How sensitive are equilibrium pricing models to real-world distortions?

HARBIR LAMBA111Department of Mathematical Sciences, George Mason University, MS 3F2, 4400 University Drive, Fairfax, VA 22030 USA

Abstract

In both finance and economics, quantitative models are usually studied as isolated mathematical objects — most often defined by very strong simplifying assumptions concerning rationality, efficiency and the existence of disequilibrium adjustment mechanisms. This raises the important question of how sensitive such models might be to real-world effects that violate the assumptions.

We show how the consequences of rational behavior caused by perverse incentives, as well as various irrational tendencies identified by behavioral economists, can be systematically and consistently introduced into an agent-based model for a financial asset. This generates a class of models which, in the special case where such effects are absent, reduces to geometric Brownian motion — the usual equilibrium pricing model. Thus we are able to numerically perturb a widely-used equilibrium pricing model market and investigate its stability.

The magnitude of such perturbations in real markets can be estimated and the simulations imply that this is far outside the stability region of the equilibrium solution, which is no longer observed. Indeed the price fluctuations generated by endogenous dynamics, are in good general agreement with the excess kurtosis and heteroskedasticity of actual asset prices.

The methodology is presented within the context of a financial market. However, there are close links to concepts and theories from both micro- and macro-economics including rational expectations, Soros’ theory of reflexivity, and Minsky’s theory of financial instability.

JEL Classification: C62; D01; D03; D53;

Keywords: Instability; Non-equilibrium dynamics

1 Introduction

All of the mainstream schools of economic thought and, in turn, modern finance have been strongly motivated by the mathematical elegance and predictive success of Newtonian mechanics and statistical physics. This has resulted in mathematical models constructed so that the solution is a unique, stable, equilibrium whose value is both history-independent and a continuous function of the system variables.

The notion of equilibrium is close to being a unifying concept in modern economics (see Setterfield (1997); Kaldor (1972)) although its precise meaning is contextual. Here we shall take it to mean the absence (or complete cancellation) of endogenous dynamics so that the state of the system is determined solely by the current values of exogenous variables and not, say, on any prior state of the system. This is certainly the case for gas molecules in a closed box that are reacting to slow changes in temperature — the pressure is determined by the Ideal Gas Law and the current temperature. This happy state of affairs is guaranteed by the Laws of Thermodynamics that provide both a unique statistical equilibrium and a physical mechanism for reaching it.

One may speculate on what would happen if there was a special type of molecule that did not obey the First and Second Laws of Thermodynamics (Conservation of Energy and Increasing Entropy respectively). These particles can spontaneously speed up or slow down, reveal a temporary preference for one side of the box over the other, or imitate the particles close to them. One may then wonder which of these two types of molecule has more in common with agents in an economic system.

Economic systems are aggregations of many heterogeneous agents and the a priori requirement of history-independent equilibrium solutions has profound consequences (see Kirman (1992)). Most models are generated by assuming that agents display enough homogeneity to be ‘averaged’ or scaled-up and so replaced by a representative agent who is memoryless and is both perfectly rational (usually in the sense of maximizing some hypothetical utility function) and correct about future expectations. This averaging procedure, when applied to expectations, is known as the Rational Expectations Hypothesis and implies that while individual agents’ expectations may be wrong they all use all available information and, on average, agree with the expectations assumption being used with no systematic deviations. 222Such averaging assumptions are the economic analogue of the Central Limit Theorem which states that the average of independent random variables (from a distribution with finite mean and variance) is normally distributed. The assumption of independence is crucial!

In this paper we shall consider a heterogeneous agent model of a financial market to demonstrate that there are significant, systemic, real-world effects that cannot be removed by averaging once they reach a certain (rather low) level. This is the point at which positive feedback mechanisms becomes strong enough to defeat the equilibrating process. Then the equilibrium market solution loses stability completely and complex internal (endogenous) dynamics develop. This alters the future evolution of the system in a history-dependent way that cannot be adequately represented by any equilibrium model — although for much of that time the system may easily be mistaken for one that is in equilibrium with an underlying trend. Finally, the endogenous dynamics rapidly reverse in a cascade process.

The main source of positive feedback/instability (and non-averagability) in the system is herding behavior whereby agents have some additional motivation (ranging from completely irrational to hyper-rational) to prefer the position taken by the majority of agents. While there are many possible causes of herding behavior, the effects should usually be similar and can be modelled very simply using the framework developed in Section 2.

Few would argue with the statement that irrational behavior and herding are a common feature of the biggest market bubbles and crashes. Yet the question remains as to how such factors may affect the workings of a market when, even with the benefit of hindsight, no obvious mispricings are occurring. Two previous studies (Akerlof and Yellen (1985); Scharfstein and Stein (1990)) looked at the effects of small changes to otherwise maximizing rational behavior. They both showed that even small changes can cause significant (first order) changes to the value of the equilibrium. The second study is particularly relevant in that it considered rational herding by investment managers concerned about their relative performance to be the primary source of the deviation. However these analyses were performed within an equilibrium framework and so precluded the possibility of non-equilibrium dynamic solutions. Similarly Banerjee (1992) and Bikhchandani et al. (1992) introduced models of herd behavior via sequential decision-making but again within an equilibrium framework.

The modelling framework to be described in Section 2 was introduced in Lamba and Seaman (2008b) and Lamba (2010) and is based upon earlier related models (Cross et al. (2005, 2006, 2007); Lamba and Seaman (2008b)). The primary motivation for this earlier work was to show how to incorporate various systemic defects such as perverse incentives and investor psychology into an otherwise efficient market and to establish a causal link between agent behavior at the micro level and the non-Gaussian price statistics observed in financial markets. One clear conclusion was that herding can indeed induce ‘fat-tails’ consistent with observed power-law decays of real asset price changes. Thus herding is a possible, if not likely, contributor to an extremely important phenomenon that is inconsistent with standard financial models.

The motivation here is slightly different, although the modelling details are similar. The model below should be considered a ‘stress-test’ of an extant equilibrium pricing model that is carried out by weakening a particular subset of the assumptions. It is important to note that this allows us to carry over, without any detailed justification, those assumptions from the standard pricing model that are not being weakened.

The paper is organized as follows. The modelling framework is described fully in Section 2 together with an explanation of how various non-standard motivations, such as perverse incentives and the findings of behavioral economics, can be approximated. Then in Section 3 the results of numerical simulations are provided for realistic estimates of the model parameters. These demonstrate that the qualitative and quantitative changes introduced by such ‘imperfections’ are consistent with observations of real markets. In Section 4 various links are established between the modelling philosophy with concepts and theories from economics, finance, mathematics and physics. Section 5 contains the most significant numerical results. Here the herding strength is used as a bifurcation parameter to establish how much herding is required to destabilize the equilibrium market solution. The answer would appear to be far lower than a plausible estimate of herding in financial markets. Conclusions and suggestions for further research are given in Section 6.

2 The Model

The simplest, and most common, asset pricing model assumes that the price at time obeys the stochastic differential equation (SDE)

| (1) |

where and are the constant drift and volatility of the price per unit time and is a standard Brownian motion representing the arrival of uncorrelated Gaussian-distributed information. Equation (1) is justified by positing that new information is instantaneously and perfectly translated into a price change via some equilibrating process. The solution to (1), found using the Itô Calculus, is the geometric Brownian motion

| (2) |

The SDE (1) is highly unusual in that it has an explicit solution. Even more unusually, depends only upon the current value of and not the entire history of the Brownian process up to that point. Thus the variable can be considered a paradigm for other variables in economic models that are assumed to be the outcome of instantaneous equilibrating processes that are history-independent (i.e. that have no memory).

Without loss of generality, we may choose so that becomes the price relative to the risk-free interest rate plus risk premium. We may also, by rescaling time, choose and then discretize time so that the solution at the end of the time interval of length is

| (3) |

where

Note that the log-price follows a standard Brownian motion with the log-price changes having a Gaussian distribution . However this is in very poor agreement with reality. The ‘stylized facts’ of financial markets (see Mantegna and Stanley (2000); Cont (2001)) are a set of statistical observations that appear to hold across all asset classes, independent of geography, history and trading rules. There are two highly significant deviations from (3). The first is the presence of ‘fat-tailed’ price returns whereby the occurrence of the largest price changes (as measured over intervals of hours up to months or years) follows an approximate power-law decay by contrast with the exponential decay of Normal distributions. Thus the probability of the largest price moves is underestimated by many orders of magnitude. The second phenomena is volatility clustering, also known as heteroskedasticity, whereby large price moves (in either direction) are more likely to occur shortly after other large price moves. It is quantified by calculating the autocorrelation of the volatility which is again observed to follow a power-law decay. Under the Normal approximation, this autocorrelation should be precisely zero.

Almost by definition, the price changes caused by the information stream are effected by agents in the marketplace who a) act very fast and b) are motivated by the arrival of new information . The standard neoclassical argument is to suppose that it is as if all agents are continuously, instantaneously and correctly (on average) maximizing their respective utility functions. In reality the presence of transaction costs and the immense computational effort will mean that trading occurs over much longer timescales, at least for a subset of agents. We shall call them ‘slow agents’. We do not assume that slow agents are of uniform size (in terms of their trading positions) and thus weight the slow agent by her size and define .

Note that, in the standard pricing model (3), the market-clearing mechanism is assumed to be efficient and thus the details are unimportant and not specified. Similarly, only the slow agents will be explicitly simulated and it is assumed that the fast agents provide sufficient liquidity333The reader is directed to Lamba (2010) for a discussion of how the model can be modified at times of severe market stress when liquidity cannot be assumed..

We now make some assumptions that, it must be emphasized, are not fundamental to the modelling philosophy. They keep the model simple and are sufficient for the purpose at hand. Firstly, we assume that over the time interval the slow agents can only be in one of two states, the state meaning that she owns units of the asset, and the state meaning that she owns none of the asset444In reality a slow agent may choose to gradually increase or decrease their holdings, short the market, or buy derivatives, but this complicates the dynamics of the slow agents without providing further insights.. We can thus define the quantity which is a linear measure of the aggregate demand of the slow agents. Note that when none of the slow agents own the asset and when they all do. Changes in are assumed to affect the log-price in a linear manner (via the change in demand) modifying the discretized pricing formula (3) as follows

| (4) |

where and . The parameter is a measure of the total market depth of the slow agents.

At this point we note that (3) can be recovered from (4) in two different ways. We can set so that there are no slow agents, or we can suppose that the slow agents are also, on average, always correct and . In either case the models will generate the same price. However, the pricing formula (4) allows for the possibility of endogenous dynamics amongst the slow agents affecting the price . Thus one can interpret (4) as stating that price changes have an exogenous component due to new information, and an endogenous one, , caused by internal complex dynamics.

Finally, we introduce one further generalization of (3) by weakening the assumption that the fast (information driven) agents must always perfectly translate new information into price changes. This is achieved by adding a (for now unspecified) function that modifies the effect on prices of new information entering the market via

| (5) |

with the fast agents acting perfectly if .

Before continuing, the differences between the fast and slow agents should be clarified, especially since only the slow ones will be simulated directly. In the numerics that follow, will be chosen to correspond to approximately 1/10 of a trading day. Fast agents include institutions (or individuals) that regularly trade the asset over a timescale of several days or less, and/or are motivated primarily by new information. Slow traders on the other hand will typically shift investment positions over weeks, months or longer.

Equation (5) does not yet constitute a closed system because no rules governing the switching of the slow agents between the and states have been specified yet. There are many types of rule or trading strategy that could be used, involving any desired combination of pure utility function maximization, bonus/commission maximization, inductive learning, imitation among a network of slow agents, technical trading, ‘gut instinct’, profits, losses, relative performance of other investment options, market volatility, fear, greed, margin calls, the weather, and so on ad nauseam. Prior studies such as the Santa Fe model (see LeBaron et al. (1999)) do indeed use complicated ecosystems of trading strategies and there is much to commend this approach.

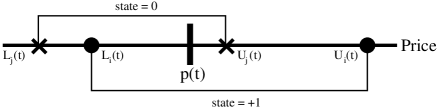

We shall use an approach based upon moving price thresholds developed in Lamba and Seaman (2008b) and Lamba (2010) which is deceptively simple but capable of mimicking various real world influences, market ‘imperfections’ and psychological biases (see Section 2.1). At the start of the time interval, the slow agent is represented by its state, or , and an evolving closed price interval where (Figure 1). The endpoints and are referred to as the lower and upper thresholds respectively. If, at the end of that time interval, the price has crossed either threshold555For example, an agent who is may be switching to either take profits or cut losses depending on which threshold is breached. An agent who is may be motivated either by a sell-off which makes them think the stock is now cheap, or an urge to follow the momentum of a rising stock or attempt to catch up with a benchmark., agent is deemed to be no longer comfortable with her current investment position, switches states, and the interval is updated so that the price is again an interior point. Furthermore, from (5) the action of switching causes a small jump in the log-price of . Each of the slow agents has their own interval straddling the current price with the price and all of the thresholds evolving at each timestep.

Since the intervals are allowed to evolve, it just remains to define the dynamics of the and . These thresholds for each agent will change (usually slowly) between switchings and correspond to that agent’s evolving strategy. Or equivalently the intervals can be thought of as their agents’ comfort zones within which that agent is still satisfied with their current investment position. Note that in the case of an algorithmic ‘black box’ or a hyper-rational utility maximizing investor these thresholds will be consciously and explicitly known by that agent but no other. A less-rational slow agent may not even be consciously aware of the threshold values but will know when one of them is violated and act to switch.

The state of the equilibrium model (3) at any given moment is completely specified by the current price (or equivalently the value of the information stream ). The situation for the full threshold model is very different. To specify the current state of the system completely requires the additional knowledge of all of the threshold values and the rules specifying their dynamics. These endogenous ‘hidden variables’ add a great deal of potential complexity to the model but we shall make some simplifying assumptions that appear to be sufficient to address the stability issues at hand.

In order to apply an averaging argument and preserve geometric Brownian motion pricing (3), we suppose that there are myriad influences on slow agents’ strategies that can be adequately represented by different (and uncorrelated, independent) geometric Brownian motions applied directly to every agent’s thresholds. These will be a mixture of purely rational independent analysis, completely irrational thought processes, and mixtures of the two almost certainly in differing proportions for each agent. Each of these influences will move each upper and lower threshold either inwards or outwards, towards or away from, the current price thus making the agent more or less likely to switch states respectively. Thus the threshold dynamics between switchings are given by

| (6) |

The quantity is the volatility of the threshold motion per unit time for the agent. Finally, if an agent does in fact switch at the end of a time interval, their threshold values will reset in such a way that is also independent of the other agents. Thus, on average, equal numbers of slow agents will be switching at each timestep and, provided that with identical threshold distributions for the agents in each state at time 0, remains close to 0 for all time resulting in the standard equilibrium pricing model (3).

We have now, finally, reached the point where we can endogenously perturb the price. To do this we need to include an influence on the slow agents that cannot be averaged away. We posit that agents who are in the minority state (e.g. those who are in state if ) will, on average, have a motivation to switch and join the majority. Furthermore the pressure to join the majority increases with the magnitude of the difference between the two groups, measured by the quantity . There are several effects that naturally lead to such a perturbation.

Firstly, any change in will lead to a drift in price that may be (mis)interpreted as a fundamental trend with the minority agents reacting accordingly to the price signal. Secondly, there may be ‘rational herding’ by investment managers who find themselves chasing a benchmark average so as not to lose their jobs, bonuses or investment capital 666These effects will be amplified by the short time-horizons of such evaluation periods.(see Keynes (1936); Akerlof and Yellen (1985); Scharfstein and Stein (1990)). A third cause is the actions of momentum investors who are consciously trying to take detect a nascent bubble as part of their investment strategy. Fourthly, there is the propensity of people, faced with uncertainty, to believe that other people are better informed than they are, or their preference to risk failing conventionally than succeeding unconventionally (Keynes (1936)). Finally, there may be purely psychological effects at work caused by the discomfort of being in a minority, especially within social or professional networks. We shall refer to all the above effects as causes of herding.

For simplicity we assume that each agent reacts to the current value of the aggregate (excess) demand/sentiment, , although in reality agents will have different perceived values of this quantity (or may be be reacting, in part, subconsciously). Herding is introduced into the model by supposing that for agents in the minority position only (6) is replaced by

| (7) |

while those in the majority remain unaffected. Note that the change is simply to suppose that each minority agent has an inward threshold drift added to the dynamics. Drifting the thresholds inwards (towards the current price of course) reduces the time to the next switching and can be described as the agent’s comfort zone being ‘squeezed’ by the majority opinion. The rate of drift is taken to be proportional to the length of the timestep, , the magnitude of the imbalance and a constant quantifying the herding effect for that agent. Note that herding is a positive-feedback effect — as moves away from it, at least initially, provides a mechanism for the imbalance to increase. This completes the description of the model.

2.1 Justifications for moving thresholds

As mentioned above, once equation (5) has been reached one can in principle use any modelling paradigm to specify the switching rules of the slow agents. Treating each slow agent as a dynamic closed interval on the positive real line (that must at all times contain the current price) is certainly unusual and at first may seem highly unnatural. However the use of pairs of price thresholds offers some compelling advantages.

Firstly there is the observation that slow agents react mostly to price changes over longer time periods rather than the arrival of new information. Indeed investment advice and analysis is usually offered in the form of price triggers, as are the outputs of computerized trading algorithms. Sometimes, such as in a margin call, the agent has no choice over the pricing point.

A second important issue is that of transaction (or sunk) costs. These are often neglected under simplifying assumptions but they profoundly change the nature of agents’ behavior777It is amusing to note that many of the people who rely on such models are actually paid from sunk costs. And all-too-often the possibility of significant transaction fees can skew the information and research entering the market.. Even if one believes that agents are continuously maximizing their utility functions this must somehow be translated into an acceptably small number of trades since a continuous process of incremental adjustments would be ruinous. Provided that switching results in new threshold values that are a non-zero distance away from the current price, then moving price thresholds are a potential mechanism for converting one into the other. The existence of sunk costs is closely linked to issues of hysteresis, memory-dependence and non-reversibility that will be discussed further in Section 4.1.

Finally we turn to behavioral economics. It has already been shown how the propensity for herding (rational and irrational) can be included by moving thresholds inwards for agents in the minority position. However other effects such as anchoring and loss-aversion can also be replicated. Anchoring is almost automatic as thresholds are reset around the last trading price while loss aversion requires slightly more complex rules involving keeping track of whether agents have made a profit or a loss. An extreme, but unfortunately quite common, example demonstrates the idea.

Imagine an individual who bought a dotcom stock at the height of the tech bubble. Immediately the price goes down but, due to loss aversion which is the emotional difficulty of acting to realize a loss, the lower threshold moves down even faster. It is likely that the upper threshold is moving downwards too but there is never enough of a temporary bounce in the stock price to cause a switch. Eventually the stock price hits zero without the agent ever selling.

Recent work (see Kahneman and Tversky (1974); Rubinstein (1998); Gigerenzer (2002); Barberis and Thaler (2003); Earl et al. (2007)) has suggested plausible heuristics that agents may be using in practice. It should be possible to recreate such rules using moving thresholds and then observe the effects upon aggregate statistics.

3 Preliminary Numerics

Detailed numerical investigations from a similar model (using two pairs of static thresholds for each agent) are compared against the stylized facts in Lamba and Seaman (2008a) and further numerical results for a moving threshold model can be found in Lamba and Seaman (2008b). Here, for completeness, we provide enough details for replication of the numerical results and sufficient simulations to reveal the nature of the non-equilibrium solution. It must be emphasized that no fine-tuning of parameters is required. Most of the parameters can be roughly estimated and we do so conservatively and as simply as possible.

Firstly, we must choose a timestep defined in units such that the variance of the external information stream is unity for . An observed daily variance in price returns of 0.6–0.7% suggests that should correspond to approximately 1/10 of a trading day. The price changes of 10 consecutive timesteps are then summed to give the daily price return.

We next assume that all slow agents have equal weight . This could be replaced by a Pareto distribution but we shall not do so here888It is not necessary to assume that each slow agent corresponds to just one individual or institution — they could each refer to a subset of agents with very similar strategies or propensities.. The behavior of the system is largely independent of the number of slow agents with being a lower-bound for representative simulations. All simulations in this paper will use slow agents.

Next we fix how the slow agents’ thresholds are reset after a switching. If agent switches at a price then immediately afterwards the interval is reset to

where are each chosen from the uniform distribution on the interval . This corresponds to an initial strategy that requires price ranges in the range 5–25% before another switching (although of course the threshold dynamics will alter the strategy as the system evolves).

We now turn to the most significant parameters, the herding parameters for each agent. Let us consider the more herding-susceptible agents and estimate that they can be pressured to switch over a period less than a reporting quarter (about 80 trading days). This is certainly the case for fund managers who are trying to keep up with a performance benchmark, or momentum investors, say, who try to time the market several times a year. Then a simple calculation based upon (7) suggests as a reasonable upper bound for the herding parameters. Thus we assign agents with a herding parameter chose uniformly from the uniform distribution on with the somewhat arbitrary but unimportant lower bound corresponding to agents who are relatively immune to herding effects.

The parameters represent the ‘volatility’ of each agents strategy (or expectations) and we simply assume they are all equal. Note that if then the volatility of the thresholds is the same as the volatility in price due to the information entering the system in (5). This is probably too large since the slow agents are not the ones motivated by new information and should alter their expectations more slowly. Thus we set .

Finally, as regards the slow agents, we come to the parameter that represents the effect of aggregate slow demand upon the price in (5) but which is much harder to estimate a priori. Simulations (not presented) show that even with endogenous dynamics and loss of equilibrium exist but without affecting the stock price at all. However if is too large the effect upon the price is so severe that the resulting price fluctuations are unrealistically large. However for a surprisingly wide range,, the price statistics are in good general agreement with the stylized facts. We conservatively choose as our default value in the simulations.

We now consider the fast agents. The function was introduced in (5) to modify the effects of the fast agents by assuming that under certain circumstances they do not accurately translate new information into price changes999This is a simple but plausible mechanism for the generation of volatility clustering..We shall suppose that at times of extreme market sentiment, when is far away from , excess speculation by fast traders occurs. This may be due to new agents entering the market or by too much attention being paid to new information by traders expecting a market correction. There is some evidence for this (see Brown (1999)) and it also helps correct for the fact that in our simple model the slow agents are not allowed to own multiple units of stock. As in previous work on this model the simplistic but plausible choice is made with . We choose so that at the most extreme mispricings, new information moves the market twice as much as it would if the fast agents were correctly incorporating it. It must be stressed that the presence of the function has no effect upon the main conclusions of this paper and will be set to for one of the simulations in Section 5 to demonstrate this.

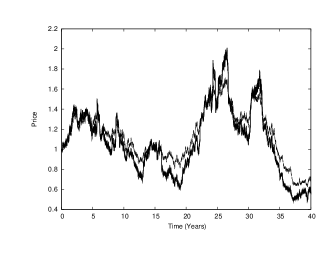

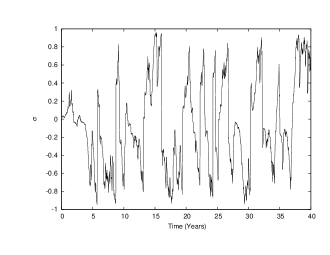

Figure 2 shows a simulation with the above parameters. The initial states of the agents and their thresholds are randomized. The thicker, more volatile curve is the pricing output of (5) while the lighter curve is the output of the geometric Brownian pricing model (that, recall, can be recovered by either setting or all of the ). A typical characteristic is that mispricings develop slowly and then suddenly reverse. This can also seen in Figure 3 which plots against time.

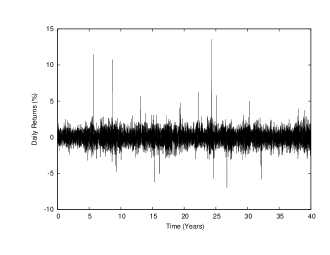

Both parts of the mispricing sequence are caused by endogenous dynamics. The incremental mispricing is due to herding effects. The sudden reversals occur because eventually enough of the majority agents switch position to start a cascade process — as agents switch they cause a change in price (due to the term in (5)) that trips other agents’ thresholds and so on. Figure 4 shows the daily percentage price returns. There are a significant number of large price changes that cannot be explained by a Gaussian information stream and lie within the fat tails101010Interestingly there is a very close correspondence between the dynamics of these cascades and Queueing Theory that is described in detail in Lamba (2010).. For comparison, the price changes from the equilibrium model are shown in Figure 5.

A snapshot of the internal structure of the market is shown in Figure 6. The density of the lower and upper thresholds of each type of agent ( and ) are plotted relative to the current price at a moment when (the mismatch between the densities is far more severe when ). The two density plots are not identical (as they were in the initial state) meaning that as the system evolves will once again move away from because different numbers of agents will be switching in either direction. The question that will be asked in Section 5 is: how strong must the herding effect be to generate significant endogenous dynamics?

4 Links to economic concepts and extant models

4.1 Equilibria, memory and history-dependence

The notion of equilibrium described in the introduction is a very strong one, precluding the possibility of multiple internal configurations for the same external parameters. Nonetheless the absence of (non-trivial) endogenous dynamics is a prerequisite for models that are reversible and history-independent with temporary exogenous shocks having no permanent effect.

The key issue is one of memory at the micro-level. If individual agents have no memory then it becomes much easier to assume that they will reverse their actions and expectations when the external influence is removed. However economic actors are subject to many effects (both rational and irrational) that cannot reasonably be modelled in this way.

Perhaps the most significant of these rational factors is the ubiquitous presence of transaction (sunk) costs (see Dixit (1992); Piscitelli et al. (1999); Göcke (2002)). These are expenses incurred that cannot be recouped on reversing the action. As an example suppose that at the current widget price it is not profitable for a manufacturer to have a factory produce the widget. However when the price increases to (perhaps due to a demand shock) the firm switches a factory over to widget production from something else, incurring costs such as re-tooling and factory down-time. If the price then falls back below the factory will not immediately switch out of production but rather waits until the price falls below some value . Thus if one only looks at the current price and it is not possible to know what the factory is producing — one also needs to know which of the threshold values and was last crossed.

In the physical sciences this is referred to as hysteresis111111In economics the term ‘hysteresis’ is often taken to mean the persistence of deviations from equilibrium. and the reader is directed to Cross et al. (2009) for a fuller description of the role of hysteresis in economics. The presence of many such factories, all with differing threshold values, results in many possible alternative internal configurations for the same price level. Each of these possibilities results in a different future evolution of the system which now displays both irreversibility and history-dependence121212When such effects are observed in macroeconomics a common equilibrium-based explanation is the presence of a unit-root since, if a system is only marginally stable it will take a long time to return to its former value after a disturbance. There are standard tests, under assumptions of linearity and the absence of hysteresis, for determining if this might be the case (see Said and Dickey (1984)). However marginal stability implies that a system is close to instability and this should be far more worrying to economists than irreversibility..

At an abstract level, the thresholds used to describe the slow agents in Section 2 are a mechanism for introducing memory/history into the modelling process (the fast agents, by assumption, act upon new information and require no such mechanism). As an example, an agent who has been in the minority state for a long time and is influenced by a herding pressure, on average will have thresholds that are much closer together and be more likely to switch in the near future. This information is propagated from one timestep to the next along with the agent’s current state.

It is now worth revisiting the concept of equilibrium, allowing for the possibility of multiple endogenous configurations (and dynamics). Saying that the market model simulation from Section 3 is in equilibrium until just before a sharp reversal is akin to saying that a geological fault-line is in equilibrium until just before the earthquake. This is true, in that there is a balance of both external and internal forces, but the statement that the fault-line is in equilibrium just after the earthquake is equally true. The ‘before’ and the ‘after’ can be approximated deceptively well by unique equilibrium models, but not the transition!

The ‘balance of forces’ notion of equilibrium is not sufficient to guarantee uniqueness and the system can rapidly move from one internal state to a different one (with lower energy in the case of an earthquake). Finally, it should be noted that multiple equilibrium models do exist in mainstream economics with the initial conditions determining which equilibrium is achieved. However the situation here is far worse — the set of feasible final states cannot be enumerated in advance and depend on the path taken by the process.

4.2 Rational expectations and efficient markets

The philosophical, political, social and practical consequences of the mainstream acceptance of the hypothesis of memory-free, efficient, financial markets cannot be overstated. Although the concepts were introduced by Bachelier in his 1900 Ph.D. thesis, this work was largely forgotten until the 1960s when they became known collectively as the Efficient Market Hypothesis (EMH) (see Fama (1965); Samuelson (1965); Fama (1970)).

The three versions of the EMH (weak, semi-strong and strong) all rely upon two qualitatively different classes of assumption. Firstly, there are strong assumptions about the market itself and the nature of the information stream entering it. Such information consists of, amongst other things, economic statistics, performance reports, geopolitical events, and analysts’ projections. It is assumed to be instantly available to all economic participants, uncorrelated with itself, and is usually modeled as a Brownian motion, possibly with drift.

The second class of assumptions relates to the market participants themselves, who are deemed to be perfectly rational, correctly incentivized, and capable of instantaneously incorporating new data into their differing market strategies and predictions. However, heterogeneity of agents (or their expectations) is necessary to ensure that trading occurs in the absence of arbitrage opportunities. Thus the final ingredient in the EMH description is the Rational Expectations Hypothesis (REH) (see Muth (1961)) stating that the differing expectations driving trades, when used as predictions, are on average correct131313As opposed to being consistent with the modelling assumptions which is the form of the REH most often used in macroeconomic modelling. and do not result in market mispricing. Additional assumptions, such as the absence of transaction costs, yield the standard formulae used for risk management and derivative pricing which form the bedrock of modern financial engineering (Black and Scholes (1973)). It is this second class of assumptions that are the focus of this paper.

As described in Section 2, if one sets , and further assumes that all threshold dynamics for the slow agents are the result of perfectly rational, independent, utility maximizing behavior (satisfying the REH) then one recovers an equilibrium market following geometric Brownian motion and satisfying the EMH. Once one weakens these assumptions to allow for more general dynamics (and motivations), the moving threshold model can be thought of as a ‘perturbation space’ within which one can explore the robustness/stability of the default EMH model.

Even if agents are not perfectly rational and other factors influence the threshold dynamics, the pricing should remain correct provided that the REH still holds. However the presence of just one REH-violating perturbation potentially invalidates its use. As was shown in the numerical simulation of Section 3, real-world effects that induce herding do exactly that, giving rise to price dynamics that differ greatly (qualitatively and quantitatively) from the equilibrium model by introducing a form of coupling between agents’ actions. However it is possible that lower levels of herding may result in acceptably small deviations from equilibrium. In Section 5 the herding parameter will be systematically varied to show that this does appear to be the case, although only if the herding parameter is reduced by a significant factor from its estimated real-world value.

Even markets in which irrationality exists can be ‘efficient’ in the sense that investors cannot earn above-average returns without taking on above-average risk. Indeed, this is a minimal requirement for any predictive market model (see Malkiel (2003))141414The aim of this work is not to show that irrational markets are inefficient, rather that equilibrium models are fundamentally inadequate.. In Cross et al. (2007) it was shown that there is no statistically significant different between the the investment performance of agents with differing herding propensities (and hence nothing to be gained by adaptively changing their reaction to herding). Indeed when transaction costs are taken into account the traders with the highest values of , that includes momentum traders, performed significantly worse, in agreement with previous studies (Odean (1999)).

One potential criticism of the model is that the fast agents are assumed to be reacting to new information and converting it into price changes. However there may also exist true fundamental fast agents who are aware of the current non-zero value of and the correct price and who view this as an arbitrage opportunity. This would act as an additional equilibrating (negative-feedback) mechanism helping to counteract the herding. This brings us to the very important issue of the limits of arbitrage, both in the model and in real markets.

Firstly, as regards the model, is assumed to be precisely known by all the slow agents. This is purely for simplicity and agents may have widely-differing perceived values that are only approximately (or on average) correct. Also, it is important to note that no agents are assumed to know the correct gemetric Brownian motion price. It is calculated and plotted in Section 3 but this is only a visual aid — none of the agents need to be made aware of it. As it stands the model is a caricature, albeit one that can be made arbitrarily more complicated and realistic. As this complexity grows, any potential model-specific opportunities for arbitrage that might exist will reduce and so now we discuss the limits to arbitrage in real markets.

Arbitrageurs and/or fundamentalist investors provide a possible to counteract herding effects. However there are severe limitations in practice. Firstly there is the noise-trader problem (see Schleifer (2000) and Shleifer and Vishny (1997)) — arbitrageurs typically have very short time-horizons and mispricings can last a very long time. Secondly there is the existence of speculative traders and short term momentum-traders who may actually make the mispricing worse. Thirdly, it is difficult in pactice to be sure what the fundamental price actually is. There is no visible, unambiguous, information stream and all trends may be misinterpreted as rational — especially by those who subscribe to the EMH! Some evidence for this may be found in the wide variations over time of even the most basic measures of value such as the P/E ratio of a stock.

This is not to dismiss entirely the possibility that herding effects can be counteracted. Indeed many, perhaps even the vast majority of, potential bubbles may get deflated before anyone even noticed by rational agents working as the EMH suggests they should. The point is that it does not happen every time. The stability results to be presented in Section 5 should, in this light, be viewed as a preliminary attempt to quantify which effect eventually wins.

4.3 Technical analysis

Given the widespread belief in the underlying notion of (at least weakly) efficient markets, a surprisingly large number of people are employed in technical analysis, looking for exploitable trends and patterns in past pricing/volume data. Some studies, such as Brock et al. (1992), claim that the most popular trading rules (based upon moving averages and support/resistance levels) can indeed produce statistically significant profits, even in the presence of transaction costs, while others dispute this (see Chan et al. (1996) and Malkiel (2003)).

An obvious question to ask is what effect such technical traders might have on the market, if any. A second question is, if a particular technical trading rule does indeed work, what are the reasons for it? It may be caused by the presence of one or more systemic defects (such as herding effects, perverse incentives, or behavioral effects) or it may in fact be a self-fulfilling prophesy caused by the large numbers of technical traders using that rule themselves. By incorporating such strategies into the threshold dynamics, it is possible to systematically explore such questions. Preliminary results will be presented elsewhere.

4.4 Soros’ Theory of Reflexivity

In Soros (2003, 2008), George Soros introduced his Theory of Reflexivity. While this is still at the stage of being a philosophical theory, and as yet has had little impact on economics or finance, its relationship to the modelling approach used here (and between its predictions and the numerical results presented above) is close enough to merit comment.

Soros’ theory rests upon two observations. Firstly, human beings are fallible and they may misinterpret an apparent trend, or some fundamental misconception may take hold. This results in investor behavior that is incorrect but in turn induces changes to the market or economic system. Positive feedback effects then cause an increasing mismatch between perception/prices and economic fundamentals that eventually becomes unsustainable and rapidly unwinds.

In the model of Section 2, herding provides the amplification mechanism. This is reflexive in the sense that beliefs affect prices, provided in (5). Soros suggests that such processes are commonplace in economic systems and result in far-from-equilibrium dynamics that only become apparent at the very end. This is exactly what is observed in the simulations from Section 3.

4.5 Minsky and the financial instability hypothesis

Recent events in financial markets have re-awakened interest in the work of Hyman Minsky and in particular his theory of financial instability (Minsky (1992, 2008)). Minsky’s work is unusual in macroeconomics in that it places a great deal of importance upon the role of the financial system and debt accumulation. He also stressed, following on from Keynes (1921), the role played by market sentiment (analogous to the quantity above), belief under uncertainty, systemic risks and contagion.

Minsky argued that a rising trend in prices (for whatever cause) during a period of relative stability will attract savings and profits leading to further price rises. Gradually there is a reduction in the perceived level of risk that encourages more lending, debt and leverage. Lending standards fall, risk-taking increases, and ‘Ponzi borrowers’ appear who are relying upon increasing prices to service their debt. Eventually the system becomes unstable, credit tightens, and prices cascade downwards in a ‘Minsky moment’.

Minsky believed that such processes were the norm rather than the exception with disequilibrium adjustment mechanisms being insufficient to counteract or prevent them. The resulting dynamics are similar to those observed in the numerics of Section 3 — there is a long period of apparent trend stability at the aggregate level (whose magnitude and duration are extremely hard to predict) that masks increasing endogenous instability. Then when the process ends it does so very rapidly. Or to put it another way, similar positions develop gradually and then unwind quickly.

There are two ways in which the model presented here relates to the work of Minsky. Firstly, the increasing availability of low-quality credit and lowered perception of risk provide yet another herding mechanism that adds ‘fuel to the fire’. Secondly, if one reinterprets the price in the model of Section 2 as being a quantity that represents the overall level of, and ease of obtaining, credit (with slow agents being potential lenders) then one has a model that is distinctly Minskian. A more sophisticated model might couple together two such models, one for price and one for credit151515It should be pointed out the model in this paper is symmetric with respect to rising and falling prices, while Minsky’s arguments are not. This is not a fundamental problem, however..

5 Stability simulations — how much herding is too much?

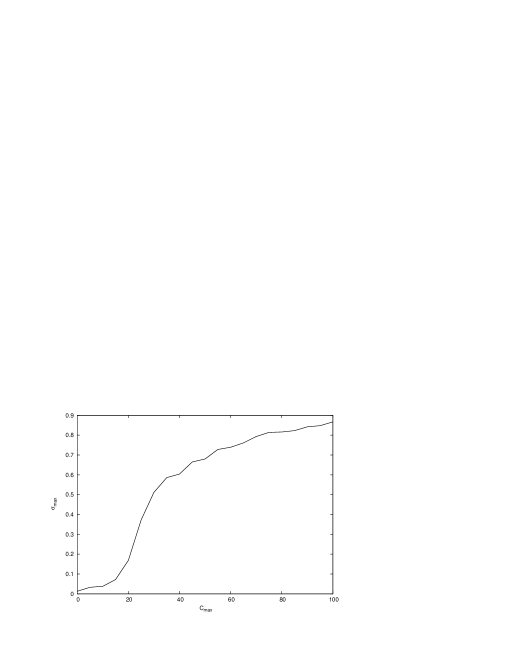

In the numerics of Section 3 the herding parameters for the slow agents were chosen from the uniform distribution on . However we know that if all the are set to then the equilibrium solution is recovered. We now investigate the manner in which the equilibrium solution loses stability as the herding is systematically increased from 0.

We introduce a bifurcation parameter and choose all the uniformly from the interval . In order to quantify the level of disequilibrium in the system we record the maximum value of over the last 30 years of the simulation (to remove any possible transient effects caused by the initial conditions).

Figure 7 shows the results (with the maximum of averaged over 10 runs) with all other parameters kept unchanged from those used to generate Figure 1 — the only difference is that the initial value of is set to 0.05 to provide an initial disturbance to the system.

As can be seen, the equilibrium solution can be considered a good approximation only for which is an order of magnitude below our (rather conservative) estimate from Section 3. The loss of stability, measured in terms of the maximum deviation of from 0, is gradual and saturates at around .

A rough description of the dynamics of the system is as follows. The drift in the threshold dynamics of the minority agents is a destabilizing influence, while the diffusion of the thresholds and the fact that the majority agents do of course eventually switch out of their position are stabilizing influences. The existence of such competing forces is a very common cause of non-trivial dynamics in complex nonlinear systems. A mathematical treatment of these stability issues will be presented elsewhere.

It could be argued that the presence of modifies the influence of the fast agents and may be in part responsible for the loss of equilibrium stability. This is ruled out by Figure 8 which shows the results with . If anything the instability is more pronounced with the full extent of far-from-equilibrium dynamics being reached at .

Finally, we consider the parameters that govern the diffusion of slow agent thresholds. In Section 3 it was argued that this would likely be lower than the price volatility and so was set to . Figure 9 sets so that the magnitudes are now comparable. The change from Figure 7 is negligible.

6 Conclusions

The numerical results of Section 5 demonstrate that a hypothetical, yet recognizable, equilibrium market model loses stability in the presence of even relatively small herding pressures — whatever their underlying cause may be. Or to put it another way, the positive feedback mechanisms caused by herding effects can overwhelm self-correcting equilibrium models. This does not by itself prove that such an instability occurs in any actual market, but there are two observations that suggest this is the case. Firstly, the price statistics of the unstable system are much closer to the stylized facts of financial markets than those of the equilibrium model. Secondly, while the model itself is quantitative and new, it shares features with qualitative and long-standing critiques of equilibrium models and neoclassical economics. Hopefully the work presented here will make a useful contribution to the debate.

Suppose for a moment that herding is indeed responsible for moving markets away from equilibrium. This has important policy implications (apart from the desirable reduction in overall leverage that is an obvious remedy for underestimating the risk from fat-tail events). The global financial crisis that finally became apparent to everyone in 2007/8 appears to have been, at least in part, caused by the increased attention to short timescales caused by, for example, fund-managers chasing the average every quarter, individuals trying to flip houses, and inappropriate short-term performance-related bonuses and upfront commissions being paid out throughout the financial system161616This general question of how complex systems with no natural timescale react to forces with an artificial time horizon may also be useful in other fields such as ecology.. Regulations to increase the time horizon of financial actors would reduce the herding pressure and indeed at the time of writing such proposals are being either discussed or enacted in the US and the UK.

The mathematical description of the threshold dynamics lies within a new class of stochastic partial differential equations for which closed-form analytic solutions almost certainly do not exist. This may be unacceptable to many economists. However, the value of such models (and solutions) in almost every other quantitative discipline is beyond dispute and there is no compelling reason to suppose that economic systems should be an exception. For example, chaos theory has shown that even very simple dynamical systems, evolving without any external influences, can be inherently unpredictable (except possibly in a statistical sense). Yet, even in the absence of explicit solutions, chaos theory is still capable of quantifying both the probabilities of events and the theoretical time limit on meaningful predictions.

Finally, it is worth stepping back to look abstractly at the process leading from (3) to the full moving threshold model. This started with the transition from an equilibrium model that implicitly relies upon averaging and a representative agent to a bigger system that explicitly allows for the possibility of endogenous dynamics. But, if the rules governing the agents’ dynamics are assumed to be uncorrelated and independent then the aggregate behavior of the system is unchanged. Then more complicated dynamics for individual agents can be introduced that correspond to the effect under investigation and can be regarded as perturbations to the equilibrium model171717The use of thresholds to specify agent dynamics seems a very natural choice but is not required. Other types of rule may have their advantages.. Dynamic Stochastic General Equilibrium (DSGE) models may provide an interesting starting point for a similar procedure as they also rely heavily upon the use of averaging, representative agents and equilibrium theory. Furthermore, the new-Keynesian DSGE models incorporate the concept of ‘sticky prices’ which suggests that the use of thresholds may again be a suitable way to introduce non-standard effects within them.

References

- (1)

- Akerlof and Yellen (1985) Akerlof, G. and J. Yellen, “Can Small Deviations from Rationality Make Significant Differences to Economic Equilibria?,” The American Economic Review, 1985, 75 (4), 708–720.

- Banerjee (1992) Banerjee, A.V., “A simple model of herd behavior,” The Quarterly Journal of Economics, 1992, pp. 797–817.

- Barberis and Thaler (2003) Barberis, N. and R. Thaler, “A Survey of Behavioral Finance,” in G.M. Constantinidos, M. Harris, and R. Stultz, eds., Handbook of Economics and Finance, Elsevier Science, 2003, pp. 1053–1123.

- Bikhchandani et al. (1992) Bikhchandani, S., D. Hirshleifer, and I. Welch, “A theory of fads, fashion, custom, and cultural change as informational cascades,” Journal of political Economy, 1992, 100 (5).

- Black and Scholes (1973) Black, F. and M. Scholes, “The pricing of options and corporate liabilities,” J. Polit. Economy, 1973, 81, 637–659.

- Brock et al. (1992) Brock, W., J. Lakonishok, and B. LeBaron, “Simple technical trading rules and the stochastic properties of stock returns,” Journal of Finance, 1992, 47 (5), 1731–1764.

- Brown (1999) Brown, G.W., “Volatility, sentiment and noise traders,” Financial Analysts Journal, 1999, pp. 82–90.

- Chan et al. (1996) Chan, L.K.C., N. Jegadeesh, and J. Lakonishok, “Momentum strategies,” Journal of Finance, 1996, 51 (5), 1681–1713.

- Cont (2001) Cont, R., “Empirical properties of asset returns: stylized facts and statistical issues,” Quantitive Finance, 2001, 1, 223–236.

- Cross et al. (2006) Cross, R., M. Grinfeld, and H. Lamba, “A mean-field model of investor behaviour,” J. Phys. Conf. Ser., 2006, 55, 55–62.

- Cross et al. (2009) , , and , “Hysteresis and economics,” IEEE Control Systems Magazine, 2009, 29 (1), 30–43.

- Cross et al. (2005) , , , and T. Seaman, “A threshold model of investor psychology,” Phys. A, 2005, 354, 463–478.

- Cross et al. (2007) , , , and , “Stylized facts from a threshold-based heterogeneous agent model,” Eur. J. Phys. B, 2007, 57, 213–218.

- Dixit (1992) Dixit, A.K., “Investment and hysteresis,” J. Econ. Persp., 1992, 6, 107–132.

- Earl et al. (2007) Earl, P.E., T.-C. Peng, and J. Potts, “Decision-rule cascades and the dynamics of speculative bubbles,” Journal of Economic Psychology, 2007, 28 (3), 351 – 364.

- Fama (1965) Fama, E.F., “The Behavior of Stock Market Prices,” Journal of Business, 1965, 38, 34–105.

- Fama (1970) , “Efficient capital markets: A review of theory and empirical work,” J. Finance, 1970, 25, 383–417.

- Gigerenzer (2002) Gigerenzer, G., Adaptive thinking: Rationality in the real world, Oxford University Press, USA, 2002.

- Göcke (2002) Göcke, M., “Various concepts of hysteresis applied in economics,” J. Econ. Surveys, 2002, 16, 167–188.

- Kahneman and Tversky (1974) Kahneman, D. and A. Tversky, “Judgement under Uncertainty: Heuristics and Biases,” Science, 1974, 185 (4157), 1124–1131.

- Kaldor (1972) Kaldor, N., “The Irrelevance of Equilibrium Economics,” The Economic Journal, 1972, 82 (4), 1237–55.

- Keynes (1921) Keynes, J.M., A treatise on probability, Macmillan & Co., Ltd., 1921.

- Keynes (1936) , “The general theory,” London, New York, 1936.

- Kirman (1992) Kirman, A., “Who or what does the representative agent represent?,” Journal of Economic Perspectives, 1992, 6, 117–136.

- Lamba (2010) Lamba, H., “A queueing theory description of cascades in financial markets and fat-tailed price returns,” 2010. To appear, European Physics Journal B.

- Lamba and Seaman (2008a) and T. Seaman, “Market statistics of a psychology-based heterogeneous agent model,” Int. J. Theor. Appl. Fin., 2008, 11, 717–737.

- Lamba and Seaman (2008b) and , “Rational expectations, psychology and learning via moving thresholds,” Phys. A, 2008, 387, 3904–3909.

- LeBaron et al. (1999) LeBaron, B., W.B. Arthur, and R. Palmer, “Time series properties of an artificial stock market,” Journal of Economic Dynamics and Control, 1999, 23 (9-10), 1487–1516.

- Malkiel (2003) Malkiel, B.G., “The efficient markets hypothesis and its critics,” Journal of Economic Perspectives, 2003, 17, 59–82.

- Mantegna and Stanley (2000) Mantegna, R. and H. Stanley, An Introduction to Econophysics, CUP, 2000.

- Minsky (1992) Minsky, H.P., “The financial instability hypothesis,” The Jerome Levy Economics Institute Working Paper, 1992, 74.

- Minsky (2008) , Stabilizing an unstable economy, McGraw Hill Professional, 2008.

- Muth (1961) Muth, J.A., “Rational expectations and the theory of price movements,” Econometrica, 1961, 6.

- Odean (1999) Odean, Terrance, “Do Investors Trade Too Much?,” American Economic Review, December 1999, 89 (5), 1279–1298.

- Piscitelli et al. (1999) Piscitelli, L., M. Grinfeld, H. Lamba, and R. Cross, “Exit-entry decisions in response to aggregate shocks,” Appl. Econ. Lett., 1999, 6, 569–572.

- Rubinstein (1998) Rubinstein, A., Modeling Bounded Rationality, Cambridge MA: MIT Press, 1998.

- Said and Dickey (1984) Said, E. and D.A. Dickey, “Testing for Unit Roots in Autoregressive Moving Average Models of Unknown Order,” Biometrica, 1984, 71, 599–607.

- Samuelson (1965) Samuelson, P., “Proof That Properly Anticipated Prices Fluctuate Randomly,” Industrial Management Review, 1965, 6, 41–49.

- Scharfstein and Stein (1990) Scharfstein, D. and J. Stein, “Herd Behavior and Investment,” The American Economic Review, 1990, 80 (3), 465–479.

- Schleifer (2000) Schleifer, A., Inefficient Markets Clarendon Lectures in Economics, OUP, 2000.

- Setterfield (1997) Setterfield, M., “Should economists dispense with the notion of equilibrium?,” Journal of post Keynesian economics, 1997, 20 (1), 47–76.

- Shleifer and Vishny (1997) Shleifer, A. and R.W. Vishny, “The limits of arbitrage,” Journal of Finance, 1997, 52 (1), 35–55.

- Soros (2003) Soros, G., The alchemy of finance, John Wiley & Sons Inc, 2003.

- Soros (2008) , The new paradigm for financial markets: the credit crisis of 2008 and what it means, Public Affairs, 2008.