Individual and collective stock dynamics: intra-day seasonalities

Abstract.

We establish several new stylised facts concerning the intra-day seasonalities of stock dynamics. Beyond the well known U-shaped pattern of the volatility, we find that the average correlation between stocks increases throughout the day, leading to a smaller relative dispersion between stocks. Somewhat paradoxically, the kurtosis (a measure of volatility surprises) reaches a minimum at the open of the market, when the volatility is at its peak. We confirm that the dispersion kurtosis is a markedly decreasing function of the index return. This means that during large market swings, the idiosyncratic component of the stock dynamics becomes sub-dominant. In a nutshell, early hours of trading are dominated by idiosyncratic or sector specific effects with little surprises, whereas the influence of the market factor increases throughout the day, and surprises become more frequent.

1. Introduction

Financial markets operate in sync with human activities. It is therefore no surprise that financial time series reveal a number of seasonalities related to human rhythms: markets open in the morning and close in the evening, remain closed during week-ends and during vacations; wages are paid and portfolios are re-balanced on a monthly basis, earnings are announced on a quarterly basis (in the US), etc. These periodicities leave a statistical trace on the time series of returns of many assets. Among the best known periodicities is the so-called U effect [1, 2], that describes the intra-day pattern of volatility of individual US stocks: the average volatility is observed to be high after the market opens, then decreases as to reach a minimum around lunch time and increases again steadily until market close.111This pattern is a little different in Europe or in the UK, with a second volatility spike at 2:30 pm GMT when the US market opens.

In this short note we want to report on additional intra-day patterns concerning both individual and collective stock dynamics. First, we study the intra-day pattern of other moments of the individual stock dynamics, beyond the well known U-shaped volatility. Second, we characterise the cross-sectional distribution of returns and its typical evolution during the day. Finally, we study the correlation matrix between stock returns and find that the leading modes also have a very well defined intra-day pattern. Our study here is entirely empirical, but our results certainly beg for a detailed theoretical interpretation in terms of agent behaviour: strategies, information processing, risk aversion, etc. We provide some hints in that direction in the conclusion.

2. Data, notations and definitions

We have considered a set of stocks of the New York Stock Exchange (which are among the largest market capitalisations) that has been continuously traded during the period between and to form a statistical ensemble of minutes stock returns. The total number of minute bins is , whereas the total number of days is ( bins per day). Stocks will be labelled by , days by and bins by . The return of stock in bin of day will be denoted as .

Different types of averages will be needed. Time averages for a given stock and a given bin are expressed with angled brackets: , whereas averages over the ensemble of stocks for a given bin in a given day appear with square brackets: . For an arbitrary function of these returns we therefore write:

| (1) |

The first set of observables concerns single stock properties. We characterise the distribution of stock in bin by its four first moments: mean , standard deviation (volatility) , skewness and kurtosis . We will in fact use low moments, less noisy estimates of the last two quantities. We will define as the median of all returns of stock in bin , and define:

| (2a) | ||||

| (2b) | ||||

| (2c) | ||||

| (2d) | ||||

Within a cumulant expansion, the last two lines coincide with the usual definition of skewness and kurtosis, but no moments larger than two are needed to estimate them. Note that the correction term to the kurtosis turns out to be negligible, and we have neglected it in the following. We will be interested below in the average over all stocks of the above quantities, as a way to characterise the typical intra-day evolution of the distribution of single stock returns.

One can also consider cross sectional distributions, i.e. the dispersion of the returns of the stocks for a given bin in a given day , i.e. one distribution every five minutes. One can again characterise these distributions in terms of the first four moments. The median of all returns for a given is now ( for “dispersion”), and we define:

| (3a) | ||||

| (3b) | ||||

| (3c) | ||||

| (3d) | ||||

Note that can be seen as the return of an index, equiweighted on all stocks. We will be interested below in the average over all days of the above quantities, as a way to characterise the typical intra-day evolution of the dispersion between stock returns.

Although the dispersion already captures part of the “Co-movements” of stocks, a more direct characterisation is through the standard correlation of returns. In order to measure the correlation matrix of the returns, we first normalise each return by the dispersion of the corresponding bin. This factors in any “trivial” intra-day seasonality, and also accounts for the fact that the volatility fluctuates quite a bit during the 10 year time interval that we consider. Therefore, we introduce: and study the correlation matrix defined for a given bin :

| (4) |

where the subscript means “connected part” (i.e. averages have been subtracted) and . Of special interest are the largest eigenvalues and eigenvectors of , which charaterize the correlation structure of stock returns. This analysis has been performed in several papers ([6, 7, 17, 14]) using daily or high frequency returns, and it is well known that the structure of large eigenvectors reflects the existence of economic sectors of activity. The largest eigenvalue , in particular, corresponds to the market mode, and is associated to an eigenvector with all entries positive and close to . In fact, can be seen as a measure of the average correlation between stocks. We will be interested below in the dependence of the largest eigenvalues and their associated eigenvectors, a study that, to the best of our knowledge, has not been reported in the literature before.

3. Single stock intra-day seasonalities

3.1. Odd moments

Odd moments tend to be small and noisy, so it is difficult to draw definite conclusions. The average return is on average over the whole period positive, but noisy and does not show any intra-day pattern. The average skewness of five minutes returns is also noisy and is compatible with zero, again without any identifiable intra-day pattern at all. This is at variance with the skewness of returns on a longer time interval, which is negative. The build up of negative skewness with time scale is a consequence of the leverage effect, i.e. negative returns tend to be followed by larger volatilities (see e.g. [6]).

3.2. Even moments

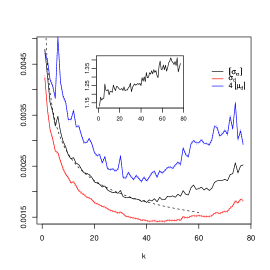

The average volatility, on the other hand, reveals a very clean U-shaped pattern that has been reported many times in the literature ([1, 2]). We show in Fig. 1 . Note that the overnight volatility is much larger than the typical five minute volatility, and is not shown in the graph. Interestingly, the average volatility is found to decay in the first two hours of trading as a power-law with . This relaxation is reminiscent of the power-law decay of the volatility after large price swings [11, 16, 18, 10]. The overnight return is indeed usually quite large, and can be seen as a strong perturbation. The power-law relaxation suggests that some critical mechanism is involved in the way volatility reverts back to ‘normal’ after market jumps.

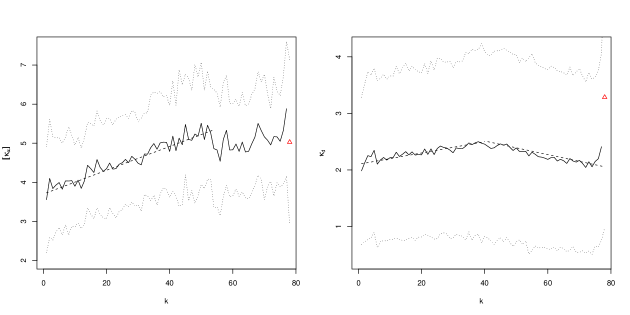

Turning now to the kurtosis , we find, perhaps surprisingly, that there is a clear intra-day growth of the kurtosis from at the beginning of the day to around 1 p.m., and stays approximately constant (but noisy) until the end of the day – see Fig. 2, left. The overnight kurtosis remains around . This finding is counter-intuitive because one would naively associate the large volatility in the morning with huge swings, symptomatic of the market uncertainty at the open. But this is not the case: the maximum of the intra-day volatility corresponds to a minimum in kurtosis. We will report similar counter-intuititive results below. Possible mechanisms are discussed in the conclusion.

4. Cross-sectional intra-day seasonalities

4.1. Odd moments

Noting that the average over stocks of is identical to the average over time of , the discussion of the first moment of the cross-sectional distribution is redundant. The average of is a proxy for the index volatility, and is displayed in Fig. 1 : it shows a U-shaped pattern similar to that of , with however a stronger end-of-day surge. This is due to the correlation pattern discussed in section 5 below: the average correlation between stock indeed increases as the day proceeds, leading to an increased index volatility.

As far as the average skewness is concerned, we again find a very noisy quantity with no particular intra-day pattern. The only notable feature is that this time, the skewness is significantly positive, albeit small: the average over of is found to be .

4.2. Even moments

As above, the even moments show clear patterns. The average dispersion exhibits a U-shaped pattern very similar to that of — see Fig. 1. In fact, the ratio is plotted in the inset of Fig. 1 as a function of and increases from at the open to at the close. In relative terms, the dispersion is thus stronger in the morning, and decreases as the day proceeds.

The dispersion kurtosis , on the other hand, has an inverted U shape, and reaches a minimum at the open and at the close of the market, i.e. when the dispersion and the volatility are locally maximum. So even when the dispersion of returns is at its peak, with stocks all over the place (so to say), the cross-sectional distribution of returns is on average closer to a Gaussian! Note however that the variation of the kurtosis is not large, from to . The overnight dispersion kurtosis, on the other hand, is much stronger: .

4.3. Conditioning on the index return

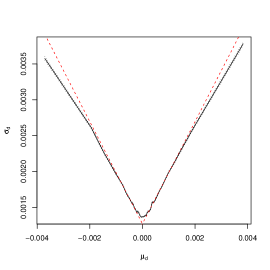

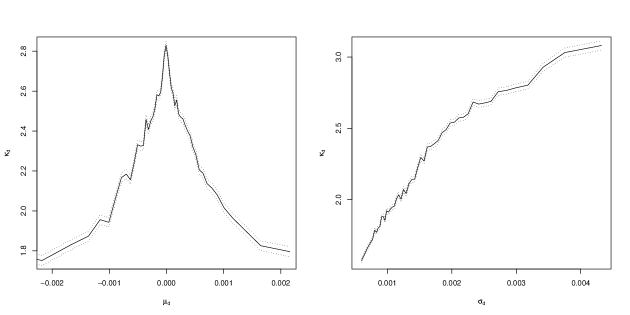

As noted above, the quantity is the return of an equiweighted index. It is interesting to condition the value of the moments of the cross-sectional dispersion on this quantity. Such a study was performed on daily returns in [13] and more recently by L. Borland [4]. In agreement with the results of [13, 9], we find that the average dispersion is an increasing function of the amplitude of the index return, see Fig. 3. As noted in [9], this observation shows that the volatility of the stock residuals in a one-factor model must depend on the volatility of the market mode. Fig. 3 furthermore suggests that this dependence is sub-linear (see [8] for some elaborations on this observation.)

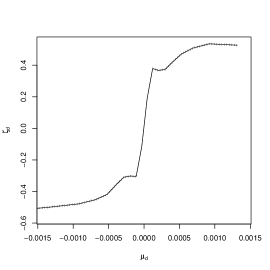

As first established in [12] on daily data, we find that the skewness is an odd function of , as shown in Fig. 4. Note that the skewness increases very abruptly for small and saturates for larger values of the index return. Pictorially, a positive index return can be thought of as resulting from a few “winners” running ahead of the pack, contributing both to the mean and to the skewness. The slope of around the origin, together with the fact that the index has made on average positive daily gains in the period 2000 – 2009, are enough to explain the average value of the dispersion skewness reported above.

Finally, the dispersion kurtosis shows again a non-intuitive decreasing behaviour as a function of , see Fig. 5. The average kurtosis conditioned to a value of decreases from for small index returns to for index returns larger than in absolute value. This was first noticed en passant in [9] on daily data and recently emphasised by Borland [4]. Here, we confirm on five minute returns this strange stylised fact: the cross-sectional distribution of returns appears to be more Gaussian when its mean is off-centred.

However, if we now condition on the dispersion (which, as we found above, is positively correlated with ), we find (see Fig. 5) the opposite behaviour, i.e. the larger the dispersion, the larger the kurtosis ! We will offer a discussion of these confusing effects in the discussion section below.

5. Intra-day seasonalities in the inter-stock correlations

Let us now turn to the properties of the eigenvalues and eigenvectors of the correlation matrix defined by Eq. (4) above.

5.1. The top eigenvalue

The largest eigenvalue of the correlation matrix of stock returns is well known to be associated with the “market mode”, i.e. all stocks moving more or less in sync. As recalled above, the quantity can be used to define the average correlation between stocks.

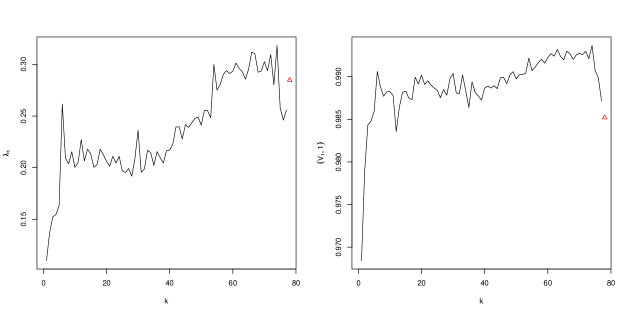

We show in Fig. 6 (left side) the magnitude of as a function of . Interestingly, the average correlation clearly increases as time elapses, from a rather small value when the market opens to near market close. This is in agreement with the fact that the dispersion is, in relative terms, smaller at the end of the day (see Fig. 1, inset). The value of for the correlation of overnight returns is also around , in continuity with the value at the end of the trading day.

In agreement with the idea that the stock dynamics become more and more uniform as the day proceeds, we find a substantial increase of the scalar product of the largest eigenvector with the uniform normalised vector — see Fig. 6 right. This scalar product is always close to unity, confirming the market mode interpretation of the top eigenvalue, but starts the day around and ends the day at , before dropping again in the last bins of the day and during the overnight, when it is equal to (i.e. larger than the open value).

5.2. Smaller eigenvalues

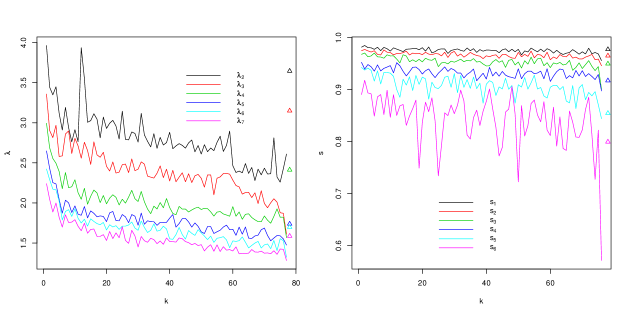

The evolution of the next six eigenvalues , is shown in Fig. 7. We see that the amplitude of this risk factors now decreases with time, before shooting back up during the overnight (see the last point of the graphs). Although by construction the trace of the correlation matrix, and therefore the sum of all eigenvalues is constant (and equal to ), this decrease is not a trivial consequence of the increase of , since the sum of the first five eigenvalues is , still small compared to . What we see here is that as the day proceeds, more and more risk is carried by the market factor, while the amplitude of sectorial moves shrivels in relative terms (but remember that the correlation matrix is defined after normalising the returns by the local volatility, which increases in the last hours of the day).

It is more difficult to visualise the evolution of the corresponding eigenvectors, since there is no natural vectors to compare them with. Furthermore, eigenvalues can “collide” and cross, resulting in an interchange between two consecutive eigenvectors. We have therefore chosen to take as a reference the eigenvectors in the opening bin , corresponding to the largest values of , . We then form the matrix of scalar products . The singular values of this matrix (equal to the square-root of the eigenvalues of ) give a measure of the overlap between the eigenspace spanned by the and that spanned by the . If the are a permutation of the , all the ’s are equal to unity, indicating maximum overlap. In particular, trivially. The evolution of the , is shown in Fig. 7 right. Using the results of [5], we conclude that all are meaningful, since in the absence of any true correlations between the and the , one would expect all singular values to lie in the interval . Therefore, although the structure of correlations clearly evolves between the opening hours and the closing hours, there is as expected a strong overlap between the principal components throughout the day.

6. Discussion & Conclusion

Let us present a synthetic account of the above empirical results, for which we only propose an interpretation stub. We have seen that during the opening hours of the market, the volatility and the dispersion of returns are high, whereas kurtosis effects are relatively low. These two quantities are different measures of the heterogeneity of stock returns, and quite paradoxically they are found to behave in opposite ways. But while the volatility and dispersion are dimensional measures of heterogeneity (measuring the spread of returns in ), the kurtosis is a relative, a-dimensional measure of surprise. What our results mean in intuitive terms is that although the typical amplitudes of stock returns are high in the morning, outliers are relatively rare, both over time and over stocks. In a sense, agitation is the norm during these early hours of trading, stocks move in different directions in such a way that the average correlation is weaker than average, and the top eigenvector of the correlation matrix is farther away from the uniform mode . But anomalously large jumps rarely take place in the morning — as expected, these jumps are more likely overnight (and are to be related to arrival of corporate specific or market-wide information), where kurtosis effects are strongest, both for single stock and cross-sectional returns. As the day proceeds, correlations increase and dispersion decreases, but unexpectedly large jumps become more probable, thereby increasing the kurtosis.

The second somewhat paradoxical effect is the dependence of the kurtosis on the index return, which was recently interpreted by L. Borland as a signature of collective behaviour during crises [4]. Again, days when the market as a whole moves a lot are also large dispersion days where all stocks move a lot in different directions, but with little outliers, i.e. one or a handful of stocks that would jump up or down. In this sense, these days are more homogeneous. Should one deduce from this that there is a stronger “synchronisation”, or collective dynamics, during these periods, as suggested by Borland? While it is true that the average correlation between stocks depends on the index return, this dependence is in fact signed: correlations are stronger for negative index returns and weaker for positive returns, see [3, 15]. This is in contrast with the kurtosis effect discussed here, which is surprisingly symmetrical (see Fig. 5). A quantitative model for this behaviour is missing at this stage. Qualitatively, however, we believe that the mechanism is the following [8]: when the index return is large, the dominant source of dispersion becomes the market exposure (the ‘’s’) of the different stocks, rather than the idiosyncratic residuals. Since the distribution of the ’s is roughly Gaussian, kurtosis effects do indeed decrease for large index returns. This interpretation however requires that the volatility of the residuals increases sub-linearly with the index volatility, as indeed suggested by the data shown in Fig. 3. The fact that during large swings of the index, the market exposure of stocks becomes the dominant factor is probably a result of index/futures arbitrage.

Finally, although large index return days are large dispersion days, the converse is not true. A typical large dispersion day is in fact a day when one or a handful of stocks gyrate wildly, contributing both to the dispersion and to the kurtosis, and explaining the positive correlation between and . If this interpretation is correct, this positive correlation should diminish when one uses the mean-absolute deviation and not the variance to compute the dispersion, since the former is less sensitive to outliers. We have checked that this is indeed the case.

To summarise, we have established several new stylised facts concerning the intra-day seasonalities of stock dynamics. Beyond the well known U-shaped pattern of the volatility, we have found that the average correlation between stocks increases throughout the day, leading to a smaller dispersion between stocks (in relative terms). However, the kurtosis, which is a measure of volatility surprises, is in fact minimum at the open of the market, when the volatility is at its peak. We have also confirmed that the dispersion kurtosis is a symmetric, markedly decreasing function of the index return. This means that during large market swings, the idiosyncratic component of the stock dynamics becomes sub-dominant, an effect that we have confirmed directly. Finally, while the market mode component of the dynamics becomes stronger as the day proceeds, the sectorial components recede. In a nutshell, early hours of trading are dominated by idiosyncratic or sector specific effects with little surprises, whereas the influence of macro, market factor increases throughout the day, and surprises become more frequent. A detailed quantitative interpretation of our results, for example of the power-law decay of the volatility in the morning, is at this stage lacking. We believe that, when available, such an interpretation will shed light on the relative importance of behavioural and informational effects on price formation and volatility.

Acknowledgements We have benefitted from insightful comments and suggestions by Rémy Chicheportiche, Stefano Ciliberti, Benoit Crespin, Laurent Laloux, Marc Potters, Pierre-Alain Reigneron and Vincent Vargas. Some of our results have been independently obtained by L. Borland (private communication and in preparation).

References

- [1] A. Admati and P. Pfleiderer. A theory of intraday patterns: Volume and price variability. Review of Financial Studies, 1:3 – 40, 1988.

- [2] T. Andersen and T. Bollerslev. Intraday periodicity and volatility persistence in financial markets. Journal of Empirical Finance, 4:115 – 158, 1997.

- [3] E. Balogh, I. Simonsen, B. Nagy, and Z. Neda. Persistent collective trend in stock markets. ArXiv e-prints, 1005.0378, 2010.

- [4] L. Borland. Statistical Signatures in Times of Panic: Markets as a Self-Organizing System. ArXiv e-prints, 0908.0111, August 2009.

- [5] J.-P. Bouchaud, L. Laloux, M. Augusta Miceli, and M. Potters. Large dimension forecasting models and random singular value spectra. Eur. Phys. J. B, 55:201, 2007.

- [6] J.-P. Bouchaud and M. Potters. Theory of financial risk and derivative pricing: from statistical physics to risk management. Cambridge University Press, 2003.

- [7] J.-P. Bouchaud and M. Potters. Financial Applications of Random Matrix Theory: a short review. ArXiv e-prints, October 2009.

- [8] R. Chicheportiche and J.-P. Bouchaud. In preparation. 2011.

- [9] P. Cizeau, M. Potters, and J.-P. Bouchaud. Correlation structure of extreme stock returns. Quantitative Finance, 1:217, 2001.

- [10] A. Joulin, A. Lefevre, D. Grunberg, and J.-P. Bouchaud. Stock price jumps: news and volume play a minor role. Wilmott Magazine, Sept/Oct, 2008.

- [11] F. Lillo and R. Mantegna. Power law relaxation in a complex system: Omori Law After a Financial Market Crash. Physical Review E, 68:016119, 2006.

- [12] F. Lillo and R. N. Mantegna. Symmetry alteration of ensemble return distribution in crash and rally days of financial markets. Eur. Phys. J. B, 15:603–606, 2000.

- [13] F. Lillo and R. N. Mantegna. Variety and volatility in financial markets. Physical Review E, 62:6126–6134, 2000.

- [14] V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. Amaral, T. Guhr, and H. E. Stanley. Random matrix approach to cross correlations in financial data. Physical Review E, 65(6):066126, 2002.

- [15] P.A. Reigneron, R. Allez, and J.-P. Bouchaud. In preparation. 2010.

- [16] D. Sornette, Y. Malevergne, and J.F. Muzy. What causes crashes? Risk, Feb., 2003.

- [17] A. Utsugi, K. Ino, and M. Oshikawa. Random matrix theory analysis of cross correlations in financial markets. Physical Review E, 70(2):026110, 2004.

- [18] A. Zawadowski, J. Kertesz, and G. Andor. Short-term market reaction after extreme price changes of liquid stocks. Quantitative Finance, 6:283–295, 2006.