A mixed effects model for longitudinal relational and network data, with applications to international trade and conflict

Abstract

The focus of this paper is an approach to the modeling of longitudinal social network or relational data. Such data arise from measurements on pairs of objects or actors made at regular temporal intervals, resulting in a social network for each point in time. In this article we represent the network and temporal dependencies with a random effects model, resulting in a stochastic process defined by a set of stationary covariance matrices. Our approach builds upon the social relations models of Warner, Kenny and Stoto [Journal of Personality and Social Psychology 37 (1979) 1742–1757] and Gill and Swartz [Canad. J. Statist. 29 (2001) 321–331] and allows for an intra- and inter-temporal representation of network structures. We apply the methodology to two longitudinal data sets: international trade (continuous response) and militarized interstate disputes (binary response).

doi:

10.1214/10-AOAS403keywords:

.and

t3Supported in part by NSF Grant SES-0631531.

1 Longitudinal network (relational) data

Radcliffe-Brown (1940) stated that an understanding of the “complex network of social relations” can be gained by measuring the relations or interactions within a set of actors. Since pairwise relations are the most elemental type of relationship, relational data which consist of measurements made on pairs of actors are ubiquitous. Our focus in this article is on relational data from the field of political science, including (1) trade between nations, and (2) militarized disputes between nations. For such data, we let denote the value of the measurement on the potentially ordered pair of actors (). In this paper we refer to social network data or relational data as the set of measurements of relations on dyads for a group of actors under study. These measurements could be binary, ordinal or continuous, as such, the methodology applies to a broad range of applications beyond those discussed in this paper.

In the case of international trade, is the directed level of trade from nation to nation . Since the relation is directed, is not necessarily equal to . Typically, social network data, directed or undirected, are represented by a socio-matrix [Wasserman and Faust (1994)], with the th row representing data for which actor is the sender, and column representing data for which is the receiver. Since the data are based on pairs of actors, the diagonal representing the relationships of actors with themselves is generally absent from the socio-matrix.

Many researchers have worked on models for this data structure. The seminal work on relational data of this form was done by Warner, Kenny and Stoto (1979), where a method of moments estimation procedure was developed based upon an ANOVA style decomposition. Models of this form have come to be known as social relations models or models for round robin data. Wong’s (1982) work derived maximum likelihood estimators for these types of models, and Gill and Swartz (2001) studied method of moments, maximum likelihood and Bayesian estimation procedures for the same problem. More broadly, Li (2002) and Li and Loken (2002) developed a general unified theory for dyadic data which derives the social relations model and other similar models from principles of group symmetry and exchangeability.

In a series of papers [Hoff, Raftery and Handcock (2002); Hoff (2003, 2005, 2007)], the social relations model was expanded in several directions: (1) A latent social space was introduced to capture patterns of transitivity, balance and clusterability that are often exhibited in dyadic data [Wasserman and Faust (1994)]; (2) A generalized linear model was developed to allow for a variety of data types (binary, ordinal and continuous); (3) A Bayesian estimation procedure was thoroughly outlined for (1) and (2) to estimate the model parameters.

However, all models mentioned thus far are for static relational data. Often, scientific questions are concerned with the evolution of networks over time. For example, in the field of international relations, questions related to the evolution of international trade or interstate conflicts are of great interest [Hoff and Ward (2003); Ward and Hoff (2007); Ward, Siverson and Cao (2007)]. In the field of biology, an understanding of the evolution of interactions of biological entities under various experimental stimuli could provide important insights [Barabasi and Oltvar (2004)]. With such applications in mind, this paper expands the social relations model to account for dependence over time.

This article proposes a model that accounts for temporal dependence among all pairwise measurements of a set of actors, thus, it falls into the realm of longitudinal data analysis methodology. To date, there has been little work on models which account for both network and temporal dependencies. A notable exception is the work by Thomas Snijders and coauthors [Huisman and Snijders 2003; Snijders, van de Bunt and Steglich (2010); Snijders, Koskinen and Schweinberger (2010)] which developed an actor-orien-ted model for network evolution that incorporated individual-level attributes. This approach is based on an economic model of rational choice, whereby individuals make unilateral changes to their networks and behaviors in order to maximize personal utility functions. Parameter estimates describe individual’s utilities for various network configurations. Parameter estimation methods for such a model have been developed into a freely-available software package (http://stat.gamma.rug.nl/siena.html), which has been applied to a number of data sets.

While this work has been groundbreaking, the applicability of an actor-oriented model may be limited to certain types of networks. As described by the primary developers of this approach [Snijders, Steglich and Schweinberger (2007)], such a model may not be appropriate in situations for which network and behavioral data might depend on unobserved latent variables. Additionally, the interpretation of the parameters in an actor-based choice model may be problematic if the data do not actually represent choices of the actors, but rather outcomes determined by other actors, which may be constrained by circumstances beyond an individual’s control. In the context of trade, for example, exports from one country to another may be determined by forces of supply and demand beyond just the pair. In the context of international conflict, countries are often unwilling participants in militarized disputes.

Recently, Hanneke, Fu and Xing (2010) considered a temporal extension of the exponential random graph modeling (ERGM) framework [Frank and Strauss (1986); Hunter and Handcock (2006); Handcock, Raftery and Tantrum (2007)]. Their work is similar to that of Thomas Snijders and coauthors in that it parameterizes various network configurations, however, they do not take an agent-based approach to the construction of the model.

Another approach to modeling dynamic network data is discussed in Xing, Fu and Song (2010). Building on ideas of Erosheva, Fienberg and Lafferty (2004) and Airoldi et al. (2005), these authors model each actor as having partial memberships to several groups. Relationships between individuals are determined by the groups of which they are members. Such models often result in a concise description of the data, as the large number of relationships between actors are summarized by the relationships between a small number of groups to which the actors belong.

In contrast to an actor-oriented utility model, ERGM, or a group-membership model, the approach we propose is more statistical, in that the main parameters in our model represent expectations and covariances of relational measurements leading to inference about network characteristics. Our reason for taking such an approach is that in the empirical study of international relations, focus is primarily on mean or regression effects and assessments of their statistical significance. As discussed in Ward and Hoff (2007), common practice is to merge data on all pairs of countries across several years and base inference on ordinary least squares estimates, treating all observations as independent. By ignoring network and temporal dependence, such an approach can potentially dramatically overestimate the significance of results and precision of estimates. One of the objectives of our methodology is to provide mean and regression estimates, by properly accounting for statistical dependencies in the data. Additionally, our modeling framework is very flexible and extendable: Using a generalized linear model framework, it can accommodate continuous and ordinal relational data. This could include data on intensity or duration of relationships, or the number of contacts between two individuals.

The next section will outline the set of possible second-order dependencies inherent in this data structure. Section 3 represents the dependencies with a mixed-effects model, and Section 4 outlines a Bayesian approach to parameter estimation. Sections 5 and 6 provide in-depth data analysis examples involving international trade and militarized disputes, including comparisons to simpler modeling approaches. A discussion follows in Section 7.

2 Dependence structure for LSR data

Figure 1 summarizes the set of pairwise (second order) potential dependencies for directed longitudinal social network data that we will consider in this article. These are the dependencies possible assuming a dependence structure in which two relational measurements are dependent if and only if they share a common actor. In the figure, three nonidentical actors and two time points are used to illustrate the dependencies. The arrow represents the random variable for a particular relationship from actor to actor at time . If we are to study patterns of international trade, might represent the monetary value of the exports from nation to nation during year . Based on the figure, two directed relations are potentially dependent only if they share a common actor, regardless of the relation’s time index. In other words, the random variables and are independent for all if .

| (a) same sender | (b) same receiver | (c) common participant |

| (d) reciprocity | (e) observational dependence |

To provide a description of the five dependencies depicted in Figure 1, let us first consider a fixed time point . Under this condition, (a) represents the potential dependence among measurements having a common sender (i.e., the “row effects”). As an example of such dependence, consider the exports from the United States and those from Morocco in a given year. Due to the overall difference in trade activity of these two nations, we might expect the exports from Morocco to other countries to be more similar in magnitude to each other than to the exports from the United States to other countries. Similarly, (b) represents potential dependence among measurements having a common receiver (i.e., the “column effects”). Considering the context of international trade again, some countries consume more goods than other countries, which could lead to within-column correlation of trade values. Next, (c) represents dependence between the relations sent and received by the same actor. For example, countries that import at a higher than average rate may also export at a higher rate. Next, (d) represents the idea of reciprocity or dependence between the directed relations of a pair of actors, such as between a pair of international trading partners or disputes between a pair of nations.

For we additionally consider temporal dependence: The figure in (e) indicates the dependence among a pair of actors across time.222In the case of nondirected network data, the minimal set of dependencies are obtained by replacing the directed edges in Figure 1 with nondirected edges. In this case, cases (a), (b) and (c) essentially represent the same dependencies, as do (d) and (e). This leaves only two minimal dependencies.

3 Mixed effects model with Markov temporal dependence

We base our longitudinal network model on multivariate normal distributions, with nonzero covariances corresponding to the dependencies represented by Figure 1. For example, we allow if . Otherwise, this covariance is zero. Based on this, the complete set of nonzero covariances are in Table 1. Such a covariance structure can be obtained via a mixed effects model, defined by equations (3)–(4) that follow:

In this model, is a fixed effect expressing the mean for , while the error term is decomposed into a set of mean-zero Gaussian random effects. This linear decomposition consists of a sending effect , a receiving effect and a residual error term . For a fixed , the network dependencies can be characterized by specifying covariance structures for the random effects in (3).

| (a) | |||

| (b) | |||

| (c) | |||

| (d) | |||

| (e) |

While Figure 1 describes the structure of the network dependencies (pairwise dependencies in the actor domain), it does not provide guidance about the structure of the temporal dependence. We accommodate temporal dependence by expanding the model to allow the random effects to be correlated over time. We consider the following first order (Markov) auto-regressive structure for the random effects:

| (2) | |||||

| (3) |

and and are independent mean-zero bivariate normal vectors with covariance matrices and :

| (4) |

The resulting covariance matrix for the vector can be written as

where depends on , and the time lag . The covariance matrix of the vector has a similar block Toeplitz structure, which we write as , and is made up of the blocks . Putting the two sources of variation together, Table 2 outlines the set of potentially nonzero covariances defined by the random effects model. The different ’s in Table 2 replace their more general counterparts, the ’s of Table 1.

| (a) | |||

|---|---|---|---|

| (b) | |||

| (c) | |||

| (d) | |||

| (e) |

Note that if we were to consider a static network, the covariances given by and would represent those for the social relations models as outlined in Warner, Kenny and Stoto (1979) and Gill and Swartz (2001). As such, those models are submodels of the one defined by equations (3)–(4).

Through the use of a generalized linear model [McCullagh and Nelder (1989)], the mixed effects model for Gaussian longitudinal social relations data can be extended to analyze relations that are not appropriately modeled by a Gaussian distribution, such as binary responses or counts. This is done by using the above model to describe a linear predictor in a generalized linear model. This leads to the following formulation:

Under the model, the ’s are conditionally independent given the ’s, so that we have

The covariance structure here is approximately that of the Gaussian model multiplied by a factor depending on the link function [Hoff (2005); Westveld (2007)], indicating that the second order dependence outlined by Figure 1 is still captured:

4 Parameter estimation

Estimation of model parameters is most easily done in the context of Bayesian inference. In this section we present a general Markov chain Monte Carlo (MCMC) algorithm for continuous data which are modeled as Gaussian, and binary data which are modeled through a particular probit formulation based on the work of Albert and Chib (1993) and Chib and Greenberg (1998).

4.1 Gaussian mixed effects model

The model fully defined by equations (3)–(4) has the following parameters that need to be estimated: A Bayesian analysis is conducted by examining the joint distribution of the parameters in given the data :

where “dmvn” stands for a multivariate normal density function and

The first double product of equation (4.1) is the density of the data given the sender–receiver random effects, the next product is the sampling distribution of the random effects, and the remaining terms are the priors for the model. We use the following semi-conjugate priors for , and :

The -parameters are constrained to ensure that the temporal processes for the sender–receiver effects and the residual error terms produce a stationary process [Reinsel (1997)]. Such a constraint allows the fixed-effects and covariance parameters to represent means and variances of the observed data over the observed time period. For an model, the constraint is satisfied if the absolute value of eigenvalues for the ’s are less than 1.

A conjugate prior for the Toeplitz matrix can be obtained by considering a transformation described by Wong (1982). In order to apply this approach to our problem, we consider the following bivariate innovations to obtain independent bivariate distributions:

Now using the property of bivariate normal distributions, we can create two independent vectors: and , where and . We use inverse-gamma priors for and : , The matrix can be constructed as and .

Based on this class of prior distributions, a Markov chain Monte Carlo approximation to the joint posterior distribution may be obtained via Gibbs sampling for the ’s and the sender–receiver effects, with a Metropolis–Hastings update for , , , and . However, the Metropolis–Hastings updates are based on their full conditional distributions. For example, consider that the full conditional distribution of is given by

| (6c) | |||||

If we were to ignore the first product [equation (6c)] and the stationarity constraint, the expression above would be proportional to a multivariate normal distribution. Since most of the information about is contained in equation (6c) and (6c), the full conditional distribution of will be close to this multivariate normal distribution. We use this approximation to the full conditional distribution as a proposal distribution, but make the necessary correction in the acceptance probability via the Metropolis–Hastings algorithm. We use a similar Metropolis–Hastings proposal for updating . Further details about the MCMC algorithm, including information for updating and , can be found in the Appendix.

4.2 Probit mixed effects model

In order to model data that are not approximately Gaussian, such as binary data, we move the Gaussian structure to a secondary level in the hierarchical model leading to the following formulation:

where represents the probability distribution of the response. For example, a probit model for binary data can be obtained by setting . For the probit model, we specify the covariance of the sender–receiver effects as before based upon the parameters and . However, as noted in Albert and Chib (1993), the variance parameter in covariance matrix is not identifiable. For ease of interpretation, we will set to be equal to one so that is a correlation matrix. In doing this, additional constraints are placed on and . Consider the following Yule–Walker equations for a first order auto-regressive process:

Since is a correlation matrix, is also a correlation matrix, with a correlation coefficient . Solving the Yule–Walker equations in terms of we have

Writing this out in terms of the individual parameters results in

Now we solve for and in terms of and to get

If we consider a Bayesian estimation algorithm, we can propose values of , and such that is a proper covariance matrix and it is guaranteed that will be a correlation matrix.

The joint density of the parameters conditional on the data is proportional to

Because of the nonidentifiability and reparameterization of discussed above, we impose constraints on and via the following priors:

To estimate the model parameters, the MCMC algorithm presented in Section 4.1 is modified in two ways: (1) is now explicitly updated, and (2) the latent response must also be updated. For most GLMs a Metropolis–Hastings step is required to update the latent response. However, the probit model allows for a Gibbs sampling procedure based upon the work of Albert and Chib (1993) and Chib and Greenberg (1998). The Gibbs sampling procedure for each and pair at times proceeds by sampling the conditional distribution for each , based on a truncated normal distribution: The truncation is to the left of zero if and to the right of zero if . Further details on the MCMC algorithm can be found in the Appendix.

5 International trade

In this section we apply the methodology to the study of yearly international trade between 58 countries from 1981–2000.333A list of countries (including their three-letter ISO codes) used in this analysis can be found in the Appendix. Additionally, the data and some of the R code used to fit the model are available as supplementary material [Westveld and Hoff (2010)]. A commonly used model for international trade is the gravity model [Tinbergen (1962)] which, based on Newton’s law of gravity, posits that the force of trade between two countries is proportional to the product of their economic “masses” divided by the distance between them (raised to some power). Taking logs, a formulation of the gravity model in the context of longitudinal trade is given by

where is the trade between two countries at time , the geographic distance between them, and and denote their gross domestic products at time .444As opposed to Ward and Hoff (2007) and Westveld (2007), real values for GDP and the level of trade were used in this paper. The reason the other works used nominal values was to avoid modeling the inflation rate for out of sample prediction. An inflator using the CPI-All Urban Consumers data was calculated to set the amounts into real values based on the year 2000. The CPI data can be obtained from the following: http:// www.bls.gov/data/home.htm. Note: this CPI data is used in the BLS inflation calculator: http://data.bls.gov/cgi-bin/cpicalc.pl.

Over the past forty years the gravity model of bilateral trade has become a benchmark for several reasons: (1) A gravity model can typically explain about one-half the variation in bilateral international commerce [Ward and Hoff (2007)]; (2) The gravity model can be derived from first principles of economic theory [Anderson (1979)]; (3) The linear formulation of the model is easy to work with empirically and readily accommodates other factors that might affect trade flows.

Following Ward and Hoff (2007), we will consider two other factors for this analysis: the polity of a nation and whether pairs of nations cooperated in militarized interstate disputes. Polity, denoted by Pol, measures a nation’s level of democracy, and ranges from 0 for highly authoritarian regimes to 20 for highly democratic ones. Cooperation in conflict, denoted by CC, measures active military cooperation. If the pair cooperated on a particular dispute, it receives a value of 1. However, if the two countries were on opposite sides of a dispute, a value of 1 is recorded. If there was more than one dispute in a single year involving the same pair, then the pair’s scores are summed over all disputes in that year. It should be noted that all of the covariates except distance are changing over time.555For further discussion of the data used in this paper, we refer the reader to Ward and Hoff (2007). This leads to the following model, which is motivated by the gravity model, additional covariates of interest and the longitudinal network structure:

with the following diffuse priors:

Initially we implemented the MCMC algorithm outlined in Section 4.1, however, we found the Markov chain to be very “sticky.” This result may have occurred since the semi-conjugate Gibbs proposals are similar to an independence proposal. In this case the distribution of the proposal should be close to the respective posterior distribution but should be “fatter” in the tails to prevent “stickiness” [Givens and Hoeting (2005)]. This would suggest that we should increase the variance of the semi-conjugate Gibbs proposals to increase the rate of mixing. However, the posterior distribution of is near the boundary for stationary processes, and increasing the variance of the proposals may lead to more unaccepted proposed values. Therefore, to safeguard against poor mixing of the chain, we randomly alternated between using (1) semi-conjugate Gibbs proposals (without an increased variance), and (2) random walk proposals around the current values of the parameters (). A Markov chain of 55,000 iterations was generated, the first 10,000 of which were dropped to allow convergence to the stationary distribution. Parameter values were saved every 20th scan, resulting in 2,250 samples with which to approximate the joint posterior distribution.

5.1 Results

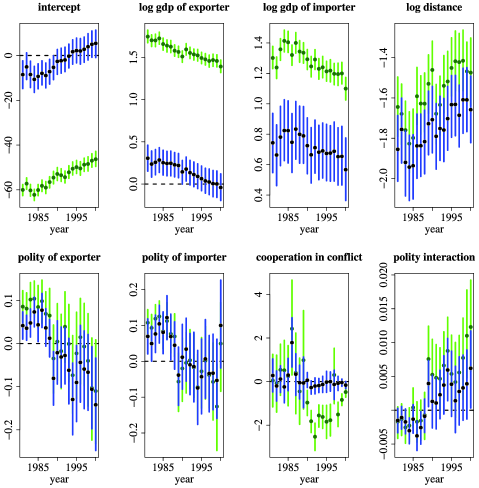

The 95% posterior credible intervals (blue bars) and their medians (black dots) for the ’s are in Figure 2. Let us first consider the panels on the top row, excluding the intercept. The posterior distributions of the coefficients in the gravity model have several features: (1) In general, the credible intervals of the coefficients for the of the exporter are shifting downward over the period. Additionally, these intervals contain zero from 1994 to 2000, heuristically suggesting that this covariate is becoming a less important correlate of bilateral trade flows. (2) The coefficients for the of the importer over the period are all positive, suggesting that the economic size of the importer is an important factor in bilateral trade flows. (3) As might be expected, over the twenty-year period the medians of the coefficients for distance are generally decreasing. An intuitive explanation is that the transportation of goods and services has become more efficient over the period.

The four panels on the bottom row of Figure 2 are the results for the additional predictors of trade beyond the gravity model. There appears to be a general decline in the coefficients for the main effects of polity of the exporter and importer over the period, with a notable exception for the latter in the year 2000 (the 95% credible interval still contains zero). However, there appears to be a rising trend in the coefficients of polity interaction () over the period. The trend suggests that trade between democratic countries is increasing faster than the average. Finally, for the polity coefficients in general we see that our estimate is becoming more uncertain over time, as the credible intervals are widening over the period. A plausible explanation for this phenomenon is that the countries under study are becoming more democratic, thus, there is less variation in the polity covariate. The sample mean and variance of the polity score for 1980 are 3.62 and 56.66, respectively, while in 2000 they are 7.43 and 20.56. Based upon the model, whether two nations cooperate in conflicts is not indicative of the level of trade between them, except for the notable case of 1986, where bilateral trade is positively correlated with military cooperation.

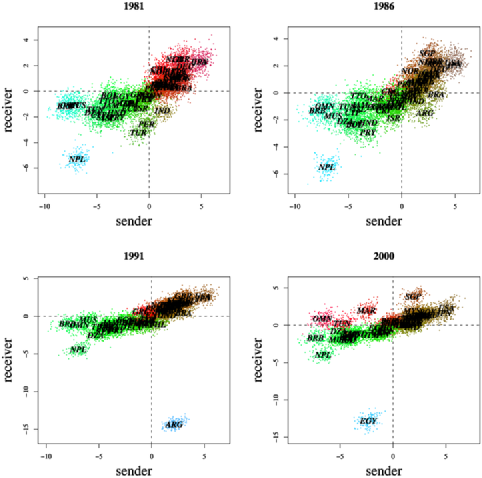

We now examine the posterior distributions of the country-specific sender and receiver random effects. These effects describe the average deviations of a country’s export and import levels from those that would be predicted by the regression model alone. In Figure 3 the colored dots are a random sample of 150 values from the bivariate posterior distribution of the sending and receiving effects for each country, and the country labels are located at the posterior means. Countries that are close to each other, based on their posterior mean, are similar in color. As might be expected, we see in each plot that there exists a strong positive relationship between exporting (sending) and importing (receiving) and that the relative positions of the nations change only slightly over the four years shown in the figure. This strong positive relationship suggests a possible model simplification for these data in which the sender and receiver effects are co-linear, although such a model reduction may not be appropriate for other data sets.

=224pt

Parameter

Markov chain

2.5%

Median

97.5%

![[Uncaptioned image]](/html/1009.1436/assets/x8.png)

![[Uncaptioned image]](/html/1009.1436/assets/x9.png)

![[Uncaptioned image]](/html/1009.1436/assets/x10.png)

![[Uncaptioned image]](/html/1009.1436/assets/x11.png)

![[Uncaptioned image]](/html/1009.1436/assets/x12.png)

![[Uncaptioned image]](/html/1009.1436/assets/x13.png)

![[Uncaptioned image]](/html/1009.1436/assets/x14.png)

A closer examination of the plots reveals that the United States (USA), Germany (DEU), Japan (JPN) and the United Kingdom (GBR) are located at the top right corner for most of these plots, and thus are considered some of the most active nations in the network, even after accounting for their covariate information. On the other hand, nations such as Nepal (NPL), Oman (OMN), Barbados (BRB) and Mauritius (MUS) are among the least active, based on their location in the plots. Over the period, the rise of East Asian countries through trade is exemplified by the movement of Singapore (SGP) on the receiving axis—the 95% credible interval of Singapore’s receiving position in 2000 minus its receiving position in 1981 is (1.449, 3.967). Finally, note the dip in imports to Argentina (ARG) in 1991 and Egypt (EGY) in 2000. In each situation, the value of imports from all countries in the data is zero. It is unlikely that there were no imports for either country for those years. A plausible explanation for the imports to Argentina being “zeroed-out” might be due to a currency reform that the country undertook in 1991. As for the Egyptian case, around the year 2000 there was not a period of financial instability, suggesting that the zero imports are an aberration in the data. We note that, by allowing for time and country-specific importer and exporter effects, our estimates of the regression coefficients will be fairly robust to such outliers.

The assumption of a stationary covariance structure allows us to interpret the the marginal covariances and as across-year average covariances. Using the posterior samples from and , the empirical posterior distributions for and can be computed. The results are in Table 3, which presents the trace plots of the Markov chains along with the 95% credible intervals and posterior medians. Notice that the medians of the posterior distributions for and coincide with the spread of the posteriors of the sender–receiver estimates for the nations (Figure 3). Also from the table we see that: (1) the median posterior correlation between the sending and receiving effects is 0.705, and (2) the median posterior residual correlation within a pair of nations is 0.323. The latter suggests a modest degree of reciprocity among pairs of actors in the network at a given point in time.

| Parameter | Markov chain | 2.5% | Median | 97.5% |

|---|---|---|---|---|

We also examine the auto-regressive coefficients to see what effect the previous year has on exports, imports and reciprocity for the current year. From Table 4, the medians of the posterior distributions of and are 0.997 and 0.005, respectively. This suggests that the level of exports this year is highly dependent on level of exports from the previous year but perhaps not dependent on imports from the previous year. Comparatively, the medians of the posterior distribution for and are 0.572 and 0.161, respectively. That is, the level of imports this year is fairly dependent on imports from the previous year and somewhat dependent on exports from the previous year, indicating a possible effect of increased purchasing power after a year of high exports. Since the median of the posterior distribution of is 0.106, we see that a relatively small amount of positive reciprocity in a given year can be explained by the level of reciprocity in the previous year.

5.2 Out-of-sample prediction

In order to investigate the possibility that we are overfitting the data, we randomly deleted 25% of the responses, amounting to 16,120 cases, and compared the out-of-sample predictions for the LSR model with covariates (M1) against four submodels (M2–M5). The first submodel (M2) used the LSR structure but did not use any covariate information (). The rest of the submodels considered (M3–M5) used covariate information along with either only network dependence, only temporal dependence, or neither dependence structure:

-

[(M5)]

-

(M3)

Social Relations Model:

-

(M4)

AR(1) Model:

-

(M5)

Standard Regression Model:

| Model | Temporal dep. | Network dep. | MSE |

|---|---|---|---|

| (M1) LSR Cov | yes | yes | |

| (M2) LSR mean | yes | yes | |

| (M4) AR(1) | yes | no | |

| (M3) Social relations | no | yes | |

| (M5) Standard regression | no | no |

For each of the five models, we used the median of the posterior of the missing values as our predictor and compared the overall predictions using the mean squared error score. Table 5 presents these scores for the LSR model with covariates and the four submodels. From the ranking, the LSR model with covariates has the best performance, suggesting that we may not be overfitting the data. Interestingly, the next best model is the LSR mean model and is just slightly worse than M1, suggesting that the covariates add little to the predictive performance after the network and temporal dependence structures are taken into account. The fact that the AR(1) model is next and performs better than the Social Relations model suggests that there are strong temporal dependencies in the data and these dependencies may be more critical than capturing the second order network dependencies. As might be expected, the standard regression model performs substantially worse than the others. Finally, it is interesting to examine the estimates of the ’s for the standard regression model against those of the LSR model, which accounts for the temporal and network dependence inherent in the data. The results are shown graphically in Figure 4. The figure illustrates two main points: (1) Even though the model for the expected value, unconditional on the random effects, is the same (), there is a definite difference in the estimated values of the coefficients; (2) The 95% credible intervals for standard regression are generally shorter than those for the LSR model. However, the length of the intervals of the ’s for the polity of the exporter, cooperation in conflict and polity interaction are actually shorter for the LSR model compared to those of the standard regression model. These results illustrate that accounting for dependency in data typically increases the nominal precision of the estimated coefficients, but this is not always the case, and depends on the distribution of the covariates themselves.

6 Militarized interstate disputes

Jones, Bremer and Singer (1996) defined the term militarized interstate dispute (MID) as an event “in which the threat, display or use of military force short of war by one member state is explicitly directed toward the government, official representatives, official forces, property, or territory of another state.” In this analysis, we will investigate the patterns of MIDs in the Middle East and United States from 1991 to 2000.666A list of countries used in this analysis (including their three-letter ISO code) can be found in the Appendix. Additionally, the data and some of the R code used to fit the model are available as supplementary material [Westveld and Hoff (2010)]. For this data analysis, is the binary indicator of a MID initiated by country with target in year . We are interested in relating the response to the following covariates: (1) the ordinal level of alliance between and , ranging from 0 (no alliance) to 3 (will defend each other militarily), (2) the real value of the log trade from to , (3) the real value of the log trade from to , (4) the number of inter-governmental associations of which both nations are members, and (5) the log distance between the two nations. Note that all of the covariates, except distance, are potentially changing over time.

As discussed in Section 4.2, for the probit mixed effects model the variance of is set to one, leading to additional restrictions on the priors for , and . Specifically, we considered the following set of diffuse priors:

The posterior distribution for these parameters was approximated witha Markov chain Monte Carlo algorithm consisting of 7 million scans. The first two million of these scans were dropped to allow for convergence to the stationary distribution. Parameter values were saved every 1,000th scan, resulting in 5,000 samples for each parameter with which to approximate the posterior distribution.

6.1 Results

Figure 5 presents the 95% credible intervals for the coefficients of the covariates. We focus attention on the intervals not containing zero (with high credibility), suggesting an effect on MIDs. Overall, the pattern of the intervals for the level of alliance between a pair of nations appears mixed. As might be expected, for four of the years (1993, 1996, 1997, 1999) the medians are below zero, suggesting a negative impact on MIDs for higher levels of alliance—in 1999, the empirical probability that the coefficient is below zero is 79%. However, in 1991 and 1994, it appears that the higher the level of alliance between two nations, the more likely that they would have a MID. A possible reason for this paradox is that Oman has the only level 3 alliances in the data and in 1991 it had disputes with both Iraq and Jordan, and in 1994 it had a dispute with Iraq. The effect of the number of inter-governmental organizations to which a pair of nations belong also appears to be minimal over the period, except for the year 1993. The effects of the log of exports from the initiator to the target and the log of imports from the target to the initiator are very interesting. Over the period, there appears to be a slight trend for the coefficients of both of the covariates (with extremely large variability in the final year).777We also fit the model without the year 2000 and found the precision of the ’s for 1991–1999 to be similar to those in Figure 5. These trends suggest that the more a potential initiator of a dispute exports to a particular nation, the less likely it is for a dispute to occur. This is in contrast to importing from a particular country. Finally, distance appears to be a deterrent to conflict; the farther a pair of nations are from each other, the smaller the chance of a militarized dispute between the pair.

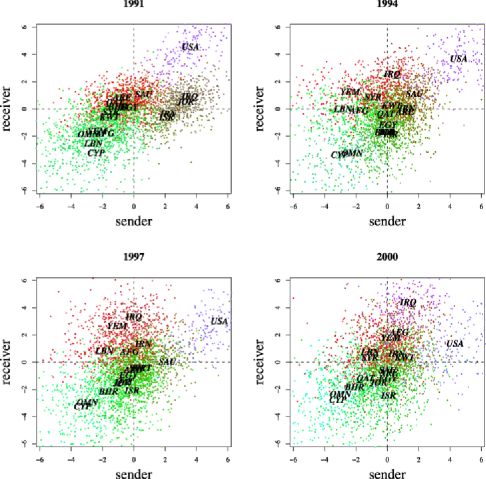

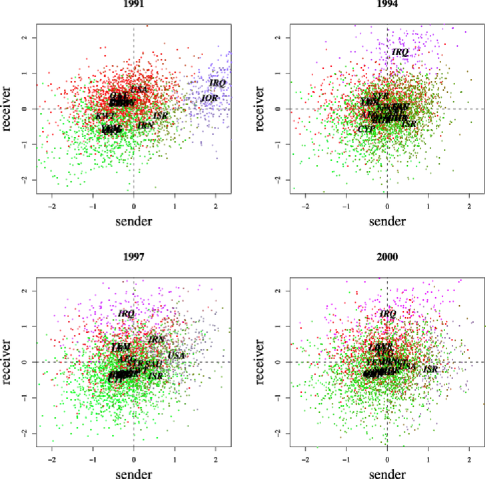

Figure 6 presents 200 random samples from the bivariate posterior distribution of the sender and receiver effects for each country. These effects represent deviations of the country-specific rates of initiating and receiving MIDs from what would be predicted by a probit regression model alone. From the figure, we see that there are some nations for which the distributions do not overlap, suggesting differences between the nations with respect to their sending and receiving effects. There appears to be a positive correlation between the sending and receiving of militarized disputes—the median correlation turns out to be 0.563 (Table 6). As the United States (USA) is near the far right corner for all the plots in the figure, it is the most active in the network over the period. This suggests that the United States has far more disputes than would be expected, given just its covariate information. In particular, since distance is generally a significant deterrent to disputes, the United States has far more disputes than would be expected, based on its distance from the Middle East. Note that in 1991, Iraq (IRQ) and Jordan (JOR) are also high initiators of disputes. However, Oman (OMN), Lebanon (LBN) and Cyprus (CYP) neither initiate nor are the target of many disputes over the period. In contrast, the results can be compared to those in Figure 7, where the analysis was conducted without the covariates; that is, only a mean was fit at each point in time (). Now the United States is no longer in the upper right-hand corner of the plots. However, Cyprus is still in the lower left-hand corner of all the plots. In this case, accounting for influential covariate information induces greater variability in the sender–receiver random effects.

| Parameter | Markov chain | 2.5% | Median | 97.5% |

|---|---|---|---|---|

Tables 6 and 7 describe the variability of the sender and receiver effects and the temporal variation. The median of is 0.683, and while the 95% credible interval is quite spread out, its range is completely above zero, suggesting a certain amount of positive reciprocity in the network at a given point in time. However, since the median of the posterior distribution of is 0.189 (and this interval partially contains zero), we see that positive reciprocity in a given year may not be readily explained by the level of reciprocity in the previous year. Since the median of the posterior distributions for and are 0.761 and 0.245, respectively, we see that the initiation of disputes by a particular nation depends to a large degree on whether they initiated disputes in the previous year and, to a lesser extent, on whether they were a target in the previous year. Finally, the median of the posterior distributions for and are 0.909 and 0.029, respectively. This suggests that whether a nation is a target this year depends heavily on whether they were a target in the previous year, but depends very little on whether they initiated disputes in the previous year.

7 Discussion

This paper has developed a framework that incorporates temporal dependence within the domain of social relations regression models. We showed that our particular mixed effects model can account for both second order network dependence and temporal dependence. By placing the temporal dependence on the random effects representing the network dependence, the network is allowed to evolve over time. Additionally, a generalized linear modeling framework was developed and a general Bayesian estimation approach was outlined. Specific examples for Gaussian and binary responses were illustrated and applied to the study of international trade and militarized interstate disputes, respectively. The incorporation of temporal dependence allowed for insight into the network of international trade by noting that after accounting for covariate information, the level of exports in a given year is highly dependent on the level from the previous year, but not dependent on the level of imports. Conversely, the level of imports in a particular year is fairly dependent on imports from the previous year and only somewhat dependent on exports the previous year. Additionally, only a slight degree of reciprocity can be explained by the level of reciprocity in the previous year.

| Parameter | Markov chain | 2.5% | Median | 97.5% |

|---|---|---|---|---|

Appendix A MCMC algorithm for the Gaussian case

Parameter estimation is conducted through the construction of a Markov chain in the parameters . The following MCMC algorithm presents one possible construction:

-

[6.]

-

1.

Sample from its full conditional distribution, where

-

2.

Sample each , , from its full conditional distribution, where

-

3.

Sample from a distribution, where

-

[(b)]

-

(a)

Calculate from and and compute the Metropolis–Hastings ratio:

-

(b)

Accept with probability

-

-

4.

Sample from a distribution, where

-

[(b)]

-

(a)

Calculate from and and compute the Metropolis–Hastings ratio:

-

(b)

Accept with probability

-

-

5.

Sample from an inverse-Wishart distribution, where

-

[(b)]

-

(a)

Calculate from and and compute the Metropolis–Hastings ratio:

-

(b)

Accept with probability

-

-

6.

Sample a proposal for as follows:

where , and set and .

-

[(b)]

-

(a)

Calculate from and and compute the Metropolis–Hastings ratio:

-

(b)

Accept with probability

-

-

7.

Sample the missing data from its full conditional distribution, where

-

[(b)]

-

(a)

:

-

(b)

:

-

(c)

:

-

Appendix B MCMC algorithm for the probit model

In order to augment the previous algorithm for the probit LSR model, the Gibbs sampling procedure for each and pair at the following times proceeds by sampling the conditional distribution for each , based on a truncated normal distribution; the truncation is to the left of zero if and to the right of zero if :

The means and variances of for have the same expressions as those for in Step 7 of Appendix A. For we simply suggest using a Metropolis–Hastings update using an uniform proposal distribution around the current value. The range of this distribution is the only tuning parameter in the Markov chain Monte Carlo algorithm.

Appendix C Set of nations in the trade application

Algeria (DZA), Argentina (ARG), Australia (AUS), Austria (AUT), Barbados (BRB), Belgium (BEL), Bolivia (BOL), Brazil (BRA), Canada (CAN), Chile (CHL), Colombia (COL), Costa Rica (CRI), Cyprus (CYP), Denmark (DNK), Ecuador (ECU), Egypt (EGY), El Salvador (SLV), Finland (FIN), France (FRA), Germany (DEU), Greece (GRC), Guatemala (GTM), Honduras (HND), Iceland (ISL), India (IND), Indonesia (IDN), Ireland (IRL), Israel (ISR), Italy (ITA), Jamaica (JAM), Japan (JPN), Malaysia (MYS), Mauritius (MUS), Mexico (MEX), Morocco (MAR), Nepal (NPL), Netherlands (NLD), New Zealand (NZL), Norway (NOR), Oman (OMN), Panama (PAN), Paraguay (PRY), Peru (PER), Philippines (PHL), Portugal (PRT), Republic of Korea (KOR), Singapore (SGP), Spain (ESP), Sweden (SWE), Switzerland (CHE), Thailand (THA), Trinidad and Tobago (TTO), Tunisia (TUN), Turkey (TUR), United Kingdom (GBR), United States (USA), Uruguay (URY), Venezuela (VEN).

Appendix D Set of nations in the MIDs application

Afghanistan (AFG), Bahrain (BHR), Cyprus (CYP), Egypt (EGY), Iran (IRN), Iraq (IRQ), Israel (ISR), Jordan (JOR), Kuwait (KWT), Lebanon (LBN), Oman (OMN), Qatar (QAT), Saudi Arabia (SAU), Syria (SYR), United Arab Emirates (ARE), United States (USA), and Yemen (YEM).

Acknowledgments

The authors would like to thank the Associate Editor and referees for their advice on this manuscript. Additionally, we are appreciative to both Michael D. Ward and Xun Cao for collecting and supplying the data used in this paper. Finally, the corresponding author would also like to thank Grace S. Chiu, Patrick J. Heagerty, Kevin M. Quinn and Michael D. Ward for enlightening discussions on this topic.

[id=suppA] \stitleData and R Code for the Examples \slink[doi]10.1214/10-AOAS403SUPP \slink[url]http://lib.stat.cmu.edu/aoas/403/supplement.zip \sdatatype.zip \sdescriptionA zip file associated with the paper contains the data and some of the R code used in the examples.

References

- Airoldi et al. (2005) Airoldi, E., Blei, D. Xing, E. and Fienberg, S. (2005). A latent mixed membership model for relational data. In Proceedings of the 3rd International Workshop on Link Discovery 82–89. ACM, New York.

- Albert and Chib (1993) Albert, J. H. and Chib, S. (1993). Bayesian analysis of binary and polychotomous response data. J. Amer. Statist. Assoc. 88 669–679. \MR1224394

- Anderson (1979) Anderson, J. E. (1979). A theoretical foundation for the gravity equation. American Economic Review 69 106–116.

- Barabasi and Oltvar (2004) Barabasi, A.-L. and Oltvar, Z. N. (2004). Network biology: Understanding the cell’s functional organization. Nat. Rev. Genet. 5 101–113.

- Chib and Greenberg (1998) Chib, S. and Greenberg, E. (1998). Analysis of multivariate probit models. Biometrika 2 347–361.

- Erosheva, Fienberg and Lafferty (2004) Erosheva, E., Fienberg, S. and Lafferty, J. (2004). Mixed-membership models of scientific publications. In Proceedings of the National Academy of Sciences of the United States of America 101 5220–5227.

- Frank and Strauss (1986) Frank, O. and Strauss, D. (1986). Markov graphs. J. Amer. Statist. Assoc. 81 832–842. \MR0860518

- Gill and Swartz (2001) Gill, P. S. and Swartz, T. B. (2001). Statistical analyses for round robin interaction data. Canad. J. Statist. 29 321–331. \MR1840712

- Givens and Hoeting (2005) Givens, G. H. and Hoeting, J. A. (2005). Computational Statistics. Wiley, Hoboken, NJ. \MR2112774

- Handcock, Raftery and Tantrum (2007) Handcock, M. S., Raftery, A. E. and Tantrum, J. (2007). Model-based clustering for social networks. J. Roy. Statist. Soc. Ser. A 170 301–354. \MR2364300

- Hanneke, Fu and Xing (2010) Hanneke, S., Fu, W. and Xing, E. P. (2010). Discrete temporal models for social networks. Electronic Journal of Statistics 4 585–605.

- Hoff (2003) Hoff, P. D. (2003). Random effects models for network data. In Dynamic Social Network Modeling and Analysis: Workshop Summary and Papers (R. Breiger, K. Carley and P. Pattison, eds.) 303–312. National Academies Press, Washington, DC.

- Hoff (2005) Hoff, P. D. (2005). Bilinear mixed-effects models for dyadic data. J. Amer. Statist. Assoc. 100 286–295. \MR2156838

- Hoff (2007) Hoff, P. D. (2007). Model averaging and dimension selection for the singular value decomposition. J. Amer. Statist. Assoc. 102 674–685. \MR2325118

- Hoff, Raftery and Handcock (2002) Hoff, P. D., Raftery, A. E. and Handcock, M. S. (2002). Latent space approaches to social network analysis. J. Amer. Statist. Assoc. 97 1090–1098. \MR1951262

- Hoff and Ward (2003) Hoff, P. D. and Ward, M. D. (2003). Modeling dependencies in international networks. Technical report. Center for Statistics and the Social Sciences, Univ. Washington, Seattle, WA.

- Huisman and Snijders (2003) Huisman, M. and Snijders, T. A. B. (2003). Statistical analysis of longitudinal network data with changing composition. Sociol. Methods Res. 32 253–287. \MR1982524

- Hunter and Handcock (2006) Hunter, D. R. and Handcock, M. S. (2006). Inference in curved exponential family models for networks. J. Comput. Graph. Statist. 15 565–583. \MR2291264

- Jones, Bremer and Singer (1996) Jones, D. M., Bremer, S. A. and Singer, J. D. (1996). Militarized interstate disputes, 1816–1992: Rationale, coding rules, and emirical patterns. Conflict Manegment and Peace Science 15 163–213.

- Li (2002) Li, H. (2002). Modeling through group invariance: An interesting example with potential applications. Ann. Statist. 30 1069–1080. \MR1926168

- Li and Loken (2002) Li, H. and Loken, E. (2002). A unified theory of statistical analysis and inference for variance component models for dyadic data. Statist. Sinica 12 519–535. \MR1902723

- McCullagh and Nelder (1989) McCullagh, P. and Nelder, J. A. (1989). Generalized Linear Models. Chapman & Hall/CRC, Washington, DC. \MR0727836

- Radcliffe-Brown (1940) Radcliffe-Brown, A. R. (1940). On social structure. The Journal of the Royal Anthropological Institute of Great Britain and Ireland 70 1–12.

- Reinsel (1997) Reinsel, G. C. (1997). Elements of Multivariate Time Series Analysis. Springer, New York. \MR1451875

- Snijders, Steglich and Schweinberger (2007) Snijders, T. A. B, Steglich, C. E. G. and Schweinberger, M. (2007). Modeling the co-evolution of networks and behavior. In Longitudinal Models in the Behavioral and Related Sciences (K. van Montfort, J. Oud and A. Satorra, eds.) 41–71. Routledge Academic, London.

- Snijders, van de Bunt and Steglich (2010) Snijders, T. A. B., van de Bunt, G. G. and Steglich, C. E. G. (2010). Introduction to stochastic actor-based models for network dynamics. Social Networks 32 44–60.

- Snijders, Koskinen and Schweinberger (2010) Snijders, T. A. B., Koskinen, J. and Schweinberger, M. (2010). Maximum likelihood estimation for social dynamics. Ann. Appl. Statist. 4 567–588.

- Tinbergen (1962) Tinbergen, J. (1962). Shaping the World Economy-Suggestions for an International Economic Policy. The Twentieth Century Fund, New York.

- Ward and Hoff (2007) Ward, M. D. and Hoff, P. D. (2007). Persistent patterns of international commerce. Journal of Peace Research 44 157–175.

- Ward, Siverson and Cao (2007) Ward, M. D., Siverson, R. M. and Cao, X. (2007). Disputes, democracies, and dependencies: A reexamination of the Kantian Peace. American J. Political Sci. 51 583–601.

- Warner, Kenny and Stoto (1979) Warner, R. M., Kenny, D. A. and Stoto, M. (1979). A new round robin analysis of variance for social interaction data. Journal of Personality and Social Psychology 37 1742–1757.

- Wasserman and Faust (1994) Wasserman, S. and Faust, K. (1994). Social Network Analysis: Methods and Applications. Cambridge Univ. Press, Cambridge.

- Westveld (2007) Westveld, A. H. (2007). Statistical methodology for longitudinal social network data. Ph.D. thesis, Dept. Statistics, Univ. Washington, Seattle, WA. \MR2717382

- Westveld and Hoff (2010) Westveld, A. H. and Hoff, P. D. (2010). Supplement to “A mixed effects model for longitudinal relational and network data, with applications to international trade and conflict.” DOI: 10.1214/10-AOAS403SUPP.

- Wong (1982) Wong, G. Y. (1982). Round robin analysis of variance via maximum likelihood. J. Amer. Statist. Assoc. 77 714–724.\MR0686400

- Xing, Fu and Song (2010) Xing, E. P., Fu, W. and Song, L. (2010). A state-space mixed membership blockmodel for dynamic network tomography. Ann. Appl. Statist. 4 535–566.