A Bregman Extension of quasi-Newton updates II:

Convergence and Robustness Properties

Abstract

We propose an extension of quasi-Newton methods, and investigate the convergence and the robustness properties of the proposed update formulae for the approximate Hessian matrix. Fletcher has studied a variational problem which derives the approximate Hessian update formula of the quasi-Newton methods. We point out that the variational problem is identical to optimization of the Kullback-Leibler divergence, which is a discrepancy measure between two probability distributions. Then, we introduce the Bregman divergence as an extension of the Kullback-Leibler divergence, and derive extended quasi-Newton update formulae based on the variational problem with the Bregman divergence. The proposed update formulae belong to a class of self-scaling quasi-Newton methods. We study the convergence property of the proposed quasi-Newton method, and moreover, we apply the tools in the robust statistics to analyze the robustness property of the Hessian update formulae against the numerical rounding errors included in the line search for the step length. As the result, we found that the influence of the inexact line search is bounded only for the standard BFGS formula for the Hessian approximation. Numerical studies are conducted to verify the usefulness of the tools borrowed from robust statistics.

1 Introduction

We consider quasi-Newton methods for the unconstrained optimization problem

| (1) |

in which the function is twice continuously differentiable on . The quasi-Newton method is known to be one of the most successful methods for unconstrained function minimization. Details are shown in [15, 13] and references therein.

The main purpose of this paper is to present an extended framework of quasi-Newton method, and to study the robustness property of quasi-Newton update formulae against numerical errors of line search. There are mainly two standard quasi-Newton method; one is the DFP formula and the other is the BFGS formula. Fletcher [7] has pointed out that the standard formulae, DFP and BFGS, are obtained as the optimal solution of a variational problem over the set of positive definite matrices. Along this line, we extend the quasi-Newton update formula. Then, we study the robustness property of the extended quasi-Newton methods, where we apply some techniques exploited in the field of robust statistics [11].

We briefly introduce quasi-Newton formulae and its variational result. In quasi-Newton method, a sequence is successively generated in a manner such that . The coefficient is a step-size computed by a line search, and is a positive definite matrix approximating the Hessian matrix at the point . Let and be column vectors defined by

We need a Hessian approximation for to keep on the computation. In the DFP method, is given by

| (2) |

and the BFGS method provides the different formula such that

| (3) |

When and hold, both and are also positive definite matrices. In practice, the Cholesky decomposition of will be successively updated in order to compute the search direction efficiently. The idea of updating Cholesky factors is pioneered by Gill and Murray [9]. Note that the equality

holds. Hence, the update formula for the inverse can be directly derived from without computing inversion of matrix.

We introduce a variational approach in quasi-Newton methods. Let be the set of all by symmetric positive definite matrices, and the function be a strictly convex function over defined by

Fletcher [7] has shown that the DFP update formula (2) is obtained as the unique solution of the constraint optimization problem,

where for is the matrix satisfying and . The BFGS formula is also obtained as the optimal solution of

in which denotes or equivalently .

It will be worthwhile to point out that the function is identical to Kullback-Leibler(KL) divergence [1, 12] up to an additive constant. Let be the dimensional Gaussian distribution with mean zero and variance-covariance matrix , then the KL-divergence between and is defined by

which is equal to . The KL-divergence is regarded as a generalization of squared distance over the space of probability distributions. Using the KL-divergence, we can represent the update formulas as the optimal solution of the following minimization problems,

| (DFP) | (4) | |||

| (BFGS) | (5) |

The KL-divergence is asymmetric, that is, in general. Hence the above problems will provide different solutions.

Here is the brief outline of the article. In Section 2 we introduce the so-called Bregman divergence which is an extension of the KL-divergence. In Section 3, an extended quasi-Newton formula is derived based on the Bregman divergence. In Section 4, the convergence property of the proposed quasi-Newton method is studied, and Section 5 is devoted to discuss the robustness of the Hessian update formula. Numerical simulations are presented in Section 6. We conclude with a discussion and outlook in Section 7. Some proofs of the theorems are postponed to Appendix.

Throughout the paper, we use the following notations: The set of positive real numbers are denoted as . Let be the determinant of square matrix , and denotes the set of by non-degenerate real matrices. The set of all by real symmetric matrices is denoted as , and let be the set of by symmetric positive definite matrices. For two square matrices , the inner product is defined by , and is the Frobenius norm defined by the square root of . Throughout the paper we only deal with the inner product of symmetric matrices, and the transposition in the trace will be dropped. For a vector , denotes the Euclidean norm. The first and second order derivative of a function are denoted as and , respectively.

2 Bregman Divergence induced from Potential Functions

As introduced in Section 1, the update formulae of the DFP and the BFGS methods are derived from the optimization problem of KL-divergence. In this section we introduce Bregman divergence [3] which is an extension of the KL-divergence. Especially we focus on the Bregman divergence induced from potential function. Then, we present extended quasi-Newton formulae derived from the variational problem for the Bregman divergence.

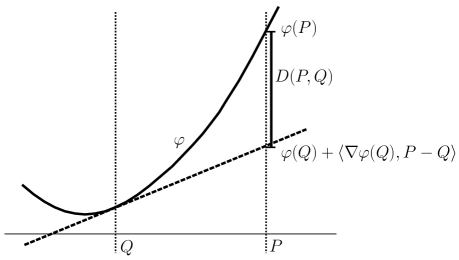

Let be a differentiable, strictly convex function that maps positive definite matrices to real numbers. We define Bregman divergence of the matrix from the matrix as

| (6) |

where is the by matrix whose element is given as . The strict convexity of guarantees that is non-negative and equals to zero if and only if holds. Figure 1 illustrates the relation between the function and the Bregman divergence. Note that is convex in but not necessarily convex in . Bregman divergences have been well studied for nearness problems in the fields of statistics and machine learning [2, 6, 14].

In this paper, we focus on the Bregman divergence induced from potential function [17]. Let be a strictly convex, decreasing, and third order continuously differentiable function. For the derivative , the inequality holds from the assumption. Indeed, the assumption leads to and , and if holds for some , then holds for all . Hence is affine function for . This contradicts the strict convexity of . We define the functions and such that

The subscript of and will be dropped if there is no confusion.

Definition 1 (potential function).

Let be a function which is strictly convex, decreasing, and third order continuously differentiable. Suppose that the functions and defined from satisfy the following conditions:

| (7) | ||||

| (8) |

for all and

| (9) |

Then, is called potential function or potential for short. For , the function is also referred to as potential on .

As shown in [17], the function is strictly convex in if and only if satisfies (7) and (8). The condition (9) guarantees the existence of Hessian update formula, which is discussed in Section 3.

Given a potential function , the Bregman divergence defined from the potential function in (6) is denotes as , and referred to as -Bregman divergence. The -Bregman divergence has the form of

Indeed, substituting

into (6), we obtain the expression of . Below we show some examples of -Bregman divergence.

Example 1.

For the negative logarithmic function , we have . Then -divergence is equal to KL-divergence,

Note that holds. Hence, is convex in both and .

Example 2.

For the power potential with , we have and . Then, we obtain

The KL-divergence is recovered by taking the limit of .

Example 3.

For , let be . Then is a convex and decreasing function, and we obtain

for . The negative-log potential is derived by setting . This potential satisfies the inequality . The bounding condition of will be assumed in the convergence analysis of Section 4.

We apply -Bregman divergences to extend quasi-Newton update formula.

3 Extended quasi-Newton update formula

To extend the standard quasi-Newton methods, we consider the optimization problem of the -Bregman divergence instead of the KL-divergence. Let us define the -BFGS formula as the optimal solution of the problem,

| (10) |

Next we define -DFP update formula which is an extension of the standard DFP formula (2). Note that KL-divergence satisfies .

Then, the optimization problem associated with the DFP update formula (4) can be extended to the problem,

| (11) |

The problem (11) is convex in , since the objective function is convex in and the constraint is affine in . Mainly we consider the -BFGS update formula. The argument on the -DFP update is almost the same.

Theorem 1.

Let , and suppose . Then the problem (10) has the unique optimal solution satisfying

| (12) |

The proof is found in Appendix A.

Note that the -BFGS update formula is represented by the affine sum of and . This form is equivalent to the self-scaling quasi-Newton update [18, 16] defined as

| (13) |

where is a positive real number. In the -BFGS update formula, the coefficient is determined from the function . The inverse of the matrix (13) is given by

| (14) |

As the result, for any , the matrix in (13) is positive definite. Indeed, for the expression (13) guarantees the positive definiteness of , and for , the expression (14) implies . Therefore in (12) is also positive definite matrix, since any potential satisfies .

In the self-scaling update formula in (13), the choice

| (15) |

is often recommended. As analyzed in [16], however, the self-scaling method with inexact line search for the step length tends to lead the relative inefficiency compared to the standard BFGS method. Following Example 4 below, we prove that the self-scaling method with the scaling parameter (15) is not derived from the -Bregman divergence.

We present a practical way of computing the Hessian approximation (12). In Eq (12), the optimal solution appears in both sides, that is, we have only the implicit expression of . The numerical computation is, however, efficiently performed as well as the standard BFGS update. To compute the update formula , first we compute . The determinant of both sides of (12) leads to

| (16) |

Hence, by solving the nonlinear equation

we can find . As shown in the proof of Theorem 1, the function is monotone increasing. Hence the Newton method is available to find the root of the above equation efficiently. Once we obtain the value of , we can compute the Hessian approximation by substituting into Eq (12). Figure 2 shows the update algorithm of the -BFGS formula which exploits the Cholesky decomposition of the approximate Hessian matrix. By maintaining the Cholesky decomposition, we can easily compute the the determinant and the search direction. In the algorithm of Figure 2, we require the Wolfe condition [15, Section 3.1] for the step length . As shown in Section 4, the Wolfe condition is useful to establish the convergence property of the optimization algorithm.

In the same way as the proof of Theorem 1, we obtain the -DFP update formula defined from (11) such that

| (17) |

It is straightforward to unify the -BFGS method and the -DFP method in the same way as the standard Broyden family [4]. Let be the Hessian approximation given by the -BFGS update formula with the potential , and be the Hessian approximation given by the -DFP update formula with the potential . Then the update formula of the -Broyden family is defined by

| (18) |

for . The -Broyden family is obtained by a convex-full of , and . The standard Broyden family is recovered by setting .

-BFGS update: Initialization: The function denotes . Let be a matrix which is an initial approximation of the Hessian matrix, and be the Cholesky decomposition of . Let be an initial point, and set . Repeat: If stopping criterion is satisfied, go to Output. 1. Let , where is a step length satisfying the Wolfe condition [15, Section 3.1]. The Cholesky decomposition is available to compute . 2. Set and . 3. Update to which is the Cholesky decomposition of , that is, The Cholesky decomposition with rank-one update is available. 4. Compute and find the root of the equation Let the solution be . 5. Compute the Cholesky decomposition such that 6. . Output: Local optimal solution .

Example 4.

We show the -BFGS formula derived from the power potential. Let be the power potential with . As shown in Example 2, we have . Due to the equality

and Eq. (16), for the power potential we have

Then the -BFGS update formula is given as

For such that , we have . Remember that the standard self-scaling update formula corresponds to the above update with . Therefore, the standard self-scaling update formula is not derived from the power potential. Indeed, the power potential with or equivalently is a convex function but not a strictly convex function.

In terms of the self-scaling update formula, we show the following proposition.

Proposition 2.

There does not exist the potential function such that in Eq. (12) the equality

| (19) |

holds for any and any satisfying .

Proof.

We have two equalities,

Hence, we have

Suppose that there exists a potential function satisfying (19). Then we have

and hence the equality

holds. Substituting the above formula into (19), we have

Let be a positive definite matrix such that , and be . Then we have for . The corresponding is given as , and this does not satisfy the definition of the potential function.

4 Convergence Analysis

We consider the convergence property of the -BFGS method. Some standard assumptions about the objective function are stated below. See Section 6.4 of [15] for details.

Assumption 1.

-

1.

The objective function is twice continuously differentiable.

-

2.

Let be the Hessian matrix of at . For the starting point , the level set is convex, and there exist positive constants and such that

(20) holds for all and .

The following theorem implies that the sequence generated by the -BFGS update formula converges to the local minimizer of if the function of a potential satisfies the bounding condition.

Theorem 3.

Let be an initial matrix and be a starting point which meets Assumption 1. Suppose that there exist positive constants such that . Then the sequence generated by the -BFGS update converges to the minimizer of .

Lemma 4 (Eq. 6.12 in [15]).

Let be the averaged Hessian

then the property follows from Taylor’s theorem, where .

Proof of Theorem 3.

Let be the sequence of approximate Hessian matrices generated by the -BFGS update formula. We define and by and , respectively. Then the update formula shown in Theorem 1 is represented as

| (21) |

We compute

The inequality (20) yields

| (22) | ||||

| (23) |

We now define

Then the trace of is bounded above. Indeed, the inequality

holds, where (23) is used. Using the formula for , we obtain a lower bound of the determinant such that

These inequalities present an upper bound of ,

The second inequality is derived from

As the result we obtain

where is a positive constant such that . Let us then proceed by contradiction and assume that . Then there exists such that for all , we have

Thus the following inequality holds for all :

The right-hand-side is negative for large , giving a contradiction. Therefore there exists a subsequence satisfying . By Zoutendijk’s result111Under some condition, holds. See Theorem 3.2 in [15] with the Wolfe condition, this limit implies that . The convexity of on guarantees that converges to the local optimal solution.

5 Robustness against Inexact Line Search

The robustness against numerical errors such as the round-off error is an important feature in numerical computation. In this section we study the robustness of quasi-Newton update against numerical errors involved in the line search. Mainly there are two types of quasi-Newton updates: one is the update formula for approximate Hessian matrix; and the other is the update for approximate inverse Hessian matrix. In the approximate inverse Hessian update, the matrix is directly update to under the secant condition . We study four kinds of update formulae, that is, -BFGS/-DFP method for the Hessian approximation/the inverse Hessian approximation.

Let us consider the Hessian approximation formula. Under the exact line search, the matrix is updated to which is the minimum solution of or subject to . Let

be the point computed by the exact line search. When the line search is inexact, the step length will be slightly perturbed and then will be changed to where is an infinitesimal. The vector will also change to defined by

Then the constraint for the Hessian update becomes .

We study the relation between the perturbation of and the Hessian approximation or the inverse Hessian approximation . Based on the above argument, we consider the optimization problem defined by

| (-BFGS-B) | (24) | |||

| (-DFP-B) | (25) |

for a fixed matrix and fixed vectors , where the subscript for the vectors is dropped for simplicity. In the same way, the update formula for the inverse Hessian under the inexact line search is defined as the optimal solution of the following problem,

| (-BFGS-H) | (26) | |||

| (-DFP-H) | (27) |

for fixed . The update formula given by -BFGS-H/-DFP-H directly provides the inverse matrix of computed by -BFGS-B/-DFP-B, respectively. Theorem 1 guarantees that there exists the unique optimal solution as long as holds. Though Theorem 1 deals with only -BFGS-B formula, we can prove the existence and the uniqueness of optimal solution for the other problems in the same manner.

In order to study the robustness of update formulae, we borrow the concepts such that the influence function or the gross error sensitivity from the study of robust statistics [11]. Below the -BFGS-B update formula is considered as an example. Let be the optimal solution of -BFGS-B in (24). Then the influence function of is defined as the derivative of at , that is,

Later we prove the differentiability of . From the definition of the influence function, the optimal solution is asymptotically equal to . This implies that the inexact line search has a large impact on the computation of Hessian approximation, when the norm of is large. In the sense of the influence function, the preferable potential is the function which provides the influence function with a small norm.

For fixed vectors and such that , the influence function depends on the matrix and the vector . We consider the worst-case evaluation of the influence function in terms of and . The gross error sensitivity is defined as the largest norm of the influence function, that is,

where and are appropriate subsets. In many case, the gross error sensitivity becomes infinity if or is unbounded. Our concern is to find the potential function which leads finite gross error sensitivity under some reasonable setup.

The influence function and the gross error sensitivity have been studied in robust statistics [11]. We use these statistical techniques to analyze the stability of numerical computation. In the literature of statistics, the “statistical model” or is fixed, and the “observed data” or is contaminated such that , while in the present analysis, the matrix is fixed and the model corresponding to the secant condition is perturbed.

The potential function minimizing the gross error sensitivity will be preferable for robust computation. Below we prove that the standard BFGS update for the Hessian approximation is the more robust than the other update formulae. This result meets the empirical observations [5, 15]. Moreover, only the standard BFGS update for the Hessian approximation has finite gross error sensitivity. Theoretical results are summarized in Table 1.

| -BFGS | -DFP | |

|---|---|---|

| Hessian approx. | finite only for BFGS | |

| inverse Hessian approx. |

In the following, the gross error sensitivity with and a bounded subset is considered. Note that the boundedness of follows the assumption that is bounded above over . First, we note that the influence function and the gross error sensitivity make sense for minimization of non-quadratic functions.

Lemma 5.

Suppose that the objective function is a convex quadratic function. Then, the influence function and the gross error sensitivity are equal to zero.

Lemma 5 is clear, since for the quadratic objective function the secant condition is changed to under the inexact line search. That is, the secant condition is kept unchanged, and thus holds.

We prove that generally the influence function is well-defined.

Theorem 6.

Proof is deferred to Appendix B.

The gross error sensitivity of each update formula is computed in the following theorems. Proofs are deferred to Appendix C.

Theorem 7 (gross error sensitivity of -BFGS-B).

Suppose . Let and be fixed vectors such that and be a bounded subset in . For small , let be the optimal solution of -BFGS-B in (24). Then, the optimal potential function of the problem

| (28) |

is given as up to a constant factor. In the above min-max problem, the function is sought from among all potentials.

Theorem 8 (gross error sensitivity of -DFP-B).

Suppose . Let and be fixed vectors such that and be a bounded subset in . Suppose that there exists an open subset included in . Let be the optimal solution of -DFP-B in (25). Then for any potential , the equality

holds.

Theorem 9 (gross error sensitivity of -BFGS-H).

Suppose . Let and be fixed vectors such that and be a bounded subset in . Suppose that there exists an open subset included in . Let be the optimal solution of -BFGS-H in (26). Then, for any potential , the equality

holds.

Theorem 10 (gross error sensitivity of -DFP-H).

Suppose . Let and be fixed vectors such that and be a bounded subset in . Let be the optimal solution of -DFP-H in (27). Then, for any potential , the equality

holds.

It is well-known that there is the dual relation between the BFGS formula and the DFP formula. Indeed, the -DFP update for the inverse Hessian approximation is derived from the -BFGS update formula for the Hessian approximation by replacing with . For the robustness against inexact line search, however, the dual relation is violated as shown in Table 1. In this problem, we focus on the perturbation of the vector rather than that of . This is the reason why the dual relation is violated. Powell has shown a critical difference between BFGS and DFP for quadratic convex objective functions [19] by considering the behaviour of eigenvalues of approximate Hessian matrix. In the present paper, we exploited the gross error sensitivity which is meaningful for non-quadratic objective functions as shown in Lemma 5. Our approach also provides a critical difference between BFGS and DFP methods.

6 Numerical Studies

We demonstrate numerical experiments on robustness of quasi-Newton update formulae such as -BFGS-B, -DFP-B, -BFGS-H, and -DFP-H proposed in Section 5. Especially, the update formula derived from power potential in Example 2 is examined.

In the first numerical study, we consider numerical stability of update formulae. Let be the optimal solution of -BFGS-B (24) or -DFP-B (25), and be the optimal solution of -BFGS-H (26) or -DFP-H (27). For each update formula, we numerically compute the approximate influence function and with small , where the power potential is used to derive the approximate Hessian matrix. Remember that -BFGS and -DFP are respectively reduced to the standard BFGS and DFP when is equal to zero.

In what follows, we show the setup of numerical studies. Let be the by diagonal matrix with diagonal elements . For -BFGS-B and -DFP-B, the matrix is set to one of the following three matrices:

where in the last one is the identity matrix and is a column unit vector defined below. The dimension of the matrix is set to or . The first matrix has the determinant one, and the other two matrices have a large determinant. Below we show the procedure for generating the vectors and and the contaminated vectors and for -BFGS-B and -DFP-B. In the numerical studies for -BFGS-H and -DFP-H, the matrix is replaced with the approximate inverse Hessian .

-

1.

In the case that is or , the vectors and are both generated according to the multivariate normal distribution with mean zero and variance-covariance matrix . If the inner product is non-positive, the sign of is flipped. The intensity of noise involved in the line search is determined by , which is generated according to the uniform distribution on the interval . Then, the vector is also generated according to the multivariate standard normal distribution. If the inequality does not hold, again and are generated until the vectors enjoy the positivity condition.

-

2.

In the case that is supposed to have the expression , first the vector is generated according to the multivariate normal distribution with mean zero and variance-covariance matrix , and is defined such that . The vector is a unit vector which is orthogonal to , that is, is a vector satisfying and , and let be . Then the vector is defined as . The construction of these vectors is used in the proof of Theorem 9 and Theorem 10.

Hessian or inverse Hessian update formula is applied to or with the randomly generated secant condition. The updated matrix and are respectively computed under the constraint and by using -BFGS-B and -DFP-B update formula. In the same way, -BFGS-H and -DFP-H are respectively applied to compute with the constraint and with the perturbed secant condition . The influence function of each update formula is approximated by or .

Table 2 shows the average of the approximate influence function over runs for each setup. When or is equal to the diagonal matrix , we see that the power of the power potential does not significantly affect the influence function in both -BFGS and -DFP. For the other setups, overall the BFGS method for Hessian matrix, i.e. -BFGS-B with , has smaller influence function than the other update formulae. The -DFP-H for inverse Hessian update also has relatively small influence function when is proportional to . For , however, we find that -DFP-H is sensitive against noise involved in the line search.

These numerical results meet the theoretical analysis as shown below:

-

1.

Theorem 7 implies that the standard BFGS method is robust against inexact line search.

-

2.

As shown in Example 4, -BFGS-B update with power potential is close to the standard BFGS update for large and moderate . That is, the mixing parameter in Example 4 will be close to one if is large and does not depend on the dimension that much. When has a large determinant which grows with the dimension , the number of will severely depend on the dimension . Hence, the mixing parameter will not close to one even for large . Hence, in such case the influence function is affected by the choice of the power . The same argument on the relation between influence function and the power will hold for the inverse Hessian update, that is, -BFGS-H and -DFP-H.

-

3.

For the result on -BFGS-B and -DFP-B is numerically the same. Under this setup, we can theoretically confirm that the influence functions of both update formula are identical to each other. On the other hand, some calculation yields that the influence functions of -BFGS-H and -DFP-H are not the same.

The standard BFGS update formula achieves the min-max optimality of the gross error sensitivity. That is, BFGS method may not be necessarily optimal for each setup. In numerical studies, however, BFGS method uniformly provides fairly stable update formula compared to the other methods.

| -BFGS-B | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| 9.5e+00 | 9.5e+00 | 9.5e+00 | 1.5e+01 | 9.7e+00 | 9.5e+00 | 2.0e+02 | 1.0e+02 | 5.0e+01 | |

| 2.7e+01 | 2.7e+01 | 2.7e+01 | 2.3e+02 | 2.8e+01 | 2.7e+01 | 1.1e+04 | 1.0e+04 | 8.7e+03 | |

| 9.3e+01 | 9.3e+01 | 9.3e+01 | 2.8e+03 | 9.6e+01 | 9.3e+01 | 2.6e+05 | 2.5e+05 | 2.4e+05 | |

| 1.0e+02 | 1.0e+02 | 1.0e+02 | 7.4e+03 | 1.1e+02 | 1.0e+02 | 1.0e+06 | 9.9e+05 | 9.7e+05 | |

| -DFP-B | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| 1.3e+02 | 1.3e+02 | 1.3e+02 | 2.9e+03 | 6.5e+02 | 1.5e+02 | 2.0e+02 | 1.0e+02 | 5.0e+01 | |

| 1.7e+03 | 1.7e+03 | 1.7e+03 | 2.5e+06 | 6.5e+04 | 1.7e+03 | 1.1e+04 | 1.0e+04 | 8.7e+03 | |

| 4.6e+04 | 4.6e+04 | 4.6e+04 | 1.6e+09 | 8.7e+06 | 4.7e+04 | 2.6e+05 | 2.5e+05 | 2.4e+05 | |

| 3.0e+04 | 3.0e+04 | 3.0e+04 | 4.1e+09 | 1.1e+07 | 3.0e+04 | 1.0e+06 | 9.9e+05 | 9.7e+05 | |

| -BFGS-H | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| 2.1e+02 | 2.1e+02 | 2.1e+02 | 4.8e+03 | 1.1e+03 | 2.4e+02 | 2.2e+02 | 1.1e+02 | 5.6e+01 | |

| 1.1e+03 | 1.1e+03 | 1.1e+03 | 1.6e+06 | 4.1e+04 | 1.1e+03 | 2.0e+04 | 1.7e+04 | 1.5e+04 | |

| 8.2e+04 | 8.2e+04 | 8.2e+04 | 2.8e+09 | 1.5e+07 | 8.3e+04 | 8.7e+05 | 8.4e+05 | 8.1e+05 | |

| 2.6e+04 | 2.6e+04 | 2.6e+04 | 3.6e+09 | 9.8e+06 | 2.7e+04 | 4.7e+06 | 4.6e+06 | 4.5e+06 | |

| -DFP-H | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| 1.0e+01 | 1.0e+01 | 1.0e+01 | 1.7e+01 | 1.1e+01 | 1.0e+01 | 2.5e+02 | 1.3e+02 | 6.4e+01 | |

| 2.1e+01 | 2.1e+01 | 2.1e+01 | 4.5e+02 | 2.5e+01 | 2.1e+01 | 4.1e+06 | 3.6e+06 | 3.1e+06 | |

| 9.9e+01 | 9.9e+01 | 9.9e+01 | 9.5e+03 | 1.2e+02 | 9.9e+01 | 1.4e+09 | 1.4e+09 | 1.3e+09 | |

| 1.2e+02 | 1.2e+02 | 1.2e+02 | 3.6e+04 | 1.7e+02 | 1.2e+02 | 1.2e+10 | 1.2e+10 | 1.2e+10 | |

Next, we apply the standard BFGS-B and DFP-B to solve the following two optimization problems: the quadratic convex problem

where and

and the boundary value problem [8]

where the vector and the matrix are the same as problem 1. The objective function in problem 2 is non-linear and non-convex. The initial point is randomly generated by -dimensional normal distribution with mean zero and variance-covariance matrix . The termination criterion

is employed, which is the same criterion used by Yamashita [20]. Although the second criterion above implies that the method fails to obtain a solution, all trials did not reach the maximum number of iterations. In each problem, the step-length is computed by the matlab command “fminbnd” with the option which denotes the termination tolerance on . In the same way as the numerical studies on robustness of update formulae, the vector is randomly perturbed such that , where is a random variable according to the uniform distribution on the interval . The number of varies from to . Accordingly, the vector is also changed to . As the result, for each iteration the secant condition with inexact line search is given as .

The average number of iterations over runs for BFGS and DFP is shown in Table 3. Compared to DFP method, BFGS method requires fewer number of iterations to reach the optimal solution. Moreover, in BFGS update the number of iterations is stable against the number of . This result implies that BFGS is robust against random noise involved in inexact line search. On the other hand, the behaviour of DFP method is sensitive to contaminated step-length. Indeed, the number of iterations in DFP method rises drastically with the intensity of the noise. For the quadratic convex objective function, the inexact line search does not affect the secant condition. Hence the numerical result will impliy that the goodness of the descent direction in DFP will be easily degraded by inexact line search. These numerical properties in quasi-Newton methods have been empirically well-known [5, 15]. Powell [19] has theoretically studied the progression of eigenvalues in approximate Hessian matrices in order to illustrate the difference between BFGS and DFP.

Through the numerical stduies in this section, we found that the theoretical framework exploiting robust statistics can be a useful tool to investigate the property of quasi-Newton methods.

| BFGS | DFP | BFGS | DFP | BFGS | DFP | ||

|---|---|---|---|---|---|---|---|

| Problem 1 | 0.0 | 100.4 | 110.6 | 434.6 | 577.8 | 682.1 | 1788.5 |

| 0.1 | 102.9 | 166.2 | 430.6 | 1165.2 | 680.9 | 2628.9 | |

| 0.2 | 104.5 | 198.6 | 443.6 | 1361.8 | 685.1 | 3099.2 | |

| 0.3 | 106.0 | 223.0 | 444.2 | 1501.6 | 687.6 | 3365.9 | |

| Problem 2 | 0.0 | 100.9 | 111.6 | 428.5 | 585.7 | 661.5 | 2489.8 |

| 0.1 | 102.8 | 153.5 | 443.5 | 1237.4 | 672.4 | 2762.1 | |

| 0.2 | 104.4 | 177.7 | 438.3 | 1419.6 | 682.7 | 3301.2 | |

| 0.3 | 106.1 | 199.4 | 454.0 | 1592.8 | 694.0 | 3730.8 | |

7 Concluding Remarks

Along the line of the research stared by Fletcher [7], we considered the quasi-Newton update formula based on the Bregman divergence induced from potential functions. The proposed update formulae for the Hessian approximation belong to the class of self-scaling quasi-Newton method. We studied the convergence property. Then, we applied the tools in the robust statistics to analyze the robustness of the Hessian update formulae. As the result, we found that the influence of the inexact line search is bounded only for the standard BFGS formula for the Hessian approximation. Numerical studies support the usefulness of the theoretical framework borrowed from the robust statistics.

It will be an interesting future work to investigate the practical advantage of the self-scaling quasi-Newton methods derived from the -Bregman divergence. Nocedal and Yuan proved that the self-scaling quasi-Newton method with the popular scaling parameter (15) has some drawbacks [16]. In our framework, the self-scaling quasi-Newton method with the scaling parameter (15) is out of the formulae derived from -Bregman divergence. More precisely, the function , which is not potential, formally leads the popular self-scaling quasi-Newton formula. For the corresponding Bregman divergence , the equality holds for any and any . This property implies that the scale of the Hessian approximation is not fixed. We think that this property may lead some inefficiency of the self-scaling quasi-Newton method with (15). The self-scaling quasi-Newton method associated with -Bregman divergence may performs well in practice.

Another research direction is to consider the choice of the potential function . Under the criterion of the gross error sensitivity, we found that the negative logarithmic function is the optimal choice. The other criterion may lead other optimal potentials. Investigating the relation between the criterion for the update formula and the optimal potential will be beneficial for the design of numerical algorithms.

8 Acknowledgements

The authors are grateful to Dr. Nobuo Yamashita of Kyoto university for helpful comments. T. Kanamori was partially supported by Grant-in-Aid for Young Scientists (20700251).

Appendix A Proof of Theorems 1

We prove the following lemma which is useful to show the existence of the optimal solution.

Lemma 11.

Let be a potential and . For any the equation

| (29) |

has the unique solution.

Proof.

We define the function by , then, the (29) is equivalent to the equation

| (30) |

Since the potential function satisfies from the definition, we have . In terms of the derivative of , we have the following inequality

Thus, is an increasing function on . Moreover we have

The above inequality implies that . Since is continuous, the equation (30) has the unique solution.

Proof of Theorem 1.

First, we show the existence of the matrix satisfying (12). Lemma 11 now shows that there exists a solution for the equation

By using the solution , we define the matrix such that

then the determinant of satisfies

in which the first equality comes from the formula and the second one follows the definition of . Hence there exists satisfying (12).

Next, we show that the matrix in (12) satisfies the optimality condition of (10). According to Güler, et al. [10], the normal vector for the affine subspace

is characterized by the form of

| (31) |

In fact for we have

and thus is a normal vector of . Güler, et al. [10] have shown that the normal vector is restricted to the form of (31).

Suppose be an optimal solution of (10), then satisfies the optimality condition that there exists a vector such that

where denotes the gradient of with respect to the variable . Also, the optimal solution should satisfy the constraint . On the other hand, the matrix defined by (12) satisfies

The conditions and guarantees the existence of the above vector . In addition, the direct computation yields that the constraint is satisfied. Hence, satisfies the optimality condition. Since (10) is a strictly convex problem, is the unique optimal solution.

Appendix B Proofs of Theorems 6

We show that the optimal solution of -BFGS-B is second order continuously differentiable. The same proof works for the other update formulae.

Proof.

We consider the problem (24). Since the inequality holds for infinitesimal , Theorem 1 guarantees that there exists the unique optimal solution around . Let the function be

for and . For infinitesimal , the equality holds, where is the null matrix. We apply the implicit function theorem to prove the differentiability of . Since the potential function is third order continuously differentiable, clearly is second order continuously differentiable in a vicinity of . For any symmetric matrix , the equality

holds, where denotes the gradient with respect to the variable . This implies that the gradient of does not vanish at . Hence, the implicit function theorem for guarantees that is a second order continuously differentiable function with respect to in a vicinity of .

Appendix C Computations of Gross Error Sensitivity

First, a universal formula for the computation of influence function is proved, and some useful lemmas are prepared. Then, the gross error sensitivity for each update formula is computed in Section C.1, C.2, C.3 and C.4.

Lemma 12.

Let and be column vectors in such that , and be a positive definite matrix. For an infinitesimal let be the optimal solution of

| (32) |

and let be the influence function . Then we have

| (33) |

The matrix is well-defined, since the inequalities and hold for any potential function. Note that holds. This is another proof of Lemma 5.

Proof of Lemma 12.

In the same way as the proof of Theorem 1 and Theorem 6, we can prove the existence and the differentiability of . Since is second order continuously differentiable around , the equality

holds, where . Then we have

and thus we obtain

For simplicity let be

| (34) |

then the equality

| (35) |

holds. By some calculation, we see that the asymptotic expansion of and are respectively given by

| (36) |

and

| (37) |

Substituting (35), (36) and (37) into the equality

we obtain

and thus is represented as

in which we use the equality

Substituting the above into (34), we have

As the result, we obtain

Letting tend to zero, we obtain the influence function .

Lemma 13.

Let and be a set of column vectors in such that and be a matrix in . For an infinitesimal let be the optimal solution of

and let be then we have

| (38) |

where is the function defined in Lemma 12.

Proof.

Let be the optimal solution of

then, clearly holds. Thus we have

where is applied.

We show another lemma which is useful to prove that the gross error sensitivity diverges to infinity.

Lemma 14.

Suppose for non-negative integers and . For any set of vectors such that and any positive real number , there exists a sequence satisfying the following three conditions:

-

1.

The equalities and hold for all and .

-

2.

for all .

-

3.

.

Proof.

For any such that there exists satisfying . Indeed, for the by identity matrix , the matrix is well-defined and satisfies . When holds, there exist two unit vectors satisfying and

We will show that the matrix

with

| (39) |

satisfies four conditions: and for all . The first two equalities are clear from the definition of and . The determinant of is equal to

For any unit vector we have

and in addition the determinant of is equal to . Thus is positive definite. Let be the maximum eigenvalue of , and be a unit vector defined by . Then in terms of the maximum eigenvalue of we have

Then tends to infinity when tends to infinity. Thus the sequence defined by

| (40) |

satisfies the conditions of the lemma.

C.1 Proof of Theorem 7

Let be the optimal solution of (24). Under the inexact line search, the influence function for -BFGS-B is equal to which is defined in Lemma 12. Thus we have

| (41) |

If holds for any , the potential does not affect the norm of the influence function, because the first term of the above expression vanishes. Thus, clearly is an optimal potential. Below we assume for a vector . Suppose that satisfies . Then holds, and the triangle inequality yields that

If is not the null function, there exists such that . Lemma 14 with implies that for there exists a sequence satisfying for all and . Hence

holds, and then we obtain

On the other hand, if for all , we obtain

since is bounded. As the result, the potential such that minimizes the gross error sensitivity. The condition leads to up to a constant factor.

C.2 Proof of Theorem 8

Let be the optimal solution of (25). Under the inexact line search, the influence function for -DFP-B is equal to which is defined in Lemma 13.

First, we study the case that is not the null function. For the matrix such that , we have . Using Lemma 13 for , we have

in which the equality is used. The above expression is almost same as (41) with , and thus the same proof works to obtain

Next, we study the case that is the null function, that is, . Then, and hold. Let be a positive definite matrix which does not necessarily satisfy . Then we obtain

in which we used . For , the updated matrix is equal to and thus, we have

| (42) |

Let and be a positive real number, and we define , then for some calculation yields

where is defined by

Since contains an open subset, there exists a vector which is linearly independent to . Clearly there exists such that three vectors, and , are linearly independent. For such choice, is not the null matrix, and the equality

holds. As the result, even for the standard DFP formula, we have

In summary, for all -DFP update for the Hessian approximation, the gross error sensitivity defined in Theorem 8 is equal to infinity.

C.3 Proof of Theorem 9

Let be the optimal solution of (26). Under the inexact line search, the influence function for -BFGS-H is equal to which is defined in Lemma 13.

First, we study the case that is not the null function. Suppose . If satisfies , then we have . Using Lemma 12 and Lemma 13 for the matrix such that , we obtain

| (43) |

Lemma 14 with implies that for there exists a sequence satisfying the following conditions: and for all ; for all ; . We define which does not depend on . Then for we have

Hence the equality

holds, and thus we obtain

Next, we study the case that is the null function, that is, . Then, and holds. For such that , we have

| (44) |

Let be a matrix satisfying . Let and be vectors satisfying and . For , the existence of and is guaranteed by the assumption on . Indeed, there exists such that and are linearly independent. We now define the matrix by

Then we have

where and . Substituting into (44), we obtain

This implies that

for . Hence we obtain

even for the standard BFGS update of the inverse Hessian approximation.

C.4 Proof of Theorem 10

Let be the optimal solution of (27). Under the inexact line search, the influence function for -DFP-H is equal to which is defined in Lemma 12.

First, we study the case that is not the null function. Suppose for . If satisfies , we have . Using Lemma 12 for the matrix such that , we obtain

The above expression is almost same as (43), and thus the same proof remains valid to obtain

Next, we consider the case that is the null function. Then and hold. For such that , we have

This is the same as the influence function of (44), and thus, we obtain

References

- [1] S. Amari and H. Nagaoka. Methods of Information Geometry, volume 191 of Translations of Mathematical Monographs. Oxford University Press, 2000.

- [2] A. Banerjee, S. Merugu, I. Dhillon, and J. Ghosh. Clustering with bregman divergences. Journal of Machine Learning Research, 6:1705–1749, 2005.

- [3] L. M. Bregman. The relaxation method of finding the common point of convex sets and its application to the solution of problems in convex programming. USSR Computational Mathematics and Mathematical Physics, 7:200–217, 1967.

- [4] C. G. Broyden. Quasi-newton methods and their application to function minimisation. Mathematics of Computation, 21(99):368–381, 1967.

- [5] A. R. Conn, N. I. M Gould, and P. L. Toint. Testing a class of algorithms for solving minimization problems with simple bounds on the variables. Mathematics of Computation, 50:399–430, 1988.

- [6] I. Dhillon and J. Tropp. Matrix nearness problems with bregman divergences. SIAM J. Matrix Anal. Appl., 29(4):1120–1146, 2007.

- [7] R. Fletcher. A new result for quasi-Newton formulae. SIMA J. Optim., 1:18–21, 1991.

- [8] R. Fletcher. An optimal positive definite update form sparse hessian matrices. SIMA J. Optim., 5:192–218, 1995.

- [9] P. E. Gill and W. Murray. Quasi-Newton methods for unconstrained optimization. J. Inst. Math Appl., 9:91–108, 1972.

- [10] O. Güler, F. Gürtuna, and O. Shevchenko. Duality in quasi-newton methods and new variational characterizations of the DFP and BFGS updates. Optimization Methods and Software, 24(1):45–62, 2009.

- [11] F. R. Hampel, P. J. Rousseeuw, E. M. Ronchetti, and W. A. Stahel. Robust Statistics. The Approach based on Influence Functions. John Wiley and Sons, Inc., 1986.

- [12] S. Kullback and R. A. Leibler. On information and sufficiency. The Annals of Mathematical Statistics, 22(1):79–86, 1951.

- [13] D. Luenberger and Y. Ye. Linear and Nonlinear Programming. Springer, 2008.

- [14] N. Murata, T. Takenouchi, T. Kanamori, and S. Eguchi. Information geometry of -Boost and Bregman divergence. Neural Computation, 16(7):1437–1481, 2004.

- [15] J. Nocedal and S. Wright. Numerical Optimization. Springer, 1999.

- [16] J. Nocedal and Y.-X. Yuan. Analysis of a self-scaling quasi-newton method. Math. Program., 61:19–37, 1993.

- [17] A. Ohara and S. Eguchi. Geometry on positive definite matrices and v-potential function. Technical report, ISM Research Memo, 2005.

- [18] S. S. Oren and D. G. Luenberger. Self-scaling variable metric (ssvm) algorithms, part i. criteria and sufficient conditions for scaling a class of algorithms. Management Science, 20:845–862, 1974.

- [19] M. J. D. Powell. How bad are the bfgs and dfp methods when the objective function is quadratic? Math. Prog., 34(1):34–47, 1986.

- [20] N. Yamashita. Sparse quasi-newton updates with positive definite matrix completion. Math. Program., 115(1):1–30, 2008.