Bayesian Model Selection for Beta Autoregressive Processes

Abstract

We deal with Bayesian inference for Beta autoregressive processes. We restrict our attention to the class of conditionally linear processes. These processes are particularly suitable for forecasting purposes, but are difficult to estimate due to the constraints on the parameter space. We provide a full Bayesian approach to the estimation and include the parameter restrictions in the inference problem by a suitable specification of the prior distributions. Moreover in a Bayesian framework parameter estimation and model choice can be solved simultaneously. In particular we suggest a Markov-Chain Monte Carlo (MCMC) procedure based on a Metropolis-Hastings within Gibbs algorithm and solve the model selection problem following a reversible jump MCMC approach.

AMS codes: 62M10, 91B84, 62F15.

Keywords: Bayesian Inference, Beta Autoregressive Processes, Reversible Jump MCMC.

1 Introduction

The analysis of time series data defined on a bounded interval (such as rates or proportions) has been a challenging issues for many years and still represents an open issue. For modelling data defined on a bounded interval there are at least two alternative approaches. Historically the main approach applies a transform to the data in order to map the interval to the real line and then uses standard time series models. Typical examples of transformations are the additive log-ratio transformation and the Box-Cox transformation (see Aitchinson (1986)). One of the earlier and relevant contributions in this framework is Wallis (1987).

In this paper we follow the second approach, that is based on a direct modelling on the original sample space. Among the first contributions along this line we refer to Grunwald et al. (1993) who suggest a multivariate state space model for times series data defined on the standard simplex. Another seminal contribution is McKenzie (1985) which introduces a new Beta autoregressive process for times series defined on the standard unit interval . In the recent years, Ferrari and Cribari-Neto (2004) introduce the general Beta regression model, showing that is more convenient to consider the data in the original sample space instead of using a transformation. In particular they use a reparametrization, which is often employed for the inference of Beta mixtures (see Robert and Rousseau (2002)), that allows to identify the mean as a parameter of the distribution. Rocha and Cribari-Neto (2009) extend the Beta regression model and propose a Beta autoregressive moving average process which possibly includes exogenous variables in the dynamics. In an applied context Beta regression models have been also recently used in Amisano and Casarin (2007) for modelling dynamic correlation, in Calabrese (2010) for modeling the recovery rate as a mixed random variable and in Billio and Casarin (2010a) and Billio and Casarin (2010b) for modeling the transition matrix of a Markov-switching model. In Billio and Casarin (2010b) a Bayesian procedure for latent Beta autoregressive models of the first order with nonlinear conditional mean is presented.

In particular, the main contribution of this paper is to propose a Bayesian estimation method that allows to estimate the parameters as well as the number of components of Beta autoregressive models. The parametrization used is the same given in Rocha and Cribari-Neto (2009). We handle the autoregressive part of the model, while the moving average part will be object of future research. Without loss of generality, we focus our attention on the linear conditional mean process, which is appealing for forecasting purposes but is more challenging due to the constraints on the parameters. The extension to the nonlinear conditional mean case requires minor modifications of the procedure proposed in this paper. Considering the parameter estimation, we extend the work of Billio and Casarin (2010b) to the case of Beta autoregressive models of order and discuss the choice of priors for autoregressive coefficients, that becomes quite a challenging matter for a Beta autoregressive of general order.

Moreover, in order to select the model order, we propose a Reversible Jump Markov chain Monte Carlo (RJMCMC) algorithm for Beta autoregressive models, extending the works of Brooks et al. (2003b) and Ehlers and Brooks (2008) for Gaussian autoregressive models and Enciso-Mora et al. (2009) for Integer-Valued ARMA processes.

The reversible jump algorithm (see Green (1995)) is an extension of the Metropolis-Hasting algorithm in which the dimension of the parameter space can vary between iterates of the Markov Chain. From a Bayesian point of view, suppose to have a set of models where the model has a vector of parameters of dimension . The set is indexed by a parameter . Then the joint distribution of given the observed data is

| (1) |

where is the product of the likelihood and the joint prior is constructed from the prior distribution of under model and the prior for the model indicator (i.e. the prior for model ).

The RJMCMC algorithm uses the joint posterior distribution in Equation (1) as the target of a Markov chain Monte Carlo sampler over the state space where the states of the Markov chain are of the form , and the dimension of which can vary over the state space. Accordingly, from the output of a single Markov chain sampler, the user is able to obtain a full probabilistic description of the posterior probabilities of each model having observed the data, , in addition to the posterior distributions of the individual models. For a recent account about reversible jump algorithm see Fan and Sisson (2010).

In this paper, in order to design an efficient reversible jump algorithm for Beta autoregressive processes we follow the strategy of Brooks et al. (2003b) and Ehlers and Brooks (2008). We consider jump move and stochastic reverse jump move between spaces of different dimensions and calibrate the parameters of the jump proposal distribution in order to increase the acceptance rate of the move (see Ehlers and Brooks (2008)). The Gaussian assumption allows Ehlers and Brooks (2008) to have a close form solution of the calibration problem, while in the case of the Beta processes this result is no more valid. In our contribution we propose to combine an algorithm for the approximation of the parameter posterior mode with the calibration strategy of the jump proposal. The mode approximation allows us to find a close form solution to the parameter choice of the proposal distribution.

The outline of the paper is as follows. In Section 2 the Beta autoregressive process of order (BAR(k)) is introduced with a suitable parametrization. In Section 3 the Bayesian inference is developed for the BAR(k) model under the choice of some priors. In Section 4 the RJ algorithm is developed for the BAR processes, in particular we studied two strategies. In Section 5 some simulation results are shown and in Section 6 the new machinery is applied to an unemployment rate and capacity utilization datasets.

2 The Beta AR(k) model

Let us define a Beta autoregressive process of the order as follows

| (2) |

where the is the -algebra generated by the process, denotes the type I Beta distribution and and are the two parameters of the distribution, usually referred as shape parameters. The two parameters are -measurable functions and depend possibly on the past values of the process. The process has the following transition density

| (3) |

where is the Beta function with and is the order of the process. In the following we will denote with the -order Beta autoregressive process and assume , with the maximum order of the process.

We considered the Beta distribution because it is a fairly flexible distribution. It is unimodal, uniantimodal, increasing, decreasing or constant depending on the values of its parameters. We refer the reader to Gupta and Nadarajah (2004) for a review on the families of Beta distributions and to Kotz and van Dorp (2004) for a review on the finite range distributions. We consider the Beta of the first type, because the first and second moments of this distribution have a simple expression, which makes it easy to deal with the parameter identification issues. In fact, as suggested by many parts in the literature, the parameters identification should be accurately discussed. For inference and model interpretation purposes it is desiderable that the two parameters and of the Beta distribution are not jointly determining both the shape and the moments of the distribution.

In this work, in order to have an exact identification of the parameters of the conditional mean of the process and of the shape parameter, we consider the parametrization of the Beta distribution suggested for example in Robert and Rousseau (2002) in the context of Bayesian inference for Beta mixtures and in Ferrari and Cribari-Neto (2004) and Rocha and Cribari-Neto (2009) in the context of maximum likelihood inference for general beta regression models.

In the chosen parametrization the conditional distribution of the process at time is

| (4) |

where and represent the precision and location parameters respectively (see Rocha and Cribari-Neto (2009)). In this parametrization the conditional mean of the process coincides with the location parameter and the variance is a quadratic function of the location parameter as well

| (5) |

The process naturally exhibit heteroscedasticity, thus, in the following, we assume that the precision parameter is constant over time, i.e. .

We define , , with and . We assume that is a linear combination of a constant and of the past values of the process. We will assume that where and refer to it as convexity constraints.

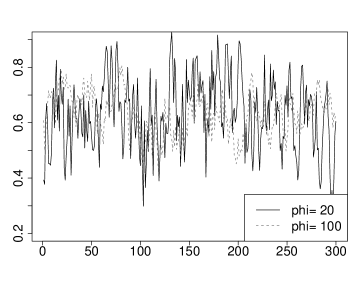

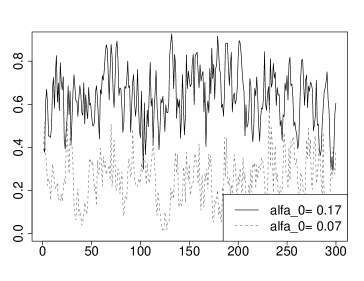

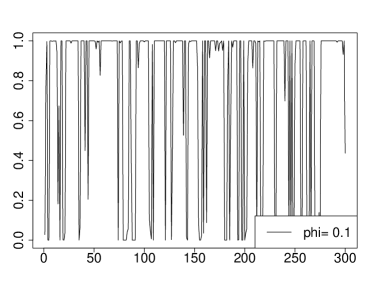

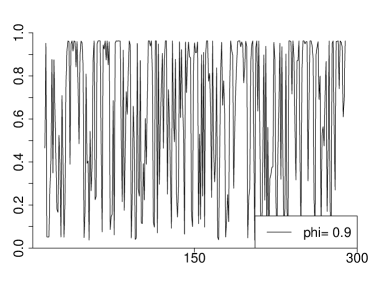

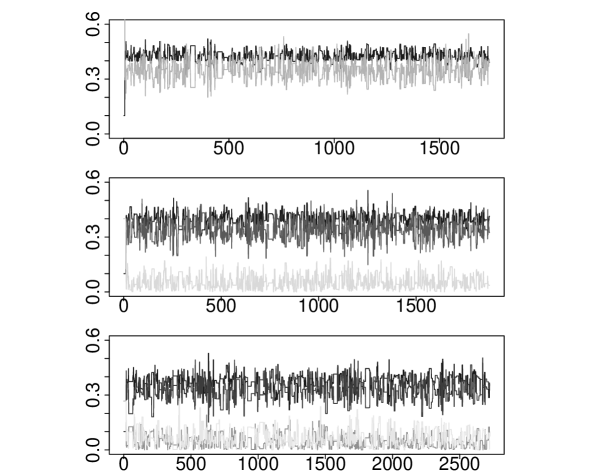

In Fig. 1 there are some sample paths of a Beta process of the third order. The paths are given for different values of the precision parameter and of the constant term . For higher values of the process exhibits less volatility (upper-left chart). The larger the value of the constant term the greater is stationary mean of the process (upper-right chart). Finally we observe that the conditional mean of the process , where and . When and , then and and the transition density of the process is anti-unimodal. In this case the process exhibits a switching-type behavior (see the left and right charts at the bottom of Fig. 1).

This process extends to the order the first-order Beta process proposed in Nieto-Barajas and Walker (2002) and then discussed in a latent variable framework by Amisano and Casarin (2007). The Beta process considered in our work represents a special case of the beta regression model proposed in Ferrari and Cribari-Neto (2004) and of the beta ARMA process introduced by Rocha and Cribari-Neto (2009). We focus on the linear case because it is particularly suitable for forecasting purposes and is more difficult to estimate than the nonlinear case due to the constraints on the parameters, which are necessary in order the process to be defined. In particular we show how to deal with the first-order stationarity constraints in the inference procedure. The Bayesian inference approach presented in the following apply in a straightforward way to the beta ARMA process with non-linear conditional mean given in Rocha and Cribari-Neto (2009).

3 Bayesian inference

The likelihood function of the model is

| (6) |

where and . Note that we consider an approximated likelihood because for a Beta process of the order we assume the observations start in and thus forget the first observations on . Moreover in the following we will assume that the first initial values of the process are known. It is possible to include the initial values in the inference process following, for example, the approach given in Vermaak et al. (2004) for the Gaussian autoregressive processes.

3.1 The priors

The constant term and the coefficients of a BAR(k) belong to the set , thus the usual assumption of Gaussian prior distribution has to be modified. In the following we consider some alternative prior specifications.

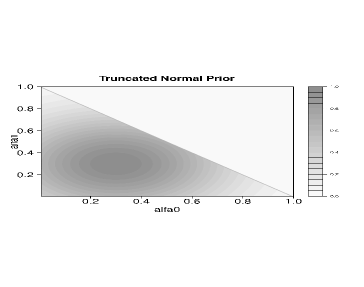

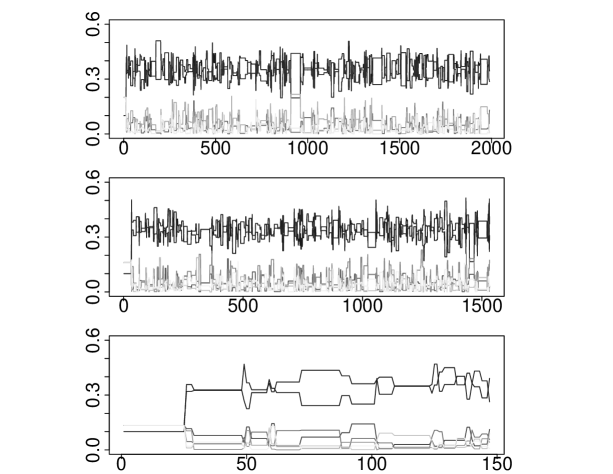

We first considered a multivariate normal with mean and variance , truncated to the set . In the following we will denote with

| (7) |

the density function of the prior on , where is the indicator function. This prior distribution is given, for the case , in the upper-left chart of Fig. 2. In the example we assumed and , where is the -dimensional identity matrix. Using this prior it is not easy to have a uniform prior and at the same time to guarantee the positivity of the parameters of the Beta process transition density, i.e. and . The truncation on the simplex of the normal prior distribution can not guarantee that the inference procedure returns parameter values which satisfy at the desired constraints, and can generate numerical problems in the Monte Carlo procedures employed in the inference process.

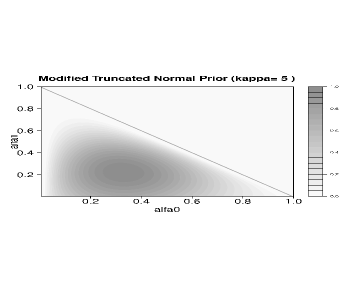

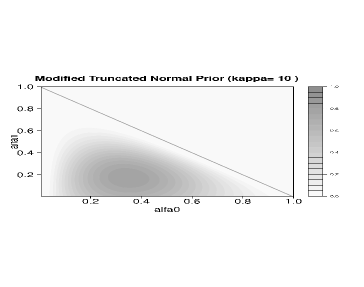

In order to prevent the posterior to take values near the boundaries of the parameter space we follow Robert and Rousseau (2002) and introduce a repulsive factor around the boundaries of the standard simplex defined in the previous section. We observe that and propose the following prior distribution conditional on

| (8) |

where is an hyperparameter. In the upper-right and bottom-left charts of Fig. 2 we show, for the bivariate case, the shape of this prior distribution conditional on for two values of the hyperparameters ( and ). The multiplicative factor creates low density regions near the boundaries for all . In both the simulation experiments and the real data applications considered in Section 5, this kind of prior contributes considerably to avoid the numerical problems in the evaluation of the posterior density and of its gradient and Hessian which are needed for the Monte Carlo based inference procedures. We note the solution of the numerical problems in the evaluation of the posterior distribution is due to the fact that the prior distribution behaves like a penalizing term for the likelihood function and the penalization allows the algorithm to account for the constraints on the parameters.

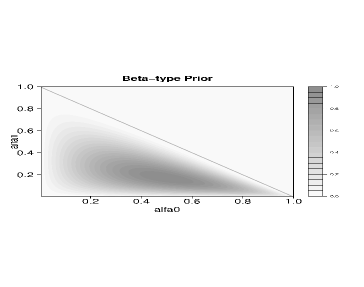

As an alternative, we consider a multivariate distribution which is naturally defined on and which has density function

| (9) |

where and the parameters and .

This distribution has been obtained by considering a set of independent Beta random variables , with , and then the multivariate transformation

| (10) |

This stochastic representation constitutes a natural way to generate random numbers from the multivariate distribution defined above. It is easy to show that thanks to this representation the constraints on the parameters of the Beta process are satisfied, in particular . Bottom-right chart of Fig. 2 shows this prior for the parameter setting and . It can be seen from the picture that this prior gives a low probability mass to the values of near the boundaries and .

The precision parameter is positive, thus we assume a gamma prior

| (11) |

with parameters and and denote with the associated density function.

3.2 A MCMC algorithm

In order to approximate the posterior mean for the parameters of the process we consider a Gibbs algorithm. The full conditional distributions can not be simulated exactly and are simulated by a Metropolis-Hastings (M.-H.) step (see Chib and Greenberg (1995)). The full conditional distribution and the associated simulation method are described in the following.

The full conditional distribution of is

| (12) |

where . To simulate from this distribution we employ a M.-H. algorithm with a proposal distribution which makes use of the information on the local structure of the posterior surface (see Albert and Chib (1993) and Lenk and DeSarbo (2000)). Consider the second-order Taylor expansion of the log-posterior, , centered around .

| (13) |

where represents the approximated mode of the posterior, then at the -th iteration of the M.-H. step we generate a candidate as follows

| (14) |

where . The acceptance rate of this M.-H. step can be easily found. Due to its relevance in the model selection procedure, the approximation method for the posterior mode will be discussed in Section 4.

The full conditional distribution of is

| (15) |

We simulate from the full conditional by a M.-H. step. We consider a Gamma random walk proposal and at the -th step of the algorithm, given the previous value of the chain, we simulate

| (16) |

and accept with probability

| (17) |

4 Model Selection

In this work we propose a Reversible-Jump MCMC (RJMCMC) approach to model selection for Beta autoregressive. See Brooks et al. (2003b) for an introduction to efficient proposal design in RJMCMC algorithms and Ehlers and Brooks (2008) for an application of some efficient adaptive proposals to Gaussian autoregressive processes. See also Vermaak et al. (2004) for an alternative RJMCMC schemes for Gaussian autoregressive. To the best of our knowledge only a few studies exist on the application of RJMCMC algorithms to non-Gaussian autoregressive models. Among the other we refer the interested reader to Enciso-Mora et al. (2009) who proposed a RJMCMC algorithm for model selection in integer valued ARMA models.

In this work we extend the RJMCMC approach of Ehlers and Brooks (2008) to the case of the Beta autoregressive processes of a unknown order. We consider the definition of Beta autoregressive given in Rocha and Cribari-Neto (2009) and restrict our attention to the case of conditionally linear processes because the inference in this context is more difficult due to the restriction on the parameters. Nevertheless the proposed RJMCMC algorithm can be easily extended to the case of a Beta process with a nonlinear conditional mean.

In the following we will show how to deal, in a Beta autoregressive context, with some special constraints which can be imposed in the inference process. First we show how to deal with first order stationarity constraints. We suggest to move between and processes and to consider the innovation process naturally associated to a to design this move. As suggested in Ehlers and Brooks (2008) we choose the parameters of the proposal for jumps between and in such a way to make the acceptance rate close to one.

Secondly we consider convexity constraints on the parameters of the conditional means and suggest to use a trans-dimensional MCMC chain which moves between spaces of any finite dimensions and by employing a suitable proposal distribution. In order to make the acceptance rate close to one we suggest to combine the second-order proposal strategy with a Newton-Rapson type sequential approximation of the posterior mode.

4.1 Stationarity Constraints

Let us define the innovation process , then

| (18) |

where is the lag operator. The innovation process can be written in terms of reciprocal roots

| (19) |

and it is stationary in mean if .

Let be the innovation term associated to and the one associated to a then

| (20) | |||||

if .

Thanks to this representation of the location parameter, the likelihood function of the process will write as

| (21) |

where , is the vector of reciprocal roots of the process which coincide with the first reciprocal roots of the and is the -th reciprocal root of the process.

We assume independent Beta priors for the reciprocal roots of the process and in order to assure that the constraints on the autoregressive coefficients are satisfied (see Appendix A), we let and define for , with . We denote with and the densities associated to these priors.

In order to design a reversible jump algorithm, which allows for jumps between posterior distributions with different dimensions, we need a model prior, a proposal distribution for the model order and for the new parameters and finally a link function between the parameter spaces of the two models. In the following we will assume that the model prior associated to is uniform: , where is the maximum order of the process and denote with the associated density function. As a proposal for the order of the new model we consider a Bernoulli distribution with probability . We assume a truncated normal distribution as a proposal for the new root, i.e. truncated to and denote with its density. Finally, as suggested in Ehlers and Brooks (2008), we consider an identity dimension matching function .

The acceptance ratio of the move from a -order autoregressive to an autoregressive of order is

| (22) |

where is the Jacobian of the transformation. Under the above assumptions the acceptance rate simplifies to

| (23) |

As suggested in Ehlers and Brooks (2008) the likelihood of the and the models are identical at , which is a weak non-identifiability centring point. We use the centring point to find the parameters of the second-order proposal. To this aim we consider the first and second order derivatives of the log-acceptance ratio.

The log-acceptance ratio of the move from a Beta process of order to one of order is

| (24) |

where is the log of a normalizing constant which does not depend on . The first- and second-order derivatives of the log-acceptance ratio are

| (25) | |||

| (26) |

where and are the digamma and trigamma functions respectively.

We evaluate the first- and second-order derivatives at , solve for and and find the parameters of the proposal

| (27) | |||||

| (28) |

where

4.2 Convexity Constraints

In order to deal with the convexity constraints on the parameters in the conditional mean of the BAR process we suggest to use RJMCMC moves between spaces with any positive dimensions difference, and to control for the constraints by a suitable choice of the proposal distribution for the parameters.

Given the parameter vector , the RJMCMC proposes a jump to the space by generating from a discrete distribution and then proposing a -dimensional parameter vector from the distribution , which we assumed to be defined on the standard simplex. For the dimensions matching we consider the transform , which has unitary Jacobian. The acceptance probability of the proposal is

As proposal we consider a parametric family of distributions and choose the parameters in such a way that the log-acceptance rate is approximately equal to zero.

We consider a second-order methods and focus on the gradient and the Hessian of the log-acceptance rate with respect to . Note that the gradient naturally splits in the two subvectors, that are the gradient with respect to and the one with respect to . The cross derivatives in the Hessian are null. In the following we consider the case for , the case for being similar.

We choose the parameters of the proposal such that

where and have been defined in the previous section.

It should be noticed that as opposite to the Gaussian autoregressive model studied in Ehlers and Brooks (2008), the gradient and the Hessian depend on . In this work we decide to evaluate the derivatives at the approximated posterior mode , which is defined on the -dim space.

As an example let use consider a Gaussian distribution as proposal with mean and variance . Assume that the prior is the Gaussian distribution truncated on the simplex, then we solve the above system of equations (see Appendix B for the gradient and the Hessian in the Gaussian case) with respect to and and find

By applying the same procedure for the derivatives with respect to we obtain a full modal centering procedure, which promotes jumps between modes in the -dimensional and -dimensional spaces.

We do not know the value of the posterior mode and in order to find an approximation we suggest to use a Newton-Rapson procedure. More specifically at the iteration of the RJMCMC procedure the approximated mode is determined by the following recursion

| (29) |

where . The gradient and the Hessian of the log-posterior, and respectively, are

In Appendix B we provide the analytical expressions for the gradient, , and the Hessian, , of the log-prior, for the different choices of the prior discussed in Section 3. After an initial learning period the posterior mode in the various spaces of different dimension is reached with a certain tolerance value and the log-acceptance rate of the jump move is close to zero as effects of the choice of the proposal parameters.

Finally it should be noticed that the approximation of the posterior mode in the jump step is also used in the M.-H. steps within the Gibbs sampler for simulating the parameters, thus no further computational burden is required for this approximation.

5 Simulation Results

In this section we study, through some simulation experiments, the efficiency of the proposals for both within and between models moves. In order to check if the chain mix well we estimate the acceptance rate of the M.H. steps, the effective sample size and the convergence diagnostic statistics.

In a first set of experiments we verify the efficiency, in terms of mixing, of the proposals of the Metropolis-Hastings step of the moves for a given dimension and for the different choices of the prior distribution and parameter settings.

In each experiment we proceed as follows. For each model order and parameter setting , we generate 50 independent random samples with size from a . On each dataset we iterate the MCMC algorithm, defined in the previous sections, for times. We consider dataset of observations because this is the typical sample size of the applications to real data we have in mind and that will be presented in the next section. This allows us to estimate the magnitude of the parameter estimation errors (root mean square error) associated to the inference procedure for the chosen sample size.

As regard to the values of the parameters we consider two scenarios. In the first one we set the precision parameter , which corresponds, as highlighted in Fig. 1, to the case of high variability in the data. We will call low precision data all the dataset simulated with this value of the precision parameter. We expect that the parameter estimation is more challenging in this context.

In the second scenario, which is more frequent in the applications we will consider in the next section, we set the precision parameter that is a higher value than the ones considered in the first scenario. In this case the data exhibits less variability (see Fig. 1). We will call high precision data all the dataset simulated with this precision value.

For each scenario we consider different values for the parameters and different autoregressive orders. The resulting parameter settings, which have been used in the MCMC experiments, are given in Tab. 1. We also evaluate the efficiency of the MCMC algorithm for different choice of the prior distribution and consider the truncated normal distribution with parameters and and the modified truncated normal distribution with parameters , and and the Beta-type distribution with parameters and .

| 1 | ||

| 2 | ||

| 3 | ||

| 4 |

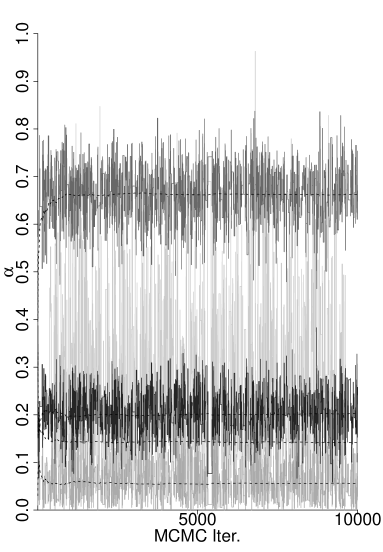

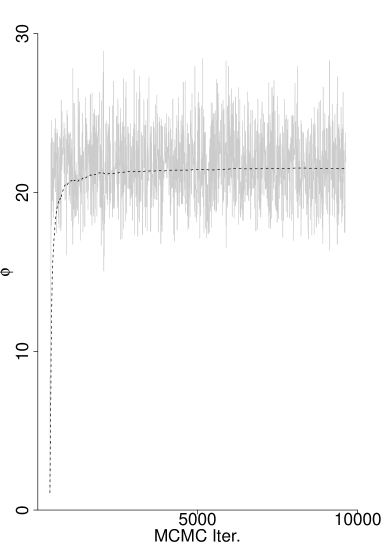

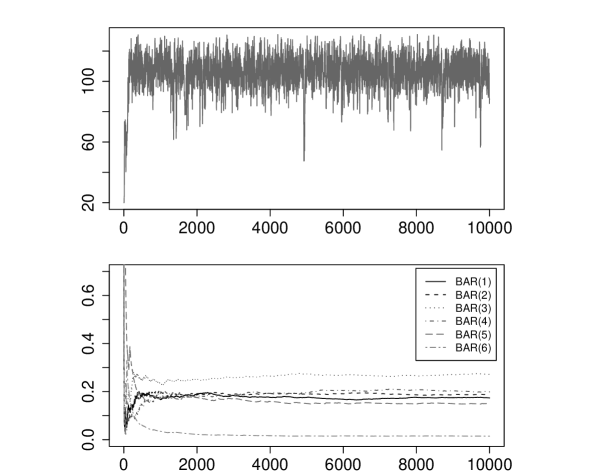

Fig. 3 shows typical raw output and progressive averages of iterations of the MCMC chain for (left chart) and (right chart). In these figures, the initial value of the Gibbs sampler and the burn-in sample are included in order to show the convergence of the MCMC progressive averages to the true values of the parameters. In this example, we considered a sample of observations simulated from a BAR(3) model with parameters and .

For each set of 50 independent MCMC experiments of length we estimate the RMSE, the average acceptance probability (ACC) of the M.-H. within Gibbs steps and the following quantity

| (30) |

that is the effective sample size (ESS) of the MCMC sample for a parameter . In order to evaluate the RMSE and the other statics we consider MCMC iterations and discard the output of the first 1000 iterations.

In the various experiments we will also evaluate the number of MCMC iterations which are necessary to our MCMC algorithm to reach convergence. It should be noticed that the choice of the number of MCMC iterations is still an open issue (see Robert and Casella (2004) and Guihenneuc-Jouyaux et al. (1998)). In this work we combine a graphical inspection of the progressive averages of the parameter posterior distribution with the evaluation of a convergence criteria based on the Kolmogorov-Smirnov (KS) test (see Robert and Casella (2004), Ch. 12). See also Brooks et al. (2003a) for an alternative use of the KS statistics for detecting convergence in RJMCMC chains. In the simulation experiments, for each component of the parameter vector , we split the associated MCMC sample , in two subsamples and with and evaluate

| (31) |

where is the batch size. The use of batches is necessary in order to obtain quasi-independent samples. The independence of the samples is one of the assumption to have a known limiting distribution for the KS statistics. For each experiment we will show the average p-value of the KS statistics over the vector of parameters and over the last 100 iterations of the MCMC chain.

We summarize the results of the MCMC experiments in Tab. 2. The results for the Beta-type prior and for the modified truncated-Gaussian are similar, thus the choose to present the results for modified truncated-Gaussian prior. From Tab. 2 we note that the RMSE of the autoregressive coefficients and of the parameter tends to grow with the model order. This suggests that the higher the number of parameters to be estimated the lower the precision of the estimates. Besides, the precision of the estimate is influenced by the number of parameters, as it decreases as the model order increases.

| Low precision data | |||||||||

| k | Estimated RMSE | ||||||||

| Truncated-Gaussian Prior (, ) | |||||||||

| 1 | 0.032 | 0.058 | 0.376 | 0.176 | 704 | 0.534 | |||

| 2 | 0.033 | 0.043 | 0.023 | 0.996 | 0.172 | 630 | 0.552 | ||

| 3 | 0.087 | 0.094 | 0.026 | 0.051 | 2.092 | 0.163 | 584 | 0.523 | |

| 4 | 0.041 | 0.011 | 0.019 | 0.075 | 0.032 | 3.727 | 0.155 | 538 | 0.541 |

| Modified Truncated-Gaussian Prior (, , ) | |||||||||

| 1 | 0.033 | 0.051 | 0.392 | 0.181 | 1013 | 0.556 | |||

| 2 | 0.032 | 0.055 | 0.021 | 0.916 | 0.183 | 853 | 0.563 | ||

| 3 | 0.015 | 0.077 | 0.018 | 0.059 | 1.701 | 0.192 | 783 | 0.574 | |

| 4 | 0.030 | 0.023 | 0.013 | 0.059 | 0.034 | 2.564 | 0.189 | 740 | 0.539 |

| High precision data | |||||||||

| k | Estimated RMSE | ||||||||

| Truncated-Gaussian Prior (, ) | |||||||||

| 1 | 0.011 | 0.018 | 0.964 | 0.392 | 923 | 0.513 | |||

| 2 | 0.029 | 0.047 | 0.031 | 1.815 | 0.402 | 827 | 0.546 | ||

| 3 | 0.038 | 0.071 | 0.032 | 0.002 | 3.122 | 0.422 | 798 | 0.593 | |

| 4 | 0.021 | 0.038 | 0.037 | 0.007 | 0.029 | 6.430 | 0.538 | 778 | 0.511 |

| Modified Truncated-Gaussian Prior (, , ) | |||||||||

| 1 | 0.017 | 0.021 | 0.392 | 0.403 | 1198 | 0.511 | |||

| 2 | 0.020 | 0.028 | 0.001 | 1.101 | 0.420 | 1012 | 0.534 | ||

| 3 | 0.031 | 0.063 | 0.003 | 0.002 | 1.539 | 0.428 | 941 | 0.529 | |

| 4 | 0.029 | 0.033 | 0.033 | 0.001 | 0.018 | 3.955 | 0.509 | 830 | 0.542 |

Moreover, the RMSEs of the high precision data results are generally lower than RMSEs of low precision data, with the exception of the parameter that seems to behave differently from the autoregressive coefficients. However, in order to correctly evaluate the outcomes, we need to compare the RMSE to the value of the parameter. For example, for the Truncated-Gaussian prior the estimated RMSE of for the low precision is equal to and the corresponding high precision RMSE is equal to . However, dividing this two values by the related value ( and respectively) we get percentages of and , showing a better performance for high precision results, as expected.

The third column of Tab. 2 lists the average acceptance rate of the parameters. As it is clear from the table, data with higher precision show a noticeably improvement in terms of ACC compared to data with lower precision. However, we need to point out that Tab. 2 displays the average acceptance rate and the improvement is due mainly to the higher ACC value of the parameter, since the ACC of the autoregressive coefficients is very similar for both type of data.

The ESS is the number of effectively independent draws from the posterior distribution and it is a measure of the mixing of the Markov chain. In our case, this measure decreases and denotes a worse mixing as the order of the process increases. Moreover, as we see in the fourth column of Tab. 2, ESS values are higher in high precision data, showing a better mixing than in low precision data.

The average p-values of the KS statistic, in the last column of Tab. 2, take values close to 0.5 for the different precision of the data and the different model orders, suggesting the acceptance of the null hypothesis that the subsamples associated to the Markov chain have the same distribution, guaranteeing convergence. Besides, since Tab. 2 displays only the average p-values, we underline that over the last 100 iterations of the Markov chains the KS p-values improved, getting closer to 1.

Comparing now the outcomes related to the priors used, the Modified Truncated-Gaussian prior performs better than the Truncated-Gaussian prior for both the low and high precision data. As we notice from Tab. 2, the RMSEs of the autoregressive coefficients are quite similar, but the RMSE of the parameter calculated with the modified prior is sensibly lower. Moreover, the ACC and the ESS values of the modified prior are slightly higher, denoting a better mixing of the Markov chains. The p-values of the KS statistic indicate convergence to the target distribution, being close to the value of 0.5.

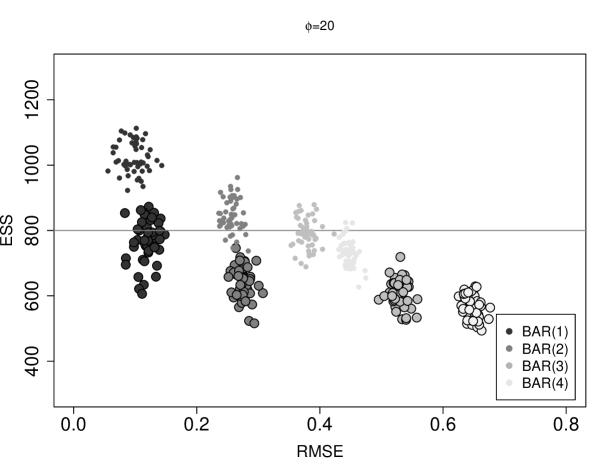

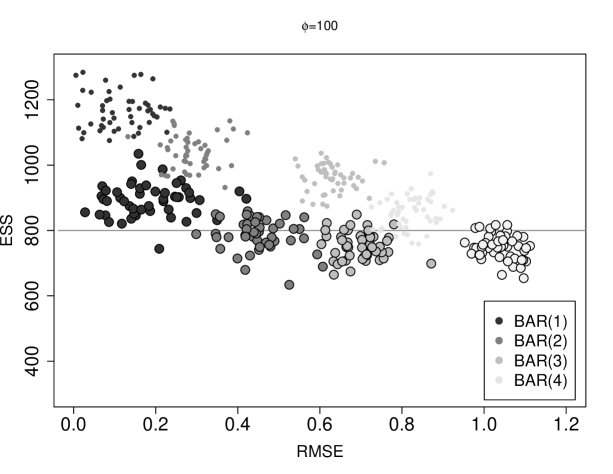

Fig. 4 gives a more detailed description of the behavior of the RMSE and of the ESS in the MCMC experiments. Fig. 4 illustrates the parameters RMSE on the -axis and the ESS of the two M.H. steps on the -axis, for the 50 MCMC simulation experiments. Large circles denote the truncated-Gaussian prior results, while small circles denote the modified truncated-Gaussian prior results. The different colors of the circles indicate the different order of the . The top plot displays low precision results () and the bottom plot displays high precision results ().

For both high and low precision data, the RMSE grows with the order of the model, while the ESS decreases. Moreover, the modified prior gives more efficient estimates, since the small circles in Fig. 4 show an improvement as in the RMSE as in the ESS.

The RMSE calculated with low precision data () is lower that the RMSE calculated with high precision data (), but it is due to the fact that the circles depicted in Fig. 4 are averages over all the parameters, including the parameter . Therefore, as illustrated above, in order to compare the outputs it is necessary to consider the different value of the parameters.

Furthermore, we note that for the different model orders high precision results appear to be more scattered, while low precision outcomes appear to be more concentrated. Since this behavior is associated to a higher ESS value, this suggest that the Markov chains explore more freely the parameter space and that they are characterized by a better mixing.

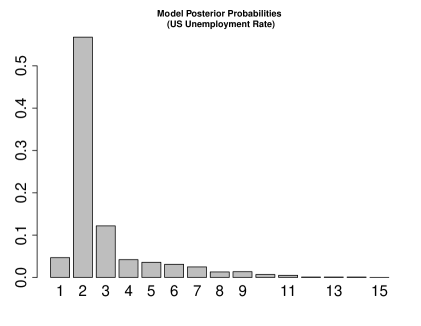

The aim of the second set of experiments is to study the relation between the size of the sample of observations and the model posterior probability. We consider a dataset of 500 observations simulated from a BAR(k) with and parameter values . Then in order to estimate both the parameters and the autoregressive order we assume a modified truncated-Gaussian prior with parameters , and apply the RJMCMC algorithm presented in the previous section to subsamples of different size (from 100 to 500 observations).

A typical output of a RJMCMC chain for a dataset of 300 observations is given in Fig. 5. Each chart shows the RJMCMC iterations for each subspace. The iterations of the chain for the precision parameter are given in the upper chart of Fig. 6. In the bottom chart of the same figure we show the model posterior probabilities.

| Estimated Model Probabilities | |||||

|---|---|---|---|---|---|

| 100 | 200 | 300 | 400 | 500 | |

| 1 | 0.06667 | 0.09143 | 0.10291 | 0.09806 | 0.00129 |

| 2 | 0.19208 | 0.38611 | 0.29345 | 0.19384 | 0.17828 |

| 3 | 0.18939 | 0.43252 | 0.35730 | 0.65473 | 0.75391 |

| 4 | 0.13245 | 0.03387 | 0.24522 | 0.05255 | 0.04449 |

| 5 | 0.10674 | 0.02291 | 0.00002 | 0.00011 | 0.00018 |

| 6 | 0.06682 | 0.01910 | 0.00001 | 0.00033 | 0.00013 |

| 7 | 0.05682 | 0.00691 | 0.00001 | 0.00001 | 0.00663 |

| 8 | 0.04682 | 0.00149 | 0.00001 | 0.00001 | 0.00012 |

| 9 | 0.04283 | 0.00139 | 0.00001 | 0.00001 | 0.00018 |

| 10 | 0.03891 | 0.00109 | 0.00042 | 0.00001 | 0.00001 |

| 11 | 0.01488 | 0.00080 | 0.00014 | 0.00001 | 0.00001 |

| 12 | 0.01455 | 0.00055 | 0.00022 | 0.00001 | 0.00001 |

| 13 | 0.01109 | 0.00062 | 0.00012 | 0.00001 | 0.00001 |

| 14 | 0.01078 | 0.00027 | 0.00011 | 0.00001 | 0.00001 |

| 15 | 0.00917 | 0.00092 | 0.00005 | 0.00030 | 0.00023 |

| Mode | 2 | 3 | 3 | 3 | 3 |

| Mean | 4.80121 | 2.65058 | 2.75522 | 2.66801 | 2.85226 |

| s.d. | 3.1253 | 1.2256 | 0.9854 | 0.76153 | 0.70101 |

The results of the model selection procedure for the different sample size are given in Tab. 3. All the estimates are based on 100,000 iterations of the RJMCMC chain. In the specific example at hand, the last three rows in the table show two interesting results. First the estimated model order is not correct ( with ) for a sample of 100 observations. Secondly the standard deviation is for and decreases for increasing , which means that the model posterior distribution is less concentrated around the mode for the samples of smaller size.

It should be noticed that, while small-sample bias in the model order estimates has also been observed in RJMCMC-based model selection procedures for other non-Gaussian autoregressive processes, such as the integer valued ARMA processes (see Enciso-Mora et al. (2009)), what we found new for the Beta autoregressive, is the high dispersion of the model order estimates in small samples.

Both of these results may contribute to explain the shape of the model posterior distribution that we will obtain in the applications to real dataset presented in Section 6.

6 Empirical Application

6.1 Unemployment Data

The dynamics of the unemployment rate is certainly one of the most studied in the economics time series analysis (see Bean (1994) and Nickel (1997) for an early review on unemployment models). Modeling and forecasting the unemployment rate still represent some of the most challenging issues in econometrics. See for example Neftci (1984), Montgomery et al. (1998) and Koop and Potter (1999) for some recent advances on nonlinear models. The unemployment rate is usually characterized by relatively brief periods of rapid economic contraction and by relatively long periods of slow expansion. In this work we do not model the asymmetric behavior of time series but focus instead on another fundamental feature of this variable, that is the unemployment rate is naturally defined on a bounded interval, let us say the interval. Data transformation is usually applied to have data on the real interval (see Wallis (1987)). Recently Rocha and Cribari-Neto (2009) suggested instead Beta autoregressive models for modeling the unemployment rate.

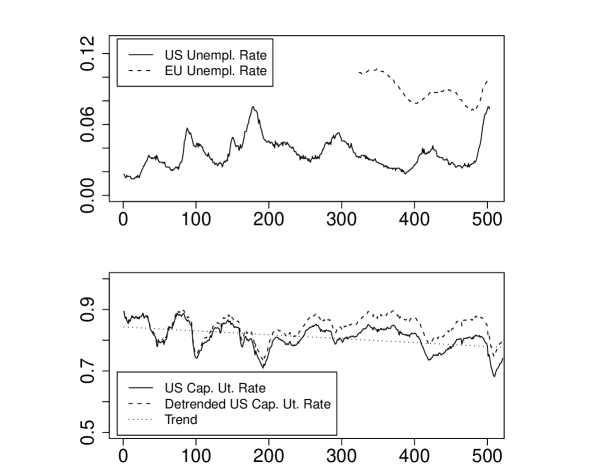

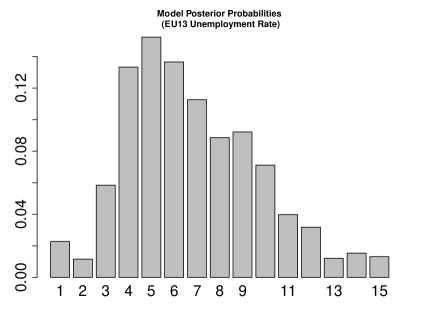

Here we consider two interesting dataset (see Fig. 7). The first one is the US unemployment rate (source: Datastream) sampled at a monthly frequency from February 1971 to December 2009. We are mainly interested in modeling the economic cycle and thus consider deseasonalized data. This dataset is quite large (467 observations) when compared to other macroeconomics dataset and is one of the most studied set of data in econometrics (see for example Nickel (1997)). The other dataset is the deseasonalized unemployment rate of the Euro Area sampled at the monthly frequency (source: Datastream), from January 1995 to December 2009. We will consider the aggregated unemployment rate for the 13 countries area. This is another well studied dataset (see Bean (1994) and inference on this dataset could be challenging due to the limited amount of observations (180 observations). Moreover modeling and forecasting of this variable represents one of the most important issues for the European Central Bank and for the European institute of official statistics (Eurostat).

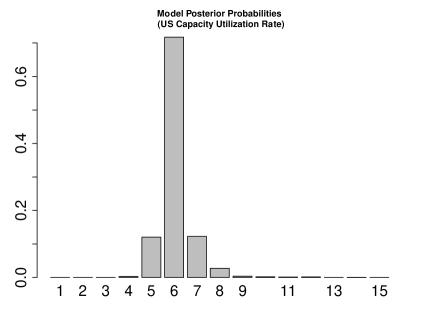

We assume modified Gaussian prior for the autoregressive parameters and a uniform prior for the autoregressive order. For the RJMCMC algorithm we consider iterations and a discard the first 10,000 samples in order to obtain an estimate of the parameters and of the model posterior. The estimation results are given in Tab. 4. Figures 8 show the model posterior probabilities for the two time series.

| US Unemployment Rate () | |||||||||

| ACC | |||||||||

| 0.011 | 0.547 | 0.272 | 130 | 0.392 | |||||

| 0.006 | 0.118 | 0.007 | 126 | ||||||

| 0.017 | 0.820 | 0.708 | 131 | ||||||

| EU Unemployment Rate () | |||||||||

| ACC | |||||||||

| 0.029 | 0.544 | 0.076 | 0.010 | 0.024 | 0.011 | 128 | 0.278 | ||

| 0.024 | 0.140 | 0.001 | 0.004 | 0.010 | 0.004 | 123 | |||

| 0.034 | 0.572 | 0.096 | 0.016 | 0.029 | 0.016 | 132 | |||

| US Capacity Utilization Rate () | |||||||||

| ACC | |||||||||

| 0.397 | 0.196 | 0.075 | 0.065 | 0.045 | 0.053 | 0.049 | 130 | 0.398 | |

| 0.390 | 0.189 | 0.058 | 0.058 | 0.040 | 0.049 | 0.030 | 126 | ||

| 0.408 | 0.207 | 0.079 | 0.074 | 0.067 | 0.060 | 0.051 | 130 | ||

6.2 Capacity Utilization

We consider the capacity utilization rate. While unemployment rate deals with utilization of the labor as a production factor, the capacity utilization deals with all production factors (i.e. labor force and stock of capital) of an economic system or sector. A detailed definition of capacity utilization and a discussion on the different ways to get a statistical measure of this quantity can be found in Klein and Su (1979).

The capacity utilization is a relevant quantity in both economic theory (see for example Burnside and Eichenbaum (1996) and Cooley et al. (1995)) and in time series macroeconometrics (see Klein and Su (1979)). In time series analysis both modelling and forecasting of this indicator are challenging issues which have a crucial role in the practice of economics analysis. In fact a decreasing capacity utilization is usually interpreted as slowdown of the aggregated demand and consequently a reduction of the inflation level. An increase of the capacity utilization reveals an expansion of the level of economic activity.

In this work we consider the capacity utilization rate series for the US sampled at a monthly frequency from January 1967 to May 2010. The series refers to all the industry sectors and is seasonally adjusted (source: Datastream).

From a graphical inspection (see the bottom chart of Fig. 8) we note that the series exhibits a negative trend. A deterministic trend could be naturally included in the Beta regression model with linear conditional mean by imposing some constraints on the slope and the intercept of the linear trend. These constraints can be imposed by a suitable specification of the prior distribution. However in this work we focus on the autoregressive components thus we follow a two steps procedure.

First we define a normalized linear trend , where is the sample size, and introduce the constrained linear regression model

| (32) |

with and . These parameter constraints insure that the residuals of the regression are in the interval. In the first step we calculate the de-trended capacity utilization rate . The results of the trend extraction are given in Fig. 7.

In the second step we estimate a Beta process on the variable . The results of the model selection procedure for the Beta process are in Tab. 4 and Fig. 8.

7 Conclusion

In this paper we consider Beta autoregressive models of order for time series data defined on a bounded interval. We focused on conditionally linear mean processes which are particularly suitable for forecasting purposes and allows for an easy interpretation of the parameters in the conditional mean of the process. We proposed a Bayesian procedure in order to estimate the parameters of the model. We showed that, in this context, the Bayesian approach is suitable for dealing with the constraints on the parameters space through a suitable specification of the prior distribution. We introduced three different informative priors and studied, through some simulation experiments, the effects of the prior choice on the inference procedure.

Moreover, we introduced an efficient RJMCMC algorithm for jointly estimating the parameters and selecting the model order. In different sets of simulation experiments, the proposed algorithm has been shown to be successful in estimating the true parameters for different parameter settings and different choices of the prior. We also found that the choice of the prior may have effects on the numerical mixing property of the RJMCMC chain by reducing the probability of the RJMCMC chain moves near the boundaries of the parameter space. In particular, within the three informative priors, the modified truncated Gaussian and the Beta-type priors could have positive effects on the mixing of the RJMCMC chain.

Through another set of simulation experiments we found that the proposed algorithm is able to find the correct order of the autoregressive model. The RJMCMC allowed us to study the effects of the sample size on the model posterior. In some cases we found evidence of bias and low efficiency of the estimators of the model posterior. Finally we also tested the performance of the Bayesian inference procedure and of the RJMCMC algorithm by providing two applications to real data. The first one considers the unemployment rates of United Stases and Euro Area and the second considers the US capacity utilization.

In this paper we focused on the Beta Autoregressive models with conditional linear mean, however the proposed RJMCMC algorithm can be extended to be applied to other type of Beta processes. In particular the authors are considering the inclusion in the inference process of the order of the moving average components and the extension to the Beta ARMA processes with nonlinear conditional mean. Both of the extensions can be considered with and without the inclusion of other explanatory variables.

Appendix A

When a new reciprocal root is proposed in the reversible jump MCMC procedure, the relationship between the autoregressive coefficients of the and of the is

| (33) |

Identification terms by terms gives the following recursion

| (34) | |||

| (35) |

with .

The constant term and the autoregressive coefficients belong to the standard simplex, that is

| (36) |

for each order of the Beta process. Thus if the parameters of the belong to the standard simplex, the following condition

| (37) |

and the positivity constraints for ,

| (38) |

are satisfied provided that

and for .

Appendix B

For the Gaussian prior we have

| (39) | |||||

| (40) |

For the modified Gaussian prior we have

| (41) | |||||

| (42) |

where , , and .

For the transformed Beta prior the -th element of is

| (43) |

and the -th element of , with , is

| (44) |

References

- Aitchinson [1986] J. Aitchinson. The Statistical Analysis of Compositional Data. Chapman & Hall, London, 1986.

- Albert and Chib [1993] J. H. Albert and S. Chib. Bayesian analysis of binary and polychotomous response data. Journal of American Statistical Association, 88:669–679, 1993.

- Amisano and Casarin [2007] G. Amisano and R. Casarin. Particle filters for Markov-switching Stochastic Correlation Models. In Proceedings of the Italian Statistical Society Conference, 2007 Intermediate Conference, Risk and Prediction, pages 305–316. CLEUP Padova, 2007.

- Bean [1994] C. Bean. European unemployment: A survey. Journal of Economic Literature, 32:573–619, 1994.

- Billio and Casarin [2010a] M. Billio and R. Casarin. Identifying Business Cycle Turning Points with Sequential Monte Carlo: An Online and Real-time Application to the Euro Area. Journal of Forecasting, 29:145–167, 2010a.

- Billio and Casarin [2010b] M. Billio and R. Casarin. Markov-switching Business Cycle Models with Beta Autoregressive Transition. Working paper, University of Brescia, 2010b.

- Brooks et al. [2003a] S. P. Brooks, P. Giudici, and A. Phililppe. Nonparametric convergence assessment for MCMC model selection. Journal of Computational and Graphical Statistics, 12:1–22, 2003a.

- Brooks et al. [2003b] S. P. Brooks, P. Giudici, and G. O. Roberts. Efficient construction of reversible jump Markov chain Monte Carlo proposal distributions. Journal of the Royal Statistical Society, B, 65:3–55, 2003b.

- Burnside and Eichenbaum [1996] C. Burnside and M. Eichenbaum. Factor Hoarding and the Propagation of Business Cycle Shocks. American Economic Review, 86:1154–1174, 1996.

- Calabrese [2010] R. Calabrese. Regression for Recovery Rates with both Continuous and Discrete Characteristics. In Proceedings of the Italian Statistical Society Conference, 2010, Padua. 2010.

- Chib and Greenberg [1995] S. Chib and E. Greenberg. Understanding the Metropolis-Hastings algorithm. The American Statistician, 49:327–335, 1995.

- Cooley et al. [1995] T. F. Cooley, G. D. Hansen, and E. C. Prescott. Equilibrium Business Cycles with Idle Resources and Variable Capacity Utilization. Economic Theory, 6:35–49, 1995.

- Ehlers and Brooks [2008] R. S. Ehlers and S. P. Brooks. Adpative Proposal Concstruction for Reversible Jump MCMC. Scandinavian Journal of Statistics, 35:677–690, 2008.

- Enciso-Mora et al. [2009] V. Enciso-Mora, P. Neal, and T. Subba Rao. Efficient order selection algorithms for integer-valued ARMA processes. Journal of Time Series Analysis, 30:1–18, 2009.

- Ferrari and Cribari-Neto [2004] S. L. P. Ferrari and F. Cribari-Neto. Beta regression for modelling rates and proportions. Journal of Applied Statistics, 31:799–815, 2004.

- Green [1995] P. J. Green. Reversible jump Markov chain Monte Carlo computation and bayesian model determination. Biometrika, 82:711–732, 1995.

- Grunwald et al. [1993] G. K. Grunwald, A. E. Raftery, and P. Guttorp. Time series of continuous proportions. Journal of the Royal Statistical Society, Series B, 55:103–116, 1993.

- Guihenneuc-Jouyaux et al. [1998] C. Guihenneuc-Jouyaux, K. Mengersen, and C. Robert. MCMC convergence diagnostics: A revieww. Papers 9816, Institut National de la Statistique et des Etudes Economiques, 1998.

- Gupta and Nadarajah [2004] A. K. Gupta and S. Nadarajah. Handbook of Beta Distribution and its Applications. Marcel Dekker, New York, 2004.

- Klein and Su [1979] L. R. Klein and V. Su. Direct estimates of unemployment rate and capacity utilization in macroeconmoetric models. International Economic Review, 20:725–740, 1979.

- Koop and Potter [1999] G. Koop and S. M. Potter. Dynamic Asymmetries in U.S. Unemployment. Journal of Business and Economic Statistics, 17:298–312, 1999.

- Kotz and van Dorp [2004] S. Kotz and J. R. van Dorp. Beyond Beta: Other Continuous Families of Distributions With Bounded Support and Applications. World Scientific, New Jersey, 2004.

- Lenk and DeSarbo [2000] P. J. Lenk and W. S. DeSarbo. Bayesian inference for Finite Mixtures of Generalized Linear Models with Random Effects. Psycometrika, 65:93–119, 2000.

- McKenzie [1985] E. McKenzie. An autoregressive process for beta random variables. Management Science, 31:988–997, 1985.

- Montgomery et al. [1998] A. L. Montgomery, V. Zarnowitz, R. S. Tasy, and G. C. Tiao. Forecasting the U.S. unemployment rate. Journal of the American Statistical Association, 93:478–493, 1998.

- Neftci [1984] S. N. Neftci. Are Economic Time Series Asymmetric Over the Business Cycles? Journal of Political Economy, 85:281–291, 1984.

- Nickel [1997] S. A. Nickel. Unemployment and labour market rigidieties: Europe versus North America. Journal of Economic Perspective, 11:55–74, 1997.

- Nieto-Barajas and Walker [2002] L. E. Nieto-Barajas and S. G. Walker. Markov Beta and Gamma Processes for Modelling Hazard Rates. Scandinavian Journal of Statistics, 29:413–424, 2002.

- Robert and Casella [2004] C. P. Robert and G. Casella. Monte Carlo Statistical Methods, 2nd Ed. Springer Verlag, New York, 2004.

- Robert and Rousseau [2002] C. P. Robert and J. Rousseau. A Mixture Approach To Bayesian Goodness of Fit. Technical Report 02009, CEREMADE, University Paris Dauphine, 2002.

- Rocha and Cribari-Neto [2009] V. A. Rocha and F. Cribari-Neto. Beta autoregressive moving averages models. Test, 18:529–545, 2009.

- Vermaak et al. [2004] J. Vermaak, C. Andrieu, A. Doucet, and S. J. Godsil. Reversible jump Markov chain Monte Carlo strategies for Bayesian model selection in autoregressive processes. Journal of Time Series Analysis, 25:785–809, 2004.

- Wallis [1987] F. K. Wallis. Time series analysis of bounded economic variables. Journal of Time Series Analysis, 8:115–123, 1987.