A Random Matrix–Theoretic Approach to Handling Singular Covariance Estimates

Abstract

In many practical situations we would like to estimate the covariance matrix of a set of variables from an insufficient amount of data. More specifically, if we have a set of independent, identically distributed measurements of an dimensional random vector the maximum likelihood estimate is the sample covariance matrix. Here we consider the case where such that this estimate is singular (non–invertible) and therefore fundamentally bad. We present a radically new approach to deal with this situation. Let be the data matrix, where the columns are the independent realizations of the random vector with covariance matrix . Without loss of generality, and for simplicity, we can assume that the random variables have zero mean. We would like to estimate from . Let be the classical sample covariance matrix. Fix a parameter and consider an ensemble of random unitary matrices, , having Haar probability measure (isotropically random). Pre– and post–multiply by , and by the conjugate transpose of respectively, to produce a non–singular reduced dimension covariance estimate. A new estimate for , denoted by , is obtained by a) projecting the reduced covariance estimate out (to ) through pre– and post–multiplication by the conjugate transpose of , and by respectively, and b) taking the expectation over the unitary ensemble. Another new estimate (this time for ), , is obtained by a) inverting the reduced covariance estimate, b) projecting the inverse out (to ) through pre– and post–multiplication by the conjugate transpose of , and by respectively, and c) taking the expectation over the unitary ensemble. We show that the estimate is equivalent to diagonal loading. Both estimates and retain the original eigenvectors and make nonzero the formerly zero eigenvalues. We have a closed form analytical expression for in terms of its eigenvector and eigenvalue decomposition. We motivate the use of through applications to linear estimation, supervised learning, and high–resolution spectral estimation. We also compare the performance of the estimator with respect to diagonal loading.

Index Terms:

Singular Covariance Matrices, Random Matrices, Limiting Distribution, Sensor Networks, Isotropically Random, Stiefel Manifold, Curse of DimensionalityI Introduction

The estimation of a covariance matrix from an insufficient amount of data is one of the most common multivariate problems in statistics, signal processing, and learning theory. Inexpensive sensors permit ever more measurements to be taken simultaneously. Thus the dimensions of feature vectors are growing. But typically the number of independent measurements of the feature vector are not increasing at a commensurate rate. Consequently, for many problems, the sample covariance matrix is almost always singular (non–invertible). More precisely, given a set of independent multivariate Gaussian feature vectors, the sample covariance matrix is a maximum likelihood estimate. When the number of feature vectors is smaller than their dimension then the estimate is singular, and the sample covariance is a fundamentally bad estimate in the sense that the maximum likelihood principle yields a non–unique estimate having infinite likelihood. The sample covariance finds linear relations among the random variables when there may be none. The estimates for the larger eigenvalues are typically too big, and the estimates for the small eigenvalues are typically too small.

The conventional treatment of covariance singularity artificially converts the singular sample covariance matrix into an invertible (positive–definite) covariance by the simple expedient of adding a positive diagonal matrix, or more generally, by taking a linear combination of the sample covariance and an identity matrix. This procedure is variously called “diagonal loading” or “ridge regression” [12], [10]. The resulting covariance has the same eigenvectors as the sample covariance, and eigenvalues which are uniformly scaled and shifted versions of the sample covariance eigenvalues. The method of Ledoit and Wolf [7] automatically chooses the combining coefficients for diagonal loading.

We propose a radically different alternative to diagonal loading which is based on an ensemble of dimensionality reducing random unitary matrices. The concept is that the unitary matrix multiplies the feature vectors to produce shortened feature vectors, having dimension significantly smaller than the number of feature vectors, which produce a statistically meaningful and invertible covariance estimate. The covariance estimate is used to compute an estimate for the ultimate quantity or quantities of interest. Finally this estimate is averaged over the ensemble of unitary matrices. We consider two versions of this scheme which we call and . We show that the estimate is equivalent to diagonal loading. Both estimates and retain the original eigenvectors and make nonzero the formerly zero eigenvalues. We have a closed form analytical expression for in terms of its eigenvector and eigenvalue decomposition. We motivate the use of through applications to linear estimation, supervised learning, and high–resolution spectral estimation. We also compare the performance of the estimator with respect to diagonal loading.

Throughout the paper we will denote by the complex conjugate transpose of the matrix . will represent the identity matrix. We let be the non–normalized trace for square matrices, defined by,

where are the diagonal elements of the matrix . We also let be the normalized trace, defined by .

II New Approach to Handling Covariance Singularity

We begin with a set of independent identically distributed measurements of an dimensional random vector where . We introduce an ensemble of random unitary matrices, such that . The unitary matrix multiplies the feature vectors to produce a set of feature vectors of dimension from which we obtain an invertible sample covariance matrix. The dimensionality reduction process is reversible (i.e., no information is thrown away) provided it is done for a sufficient multiplicity of independent unitary matrices. The key question is what to do with the ensemble of reduced dimension covariance estimates.

II-A Notation and sample covariance

We are given a data matrix, , the columns of which comprise independent identically distributed realizations of a random vector. For convenience we assume that the random vector is zero-mean. We also will assume that the random vector is circularly-symmetric complex. The sample covariance is

| (1) |

We are interested in the case where . Consequently the sample covariance is singular with rank equal to .

II-B Dimensionality–reducing ensemble

We introduce an ensemble of random unitary matrices, where and , where is the identity matrix. The multiplication of the data matrix by the unitary matrix results in a data matrix of reduced dimension, , which in turn produces a statistically meaningful sample covariance matrix provided that is sufficiently small compared with ,

| (2) |

We need to specify the distribution of the random unitary matrix. One possibility would be to use a random permutation matrix, the effect of which would be to discard all but of the components of the data vectors. Instead we utilize the Haar measure (sometimes called the “isotropically random” distribution [11]). A fundamental property of the Haar distribution is its invariance to multiplication of the random unitary matrix by an unrelated unitary matrix. Specifically, let be the joint probability density for the components of the unitary matrix, and let be any unrelated unitary matrix (i.e., either is deterministic, or it is statistically independent of ). Then has Haar measure if and only if for all unitary

| (3) |

Compared with the random permutation matrix, the Haar measure is more flexible as it permits linear constraints to be imposed.

II-C Two nonsingular covariance estimates

The generation of the ensemble of reduced-dimension covariance estimates (2) is well–motivated. It is less obvious what to do with this ensemble. We have investigated two approaches: which yields directly a non–singular estimate for the covariance matrix, and which yields directly an estimate for the inverse covariance matrix.

II-C1

If we project the covariance (2) out to a covariance using the same random unitary matrix, and then take the expectation over the unitary ensemble, we obtain the following:

| (4) |

This expectation can be evaluated in closed form (either by evaluating fourth moments, or by using Schur polynomials as shown later):

| (5) |

Thus the procedure is equivalent to diagonal loading for a particular pair of loading parameters. The dimensionality parameter, , determines the amount of diagonal loading. It is reasonable to re-scale the covariance expression (5) by the factor because the dimensionality reduction yields shortened feature vectors whose energy is typically times the energy of the original feature vectors. Note that we use the term energy to denote the of a vector . If the covariance is scaled in this manner then the trace of the sample covariance is preserved.

Although it is both interesting and surprising that is equivalent to diagonal loading, we instead pursue an approach which is better motivated and which promises more compelling action.

II-C2

We first invert the covariance (2) (which is invertible with probability one), project out to using the same unitary matrix, and then take the expectation over the unitary ensemble to obtain the following:

| (6) |

The estimate (as well as ) preserves the eigenvectors. In other words, if we perform the eigenvector and eigenvalue decomposition,

| (7) |

where is the diagonal matrix, whose diagonals are the eigenvalues, ordered from largest to smallest, and is the unitary matrix of eigenvectors, then we prove (in Section IV) that

| (8) |

Therefore it is enough to compute . We also show that is a diagonal matrix. Moreover, we show that if where is the matrix with the non–zero entries. The matrix is a diagonal matrix that can be decomposed as

In other words all the zero–eigenvalues are transformed to a non–zero constant . In Section VI we prove an exact expression for the entries of . More specifically we prove that

where the average is taken over the ensemble of all Gaussian random matrices with independent and complex entries with zero mean and unit variance. Proposition 1 (in Section VI) gives us an explicit formula for . On the other hand, using Lemma 1 (in the same Section) we prove that

where

can be explicitly computed using Theorem 1 in Section VI. Therefore, given we obtain close form expressions for all the entries of the matrix for every and .

In Section VIII using Free Probability techniques we prove asymptotic formulas for the entries of for large values of .

We focus the remainder of the paper on some potential applications of , the derivation of its fundamental properties, and how to compute it.

III Potential Applications of

Typically neither the covariance matrix nor its inverse is of direct interest. Rather some derived quantity is desired. Here we discuss three potential applications where arises in a natural way.

III-A Design of a linear estimator from training data

The problem is to design a minimum mean square linear estimator for a random vector given an observation of a random vector . Exact statistics are not available; instead we have to work with statistics that are estimated from a set of training data. If the statistics were available then the optimum estimator would be (assuming that the vectors have zero–mean)

| (9) |

where is the covariance matrix of vector and is the cross–covariance matrix of vectors and . In this case, the mean-square error is

| (10) | |||||

For the design of the estimator we have training data comprising independent joint realizations of and : () and (), where .

We introduce an ensemble of isotropically random unitary matrices, , where . We reduce the dimensionality of the observed vector, , and the training set, , and we estimate the relevant covariances as follows,

| (11) |

| (12) |

We estimate given the reduced observation by treating the covariance estimates (11) and (12) as if they were correct:

| (13) | |||||

The mean-square error of this estimator conditioned on the random unitary matrix, , is found by taking an expectation with respect to the training data, , the observation, , (which is independent of the training data), and the true value of the unknown vector, :

| (14) |

where is a random matrix comprising independent CN(0,1) random variables. We note the asymptotic result,

| (15) |

The mean–square error (14) is equal to the product of two terms: the mean-square error which results from performing estimation with a reduced observation vector and with exact statistics available, and a penalty term which account for the fact that exact statistics are not available. The first term typically decreases with increasing dimensionality parameter, , which the second term increases with .

Instead of performing the estimation using one value of the dimensionality-reducing matrix, , one can average the estimator (13) over the unitary ensemble:

| (16) | |||||

Jensen’s inequality implies that the ensemble-averaged estimator (16) has better performance than the estimator (13) that is based on a single realization of ,

| (17) |

III-B Supervised learning: Design of a quadratic classifier from training data

The problem is to design a quadratic classifier from labeled training data. Given an observation of a zero-mean complex Gaussian random vector, the classifier has to choose one of two hypotheses. Under hypothesis , , the observation is distributed as , . If the two covariance matrices were known the optimum classifier is a “likelihood ratio test” [15],

| (18) |

where is a threshold. Instead the covariances have to be estimated from two matrices of labeled training data, , , each of which comprises independent observations of the random vector under their respective hypotheses.

We introduce an ensemble of random unitary matrices, , where . For a given we reduce the dimension of both sets of training data and then estimate the reduced covariance matrices,

| (19) |

For any we could implement a likelihood ratio test based on the estimated reduced covariances (19) and the reduced observation, . Alternatively we could base the hypothesis test on the expectation of the log–likelihood ratio with respect to the unitary ensemble,

| (20) |

This classifer is of the “naive Bayes” type [16], in which statistical dependencies (in this case the individual likelihood ratios are not statistically dependent) are ignored in order to simplify the construction of the classifier.

III-C Capon MVDR spectral estimator

The Capon MVDR (minimum variance distortionless response) spectral estimator estimates power as a function of angle-of-arrival given independent realizations of a -dimensional measurement vector from an array of sensors [17]. Let be the vector of measurements, , and let the “steering vector”, , be the dimensional unit vector which describes the wavefront at the array. The conventional power estimate, as a function of the steering vector, is

| (21) |

where is the sample covariance matrix. The Capon MVDR power estimate is

| (22) |

A justification for the Capon estimator is the following: one considers the estimated covariance matrix to be the sum of two terms, the first corresponding to power arriving from the direction that is specified by the steering vector, and the second corresponding to power arriving from all other directions,

| (23) |

It can be shown that the Capon power estimate (22) is equal to the largest value of power such that, in the decomposition (23), is nonnegative definite [1]. In other words the decomposition (23) is nonunique, and the Capon power estimate is an upper bound on the possible value that the power can take.

We deal with the singularity of the covariance matrix by introducing an ensemble of unitary matrices, . Since we are looking for power that arrives from a particular direction we constrain the unitary matrices to preserve the energy of the steering vector, i.e., . This is readily done through a Householder unitary matrix, , such that

| (24) |

where is a unitary matrix whose rows are orthogonal to . We represent the ensemble as follows:

| (25) |

where is a isotropically random unitary matrix. We now use the constrained unitary matrix to reduce the dimensionality of the sample covariance matrix and the steering vector, we compute the Capon power estimate from the reduced quantities, and finally we average the power with respect to the unitary ensemble [2]:

where

| (27) |

III-D Distantly related research

Our approach to handling covariance singularity is based on an ensemble of dimensionality–reducing random unitary matrices. Here we mention some other lines of research which also involve random dimensionality reduction.

III-D1 Johnson–Lindenstauss Lemma

In qualitative terms, the Johnson–Lindenstrauss Lemma [13] has the following implication: the angle between two vectors of high dimension tends to be preserved accurately when the vectors are shortened through multiplication by a random unitary dimensionality–reducing matrix.

III-D2 Compressive Sampling or Sensing

Compressive sampling or sensing permits the recovery of a sparsely-sampled data vector (for example, obtained by multiplying the original vector by a random dimensionality–reducing matrix), provided the original data vector can be linearly transformed to a domain in which it has sparse support [14]. Compressive sampling utilizes only one dimensionality–reducing matrix. In contrast our approach to handling covariance singularity utilizes an ensemble of random dimensionality–reducing matrices.

IV Derivation of Some Basic Properties of

In this Section we state and prove two basic and fundamental properties of . We perform the eigenvector and eigenvalue decomposition,

| (28) |

where is the diagonal matrix, whose diagonals are the eigenvalues, ordered from largest to smallest, and is the unitary matrix of eigenvectors.

IV-A Eigenvectors of sample covariance are preserved

We substitute the eigenvalue decomposition (7) into the expression (6) for to obtain the following:

| (29) | |||||

where we have used the fundamental definition of the isotropic distribution (3), i.e. that the product has the same distribution as . We intend to show that is itself diagonal. We utilize the fact that a matrix is diagonal if and only if, for all diagonal unitary matrices, , . Let be a diagonal unitary matrix, we have

| (30) | |||||

where we used the fact that has the same distribution as , and that . Therefore we have established that the final expression in (29) is the eigenvector/eigenvalue decomposition of , for which the eigenvector matrix is and the diagonal matrix of eigenvalues is . Hence, we need only consider applying to diagonal matrices.

IV-B The zero-eigenvalues of the sample covariance are converted to equal positive values

When the rank of the covariance matrix is equal to , the eigenvalue matrix of has the form

| (31) |

We want to establish that the last eigenvalues of are equal. To that end we introduce a unitary matrix, ,

| (32) |

where is an arbitrary permutation matrix. We now pre– and post–multiply by and respectively: it will be shown that this does not change the diagonal matrix, so consequently the last eigenvalues are equal. We have

| (33) | |||||

where we used the fact that has the same distribution as , and that .

V Functional Equation

In this Section we will prove a functional equation for the inverse covariance estimate .

Let be an sample covariance matrix of rank . Since is positive definite there exists an unitary and an diagonal matrix of rank such that . Fix . We would like to compute,

| (34) |

where is an unitary matrix and the average is taken with respect to the isotropic measure. Let be an Gaussian random matrix with complex, independent and identically distributed entries with zero mean and variance 1. It is a well known result in random matrix theory (see [6]) that we can decompose where is an positive definite and invertible matrix (with probability one). Hence, . Therefore,

| (35) |

Moreover, as shown in the previous Section

| (36) |

Therefore it is enough to compute . Decompose as where is and is . Now performing the block matrix multiplications and taking the expectation we obtain that is equal to

| (37) |

where and an diagonal matrix of full rank.

Let us first focus on the matrix , denote this matrix by

| (38) |

Let be the matrix . Then

and

Therefore it is enough to compute

which is equal to

Let us decompose where is an unitary matrix and is an diagonal matrix of rank . Then . It is a straightforward calculation to see that

it is equal to

Doing the block matrix decomposition

where is and is we see that

where , , and . Since we see that

Putting all the pieces together we obtain that

| (42) |

where is an isotropically distributed unitary matrix and

Let us decompose the unitary matrix as , where is and is matrix. Then and isotropically distributed unitaries. It is an easy calculation to see that

| (45) | |||||

| (46) |

Remark 1

As we saw in Equation (37) the other important term in is

Let us define as

| (49) |

Since and are Gaussian independent random matrices it is clear that

where is the identity matrix of dimension . Putting all the pieces together we see that the estimate is equal to

| (50) |

VI fcov exact formula

In this Section we will prove an exact and close form expression for the entries of . We will treat separately the entries of and the constant term . As a matter of fact the analysis developed in this Section will allow us to obtain close form expressions for more general averages.

Recall that we say a matrix is said to be normal if it commutes with its conjugate transpose . Given a normal matrix and a continuous function we can always define using functional calculus. Being more precise we know by the spectral Theorem that exist unitary and such that

We then define

where . In particular, let be as before and let be a continuous function, we will obtain an exact expression for

| (51) |

where is an unitary isotropically random. Note that our covariance estimate is a particular case of the last expression when .

Let be the Stiefel manifold with the isotropic measure . By equation (18) in [3] we know that

| (52) |

where is the Schur polynomial associated with the partition . The latter are explicitly defined for any matrix in terms of the eigenvalues as

| (53) |

with being a partition, i.e. a non–increasing sequence of non–negative integers . For an introduction to the theory of symmetric functions and properties of the Schur polynomials see [4] and [5].

Denote by the partition with ones. One of the properties of the Schur polynomials is that

| (54) |

The constant see [4]. Therefore,

| (56) |

For each consider the operator defined in by . This extends linearly and continuously to a well defined linear operator where are the continuous functions in the interval . Now we are ready to state the main Theorem of this Section.

Theorem 1

Let be an diagonal matrix of rank . For any continuous (complex or real valued) function

| (57) |

is equal to

where is the Vandermonde matrix associated to and is the matrix defined by replacing the row of the Vandermonde matrix , , by the row

Proof:

By linearity and continuity (polynomials are dense in the set of continuous functions) it is enough to prove (57) in the case . By (55) and (56) we know that

is equal to

| (58) |

where

By definition of the Schur polynomials (see [4])

where the –column of the matrix is

Doing row transpositions on the rows of the matrix we obtain a new matrix where the –column of this new matrix is

Note that this matrix is identical to except of the row which was replaced by the row instead of as in . Therefore,

is equal to

| (59) |

Now and using the fact that

we obtain that

Putting all the pieces together we obtain that

is equal to

∎

The next Proposition gives us, in particular, an exact and close form expression for the term in equation (49) discussed previously.

Proposition 1

Let be an diagonal matrix of rank . Let and be an Gaussian random matrix with independent and identically distributed entries with zero mean and variance . Then

| (60) |

and

| (61) |

where is the matrix constructed by replacing the row of the Vandermonde matrix by the row

Proof:

Let and let us consider then for each we see that

since this is a multiple of the row of the Vandermonde matrix we see that for all .

It is not difficult to see that for

Therefore using Theorem 1 we see that

| (62) |

where is constructed by replacing the row of the Vandermonde matrix by the row

Now we will prove the second part of the Proposition. Given an random matrix as in the hypothesis we can decompose as

where is an isotropically random unitary and is a positive definite independent from (see Section 2.1.5 from [6]). The matrix is invertible with probability 1. Hence,

Therefore,

where in the second equality we used the trace property. Recall from random matrix theory that if are independent random matrices then

Since the matrix is independent with respect to and we conclude that

is equal to

Let then and it is known (see Lemma 2.10 [6]) that

Putting all the pieces together we see that

| (63) |

finishing the proof. ∎

VI-A Application of the Main Results to

Using Theorem 1 we can compute several averages over the Stiefel manifold. As an application let us compute

| (64) |

First let us note that the same proof in Lemma 2 gives us the following result.

Lemma 1

Let be a differentiable function in the interval where and . Then the following formula holds,

| (65) |

is equal to

where means the entry of the matrix .

Let an diagonal matrix of rank and let . By equation (64) and Lemma 1 we know that

Since

where

and

Then

Therefore, is equal to

hence

Therefore,

VI-B Application of the Main Results to

As we mention in the introduction and subsequent Sections the problem we are mainly interested is to compute when is an diagonal matrix of rank and . Let where . As we previously saw is a diagonal matrix that can be decomposed as

where

and

where the average is taken over the ensemble of all Gaussian random matrices with independent and complex entries with zero mean and unit variance.

VI-C Small Dimension Example

In this subsection we will compute for a small dimensional example. Let , and and . Hence following our previous notation . Let us first consider the case . In this case using equation (48) and equation (82) we see that

The more interesting case is . Applying Theorem 1 and Lemma 1 we see that

where

where

and

Doing the calculations we see that

| (66) |

and

| (67) |

On the other hand using Proposition 1

where

Therefore,

| (68) |

To summarize, computation of is facilitated by first taking the eigenvector and eigenvalue decomposition of the sample covariance matrix and then applying to the diagonal eigenvalue matrix. At that point there are three alternatives: a straight Monte Carlo expectation, the asymptotic expressions (81) and (88), or the closed form analytical expressions according to Proposition 1 and Theorem 1.

VII Preliminaries on the Limit of Large Random Matrices

A random matrix is a measurable map , defined on some probability space and which takes values in a matrix algebra, say. In other words, is a matrix whose entries are (complex) random variables on . One often times identifies with the probability measure it induces on and forgets about the underlying space . Random matrices appear in a variety of mathematical fields and in physics too. For a more complete and detailed discussion of random matrix limits and free probability see [21], [20], [18], [19] and [6]. Here we will review only some key points.

Let us consider a sequence of self–adjoint random matrices . In which sense can we talk about the limit of these matrices? It is evident that such a limit does not exist as an matrix and there is no convergence in the usual topologies. What converges and survives in the limit are the moments of the random matrices. Let where the entries are random variables on some probability space equipped with a probability measure . Therefore,

| (69) |

and we can talk about the –th moment of our random matrix , and it is well known that for nice random matrix ensembles these moments converge for . So let us denote by the limit of the –th moment,

| (70) |

Thus we can say that the limit consists exactly of the collection of all these numbers . However, instead of talking about a collection of numbers we prefer to identify these numbers as moments of some random variable . Now we can say that our random matrices converge to a variable in distribution (which just means that the moments of converge to the moments of ). We will denote this by .

One should note that for a self–adjoint matrix , the collection of moments corresponds also to a probability measure on the real line, determined by

| (71) |

This measure is given by the eigenvalue distribution of , i.e. it puts mass on each of the eigenvalues of (counted with multiplicity):

| (72) |

where are the eigenvalues of . In the same way, for a random matrix , is given by the averaged eigenvalue distribution of . Thus, moments of random matrices with respect to the averaged trace contain exactly that type of information in which one is usually interested when dealing with random matrices.

Example 1

Let us consider the basic example of random matrix theory. Let be an self-adjoint random matrix whose upper–triangular entries are independent zero-mean random variables with variance and fourth moments of order . Then the famous Theorem of Wigner can be stated in our language as

| (73) |

where semicircular just means that the measure is given by the semicircular distribution (or, equivalently, the even moments of the variable are given by the Catalan numbers).

Example 2

Another important example in random matrix theory is the Wishart ensemble. Let be an random matrix whose entries are independent zero-mean random variables with variance and fourth moments of order . As with ,

| (74) |

where is a random variable with the Marcenko–Pastur law with parameter .

The empirical cumulative eigenvalue distribution function of an self–adjoint random matrix is defined by the random function

where are the (random) eigenvalues of for each realization . For each this function determines a probability measure supported on the real line. These measures define a Borel measure in the following way. Let be a Borel subset then

A new and crucial concept, however, appears if we go over from the case of one variable to the case of more variables.

Definition 1

Consider random matrices and variables (living in some abstract algebra equipped with a state ). We say that

in distribution if and only if

| (75) |

for all choices of , .

The arising in the limit of random matrices are a priori abstract elements in some algebra , but it is good to know that in many cases they can also be concretely realized by some kind of creation and annihilation operators on a full Fock space. Indeed, free probability theory was introduced by Voiculescu for investigating the structure of special operator algebras generated by these type of operators. In the beginning, free probability had nothing to do with random matrices.

Example 3

Let us now consider the example of two independent Gaussian random matrices (i.e., each of them is a self–adjoint Gaussian random matrix and all entries of are independent from all entries of ). Then one knows that all joint moments converge, and we can say that

| (76) |

where Wigner’s Theorem tells us that both and are semicircular. The question is: What is the relation between and ? Does the independence between and survive in some form also in the limit? The answer is yes and is provided by a basic theorem of Voiculescu which says that and are free. For a formal definition of freeness and more results in free probability see [21], [20], [18] and [19].

VIII Asymptotic results

In practical application when the values of and are too large the expressions of the previous Section could be difficult to evaluate and we need simpler mathematical formulas. It is for this reason that in this Section we will provide asymptotic results for the entries of . As we previously saw is equal to

where and an diagonal matrix of full rank. In this Section we will get asymptotic results for both terms and as with .

Recall that was defined as

| (77) |

As we already observed, if and are Gaussian independent random matrices it is clear that

Let us introduce the –transform of an random matrix as,

Analogously, given a probability measure on we can define the –transform of as

It is not difficult to see that

and

Consider a collection of diagonal diagonal matrices such that converge in distribution to a probability measure , i.e. for all

Let be a sequence of complex Gaussian random matrices with standard i.i.d. entries. Then by Theorem 2.39 in [6] we know that converges in distribution (moreover, almost surely) as as with to a probability distribution whose –transform satisfies

| (78) |

where is the –transform of the limit in distribution of . Note that and . Therefore, taking limit as goes to infinity on both sides of equation (78) we get

| (79) |

since by definition and the convergence in distribution for sufficiently large we have that

| (80) |

and

The symbol denotes that equality holds in the limit.

where . Note that this equation implicitly and uniquely defines .

Remark 2

Now we will compute the asymptotics of the other, and more complicated, term

Lemma 2

Let be a differentiable function on the interval where and . Then the following formula holds

| (83) |

Proof:

It is enough to prove this Lemma for the case is a polynomial and by linearity it is enough to prove it for the case . Let be the matrix whose entries are all zero except the entry which is equal to 1. Note that . If then and for each it is easy to see that

Therefore,

where we use the trace property and the fact that . Taking expectation on both sides we finish the proof. ∎

As a corollary we obtain.

Corollary 1

If

then .

Before continuing let us define the Shannon transform of a probability distribution. Given a probability distribution supported in we define

It is easy to see that .

Consider, as before, a collection of diagonal diagonal matrices such that converge in distribution to a probability measure . Let be a sequence of complex Gaussian random matrices with standard i.i.d. entries. Then by equation 2.167 in [6] we know that converges in distribution (moreover, almost surely) as as with to a probability distribution whose Shannon–transform satisfies

| (84) |

Subtracting on both sides and taking the limit we obtain

| (85) |

For and sufficiently large

| (86) |

and

Hence, for sufficiently large

Taking partial derivatives on both sides with respect to we obtain

| (88) |

IX Simulations

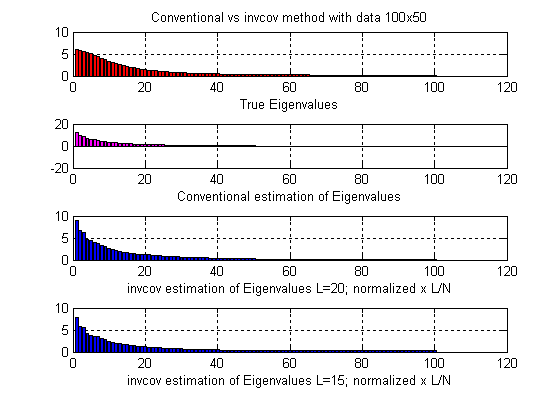

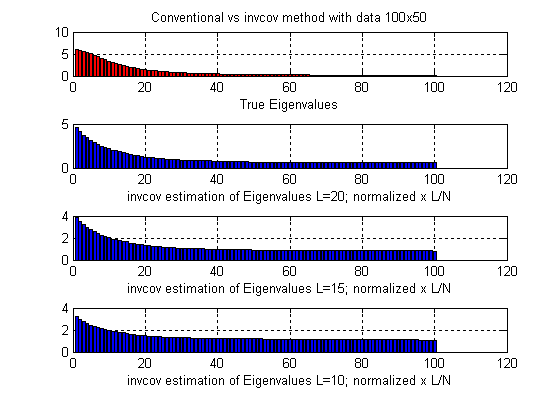

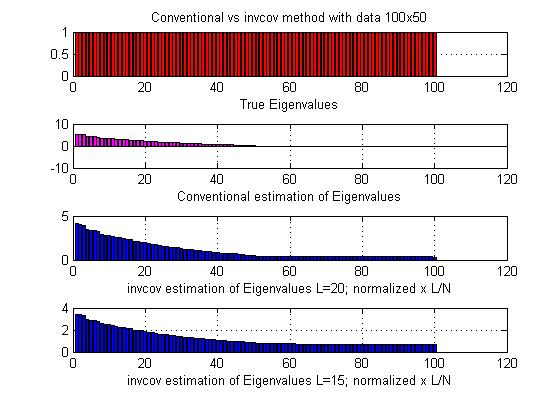

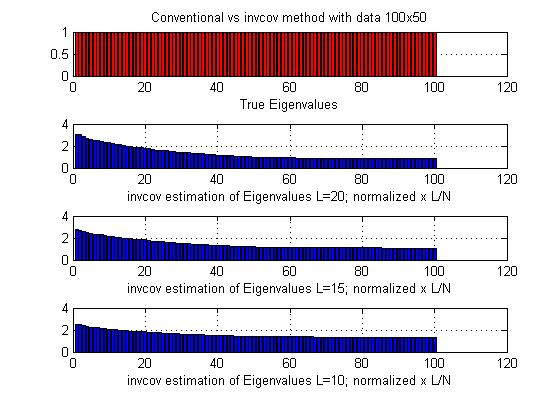

In this Section we present some of the simulations performed. Let be a true covariance matrix with Toeplitz with entries . Assume we take measurements and we want recover to the best of our knowledge. After performing the measurements we construct the sample covariance matrix . In Figure 1 and 2 we can see the eigenvalues of the true matrix, the eigenvalues of the sample covariance matrix (raw data) and the eigenvalues of the new matrix after performing the randomization to the sample covariance for different values of . In other words we are comparing the eigenvalues of , and of for different values of . Recall that is an estimate for and therefore is an estimate for . We also performed the same experiment for the case that the true covariance matrix is a multiple of the identity. This corresponds to the case in which the sensors are uncorrelated. See Figure 3 and 4.

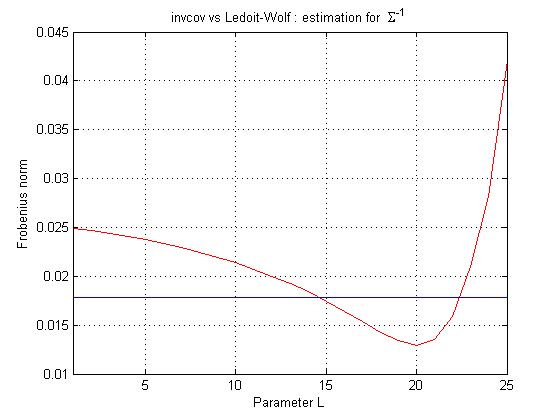

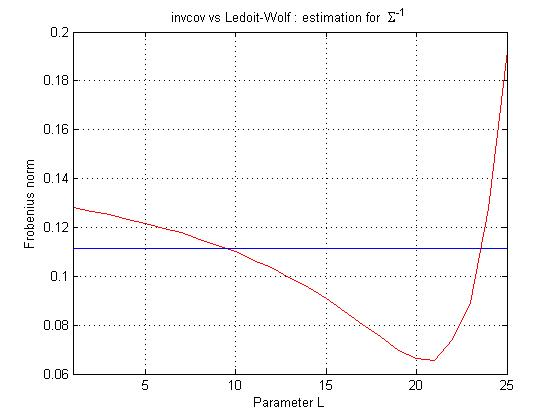

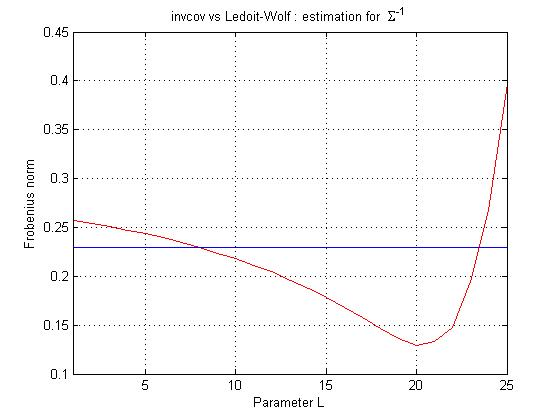

Let be an matrix we define the Frobenius norm as . In Figure 5, 6 and 7 we compare the performance of our estimator with the more standard estimator of Ledoit and Wolf [7]. The experiment was performed with a true covariance matrix with Toeplitz entries and . We compute the Frobenius norm for the different values of and we compare it with . We use and . We can see that our method outperform Ledoit and Wolf for a big range of the parameter . We also note that in the three cases is the optimum.

X Comments

Our investigation indicates that the new method presented in this article is interesting and promising from the mathematical point of view, as well as the practical one. Even though we were able to find the asymptotics formulas as well as close form expressions for , and more generally for , both estimates for and , there is a natural question still unanswered. How to find the optimum ? For instance assume we know that the matrix is an Toeplitz distributed with entries with unknown . How does the optimum depends on and ? In the simulations presented in Section IX we see that for , the optimum is equal to 20 and it seems to be independent on the value of . We believe that this a question interesting to explore.

XI Acknowledgments

We would like to thank Thomas Bengtsson and Yuliy Baryshnikov for many helpful discussions and comments.

Appendix A Average over the permutation matrices

In this Appendix we study what happen if we substitute the average over the isotropically random unitary matrices by the set of permutation matrices. Let be an diagonal matrix with and . We will denote the orthonormal vector in whose entries are zero except at the –coordinate that is 1. A permutation matrix is a matrix of the form

Theorem 2

Let be a diagonal matrix as before. Then

Proof:

We will first show that

Given then . Therefore,

Hence,

Thus,

| (90) |

Note that is the matrix that has all entries zero except at the entry which is 1. The total number of different permutation matrices is . Therefore,

where the first sum is running over all the possible permutation matrices. The number of permutation matrices that have as one of their rows is . Hence,

∎

References

- [1] T. L. Marzetta, A new interpretation for Capon’s maximum likelihood method of frequency-wavenumber spectrum estimation, IEEE Trans. on Acoustics, Speech, and Signal Processing, ASSP-31 (2), p. 445-449, 1983.

- [2] T. L. Marzetta, S. H. Simon, and H. Ren, Capon-MVDR spectral estimation from singular data covariance matrix, with no diagonal loading, Proc. Fourteenth Annual Workshop on Adaptive Sensor Array Processing (ASAP 2006), M.I.T. Lincoln Laboratory, June 6-7, 2006.

- [3] Y. V. Fyodorov and B. A. Khoruzhenko, A few remarks on Color–Flavor Transformations, truncation of random unitary matrices, Berezin reproducing kernels and Selberg type integrals, arXiv : math-ph/0610045v2, 2006.

- [4] I. G. Macdonald, Symmetric functions and Hall Polynomials, Clarendon Press, Oxford University Press, New York, 1995.

- [5] R. J. Muirhead, Aspects of Multivariate Statistical Theory, John Wiley & Sons, New York, 1982.

- [6] S. Verdu and A. M. Tulino, Random Matrix Theory and Wireless Communications, Now Publishers Inc., 2004.

- [7] O. Ledoit and M. Wolf, Some Hypothesis Tests for the Covariance Matrix when the Dimension is Large Compared to the Sample Size, Annals of Statistics, vol. 30, no. 4, pp. 1081–1102, 2002.

- [8] J. Capon, High–Resolution Frequency Wavenumber Spectrum Analysis, Proc. IEEE, Vol. 57, 1408-1418, 1969.

- [9] N. R. Rao and A. Edelman, The Probability Distribution of the MVDR Beamformer Outputs under Diagonal Loading, Proc. Thirteen Annual Adaptative Sensor Array Proc. Workshop, 7-8 June, 2005.

- [10] C. D. Richmond, R. R. Nadakuditi and A. Edelman, Asymptotic Mean Square Error Performance of Diagonally Loaded Capon-MVDR Processor, Proc. Asilomar Conf. on Signals, Systems, and Computers, Pacific Grove, CA, Oct. 29-Nov. 1, 2005.

- [11] T. L. Marzetta and B. M. Hochwald, Capacity of a Mobile Multiple-Antenna Communication Link in Rayleigh Flat Fading, IEEE Trans. Inform. Theory, vol. 45, p. 139-157, Jan. 1999.

- [12] N. R. Draper and H. Smith, Applied regression analysis, Wiley, 1998.

- [13] W. B. Johnson and J. Lindenstrauss, Extensions of Lipschtiz mappings into a Hilbert space, Contemp. Math., 26, p. 189-206, 1984.

- [14] E. J. Candes and M. B. Wakin, An introduction to compressive sampling, IEEE Signal Processing Magazine, [24], March 2008.

- [15] R. O. Duda and P. E. Hart, Pattern Classification and Scene Analysis, Wiley, 1973.

- [16] P. Domingos and M. Pazzani, Beyond independence: conditions for the optimality of the simple Bayesian classifier, Proceedings of the Thirteenth International Conference on Machine Learning, p. 105-112, Bari, Italy, 1996.

- [17] P. Stoica and R. Moses, Spectral Analysis of Signals, Pearson Prentice Hall, 2005.

- [18] A. Nica and R. Speicher, Lectures on the Combinatorics of Free Probability, Cambridge University Press, 2006.

- [19] B. Collins, J.A. Mingo, P. Sniady and R. Speicher, Second Order Freeness and Fluctuations of Random Matrices: III Higer Order Freeness and Free Cumulants, Documenta Math., vol. 12, pp. 1–70, 2007.

- [20] D. Voiculescu, Free Probability Theory, Fields Institute Communications, 1997 .

- [21] D. Voiculescu, K. Dykema and A. Nica, Free Random Variables, CRM Monograph Series, vol. 1, AMS, 1992.