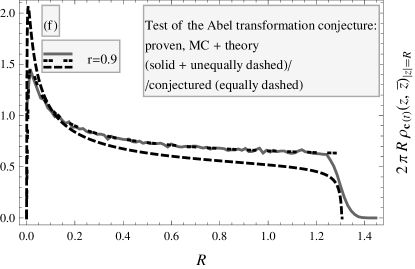

III.2.5 Previous solution based on the Abel transformation is incorrect

The MSD of the TLCE in the situation (118) has first been evaluated in BielyThurner2006 ; ThurnerBiely2007 . It will now be demonstrated that their solution is incorrect.

Abel transformation. The main idea of BielyThurner2006 ; ThurnerBiely2007 is conceptually similar to the -transform conjecture (cf. Sec. II.3.3)—which recall constitutes one way to derive the above formula (122)—in which one relates the rotationally symmetric MSD of a non-Hermitian random matrix to its ``absolute value squared'' . On the other hand, the authors of BielyThurner2006 ; ThurnerBiely2007 conjecture that under the same assumption of the rotational symmetry, one may relate the spectra of and its ``real part'' through the so-called ``Abel transformation,'' which in both ways reads

| (124a) | ||||

| (124b) | ||||

| (generally incorrect!). | ||||

They then reinforce this hypothesis by verifying that [(124a)-(124b)] work for being the Ginibre unitary ensemble with some variance (220), in which case the real part is the Gaussian unitary ensemble (194) with variance (this may be easily checked by computing the pertinent propagator). Plugging both MSD [(232), (202)] into the above formulae, one proves that they are indeed related by the Abel transformation.

Arguments against [(124a)-(124b)]. This coincidence is however accidental. The authors of BurdaJanikWaclaw2010 have first falsified the Abel transformation conjecture by constructing a counterexample, , where are two independent GUE random matrices.

This conjecture does not work for Toy Model 1 either. To show it, notice two facts: Firstly, formula (122) is certainly correct, as it has been obtained not only through the -transform conjecture but also the diagrammatic expansion method (which is a solid proof), plus it perfectly agrees in the bulk with the Monte Carlo data (cf. Fig. 1). Secondly, the MSD of the real part of the TLCE is known (cf. e.g. BurdaJaroszJurkiewiczNowakPappZahed2010 for derivation)—the holomorphic -transform obeys a quartic polynomial equation,

| (125) |

Substituting these results into [(124a)-(124b)], one finds a discrepancy between the left- and right-hand sides of both equations, as demonstrated in Fig. 2.

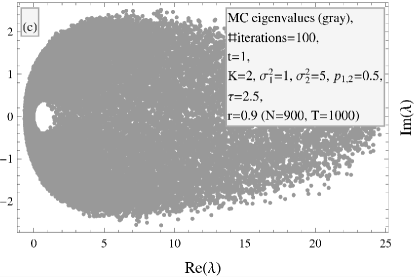

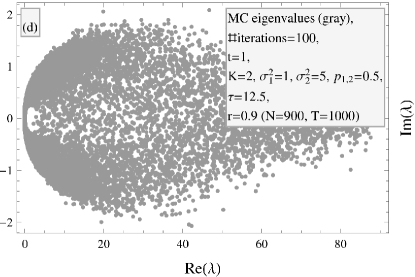

III.2.6 Generalization to the EWMA estimator

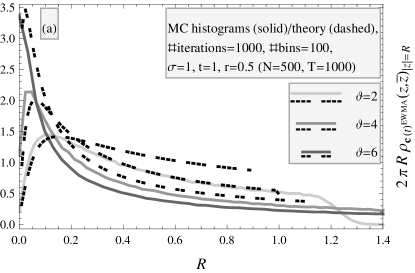

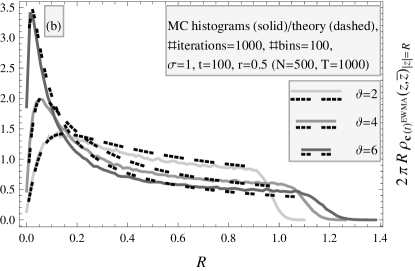

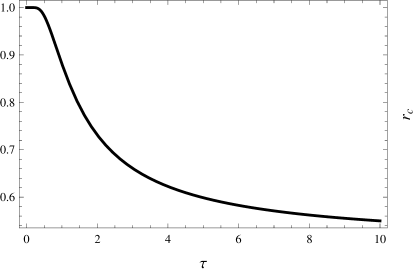

A first extension to be considered of the TLCE in the situation (118) (let for simplicity ) is its EWMA version [(3b), (4)] in the limit (7). As noted in Sec. I.1.2, this limit requires , which however is incompatible with the method used—therefore, the results will not reproduce Monte Carlo simulations precisely.

The master equation is the conjectured (71) with diagonal , since as explained in Sec. II.3.3, the exact master equations seem hard to solve. The limit (7) allows to pass in it from a discrete temporal description (summation over ) to a continuous one (integration over ) since , which yields an explicit expression for the holomorphic -transform of ,

| (126) |

It is straightforward to numerically construct the MSD from this master equation.

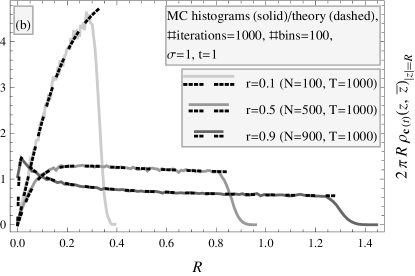

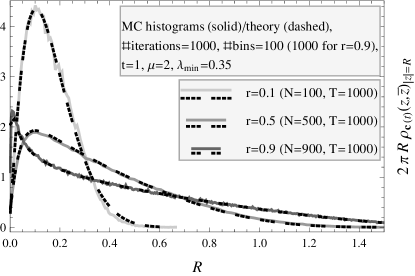

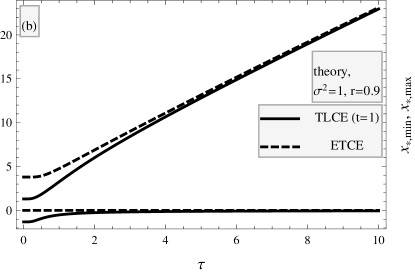

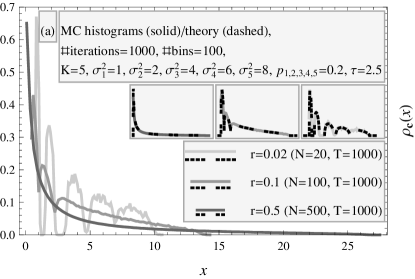

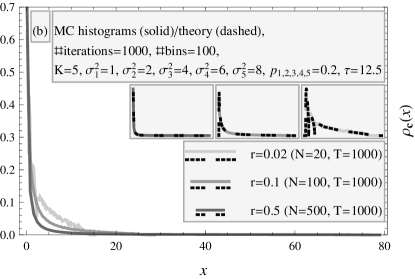

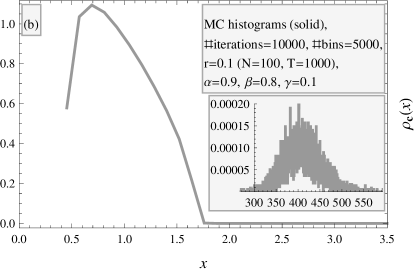

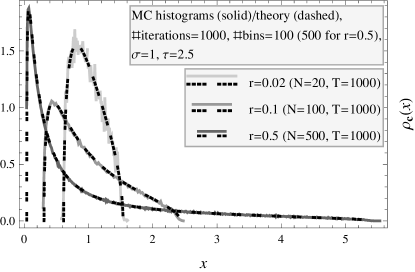

Figures 3 [(a), (b)] present the MSD derived from [(71), (126)] and compare it with Monte Carlo simulations, for , three values of and, respectively, or . The concord is satisfactory for , since this value is large enough to be comparable with and small enough for the finite-size effects not to be manifested. On the other hand, for there are anticipated discrepancies, especially close to the border of the domain. They may be checked to decrease with decreasing (if is less than about , one may quite safely use small ). Moreover, one may verify that for and the agreement between theory and numerics is excellent (not shown here). One may also infer from these plots that for decreasing they approach the MSD of the standard TLCE, while larger means a shorter effective length of the time series, hence a more ``smeared'' density.

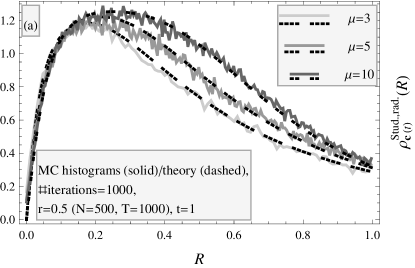

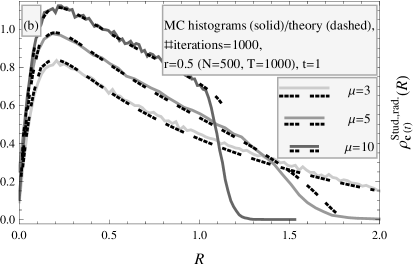

III.2.7 Generalization to the Student t-distribution

As explained in App. A.1.3, a simplest model of a non-Gaussian behavior of financial assets assumes that they are uncorrelated and distributed according to the Student t PDF (169). Moreover, it is known (cf. App. A.2.1) that a Student random variable may be thought of as a Gaussian random variable whose volatility is itself a random variable such that has the gamma distribution (177). This prescription will now be applied to transform the MSD of the TLCE to the Student case from two versions of the Gaussian model, both with independent assets and either (i) a common random volatility for all the assets BurdaGorlichWaclaw2006 ; BertuolaBohigasPato2004 ; or (ii) IID random volatilities at distinct time moments, but identical for all assets BiroliBouchaudPotters2007-1 .

Version 1: Common random volatility. Assume first that the are IID Gaussian with volatility , as above (118). Multiplying the MSD (122) with the weight function (177) and integrating it over (and changing the integration variable to ) leads to the following radial MSD of the TLCE,

| (128) |

for (i.e., it is unbounded for all values of the parameters), where the limits of integration are [(119a), (119b)].

This function is plotted and tested against Monte Carlo simulations in Fig. 4 (a), for , and three values of , with excellent concord in the whole domain—since there are no boundaries, the erfc form-factor is unnecessary. Even though the spectrum spreads to infinity, it decays fast and is effectively more restrained to the region around zero than for Gaussian assets (formally corresponding to ), the more so the smaller is.

Version 2: IID temporal random volatilities. A more realistic approach would however be to choose the to be independent Gaussian with arbitrary volatilities , dependent on but not (176), and eventually to assume these to be IID random variables distributed according to (177). In this case, analogously as for the EWMA estimator (cf. Sec. III.2.6), the master equation is the conjectured (71) with

| (129) |

and it can be straightforwardly solved numerically—with proper care, as (129) cannot be expressed by elementary functions—to produce the MSD of the TLCE.

The borderline is a ring () or an annulus (), extending to infinity for , with the radii [(72a), (72b)],

| (130c) | ||||

| (130d) | ||||

They tend to the standard values [(119a), (119b)] in the Gaussian limit, , .

The solutions have been found and checked with Monte Carlo data in Fig. 4 (b), for , and three values of , with perfect agreement, except of a small area close to the border (for , i.e., when the MSD is bounded), to amend which the erfc form-factor should be used (not shown here). Note by comparing Figs. (a) and (b) that although the qualitative behavior of the MSD is analogous for Versions 1 and 2, its precise form is quite different.

III.2.8 Generalization to the free Lévy distribution

Another non-Gaussian model considered in this paper is the free Lévy law (cf. App. A.1.4). The master equations for the TLCE in the situation of the true covariance function factorized (41) into arbitrary and trivial has been developed in Sec. II.3.3 to be [(69a), (69b)] or (LABEL:eq:Case2A1TLCELevyEq02) for zero skewness. Setting in them (i.e., ; let since the variance is generalized by ) simplifies them to

| (131a) | |||

| (131b) | |||

with real and complex auxiliary unknowns, or in the case of zero skewness,

| (132) |

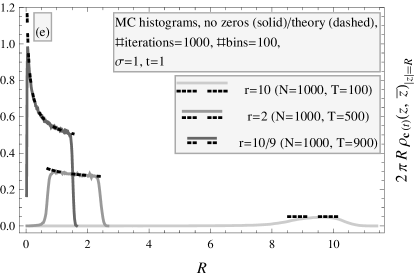

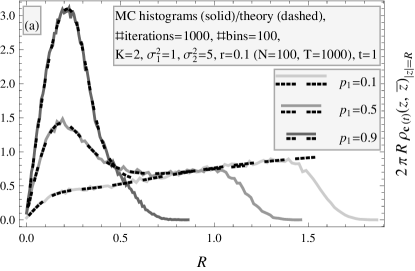

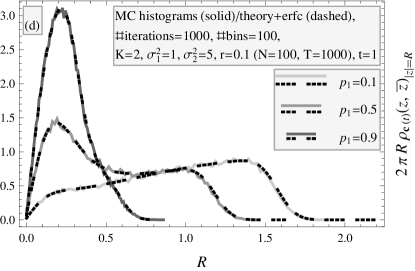

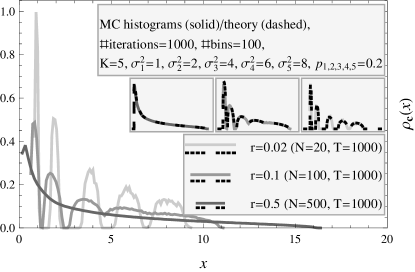

Figure 5 shows Monte Carlo histograms and the MSD following from numerical solutions to these equations for and the Lévy parameters (cf. the end of App. A.1.4), and respectively (a) or (b). The numerical eigenvalues have been obtained from Wigner-Lévy random matrices, as being more relevant for finances, hence some expected discrepancies are observed (yet not big, especially for no skewness). It is also notable that numerical histograms are nearly identical for zero and nonzero skewness, while the theoretical results differ, especially close to zero. Moreover, one may argue (by expanding and around zero, cf. Sec. II.3.3) that the domain in these cases extends to infinity, so only a part of it is shown.

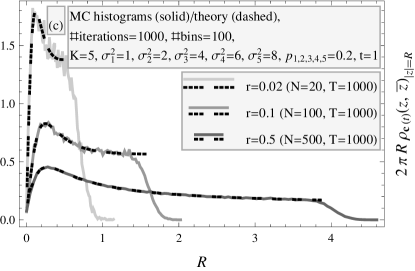

III.3 Toy Model 2: Gaussian assets with distinct variances

In this Section, effects of the presence of nontrivial true spatial covariances will be analyzed; since there are no temporal correlations here, it is enough to consider a diagonal prior .

Only the standard TLCE and Gaussian assets will be investigated below, albeit generalizations to the EWMA version of the TLCE or to Student or free Lévy assets—as for Toy Model 1 (cf. Secs. III.2.6, III.2.7, III.2.8)—are within reach of the methods described in Sec. II.3.3.

III.3.1 Toy Model 2a: Variance sectors

Definition. To begin with, in the fashion of the factor models (cf. the first part of Sec. I.2.1), consider a finite number of distinct variances,

| (133) |

where denote , for , which obey , and which are also assumed finite in the thermodynamic limit. The holomorphic -transform of , which is the basic ingredient of the master equation, thus reads

| (134) |

Borderline of the mean spectral domain. As explained in Secs. II.3.3 and II.5.3, the MSD is rotationally symmetric around zero, and its domain is either a disk () or an annulus (). The external radius (66a) reads

| (135) |

The internal radius (66b) is a function of a solution of a polynomial equation of order ,

| (136a) | ||||

| (136b) | ||||

This equation has no positive solutions (, required for positive ) for , and exactly one positive solution for . Indeed, the function has the first derivative always negative, and singularities (vertical asymptotes) at the points ; in other words, is piecewise decreasing in the intervals , , …, . A first implication is that all its zeros are real. Moreover, , which is negative or zero for and positive for ; and , which is always negative. This completes the proof.

Mean spectral density. The master equation is (65) with (134), and it is straightforward to solve it numerically for any .