On the consistency of Fréchet means in deformable models for curve and image analysis

Abstract

A new class of statistical deformable models is introduced to study high-dimensional curves or images. In addition to the standard measurement error term, these deformable models include an extra error term modeling the individual variations in intensity around a mean pattern. It is shown that an appropriate tool for statistical inference in such models is the notion of sample Fréchet means, which leads to estimators of the deformation parameters and the mean pattern. The main contribution of this paper is to study how the behavior of these estimators depends on the number of design points and the number of observed curves (or images). Numerical experiments are given to illustrate the finite sample performances of the procedure.

Keywords: Mean pattern estimation, Fréchet mean, Shape analysis, Deformable models, Curve registration, Image warping, Geometric variability, High-dimensional data.

AMS classifications: Primary 62G08; secondary 42C40

Acknowledgements - We would like to thank Dominique Bakry for fruitful discussions. Both authors would like to thank the Center for Mathematical Modeling and the CNRS for financial support and excellent hospitality while visiting Santiago where part of this work was carried out. We are very much indebted to the referees and the Associate Editor for their constructive comments and remarks that resulted in a major revision of the original manuscript.

1 Introduction

1.1 A statistical deformable model for curve and image analysis

In many applications, one observes a set of curves or grayscale images which are high-dimensional data. In such settings, it is reasonable to assume that the data at hand , denoting the -th observation for the -th curve (or image), satisfy the following regression model:

| (1.1) |

where are unknown regression functions (possibly random) with a convex subset of , the ’s are non-random points in (deterministic design), the error terms are i.i.d. normal variables with zero mean and variance , and . In this paper, we will suppose that the ’s are random elements which vary around the same mean pattern. Our goal is to estimate such a mean pattern and to study the consistency of the proposed estimators in various asymptotic settings: either when both the number of design points and the number of curves (or images) tend to infinity, or when (resp. ) remains fixed while (resp. ) tends to infinity.

In many situations, data sets of curves or images exhibit a source of geometric variations in time or shape. In such settings, the usual Euclidean mean in model (1.1) cannot be used to recover a meaningful mean pattern. Indeed, consider the following simple model of randomly shifted curves (with ) which is commonly used in many applied areas such as neuroscience [TIR10] or biology [Røn01],

| (1.2) |

where is the mean pattern of the observed curves, and the ’s are i.i.d. random variables in with density and independent of the ’s. In model (1.2), the shifts represent a source of variability in time. However, in (1.2) the Euclidean mean is not a consistent estimator of the mean pattern since by the law of large numbers

The randomly shifted curves model (1.2) is close to the perturbation model introduced by [Goo91] in shape analysis for the study of consistent estimation of a mean pattern from a set of random planar shapes. The mean pattern to estimate in [Goo91] is called a population mean, but to stress the fact that it comes from a perturbation model [Huc10] uses the term perturbation mean. To achieve consistency in such models, a Procrustean procedure is used in [Goo91], which leads to the statistical analysis of sample Fréchet means [Fré48] which are extensions of the usual Euclidean mean to non-linear spaces using non-Euclidean metrics. For random variables belonging to a nonlinear manifold, a well-known example is the computation of the mean of a set of planar shapes in the Kendall’s shape space [Ken84] which leads to the Procrustean means studied in [Goo91]. Consistent estimation of a mean planar shape has been studied by various authors, see e.g. [Goo91, KM97, KBCL99, Le98, LK00]. A detailed study of some properties of the Fréchet mean in finite dimensional Riemannian manifolds (such as consistency and uniqueness) has been performed in [Zie77, OC95, BP03, BP05, Huc10, Huc11, Afs11] .

The main goal of this paper is to introduce statistical deformable models for curve and image analysis that are analogue to Goodall’s perturbation models [Goo91], and to build consistent estimators of a mean pattern in such models. Our approach is inspired by Grenander’s pattern theory which considers that the curves or images in model (1.1) are obtained through the deformation of a mean pattern by a Lie group action [Gre93, GM07]. In the last decade, there has been a growing interest in transformation Lie groups to model the geometric variability of images, and the study of the properties of such deformation groups is now an active field of research (see e.g. [MY01, TY05] and references therein). There is also currently a growing interest in statistics on the use of Lie group actions to analyze geometric modes of variability of a data set [HHM10a, HHM10b].

To describe more formally geometric variability, denote by the set of square integrable real-valued functions on , and by an open subset of . To the set , we associate a parametric family of operators such that for each the operator represents a geometric deformation (parametrized by ) of a curve or an image. Examples of such deformation operators include the cases of:

- -

-

Shifted curves: with , (the space of periodic functions in with period 1) and an open set of .

- -

-

Rigid deformation of two-dimensional images:

with , where is a rotation matrix in , is an isotropic scaling and a translation in .

- -

-

Deformation by a Lie group action: the two above cases are examples of a Lie group action on the space (see [Hel01] for an introduction to Lie groups). More generally, assume that is a connected Lie group of dimension acting on , meaning that for any the action of onto is such that . In general, is not a linear space but can be locally parametrized by a its Lie algebra using the exponential map . If . This leads for to define the deformation operators

- -

-

Non-rigid deformation of curves or images: assume that one can construct a family of parametric diffeomorphisms of (see e.g. [BGL09]). Then, for , define the deformation operators

Then, in model (1.1), we assume that the ’s have a certain homogeneity in structure in the sense that there exists some such that

| (1.3) |

where are i.i.d. random variables (independent of the ’s) with an unknown density with compact support included in satisfying:

Assumption 1.1.

The density of the ’s is continuously differentiable on and has a compact support included in . We assume that can be written

| (1.4) |

where .

The function in model (1.3) represents the unknown mean pattern of the ’s. The ’s are supposed to be independent of the ’s and are i.i.d. realizations of a second order centered Gaussian process taking its values in . The ’s represent the individual variations in intensity around , while the random operators model geometric deformations in time or space. Then, if we assume that the ’s are linear operators, equation (1.3) leads to the following statistical deformable model for curve or image analysis

| (1.5) |

where are i.i.d. normal variables with zero mean and variance .

Model (1.5) could be also called a perturbation model using the terminology in [Goo91, Huc10] for shape analysis. To be more precise, let be a set of points in representing a planar shape. Define a deformation operator for acting on in the following way

and . Consistent estimation of a mean shape has been first studied in [Goo91] when a set of random shapes is drawn from the following perturbation model

| (1.6) |

Model (1.6) is similar to the statistical deformable model (1.5), where is the unknown perturbation mean to estimate, and are i.i.d. random vectors in with zero mean. Nevertheless, there exists major differences between our approach and the one in [Goo91]. First, in model (1.5), the deformations parameters are assumed to be random variables following an unknown distribution, whereas they are just nuisance parameters in model (1.6) for shape analysis, see [Goo91, KM97]. In some applications (e.g. in biomedical imaging [JDJG04]), it is of interest to reconstruct the unobserved parameters and to estimate their distribution. One of the main contribution of this paper is then to construct upper and lower bounds for the estimation of such deformation parameters. Moreover, in model (1.5), they are too additive error terms, whereas the model (1.6) only include the error term . In model (1.5), the is an additive noise modeling the errors in the measurements, while the ’s model (possibly smooth) variations in intensity of the individuals around the mean pattern .

In [KM97], the authors studied the relationship between isotropicity of the additive noise and the convergence of Procrustean procedures to the perturbation mean as . It is shown in [KM97] that, for isotropic errors, Procrustean means are consistent, but that, for non-isotropic errors, they may not converge to . For a recent discussion on the issues of consistency of sample Procrustes means in perturbation models and extension to non-metrical Fréchet means, we refer to [Huc10] and [Huc11]. In this paper, we carefully analyze the role of the dimension and the number of samples on the consistency of Procrustean means in model (1.5). To obtain consistent procedures, we show that it is not required to impose very restrictive conditions on the error terms such as isotropicity for the in (1.6) for shape analysis. Here, the key quantity is the dimension of the data (number of design points) which plays the central role to guarantee the converge of our estimators. This point is another major difference with the approach of statistical shape analysis [Goo91] that does not take into account the dimensionality of the shape space to analyze the consistency of Procrustean estimators.

Note that a subclass of the deformable model (1.5) is the so-called shape invariant model (SIM)

| (1.7) |

i.e. without incorporating in (1.5) the additive terms .

The goal of this paper is twofold. First, we propose a general methodology for estimating and the ’s based on observations coming from model (1.5). For this purpose, we show that an appropriate tool is the notion of sample Fréchet mean of a data set [Fré48, Zie77, BP03] that has been widely studied in shape analysis [Goo91, KM97, Le98, LK00, Huc10] and more recently in biomedical imaging [JDJG04, Pen06]. Secondly, we study the consistency of the resulting estimators in various asymptotic settings: either when and both tend to infinity, or when is fixed and , or when is fixed and .

1.2 Organization of the paper

Section 2 contains a description of our estimating procedure and a review of previous work in mean pattern estimation. In Section 3, we derive a lower bound for the quadratic risk of estimators of the deformation parameters. In Section 4, we discuss some identifiability issues in model (1.5). In Section 5 we derive consistency results for the Fréchet mean in the case (1.2) of randomly shifted curves. In Section 6 and Section 7, we give general conditions to extend these results to the more general deformable model (1.5). Section 8 contains some numerical experiments. A small conclusion with some perspectives are given in Section 9. All proofs are postponed to a technical Appendix.

2 The estimating procedure

2.1 A dissimilarity measure based on deformation operators

To define a notion of sample Fréchet mean for curves or images, let us suppose that the family of deformation operators is invertible in the sense that there exists a family of operators such that for any

Then, for two functions introduce the following dissimilarity measure

If then there exists such that meaning that the functions and are equal up to a geometric deformation. Note that is not necessarily a distance on , but it can be used to define a notion of sample Fréchet mean of data from model (1.5). For this purpose let denote a subspace of and suppose that are smooth functions in obtained from the data , for , see Section 5.2 and Section 6.2 for precise definitions. Following the definition of a Fréchet mean in general metric space [Fré48], define an estimator of the mean pattern as

| (2.1) |

Note that falls into the category of non-metrical sample Fréchet means whose definitions and asymptotic properties are discussed in [Huc10] for random variables belonging to Riemannian manifolds. However, unlike the usual approach in shape analysis, the Fréchet mean (2.1) is based on smoothed data. In what follows, we show that smoothing is a key preliminary step to obtain the convergence of to the mean pattern in the deformable model (1.5). It can be easily shown that the computation of can be done in two steps: first minimize the following criterion

| (2.2) |

where

| (2.3) |

which gives an estimation of the deformation parameters , and then in a second step take

| (2.4) |

as an estimator of the mean pattern .

2.2 Previous work in mean pattern estimation and geometric variability analysis

Estimating the mean pattern of a set of curves that differ by a time transformation is usually referred to as the curves registration problem, see e.g. [GK92, Big06, RL01, WG97, LM04]. However, in these papers, studying consistent estimators of the mean pattern as the number of curves and design points tend to infinity is not considered. For the SIM (1.7), a semiparametric point of view has been proposed in [GLM07] and [Vim10] to estimate non-random deformation parameters (such as shifts and amplitudes) as the number of observations per curve grows, but with a fixed number of curves. A generalisation of this semiparametric approach for two-dimensional images is proposed in [BGV09]. The case of image deformations by a Lie group action is also investigated in [BLV10] from a semiparametric point of view using a SIM.

In the simplest case of randomly shifted curves in a SIM, [BG10] have studied minimax estimation of the mean pattern by letting only the number of curves going to infinity. Self-modelling regression (SEMOR) methods proposed by [KG88] are semiparametric models where each observed curve is a parametric transformation of the same regression function. However, the SEMOR approach does not incorporate a random fluctuations in intensity of the individuals around a mean pattern through an unknown process as in model (1.5). The authors in [KG88] studied the consistency of the SEMOR approach using a Procrustean algorithm. Recently, there has also been a growing interest on the development of statistical deformable models for image analysis and the construction of consistent estimators of a mean pattern, see [GM01, BGV09, BGL09, AAT07, AKT09].

3 Lower bounds for the estimation of the deformation parameters

In this section, we derive non-asymptotic lower bounds for the quadratic risk of an arbitrary estimator of the deformation parameters under the following smoothness assumption of the mapping .

Assumption 3.1.

For all , is a linear operator such that the function exists and belongs to for any . Moreover, there exists a constant such that

for all and .

3.1 Shape Invariant Model

Theorem 3.1.

The lower bound given in inequality (3.1) does not decrease as increases. Thus, if the number of design points is fixed, increasing the number of curves (or images) does not improve the quality of the estimation of the deformation parameters for any estimator . Nevertheless, this lower bound is going to 0 as the dimension .

3.2 General model

The main difference between the general model (1.5) and the SIM (1.7) is the extra error terms , . In what follows, denotes expectation conditionally to . Since the random processes ’s are observed through the action of the random deformation operators it is necessary to specify how the ’s modify the law of the process .

Assumption 3.2.

There exists a positive semi-definite symmetric matrix such that the covariance matrix of satisfies .

This assumption means that the law of the random process is somewhat invariant by the deformation operators . Such an hypothesis is similar to the condition given in [KM97] to ensure consistency of Fréchet mean estimators in Kendall’s shape space using model similar to (1.5) with . After a normalization step, the deformations considered in [KM97] are rotations of the plane, and the authors in [KM97] study the case where the law of the error term is isotropic, that is to say, invariant by the action of rotations.

Theorem 3.2.

Consider the general model (1.5). Suppose that Assumption 3.1 and 3.2 hold. Assume that the density satisfies Assumption 1.1 and that . Let be any estimator (a measurable function of the data) of . Then, for any and , we have

| (3.2) |

where is the constant defined in Assumption 3.1, and denotes the smallest eigenvalue of .

3.3 Application to the shifted curves model

Consider the shifted curves model (1.2) with an equi-spaced design, namely

| (3.3) |

Theorem 3.3.

Consider the model (3.3). Assume that is continuously differentiable on and that is a centered stationary process with value in . Suppose that with and . Let be any estimator of the true random shifts , i.e. a measurable function of the data in model (3.3). Then, for any and

| (3.4) |

where with denoting the first derivative of .

4 Identifiability conditions

4.1 The shifted curves model

Without any further assumptions, the randomly shifted curves model (3.3) is not identifiable. Indeed, if satisfies , , then replacing by and by does not change the formulation of model (3.3). Choosing identifiability conditions amounts to impose constraints on the minimization of the criterion

| (4.1) |

for , which can be interpreted as a version without noise of the criterion (2.2) using the ideal smoothers . Obviously, the criterion has a minimum at such that , but this minimizer of on is clearly not unique. If the true shifts are supposed to have zero mean (i.e. ) it is natural to introduce the constrained set

| (4.2) |

It is shown in [BG10] Lemma 6, that if is such that and if (recall that ), then the criterion has a unique minimum on in the sense that for all with where

| (4.3) |

Under such assumptions, we will compute estimators of the random shifts by minimizing the criterion (2.2) over the constrained set and not directly on . Consistency of such constrained estimators will then be studied under the following identifiability conditions:

Assumption 4.1.

The mean pattern is such that .

Assumption 4.2.

The support of the density is included in for some and is such that .

Under such assumptions, can be bounded from below by the quadratic function which will be an important property to derive consistent estimators.

Proposition 4.1.

Assumption 4.2 and the condition that in Proposition 4.1 mean that the support of the density of the shifts is sufficiently small, and that the shifted curves are in some sense concentrated around the mean pattern . Such an assumption of concentration of the data around the same mean pattern has been used in various papers to prove the uniqueness and the consistency of Fréchet means for random variables lying in a Riemannian manifold, see [Kar77, Le98, BP03, Afs11, Ken90].

4.2 The general case

In the case of general deformation operators, define for the criterion

| (4.4) |

Obviously, using that for all , , the criterion has a minimum at such that . However, without any further restrictions the minimizer of is not necessarily unique on .

Assumption 4.3.

Let such that there exists a unique satisfying .

Then, is the set onto which we will carry the minimization of the criterion (2.3). In the case of shifted curves and under Assumption 4.1 and 4.2, the only set onto which the criterion vanishes is the line where . An easy way to choose the set is to take a linear subset of , see Figure 1 for an illustration. By considering the subset

where is the orthogonal of in , then Assumption 4.3 is satisfied with given in (4.3). More generally, if the deformation parameters , are supposed to be random variables with zero mean, then optimizing on is a natural choice. Another identifiability condition for shifted curves is proposed in [GLM07] and [Vim10] by taking

| (4.5) |

where . In this case, . Choosing to minimize on amounts to choose the first curve as a reference onto which all the others curves are aligned, meaning that the first shift is not random, see Figure 1.

Following the classical guidelines in M-estimation (see e.g. [vdV98]), a necessary condition to ensure the convergence of M -estimators such as (2.2) is that the local minima of over are well separated from the global minimum of at (satisfying ). The following assumption can be interpreted in this sense.

Assumption 4.4.

For all we have

| (4.6) |

for a constant independent of .

5 Consistent estimation in the shifted curves model

In this section, we give conditions to ensure consistency of the estimators defined in Section 2 in the shifted curves model (3.3) with an equi-spaced design.

5.1 The random perturbations

Following the assummtions of Theorem 3.3, will be supposed to be a stationary process with covariance function . The law of is thus invariant by the action of a shift. Conditionally to , the covariance of the vector is a Toeplitz matrix equals to

| (5.1) |

Let be the largest eigenvalue of the matrix . It follows from standard results on Toeplitz matrices (see e.g. [HJ90]) that

| (5.2) |

where is a positive constant independent of representing an upper bound of the variance of .

5.2 Choice of the smoothed estimators

A convenient choice for the smoothing of the observed curves in (3.3) is to do low-pass Fourier filtering. Let (assuming for simplicity that is odd), and define for a spectral cut-off parameter and the linear estimators

| (5.3) |

Then, define the Sobolev ball of radius and regularity as

| (5.4) |

with , for a function , and take as the smoothness class to which the mean pattern is supposed to belong.

5.3 Consistent estimation of the random shifts

Using low-pass filtering, and following the discussion in Section 4.1 on identifiability issues, the estimators of the random shifts are given by

| (5.5) |

where the criterion for is

and is the constrained set defined in (4.2).

Theorem 5.1.

First, remark that for fixed values of and , then . The term depends on the spectral cutoff via the bias and the variance of the estimators . By choosing a sequence such that and (tradeoff between low variance and low bias) it follows that for fixed and , then However, if remains fixed, then

Thus, Theorem 5.1 is consistent with the conclusions of Theorem 3.3, that is, if is fixed, then it is not possible to estimate by letting only grows to infinity. Hence, under the assumptions of Theorem 5.1, one can only prove the convergence in probability of to the true shifts by taking the double asymptotic and , provided the smoothing parameter is well chosen.

5.4 Consistent estimation of the mean pattern

In the case of randomly shifted curves, the Fréchet mean estimator (2.1) of is .

Theorem 5.2.

Similar comments to those made on the consistency of the estimators of the shifts can be made. A double asymptotic in and is needed to show that the Fréchet mean converges in probability to the true mean pattern . Moreover, if is too large (e.g. such that , which correspond to undersmoothing), then Theorem 5.2 cannot be used to prove that converges to in probability. This illustrates the fact that, to achieve consistency, a sufficient amount of pre-smoothing is necessary before computing the Fréchet mean (2.1).

5.5 A lower bound for the Fréchet mean

From the results of Theorem 3.3, it is expected that the Fréchet mean does not converge to in the setting fixed and . To support this argument, consider the following ideal estimator

| (5.6) |

where . This corresponds to the case of an ideal smoothing step from the data (3.3) that would yield for all . Obviously, is not an estimator since it depends on the unobserved quantities and , but we can consider it as a benchmark to analyse the converge of the Fréchet mean to .

Theorem 5.3.

Suppose that the assumptions of Theorem 3.3 are satisfied with . Then, for any , there exists such that implies

| (5.7) |

where the constant depends on and .

Hence, in the setting fixed and , even the ideal estimator does not converge to for the expected quadratic risk. This illustrates the central role played by the dimension of the data to obtain consistent estimators.

6 Notations and main assumptions in the general case

6.1 Smoothness of the mean pattern and the deformation operators

In this part, the notation is used to denote either or their inverse .

Assumption 6.1.

For all , is a linear operator satisfying for all . There exists a constant such that for any and

and a constant such that for any and ,

Assumption 6.1 can be interpreted as a Lipschitz condition on the mapping . The first inequality, that is , means that the action of the operator does not change too much the norm of when varies in . Such an assumption on and its inverse forces the optimization problem (2.2) to have non trivial solutions by avoiding the functional in (2.3) being arbitrarily small. It can be easily checked that Assumption 6.1 is satisfied in the case (1.2) of shifted curves with and .

6.2 The preliminary smoothing step

For the ’s are supposed to belong to the class of linear estimators in the sense of the following definition:

Definition 6.1.

Let denote either or (set of smoothing parameters). To every is associated a non-random vector valued function such that for all and all

where denotes the standard inner product in and .

Assumption 6.2.

For all and all , the function belong to , where denotes the -th component of the vector . Moreover, for all , and , the function belongs to where .

In the case (1.2) of randomly shifted curves with an equi-spaced design, then Assumption 6.2 holds with Let us now specify how the bias/variance behavior of the linear estimators depends on the smoothing parameter . For this, consider for some function the following regression model

where the ’s are i.i.d normal variables with zero mean and variance 1. The performances of a linear estimator , where , can be evaluated in term of the expected quadratic risk defined by

where and denote the usual bias and variance of given by and for where . Define also and let us make the following assumption on the asymptotic behavior of the bias/variance of :

Assumption 6.3.

There exist a constant and a real-valued function , such that for all ,

Moreover there exists a sequence of smoothing parameters with such that

Let us illustrate Assumption 6.3 in the case of shifted curves with an equi-spaced design, and a smoothing step obtained by low-pass Fourier filtering. As in Section 5, take defined in (5.4). In this setting, . It can be also checked that for some positive constant depending only on , and . Thus, Assumption 6.3 holds with .

6.3 Random perturbation of the mean pattern by the ’s

Assumption 6.4.

For any , there exists a real such that for any

where , and denotes the largest eigenvalue of a symmetric matrix . Moreover,

| (6.1) |

where is the variance defined in Assumption 6.3.

Intuitively, the condition (6.1) means that the variance of the linear smoother has to be asymptotically smaller that the maximal correlations (measured by ) between and for and all . In the case of randomly shifted curves with an equi-spaced design, a simple condition for which Assumption 6.4 holds is the case where is stationary process (see the arguments in Section 5.1).

7 Consistency in the general case

7.1 Consistent estimation of the deformation parameters

Consider for the following estimator of the deformation parameters

where

| (7.1) |

and is the constrained set introduced in Assumption 4.3. The estimator thus depends on the choice of , and it will be shown that is a consistent estimator of the vector defined in Assumption 4.3. Note that depending on the problem at hand and the choice of the constrained set , it can be shown that is close to the true deformation parameters . For example, in the case of shifted curves, if defined in (4.2) and if the density of the shifts has zero mean, then with can be shown to be close to (see Lemma C.1 in the Appendix). This allows to show the consistency of to as formulated in Theorem 5.1. Therefore, the next result only bounds the distance between and .

Theorem 7.1.

Using Assumptions 6.3 and 6.4, it follows that for any and . If remains fixed, Theorem 7.1 thus implies that converges in probability to as . To the contrary, let us fix , and consider an asymptotic setting where only . For any and , Therefore, Theorem 7.1 cannot be used to prove that converges to as . This confirms that is not a consistent estimator of (and thus of ) as remains fixed and tends to infinity.

7.2 Consistent estimation of the mean pattern

Recall that the estimator of the mean pattern is defined as We study the consistency of with respect to the shape function

defined for . Again, depending on the problem at hand and the choice of the constrained set , it can be shown that is close to the true mean pattern . For example, in the case of shifted curves with defined in (4.2), then with . In this case Hence, under the condition that , then for sufficiently large, and thus is close to which allows to show the consistency of to as formulated in Theorem 5.2.

Theorem 7.2.

The consistency of to is thus guaranteed when goes to infinity provided the level of smoothing is chosen so that . Again, if remains fixed and only is let going to infinity then Theorem 7.2 cannot be used to prove the convergence of to .

8 Numerical experiments for randomly shifted curves

Consider the model (3.3) with random shifts having a uniform density with compact support equal to , and for as a mean pattern, see Figure 2. For the constrained set we took

We use Fourier low pass filtering with spectral cut-off to which is reasonable value to reconstruct representing a good tradeoff between bias and variance. We present some results of simulations under various assumptions of the process and the level of additive noise in the measurements.

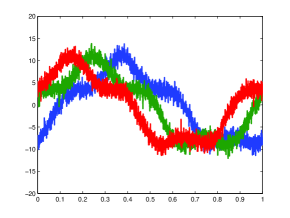

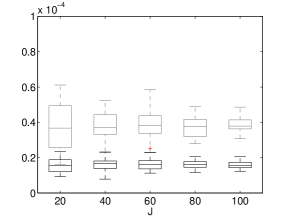

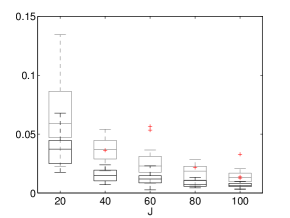

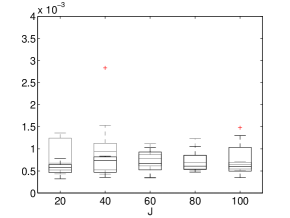

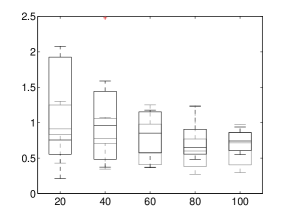

Shape invariant model (SIM). The first numerical applications illustrate the role of and in the SIM model. Figure 2 gives a sample of the data used with . The factors in the simulations are the number of curves and the number of design points . For each combination of these two factors, we simulate repetitions of model (3.3). For each repetition we computed and . Boxplot of these quantities are displayed in Figure 3 and 3 respectively, for and (in gray) and (in black). As the smoothing parameter is fixed to , increasing simply reduces the variance of the linear smoothers . Recall that the lower bound given in Theorem 3.3 shows that does not decrease as increases but should be smaller when the number of point increases. This is exactly what we observe in Figure 3. Similarly, the quantity is clearly smaller with than with .

Complete model. We now add the terms in (3.3) to model linear variations in amplitude of the curves around the template . First, we generate a stationary periodic Gaussian process. To do this, the covariance matrix must be a particular Toeplitz matrix. As suggested in [Gre93] one possibility is to choose

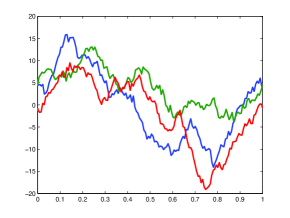

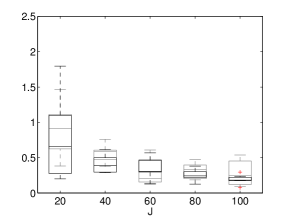

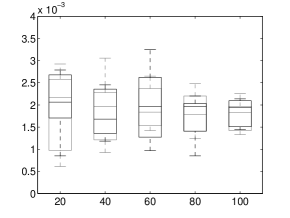

where is a strictly positive parameter (we took ) and a variance parameter. The level of additive noise is , and we took . As an illustration, in Figure 2 we plot , with . Over repetitions, we have computed the values of and for is varying from to and . The results are displayed in Figure 4 and 4. We observe the same behaviors than in the simulations with the SIM model: the variance of does not decrease as increases (see Figure 4) and has a smaller mean and variance as increases.

We finally run the same simulations with a non stationary noise where is a positive periodic smooth deterministic function such that and with . Note that, in this case, the sequence is of order and Assumption 6.4 is not verified. The levels of noise ( and ) are the same than in the stationary case in order to make things comparable. The results are presented in the same manner in Figure 5 for and in Figure 5 for . One can see that the results are very different. The estimators of the shifts have a much larger mean and variance, and the variance of remains rather high even when or increases (see Figure 5). The convergence to zero of which was clear in the stationary case, is now not so obvious in view of the numerical results displayed in Figure 5.

9 Conclusion and perspectives

We have proposed to use a Fréchet mean of smoothed data to estimate a mean pattern of curves or images satisfying a non-parametric regression model including random deformations. Upper and lower bounds (in probability and expectation) for the estimation of the deformation parameters and the mean pattern have been derived. Our main result is that these bounds go to zero as the dimension of the data (the number of sample points) goes to infinity, but that an asymptotic setting only in (the number of observed curves or images) is not sufficient to obtain consistent estimators. An interesting topic for future investigation would be to study the rate of convergence of such estimators and to analyze their optimality (e.g. from a minimax point of view).

Appendix A Proof of the results in Section 3

A.1 Proof of Theorem 3.1

Write , and let be the column vector of the observations generated by model (1.7). Conditionally to , is a Gaussian vector and its log-likelihood is equal to

| (A.1) |

where . Therefore, we have the expected score for all and and

| (A.2) |

where . Then, for each and we have

| (A.3) |

where the last inequality is a consequence of Assumption 3.1. From now on, is an arbitrary estimator (i.e any measurable function of ) of the true parameter . Let also

be a matrix of column vectors of . Then, Cauchy-Schwarz inequality implies

| (A.4) |

In the sequel we note . We have

Assumption 1.1 and the differentiability of imply that for all and all we have . Then, an integration by part and Fubini’s theorem give . Again, with the same arguments, and thus

A.2 Proof of Theorem 3.2

As above, let is the column vector generated by model (1.5). Then, conditionally to , is a Gaussian vectors and Assumption 3.2 ensures that its log-likelihood has the same expression as in equation (A.1) but with

As the matrix is positive semi definite with it smallest eigenvalue denoted by (see Assumption 3.2), the uniform bound (A.3) becomes

for all and . As above the last inequality is a consequence of Assumption 3.1 and the rest of the proof is identical to the proof of Theorem 3.1.

A.3 Proof of Theorem 3.3

For all the operators are isometric from to as a change of variable implies immediately that . For all continuously differentiable function , we have where is the sign function. Then, for all , and Assumption 3.1 is satisfied with . Finally, as the error terms ’s are i.i.d stationary random process the covariance function is invariant by the action of the shifts and Assumption 3.2 is satisfied with defined in (5.1) (see Section 5.1 for further details). Then, the result of Theorem 3.3 follows as an application of Theorem 3.2.

Appendix B Proof of the results in Section 4

B.1 Proof of Proposition 4.1

Remark that where . Thanks to Assumption 4.1, it follows that for any ,

| (B.1) |

with . Then, remark that

Using a second order Taylor expansion and the mean value theorem, one has that for any real such that with . Therefore, the above equality implies that for any

since for all by Assumption 4.2 and the hypothesis that . Hence, using the lower bound (B.1), it follows that for all

| (B.2) |

with . Now assume that . Using the properties that and , it follows from elementary algebra that This equality together with the lower bound (B.2) completes the proof.

Appendix C Proof of the results in Section 5

C.1 Proof of Theorem 5.1

Let us state the following lemma which is direct consequence of Bernstein’s inequality for bounded random variables (see e.g. Proposition 2.9 in [Mas07]):

Lemma C.1.

Suppose that Assumption 4.2 holds. Then, for any

Using the inequality , it follows that Theorem 5.1 is a consequence of Lemma C.1 and Theorem 7.1. Indeed, it can be easily checked that, under the assumptions of Theorem 5.1, Assumptions 6.1 to 6.4 are satisfied in the case of randomly shifted curves with an equi-spaced design and low-pass Fourier filtering, see the various arguments given in Section 6). The identifiability condition of Assumption 4.4 is given by Proposition 4.1.

C.2 Proof of Theorem 5.2

Consider the following inequality where and . As is assumed to be in , there exists a constant such that . As explained in part C.1 the assumptions of Theorem 5.2 are satisfied in the case of randomly shifted curves with an equi-spaced design and low-pass Fourier filtering. The result then follows from Theorem 7.2.

C.3 Proof of Theorem 5.3

Let . We have that

| (C.1) |

where for all , and , with . In the rest of the proof, we show that is bounded from below by a quantity independent of (this statement is made precise later) and that goes to zero as goes to infinity. Then, these two facts imply that there exists a such that implies that which will yield the desired result.

Lower bound on .

Recall that , then

where , the right hand side of the preceding inequality being positive since Assumption 4.2 ensures that for all . Let . Since and (by our assumption on ), Lemma E.1 implies that

| (C.2) |

Now, remark that with . By applying Theorem 3.3 we get that

Then, remark that . Hence tends to 0 as goes to infinity. Therefore, using equation (C.2), it follows that there exists and such that implies that

| (C.3) |

Upper bound on .

Appendix D Proof of the results in Section 7

D.1 Proof of Theorem 7.1

We explain here the main arguments of the proof of Theorem 7.1. Technical Lemmas are given in the second part of the Appendix. Let and decompose the criterion (7.1) as follows,

where the terms and are due to the smoothing, namely,

and the others terms contain the ’s and ’s error terms. Let and , then

At this stage, recall that and The proof follows a classical guideline in M-estimation: we show that the uniform (over ) convergence in probability of the criterion to , yielding the convergence in probability of their argmins and respectively. Assumption 4.4 ensures that there is a constant such that,

| (D.1) |

Then, a classical inequality in M-estimation and the decomposition of given above yield

| (D.2) | ||||

The rest of the proof is devoted to control the and terms.

Control of .

Control of .

We give a control in probability of the stochastic quadratic term and . As previously, one can show that there is a constant such that,

where we have used the inequality , valid for any to control the term . The quadratic terms and are controlled by Corollaries E.1 and E.2 respectively. It yields immediately to

| (D.4) |

where .

D.2 Proof of Theorem 7.2

In this part, we use the notations introduced in the proof of Theorem 7.1. We have,

Again, the first term above depends on the bias, and the second term (stochastic) can be controlled in probability. Under Assumptions 6.1 and 6.3 we have that

and

The stochastic term in the above inequality can be been controlled using Lemma E.2 and the arguments in the proof of Corollaries E.1 and E.2 to obtain that for any

Then, from Theorem 7.1 it follows that

which completes the proof.

Appendix E Technical Lemmas

Lemma E.1.

Let such that with for some for all . Then, there exists a constant such that where .

Proof.

Let . A Taylor expansion implies that there exits , such that

holds for all . Now, since it follows that

Since , we have that which finally implies that which proves the result by letting since . ∎

Lemma E.2.

Let , where and the ’s are nonrandom non-negative symmetric matrices. Then, for all and all ,

where with being the -th eigenvalue of the matrix .

Proof.

Some parts of the proof follows the arguments in [BM98] (Lemma 8, part 7.6). We have

where with . Now, denote by the eigenvalues of with and . We can write and is positive semi-definite. Then, let Let , by Markov’s inequality it follows that for all , since the ’s are independent. The log-Laplace transform of is We now use the inequality for all which holds since . This implies that where . Finally, we have

| (E.1) |

where . The right hand side of the above inequality achieves its minimum at . Evaluating (E.1) at this point and using the inequality , valid for all , one has that

by setting . We derive the following concentration inequality for , To finish the proof, remark that since all the ’s are positive. ∎

Proof.

Proof.

Assumption 6.1 gives the uniform bound

Hence, conditionally on we have that where is defined in Lemma E.2 with . Let us now give an upper bound on the largest eigenvalues of the matrices with . Under Assumption 6.4 we have that , for all and any . Thus, the result follows by arguing as in the proof of Lemma E.2 and by taking expectation with respect to . ∎

References

- [AAT07] S. Allassonière, Y. Amit, and A. Trouvé. Toward a coherent statistical framework for dense deformable template estimation. Journal of the Statistical Royal Society (B), 69:3–29, 2007.

- [Afs11] Bijan Afsari. Riemannian center of mass: existence, uniqueness, and convexity. Proceedings of the American Mathematical Society, 139(2):655–673, 2011.

- [AKT09] S. Allassonière, E. Kuhn, and A. Trouvé. Bayesian deformable models building via stochastic approximation algorithm: a convergence study. Bernoulli, To be published, 2009.

- [BG10] J. Bigot and S. Gadat. A deconvolution approach to estimation of a common shape in a shifted curves model. Annals of statistics, to be published, 2010.

- [BGL09] J. Bigot, S. Gadat, and J.-M. Loubes. Statistical M-estimation and consistency in large deformable models for image warping. J. Math. Imaging Vision, 34(3):270–290, 2009.

- [BGV09] J. Bigot, F. Gamboa, and M. Vimond. Estimation of translation, rotation and scaling between noisy images using the fourier mellin transform. SIAM Journal on Imaging Sciences, 2(2):614–645, 2009.

- [Big06] J. Bigot. Landmark-based registration of curves via the continuous wavelet transform. Journal of Computational and Graphical Statistics, 15(3):542–564, 2006.

- [BLV10] J. Bigot, J.-M. Loubes, and M. Vimond. Semiparametric estimation of shifts on compact lie groups for image registration. Probability Theory and Related Fields, to be published, 2010.

- [BM98] L. Birgé and P. Massart. Minimum contrast estimators on sieves: exponential bounds and rates of convergence. Bernoulli, 4(3):329–375, 1998.

- [BP03] R. Bhattacharya and V. Patrangenaru. Large sample theory of intrinsic and extrinsic sample means on manifolds (i). Annals of statistics, 31(1):1–29, 2003.

- [BP05] R. Bhattacharya and V. Patrangenaru. Large sample theory of intrinsic and extrinsic sample means on manifolds (ii). Annals of statistics, 33:1225–1259, 2005.

- [DM98] I. L. Dryden and K. V. Mardia. Statistical shape analysis. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons Ltd., Chichester, 1998.

- [Fré48] M. Fréchet. Les éléments aléatoires de nature quelconque dans un espace distancié. Ann. Inst. H.Poincaré, Sect. B, Prob. et Stat., 10:235–310, 1948.

- [GK92] T. Gasser and A. Kneip. Statistical tools to analyze data representing a sample of curves. Annals of Statistics, 20(3):1266–1305, 1992.

- [GL95] R. D. Gill and B. Y. Levit. Applications of the Van Trees inequality: a Bayesian Cramér-Rao bound. Bernoulli, 1(1-2):59–79, 1995.

- [GLM07] F. Gamboa, J.-M. Loubes, and E. Maza. Semi-parametric estimation of shifts. Electron. J. Stat., 1:616–640, 2007.

- [GM01] C. A. Glasbey and K. V. Mardia. A penalized likelihood approach to image warping. J. R. Stat. Soc. Ser. B Stat. Methodol., 63(3):465–514, 2001.

- [GM07] U. Grenander and M. Miller. Pattern Theory: From Representation to Inference. Oxford Univ. Press, Oxford, 2007.

- [Goo91] C. Goodall. Procrustes methods in the statistical analysis of shape. J. Roy. Statist. Soc. Ser. B, 53(2):285–339, 1991.

- [Gre93] U. Grenander. General pattern theory - A mathematical study of regular structures. Clarendon Press, Oxford, 1993.

- [Hel01] S. Helgason. Differential geometry, Lie groups, and symmetric spaces, volume 34 of Graduate Studies in Mathematics. American Mathematical Society, Providence, RI, 2001.

- [HHM10a] S. Huckemann, T. Hotz, and A. Munk. Intrinsic manova for riemannian manifolds with an application to kendalls spaces of planar shapes. IEEE Trans. Patt. Anal. Mach. Intell. Special Section on Shape Analysis and its Applications in Image Understanding, 32(4):593–603, 2010.

- [HHM10b] S. Huckemann, T. Hotz, and A. Munk. Intrinsic shape analysis: Geodesic principal component analysis for riemannian manifolds modulo lie group actions. discussion paper with rejoinder. Statistica Sinica, 20:1–100, 2010.

- [HJ90] R.A. Horn and C.R. Johnson. Matrix analysis. Cambridge University Press, Cambridge, 1990.

- [Huc10] S Huckemann. Inference on 3d procrustes means: Tree bole growth, rank deficient diffusion tensors and perturbation models. Scand. J. Statist., To appear, 2010.

- [Huc11] S Huckemann. Intrinsic inference on the mean geodesic of planar shapes and tree discrimination by leaf growth. Ann. Statist., 39(2):1098–1124, 2011.

- [JDJG04] S. Joshi, B. Davis, B. Jomier, and Guido G. Unbiased diffeomorphic atlas construction for computational anatomy. Neuroimage, 23:151–160, 2004.

- [Kar77] H. Karcher. Riemannian center of mass and mollifier smoothing. Comm. Pure Appl. Math., 30(5):509–541, 1977.

- [KBCL99] D. G. Kendall, D. Barden, T. K. Carne, and H. Le. Shape and shape theory. Wiley Series in Probability and Statistics. John Wiley & Sons Ltd., Chichester, 1999.

- [Ken84] D.G. Kendall. Shape manifolds, procrustean metrics, and complex projective spaces. Bull. London Math Soc., 16:81–121, 1984.

- [Ken90] W.S. Kendall. Probability, convexity and harmonic maps with small image i: uniqueness and fine existence. Proc. London Math. Soc., 3(61):371–406, 1990.

- [KG88] A. Kneip and T. Gasser. Convergence and consistency results for self-modelling regression. Annals of Statistics, 16:82–112, 1988.

- [KM97] J. T. Kent and K. V. Mardia. Consistency of Procrustes estimators. J. Roy. Statist. Soc. Ser. B, 59(1):281–290, 1997.

- [Le98] H. Le. On the consitency of procrustean mean shapes. Advances in Applied Probability, 30:53–63, 1998.

- [LK00] H. Le and A. Kume. The fréchet mean shape and the shape of the means. Advances in Applied Probability, 32:101–113, 2000.

- [LM04] X. Liu and H.G. Muller. Functional convex averaging and synchronization for time-warped random curves. Journal of the American Statistical Association, 99(467):687–699, 2004.

- [Mas07] P. Massart. Concentration inequalities and model selection, volume 1896 of Lecture Notes in Mathematics. Springer, Berlin, 2007.

- [MY01] M. I. Miller and L. Younes. Group actions, homeomorphisms, and matching: A general framework. International Journal of Computer Vision, 41:61–84, 2001.

- [OC95] J. M. Oller and J. M. Corcuera. Intrinsic analysis of statistical estimation. Ann. Statist., 23(5):1562–1581, 1995.

- [Pen06] X. Pennec. Intrinsic statistics on riemannian manifolds: Basic tools for geometric measurements. J. Math. Imaging Vis., 25:127–154, July 2006.

- [RL01] J.O. Ramsay and X. Li. Curve registration. Journal of the Royal Statistical Society (B), 63:243–259, 2001.

- [Røn01] B. B. Rønn. Nonparametric maximum likelihood estimation for shifted curves. J. R. Stat. Soc. Ser. B Stat. Methodol., 63(2):243–259, 2001.

- [TIR10] T. Trigano, U. Isserles, and Y. Ritov. Semiparametric curve alignment and shift density estimation for biological data. Preprint, 2010.

- [TY05] A. Trouvé and L. Younes. Metamorphoses through lie group action. Foundations of Computational Mathematics, 5(2):173–198, 2005.

- [vdV98] A. W. van der Vaart. Asymptotic statistics, volume 3 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 1998.

- [Vim10] M. Vimond. Efficient estimation for a subclass of shape invariant models. Annals of statistics, 38(3):1885–1912, 2010.

- [WG97] K. Wang and T. Gasser. Alignment of curves by dynamic time warping. Annals of Statistics, 25(3):1251–1276, 1997.

- [Zie77] H. Ziezold. On expected figures and a strong law of large numbers for random elements in quasi-metric spaces. In Transactions of the Seventh Prague Conference on Information Theory, Statistical Decision Functions, Random Processes and of the Eighth European Meeting of Statisticians (Tech. Univ. Prague, Prague, 1974), Vol. A, pages 591–602. Reidel, Dordrecht, 1977.