Efficient estimation of one-dimensional diffusion first passage time densities via Monte Carlo simulation

Abstract.

We propose a method for estimating first passage time densities of one-dimensional diffusions via Monte Carlo simulation. Our approach involves a representation of the first passage time density as expectation of a functional of the three-dimensional Brownian bridge. As the latter process can be simulated exactly, our method leads to almost unbiased estimators. Furthermore, since the density is estimated directly, a convergence of order , where is the sample size, is achieved, the last being in sharp contrast to the slower non-parametric rates achieved by kernel smoothing of cumulative distribution functions.

0. Introduction

The problem of computing the distribution of the first time that a diffusion crosses a certain level naturally arises in many different contexts. As probably the most prevalent we mention quantitative finance, where first passage times are used in credit risk (times of default) as well as in defining exotic contingent claims (so-called barrier options). In this paper, we focus on the numerical computation of the probability density function of first-passage times associated with a general one-dimensional diffusion.

Densities of first passage times have known analytic expressions only in very particular cases. The primary example is Brownian motion with certain (constant) drift and diffusion rates, where one uses a combination of Girsanov’s theorem and the special case of standard (driftless) Brownian motion. The first passage time density for the latter case can be obtained by the reflexion principle — see, for example, [11, 2.6A]. Another example of explicit form of the first-passage time density is the case of the radial Ornstein-Uhlenbeck process — see [7] and [10].

In absence of general analytic expressions for first passage time distributions, computational methods are indispensable and, in fact, widely used. One branch uses Volterra integral equations — we mention [5], [16] and [2] as representative papers dealing with this approach. Alternatively, one can use Monte-Carlo simulation to attack this problem. The simplest scheme uses the so-called Euler scheme in order to approximate the solution of the stochastic differential equation governing the diffusion at predetermined grid time-points , , where is the step size, stops at the first time that the diffusion crosses the level of interest, and continuing this way obtain an estimator for the cumulative distribution function of the first-passage time. As the Euler scheme is only approximate111To account for the fact the passage can potentially happen in-between the sampled points, a Brownian bridge interpolation may be used — this means that the conditional probability distribution of first-passage time occurred in the interval given the simulated values at the end points is approximated by that of a Brownian bridge. This could potentially reduce the bias, but the whole scheme is still only approximate and some bias remains., it causes bias in the estimation of the probability distribution function. (See [8] for general discussion, [9] for the evaluation of error via partial differential equations and [3] for a sharp large deviation principle approach.) The issue with the bias becomes immensely more severe in the numerical computation of the density, as it will involve some kind of numerical differentiation of the (non-smooth) empirical distribution function. Even if one uses an exact simulation approach for the diffusion in question (which is, of course, available only in special cases), the estimator for the density will have huge variance. To top it all, even if all the aforementioned problems can be eliminated, one can never hope for convergence of the estimators to the true density in order , where is the “path-sample” size, as the problem is non-parametric.

In this work, we offer an alternative approach which has clear advantages. First, we arrive at a representation of the density function in terms of expectation of a functional of a three-dimensional Brownian bridge. This makes it possible to estimate directly the first passage time density without having to rely on estimators of the cumulative distribution function, achieving this way the “parametric” rate of convergence , where is the sample size. Furthermore, only the three-dimensional Brownian bridge is involved in the simulation, which can be carried out exactly. There is an integral involving the previous three-dimensional Brownian bridge, which can be approximated via a Riemann sum; therefore, the error of the approximation can be estimated efficiently. By construction, our method significantly improves both the bias and variance of the density estimation obtained via the empirical distribution function. The only potential problem of our approach is large-time density estimation, since the thin grid that has to be used in the simulation of the Brownian bridge will result in high computational effort. To circumvent this issue, we notice that the tails of the first-passage distribution usually decrease exponentially with a rate that can be expressed as the principal eigenvalue of a certain Dirichlet boundary problem involving a second-order ordinary differential equation. This implies that a mixture of Monte-Carlo and ordinary differential equation techniques can be efficiently utilized and improve the quality of our estimator.

The structure of the paper is simple. In Section 1, the problem is formulated and the key representation formula is obtained. In Section 2, we discuss the Monte-Carlo estimator of the first passage time density function, and study its large-sample properties. In Section 3, the relation between the exponential tail decay of the probability density and the eigenvalues of a Dirichlet boundary problem is discussed. The proofs of all the results are deferred to Appendix A in order to keep the presentation smooth in the main body of the paper.

1. A Representation of First-Passage-Time Densities

1.1. The set-up

Consider a one-dimensional diffusion with dynamics

| (1.1) |

Above, is a standard one-dimensional Brownian motion. The restrictions on the drift function that we shall impose later (Assumptions 1.2) ensure that (1.1) has a weak solution, unique in the sense of probability law, for any initial condition . Let will denote the law on the canonical path-space of continuous functions from to that makes the coordinate processes behave according to (1.2) and is such that .

Define to be the first passage time of at level zero. We shall consider the problem of finding convenient, in terms of numerical approximation using the Monte-Carlo simulation technique, representations of the quantity

i.e., the density of the first-passage time of the diffusion at level zero.

Remark 1.1.

The fact that we are using unit diffusion coefficient in (1.1) by no means entails loss of generality in our discussion. Indeed, consider a general one-dimensional diffusion with dynamics

| (1.2) |

where is a standard one-dimensional Brownian motion, such that . If (1.2) has a weak solution unique in the sense of probability law, we may assume without loss of generality that . (Indeed, otherwise we replace by in (1.2) and we obtain the same law for the process .) Consider a level . Under the mild assumption that is locally integrable, the transformation defines a diffusion with dynamics , for a function that is easily computable from and . With , the first passage time of with at level is equal to the first passage time of with at level zero.

1.2. The representation

The following assumption on the drift function in (1.1) will allow us to arrive at a very convenient representation for the density function .

Assumption 1.2.

The function restricted on is continuously differentiable, and satisfies

In particular, under Assumption 1.2, is locally square integrable on and the function

| (1.3) |

is continuous and locally integrable. The theory of one-dimensional diffusions ensures that for all there exists a probability on such that the coordinate process has dynamics given by (1.1). Assumption 1.2 also ensures that , which is stopped at level zero, does not explode to infinity — see, for example, [11, Proposition 5.32 (iii)].

Proposition 1.3.

Suppose that Assumption 1.2 is in force. On , consider the probability under which the coordinate process is a standard 3-dimensional Brownian bridge. Then,

holds for all , where and is the density given for all by

| (1.4) |

corresponding to the first-passage time to zero of a standard Brownian motion starting from .

2. Monte-Carlo Density Estimation

We now discuss issues related to estimation of the density . For the purposes of this and the next section, we fix a drift function satisfying Assumption 1.2 and we write for in order to simplify notation.

2.1. Convergence

It is clear how to get an estimate of the density for a given , at least in theory. One simulates independent paths of 3-dimensional Brownian bridge , and then defines the estimator for via

| (2.1) |

where recall that is given in (1.4). By the strong law of large numbers, the estimator converges almost surely to the true density as goes to infinity for each fixed . Moreover, the estimator is unbiased222Of course, only holds if we assume that we actually have the whole path of each Brownian bridge simulated exactly, which is not possible in practice. However, we can simulate exactly discretized paths of the Brownian bridge, and then can easily estimate the order of bias from the Riemann approximation of the integral. In this respect, see also §3.2. and the variance of the estimator decreases in the order of , for every fixed , as a direct consequence of (2.1). In order to get weak convergence of the whole empirical densities , as well as the uniform rate of convergence over compact time-intervals, we introduce an additional assumption.

Assumption 2.1.

The next two results are concerned with a central limit theorem for the whole density function estimator as well as the uniform rate of convergence on compact intervals of .

Proposition 2.2.

Suppose that Assumption 2.1 holds. For , define . Then, the family of stochastic processes is tight. As , converges weakly to a centered Gaussian process with continuous covariance function , where, with for ,

Proposition 2.3.

Remark 2.4.

In a similar manner, for fixed and in with , we may show that

is bounded in probability. Moreover, under some additional conditions on differentiability of , we may estimate the partial derivatives of with respect to via differentiating the estimator with respect to the variable of interest.

3. The Rate Function

Recall that we are dropping the qualifying “” from “” in order to simplify notation. Define implicitly the function via

In other words, and in view of Proposition 1.3, we have

| (3.1) |

3.1. Theoretical results

Proposition 2.3 ensures the uniform convergence of the estimator on finite intervals for fixed . Of course, it is almost always the case that . For large , gives a better understanding of the behavior of the density function, as it represents in a certain sense the exponential decrease of ; therefore, it makes more sense to focus on rather than . In fact, the following result implies that the function is frequently bounded on — this is the case, for example, when is bounded from below.

Proposition 3.1.

Let Assumption 1.2 be valid. Then,

| (3.2) |

where for . Furthermore, if is bounded from below, then

| (3.3) |

Remark 3.2.

The inequalities (3.2) only imply bounds for the inferior and superior limit of as . In fact, it is expected that exists, possibly except in pathological cases. Let us argue below for this point on a rather loose and intuitive level.

The stopping time can be approximated by the sequence , where, for all , is the first exit time of from the interval . Therefore, the rate function may be approximated by the corresponding rate functions corresponding to , . It follows from [6] that the density function of has the eigenvalue expansion (see also [12], [17] for similar problems)

for some functions computed from the eigenfunctions and the corresponding eigenvalues of the Dirichlet problem

| (3.4) |

for with . Thus, the limit as for the rate function of is exactly the principal eigenvalue :

which does not depend on the initial value . Since , it is conjectured that the limit of as actually exists and is equal to . A thorough study of finding a reasonable sufficient conditions for

to hold for lies beyond the scope of this paper.

3.2. Practical issues

In view of Proposition 2.2 and Proposition 2.3, the estimator of (2.1) convergences uniformly with rate over compact time-intervals. In practice, the computation of (2.1) is implemented by generating a standard 3-dimensional Brownian bridge, which is simulated in an exact way over a thin enough grid. The approximation error for the Riemann integral over the finite interval in (2.1) can be controlled very efficiently. More precisely, the numerical computation of the exponential functional of the Brownian bridge in (2.1) can be carried out using the fourth-order Runge-Kutta scheme which is proposed and analyzed in [14]. Under appropriate mild regularity conditions on the function , it is shown that this numerical scheme is weak order of convergence . For this numerical issue, consult the original paper [14] and the related monographs [8], [13] and [15].

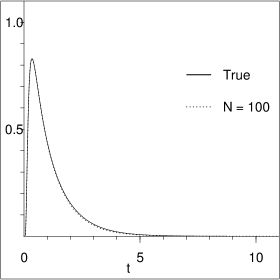

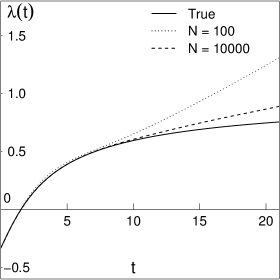

A potential problem with our estimator can arise for large , that is, the density function at the tail. Note that what is meant here is that the relative error of the estimator of tends to be large; the absolute error tends to be extremely small, as is very close to being zero for large . To visualize the issue, it is helpful to study by experiment the large-time behavior of the rate function (3.1) when is an Ornstein-Uhlenbeck (OU) process starting with . Here and for . The first-passage time density of this OU process is known analytically (see, for example, [10, equation (8)]) and reads

| (3.5) |

|

|

| (a) Density functions and . | (b) Rate functions and . |

The true density (3.5) and the estimated density (2.1) with simulations are shown over interval in Figure 1(a). Note that even with this small number of simulations, the two curves are almost indistinguishable. Figure 1(b) contains graphs of the more refined rate functions. In this scale, one can see that the estimation of the exponential rate of decay of the density for large is not as good. (As can be seen from 1(b), on the interval , the true and estimated rate functions almost coincide. However, on the interval , the estimated rate functions are much larger than the true rate function , which implies that the estimator (2.1) underestimates the tail probability.) In fact, the estimated asymptotic rate seems to increase linearly instead of converging to a finite limit. This becomes clear once one notes that, in this OU example,

therefore, the estimator for for sample size becomes

| (3.6) |

Observe that the leading term in the estimator of will be increasing linearly in .

In order to overcome this poor situation in the tail, one can use a mixture method combining the estimator (2.1) on the finite interval and an estimator for the tail probability of the form

for some choice of large threshold , where is the principal eigenvalue of the Dirichlet problem (3.4) for some choice of large threshold , and is chosen so that the density estimator is continuous. The principal eigenvalue can be numerically computed from the Sturm-Liouville problem

(see [20]) with the same Dirichlet boundary conditions, by use of either the variational method or the Liouville transform method. In the variational method, the principal eigenvalue is obtained by minimizing numerically the corresponding Rayleigh quotient. The Liouville transform method turns the Sturm-Liouville equation into a Schrödinger-type equation, which is then numerically solvable with discrete approximation. Both numerical methods are well studied — see [1] and their references within.

Appendix A Proofs

A.1. Proof of Proposition 1.3

Consider the non-negative -supermartingale

| (A.1) |

As follows from a modification of [11, Exercise 5.5.38] for the restricted state space , is a -martingale. With being the probability on that makes the coordinate process behave like a Brownian motion staring from and stopped when it reaches level zero, Girsanov’s theorem implies that

| (A.2) |

for all . Moreover, since , Itô’s formula (under ) implies that, on the set ,

Combining this with (1.1) and (1.3), the stochastic exponential defined in (A.1) under satisfies

| (A.3) |

on , where is a standard Brownian motion under . Therefore, (A.2) and (A.3) imply

for .

Note that the density function of under is given by in (1.4). Using the regular conditional -expectation of , given , we can write

| (A.4) |

Given , the regular conditional -distribution of is that of a 3-dimensional Bessel bridge from to over as a consequence of [19, Proposition VI.3.10 and Proposition VII.4.8]. On the canonical space with coordinate process , the process has the exact law of the aforementioned Bessel bridge. Therefore,

Combining this with (A.4), the proof of Proposition 1.3 is complete.

A.2. Proof of Proposition 2.2

The following technical result is the backbone of the proof.

Lemma A.1.

Proof.

First, note that (2.2) in Assumption 2.1 implies that for every ,

Using these inequalities, we obtain estimates for for every and every ,

| (A.6) |

where , , are polynomial functions of and do not depend on , .

Fix . For , and , consider the random variables , , . Using the estimates established before, we obtain estimates for in (A.5):

| (A.7) |

where we have used (A.6) in the second inequality, since , , used in the third inequality, and in the fourth inequality for .

Finally, since is bounded from below by Assumption 2.1, so is in (A.5), that is, for every . With this observation, because of monotonicity and differentiability of exponential function, we obtain for ,

where . Combining this with the estimates for and in (A.7), we obtain, for ,

where and are defined in (A.6), and hence can be written as a polynomial function of whose coefficients do not depend on nor on but on . Letting be , and noting that all positive integer moments of maximum of standard -dimensional Bessel Bridge are finite ([18, Corollary 7]), we conclude the proof of Lemma A.1. ∎

Let us define for . It follows from Lemma A.1 that is locally Lipschitz continuous and moreover,

Since the random paths are independent and identically distributed, for any we obtain

| (A.8) |

where the constant depends on but not on . This inequality is a sufficient condition for the tightness of the sequence of continuous stochastic processes starting at in — see [11, Problem 2.4.12]. By the usual multi-dimensional central limit theorem, for each , the sequence of random vectors converges in distribution to a Gaussian random vector with mean zero and and variance-covariance matrix , where

Therefore, we conclude that the tight sequence converges weakly to a continuous Gaussian process with mean zero and continuous covariance function .

A.3. Proof of Proposition 2.3

Define that Gaussian tail function via

Furthermore, for fixed , define the modulus of continuity in :

| (A.9) |

It follows from (A.8) that for ; therefore, . We recall the following Fernique’s inequality for Gaussian processes, which we shall use.

Lemma A.2 (Fernique’s inequality — see (2.2) of [4]).

The weak convergence of to and the invariance principle for the maximum function imply that the sequence of normalized maxima converges weakly to , where is the limiting Gaussian process, as goes to infinity. Since the law of the last random variable does not charge , we conclude that the family is bounded in probability.

A.4. Proof of Proposition 3.1

For the lower bound in (3.2) let us observe

by Assumption 2.1. Therefore,

For the upper bound in (3.2), for a fixed let us consider . On , holds for ; hence,

where for . It follows that, for ,

and hence

| (A.10) |

The distribution for the maximum of the absolute value of the standard 3-dimensional Bessel bridge is known — see, for example, [18, (5)]. More precisely, we have

| (A.11) |

where is the Bessel function of index . In particular,

as only the first term in the summand in the series in (A.11) will play a role in the limit. Combining the last limiting relationship with inequality (A.10), we obtain

Upon minimizing the right-hand side of the last inequality, the upper bound in (3.2) is obtained.

Finally, to verify (3.3), observe that being bounded from below implies that the random variables are uniformly bounded for small . Then, de L’Hôspital’s rule and the bounded convergence theorem give

References

- [1] Spectral theory and computational methods of Sturm-Liouville problems, vol. 191 of Lecture Notes in Pure and Applied Mathematics, New York, 1997, Marcel Dekker Inc. Edited by Don Hinton and Philip W. Schaefer.

- [2] L. Alili and P. Patie, Boundary-crossing identities for diffusions having the time-inversion property, J. Theoret. Probab., 23 (2010), pp. 65–84.

- [3] P. Baldi, L. Caramellino, and M. G. Iovino, Pricing general barrier options: a numerical approach using sharp large deviations, Math. Finance, 9 (1999), pp. 293–322.

- [4] S. M. Berman, An asymptotic bound for the tail of the distribution of the maximum of a Gaussian process, Ann. Inst. H. Poincaré Probab. Statist., 21 (1985), pp. 47–57.

- [5] J. Durbin, The first-passage density of a continuous Gaussian process to a general boundary, J. Appl. Probab., 22 (1985), pp. 99–122.

- [6] J. Elliott, Eigenfunction expansions associated with singular differential operators, Trans. Amer. Math. Soc., 78 (1955), pp. 406–425.

- [7] K. D. Elworthy, X.-M. Li, and M. Yor, The importance of strictly local martingales; applications to radial Ornstein-Uhlenbeck processes, Probab. Theory Related Fields, 115 (1999), pp. 325–355.

- [8] P. Glasserman, Monte Carlo methods in financial engineering, vol. 53 of Applications of Mathematics (New York), Springer-Verlag, New York, 2004. Stochastic Modelling and Applied Probability.

- [9] E. Gobet, Weak approximation of killed diffusion using Euler schemes, Stochastic Process. Appl., 87 (2000), pp. 167–197.

- [10] A. Göing-Jaeschke and M. Yor, A clarification note about hitting times densities for ornstein-uhlenbeck processes, Finance and Stochastics, 7 (2003), pp. 413–415.

- [11] I. Karatzas and S. E. Shreve, Brownian motion and stochastic calculus, vol. 113 of Graduate Texts in Mathematics, Springer-Verlag, New York, second ed., 1991.

- [12] J. T. Kent, Eigenvalue expansions for diffusion hitting times, Z. Wahrsch. Verw. Gebiete, 52 (1980), pp. 309–319.

- [13] P. E. Kloeden and E. Platen, Numerical solution of stochastic differential equations, vol. 23 of Applications of Mathematics (New York), Springer-Verlag, Berlin, 1992.

- [14] G. N. Milstein and M. V. Tretyakov, Evaluation of conditional Wiener integrals by numerical integration of stochastic differential equations, J. Comput. Phys., 197 (2004), pp. 275–298.

- [15] , Stochastic numerics for mathematical physics, Scientific Computation, Springer-Verlag, Berlin, 2004.

- [16] G. Peskir, On integral equations arising in the first-passage problem for Brownian motion, J. Integral Equations Appl., 14 (2002), pp. 397–423.

- [17] R. G. Pinsky, Positive harmonic functions and diffusion, vol. 45 of Cambridge Studies in Advanced Mathematics, Cambridge University Press, Cambridge, 1995.

- [18] J. Pitman and M. Yor, The law of the maximum of a Bessel bridge, Electron. J. Probab., 4 (1999), pp. no. 15, 35 pp.1–35 (electronic).

- [19] D. Revuz and M. Yor, Continuous Martingales and Brownian Motion, Volume 293 of Grundlehren der Mathematischen Wissenschaften Fundamental Principles of Mathematical Sciences, Springer-Verlag, Berlin, third ed., 1999.

- [20] A. Zettl, Sturm-Liouville theory, vol. 121 of Mathematical Surveys and Monographs, American Mathematical Society, Providence, RI, 2005.