The Lambert Way to Gaussianize heavy tailed data with the inverse of Tukey’s h transformation as a special case

I present a parametric, bijective transformation to generate heavy tail versions of arbitrary RVs . The tail behavior of the so-called heavy tail Lambert W RV depends on a tail parameter : for , , for has heavier tails than . For being Gaussian, this meta-family of heavy-tailed distributions reduces to Tukey’s distribution. Lambert’s function provides an explicit inverse transformation, which can be estimated by maximum likelihood. This inverse can remove heavy tails from data, and also provide analytical expressions for the cumulative distribution (cdf) and probability density function (pdf). As a special case, these yield explicit formulas for Tukey’s pdf and cdf - to the author’s knowledge for the first time in the literature. Simulations and applications to S&P 500 log-returns and solar flares data demonstrate the usefulness of the introduced methodology.

1 Introduction

Statistical theory and practice are both tightly linked to Gaussianity. In theory, many methods require Gaussian data or noise: i) regression often assumes Gaussian errors; ii) pattern recognition for images often model noise as a Gaussian random field (Achim et al., 2003); iii) many time series models are based on Gaussian white noise (Brockwell and Davis, 1998; Engle, 1982; Granger and Joyeux, 2001).

In all these cases, a model , parameter estimates and their standard errors, and other properties, are then studied – all based on the ideal(istic) assumption of Gaussianity.

In practice, however, data/noise often exhibits asymmetry and heavy tails; for example wind speed data (Field, 2004), human dynamics

(Vázquez et al., 2006), or Internet traffic data (Gidlund and Debernardi, 2009) – just to a name few. Particularly notable examples are financial data (Cont, 2001; Kim and White, 2003) and speech signals (Aysal and Barner, 2006), which almost exclusively exhibit heavy tails. Thus a model developed for the Gaussian case does not necessarily provide accurate inference anymore.

One way to overcome this shortcoming is to replace with a new model , where is a heavy tail distribution: i) regression with Cauchy errors (Smith, 1973); ii) image denoising for -stable noise (Achim et al., 2003); iii) forecasting long memory processes with heavy tail innovations (Ilow, 2000; Palma and Zevallos, 2011), or ARMA modeling of electricity loads with hyperbolic noise (Nowicka-Zagrajek and Weron, 2002).

While such fundamental approaches are attractive from a theoretical perspective, they can become unsatisfactory from a practical viewpoint. Many successful statistical models assume Gaussianity, their theory is very well understood, and many algorithms are implemented for the simple – and often much faster – Gaussian case. Thus developing models based on an entirely unrelated distribution is like throwing out the (Gaussian) baby with the bathwater.

It would be very useful to transform a Gaussian RV to a heavy-tailed RV and vice versa, and thus rely on knowledge - and software - for the well-understood Gaussian case, while still capturing heavy tails in the data. Optimally such a transformation should: a) be bijective; b) include Normality as a special case for hypothesis testing; and c) be parametric so the optimal transformation can be estimated efficiently.

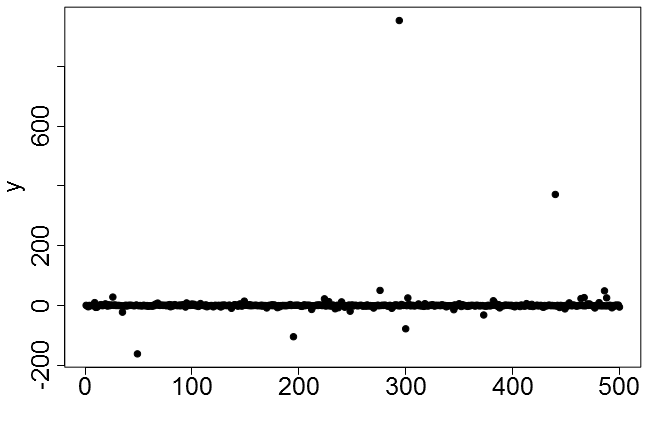

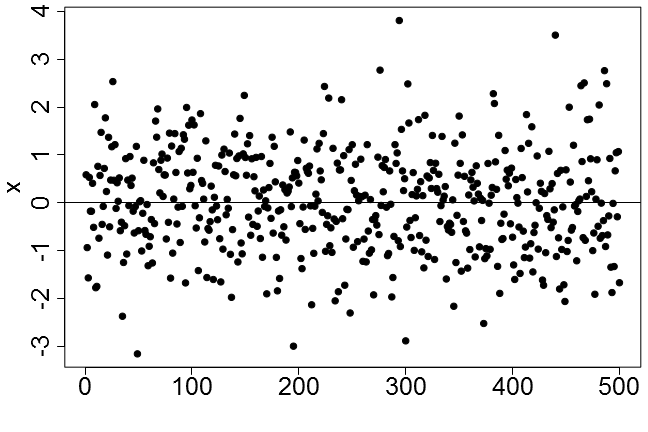

Figure 1 illustrates this pragmatic approach: researchers can make their observations as Gaussian as possible () before making inference based on their favorite Gaussian model . This avoids the development of - or the data analysts waiting for - a whole new theory of and new implementations based on a particular heavy-tailed distribution , while still improving statistical inference on heavy-tailed data . For example, consider from a standard Cauchy distribution in Fig. 2a: modeling heavy tails by a transformation makes it even possible to Gaussianize this Cauchy sample (Fig. 2c). This “nice” data can then be subsequently analyzed with common techniques. For example, the location can now be estimated using the sample average (Fig. 2d). For details see Section 6.1.

Liu

et al. (2009) use a semi-parametric approach, where has a nonparanormal distribution if where is an increasing smooth function; they estimate using non-parametric methods. This leads to a greater flexibility in the distribution of , but it suffers from two drawbacks:

i) non-parametric methods have slower convergence rates and thus need large samples, and

ii) for identifiability of , and must hold.

While i) is inherent to non-parametric methods, point ii) requires to have finite mean and variance, which is especially limiting for heavy-tailed data where this condition is often not met. Thus here we use parametric transformations which do not rely on restrictive identifiability conditions and also work well for small sample sizes.

The main contributions of this work are three-fold: a) following Goerg (2011) I introduce a meta-family of heavy tail Lambert W distributions with Tukey’s (Hoaglin, 2006) as a special case; b) I present a bijective transformation to “Gaussianize” heavy-tailed data (Section 2); and c) I also provide simple expressions for the cumulative distribution function (cdf) and probability density function (pdf) - also for Tukey’s –, which can be easily implemented in statistics software (Section 2.4).

To the author’s knowledge analytic expressions for Tukey’s cdf and pdf are presented here (Section 3) for the first time in the literature. Section 4 introduces a methods of moments estimator and studies the maximum likelihood estimator (MLE). Section 5 shows their finite sample properties.

As has been shown in many case studies, Tukey’s distribution (heavy tail Lambert W Gaussian) is useful to model data with unimodal, heavy-tailed densities. Section 6 not only confirms this finding for S&P 500 log-returns, but also demonstrates the benefits of removing heavy tails for exploratory data analysis: Gaussianizing -ray intensity data reveals a bimodal density, which even non-parametric estimators fail to detect if heavy tails are not removed. Finally, we discuss the new methodology and future work in Section 7. All proofs are given in the Supplementary Material, Appendix B.

Computations, figures, and simulations were done in R (R Development Core Team, 2010). The R package LambertW is publicly available on CRAN.

1.1 Multivariate Extensions

While this work focuses on univariate case, multivariate extensions of the presented methods can be defined component-wise – analogously to the multivariate version of Tukey’s distribution (Field and Genton, 2006). While this may not make the transformed RVs jointly Gaussian, it still provides a good starting point for more well-behaved multivariate modeling.

1.2 Box-Cox Transformation to Remove Heavy Tails

A popular method to deal with skewed, high variance data is the Box-Cox transformation

| (1) |

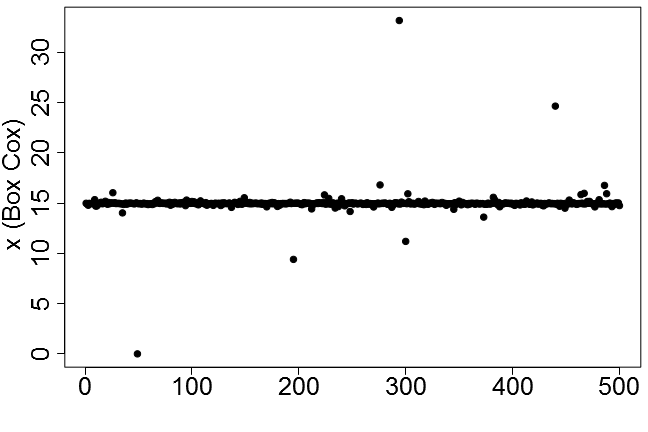

The parameter can be chosen by MLE. However one major limitation of (1) is the non-negativity constraint on , which prohibits its use in many applications. To avoid this limitation it is common to shift the data, . However, as Fig. 2b shows applying the Box-Cox transformation to the Cauchy sample111We use and use boxcox from the MASS R package; . completely fails. Furthermore, this restricts to a half-open interval and is not desirable if the underlying process can occur on the entire real line, since it undermines statistical inference for yet unobserved data. See Sakia (1992) for a more detailed discussion and the Box-Cox transformation in general.

Furthermore, the main purpose of the Box-Cox transformation is to stabilize variance (Blaylock et al., 1980; Lawrance, 1987; Tsiotas, 2007) and remove right tail skewness (Goncalves and Meddahi, 2011); a lower empirical kurtosis is merely a by-result of the variance stabilization. In contrast, the Lambert W framework is designed to model heavy-tailed RVs and remove heavy tails from data, and has no difficulties with negative values.

2 Generating Heavy Tails Using Transformations

Random variables exhibit heavy tails if more mass than for a Gaussian RV lies at the outer end of the density support. A RV has a tail index if its cdf satisfies , where is a slowly varying function at infinity, i.e. for all (Baek and Pipiras, 2010).222There are various similar definitions of heavy/fat/long tails; for this work these differences are not essential. The heavy tail index is an important characteristic of ; for example, only moments up to order exist.

2.1 Tukey’s Distribution

A parametric transformation is the basis of Tukey’s RVs (Hoaglin, 2006)

| (2) |

where is standard Normal RV and is the heavy tail parameter. The RV has tail parameter (Morgenthaler and Tukey, 2000) and reduces to the Gaussian for . Morgenthaler and Tukey (2000) extend the distribution to the skewed, heavy-tailed family of RVs

| (3) |

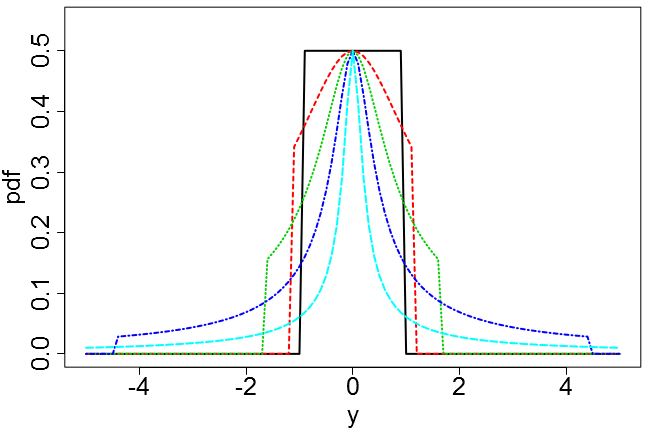

where again . Here and shape the left and right tail of , respectively; thus transformation (3) can model skewed and heavy-tailed data - see Fig. 3a. For simplicity let .

Despite their great flexibility they are not popular in statistical practice, because the inverse of (2) or (3) has not been found. Consequently, no closed-form expressions for the cdf or pdf are available. Although Morgenthaler and Tukey (2000) express the pdf of (2) as ()

| (4) |

they fall short of explicitly specifying . So far this inverse has been considered analytically intractable (Field, 2004), or was only numerically approximated (Headrick

et al., 2008; Fischer, 2010). Thus parameter inference relied on matching empirical and theoretical quantiles (Field, 2004; Morgenthaler and

Tukey, 2000), or by the method of moments (Headrick

et al., 2008). Only recently Headrick

et al. (2008) provided numerical approximations. Hence, a closed form, analytically tractable pdf that can be computed efficiently is essential for a wide-spread use of Tukey’s (& variants).

In this work I present this long sought explicit inverse, which is readily available in standard statistics software. For ease of notation and concision main results are shown for ; analogous results for will be stated without details.

2.2 Heavy Tail Lambert W Random Variables

Tukey’s transformation (2) is strongly related to the approach taken by Goerg (2011) to introduce skewness in continuous RVs . In particular, if Tukey’s , then skewed Lambert W with skew parameter .

Adapting the skew Lambert W input/output idea333Most concepts and methods from the skew Lambert W case transfer one-to-one to the heavy tail Lambert W RVs presented here. Thus for the sake of concision I refer to Goerg (2011) for details and background information on the Lambert W framework. (see Fig. 1), Tukey’s RVs can be generalized to heavy-tailed Lambert W RVs.

Definition 2.1.

Let be a continuous RV with cdf , pdf , and parameter vector . Then,

| (5) |

is a non-central, non-scaled heavy tail Lambert W RV with parameter vector , where is the tail parameter.

Tukey’s distribution results for being a standard Gaussian .

Definition 2.2.

For a continuous location-scale family RV define a location-scale heavy-tailed Lambert W RV

| (6) |

with parameter vector , where .

The input is not necessarily Gaussian but can be any other location-scale continuous RV, e.g., from a uniform distribution: .

Definition 2.3.

Let be a continuous scale-family RV, with standard deviation ; let . Then,

| (7) |

is a scaled heavy-tailed Lambert W RV with parameter .

Let define transformation (6).444For non-central, non-scale input set ; for scale-family input . If , then for all also the location-scale . For a scale family also the scale Lambert W RV .

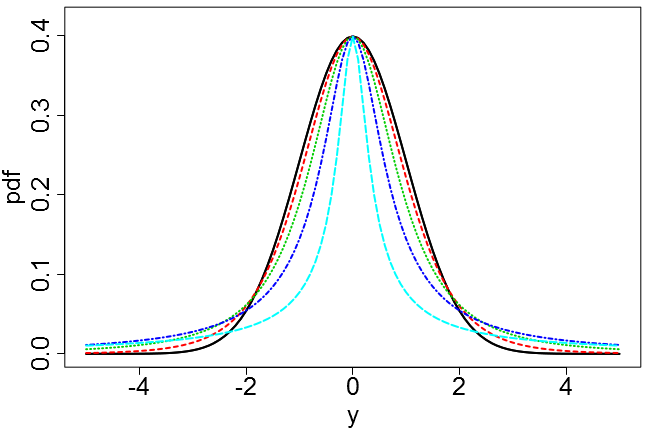

The shape parameter ( Tukey’s ) governs the tail behavior of : for values further away from are increasingly emphasized, leading to a heavy-tailed version of ; for , ; and for values far away from the mean are mapped back again closer to . Thus heavy tail Lambert W RVs generalize to heavy-tailed versions of itself, , with a reduction to for .

The Lambert W formulation of heavy tail modeling is more general than Tukey’s distribution as can have any distribution , not necessarily Gaussian (Fig. 4).

Remark 2.4 (Only non-negative ).

Although leads to interesting properties of , it yields a non-bijective transformation and thus to parameter-dependent support and non-unique input. Thus for the remainder of this work I tacitly assume , unless stated otherwise.

2.3 Inverse Transformation: “Gaussianize” Heavy-Tailed Data

Transformation (6) is bijective and its inverse can be obtained via Lambert’s function, which is the inverse of , i.e., that function which satisfies . Lambert’s has been studied extensively in mathematics, physics, and other areas of science (Rosenlicht, 1969; Corless et al., 1996; Valluri et al., 2000), and is implemented in the GNU Scientific Library (GSL) (Galassi et al., 2011). Only very recently it received attention in the statistics literature (Jodrá, 2009; Rathie and Silva, 2011; Goerg, 2011; Pakes, 2011). It has many useful properties (see Appendix A and Corless et al. (1996)), in particular is bijective for .

Lemma 2.5.

The inverse transformation of (6) is

| (8) |

where

| (9) |

and is the sign of . is bijective for all and all .

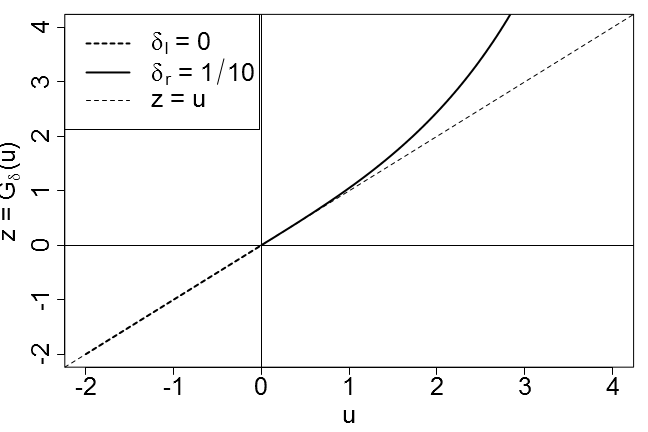

Lemma 2.5 gives for the first time an analytic, bijective inverse of Tukey’s transformation: of Morgenthaler and Tukey (2000) is now analytically available as (8). Bijectivity implies that for any data and parameter , the exact input can be obtained.

In view of the importance and popularity of Gaussianity, we clearly want to back-transform heavy-tailed data to a Gaussian rather than yet another heavy-tailed distribution. Typically tail behavior of RVs are compared by their kurtosis , which for a Gaussian RV equals . Hence for the future when we “normalize ” we can not only subtract the mean, and divide by the standard deviation, but also transform it to with – a “Normalization” in the true sense of the word (see Fig. 2c).

This data-driven view of the Lambert W framework can also be useful for kernel density estimation (KDE), where multivariate data is often pre-scaled to unit-variance, so the same bandwidth can be used in each dimension (Wasserman, 2007; Hwang et al., 1994). Thus “normalizing” the Lambert Way might likely also improve KDE for heavy-tailed data (see also Markovich, 2005; Maiboroda and Markovich, 2004).

Corollary 2.6 (Inverse transformation for Tukey’s ).

The inverse transformation of (3) is

| (10) |

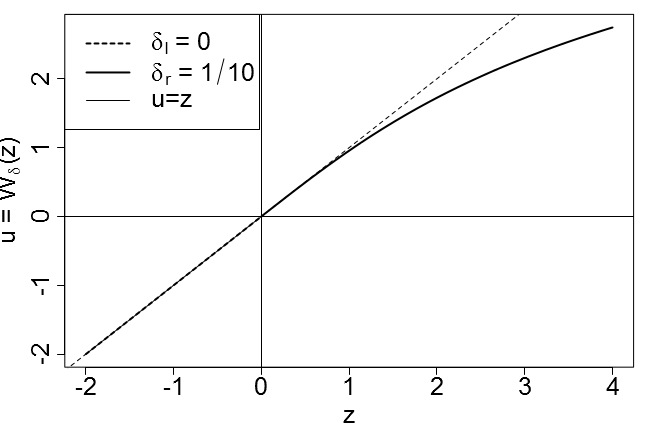

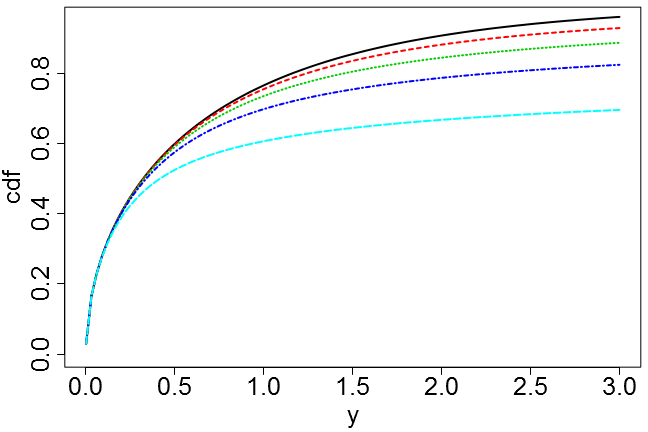

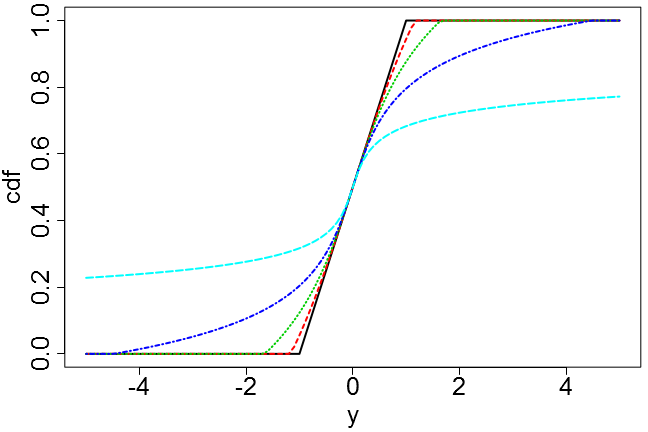

Figure 3b shows for and . The transformation in Fig. 3a generates a right heavy tail version of (x-axis) by stretching only the positive axis (y-axis). By definition removes the heavier right tail in (positive y-axis). Figure 3c shows how operates for various degrees of heavy tails and . If is close to zero, then also ; for larger , the inverse maps to (much) smaller .

2.4 Distribution and Density

For ease of notation let

| (13) |

Theorem 2.8 (Distribution and Density of ).

The cdf and pdf of a location-scale heavy tail Lambert W RV equal

| (14) |

and

| (15) |

Clearly, and , since and for all .

For scale family or non-central, non-scale input set or .

The explicit formula (15) allows a fast computation and theoretical analysis of the likelihood, which is essential for – either frequentist or Bayesian – statistical inference. Detailed properties of (15) are given in Section 4.1.

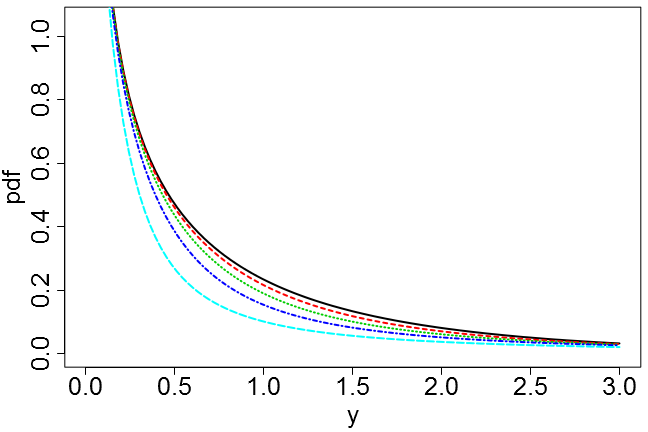

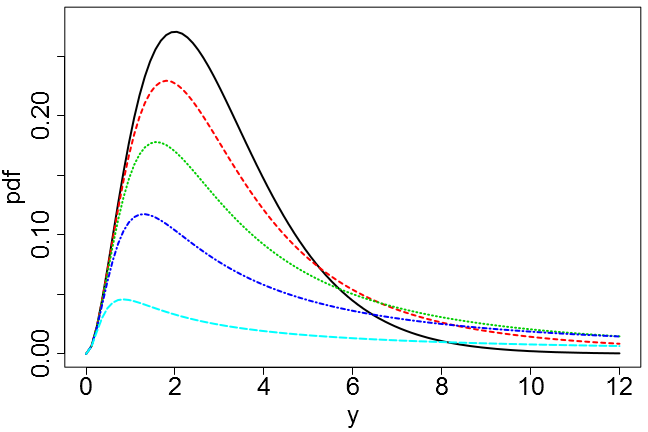

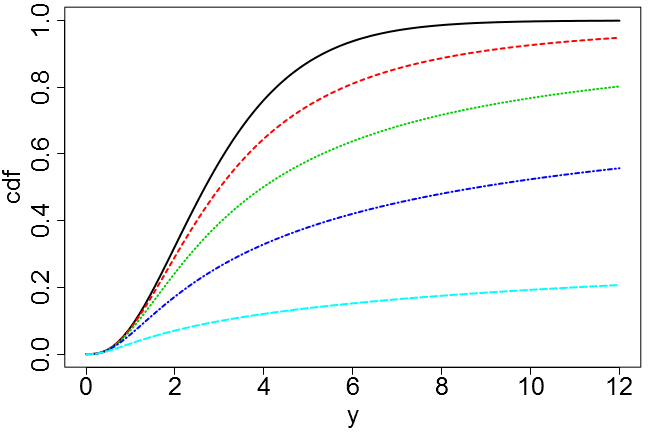

Figure 4 shows (14) and (15) for various with for four different input : for the input equals the output (solid black); for larger the tails of and get heavier (dashed colored).

with .

with .

with .

with .

Corollary 2.9.

2.5 Quantile Function

Quantile fitting has been the standard technique to estimate , , and of Tukey’s . In particular, the median of and are equal. Thus for symmetric, location-scale family input the sample median of is a robust estimate for for any (see also Section 5). General quantiles can be computed via (Hoaglin, 2006)

| (18) |

where are the -quantiles of . As quantiles of are typically tabulated, or easily available in software packages, (18) can be computed very efficiently using and .

This simple conversion can be especially useful for education: teaching heavy-tailed statistics in introductory courses soon becomes too difficult using e.g., Cauchy or -stable distributions. Yet, transforming data via Lambert’s , using previously learned methods for the Gaussian case, and then transforming the inference back to the “heavy-tailed world” – e.g., transforming quantiles using (18) – is straightforward. Thus the Lambert W framework can promote heavy-tailed statistics in introductory courses.

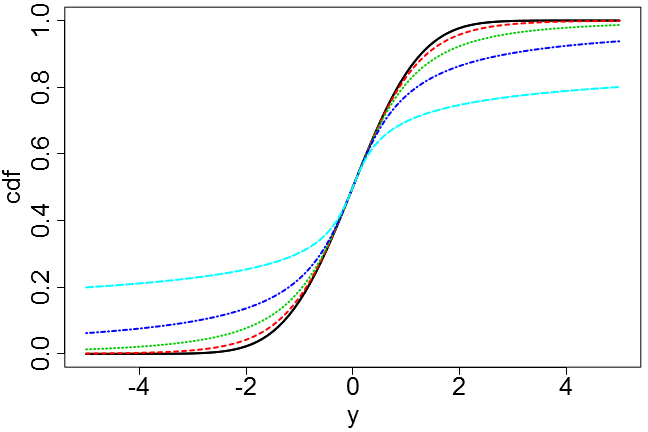

3 Tukey’s h distribution: Gaussian input

For Gaussian input Lambert W equals Tukey’s , which has been studied extensively. Dutta and Babbel (2002) show that

| (19) |

which in particular implies (Headrick et al., 2008)

| (20) | ||||

| (21) |

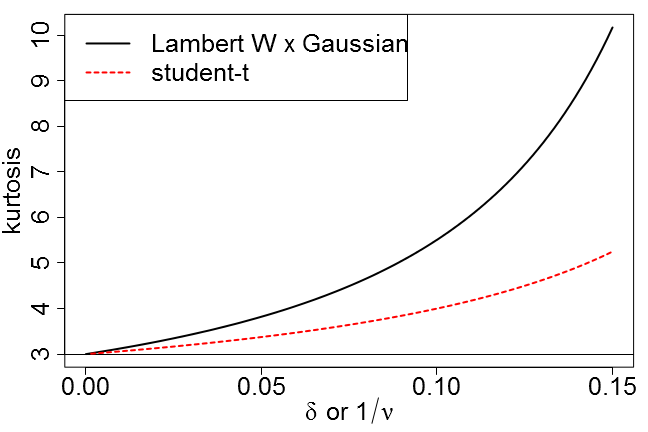

Thus the kurtosis of equals (see Fig. 5)

| (22) |

Corollary 3.1.

The cdf of Tukey’s equals

| (23) |

where is the cdf of a standard Normal. The pdf equals (for )

| (24) |

Proof.

Take in Theorem 2.8. ∎

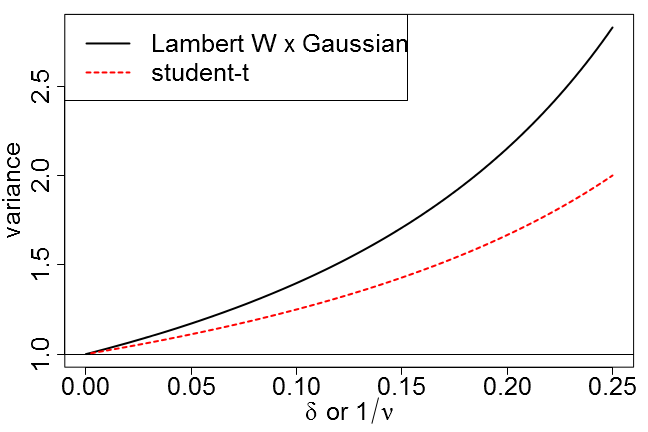

3.1 Tukey’s h versus student’s t

Student’s distribution with degrees of freedom is often used to model heavy-tailed data (Yan, 2005; Wong et al., 2009), as its tail index equals . Thus the th moment of a student t RV exists if . In particular,

| (25) |

and kurtosis

| (26) |

Comparing (26) and (21) with (22) and (25) shows a natural association between and and a close similarity between the first four moments of student’s and Tukey’s (Fig. 5). By continuity and monotonicity, the first four moments of a location-scale distribution can always be exactly matched by a corresponding location-scale Lambert W Gaussian. Thus if student’s is used to model heavy tails, and not as the true distribution of a test statistic, it might be worthwhile to also fit heavy tail Lambert W Gaussian distributions for an equally valuable “second opinion”. For example, a parallel analysis on S&P 500 -returns in Section 6.2 leads to divergent inference regarding the existence of fourth moments. Additionally, the Lambert W approach allows to Gaussianize and thus reveal hidden patterns in the data; patterns that can be easily overseen in presence of heavy tails (Section 6.3).

4 Parameter Estimation

For a sample of independent identically distributed (i.i.d.) observations from transformation (6), has to be estimated from the data. Due to the lack of a closed form pdf of , this has been typically done by matching quantiles or a method of moments estimator (Field, 2004; Morgenthaler and Tukey, 2000; Headrick et al., 2008). These inefficient methods can now be replaced by the – fast and usually efficient – maximum likelihood estimator (MLE) using the pdf in (15). Rayner and MacGillivray (2002) introduce a numerical MLE procedure based on quantile functions, but they conclude that “sample sizes significantly larger than should be used to obtain reliable estimates through maximum likelihood”. Simulations in Section 5 show that log-likelihood maximization with the Lambert W methodology converges quickly and is accurate even for sample sizes as small as .

4.1 Maximum Likelihood Estimation (MLE)

For an i.i.d. sample the log-likelihood function equals

| (27) |

The MLE is that which maximizes (27), i.e.

| (28) |

Since is a function of , the MLE depends on the specification of the input density. Eq. (27) can be decomposed as

| (29) |

where

| (30) |

is the log-likelihood of the back-transformed data and

| (31) |

where

| (32) |

Note that only depends on and (and ), but not necessarily on every coordinate of .

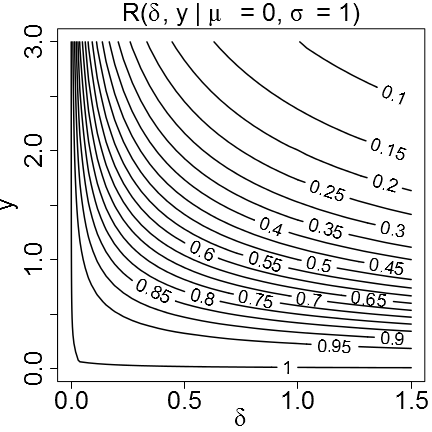

Decomposition (29) shows the difference between the exact MLE based on and the approximate MLE based on alone: if we knew beforehand, then we could back-transform to and estimate from (maximize (30) with respect to ). In practice, however, must also be estimated and this enters the likelihood via the additive term . A little calculation shows that for any , if , with equality if and only if . Thus can be interpreted as a penalty for transforming the data. Maximizing (29) faces a trade-off between transforming the data to follow (and thus increasing ) versus the penalty of a more extreme transformation (and thus decreasing ) – see Fig. 6b.

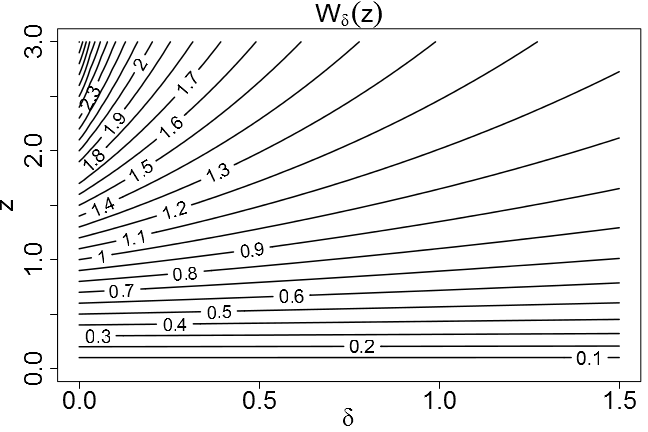

Figure 6a shows a contour plot of as a function of and . The penalty for transforming the data increases (in absolute value) either if gets larger (for fixed ) or for larger (for fixed ). In both cases, increasing makes the transformed data get closer to , which in turn increases its input likelihood. For , the penalty disappears since input equals output; for there is no penalty since for all .

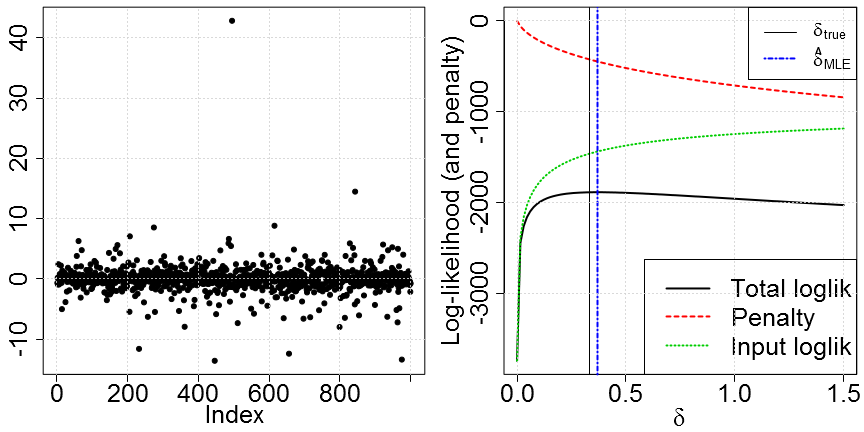

Figure 6b shows a random sample () Lambert W Gaussian with and the decomposition of the log-likelihood as in (29). Since is known, the likelihood and penalty are only functions of . The monotonicity of the penalty (decreasing, red) and the input likelihood (increasing, green) as a function of is not particular to this sample, but holds true in general (see Theorem 4.1 below). This monotonicity in each component implies that their sum (black line) has a unique maximum; here (blue, dashed vertical line).

The maximization of (29) can be carried out numerically. Here I show existence and uniqueness of assuming that and are known. Theoretical results for remain for future work. Given the “nice” form of - continuous, twice differentiable,555Assuming that is twice differentiable. its support does not depend on the parameter, etc. - the MLE for should have the usual optimality properties (Lehmann and Casella, 1998).

4.1.1 Properties of The MLE For The Heavy Tail Parameter

Without loss of generality let and . In this case

| (33) | ||||

| (34) |

Theorem 4.1 (Unique MLE for ).

Let have a Lambert W Gaussian distribution, where and are assumed to be known and fixed. Also consider only the case .666While for some samples the MLE also exists for , it can not be guaranteed for all . If (and ), then is either not unique in (principal and non-principal branch) or may not even have a real-valued solution.

-

a)

If

(35) then .

If (35) does not hold, then

-

b)

exists and is a positive solution to

(36) -

c)

There is only one such satisfying (36), i.e. is unique.

Condition (35) says that only if the data is heavy-tailed enough. Points b) and c) guarantee that there is no ambiguity in the heavy tail estimate. This is an advantage over student’s distribution, for example, which has numerical problems and local maxima for unknown (and small) ( large ) (see also Fernandez and

Steel, 1999; Liu and

Rubin, 1995). On the contrary, is always a global maximum.

The log-likelihood and its gradient depend on and only via . Given the heavy tails in (for ) one might expect convergence issues for larger (e.g. expected log-likelihood, Fisher information). However, for the true , and close to a standard Gaussian if . Thus the performance of the MLE should not get worse for large as long as the initial estimate is close enough to the truth. Simulations in Section 5 support this conjecture, even for .

4.2 Iterative Generalized Method of Moments (IGMM)

A disadvantage of the MLE is the mandatory a-priori specification of the input distribution. Especially for heavy-tailed data the eye is a bad judgement to choose a particular parametric . It would be useful to directly estimate , without the intermediate step of estimating first (and thus no distributional assumption for the input is necessary).

Goerg (2011) presented an estimator for based on iterative generalized methods of moments (IGMM). The idea of IGMM is to find a such that the back-transformed data has desired properties, e.g., is symmetric or has kurtosis . An estimator for , , and can be constructed completely analogously to the skewed IGMM, with the advantage that the heavy tail transformation is bijective (the skewed transformation is not). Since the algorithm is entirely analogous to the skewed case, details are given in the Supplementary Material, Appendix C.

An advantage of IGMM is that it requires less specific knowledge about the input distribution. Usually, it is also faster than the MLE. Once has been obtained, the back-transformed can be used to check if has characteristics of a known parametric distribution . It must be noted though that testing for a particular distribution are too optimistic as will have “nicer” properties regarding than the true would have. However, estimating the transformation requires only three parameters and for a large enough sample, losing three degrees of freedom should not matter for all practical purposes.

5 Simulations

This section explores finite sample properties of estimators for and under Gaussian input . In particular, it compares Gaussian MLE (estimation of and only), IGMM and Lambert W Gaussian MLE, and - for a heavy tail competitor – the median.777For IGMM, optimization was restricted to . All results below are based on replications.

5.1 Estimating Only

Here I show finite sample properties of for , where and are known and fixed. Theorem 4.1 shows that is unique: either at the boundary or at the globally optimal solution to (36). Results in Table 1 were obtained by numerical optimization restricted to () using the nlm function in R.

N 10 50 100 400 1000 2000 N 10 50 100 400 1000 2000

Table 1 shows that the MLE is unbiased for every and settles down (about ) to an asymptotic variance, which is increasing with . Assuming and to be known is unrealistic and thus these finite sample properties are only an indication of the behavior of the joint MLE, . Nevertheless they are very remarkable for extremely heavy-tailed data (), where standard statistical methods typically break down. One explanation in this behavior lies in the particular form of the likelihood (33) and its gradient (36) (Theorem 4.1). Although both depend on , they only do so through . Hence as long as is sufficiently close to the true , (33) and (36) are functions of almost Gaussian RVs and standard asymptotic results should still apply.

5.2 Estimating All Parameters Jointly

Here we consider the realistic scenario where and are also unknown. We consider various sample sizes (, , and ) and different degrees of heavy tails, , each one representing a particularly interesting situation: i) Gaussian data (does additional - superfluous - estimation of affect other estimates?), ii) fourth moments do not exist anymore, iii) non-existing mean, iv) extremely heavy-tailed data – can we get useful estimates at all?

| median | Gaussian MLE | IGMM | Lambert W MLE | NA | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | ratio | |||||||||||

| median | Gaussian MLE | IGMM | Lambert W MLE | NA | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | ratio | |||||||||||

| median | Gaussian MLE | IGMM | Lambert W MLE | NA | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | ratio | |||||||||||

| 50 | ||||||||||||

| 100 | ||||||||||||

| 1000 | ||||||||||||

| 50 | ||||||||||||

| 100 | ||||||||||||

| 1000 | ||||||||||||

| 50 | ||||||||||||

| 100 | ||||||||||||

| 1000 | ||||||||||||

| median | Gaussian MLE | IGMM | Lambert W MLE | NA | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | ratio | |||||||||||

| 50 | ||||||||||||

| 100 | ||||||||||||

| 1000 | ||||||||||||

| 50 | ||||||||||||

| 100 | ||||||||||||

| 1000 | ||||||||||||

| 50 | ||||||||||||

| 100 | ||||||||||||

| 1000 | ||||||||||||

The convergence tolerance for IGMM was set to . Table 5 summarizes the simulation. Each sub-table is organized as follows: columns represent parameter estimates; the three main rows are the average over replications (top), the proportion of estimates below the true value (middle), and the empirical standard deviation around the empirical average times – not around the truth (bottom).

The Gaussian MLE estimates directly, while IGMM and the Lambert W Gaussian MLE estimates and , which implicitly give through if (see (21)). For a fair comparison each sub-table also includes a column for . Some of these entries contain “”, even for ; this occurs if at least one .

For any , , thus they can be directly compared. For , the mean does not exist; each sub-table for these interprets as the median.

Gaussian data:

This setting checks if imposing the Lambert W framework, even though its use is superfluous, causes a quality loss in the estimation of or . Furthermore, critical values for (Gaussian tails) can be obtained. Table 2a shows that all estimators are unbiased and quickly tend to a large-sample variance. Additional estimation of does not affect the efficiency of compared to estimating solely (both for IGMM and Lambert W Gaussian MLE). Estimating directly by Gaussian MLE does not give better results than the Lambert W Gaussian MLE: both are unbiased and have similar standard deviation.

No fourth moment:

Here , but fourth moments do not exist anymore. This results in an increasing empirical standard deviation of as grows. In contrast, estimates for are not drifting off. In presence of these large heavy tails the median is much less variable than Gaussian MLE and IGMM. Yet, Lambert W Gaussian MLE for even outperforms the median.

Non-existing mean:

Here the mean is non-finite. Thus both sample moments diverge, and their standard errors are also growing quickly. The median still provides a very good estimate for the location, but is again inferior to both Lambert W estimators, which are unbiased and seem to converge to an asymptotic variance at rate .

Extreme heavy tails:

As in Section 5.1, IGMM and Lambert W MLE continue to be unbiased even though the data is extremely heavy-tailed. Moreover, Lambert W MLE also has the smallest empirical standard deviation overall. In particular, the Lambert W MLE for has an approximately lower standard deviation than the median.

The last column shows that for some about of the simulations generated invalid likelihood values (NA and ). Here the search for the optimal lead into regions with a numerical overflow in the evaluation of . For a comparable summary, these few cases were omitted and new simulations added until a full finite estimates were found. Since this only happened in of the cases and also such heavy-tailed data is rarely encountered in practice, this numerical issue is not a real limitation in statistical practice.

5.3 Discussion of the Simulations

This simulation study confirms well-known facts about the sample average, standard deviation, and median and compares them to finite sample properties of the two Lambert W estimators. The median is known to be robust, which shows here as its quality does not depend on the thickness of the tails.

IGMM is unbiased for independent of the magnitude of . As expected the Lambert W MLE for has the best properties: it is unbiased for all , and for it performs as well as the classic sample mean and standard deviation. For small it has the same empirical standard deviation as the Gaussian MLE, but a lower one than the median for large .

Hence the only advantage of estimating and by sample moments of is speed; otherwise the Lambert W Gaussian MLE is at least as good as the Gaussian MLE and clearly outperforms it for heavy-tailed data.

6 Applications

Tukey’s distribution has already proven useful to model heavy-tailed data, but parametric inference was limited to quantile fitting or methods of moments estimation (Headrick et al., 2008; Fischer, 2010; Field, 2004). Theorem 2.8 allows us to estimate by ML.

This section shows the usefulness of the presented methodology on simulated as well as real world data: i) Section 6.1 demonstrates Gaussianizing on the Cauchy sample from the Introduction; ii) Section 6.2 shows that heavy tail Lambert W Gaussian distributions provide an excellent fit to daily S&P 500 log-return series; and iii) Section 6.3 shows how removing heavy tails reveals hidden patterns in power-law type data.

6.1 Estimating Location of a Cauchy With The Sample Mean

It is well-known that the sample mean is a poor estimate of the location parameter of a Cauchy distribution, since the sampling distribution of is again a Cauchy; in particular, its variance does not go to for .

Heavy-tailed Lambert W Gaussian distributions have similar properties to a Cauchy for . The mean of equals the location of , due to symmetry around (for all ) and , respectively. Thus we can estimate from the Cauchy sample , transform to , estimate from , and thus obtain an estimate of .

The data in Fig. 2a has heavy tails with two extreme (positive) samples. A Cauchy ML fit gives and (standard errors in parenthesis). A Lambert W Gaussian MLE gives , , and . Thus both fits correctly fail to reject . Table 3a shows summary statistics on both samples. Since the Cauchy distribution does not have a well-defined mean, is not meaningful. However, is approximately Gaussian and we use the sample average to do inference: correctly fails to reject a zero location for . The transformed features additional Gaussian characteristics (symmetric, no excess kurtosis), and even the null hypothesis of Normality cannot be rejected (p-value ).

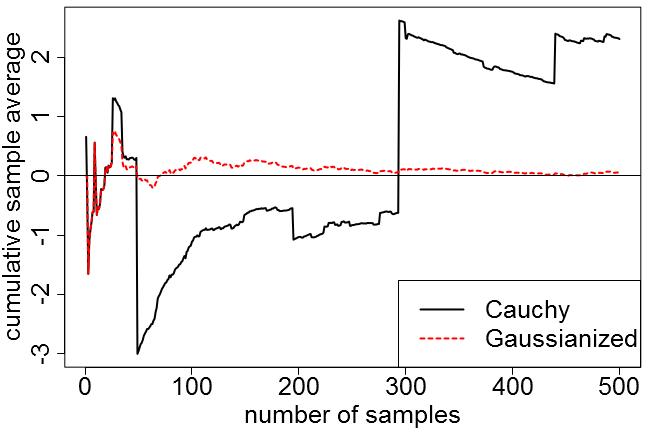

Figure 2d shows the running sample average for the original sample and its Gaussianized version. For a fair comparison was re-estimated cumulatively for each , and then used to compute . Even for small the transformation works extremely well: the highly influential point around greatly affects , but has no relevant effect on . Overall, the sample average of the Gaussianized data has the usual good properties. And even for very small it is already clear that the location of the underlying Cauchy distribution is approximately zero.

Although a toy example, it shows that removing (strong) heavy tails from data works and provides new, “nice” data which can then be used for more refined methods.

Min Max Mean Median Stdev Skewness Kurtosis SW AD

-161.59 -3.16 0 952.95 3.81 33.18 2.30 0.03 14.98 0.04 0.04 14.96 46.980 1.06 1.20 17.43 0.12 3.90 343.34 3.21 161.75 0.71 0.51

(Section 6.1)

-7.11 -2.42 4.99 2.23 0.05 0.05 0.04 0.04 0.95 0.71 -0.30 -0.04 7.70 2.93 0.24 0.18

(Section 6.2)

20 20 231300 157 689.4 89.0 87 87 6520.6 27.0 22.2 0.1 582.1 1.9

(Section 6.3)

6.2 Heavy Tails in Finance: S&P 500 Case Study

A lot of financial data displays negative skewness and excess kurtosis. Since financial data is in general not i.i.d., it is often modeled with a (skew) student-t distribution underlying a (generalized) auto-regressive conditional heteroskedastic (GARCH) (Engle, 1982; Bollerslev, 1986) or a stochastic volatility (SV) model (Melino and Turnbull, 1990; Deo et al., 2006). Using the Lambert W approach we can build upon the knowledge and implications of Gaussianity (and avoid deriving properties of a GARCH or SV model with heavy-tailed innovations), and simply “Gaussianize” the reutns before fitting more complex – GARCH or SV – models.

Remark 6.1.

Time series models with Lambert W Gaussian white noise are far beyond the scope of this work, but can be a direction of future research. Here I only consider the unconditional distribution.

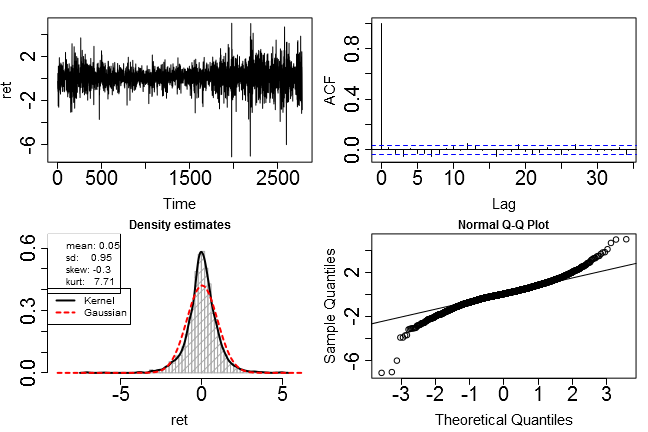

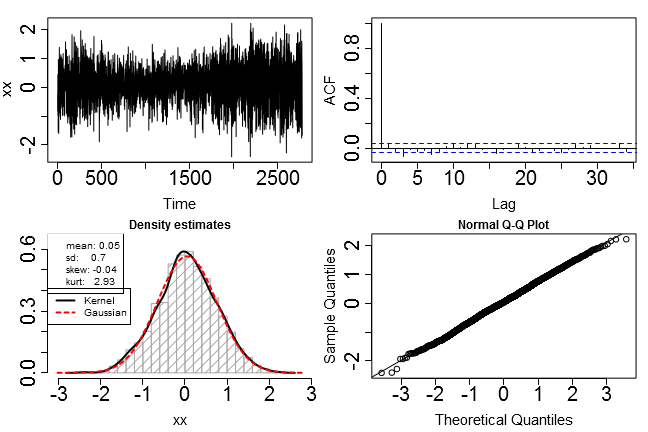

Figure 7a shows the S&P 500 log-returns with a total of daily observations.888R package MASS, dataset SP500. Table 3b confirms the heavy tails (sample kurtosis ), but also indicates negative skewness (). As the sample skewness is very sensitive to outliers, we should test for symmetry by fitting a skewed distribution and testing its skewness parameter(s) for zero. In case of the double-tail Lambert W Gaussian this means to test versus . Since the likelihood can now be computed by (29), we can use a likelihood ratio test with one degree of freedom ( versus parameters). The log-likelihood of the double-tail Lambert W Gaussian fit (Table 4a) equals (input + penalty), while the one fit gives . Here the double tails pay a lower penalty for transforming the data, but in turn give less Gaussian transformed sample. Comparing twice their difference to a distribution gives a p-value of . For comparison, a skew-t fit (Azzalini and

Capitanio, 2003), with location , scale , shape , and degrees of freedom also yields 999Function st.mle in the R package sn. a non-significant (Table 4b). Thus both fits cannot reject symmetry.

Assume we have to make a decision if we should trade a certificate replicating the S&P 500. Since we can either buy or sell, it is not important if the average return is positive or negative, as long as it is significantly different from zero.

6.2.1 Gaussian Fit to Returns

If we ignore heavy tails and estimate by Gaussian MLE, can not be rejected on a level (Table 4e). However, a plain sample average over-estimates the variance in presence of heavy tails, and thus adds bias to the test statistic.

6.2.2 Heavy Tail Fit to Returns

Both a heavy tail Lambert W Gaussian (Table 4c) and student- fit (Table 4d) reject the zero mean null (p-values, and , respectively). The standard errors for the location parameter are essentially the same.

While location and scale estimates are almost identical, the tail estimates lead to very different conclusions: while for only moments up to order exist, in the Lambert W Gaussian case moments up to order exist (). This is especially noteworthy as many theoretical results in the (financial) time series literature rely on finite fourth moments (Zadrozny, 2005; Mantegna and Stanley, 1998); consequently many empirical studies test if financial data actually satisfy this assumption (Cont, 2001; Huisman et al., 2001). For this particular dataset student’s and a Lambert W Gaussian fit give different answers to the same question. Since previous empirical studies often use student’s as a baseline (Wong et al., 2009), it might be worthwhile to re-examine their findings in light of heavy tail Lambert W Gaussian distributions.

| Est. | se | t | Pr() | |

|---|---|---|---|---|

| 0.06 | 0.015 | 3.66 | 0.00 | |

| 0.71 | 0.016 | 44.00 | 0.00 | |

| 0.19 | 0.021 | 8.99 | 0.00 | |

| 0.16 | 0.019 | 8.24 | 0.00 |

| Est. | se | t | Pr() | |

|---|---|---|---|---|

| 0.10 | 0.061 | 1.65 | 0.10 | |

| 0.67 | 0.017 | 38.47 | 0.00 | |

| -0.08 | 0.101 | -0.77 | 0.44 | |

| 3.73 | 0.297 | 12.57 | 0.00 |

| Est. | se | t | Pr() | |

|---|---|---|---|---|

| 0.06 | 0.015 | 3.65 | 0.000 | |

| 0.71 | 0.016 | 43.95 | 0.000 | |

| 0.17 | 0.016 | 11.05 | 0.000 |

| Est. | se | t | Pr() | |

|---|---|---|---|---|

| 0.06 | 0.015 | 3.65 | 0.00 | |

| 0.67 | 0.017 | 39.51 | 0.00 | |

| 3.72 | 0.295 | 12.61 | 0.00 |

| Est. | se | t | Pr() | |

|---|---|---|---|---|

| 0.05 | 0.018 | 2.55 | 0.01 | |

| 0.95 | 0.013 | 74.57 | 0.00 |

| Est. | se | t | Pr() | |

|---|---|---|---|---|

| 0.05 | 0.013 | 3.81 | 0.00 | |

| 0.71 | 0.009 | 74.57 | 0.00 |

6.2.3 “Gaussianizing” Returns

A typical parameter inference study would conclude here. Using Lambert’s W function we can analyze the back-transformed to test if a Lambert W Gaussian distribution is indeed appropriate. Figure 7b shows that is indistinguishable from a Gaussian sample. Not even one Normality test can reject Gaussianity: p-values are , , , and , respectively (Anderson Darling, Cramer-von-Mises, Shapiro-Francia, Shapiro-Wilk; see Thode (2002)). Table 3b also shows that Lambert W “Gaussianiziation” was successful: and are within the typical variation for a Gaussian sample. Thus

| (37) |

is an adequate (unconditional) Lambert W Gaussian model for the S&P 500 log-returns . For trading, this means that the expected return is significantly larger than zero (), and thus replicating certificates should be bought.

6.2.4 Gaussian MLE for Gaussianized Data

For , also . We can therefore replace testing versus for a non-Gaussian , with the very well understood hypothesis test versus for the Gaussian . In particular, standard errors based on - and thus t and p-values - should be closer to the “truth” (Table 4c and 4d) than a Gaussian MLE on the non-Gaussian (Table 4e). Table 4f shows that standard errors for are even a bit too small compared to the heavy-tailed versions. Since the “Gaussianizing” transformation was estimated, treating as if it was original data is too optimistic regarding its Gaussianity (recall the penalty (31) in the total likelihood (29)).

This example confirms that if a model and its theoretical properties are based on Gaussianity, but the observed data is heavy-tailed, then Gaussianizing the data first gives more reliable inference than applying the Gaussian methods to the original, heavy-tailed data (Fig. 1). Clearly, a joint estimation of the model parameters based on Lambert W Gaussian errors (or any other heavy-tailed distribution) would be optimal. However, theoretical properties and estimation techniques may not have been developed and implemented yet, or are simply not known to researchers who are non-experts in heavy-tailed statistics. The Lambert Way to Gaussianize data thus is a pragmatic method to improve statistical inference on heavy-tailed data, while preserving the ease of usage and interpretation of Gaussian models.

6.3 Removing Power Law From Solar Flare Counts

The previous section focused on Lambert W distributions as a “true” model for the data . Here I consider it merely as a data transformation to remove heavy tails. In the same way as scaling to zero-mean, unit-variance data, , does not necessarily mean we believe the underlying process is Gaussian, we can also convert to without assuming that is actually Lambert W Gaussian. While might lose the interpretability of the observed data (e.g. units become distorted), it can be helpful for exploratory data analysis (EDA), as the eye is a bad judgment to detect regularities corrupted by heavy tails. Removing them can reveal hidden patterns and thus greatly improve the accuracy of statistical inference for .

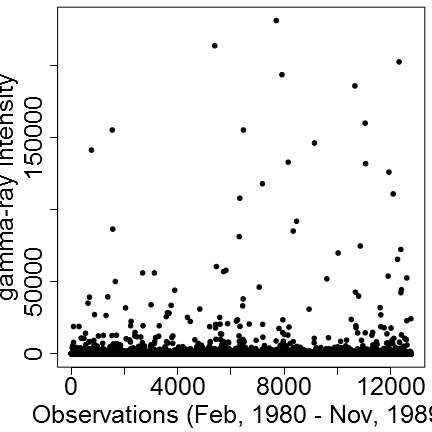

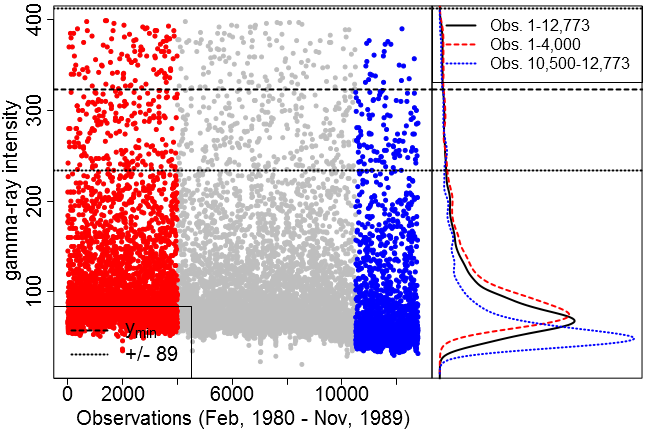

Here I study solar flare gamma-ray count rates (Clauset

et al., 2009; Newman, 2005). The data101010Dataset SolarFlares in the LambertW package. were collected approximately four times a day from Feb. 1980 until Nov. 1989 giving observations. See Dennis

et al. (1991) for details and scientific background.

The gamma-ray count rates exhibit a strong right heavy tail (Fig. 8a), which makes more detailed visual inspection as well as simple EDA difficult. A zoom to in Fig. 8d shows that a lot of counts lie between and and this level drops off at the end of the observation cycle. This drop is not an intrinsic characteristic of solar flares but due to a decreasing sensitivity of the X-ray detectors over time (Dennis

et al., 1991). For the sake of comparison with Clauset

et al. (2009); Newman (2005) most estimates are based on all observations. Figures 8d, 8e, and 8f also show separate density estimates for the first and last observations, and while the estimates change, the qualitative findings do not.

Clauset et al. (2009) find that a power-law () with cut-off () gives the best fit amongst various alternatives. However, this first EDA might not be complete: not only visually heavy tails can obscure underlying non-trivial structure, but also estimates - such as the power law fit or non-parametric density estimates (Fig. 8d and 8b) - are affected by the heavy right tail. Here I show that Gaussianizing this data reveals new insights for the data-generating process, with a new interpretation for the optimality of the cut-off.

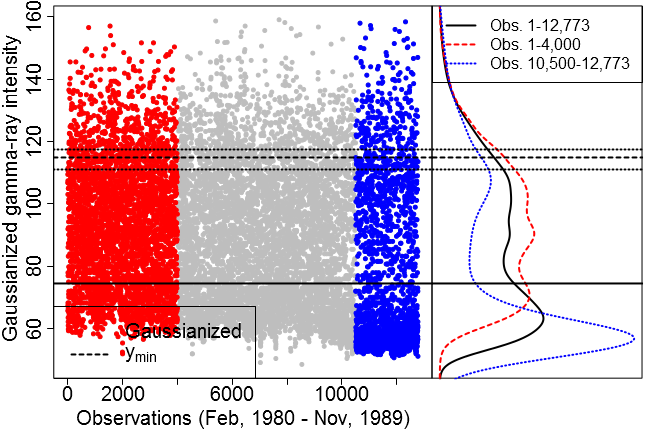

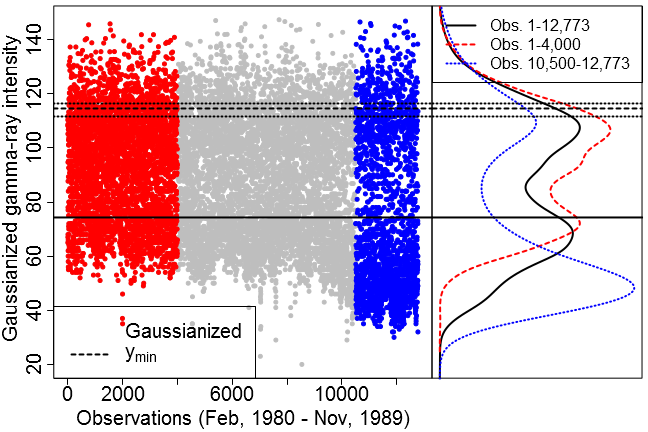

A Lambert W Gaussian MLE fit confirms that only the right tail (tail index ) needs a Gaussianizing transformation.111111For comparison Fig. 8e also shows the back-transformed data using the same on each tail (). However, due to the clear right heavy tail I will continue with the transformation.

The last column of Fig. 8 shows EDA for the Gaussianized data. Removing the heavy right tail reveals a bimodal structure, which gives additional meaning to . The Gaussianized cut-off value equals with the transformed standard deviation interval (corresponding to ). Fitting a two component Gaussian mixture model to yields with and optimal decision boundary between classes of . The mean of the larger component, , lies within one standard deviation of the optimal Gaussianized cut-off : for lower cut-offs the left-tail of the larger component – or for much lower cut-offs even the smaller component – would counteract the power-law decay of the upper gamma-ray count rates.

As mentioned above, this analysis is not intended to describe the underlying process of solar flare gamma rays; it should rather show new insights that can be gained by Gaussianizing. Future research based on these new findings might lead to new physical interpretations of the statistical properties gamma-ray count rates, see for example Aschwanden (2011).

7 Discussion and Outlook

I adapt the skewed Lambert W input / output framework to introduce heavy tails in continuous RVs . For Gaussian input this not only contributes to existing work on Tukey’s distribution, but also gives convincing empirical results: unimodal data with heavy tails can be transformed to Gaussian data/RVs. Properties of a Gaussian model on the back-transformed data mimic the features of the “true” skewed, heavy-tailed model very closely.

Since Gaussianity is the single most typical, and often required, assumption in many areas of statistics, machine learning, and signal processing, future research can take many directions. From a theoretical perspective properties of Lambert W distributions viewed as a generalization of already well-known distributions can be studied. This area will profit from existing literature on the Lambert W function, which has been discovered only recently by the statistics community. Empirical work can focus on transforming the data and compare performances of approximate Gaussian versus joint heavy-tail analysis. The comparisons in this work showed that approximate inference for Gaussianized data is comparable with the direct heavy tail modeling, and so provides an easy tool to improve inference for heavy-tailed data in statistical practice.

I also provide the R package LambertW, publicly available at CRAN, to facilitate the use of Lambert W distributions in practice.

Acknowledgments

I want to thank Andrew F. Siegel who brought Tukey’s distribution to my attention, and Brian R. Dennis who gave detailed background information and suggestions on the solar flares dataset.

References

- Achim et al. (2003) Achim, A., P. Tsakalides, and A. Bezerianos (2003). SAR image denoising via Bayesian wavelet shrinkage based on heavy-tailed modeling. Geoscience and Remote Sensing, IEEE Transactions on 41(8), 1773 – 1784.

- Aschwanden (2011) Aschwanden, M. J. (2011). The State of Self-Organized Criticality of the Sun During the Last Three Solar Cycles. II. Theoretical Model. Solar Physics 274, 119–129.

- Aysal and Barner (2006) Aysal, T. C. and K. E. Barner (2006). Second-order heavy-tailed distributions and tail analysis. IEEE Transactions on Signal Processing 54(7), 2827–2832.

- Azzalini and Capitanio (2003) Azzalini, A. and A. Capitanio (2003). Distributions generated by perturbation of symmetry with emphasis on a multivariate skew t distribution. Journal of the Royal Statistical Society ser B 65, 367–389.

- Baek and Pipiras (2010) Baek, C. and V. Pipiras (2010). Estimation of parameters in heavy-tailed distribution when its second order tail parameter is known. Journal of Statistical Planning and Inference 140(7), 1957 – 1967.

- Blaylock et al. (1980) Blaylock, J. R., L. E. Salathe, and R. D. Green (1980). A note on the Box-Cox transformation under heteroskedasticity. Western Journal of Agricultural Economics 05(02), 129–136.

- Bollerslev (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31, 307 – 327.

- Brockwell and Davis (1998) Brockwell, P. J. and R. A. Davis (1998). Time Series: Theory and Methods. Springer Series in Statistics.

- Clauset et al. (2009) Clauset, A., C. R. Shalizi, and M. E. J. Newman (2009). Power-law distributions in empirical data. SIAM Review 51, 661–703.

- Cont (2001) Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance 1, 223–236.

- Corless et al. (1996) Corless, R. M., G. H. Gonnet, D. E. G. Hare, and D. J. Jeffrey (1996). On the Lambert W function. Advances in Computational Mathematics 5, 329–359.

- Dennis et al. (1991) Dennis, B. R., L. E. Orwig, G. S. Kennard, G. J. Labow, R. A. Schwartz, A. R. Shaver, and A. K. Tolbert (1991). The complete Hard X Ray Burst Spectrometer event list, 1980-1989. Available http://adsabs.harvard.edu/abs/1991chxb.book.....D and http://umbra.nascom.nasa.gov/smm/hxrbs.html.

- Deo et al. (2006) Deo, R., C. Hurvich, and Y. Lu (2006). Forecasting Realized Volatility Using a Long Memory Stochastic VolatilityModel: Estimation, Prediction and Seasonal Adjustment. Journal of Econometrics 127, 29 – 58.

- Dutta and Babbel (2002) Dutta, K. K. and D. Babbel (2002). On Measuring Skewness and Kurtosis in Short Rate Distributions: The Case of the US Dollar London Inter Bank Offer Rates. Technical report, Wharton School Center for Financial Institutions, University of Pennsylvania.

- Engle (1982) Engle, R. (1982). Autoregressive conditional heteroskedasticity with estimates of the variance of U.K. inflation. Econometrica 50, 987 – 1008.

- Fernandez and Steel (1999) Fernandez, C. and M. F. J. Steel (1999). Multivariate Student-t Regression Models: Pitfalls and Inference. Biometrika 86, 153–167.

- Field and Genton (2006) Field, C. and M. G. Genton (2006). The Multivariate g-and-h Distribution. Technometrics 48(1), 104–111.

- Field (2004) Field, C. A. (2004). Using the gh distribution to model extreme wind speeds. Journal of Statistical Planning and Inference 122(1-2), 15 – 22.

- Fischer (2010) Fischer, M. (2010). Generalized Tukey-type distributions with application to financial and teletraffic data. Statistical Papers 51, 41–56. 10.1007/s00362-007-0114-z.

- Galassi et al. (2011) Galassi, M., J. Davies, J. Theiler, B. Gough, G. Jungman, P. Alken, M. Booth, and F. Rossi (2011). GNU Scientific Library Reference Manual (3rd ed.). ISBN 0954612078; www.gnu.org/software/gsl.

- Gidlund and Debernardi (2009) Gidlund, M. and N. Debernardi (2009). Scheduling performance of heavy-tailed data traffic in wireless high-speed shared channels. In Proceedings of the 2009 IEEE conference on Wireless Communications & Networking Conference, WCNC’09, Piscataway, NJ, USA, pp. 1818–1823. IEEE Press.

- Goerg (2011) Goerg, G. M. (2011). Lambert W Random Variables - A New Family of Generalized Skewed Distributions with Applications to Risk Estimation. The Annals of Applied Statistics 5(3), p. 2197 – 2230. arxiv.org/abs/0912.4554.

- Goncalves and Meddahi (2011) Goncalves, S. and N. Meddahi (2011). Box-Cox transforms for realized volatility. Journal of Econometrics 160(1), 129–144.

- Granger and Joyeux (2001) Granger, C. W. J. and R. Joyeux (2001). An introduction to long-memory time series models and fractional differencing. Journal of Time Series Analysis 1, 15 – 30.

- Headrick et al. (2008) Headrick, T. C., R. K. Kowalchuk, and Y. Sheng (2008). Parametric Probability Densities and Distribution Functions for Tukey g-and-h Transformations and their Use for Fitting Data. Applied Mathematical Sciences 2(9), 449 – 462.

- Hoaglin (2006) Hoaglin, D. C. (2006). Summarizing Shape Numerically: The g-and-h Distributions, pp. 461–513. Hoboken, NJ, USA: John Wiley and Sons, Inc.

- Huisman et al. (2001) Huisman, R., K. G. Koedijk, C. J. M. Kool, and F. Palm (2001). Tail-index estimates in small samples. Journal of Business & Economic Statistics 19(2), 208–16.

- Hwang et al. (1994) Hwang, J., S. Lay, and A. Lippman (1994). Nonparametric multivariate density estimation: A comparative study. IEEE Trans. Signal Processing 42, 2795–2810.

- Ilow (2000) Ilow, J. (2000). Forecasting network traffic using farima models with heavy tailed innovations. Acoustics, Speech, and Signal Processing, IEEE International Conference on 6, 3814–3817.

- Jodrá (2009) Jodrá, P. (2009). A closed-form expression for the quantile function of the Gompertz-Makeham distribution. Math. Comput. Simul. 79, 3069–3075.

- Kim and White (2003) Kim, T.-H. and H. White (2003). On More Robust Estimation of Skewness and Kurtosis: Simulation and Application to the S&P500 Index.

- Lawrance (1987) Lawrance, A. J. (1987). A note on the variance of the Box-Cox regression transformation estimate. Journal of the Royal Statistical Society. Series C (Applied Statistics) 36(2), 221–223.

- Lehmann and Casella (1998) Lehmann, E. L. and G. Casella (1998). Theory of Point Estimation (2 ed.). Springer Texts in Statistics.

- Liu and Rubin (1995) Liu, C. and D. B. Rubin (1995). ML Estimation of the t distribution using EM and its extensions, ECM and ECME. Statistica Sinica 5, 19–39.

- Liu et al. (2009) Liu, H., J. Lafferty, and L. Wasserman (2009). The Nonparanormal: Semiparametric Estimation of High Dimensional Undirected Graphs. Journal of Machine Learning Research 10, 2295–2328.

- Maiboroda and Markovich (2004) Maiboroda, R. and N. Markovich (2004). Estimation of heavy-tailed probability density function with application to web data. Computational Statistics 19, 569–592. 10.1007/BF02753913.

- Mantegna and Stanley (1998) Mantegna, R. N. and H. E. Stanley (1998). Modeling of financial data: Comparison of the truncated Lévy flight and the ARCH(1) and GARCH(1,1) processes. Physica A: Statistical and Theoretical Physics 254(1-2), 77 – 84.

- Markovich (2005) Markovich, N. M. (2005). Accuracy of transformed kernel density estimates for a heavy-tailed distribution. Autom. Remote Control 66, 217–232.

- Melino and Turnbull (1990) Melino, A. and S. M. Turnbull (1990). Pricing foreign currency options with stochastic volatility. Journal of Econometrics 45(1-2), 239 – 265.

- Morgenthaler and Tukey (2000) Morgenthaler, S. and J. W. Tukey (2000). Fitting quantiles: Doubling, hr, hq, and hhh distributions. Journal of Computational and Graphical Statistics 9(1), pp. 180–195.

- Newman (2005) Newman, M. E. J. (2005). Power laws, Pareto distributions and Zipf’s law. Contemporary Physics 46, 323–351.

- Nowicka-Zagrajek and Weron (2002) Nowicka-Zagrajek, J. and R. Weron (2002). Modeling electricity loads in California: ARMA models with hyperbolic noise. Signal Process. 82, 1903–1915.

- Pakes (2011) Pakes, A. G. (2011). Lambert’s W, infinite divisibility and Poisson mixtures. Journal of Mathematical Analysis and Applications 378, 480 492.

- Palma and Zevallos (2011) Palma, W. and M. Zevallos (2011). Fitting non-gaussian persistent data. Applied Stochastic Models in Business and Industry 27(1), 23–36.

- R Development Core Team (2010) R Development Core Team (2010). R: A Language and Environment for Statistical Computing. Vienna, Austria: R Foundation for Statistical Computing. ISBN 3-900051-07-0.

- Rathie and Silva (2011) Rathie, R. N. and P. Silva (2011). Applications of Lambert W Function. International Journal of Applied Mathematics & Statistics 23(D11), –.

- Rayner and MacGillivray (2002) Rayner, G. D. and H. L. MacGillivray (2002). Numerical maximum likelihood estimation for the g-and-k and generalized g-and-h distributions. Statistics and Computing 12, 57–75.

- Rosenlicht (1969) Rosenlicht, M. (1969). On the explicit solvability of certain transcendental equations. Pub. Math. Institut des Hautes Etudes Scientifiques 36, 15 – 22.

- Sakia (1992) Sakia, R. M. (1992). The Box-Cox transformation technique: A review. Journal of the Royal Statistical Society. Series D (The Statistician) 41(2), 169–178.

- Smith (1973) Smith, V. K. (1973). Least Squares Regression with Cauchy Errors. Oxford Bulletin of Economics and Statistics 35(3), 223–31.

- Thode (2002) Thode, Jr., H. C. (2002). Testing for Normality. CRC Press.

- Tsiotas (2007) Tsiotas, G. (2007). On the use of the Box-Cox transformation on conditional variance models. Finance Research Letters 4(1), 28–32.

- Valluri et al. (2000) Valluri, S. R., D. J. Jeffrey, and R. M. Corless (2000). Some Applications of the Lambert W Function to Physics. Canadian Journal of Physics 78, 823 – 831.

- Vázquez et al. (2006) Vázquez, A., J. G. Oliveira, Z. Dezsö, K.-I. Goh, I. Kondor, and A.-L. Barabási (2006). Modeling bursts and heavy tails in human dynamics. Phys. Rev. E 73(3), 036127.

- Wasserman (2007) Wasserman, L. (2007). All of Nonparametric Statistics. Springer Texts in Statistics.

- Wong et al. (2009) Wong, C. S., W. S. Chan, and P. L. Kam (2009). A Student t-mixture autoregressive model with applications to heavy-tailed financial data. Biometrika 96(3), 751–760.

- Yan (2005) Yan, J. (2005). Asymmetry, fat-tail, and autoregressive conditional density in financial return data with systems of frequency curves. citeseerx.ist.psu.edu/viewdoc/summary?doi=10.1.1.76.2741.

- Zadrozny (2005) Zadrozny, P. A. (2005). Necessary and Sufficient Restrictions for Existence of a Unique Fourth Moment of a Univariate GARCH(p,q) Process, Volume 20 of Advances in Econometrics, Chapter –, pp. 365–379. Emerald Group Publishing Limited. ideas.repec.org/p/ces/ceswps/_1505.html.

Supplementary Material

Appendix A Auxiliary Results and Properties

A.1 Inverse Transformation

The function is the building block of Lambert W distributions. This section lists useful properties of as a function of as well as a function of .

Properties A.1.

For ,

| (38) |

By definition and therefore

| (39) |

Lemma A.2 (Derivative of with respect to ).

It holds

| (40) |

Proof.

One of the many interesting properties of the Lambert W function relates to its derivative which satisfies

| (41) |

Hence,

| (42) |

Therefore,

| (43) | |||||

| (44) | |||||

| (45) |

As the last line simplifies to

| (46) |

Now use again . ∎

Lemma A.3 (Derivative of with respect to ).

For all

| (47) |

Proof.

By definition . Thus

| (48) | ||||

| (49) | ||||

| (50) | ||||

| (51) | ||||

| (52) | ||||

| (53) |

Since both terms are non-negative for all , the result follows. ∎

That is is a decreasing function in for every , i.e. the more we remove heavy tails the more gets shrinked (non-linearly) towards . In particular, and for and .

Lemma A.4 (Derivative of with respect to ).

It holds

| (54) |

Proof.

| (55) | ||||

| (56) | ||||

| (57) | ||||

| (58) |

where the last line follows by Lemma A.3. ∎

A.2 Penalty for Standard Gaussian Input

For and the penalty equals ()

| (59) |

and thus

| (60) | ||||

| (61) |

Lemma A.5 (Derivative of with respect to ).

For all and all

| (62) |

A.3 Gaussian log-Likelihood at

Lemma A.6 (Derivative of the Gaussian log-likelihood at ).

For all and for

| (66) |

Proof.

Appendix B Proofs

B.1 Inverse transformation

B.2 Cdf and pdf

B.3 MLE for

Lemma B.1 (Derivative of the Lambert W Gaussian log-likelihood).

We have

| (77) | ||||

| (78) | ||||

| (79) |

Proof sketch of Theorem 4.1.

-

a)

If condition (35) holds, then at and stays negative for all . Hence the maximizer occurs at the boundary .

-

b)

If (35) does not hold, then , decreases in and crosses the zero line (one candidate for occurs here).

-

c)

As gets larger, reaches a minimum (negative value) and starts increasing. However, for the derivative approaches zero from below and never equals zero again; thus is unique.

∎

Proof of Theorem 4.1.

-

a)

The log-likelihood is increasing at if and only if (set in (79) and use Property A.1)

(80) Eq. (80) means that transforming the data (choosing ) increases the overall likelihood only if the data is heavy-tailed enough. Note that the sum of squares is not squared again. Hence condition (80) is not equivalent for the data having empirical kurtosis larger than .

-

b)

If (80) does not hold, then must satisfy from (77) in Lemma B.1. It remains to be shown that this equation has (at least) one positive solution.

-

i)

Since for all , (79) is also true in the limit; however, we can ignore this solution as we require .

-

ii)

By continuity and , for sufficiently large , for all . Hence and therefore

(81) (82) showing that . That is, approaches from below for .

-

iii)

By continuity and (if (80) does not hold), it must cross the line at least once in the interval , proving the existence of .

-

i)

-

c)

The log-likelihood can be decomposed in

(83) Lemmas A.5 and A.6 show that is monotonically decreasing and is monotonically increasing in .

Furthermore, , that is the input likelihood is monotonically increasing but bounded from above (by ). On the other hand the penalty is decreasing without bounds, . Thus their sum attains a global maximum either at the unique mode of or at the boundary - see also Fig. 6b.

∎

Appendix C Details on IGMM

Here I present an iterative method to obtain , which builds on the input/output aspect and theoretical properties of the input . For example, if a random variable should be exponentially distributed (e.g. waiting times), but the observed data shows heavier tails then it is natural to estimate and such that the back-transformed data has skewness , as this is a particular property of exponential RVs - independent of the rate parameter ; to remove heavy tails in we should choose such that the back-transformed data has sample kurtosis ; or for uniform input, we can try to find a such that has a flat density estimate.

Here I describe the estimator for to remove heavy-tails in location-scale data, in the sense that the kurtosis of the input equals . It can be easily adapted to match other properties of the input as outlined above.

For a moment assume that and are known and fixed; only has to be estimated. A natural choice for is the one that results in back transformed data () with sample kurtosis equal to the theoretical kurtosis . Formally,

| (84) |

where is a proper norm in .

While the concept of this estimator is identical to its skewed version (Goerg, 2011), it has one important advantage: the inverse transformation is bijective. Thus here we do not have to consider “lost” data points when applying the inverse transformation.

Discussion of Algorithm 1:

The kurtosis of as a function of is continuous and monotonically increasing (see (22)). Also has a smaller slope than the identity , and the slope is decreasing as is increasing. Thus if the kurtosis of the original data is larger than the target kurtosis of the back-transformed data, , then there always exists a that achieves . By the re-parametrization the bounded optimization problem can be solved by standard (unbounded) optimization algorithms.

In practice, and are rarely known but also have to be estimated from the data. As is shifted and scaled ahead of the back-transformation , the initial choice of and affects the optimal choice of . Therefore the optimal triple must be obtained iteratively.

Discussion of Algorithm 2:

Algorithm 2 first computes using and from the previous step. This normalized output can then be passed to Algorithm 1 to obtain an updated . Using this new one can back-transform to , and consequently obtain a better approximation to the “true” latent by . However, - and therefore - has been obtained using and , which are not necessarily the most accurate estimates in light of the updated approximation . Thus Algorithm 2 computes new estimates and by the sample mean and standard deviation of , and starts another iteration by passing the updated normalized output to Algorithm 1 to obtain a new .

It returns the optimal once convergence has been reached, i.e., if .

Appendix D Simulation Details

Slightly heavy-tailed: .

Here the RV has slight excess kurtosis () and . The Lambert W estimates of are unbiased, and have smaller empirical standard deviation for than the Gaussian MLE or the median. Also using Lambert W estimators does not give worse estimates for .

| median | Gaussian MLE | IGMM | Lambert W MLE | NA | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | ratio | |||||||||||