Multiple Timescale Dispatch and Scheduling for Stochastic Reliability in Smart Grids with Wind Generation Integration

Abstract

Integrating volatile renewable energy resources into the bulk power grid is challenging, due to the reliability requirement that at each instant the load and generation in the system remain balanced. In this study, we tackle this challenge for smart grid with integrated wind generation, by leveraging multi-timescale dispatch and scheduling. Specifically, we consider smart grids with two classes of energy users - traditional energy users and opportunistic energy users (e.g., smart meters or smart appliances), and investigate pricing and dispatch at two timescales, via day-ahead scheduling and real-time scheduling. In day-ahead scheduling, with the statistical information on wind generation and energy demands, we characterize the optimal procurement of the energy supply and the day-ahead retail price for the traditional energy users; in real-time scheduling, with the realization of wind generation and the load of traditional energy users, we optimize real-time prices to manage the opportunistic energy users so as to achieve system-wide reliability. More specifically, when the opportunistic users are non-persistent, i.e., a subset of them leave the power market when the real-time price is not acceptable, we obtain closed-form solutions to the two-level scheduling problem. For the persistent case, we treat the scheduling problem as a multi-timescale Markov decision process. We show that it can be recast, explicitly, as a classic Markov decision process with continuous state and action spaces, the solution to which can be found via standard techniques.

We conclude that the proposed multi-scale dispatch and scheduling with real-time pricing can effectively address the volatility and uncertainty of wind generation and energy demand, and has the potential to improve the penetration of renewable energy into smart grids.

I Introduction

I-A Motivation

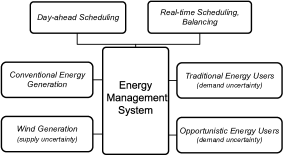

To address the grand challenge of a sustainable energy industry, there has recently been a surge of interest in alternative energy resources, including wind, solar, bio-fuel, and geothermal energy. Ultimately, all these energy solutions hinge heavily on smart grid technologies that are capable of coordinating and managing dynamically interacting power grid participants. There is therefore an urgent need to develop a new generation of cyber-enabled energy management system (EMS) and supervisory control and data acquisition (SCADA), which can carry out reliable and possibly distributed management of these energy sources.

For normal operations of power systems, the precise balance between energy supply and demand is of the most significance to system reliability. Integrating a large amount of intermittent renewable energy resources (e.g., wind generation) into the bulk power grid has put forth great challenges for generation planning and system reliability. In particular, a complication that arises is that some primary elements of renewable energy sources, such as wind and solar power, are highly variable (stochastic) and often uncontrollable, making it difficult to guarantee that the load and generation in the system remain balanced at each instant. A mismatch between supply and demand could cause a deviation of zonal frequency from nominal value [1], and when it gets severe power outages and blackouts may occur. Further, wind generation is non-dispatchable, in the sense that the output of wind turbines must be taken by all rather than by request. Moreover, the volatility and intermittence makes it difficult for system operators to obtain accurate knowledge of future wind generations. Traditionally, system operators maintain additional generation capacity and reserves (on-line or fast-start), at additional costs, to address the supply uncertainty.

While the volatility of wind generation induces uncertainties in the supply side of the power grid, an emerging class of energy users, namely opportunistic energy users, induce uncertainties on the demand side as well. It is noted in [2] that over daily energy consumption in United States is from the usage of appliances such as water heater, cloth dryers, and dish washers, which are envisaged to become smart and be branded as opportunistic energy users, with the following behaviors distinct from traditional energy users: 1) they access the energy system in an opportunistic manner, according to the availability of system resources; 2) different from the ‘always-on’ demand of traditional energy users, the load profiles of opportunistic energy users can be bursty and can be either inelastic or elastic; 3) opportunistic energy users respond to the power market on a much finer timescale.

The prevalence of the new class of opportunistic energy users, if utilized intelligently, makes demand side management (DSM) a promising solution to reduce the costs incurred by the deep penetration of wind generation [3]. Traditionally, some energy users (e.g., residential and small commercial users) pay a fixed price per unit of electricity that is established to represent an average cost of power generation over a given time-frame (e.g., a month), independent of the generation cost. In contrast, under price-based DSM programs [4], the retail prices are tied with the generation cost and may vary according to the availability of energy supplies. Often times, the energy market consists of a day-ahead market and a real-time market for electricity. Simply put, the day-ahead market produces financially binding schedules for the energy generation and consumption one day before the operating day. Further, the real-time market is used to tune the balance between the energy amount scheduled day-ahead and the real-time load. However, it is known that existing dynamic pricing mechanisms (term of use, critical peak pricing, etc) do not work well for handling generation uncertainty and managing the demand uncertainty in a real-time manner (i.e., within minutes).

In this study, we will explore multi-timescale dispatch and scheduling to address the following challenges: 1) the supply uncertainty as a result of the volatility and non-stationarity of wind generation; 2) the demand uncertainty due to a large number of opportunistic energy users and their stochastic behaviors; 3) the coupling between sequential decisions across multiple timescales.

I-B Summary of Main Contributions

Aiming to tackle the challenge of integrating volatile wind generation into the bulk power grid, we study dispatch and scheduling, for a smart grid model with two classes of energy users, namely traditional energy users and opportunistic energy users (e.g., smart meters or smart appliances). We consider a power grid with both conventional energy sources (e.g., thermal) and wind generation. Notably, wind generation is among the renewable resources that has most variability and uncertainty, and exhibits multi-level dynamics across time. To enhance the penetration of wind energy, we study multi-timescale dispatch and scheduling based on a marriage of real-time pricing and multi-settlement power market economics.

Specifically, the system controller performs scheduling at two timescales. In the day-ahead schedule, with the statistical information on wind generation and energy demands, the operator optimally procures conventional energy supply and decides the optimal retail price for the traditional energy users, for the next day. In the real-time schedule, upon the realization of the wind energy generation and the demand from traditional energy users (which is stochastically dependent on the day-ahead retail price), the controller decides the real-time retail price for the opportunistic energy users.

In particular, we explore multi-scale scheduling for two types of opportunistic energy users: the non-persistent and the persistent users. The non-persistent users leave the power market when they find that the current real-time price is unacceptable, whereas the persistent opportunistic users wait for the next acceptable real-time price. We obtain closed-form solutions for the scheduling problem when the users are non-persistent. For the persistent case, the scheduling problem is a multi-timescale Markov decision process (MMDP) that we recast, explicitly, as a standard Markov decision process that can be solved via standard solution techniques. We demonstrate, via numerical experiments, that the proposed two-timescale dispatch and scheduling enables the penetration of wind generation and hence improves the overall efficiency, by enabling two-way energy exchange between providers and customers, and by facilitating both information interaction as well as energy interaction.

I-C Related Work

Roughly speaking, related work falls into two major categories: the scheduling of power systems with wind generation integration; and the pricing and management of opportunistic users.

Very recent work [5] proposed risk-limiting dispatch in contrast to worst-case dispatch for traditional generation planning, by treating scheduling with known demand and uncertain supply as a multi-stage decision problem with recourse. With the same spirit, [6] proposed stochastic security criterion in scheduling with wind generation. Specifically, a scenario-based approach (a scenario is defined as the trajectory of potential realization of future supply) is used to minimize the expected aggregated social cost incurred by all the scenarios in the scheduling horizon. Model predictive dispatch of wind generation was studied in [7], which treats future wind generation in the scheduling horizon as a dynamic process specified by an ARMA model, aiming to minimize the total generation cost subject to the physical constraints of conventional generators. In a nutshell, all the works noted above focus on managing the energy supply and treat the energy demand as known (or statistically known) but uncontrollable.

Real-time pricing in related works [4, 3] takes place on the timescale of hours in conventional power systems, and the price response of energy users are understood with some high-level models. For a cyber-enabled energy system with a large number of opportunistic energy users, clearly it is more desirable to accomplish the price response and manage the energy demand in a much finer timescale (e.g. minutes). Indeed, this is one salient feature envisioned for future smart grids, although this poses significant challenges for planning, modeling, and controlling energy generation, transmission and distribution.

The remainder of the paper is organized as follows. In Section II, we describe the energy system model and give a brief overview of the two-timescale settlement power market. We study two-timescale dispatch and scheduling when the opportunistic users are non-persistent in Section III. In Section IV, we consider persistent opportunistic users and formulate the scheduling problem as a multi-timescale Markov decision process. We provide concluding remarks and identify directions for future research in Section V.

II System Model and Problem Formulation

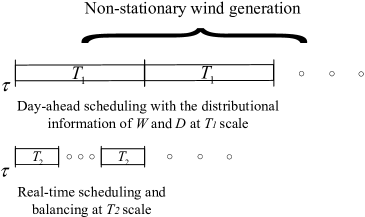

We divide a 24-hour period into slots of length each, where ; and each -slot, in turn, consists of slots, each of length , with . For example, the -slots can correspond to hours in a day and the -slots can correspond to minutes. We begin with an introduction to the supply side of the power system.

II-A Energy Sources and Generation Costs

We consider a power grid with two kinds of energy sources: the conventional energy (e.g., thermal) and the wind energy. The conventional energy is, in turn, drawn from two sources: base-load generation and peaking generation, with generation cost and per unit, respectively111The wind energy is assumed to be cost-free, based on [8].. Peaking generation is typically from fast-start generators (e.g., gas turbines), with a higher generation cost (). Due to the start-up time and ramp rate of generators, the base-load generators are scheduled day-ahead (24-hours ahead of the corresponding time) for each slot of the next day, and the generation cost contains start-up cost and other operating costs. In real-time scheduling of each slot, peaking generation and wind generation are used, as needed, to clear the balance between demand and the base-load generation.

Let denote the aggregate energy demand (from both traditional and opportunistic users) and be the wind generation amount, in a -slot. Let denote the net demand for conventional energy in a slot. Suppose that the system operator schedules a base-load generation amount of for a -slot and thus schedules for each -slot within the -slot, for the next day. In real-time scheduling, the system operator need to balance demand and supply: 1) If , then system operator dispatches a base-load generation of and a peaking generation of ; 2) Otherwise, the over-scheduled generation incurs a start-up cost of per unit.

II-B Day-Ahead Pricing and Real-Time Pricing

As is standard, dynamic pricing contracts between the system operator and end-users are used to manage the demand of both traditional energy users and opportunistic energy users, on both and timescales. We consider the following two-timescale pricing model:

-

•

Traditional energy users and opportunistic energy users have separate pricing contracts: day-ahead pricing for traditional users and real-time pricing for opportunistic users, respectively;

-

•

Day-ahead retail price: Traditional energy users are informed, one day ahead, of the day-ahead prices corresponding to each -slot;

-

•

Real-time retail price: opportunistic energy users receive the real-time retail prices at the beginning of each -slot;

-

•

Both retail prices have price cap and , respectively.

Note that besides the day-ahead pricing model for the traditional users, which was proposed in [4], we take a forward-looking perspective to identify a new class of users, namely the opportunistic energy users, and devise a real-time pricing model for these users that is cognizant of the uncertainties in the demand and supply. We discuss these uncertainties next.

II-C Supply Uncertainty of Wind Generation

Wind generation is determined by the geographical and meteorological conditions, and may assume high fluctuations or relative steady patterns at different time-scales. Therefore, wind generation are generally considered to be non-stationary and volatile. Based on recent works [9], [10], the wind generation can be modeled as a non-stationary Gaussian random process across -slots, i.e., the wind generation amount in th -slot of th -slot is given by

| (1) |

where is the mean and is the variance. The statistical information is available, one day ahead, to the day-ahead scheduler. Indeed, this information is commonly provided by the forecasting functions of EMS or commercial entities.

II-D Demand Uncertainty under Real-time Pricing

In a -slot, the aggregated demand from energy users, i.e., ,

consists of two components:

from the traditional energy users, and from the opportunistic energy users.

Demand model for traditional energy users: The demands of

traditional energy users could be known with reasonable accuracy,

and the short-term price response of demand is well understood

[11, 12]. Based on [13], we model the

energy demand of traditional energy users in a -slot as a

random variable with mean depending on the day-ahead price :

| (2) |

with

| (3) |

where accounts for the uncertainty of and is the price elasticity of the traditional energy users at the corresponding -slot. Price elasticity is traditionally used to characterize the price response of energy users and is formally defined as the ratio of marginal percentage change in demand to that of price, i.e.,

| (4) |

Note that, for power systems, the price elasticity is negative, and

is the normalizing constant. Worth noting is that

and could be different for each of the

-slots, since traditional energy users’ demand and persistence

for consumption may depend on the term of the day (noon or evening,

peaking or off-peaking hours).

Demand model for opportunistic energy users: Under real-time

pricing, we assume that opportunistic energy users have the

following behaviors:

-

•

Opportunistic energy users arrive according to a Poisson process with rate , which is constant within a -slot but can vary across the -slots;

-

•

Opportunistic energy users choose the access time randomly and independently;

-

•

In each -slot, an opportunistic user arriving in the system decides to accept or reject the announced real-time price by comparing with a price acceptance level . This price acceptance level is randomly chosen and is i.i.d across the opportunistic users. Thus with denoting the total number of opportunistic energy users in a -slot, the number of active opportunistic users, , is given by

(5) -

•

Each active opportunistic energy user has a per-unit energy consumption of . Thus the total energy demand from opportunistic energy users is given by ;

-

•

Under real-time pricing, the response of opportunistic energy users may vary according to the applications. Recent study [11] suggests that households respond to high energy prices through energy conservation with no load shifting, while [12] finds that most of the commercial customers respond by load shifting to a later time. With these insights, we consider two kinds of opportunistic energy users: non-persistent and persistent, of which the former leaves the system if the real-time price is unacceptable, while the latter waits in the system for a new real-time price in the next -slot.

II-E General Problem Formulation

As illustrated in Fig. 2, we consider day-ahead scheduling and real-time scheduling with non-stationary wind generation over a horizon of -slots, with the main objective being to maximize the overall expected profit. We elaborate further on multi-timescale dispatch and scheduling below.

In day-ahead scheduling, with the distributional information of next-day wind generation, the system operator aims to find a policy that dictates the two-timescale decisions , , and . A general formulation of the two-timescale scheduling problem is provided below:

| (6) |

where, is the total profit in a -slot under policy , given by

| (7) |

where is the net profit in the th -slot of the th -slot (henceforth called the th slot) and is the system state in the th slot, which is observable in real time. When the opportunistic users are non-persistent, consists of the wind energy and the energy demand from traditional users. When the opportunistic users are persistent, consists of wind generation and traditional users’ energy demand, as well as the energy requests of opportunistic users carried over from the previous -slot.

III Dispatch and Scheduling with Non-persistent Opportunistic Energy Users

Note that the energy procurement and retail price in day-ahead schedule have significant impact on the real-time retail price. The real-time pricing policy, in turn, affects the optimization of the day-ahead schedule. This tight coupling, underscores the need for joint optimization of the day-ahead and real-time schedules. To this end, we take a “bottom-up” approach in formulating the two-level scheduling problem. Specifically, we first formulate the real-time scheduling problem, conditioned on the day-ahead scheduling decisions and ; and then introduce the day-ahead scheduling problem while taking into account the real-time scheduling policy.

III-A Real-time Scheduling on Timescale

Given the amount of conventional energy procurement and the day-ahead price settled in day-ahead scheduling, together with the realizations of wind generation and traditional energy demand , the real-time scheduling problem in a -slot is formulated as:

| (8) |

where is the system state and

| (9) | |||||

where, recall that denotes the energy demand of opportunistic energy users. The quantity denotes the surplus energy, given by

| (10) |

The indicator function corresponds to the event when the wind energy is sufficient to meet the demands of both types of users. Indicator refers to the event when the wind energy is not sufficient but the total of the scheduled traditional energy and the wind energy is higher than the aggregate demand , which necessitates the cancelation of part of the scheduled generation from the base-line generators incurring a penalty per unit for the canceled amount of generation. Indicator corresponds to the event that the total of scheduled baseline generation and the wind generation is insufficient to meet the aggregate energy demand and the controller must purchase the deficit energy from fast start-up generators at a cost . Formally, the events are described below:

| (11) |

| (12) |

| (13) |

III-B Day-ahead Scheduling on Timescale

The day-ahead scheduling problem in the non-persistence case is formally given by

| (14) |

where the inner maximization corresponds to the real-time scheduling studied above. Since and are independent and identically distributed across the -slots, the day-ahead scheduling problem in the non-persistent case can be optimized by simply considering the snapshot problem in a specific -slot, given by222We drop the suffix for notational simplicity.:

| (15) |

III-C Approximate Solutions

The tight coupling between the day-ahead and real-time scheduling problems, along with the convolved nature of the uncertainties involved, makes a direct joint optimization challenging. We therefore take an alternate approach and obtain approximate solutions to the real-time schedule. Based on the approximate real-time schedule, we propose solutions to the day-ahead schedule. In light of the characteristics of practical systems, we impose the following general conditions first.

-

•

Condition : Wind generation is not sufficient to meet the total energy demand in the system.

Needless to say, under condition , in (9). Define as the energy procurement for the demand of opportunistic energy users, then (9) reduces to

| (16) |

where .

We begin with an analysis of the real-time scheduling problem. Recall that the number of non-persistent opportunistic energy users arriving in the -slot has a Poisson distribution, with mean . It follows that the number of users that become active, denoted as , is also a Poisson random variable with mean .

Note that the price elasticity of the opportunistic energy users, is given by

| (17) |

The opportunistic energy users are said to be relatively inelastic if , i.e., the percentage change in demand is greater than that of price; otherwise, they are relatively elastic. Further, let be the highest price that is acceptable to all opportunistic energy users.

Then, the solution to (17) is given by:

| (18) |

It is known [2] that, is typically large in practical power systems, and hence, could be approximated by a Gaussian random variable. Accordingly, the demand of opportunistic energy users follows a Gaussian distribution , with

| (20) |

where . Denote the real-time pricing policy that solves the preceding equation by the mapping , where, recall that is the system state .

Using the statistical properties of the wind generation and the opportunistic user demand, reported in literature, we now further simplify . According to [14], the standard deviation of wind generation, is of the same order as the mean of wind generation. Typically, wind generation and the demand of opportunistic energy users are comparable. Observe from (20) that the variance of the demand of opportunistic energy users is of the same order as its mean. We conclude that has the same order as the square root of the average demand of opportunistic users. Thus, with , it follows that .

Recall that the opportunistic energy users are said to be relatively inelastic if , i.e., the percentage change in demand is greater than that of price; otherwise, they are relatively elastic. Since the price elasticity can have significant impact on and , we proceed to study real-time schedule for different cases of elasticity, with .

Proposition 1.

Suppose condition holds. When the non-persistent opportunistic energy users are relatively inelastic, i.e., , the real-time pricing policy is given by .

Proof.

In practical power systems, according to [13, 14], and usually have continuous, symmetrical and unimodal probability distributions. Since , intuitively, there exists a finite constant , such that:

| (22) |

and333It is well-known that (23) is valid for .

| (23) |

If , (21) boils down to:

| (24) |

When , (21) simplifies to

| (25) |

It is clear that (24) and (25) are unimodal for , both with peaks at . This yields the real-time pricing policy: . ∎

Remarks: Note that the result in the preceding proposition is intuitive, since, with the opportunistic users’ energy demand being relatively insensitive (inelastic) to the announced real-time price, the scheduler can maximize profit by simply announcing the highest possible price, .

Proposition 2.

Suppose condition holds. When the non-persistent opportunistic energy users are relatively elastic, i.e., , the real-time pricing policy is given by

Proof.

When , can be expected to be much smaller than that in the inelastic case under the same real-time prices. With this observation, we resort to the certainty equivalence techniques [15]. By approximating with its mean , the profit in real-time scheduling is given by:

| (26) |

which achieves the optimum at:

| (27) |

which yields the real-time pricing policy in the elastic case. ∎

Remarks: Note that the first case, i.e., , points to a case with energy surplus, i.e., there is more energy supply than the total demand from traditional and opportunistic users, whereas the second case is tied to a case with energy deficit. Then, it is natural that the real-time price in the first case depends on the penalty in canceling a scheduled generation; and that the real-time price in the second case is a function of the cost of fast start-up generation. Note also that, in both cases, when the opportunistic users become increasingly elastic, i.e., , the real-time price progressively decreases to the minimum allowable prices, i.e., and , respectively. This monotonic behavior of the real-time price with respect to increasing elasticity comes at no surprise, since, as , the average opportunistic user demand , i.e., the opportunistic energy users become more and more thrifty. Therefore, the scheduler must offer power at increasingly cheaper prices, up to the lowest possible price, to maximize profit.

Having established an approximate real-time scheduling policy for both kind of opportunistic energy users, an approximate day-ahead schedule can be obtained by solving the following single-stage optimization:

| (28) |

where is given by (9) and the expectations depend on the exact stochastic models assumed for wind generation and traditional users’ energy demand.

Proposition 3.

The optimal decision of is given by

| (31) | |||||

Proof.

We first show that depend on and only through . For convenience, define:

Since , it is clear from Proposition 1 and Proposition 2 that the real-time pricing policy depends on the day-ahead decision only through . We denote this policy as . With this insight, by using the change of variable technique in (16), the objective function of can be rewritten as

| (32) |

where

| (33) |

| (34) |

Let denote the solution space for the objective function of defined in (32). Thus

| (35) |

It can be verified that defined in the proposition statement maximizes . Define , and let maximize . If we show that belongs to the solution space , then optimizes the day-ahead scheduling problem in (32). Since , it is now sufficient to show that . A sufficient condition to establish this is given by

| (36) |

Under condition , wind energy is not sufficient to meet the total energy demand when day-ahead price is , thus:

| (37) |

Therefore,

| (38) |

It follows that 1) , i.e., there is no scheduled energy surplus, thus in (32); 2) Using the preceding statement, recalling the definition of , we see that . Thus, from Proposition 2, the optimal real-time price turns out to be a constant , i.e., independent of the system state and the day-ahead decisions, when the opportunistic users are relatively elastic. Also, for the relatively inelastic case, we know from Proposition 1 that the optimal real-time price is a constant . Letting denote this constant real-time price for both the elastic and inelastic cases, respectively, we have

| (39) |

Therefore, , and indeed lies in the feasible region and hence optimizes the day-ahead scheduling problem in (32). The optimal day-ahead decision, , can now be computed using and . ∎

Corollary 4.

When the non-persistent opportunistic energy users are relatively inelastic, the complete two-timescale scheduling decision is given by:

where denotes the inverse of the CDF of .

IV Dispatch and Scheduling with Persistent Opportunistic Energy Users

We now study multi-timescale dispatch and scheduling when the opportunistic users are persistent. Simply put, a persistent opportunistic user waits in the system for a new real-time price, in the next -slot, if the current real-time price is not acceptable. We assume that the opportunistic users are persistent across both and slots, and that the opportunistic energy users that arrived in the day leave the system at the end of the day.

Due to the persistent nature of the opportunistic users, scheduling decisions in both and -slots affect the system trajectory and hence scheduling decisions in future time-slots, across both timescales. Thus, the scheduling problem involves hierarchically structured control [16], with the hierarchy defined across timescales. With this insight, we treat the scheduling problem as a multi-timescale Markov decision process (MMDP) [17] where decisions made in the higher level affects both the state transition dynamics and the decision process at the lower level, while decisions at the lower level affect only the decisions made at the upper level. The multi-timescale dispatch and scheduling problem at hand is particularly unique in the following sense: the two timescales do not overlap, since the upper level decisions (day-ahead) are made in non real-time. Thus the upper level scheduler does not have any direct observation of the effect it has on the lower level system dynamics, until the horizon, and make decisions solely based on stochastic understanding of the behavior of the lower level process. These properties make the two-timescale scheduling problem, with persistent users, uniquely challenging. We now describe the problem in detail.

| (43) | |||||

| (46) |

For day-ahead scheduling, the scheduler decides the energy dispatch and the retail price for the th -slot in the next day. Recall that the day-ahead scheduler has an accurate forecast of the expected amount of wind generation . We define the system state, , corresponding to the th -slot in the next day as , where denotes the number of persistent opportunistic users carried over from the th -slot. During real-time scheduling, the scheduler, in each -slot, has knowledge of the wind generation and the demand from traditional energy users, along with the number of persistent opportunistic users carried over from previous -slot. Based on this information, it must decide a real-time price for the th -slot in the th -slot, i.e., the th -slot). We define the observable (observable in real time) state of the system in th -slot as , where denotes the wind generation in the th -slot in the th -slot , is the energy demand from traditional energy users in the th -slot, denotes the number of persistent opportunistic energy users carried over from the previous -slot to the th slot. Having explicitly defined the states of the system for the day-ahead scheduling and real-time scheduling, we introduce the optimality equations next. With , we have

| (47) | |||||

As noted earlier, this is a MMDP over a finite horizon, with being the upper level (slower timescale) decisions and being the lower level decisions.

To mitigate the complexity of the MMDP problem, next we exploit the structural properties of the multi-scale dispatch and scheduling problem and recast it as a classic Markov decision process (MDP) (e.g., [18]).

Proposition 5.

With appropriately defined immediate reward and action space , the two-level scheduling problem can be written as a classic MDP at the slower time-scale, as below:

We now proceed to discuss the transformation of the two-level scheduling problem from a MMDP to a classic MDP. In the two-level scheduling problem, recall that the lower level decisions are essentially the mapping from the realizations of wind energy, traditional users’ energy demand and persistent opportunistic users to the real-time price, i.e., . Consider a stationary real-time pricing rule within each slot, i.e. , and denote this stationary mapping by . A key step is to view as an action at the day-ahead scheduling level, in addition to actions . With this insight, we can simplify the MMDP into a classic MDP. We elaborate further on this below.

The expected net reward from slot until slot in the day-ahead market is thus given by the Bellman equation:

| (48) | |||||

where, recall, refers to the expectation over conditioned on . The expectations used in the MDP formulation are explicitly provided in (IV). The terminal reward, , is given by

| (49) |

Note that the immediate reward corresponding to th -slot is a function of the realized values of wind generation mean (that is accurately forcast 24 hours ahead) and the number of persistent opportunistic users carried over from previous -slot. We now proceed to explicitly characterize the immediate reward , for :

| (50) | |||||

where, by definition, and for ,

| (51) | |||||

where is given by

| (52) | |||||

Note that the quantities and can be regarded as the immediate reward and the net reward at the lower level MDP, if the problem is viewed as an MMDP. The quantity is a function of the realizations of the wind generation, the demand from traditional energy users and the number of persistent opportunistic energy users carried over from previous -slot. More specifically, we have that

| (53) | |||||

where denotes the number of opportunistic users arriving at the th slot, and denotes the number of opportuinstic users that become active in slot . denotes the energy consumption by the opportunistic users in slot . Recall that denotes the energy demand per active opportunistic energy user. Thus, we have

| (54) |

The quantity denotes the surplus energy, given by

| (55) |

Recall, the real-time price is given by the mapping as

| (56) |

The indicator functions , and correspond to the various deficit/surplus energy states, and were explicitly defined in Section III.

Summarizing, we have shown that the two-timescale dispatch and scheduling problem with persistent users can be recast as an MDP with continuous state and action spaces. Using appropriate discretization techniques, we can reformulate it as a classic discrete state and action space MDP, which can be solved optimally or near-optimally using various solution techniques available in the literature [19].

V Numerical Results

For concreteness, we now study, via numerical experiments, the performance of the proposed multi-timescale dispatch and scheduling policy. First, we define profit margin as the ratio of the average net profit to the sales in a -slot. We assume the opportunistic users are non-persistent.

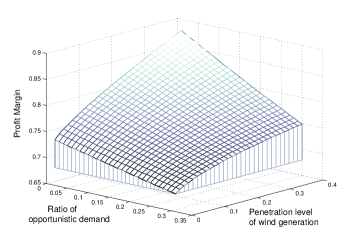

In Fig. 3, the profit margin is plotted against various values of the penetration of opportunistic users and penetration of wind energy in the system with two-timescale scheduling. We use price elasticity of for traditional users and for opportunistic users. As expected, the penetration of wind energy increases the profit margin since wind energy is harvested ‘cost-free’. In contrast, as the demand of penetration of opportunistic energy users increases, the profit margin decreases. To explain this, we first identify the two principal events that lead to losses in the system operator’s profit: (a) The penalty () when a fraction of the dispatched conventional generation is reverted; (b) the loss of revenue when the dispatched energy is insufficient to meet the total energy needs and the operator purchases energy from fast-start up generators at higher cost . The uncertainty in opportunistic energy users’ demand is one of the factors that could lead to either of these events. An over-estimation of this demand in the day-ahead schedule leads to event (a), while an underestimation of this demand leads to event (b). In our experiments, since the demand from traditional users is deterministic, the higher the demand from opportunistic users, the higher the uncertainties on the demand side and hence the higher the losses at the system operator. This insight further underscores the need for efficient pricing mechanisms that intelligently tackles the ever-increasing uncertainties in the power system.

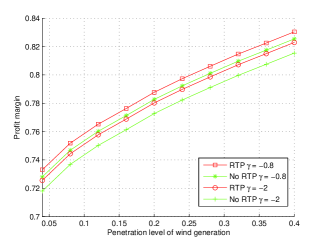

Fig. 4 compares the profit margins with and without multi-timescale pricing for various values of wind energy penetration levels, i.e., the ratio of the wind energy generation to the total energy. In the benchmark system, without multi-timescale price, all the users exhibit traditional response to prices with the same price elasticity . The prices are optimized by taking into consideration the statistics of the traditional users’ demand and wind generation. Considering the multi-timescale scheduling system, for fair comparison, we assume that the opportunistic users have the same elasticity as the traditional users in the system. We compare the two systems for different values of . As expected, for a fixed wind penetration level, for the same value of , the profit margin is higher when real-time pricing is employed to mitigate the uncertainties in demand and supply. Also, note that, as the price elasticity increases, the opportunistic users exhibit increasingly thrifty behavior essentially reducing the profit margin for the operator. In addition, as expected, the profit margin increases with wind penetration with or without real-time pricing since wind energy is assumed to be cost-free.

To summarize, numerical results suggest that two-time scale scheduling effectively addresses the volatility of energy generation and the uncertainties in the demand from opportunistic users. Additional insights include the following: the profit margin of system operators increases with the penetration level of wind and decreases with demand from opportunistic users and that the elasticity of the opportunistic users plays a major role in the power system design.

VI Conclusion

Wind generation is among the renewable resources that has most variability and uncertainty, and exhibits multi-level dynamics across time. Aiming to tackle the challenge of integrating volatile wind generation into the bulk power grid, we study multiple timescale dispatch and scheduling, for a smart grid model, via day-ahead scheduling and real-time scheduling. In day-ahead scheduling, with the statistical information on wind generation and energy demands, we characterize the optimal procurement of the energy supply and the day-ahead retail price for the traditional energy users; in real-time scheduling, with the realization of wind generation and the load of traditional energy users, we optimize real-time prices to manage the opportunistic energy users so as to achieve system-wide reliability. More specifically, when the opportunistic users are non-persistent, we obtain closed-form solutions to the multi-scale scheduling problem. For the persistent case, we treat the scheduling problem as a multi-timescale Markov decision process, and then we show that it can be recast, explicitly, as a classic Markov decision process.

We believe that the studies we initiated here on multi-timescale dispatch and scheduling for integrating volatile renewal energy into smart grids, scratch only the tip of the iceberg. There are still many questions remaining open to improve the penetration of renewable energy into power grids, and we are currently investigating these issues along this avenue.

References

- [1] J. Chow, W. De Mello, and K. Cheung, “Electricity market design: An integrated approach to reliability assurance,” Proceedings of the IEEE, vol. 93, pp. 1956 –1969, nov. 2005.

- [2] S. Newman, “Smart appliances for an energy-efficient future.” http://green.yahoo.com, 2008.

- [3] R. Sioshansi, “Evaluating the impacts of real-time pricing on the cost and value of wind generation,” Power Systems, IEEE Transactions on, vol. 25, pp. 741 –748, may 2010.

- [4] M. Albadi and E. El-Saadany, “Demand response in electricity markets: An overview,” in Power Engineering Society General Meeting, 2007. IEEE, pp. 1 –5, 24-28 2007.

- [5] J. Bialek, P. Varaiya, and F. Wu, “Risk limiting dispatching smart grid.” Talk at CNLS Smart Grid Seminar Series, 2009.

- [6] F. Bouffard and F. Galiana, “Stochastic security for operations planning with significant wind power generation,” Power Systems, IEEE Transactions on, vol. 23, pp. 306 –316, may 2008.

- [7] L. Xie and M. Ilic, “Model predictive dispatch in electric energy systems with intermittent resources,” in Systems, Man and Cybernetics, 2008. SMC 2008. IEEE International Conference on, pp. 42 –47, 12-15 2008.

- [8] A. J. Wood and B. F. Wollenberg., Power generation, operation, and control. New York : J. Wiley Sons, 1996.

- [9] J. Hetzer, D. Yu, and K. Bhattarai, “An economic dispatch model incorporating wind power,” Energy Conversion, IEEE Transactions on, vol. 23, pp. 603 –611, june 2008.

- [10] Y. L. Xu and J. Chen, “Characterizing nonstationary wind speed using empirical mode decomposition,” Journal of Structural Engineering, vol. 130, no. 6, pp. 912–920, 2004.

- [11] H. Allcott, “Real time pricing and electricity markets.” Harvard University, Jan. 2009.

- [12] R. Boisvert, P. Cappers, B. Neenan, and B. Scott, “Industrial and commercial customer response to real time electricity prices.” available online at http://eetd.lbl.gov/ea/EMS/drlm-pubs.html, Dec. 2004.

- [13] S.-E. Fleten and E. Pettersen, “Constructing bidding curves for a price-taking retailer in the norwegian electricity market,” Power Systems, IEEE Transactions on, vol. 20, pp. 701 – 708, may 2005.

- [14] H. Agabus and H. Tammoja, “Estimation of wind power production through short-term forecast,” Oil shale, vol. 26, no. 3S, pp. 208–219, 2009.

- [15] H. Van de Water and J. Willems, “The certainty equivalence property in stochastic control theory,” Automatic Control, IEEE Transactions on, vol. 26, pp. 1080 – 1087, oct 1981.

- [16] M. Mahmoud, “Multilevel systems control and applications,” IEEE Trans. Syst., Man, Cybern., vol. SMC-7, jun 1977.

- [17] H. S. Chang, P. J. Fard, S. I. Marcus, and M. Shayman, “Multitime scale markov decision processes,” Automatic Control, IEEE Transactions on, vol. 48, jun 2003.

- [18] M. L. Puterman, Markov decision processes: discrete stochastic dynamic programming. New York : J. Wiley Sons, 1994.

- [19] E. A. Feinberg and A. Shwartz, Handbook of Markov Decision Processes. Springer Netherlands: International Series in Operations Research and Management Science Series, jun 2005.