High order recombination and an application to cubature on Wiener space

Abstract

Particle methods are widely used because they can provide accurate descriptions of evolving measures. Recently it has become clear that by stepping outside the Monte Carlo paradigm these methods can be of higher order with effective and transparent error bounds. A weakness of particle methods (particularly in the higher order case) is the tendency for the number of particles to explode if the process is iterated and accuracy preserved. In this paper we identify a new approach that allows dynamic recombination in such methods and retains the high order accuracy by simplifying the support of the intermediate measures used in the iteration. We describe an algorithm that can be used to simplify the support of a discrete measure and give an application to the cubature on Wiener space method developed by Lyons and Victoir [Proc. R. Soc. Lond. Ser. A Math. Phys. Eng. Sci. 460 (2004) 169–198].

doi:

10.1214/11-AAP786keywords:

[class=AMS] .keywords:

.and

t1Supported by the Leverhulme trust Grant F/08772/E. Final version of the paper prepared at TU Berlin spported by ERC Grant 258237 (FP7/2007-2013).

t2Supported by the EPSRC Grant EP/H000100/1.

1 Introduction

In pricing and hedging financial derivatives, as well as in assessing the risk inherent in complex systems, we often have to find approximations to expectations of functionals of solutions to stochastic differential equations (SDE). We consider a Stratonovich stochastic differential equation

defined by a family of smooth vector fields and driven by Brownian motion. It is well known that computing corresponds to solving a parabolic partial differential equation (PDE). High dimension and hypo-ellipticity are common obstacles that arise when one calculates these quantities numerically. When facing these obstacles some classical computational methods become unstable and/or intractable.

There are many settings where one is interested in tracking the evolution of a measure over time in an effective numerical fashion. One example is the numerical approximation to the solution of a linear parabolic PDE. In this case, one tracks the evolution of the heat kernel measure associated to the PDE. Another example is the filtering problem where one wishes to approximate the unnormalized conditional distribution of the signal, which is governed by a stochastic partial differential equation known as the Zakai equation.

An evolving measure can be viewed as a path in the space of measures. Thus, even if the underlying state space is finite dimensional, we potentially face an infinite-dimensional problem. Particle approximations can, in many cases, provide good descriptions of evolving measures (see, e.g., the survey articles Cr , CrDou1 ). Higher order methods may allow us to take far fewer time steps than classical methods in the approximations. An example of a higher order particle method may be found in Kusuoka kusuoka3 . Although effective in practice (compare Ninomiya ninomiya and Ninomiya and Victoir ninomiya-victoir ), these methods have the drawback that the number of particles can explode exponentially if the process is iterated and accuracy preserved (see, e.g., Lyons and Victoir lyons ).

Sometimes the essential properties of a probability measure we care about can accurately be described and captured by the expectations of a finite set of test functions. If we can find such a family of test functions we can replace the original measure with a simpler measure with smaller support that integrates all test functions correctly and hence, still has the right properties, provided, of course, the number of test functions is small compared to the cardinality of the support of the original measure. We will also insist that the reduced measure has . This condition ensures that feasibility constraints imposed on the measure will also be satisfied by . For a finite Borel measure on a polish space and a set of integrable functions , we can show that such a reduced measure always exists with .

In this paper we present a simple algorithm that can be used to compute reduced measures for discrete measures . The runtime is polynomial in the size of the support of the measure . The algorithm relies on the observation that if is the valued random variable and the law of under the measure , then finding a reduced measure is equivalent to finding a discrete measure on with and the same center of mass (CoM) as .

We describe an application to the Kusuoka–Lyons–Victoir (or KLV cubature on Wiener space) method developed by Lyons and Victoir lyons , following Kusuoka kusuoka3 . It provides higher order approximations to if the test function is Lipschitz and the vector fields satisfy Kusuoka’s UFG condition (see kusuoka2 ) which is weaker than the usual Hörmander condition. The expectation might be viewed as an infinite-dimensional integral against Wiener measure. The authors construct discrete cubature measures supported on continuous paths of bounded variation that approximate Wiener measure in the sense that they integrate iterated integrals up to a fixed degree correctly. The expectation of a Wiener functional against the discrete cubature measure may be obtained by computing the endpoints of the solution of the SDE along the paths in the support of . Thus the KLV method might be viewed as a discrete Markov kernel taking discrete measures on to discrete measures on . More explicitly we have

and

The bound on the error when replacing the Wiener measure with a cubature measure is given in terms of higher order derivatives of , so in general will not be small as is only assumed to be Lipschitz. The results in Kusuoka and Stroock kusuoka1 and Kusuoka kusuoka2 show that will be smooth, at least in the direction of the vector fields . This is resolved by applying the method iteratively over a partition of the time interval . The operator corresponding to the iterated application of the KLV method is Markov and hence, the error of the approximation of on the global time interval is the sum of the error of the approximations over the subintervals of the partition. So considering an uneven partition of the global time interval with time steps getting smaller toward the end, we can iteratively apply the cubature method over the subintervals and reduce the error in the approximation to any accuracy. If is the degree of the cubature formula, we can find a partition such that the error in the weak approximation is uniformly bounded by

where is the number of time steps in the partition and a constant independent of and .

The iterated KLV method might be viewed as a particle system on where the particles branch in an -ary tree. Hence, the number of ODEs to solve grows exponentially in the number of iterations. In this paper we add recombination to the KLV method. After each application of the KLV operation we replace the intermediate measures by reduced measures. The property of the KLV measure we are targeting is to integrate , the heat kernel applied to , correctly. We have identified a finite set of test functions that ensures that the bound on the overall error of the approximation of is only increased by a constant factor and hence, the modified method has the same convergence properties. Moreover, we can show that under the Hörmander condition for bounded vector fields the number of test functions required grows polynomially in the number of iterations.

We finish the paper with a toy numerical example that illustrates how one blends the methods of this paper together in a concrete example to compute a solution of a one-dimensional PDE to high accuracy when the boundary data is piecewise smooth and the discontinuities are not known to the PDE solver.

We believe that the combination of the two ideas—higher order particle methods to describe the evolution of a measure on the one hand and simplifying the support of the measures used in the description, by characterizing essential properties of a measure using the expectations of a finite set of test functions on the other hand—have more general applications than investigated so far. Applications to the stochastic filtering problem appear to be particularly promising (see Litterer and Lyons litterer , litterer2 for an outline).

2 A reduction algorithm for the support of a discrete measure

Let us start the precise description of the reduction problem. The notation in this section is independent of the notation used in the description of the cubature method in the following sections. Consider a finite set of test functions on , a measure space with a finite discrete measure

with large support. By this we mean that is at least of order . In the following we assume that is a probability measure, that is, the weights add up to one.

Definition 1.

We will call a discrete probability measure a reduced measure with respect to and if it satisfies the following three conditions:

[(3)]

.

For all

.

The first condition is more important than it looks as it ensures that feasibility constraints imposed on samples drawn from will also be satisfied by . We wish to construct effective algorithms to compute the reduced measure.

Let be the -valued random variable defined on . Then the law of is the discrete measure on

| (1) |

The center of mass (CoM) for the measure is given by

| (2) |

To find a reduced measure we articulate an equivalent problem in terms of . The problem becomes finding a subset of the points and positive weights to produce a new probability measure such that . A reduced measure is then easily obtained from by taking

with satisfying .

Note that given any subset there exist suitable weights if and only if is contained in the convex hull of these points. Caratheodory’s theorem implies that in principle one can always find with support having cardinality at most and the algorithm explained below provides a constructive proof to that.

By considering in place of the , we may assume without loss of generality that is at the origin. We may also assume that the are all distinct, as we can otherwise eliminate points from the original measure by sorting and combining them.

A first algorithm (Algorithm 1), communicated to us by Victoir victoir , sequentially eliminates particles from the support of the measure. It is well known and has, for example, been used in constructive proofs of Tchakaloff’s theorem (Davis davis ).

Given any points, the system given by

| (3) | |||||

is a linear system with variables, but only constraints. Therefore, it has a nontrivial solution, which may, for example, be determined using Gaussian elimination. Thus we may either add

to (2) or subtract

from (2) leaving all weights in the result nonnegative and their overall sum unchanged. In either case, by construction, the coefficient of some vanishes. We now have obtained a new probability measure with the same center of mass and at least one point less in the support. Applying the procedure iteratively until there are only points left, we obtain a reduced measure. Clearly the method requires no more than iterations of the above procedure.

Remark 2.

If is the dimension of the lowest-dimensional (affine) subspace of containing the set , we can continue to apply the elimination procedure described in Algorithm until .

For improving the order of the overall algorithm we now look at suitable linear combinations instead of points.

To describe the algorithm we define an abstract procedure that takes a discrete probability measure with particles in its support and returns another discrete probability measure with particles in its support satisfying and . Procedure may, for example, be realized by applications of the reduction procedure of Algorithm 1.

Main reduction algorithm (Algorithm 2): (1) Partition the support of into sets of as near equal size as possible. Let these sets be denoted by , .

(2) Compute the probability measure where

and .

(3) Apply procedure to compute a measure with .

(4) Repeat (1)–(3) with

for until particles are left in the support of .

Proposition 3.

Given and , the algorithm described above requires iterations of procedure to compute a reduced measure.

We might interpret the points as the respective center of masses of the individual subsets .

It is clear that has positive weights and support contained in the support of . Hence, we only need to show that .

We have

As , we may assume without loss of generality that . It is obvious that each iteration halves the number of particles in the support of and we require exactly iterations.

Corollary 4

Using the main reduction algorithm we can compute a reduced measure with respect to and in

steps where represents the number of steps required to solve a system of linear equations with variables and constraints.

To compute the intermediate measures , we need to calculate -dimensional linear combinations. The number of steps required for these additions is bounded above by the series

The procedure may be realized by applications of the reduction procedure used in Algorithm 1 described above.

Remark 5.

Note that the linear systems of equations we need to solve in the algorithm are singular. Hence, for a practical implementation we have used a method based on the singular value decomposition (SVD) to avoid numerical instability.333A dll with an implementation of a version of the algorithm and a Visual Studio project with a simple example for its use can currently be found at http://www.maths.ox.ac.uk/ ~tlyons/Recombination/reduce_dist_01_paper.zip.

If the support of the measure we wish to target is particularly large or possibly even infinite, we can consider a different approach. If we can find a subset of points that with a reasonably high probability contains the CoM in its convex hull, we may use linear programming to check if a given set of points contains the CoM in its convex hull and reconstruct the weights. The results in Wendel wendel imply, for example, that a collection of uniform i.i.d. random variables on the unit sphere in contains the origin with probability

In particular this yields .

3 Outline of the cubature algorithm

We describe the cubature method developed by Lyons and Victoir lyons . Throughout the paper, is a constant that may change from line to line; specific constants, however, will be indexed Let denote the smooth bounded valued functions whose derivatives of any order are bounded. Then , may be regarded as vector fields on . We define a partial differential operator and consider the following parabolic partial differential equation (PDE)

for a given Lipschitz function . The aim is to find an approximation of for a given . Consider the probability space , where is the space of valued continuous functions starting at , its usual Borel -field and the Wiener measure. Define the coordinate mapping process for , . Under Wiener measure, is a Brownian motion starting at zero. Furthermore, let . Let , , be a version of the solution of the Stratonovich stochastic differential equation (SDE)

| (5) |

that coincides with the pathwise solution on continuous paths of bounded variation. In this case, classical theory tells us that is the solution to (3).

We define the Itô functional by

| (6) |

Denote by the space of polynomials444Any finite-dimensional space of integrable and continuous functions could be used to define cubature. This extension can be helpful. in variables having degree less or equal to . Let be a positive Borel measure on . A discrete measure

with contained in satisfies a cubature formula of degree if and only if for all polynomials ,

It is well known that if all moments of up to degree exist we can always find such a measure with

(see, e.g., Bayer and Teichmann teichmann ). More generally we have the following lemma, which we state without proof.

Lemma 6.

Let be a polish space, its Borel sets and a Borel probability measure on . Let be a finite sequence of real-valued Borel measurable functions on the probability space with for . Moreover, suppose that is a Borel set with . Then there exist points and a discrete measure

such that

for .

In other words, admits a reduced measure with respect to any finite set of integrable functions. In connection with the use of the Taylor formula, a cubature measure provides an effective tool for integration over finite-dimensional spaces.

One can formulate an analogous condition to identify cubature measures on Wiener space. Here the role of polynomials is taken by iterated integrals of the form

We identify this iterated integral by the multi-index .

Define the set of all multi-indices by

and let be a multi-index. Furthermore, we define a degree on a multi-index by and let

Moreover, define by and let . It follows from the scaling property of Brownian motion that

equals, in law,

| (7) |

Definition 7.

Fix a finite set of multi-indices . We say that a discrete measure assigning positive weights to paths

is a cubature measure if for all ,

where the expectation is taken under Wiener measure. If we say that

is cubature measure of degree .

In lyons , the authors show that one can always find a cubature measure supported on, at most, continuous paths of bounded variation. More importantly, they give an explicit construction of a degree cubature formula with paths in its support.

Suppose paths and weights define a cubature measure for . It follows immediately from (7) that the measure supported on paths given by

| (8) |

and unchanged weights defines a cubature measure for general . From now on suppose that the measure is a cubature measure of degree .

The following proposition, taken from lyons , is the key step in estimating the error when one approximates the expectation of under the Wiener measure by its expectation against .

Proposition 8.

where is a constant that only depends on , and .

In general, the right-hand side of the inequality in Theorem 8 is not sufficient to directly obtain a good error bound for the approximation of the expectation, in particular if is only assumed to be Lipschitz, the estimate appears useless. So, instead of approximating

in one step, one considers a partition of the interval

with and solves the problem over each of the smaller subintervals by applying the cubature method recursively. If and are two path segments, we denote their concatenation by . For the approximation, we consider all possible concatenations of cubature paths over the subintervals, that is, all paths of the form . We define a corresponding probability measure by

The following theorem taken from Lyons and Victoir lyons is the main error estimate for the iterated cubature method, which we in the following also refer to as the Kusuoka–Lyons–Victoir (KLV) method.

Theorem 9

The total error for the approximation

is bounded by

| (9) |

where is a constant independent of and , the number of time steps in the partition of the time interval .

To compute the expectation with respect to the measure exactly requires one to solve

inhomogeneous ODEs (each corresponding to a path ) where denotes the number of paths in the support of the cubature measure and the number of subintervals in the partition. Hence, the number of ODEs to solve grows exponentially in the number of iterations.

Following Kusuoka kusuoka2 , we define for multi-indices a multiplication by

We inductively define a family of vector fields indexed by by taking

The main ingredients used when obtaining the bound (9) are Proposition 8 and the following regularity result due to Kusuoka and Stroock kusuoka1 and Kusuoka kusuoka2 , which says that even if is not smooth, is smooth in the directions of the vector fields . Let be Lipschitz and , then for all ,

| (10) |

provided the vector fields satisfy the UFG condition defined below.

Following Kusuoka kusuoka2 we introduce a condition on the vector fields.

Definition 10.

The family of vector fields , , is said to satisfy the condition (UFG) if the Lie algebra generated by it is finitely generated as a left module, that is, there exists a positive and satisfying for all ,

| (11) |

The bounds for the error of the KLV method derived in Theorem 9 (see Lyons and Victoir lyons for details) assume that the system of vector fields , , satisfies the UFG condition.

Definition 11.

We define the (formal) degree of a vector field , denoted by to be the minimal integer such that may be written as

with .

Note that for we always have . It was pointed out in Crisan and Ghazali crisan that the analysis in Lyons and Victoir lyons for the bound in (9) requires to have formal degree at most 2. If the formal degree of is greater, the bound in (12) changes and all bounds in the paper will change accordingly. For sake of simplicity we will in the following assume that has formal degree 2. The bounds can be improved in an obvious way if the degree is or . For a generalized error estimate based on Kusuoka’s ideas kusuoka3 that does not require this additional condition, see Litterer thesis .

A trivial generalization of Corollary 18 in Crisan and Ghazali crisan allows us to state a version of the Kusuoka and Stroock estimate in terms of the formal degree of a vector field. Let be as above and then for all

| (12) |

For the remainder of the paper, when we consider recombination, we are going to assume the following uniform Hörmander condition.

Definition 12.

We say that a collection of smooth vector fields , , satisfies the uniform Hörmander condition (UH) if there is an integer such that

Note that the uniform Hörmander condition implies the UFG condition. Under this stronger assumption it is straightforward to show that, in addition, is a smooth function on with explicit bounds on its derivatives. We outline an argument below that follows Kusuoka kusuoka2 and gives bounds on the regularity of , which we will use in the following section when we apply recombination to the cubature method.

Following Kusuoka kusuoka2 , let be given by

and be the continuous function

Note that

and hence, under the Hörmander condition (UH), we have for all . As in Kusuoka kusuoka2 , let and , , be given by

| (13) |

and observe that

| (14) |

The following lemma may be found in Kusuoka kusuoka2 , page 274.

Lemma 13.

The lemma shows that the functions are in . Together with (14) this immediately implies that the vector fields , , have finite formal degree no greater than . Just like identity (12), the following corollary is a trivial generalization of Corollary 18 in crisan , the result is also implicit in Kusuoka kusuoka2 , Proposition 14.

Corollary 14

Suppose the vector fields satisfy the uniform Hörmander condition. Then for any there is a constant independent of and such that

for all , .

We point out that the constant does (via the constant in the Hörmander condition) depend on the underlying family of vector fields .

4 Application to cubature on Wiener space

4.1 The reduction operation

In the iterated KLV method (Section 3), the total error over the interval of approximation is bounded by the sum of the individual errors over smaller time intervals. The KLV method is sequential. Starting with a unit mass particle at a single point in space time, the measures evolve through time by replacing each particle at time with a family of particles at time . Together these new particles have the same mass as their parent particle and are carefully positioned to provide a high order approximation to the diffusion of the underlying SDE. The algorithms introduced in Section 2 can be used very effectively to perform a global redistribution of the mass on the particles alive at time so that an essentially minimal number of particles has positive mass. At the same time we do not increase the one step errors significantly or affect the order of the approximation. In this way we obtain (see Section 4.2) a global error bound over for this algorithm that is of the same order (in the number of time steps) as the unmodified KLV method. On the other hand, the blow up in the number of particles is radically reduced.

The property of the intermediate measures we are targeting is to integrate correctly. To approximate the integral of a smooth function such as with respect to a discrete measure, we need to find uniform functional approximation schemes that apply to smooth functions on the support of this measure. By definition, smooth functions can always be well approximated on balls by polynomials. However, only after one has set a fixed error bound and a degree for the polynomials, the size of the balls on which the approximation holds becomes clear. The main idea will be to localize the intermediate particle measures into measures , where each has its support in such a good ball. We then replace (using the algorithms of Section 2) the measures by reduced measures that integrate polynomial test functions of degree at most correctly. In that way one knows that for a smooth function

is a good approximation to . We subsequently prove that we can choose the localization of the measure in a way that ensures that we increase the overall bound on the error of the approximation only by a constant factor and examine how well we can cover the support of the intermediate measures by balls for the localization.

A main idea for estimating is to consider Taylor expansions of the function . We define to be the minimal integer such that the vector fields uniformly span at each point of (as in the UH condition). For a smooth function on let denote the full derivative of . The second order derivative is then mapping

The higher order derivatives can similarly be regarded as sections of

We define the th degree Taylor approximation of centered at to be

| (16) |

and the remainder by

It is clear that the th degree Taylor approximation centered at is a polynomial of degree at most . Given and let denote the Euclidean ball of radius centered at Our estimate for the remainder of the polynomial approximation is the following.

Lemma 15.

Let . The remainder function is uniformly bounded on , that is,

where is a constant independent of , and .

By Taylor’s theorem we have for

and we note that

for some constant that only depends on and . From Corollary 14 we see that

where is the constant from Corollary 14 and the claim follows.

The bound on the remainder of the Taylor expansion of implies that cubature measures which integrate polynomials up to degree correctly provide good approximations provided the support of the measure we are targeting is contained in a sufficiently small patch.

Proposition 16.

Suppose the uniform Hörmander condition is satisfied. Let and be a positive measure on with finite mass satisfying for some , . Suppose a measure is a degree cubature measure for (a reduced measure with respect to and the polynomials of degree at most ). Then

where is the constant from Lemma 15 and independent of , and .

We have

Since is a cubature measure and integrates polynomials of degree at most correctly, the first term of the sum vanishes. Lemma 15 gives us the required bounds on the remaining terms.

Let be a discrete probability measure on and be a collection of balls of radius on that covers the support of . Then there exists a collection of positive measures , such that for all (i.e., the measures have disjoint support),

and . We call such a collection a localization of to the cover and say is the radius of the localization.

Definition 17.

We say that a measure is a reduced measure with respect to the localization and a finite set of integrable test functions if there exists a localization of such that for the measures are reduced measures (see Definition 1) with respect to and .

Note that the localization of the reduced measure is with respect to the same cover as the original measure . It is trivial to show that reduced measures exist for any localization of a discrete probability measure and any finite set of integrable test functions . Moreover, the number of particles in the support of is bounded above by . The following corollary is an immediate consequence of Proposition 16. Let in the following be a basis for the space of polynomials on with degree at most .

Corollary 18

Let , be a discrete probability measure on and a localization of radius . If is a reduced measure with respect to and , we have

where is the constant from Lemma 15 and independent of , , and the localization of radius .

We define the Kusuoka–Lyons–Victoir transition (KLV) over a specified time interval , based on the cubature on Wiener space approach and already used in the iterative method in Section 3. The transition KLV takes discrete measures on to discrete measure on and may be interpreted as a discrete Markov kernel. Given a measure on the new measure is obtained by solving differential equations along any path in the support of the cubature measure

starting from any particle in the support of . We define

We are ready to consider recombination for the iterated KLV method. Let be a step partition of the global time interval of the approximation and recall that . We also let where each . Let be a basis for the space of polynomials on with degree at most . For each time step we first apply the KLV method to move particles forward in time to a measure . We then localize the measure and use the algorithm of Section 2 to compute a reduced measure with respect to the localized measure and replace by this reduced measure. The determine the radius of the balls in the localization of the measure in the th iteration of the method. The polynomials in serve as the test function in the reduction.

More precisely, we define two interrelated families and of measures. As base case we have the measures obtained by applying twice the KLV operation starting from the point mass at .

| (17) |

For the recursion, the measure is defined to be a reduced measure with respect to any fixed localization of the measure with radius and the set of test functions (polynomials of degree at most ). We define by the relation

| (18) |

for all . Note that we do not recombine after the first and last application of the KLV operation. The reduced measures are not unique even after we fix a localization of and a reduced measure may be computed using the reduction algorithms of Section 2.

The main result of the section is the following theorem.

Theorem 19

For any choice of localizations with radius and any reduced measures with respect to and test functions , , we have

where and are constants independent of and the choice localizations with radius . The constant can be taken equal to if .

The global error is bounded by

The first two terms and the terms in the second sum are the errors introduced by the KLV operation and can be bounded as in the proof of Theorem 9.

The terms in the first sum may each be bounded by using Corollary 18.

The bounds for the error derived in this section assume that the function is Lipschitz. If has more regularity, it is clear different estimates can be applied to estimate the derivatives of giving alternate bounds for . Clearly, a smaller number of balls in the localizations of the measures reduces the computational complexity of the method. We have not discussed yet how to choose the localization and the degree in the reduction to optimize the computational complexity of the method (see Section 4.3).

4.2 Examples for the rate of convergence of the recombining KLV method

In this subsection we consider some particular choices of parameters for the recombining KLV method and examine their rate of convergence. We first fix for the remainder of this section (a family of) partitions for the time interval . We recall a family of uneven partitions from Lyons and Victoir lyons which has smaller time steps toward the end and is given by

| (20) |

For the results in lyons (see also Kusuoka kusuoka3 ) show that

| (21) |

while for the case one obtains

In the following two examples we work with the partition defined in (20) and the notation of Theorem 19. Using this particular choice of partitions ensures that the bound on the KLV error is of high order in the number of iterations .

Example 20.

Let , and , where . Then

| (22) | |||

where .

Note that for all positive integers and and that for we have . In the next example we choose the radius of the balls in the reduction operation such that at each step in the iteration the bound on the recombination error matches the bound on the KLV error.

Example 21.

Let , that is, the degree of the polynomials used in the reduction operation equals the degree of the cubature in the KLV method. Let , be given by

Then

| (23) | |||

where .

As before, if , the constants and can be taken to be . The parameters chosen in the above examples guarantee high order convergence, but are not necessarily computationally optimal. In the following section we examine how, for a fixed error , the choice of and can be varied to be closer to the optimal computational effort in the recombination operation.

4.3 An optimization

This paper establishes stable higher order particle approximation methods where the computational effort involved grows polynomially with the number of time steps when the number of steps is large and the underlying system remains compact (see Section 4.4). In concrete examples, an optimization of the different aspects of this algorithm, under the constraint of fixed total error, leads to even more effective approaches; although we expect that different problems would benefit from different distributions of the computational effort. For example, there is a trade-off between the degree of the polynomials that are used as test functions and the size of the balls used to define the localization of the measure for the recombination (smaller patches if we use higher degree polynomials in the test functions and we fix the error of the approximation).

Specifically, suppose we are given a discrete measure and the property we care about is the integral of against a smooth function . As in our application to the KLV method we consider a reduced measure (Definition 1) with respect to the polynomials of degree at most and a localization of with radius at most . The number of balls of radius required to cover the support of is at most of order , where is the diameter of . Let be the error of the approximation of by .

Note that

for some . Fixing the error gives a simple relation for and

| (24) |

Let be the number of particles in the support of . The computational complexity of the recombination operation as a function of , and is at most of order

which may be optimized subject to the constraint (24).

Note that in our application to cubature on Wiener, correspondsto and the function is given by . The calculation above also allows us to decide after each step of the iteration if it is of computational benefit to carry out a (full) recombination operation.

4.4 Simple bounds on the number of test functions; covering the support of the particle measures

In this section we obtain upper bounds for the number of ODEs required to solve in the recombining KLV method with iterations. For this, it is sufficient to bound the number of balls in the cover of the localizations of the particle measures uniformly for all iterations. We first find a large ball that covers , , and then estimate the number of balls that are required to cover . The balls in the covers of the localizations will have to be sufficiently small to preserve the high order accuracy of the method. We can show that under the assumption that the vector fields are bounded and satisfy the UH condition, we have a high order method and the computational complexity is polynomial in the number of iterations. Similar results can be obtained if the underlying system remains compact.

The following theorem demonstrates that we can achieve the same rate of convergence in the number of iterations as in Kusuoka’s algorithm and the vanilla KLV method, but control the complexity of the method by an explicit polynomial in . This compares to exponential growth in the vanilla KLV method without recombination, which despite its exponential growth leads to numerically highly effective algorithms (see, e.g., Ninomiya and Victoir ninomiya-victoir ). The estimates in this section are not designed to be optimal and can be improved. Closer to optimal choices for the radius and degree in the reduction operation have been discussed in Section 4.3 and may be used to decide if it is computationally efficient to recombine the particle measure at time .

Theorem 22

Suppose the uniform Hörmander condition is satisfied and the vector fields are uniformly bounded by some constant . We can achieve

| (25) |

while the number of test functions in the reduction operation, and hence the number of elementary ODEs to solve grows polynomially in .

Let be the degree of the cubature in the KLV method. Fix the partition to (20) for some . As in Example 20, let and , in the reduction operation. We note that the error satisfies (25) and it remains to show that the number of particles in support of the measures grows polynomially in , which is equivalent to the number of balls in the localizations growing polynomially in .

Note that if is a continuous path of bounded variation of length , we have

where is the Itô functional defined in (6), that is, is the point we obtain by solving the equation (5) along the path starting at . Let be given by length, the maximum of the lengths of the paths in the support of the degree cubature formula on Wiener space over the unit time interval. Observe that by construction any particle in the support of [compare the definition of the measures in (18)] may be written as

some , the are the rescaled paths defined in (8) and denotes to the concatenation of paths. For sufficiently large we may assume and we deduce that

In the reduction operations we consider a basis of the polynomials of degree at most and the measure is localized by balls of radius which need to cover . For , that is, for sufficiently large, we have and for our uneven family of partitions . Thus, the number of particles in each of the reduced measures is uniformly bounded above by times the number of balls of radius required to cover the ball in -dimensional space, which is a polynomial of degree at most in .

Similarly, we can derive a result analogous to Theorem 22 if the underlying system remains compact.

Appendix: A numerical toy example

We consider a linear one-dimensional problem. The boundary data is Lipschitz, piecewise smooth, and the locations of the discontinuities in the derivatives are not known to the program. The answer is required to high accuracy. In our test case we applied the approximation method to the heat equation with boundary data

which corresponds to the calculation of a Black–Scholes put option at logarithmic scale. We considered a time horizon of and various initial conditions . We set our goal to achieve an accuracy of . This example is particularly suitable as a test example because the solution to the equation is known in closed form in terms of well known special functions which can be used to determine the precise error in the approximation.

We applied a modified form of the KLV method with recombination introduced in this paper. For consider a geometrically converging partition of the unit time interval given by

and . Note that the length of the time steps in the partition is given by . In our particular example we chose to be . To achieve the required accuracy we used a point Gaussian quadrature which we had previously computed to high accuracy. For the heat equation, the particles of the cubature approximation are given by the Gaussian quadrature and we do not require to solve ODEs. As described in Section 4.1 we used polynomial test functions of degree and localized the support of intermediate particle measures in the approximation. We then used a heuristic based on the information provided by the norm of to determine, as outlined in Section 4.3, the degree of polynomial approximation that minimizes the computational complexity of the overall reduction process subject to achieving the required accuracy.

In addition, we modified the algorithm to make use of the piecewise smooth nature of the boundary data. The algorithm compares for each particle a two step KLV with a one step KLV estimate to the boundary. If both approximates agree to the error tolerance, the algorithm immediately leaps to the boundary. As the required accuracy is close to machine precision, false positives are very unlikely. Recombination is then performed on the remaining particles.

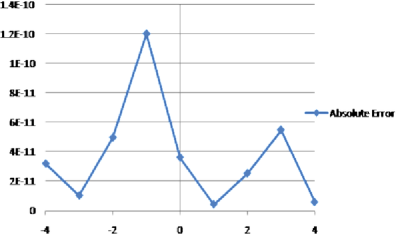

| Absolute error | 3.186E–11 | 1.01E–11 | 4.962E–11 | 1.2014E–10 |

|---|---|---|---|---|

| Evaluations at the boundary | 1,410,075 | 1,416,600 | 1,426,050 | 1,432,350 |

| Particles | 94,005 | 94,440 | 95,070 | 95,490 |

| 3.612E–11 | 4.173E–12 | 2.52E–11 | 5.47E–11 | 5.62E–12 | |

| Evaluations | 1,430,775 | 1,425,600 | 1,424,700 | 1,417,725 | 1,418,175 |

| Particles | 95,385 | 95,040 | 94,980 | 94,515 | 94,545 |

In order to achieve an accuracy of we chose and a radius for the localization that was proportional to and covered the surviving measure with approximately 13 nonempty components in the localization. The runtime of our single threaded C code555As measured on a Lenovo Thinkpad x201t notebook computer. We used intel mkl for the lapack support and this might use omp internally. was between 0.5 and 0.6 s. The parameter restricting the maximal depth of the approximation tree was set to . Table 1 and Figure 1 summarize the absolute error of the approximation, the number of reduced particles inside the domain and the total number of evaluations of the cubature at the boundary for various values of . Note that the number of particles compares to 1527 internal particles for the vanilla cubature algorithm and even if combined with a partial sampling scheme such as the tree based branching algorithm one could not hope to compute an approximation to ten digit accuracy.

Even though the problem we have considered is merely a toy example, computing the solution to high accuracy with a vanilla off the shelf PDE solver appears to be nontrivial. However, a fair comparison must involve at least adaptive methods; we were afraid to do this ourselves as it would not carry much weight because we do not have the computational expertise to get good outcomes from these packages. So we were very grateful that our colleague Kathryn Gillow in Oxford was willing to give it a quick spin on adaptive software she had developed with Endre Suli.

She says: “I’ve now tried a few approaches to solving your problem but can’t get results even close to yours in terms of accuracy achieved in such a small amount of CPU time. In all cases I’ve solved the heat equation on the spatial interval (so that with a coarse uniform mesh the point was not a node). Then to look at the error I have computed the solution at time and for integer between and as you suggest. The first approach I took was to do an adaptive finite element solution with the adaptivity geared toward getting an accurate solution at time . The mesh can change at every timestep which is obviously less than ideal as you then need to keep recomputing the matrices. The code is taking about seconds and giving accuracy of between and depending on which integer you look at. It actually turns out to be more efficient to do something a bit more naive, namely, to adapt the mesh to resolve the initial condition well and then use that mesh for the rest of the computation. As expected, this clusters the nodes around and the mesh is fairly coarse elsewhere. The advantage of this is that you just solve the same matrix problem at every time-step. This speeds things up a lot without degrading the accuracy for this problem. So here I’m getting accuracy of between and in about second. Then, finally, I gave Nick Trefethen et al’s Matlab package Chebfun a go. In order to solve the heat equation which exploits the fact that the problem is linear so you can write the solution at a given time as where is the spatial operator (including boundary conditions) and is the initial condition. It seems that Chebfun struggles when is not smooth and it actually turns out to be more efficient to compute the solution at time in two stages, namely, , . The best accuracy using this approach is taking seconds. Chebfun does a lot better when you have smooth initial data. Then it can solve the same type of problem in s giving errors of .”

No doubt the approach we take tries to do less than that taken by our colleagues, (it only computes the solution at the required points, etc.) and we have tried to polish the code for our problem but still we find it encouraging evidence that this paper is putting ideas together in a novel way. The linear algebra we do is numerically really heavy, but it seems to pay.

References

- (1) {barticle}[mr] \bauthor\bsnmBayer, \bfnmChristian\binitsC. and \bauthor\bsnmTeichmann, \bfnmJosef\binitsJ. (\byear2006). \btitleThe proof of Tchakaloff’s theorem. \bjournalProc. Amer. Math. Soc. \bvolume134 \bpages3035–3040 (electronic). \biddoi=10.1090/S0002-9939-06-08249-9, issn=0002-9939, mr=2231629 \bptokimsref \endbibitem

- (2) {bincollection}[mr] \bauthor\bsnmCrisan, \bfnmDan\binitsD. (\byear2002). \btitleNumerical methods for solving the stochastic filtering problem. In \bbooktitleNumerical Methods and Stochastics (Toronto, ON, 1999) (\beditorT. J. Lyons, \beditorT. S. Salisbury, eds.). \bseriesFields Institute Communications \bvolume34 \bpages1–20. \bpublisherAmer. Math. Soc., \baddressProvidence, RI. \bidmr=1944741 \bptokimsref \endbibitem

- (3) {barticle}[mr] \bauthor\bsnmCrisan, \bfnmDan\binitsD. and \bauthor\bsnmDoucet, \bfnmArnaud\binitsA. (\byear2002). \btitleA survey of convergence results on particle filtering methods for practitioners. \bjournalIEEE Trans. Signal Process. \bvolume50 \bpages736–746. \biddoi=10.1109/78.984773, issn=1053-587X, mr=1895071 \bptokimsref \endbibitem

- (4) {bincollection}[mr] \bauthor\bsnmCrisan, \bfnmDan\binitsD. and \bauthor\bsnmGhazali, \bfnmSaadia\binitsS. (\byear2007). \btitleOn the convergence rates of a general class of weak approximations of SDEs. In \bbooktitleStochastic Differential Equations: Theory and Applications. \bseriesInterdisciplinary Mathematical Sciences \bvolume2 \bpages221–248. \bpublisherWorld Scientific, \baddressHackensack, NJ. \bidmr=2393578 \bptokimsref \endbibitem

- (5) {barticle}[mr] \bauthor\bsnmDavis, \bfnmPhilip J.\binitsP. J. (\byear1967). \btitleA construction of nonnegative approximate quadratures. \bjournalMath. Comp. \bvolume21 \bpages578–582. \bidissn=0025-5718, mr=0222534 \bptokimsref \endbibitem

- (6) {bincollection}[mr] \bauthor\bsnmKusuoka, \bfnmShigeo\binitsS. (\byear2001). \btitleApproximation of expectation of diffusion process and mathematical finance. In \bbooktitleTaniguchi Conference on Mathematics Nara ’98. \bseriesAdvanced Studies in Pure Mathematics \bvolume31 \bpages147–165. \bpublisherMath. Soc. Japan, \baddressTokyo. \bidmr=1865091 \bptnotecheck year\bptokimsref \endbibitem

- (7) {barticle}[mr] \bauthor\bsnmKusuoka, \bfnmShigeo\binitsS. (\byear2003). \btitleMalliavin calculus revisited. \bjournalJ. Math. Sci. Univ. Tokyo \bvolume10 \bpages261–277. \bidissn=1340-5705, mr=1987133 \bptokimsref \endbibitem

- (8) {barticle}[mr] \bauthor\bsnmKusuoka, \bfnmS.\binitsS. and \bauthor\bsnmStroock, \bfnmD.\binitsD. (\byear1987). \btitleApplications of the Malliavin calculus. III. \bjournalJ. Fac. Sci. Univ. Tokyo Sect. IA Math. \bvolume34 \bpages391–442. \bidissn=0040-8980, mr=0914028 \bptnotecheck year\bptokimsref \endbibitem

- (9) {bmisc}[auto:STB—2011/12/07—13:41:22] \bauthor\bsnmLitterer, \bfnmC.\binitsC. (\byear2008). \bhowpublishedThe signature in numerical algorithms. Ph.D. thesis, Univ. Oxford. \bptokimsref \endbibitem

- (10) {bmisc}[auto:STB—2011/12/07—13:41:22] \bauthor\bsnmLitterer, \bfnmC.\binitsC. and \bauthor\bsnmLyons, \bfnmT.\binitsT. (\byear2011). \bhowpublishedCubature on Wiener space continued. In Stochastic Processes and Application to Mathematical Finance, Proceedings of the 6th Ritsumeikan International Symposium. Oxford Univ. Press, Oxford. \bptokimsref \endbibitem

- (11) {bmisc}[auto:STB—2011/12/07—13:41:22] \bauthor\bsnmLitterer, \bfnmC.\binitsC. and \bauthor\bsnmLyons, \bfnmT.\binitsT. (\byear2011). \bhowpublishedIntroducing cubature to filtering. In Oxford Handbook of Non-Linear Filtering (D. Crisan and B. Rozovsky, eds.) 786–798. Oxford Univ. Press, Oxford. \bptokimsref \endbibitem

- (12) {barticle}[mr] \bauthor\bsnmLyons, \bfnmTerry\binitsT. and \bauthor\bsnmVictoir, \bfnmNicolas\binitsN. (\byear2004). \btitleCubature on Wiener space. \bjournalProc. R. Soc. Lond. Ser. A Math. Phys. Eng. Sci. \bvolume460 \bpages169–198. \biddoi=10.1098/rspa.2003.1239, issn=1364-5021, mr=2052260 \bptokimsref \endbibitem

- (13) {barticle}[mr] \bauthor\bsnmNinomiya, \bfnmSyoiti\binitsS. (\byear2003). \btitleA partial sampling method applied to the Kusuoka approximation. \bjournalMonte Carlo Methods Appl. \bvolume9 \bpages27–38. \biddoi=10.1163/156939603322587443, issn=0929-9629, mr=1987415 \bptokimsref \endbibitem

- (14) {barticle}[mr] \bauthor\bsnmNinomiya, \bfnmSyoiti\binitsS. and \bauthor\bsnmVictoir, \bfnmNicolas\binitsN. (\byear2008). \btitleWeak approximation of stochastic differential equations and application to derivative pricing. \bjournalAppl. Math. Finance \bvolume15 \bpages107–121. \biddoi=10.1080/13504860701413958, issn=1350-486X, mr=2409419 \bptokimsref \endbibitem

- (15) {bmisc}[auto:STB—2011/12/07—13:41:22] \bauthor\bsnmVictoir, \bfnmN.\binitsN. \bhowpublishedPrivate communication. \bptokimsref \endbibitem

- (16) {barticle}[mr] \bauthor\bsnmWendel, \bfnmJ. G.\binitsJ. G. (\byear1962). \btitleA problem in geometric probability. \bjournalMath. Scand. \bvolume11 \bpages109–111. \bidissn=0025-5521, mr=0146858 \bptokimsref \endbibitem