A probabilistic interpretation of the Macdonald polynomials

Abstract

The two-parameter Macdonald polynomials are a central object of algebraic combinatorics and representation theory. We give a Markov chain on partitions of with eigenfunctions the coefficients of the Macdonald polynomials when expanded in the power sum polynomials. The Markov chain has stationary distribution a new two-parameter family of measures on partitions, the inverse of the Macdonald weight (rescaled). The uniform distribution on permutations and the Ewens sampling formula are special cases. The Markov chain is a version of the auxiliary variables algorithm of statistical physics. Properties of the Macdonald polynomials allow a sharp analysis of the running time. In natural cases, a bounded number of steps suffice for arbitrarily large .

Keywords:

Macdonald polynomials, random permutations, measures on partitions, auxiliary variables, Markov chain, rates of convergence

AMS 2010 subject classifications:

05E05 primary; 60J10 secondary.

1 Introduction

The Macdonald polynomials are a widely studied family of symmetric polynomials in variables . Let denote the vector space of homogeneous symmetric polynomials of degree (with coefficients in ). The Macdonald inner product is determined by setting the inner product between power sum symmetric functions as

with

| (1.1) |

for a partition of with parts of size .

For each , as ranges over partitions of , the are an orthogonal basis for . Special values of give classical bases such as Schur functions (), Hall–Littlewood functions (), and the Jack symmetric functions (limit as with ). An enormous amount of combinatorics, group theory, and algebraic geometry is coded into these polynomials. A more careful description and literature review is in 2.

The original definition of Macdonald constructs as the eigenfunctions of a somewhat mysterious family of operators . This is used to develop their basic properties in [39]. A main result of the present paper is that the Macdonald polynomials can be understood through a natural Markov chain on the partitions of . For , this Markov chain has stationary distribution

| (1.2) |

Here is the Macdonald weight (1.1) and is a normalizing constant. The coefficients of the Macdonald polynomials expanded in the power sums give the eigenvectors of , and there is a simple formula for the eigenvalues.

Here is a brief description of . From a current partition , choose some parts to delete: call these . This leaves . The choice of given is made with probability

| (1.3) |

It is shown in 2.4 that for each , is a probability distribution with a simple-to-implement interpretation. Having chosen , choose a partition of size with probability

| (1.4) |

Adding to gives a final partition . These two steps define the Markov chain with stationary distribution . It will be shown to be a natural extension of basic algorithms of statistical physics: the Swendsen–Wang and auxiliary variables algorithms. Properties of the Macdonald polynomials give a sharp analysis of the running time for .

2 gives background on Macdonald polynomials (2.1), Markov chains (2.2), and auxiliary variables algorithms (2.3). The Markov chain is shown to be a special case of auxiliary variables and hence is reversible with as stationary distribution. 2.4 reviews some of the many different measures used on partitions, showing that and above have simple interpretations and efficient sampling algorithms. 2.4 also presents simulations of the measure using . This gives an understanding of ; it also illustrates (numerically) that a few steps of suffice for large while classical sampling algorithms (rejection sampling or Metropolis) become impractical.

The main theorems are in 3. The Markov chain is identified as one term of Macdonald operators . The coefficients of the Macdonald polynomials in the power sum basis (suitably scaled) are shown to be the eigenfunctions of with a simple formula for the eigenvalues. Needed values of the eigenvectors are derived. A heuristic overview of the argument is given (3.2), which may be read now for further motivation.

The main theorem is an extension of earlier work by Hanlon [31, 15] giving a similar interpretation of the coefficients of the family of Jack symmetric functions as eigenfunctions of a natural Markov chain: the Metropolis algorithm on the symmetric group for generating from the Ewens sampling formula. 4 develops the connection to the present study.

5 gives an analysis of the convergence of iterates of to the stationary distibution for natural values of and . Starting from , it is shown that a bounded number of steps suffice for arbitrary . Starting from , order steps are necessary and sufficient for convergence.

2 Background and examples

This section contains needed background on four topics: Macdonald polynomials, Markov chains, auxiliary variables algorithms, and measures on partitions and permutations. Each of these has a large literature. We give basic definitions, needed formulae, and pointers to literature. 2.3 shows that the Markov chain of the introduction is a special case of the auxiliary variables algorithm. 2.4 shows that the steps of the algorithm are easy to run, and has numerical examples.

2.1 Macdonald polynomials

Let be the algebra of symmetric polynomials in variables (coefficients in ). There are many useful bases of ; the monomial , power sum , elementary , homogeneous , and Schur functions are bases whose change of basis formulae contain a lot of basic combinatorics [50, Chap. 7], [39, Chap. I]. More esoteric bases such as the Hall–Littlewood functions , zonal polynomials , and Jack symmetric functions occur as the spherical functions of natural homogeneous spaces [39]. In all cases, as runs over partitions of , the associated polynomials form a basis of the vector space : homogeneous symmetric polynomials of degree .

Macdonald introduced a two-parameter family of bases which, specializing in various ways, gives essentially all the previous bases. The Macdonald polynomials can be succinctly characterized by using the inner product with from (1.1). This is positive definite [39, VI (4.7)] and there is a unique family of symmetric functions such that if and with [39, VI (4.7)]. The properties of are developed by studying as the eigenfunctions of a family of operators from to .

Define an operator on polynomials by . Define and by

| (2.1) |

where , is the Vandermonde determinant and for . For any ,

| (2.2) |

where the sum is over all -element subsets of and

| (2.3) |

Macdonald [39, VI (4.15)] shows that the Macdonald polynomials are eigenfunctions of :

| (2.4) |

This implies that the operators commute, and have the as eigenfunctions with eigenvalues the th elementary symmetric function in . We will use in our work below. The are self-adjoint in the Macdonald inner product . This will translate into having as stationary distribution.

The Macdonald polynomials may be expanded in the power sums [39, VI (8.19)],

| (2.5) |

with [39, VI (8.1)] where the product is over the boxes in the shape of , the arm length and the leg length of box . The are closely related to the two-parameter Kostka numbers via [39, VI (8.20)],

| (2.6) |

with the characters of the symmetric group for the th representation at the th conjugacy class. These have been a central object of study in algebraic combinatorics [5], [23], [26], [28, 27, 29], [30]. The main result of 3 shows that are the eigenfunctions of the Markov chain .

The Macdonald polynomials used here are associated to the root system . Macdonald [40] has defined analogous functions for the other root systems using similar operators. In a major step forward, Cherednik [13] gives an independent development in all types, using the double affine Hecke algebra. See [39, 41] for a comprehensive treatment. Using this language, Ram and Yip [48] give a “formula” for the Macdonald polynomials in general type. In general type the double affine Hecke is a powerful tool for understanding actions. We believe that our Markov chain can be developed in general type if a suitable analogue of the power sum basis is established.

2.2 Markov chains

Let be a finite set. A Markov chain on may be specified by a matrix . The interpretation being that is the chance of moving from to in one step. Then is the chance of moving from to in two steps, and is the chance of moving from to in steps. Under mild conditions, always met in our examples, there is a unique stationary distribution . This satisfies . Hence, the (row) vector is a left eigenvector of with eigenvalue 1. Probabilistically, picking from and taking one further step in the chain leads to the chance of being at .

All of the Markov chains used here are reversible, satisfying the detailed balance condition , for all in . Set to be with . Then acts as a contraction on by . Reversibility is equivalent to being self-adjoint. In this case, there is an orthogonal basis of (right) eigenfunctions and real eigenvalues with . For reversible chains, if is a left eigenvector, then is a right eigenvector with the same eigenvalue.

A basic theorem of Markov chain theory shows that . (Again, there are mild conditions, met in our examples.) The distance to stationarity can be measured in by the total variation distance:

| (2.7) |

Distance is measured in by the chi-squared distance:

| (2.8) |

where is the eigenvector , normalized to have -norm . The Cauchy–Schwarz inequality shows

| (2.9) |

Using these bounds calls for getting one’s hands on eigenvalues and eigenvectors. This can be hard work, but has been done in many cases. A central question is this: given , and a starting state , how large must be so that ?

Background on the quantitative study of rates of convergence of Markov chains is treated in the textbook of Brémaud [11]. The identities and inequalities that appear above are derived in the very useful treatment by Saloff-Coste [49]. He shows how tools of analysis can be brought to bear. The recent monograph of Levin, Peres and Wilmer [37] is readable by non-specialists and covers both analytic and probabilistic techniques.

2.3 Auxiliary variables

This is a method of constructing a reversible Markov chain with as stationary distribution. It was invented by Edwards and Sokal [20] as an abstraction of the remarkable Swendsen–Wang algorithm. The Swendsen–Wang algorithm was introduced as a superfast method for simulating from the Ising and Potts models of statistical mechanics. It is a block-spin procedure which changes large pieces of the current state. A good overview of such block spin algorithms is in [42]. The abstraction to auxiliary variables is itself equivalent to several other classes of widely used procedures, data augmentation and the hit-and-run algorithm. For these connections and much further literature, see [14].

To describe auxiliary variables, let be a probability distribution on a finite set Let be an auxiliary index set. For each , let be a probability distribution on (the chance of moving to ). These define a joint distribution and a marginal distribution . Let denote the conditional distribution. The final ingredient needed is a Markov matrix with as reversing measure ( for all ). This allows for defining

| (2.10) |

The Markov chain has the following interpretation: from , choose from and then from . The resulting kernel is reversible with respect to :

We now specialize things to , the space of partitions of . Take . The stationary distribution is as in (1.2):

| (2.11) |

From , the algorithm chooses some parts to delete, call these , leaving parts . Thus if and . We allow but demand . Clearly, and determine and determine . We let be the auxiliary variable. The choice of given is made with probability

| (2.12) | ||||

Thus, for . It is shown in 2.4 below that is a probability distribution with a simple interpretation. Having chosen with , the algorithm chooses with probability given in (1.4). Adding these parts to gives . More carefully,

| (2.13) |

Here it is assumed that is a part of both and ; the kernel is zero otherwise.

It is shown in 2.4 below that has a simple interpretation which is easy to sample from. The joint density is proportional to and to

| (2.14) |

The normalizing constant depends on but this is fixed in the following. We must now check reversibility of . For this, compute (up to a constant depending on ) as

This is symmetric in and so equals . This proves the following:

Proposition 2.1.

Example 1.

With , let

From the definitions, with rows and columns labeled (2), , the transition matrix is

| (2.15) |

In this example, it is straightforward to check that sums to , the rows of sum to , and that .

2.4 Measures on partitions and permutations

The measure of (1.2) has familiar specializations: to the distribution of conjugacy classes of a uniform permutation (), and the Ewens sampling measure (). After recalling these, the measures and used in the auxiliary variables algorithm are treated. Finally, there is a brief review of the many other, nonuniform distributions used on partitions and permutations . Along the way, many results on the “shape” of a typical partition drawn from appear.

2.4.1 Uniform permutations ()

If is chosen uniformly on , the chance that the cycle type of is is . There is a healthy literature on the structure of random permutations (number of fixed points, cycles of length , number of cycles, longest and shortest cycles, order, …). This is reviewed in [22, 46], which also contain extensions to the distribution of conjugacy classes of finite groups of Lie type.

One natural appearance of the measure comes from the coagulation/fragmentation process. This is a Markov chain on partitions of introduced by chemists and physicists to study clump sizes. Two parts are chosen with probability proportional to their size. If different parts are chosen, they are combined. If the same part is chosen twice, it is split uniformly into two parts. This Markov chain has stationary distribution . See [2] for a review of a surprisingly large literature and [17] for recent developments. These authors note that the coagulation/fragmentation process is the random transpositions walk, viewed on conjugacy classes. Using the Metropolis algorithm (as in 2.4.6 below) gives a similar process with stationary distribution .

Algorithmically, a fast way to pick with probability is by uniform stick-breaking: Pick uniformly. Pick uniformly. Continue until the first time that the uniform choice equals its maximum value. The partition with parts equals with probability .

2.4.2 Ewens and Jack measures

Set and let . Then converges to

| (2.16) |

In population genetics, setting , with a “fitness parameter,” this measure is called the Ewens sampling formula. It has myriad practical appearances through its connection with Kingman’s coalescent process, and has generated a large enumerative literature in the combinatorics and probability community [4, 32, 47]. It also makes numerous appearances in the statistics literature through its occurrence in non-parametric Bayesian statistics via Dirichlet random measures and the Dubins–Pitman Chinese restaurant process [24], [47, sec. 3.1].

Algorithmically, a fast way to pick with probability is by the Chinese restaurant construction. Picture a collection of circular tables. Person 1 sits at the first table. Successive people sit sequentially, by choosing to sit to the right of a (uniformly chosen) previously seated person (probability ) or at a new table (probability ). When people have been seated, this generates the cycles of a random permutation with probability . It would be nice to have a similar construction for the measures .

The Macdonald polynomials associated to this weight function are called the Jack symmetric functions [39, VI Sect. 1]. Hanlon [31, 15] uses properties of Jack polynomials to diagonalize a related Markov chain; see 4. When , the Jack polynomials become the zonal-spherical functions of . Here, an analysis closely related to the present paper is carried out for a natural Markov chain on perfect matchings and phylogenetic trees [12, Chap. X], [16].

2.4.3 The measure

Fix with parts and . Define, for ,

| (2.17) |

The auxiliary variables algorithm for sampling from involves sampling from , and setting (see (1.3) and (2.12)). The measure has the following interpretation, which leads to a useful sampling algorithm: Consider places divided into blocks of length :

Flip a coin for each place. Let, for ,

| (2.18) |

Thus . Let . So and

| (2.19) |

This makes it clear that summing over all non-empty subsets of gives 1.

The simple rejection algorithm for sampling from is: Flip coins as above. If , output . If , sample again. The chance of success is . Thus, unless is very close to 1, this is an efficient algorithm.

As tends to infinity, converges to point mass at . As tends to one, converges to the measure putting mass on .

2.4.4 The measure

Generating from the kernel of (2.13) with , requires generating a partition in from

This measure has the following interpretation: Pick with probability . This may be done by picking a random permutation in uniformly and reporting the cycle decomposition, or by the uniform stick-breaking of 2.4.1 above. For each part of , flip a coin times. If this comes up tails at least once, and this happens simultaneously for each , set . If some part of produces all heads, start again and choose with probability …. The chance of failure is , independent of . Thus, unless is close to 1, this gives a simple, useful algorithm.

The shape of a typical pick from is described in the following section. When tends to infinity, the measure converges to . When tends to one, the measure converges to point mass at the one part partition .

2.4.5 Multiplicative measures

For , define a probability on (equivalently, ) by

| (2.20) |

Such multiplicative measures are classical objects of study. They are considered in [4] and [52], where many useful cases are given. The measures fall into this class with . If and are two sequences of numbers and is a multiplicative basis of such as , setting gives . This is in rough analogy to the Schur measures defined in 2.4.7. For the choices , with positive numbers, the associated measures are positive. The power sums, with all , gives the Ewens measure with . Setting otherwise, gives the measure after normalization. To our knowledge, general multiplicative measures have not been previously studied. Multiplicative systems are studied in [39, VI Sect. 1 Ex.].

It is natural to try out the simple rejection algorithms of 2.4.3 and 2.4.4 for the measures . To begin, suppose that for all . The measure has the following interpretation: Pick with probability . As above, for each part of of size , generate a random variable taking values 1 or 0 with probability . If the values for all parts equal 1, set . If not, try again. For more general , divide all by , and generate from . This yields the measure on partitions.

Alas, this algorithm performs poorly for and in ranges of interest. For example, with for , when , the chance of success (empirically) is . We never succeeded in generating a partition for any .

The asymptotic distribution of the parts of a partition chosen from when is large can be studied by classical tools of combinatorial enumeration. For fixed values of , these problems fall squarely into the domain of the logarithmic combinatorial structures studied in [4]. A series of further results for more general have been developed by Jiang and Zhao [34]. The following brief survey of their results gives a good picture of typical partitions.

Of course, the theorems vary with the choice of . One convenient condition, which includes the measure for fixed , is

| (2.21) |

Theorem 2.2.

Suppose , satisfy (2.21). If is chosen from of (2.20), then, for large:

| For any , the distribution of converges to the distribution | |||

| (2.22) | of an independent Poisson vector with parameters . | ||

| The number of parts of has mean and variance asymptotic to | |||

| (2.23) | and, normalized by its mean and standard deviation, | ||

| a limiting standard normal distribution. | |||

| The length of the largest parts of converge to | |||

| (2.24) |

These and other results from [34, 4] show that the parts of a random partition are quite similar to the cycles of a unformly chosen random permutation, with the small cycles having slightly adjusted parameters. These results are used to give a lower bound on the mixing time of the auxiliary variables Markov chain in Proposition 3.10 below.

2.4.6 Simulation results

| Partition | Probability | Partition | Probability |

|---|---|---|---|

| 10 | 0.164003 | 4,4,2 | 0.018177 |

| 9,1 | 0.121365 | 4,4,1,1 | 0.010098 |

| 8,2 | 0.081762 | 4,3,3 | 0.016955 |

| 8,1,1 | 0.045423 | 4,3,2,1 | 0.030520 |

| 7,3 | 0.068948 | 4,3,1,1,1 | 0.005652 |

| 7,2,1 | 0.062054 | 4,2,2,2 | 0.004120 |

| 7,1,1,1 | 0.011491 | 4,2,2,1,1 | 0.006867 |

| 6,4 | 0.063387 | 4,2,1,1,1,1 | 0.001272 |

| 6,3,1 | 0.053214 | 4,1,1,1,1,1,1 | 0.000047 |

| 6,2,2 | 0.021552 | 3,3,3,1 | 0.004745 |

| 6,2,1,1 | 0.023946 | 3,3,2,2 | 0.005765 |

| 6,1,1,1,1 | 0.002217 | 3,3,2,1,1 | 0.006405 |

| 5,5 | 0.030873 | 3,3,1,1,1,1 | 0.000593 |

| 5,4,1 | 0.049942 | 3,2,2,2,1 | 0.003459 |

| 5,3,2 | 0.037734 | 3,2,2,1,1,1 | 0.001922 |

| 5,3,1,1 | 0.020963 | 3,2,1,1,1,1,1 | 0.000214 |

| 5,2,2,1 | 0.016980 | 3,1,1,1,1,1,1,1 | 0.000006 |

| 5,2,1,1,1 | 0.006289 | 2,2,2,2,2 | 0.000140 |

| 5,1,1,1,1,1 | 0.000349 | 2,2,2,2,1,1 | 0.000389 |

| 2,2,2,1,1,1,1 | 0.000144 | ||

| 2,2,1,1,1,1,1,1 | 0.000016 | ||

| 2,1,1,1,1,1,1,1,1 | 0.000001 | ||

| 1,1,1,1,1,1,1,1,1,1 | 0.000000 |

| Sample 100-step walk for Auxiliary Variables | |||

| 1. 10 | 26. 6,4 | 51. 6,2,1,1 | 76. 7,2,1 |

| 2. 4,3,3 | 27. 10 | 52. 10 | 77. 10 |

| 3. 6,3,1 | 28. 4,3,2,1 | 53. 7,3 | 78. 7,2,1 |

| 4. 5,5 | 29. 8,1,1 | 54. 8,2 | 79. 9,1 |

| 5. 9,1 | 30. 8,2 | 55. 6,2,2 | 80. 5,4,1 |

| 6. 8,1,1 | 31. 7,3 | 56. 6,4 | 81. 10 |

| 7. 6,2,2 | 32. 9,1 | 57. 4,2,211 | 82. 6,3,1 |

| 8. 9,1 | 33. 8,2 | 58. 5,3,2 | 83. 6,3,1 |

| 9. 4,4,2 | 34. 8,2 | 59. 6,4 | 84. 5,4,1 |

| 10. 4,4,1,1 | 35. 8,2 | 60. 10 | 85. 8,1,1 |

| 11. 4,3,1,1,1 | 36. 10 | 61. 9,1 | 86. 5,3,2 |

| 12. 7,2,1 | 37. 7,1,1,1 | 62. 6,3,1 | 87. 5,3,1,1 |

| 13. 5,3,1,1 | 38. 10 | 63. 4,3,3 | 88. 5,2,2,1 |

| 14. 6,4 | 39. 5,3,2 | 64. 10 | 89. 10 |

| 15. 10 | 40. 4,3,3 | 65. 5,5 | 90. 5,3,2 |

| 16. 5,3,2 | 41. 8,2 | 66. 8,2 | 91. 8,2 |

| 17. 4,3,3 | 42. 7,3 | 67. 5,4,1 | 92. 5,3,2 |

| 18. 9,1 | 43. 6,3,1 | 68. 3,3,2,1,1 | 93. 6,3,1 |

| 19. 7,3 | 44. 10 | 69. 6,4 | 94. 5,4,1 |

| 20. 7,3 | 45. 5,5 | 70. 6,1,1,1,1 | 95. 4,3,2,1 |

| 21. 5,3,2 | 46. 6,3,1 | 71. 4,3,2,1 | 96. 7,3 |

| 22. 5,3,1,1 | 47. 8,1,1 | 72. 5,4,1 | 97. 7,2,1 |

| 23. 5,3,1,1 | 48. 6,1,1,1,1 | 73. 10 | 98. 7,2,1 |

| 24. 6,3,1 | 49. 10 | 74. 5,2,1,1,1 | 99. 5,2,2,1 |

| 25. 5,3,2 | 50. 9,1 | 75. 5,2,2,1 | 100. 4,2,2,1,1 |

The distribution can be far from uniform. An example, with , is shown in 1; . The auxiliary variables algorithm for the measure has been programmed by Jiang and Zhao [34]. It seems to work well over a wide range of and . A tiny example, 100 steps when , is shown in 2. A comparison of the simulations with the exact distribution (easily computed from (1.2) when ) shows perfect agreement. In our experiments, the choice of and does not seriously affect the running time, and simulations seem possible for up to .

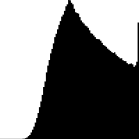

The distribution of the largest part, for and , , and , based on steps of the algorithm, is shown in 1. Comparison with the limiting results of Theorem 2.2 above seems good. The blip at the right side of the figures comes from ; the rest of the distribution follows the limit (2.24) approximately.

We have compared the auxiliary variables algorithm with the rejection algorithm of 2.4.5 and the Metropolis algorithm. As reported in 2.4.5, rejection fails completely for . The Metropolis algorithm we used works by simulating permutations from lifted to . From the current permutation , propose by making a random transposition (all choices equally likely). If , move to . If , flip a coin with probability and move to if the coin comes up heads; else stay at . For small values of , Metropolis is competitive with auxiliary variables. Jiang and Zhao have computed the mixing time for by a clever sampling algorithm. For , the following table shows the number of steps required to have total variation distance less than starting from the partition . Also shown is , the number of partitions of , to give a feeling for the size of the state space.

| 10 | 20 | 30 | 40 | 50 | |

|---|---|---|---|---|---|

| Aux | 1 | 1 | 1 | 1 | 1 |

| Met | 8 | 17 | 26 | 37 | 53 |

| 42 | 627 | 5604 | 37338 | 204,226 |

The theorems of 3 show that auxiliary variables requires a bounded number of steps for arbitrary . In the computations above, the distance to stationarity after one step of the auxiliary variables is 0.093 (within a 1% error in the last decimal) for . For larger (e.g., ), the Metropolis algorithm seemed to need a very large number of steps to move at all. This is consistent with other instances of auxiliary variables, such as the Swendsen–Wang algorithm for the Ising and Potts model (away from the critical temperature; see [9]).

2.4.7 Other measures on partitions

This portmanteau section gives pointers to some of the many other measures that have been studied on . Often these studies are fascinating, deep, and extensive. All measures studied here seem distinct from .

A remarkable two-parameter family of measures on partitions has been introduced by Jim Pitman. For , and with parts, set

where

These measures specialize to , and the Ewens measure ( fixed, , see [47, sec. 3.2]. They arise in a host of probability problems connected to stable stochastic problems of index . They are also being used in applied probability connected to genetics and Bayesian statistics. They satisfy elegant consistency properties as varies. For example, deleting a random part gives the corresponding measure on . For these and many other developments, see the book-length treatments of [7], [47, sec. 3.2].

One widely studied measure on partitions is the Plancherel measure,

with the dimension of the irreducible representation of associated to shape . This measure was perhaps first studied in connection with Ulam’s problem on the distribution of the length of the longest increasing sequence in a random permutation; see [38, 51]. For extensive developments and references, see [35, 1].

The Schur measures of [43, 44, 45, 10] are generalizations of the Plancherel measure. Here the chance of is taken as proportional to , with the Schur function and collections of real-valued entries. Specializing and in various ways yields a variety of previously studied measures. One key property, if the partition is “tilted 135∘” to make a v-shape and the local maxima projected onto the -axis, the resulting points form a determinantal point process with a tractable kernel. This gives a fascinating collection of shape theorems for the original partition.

One final distribution, the uniform distribution on , has also been extensively studied. For example, a uniformly chosen partition has order parts of size 1, the largest part is of size , the number of parts is of size . A survey with much more refined results is in [21].

The above only scratches the surface. The reader is encouraged to look at [43, 44, 45] to see the breadth and depth of the subject as applied to Gromov–Witten theory, algebraic geometry, and physics. The measures there seem closely connected to the “Plancherel dual” of our . This dual puts mass proportional to on , with the arm-leg length products defined in 3.1 below.

3 Main results

This section shows that the auxiliary variables Markov chain with stationary distribution , is explicitly diagonalizable with eigenfunctions essentially the coefficients of the Macdonald polynomials expanded in the power sum basis. The result is stated in 3.1. The proof, given in 3.3, is somewhat computational. An explanatory overview is in 3.2. In 5, these eigenvalue/eigenvector results are used to bound rates of convergence of .

3.1 Statement of main results

Fix and . Let be the auxiliary variables Markov chain on . Here, and are defined in (2.12), (2.13), and studied in 2.4.3 and 2.4.4. For a partition , let

| (3.1) |

where the product is over the boxes in the shape , and is the arm length and the leg length of box [39, VI (8.1)].

Theorem 3.1.

The Markov chain is reversible and ergodic with stationary distribution defined in (1.2). This distribution is properly normalized.

The eigenvalues of are given by

Thus, .

The corresponding right eigenfunctions are

with the coefficients occurring in the following expansion of the Macdonald polynomials in terms of the power sums [39, VI (8.19)]:

| (3.2) |

The are orthogonal in with

Example 2.

When , from (2.15), the matrix with rows and columns indexed by 2, , is

Macdonald [39, p. 359] gives tables of for . For , is . The character matrix is , and the product is . From Theorem 3.1(3), the rows of this matrix, multiplied coordinate-wise by , give the right eigenvectors:

Then is a constant function, and satisfies , with .

3.2 Overview of the argument

Macdonald [39, VI] defines the Macdonald polynomials as the eigenfunctions of the operator from (2.2). As described in 2.1 above, is self-adjoint for the Macdonald inner product and sends into itself [39, VI (4.15)]. For ,

| (3.4) |

The Markov chain is related to an affine rescaling of the operator , which [39, VI (4.1)] calls . We work directly with to give direct access to Macdonald’s formulae. The affine rescaling is carried out at the end of 3.3 below.

The integral form of Macdonald polynomials [39, VI Sect. 8] is

for defined in (3.1). Of course, the are also eigenfunctions of . The may be expressed in terms of the shifted power sums via [39, VI (8.19)]:

| (3.5) |

This is our equation (3.2) above. In Proposition 3.10 below, we compute the action of on the power sum basis: for with parts,

| (3.6) | ||||

On the right, the coefficient of is essentially the Markov chain ; we use for this unnormalized version. Indeed, we first computed (3.6) and then recognized the operator as a special case of the auxiliary variables operator.

Equations (3.4)–(3.6) show that simply scaled versions of are eigenvectors of the matrix as follows. From (3.4), (3.5),

| (3.7) | ||||

| (3.8) |

Equating coefficients of on both sides of (3.7), (3.8), gives

| (3.9) |

This shows that is a left eigenfunction for with eigenvalue . It follows from reversibility that is a right eigenfunction for . Since , simple manipulations give the formulae of part (3) of Theorem 3.1.

3.3 Proof of Theorem 3.1

As in 2.1 above, let . Let . The main result identifies , operating on the power sums, as an affine transformation of the auxiliary variables Markov chain. The following Proposition is the first step, providing the expansion of acting on power sums. A related computation is in [6, App. B Prop. 2].

Proposition 3.2.

If is homogeneous, then

If is a partition then

| (3.10) |

Proof of Proposition 3.10.

If is homogeneous then

| (3.11) |

By definition,

| (3.12) |

Letting for ,

and it follows that

| (3.13) |

if is homogeneous. Thus,

Hence,

| (3.14) |

Let us show that the measure is properly normalized and compute the normalization of the eigenvectors.

Proof of Lemma 3.3.

We next show that an affine renormalization of the discrete version (3.5) of the Macdonald operator equals the auxiliary variables Markov chain of 2.3. Along with Macdonald [39, VI (4.1)], define

operating on . From (3.3), the eigenvalues of are . Noting that , the operator is a normalization of with top eigenvalue . From Proposition 3.10(b), for a partition with parts,

Using as a surrogate for as in 3.2, the coefficient of is exactly of 2.3.

This completes the proof of Theorem 3.1.∎

Example 3.

When , from the definitions

Thus, on partitions of 2, the matrix of is

This is the matrix of (2.15) derived there from the probabilistic description.

4 Jack polynomials and Hanlon’s walk

The Jack polynomials are a one-parameter family of bases for the symmetric polynomials, orthogonal for the weight . They are an important precursor to the full two-parameter Macdonald polynomial theory, containing several classical bases: the limits , suitably interpreted, give the bases; gives Schur functions; gives zonal polynomials for ; gives zonal polynomials for where is the quaternions (see [39, VII]). A good deal of the combinatorial theory for Macdonald polynomials was first developed in the Jack case. Further, the Jack theory has been developed in more detail [31, 50, 36] and [39, VI Sect. 10].

Hanlon [31] managed to interpret the differential operators defining the Jack polynomials as the transition matrix of a Markov chain on partitions with stationary distribution , described in 2.4.2 above. In later work [15], this Markov chain was recognized as the Metropolis algorithm for generating from the proposal of random transpositions. This gives one of the few cases where this important algorithm can be fully diagonalized. See [33] for a different perspective.

Our original aim was to extend Hanlon’s findings, adding a second “sufficient statistic” to , and discovering a Metropolis-type Markov chain with the Macdonald coefficients as eigenfunctions. It did not work out this way. The auxiliary variables Markov chain makes more vigorous moves than transpositions, and there is no Metropolis step. Nevertheless, as shown below, Hanlon’s chain follows from interpreting a limiting case of , one of Macdonald’s operators. We believe that all of the operators should have interesting interpretations. In this section, we derive Hanlon’s chain from the Macdonald operator perspective.

Overview

There are several closely related operators used to develop the Jack theory. Macdonald [39, VI Sect. 3 Ex. 3] uses and , defined by

| (4.1) |

where , is the Vandermonde determinant, and for . He shows [39, VI Sect. 3 Ex. 3c] that

| (4.2) |

so that the Jack operators are a limiting case of Macdonald polynomials.

Macdonald [39, VI Sect. 4 Ex. 2b] shows that the Jack polynomials are eigenfunctions of with eigenvalues . Stanley [50, Pf. of Th. 3.1] and Hanlon [31, (3.5)] use defined as follows. Let

| (4.3) | |||

| (4.4) |

Hanlon computes the action of on the power sums in the form (see (4.7))

| (4.5) |

where is the number of variables and is a partition of .

The matrix can be interpreted as the transition matrix of the following Markov chain on the symmetric group . For , set # cycles. If the chain is currently at , pick a transposition uniformly; set . If , move to . If , move to with probability ; else stay at . This Markov chain has transition matrix

where for of cycle type . Hanlon notes that this chain only depends on the conjugacy class of , and the induced process on conjugacy classes is still a Markov chain for which the transition matrix is the matrix of of (4.5).

The Jack polynomial theory now gives the eigenvalues of the Markov chain , and shows that the corresponding eigenvectors are the coefficients when the Jack polynomials are expanded in the power sum basis. The formulae available for Jack polynomials then allow for a careful analysis of rates of convergence to stationarity; see [15].

We may see this from the present perspective as follows.

Proposition 4.1.

Let be the coefficient of in (see [39, VI Sect. 3 Ex. 3d]). If is a homogeneous polynomial in of degree , then

| (4.6) |

where

From [50, Pf. of Th. 3.1],

| (4.7) |

Remark.

From part (a), up to affine rescaling, is the Stanley–Hanlon operator. From part (b), this operates on the power sums in precisely the way that the Metropolis algorithm operates. Indeed, multiplying a permutation by a transposition changes the number of cycles by one; the change takes place by fusing two cycles (the first term in (4.7)) or by breaking one of the cycles in into parts (the second term in (4.7)). The final term constitutes the “holding” probability from the Metropolis algorithm.

Proof of Proposition 4.7.

is the cofficient of in , so

is the coefficient of in , so

is the coefficient of in , so

| (4.8) |

Since for all , and for ,

so that the coefficient of in (4.8) is

The coefficient of in equation (4.8) is

since, for each ,

Since , then, for fixed ,

so that the coefficient of in (4.8) is

Since ,

Since

then

Hence

The formula for now follows. ∎

5 Rates of convergence

This section uses the eigenvectors and eigenvalues derived above to give rates of convergence for the auxiliary variables Markov chain. 5.1 states the main results: starting from the partition a bounded number of steps suffice for convergence, independent of . 5.2 contains an overview of the argument and needed lemmas. 5.3 gives the proof of Theorem 5.1, and 5.4 develops the analysis starting from , showing that steps are needed.

5.1 Statement of main results

Fix and . Let be the partitions of the stationary distribution defined in (1.2), and the auxiliary variables Markov chain defined in Proposition 2.1. The total variation distance used below is defined in (2.7).

Theorem 5.1.

Consider the auxiliary variables Markov chain on partitions of . Then, for all

| (5.1) |

For example, if , , and the bound becomes . Thus, when the total variation distance is at most .05 in this example.

5.2 Outline of proof and basic lemmas

Let be the eigenfunctions and eigenvalues of given in Theorem 3.1. From 2.2, for any starting state ,

| (5.2) |

with right eigenfunctions normalized to have norm one. At the end of this subsection we prove the following:

| (5.3) | |||

| (5.4) | |||

| (5.5) | |||

| (5.6) |

Using these results, consider the sum on the right side of (5.2), for with largest part less than . Using monotonicity, (5.5), and the bound (5.3),

| (5.7) |

By taking gives the second term on the right hand side of (5.1).

Using monotonicity again,

| (5.8) |

The argument proceeds by looking carefully at and showing

| (5.9) |

for a constant . In (5.9) and throughout this section, denotes a positive constant which depends only on and , but not on . Its value may change from line to line. Using (5.3) on shows . Using this and (5.6) in (5.8) gives an upper bound

| (5.10) |

This completes the outline for starting state .

This section concludes by proving the preliminary results announced above.

Lemma 5.2.

For any , the normalized eigenfunctions satisfy

Proof.

The are orthonormal in . Fix and let be the measure concentrated at . Expand the function in this basis: . Using the Plancherel identity, . Here, the left side equals and . So the right side is the needed sum of squares. ∎

The asymptotics in (5.4) follow from the following lemma.

Lemma 5.3.

For , the sequence

is increasing and bounded by .

Proof.

The equalities follow from the definitions of , and . Since , the sequence is increasing. The bound follows from

Remark.

The function is an analytic function of for , thoroughly studied in the classical theory of partitions [3, Sect. 2.2].

For the next lemma, recall the usual dominance partial order on if for all [39, I.1]. This amounts to “moving up boxes” in the diagram for . Thus is largest, smallest. When , , but (3,3) and (4,1,1) are not comparable. The following result shows that the eigenvalues are monotone in this order. A similar monotonicity holds for the random transpositions chain [19], the Ewens sampling chain [15], and the Hecke algebra deformation chain [18].

Lemma 5.4.

For , the eigenvalues

are monotone in .

Proof.

Consider first a partition , with , where moving one box from row to row is allowed. It must be shown that . Equivalently,

Since and , this always holds. ∎

5.3 Proof of Theorem 5.1

Lemma 5.5.

For , with and ,

Proof.

![[Uncaptioned image]](/html/1007.4779/assets/x3.png)

Let with and . Let be the boxes in the first row of , and let be the shaded boxes in the figure above.

For a box in , let be the row number and the column number of . Then

where is the length of the th column of . Next,

Thus,

Since and , then , so that implies

Similarly, since and , then , so that implies

Similarly, and imply

So

Thus,

5.4 Bounds starting at

We have not worked as seriously at bounding the chain starting from the partition . The following results show that steps are required, and offer evidence for the conjecture that steps suffice (where the distance to stationarity tends to zero with , so there is a sharp cutoff at ).

The or chi-square distance on the right hand side of (5.2) has first term .

Lemma 5.6.

For fixed , as tends to infinity,

Proof.

Corollary 5.7.

There is a constant such that, for all ,

Proof.

The corollary shows that if . Thus, more than steps are required to drive the chi-square distance to zero. In many examples, the asymptotics of the lead term in the bound (5.2) sharply controls the behavior of total variation and chi-square convergence. We conjecture this is the case here, and that there is a sharp cut-off at .

It is easy to give a total variation lower bound:

Proposition 5.8.

For the auxiliary variables chain , after steps with , for large and ,

Proof.

Consider the Markov chain starting from . At each stage, the algorithm chooses some parts of the current partition to discard, with probability given by (1.3). From the detailed description given in 2.4.3, the chance of a specific singleton being eliminated is . Of course, in the replacement stage (1.4) this (and more singletons) may reappear. Let be the first time that all of the original singletons have been removed at least once; this depends on the history of the entire Markov chain. Then is distributed as the maximum of independent geometric random variables with (here is the first time that the th singleton is removed).

Let . From the definition

and

From the limiting results in 2.4.5, under has an approximate Poisson distribution. Thus, . The result follows. ∎

Acknowledgments

We thank John Jiang and James Zhao for their extensive help in understanding the measures . We thank Alexei Borodin for telling us about multiplicative measures and Martha Yip for help and company in working out exercises from [39] over the past several years. We thank Cindy Kirby for her expert help.

References

- Aldous and Diaconis [1999] Aldous, D. and Diaconis, P. (1999). Longest increasing subsequences: From patience sorting to the Baik–Deift–Johansson theorem. Bull. Amer. Math. Soc. (N.S.), 36 413–432.

- Aldous [1999] Aldous, D. J. (1999). Deterministic and stochastic models for coalescence (aggregation and coagulation): A review of the mean-field theory for probabilists. Bernoulli, 5 3–48. URL http://dx.doi.org/10.2307/3318611.

- Andrews [1998] Andrews, G. E. (1998). The Theory of Partitions. Cambridge Mathematical Library, Cambridge University Press, Cambridge. Reprint of the 1976 original.

- Arratia et al. [2003] Arratia, R., Barbour, A. D. and Tavaré, S. (2003). Logarithmic Combinatorial Structures: A Probabilistic Approach. EMS Monographs in Mathematics, European Mathematical Society (EMS), Zürich. URL http://dx.doi.org/10.4171/000.

- Assaf [2007] Assaf, S. H. (2007). Dual equivalence graphs, ribbon tableaux and Macdonald polynomials. Ph.D. thesis, University of California, Berkeley, Department of Mathematics.

- Awata et al. [1996] Awata, H., Kubo, H., Odake, S. and Shiraishi, J. (1996). Quantum algebras and Macdonald polynomials. Commun. Math. Phys., 179 401–415.

- Bertoin [2006] Bertoin, J. (2006). Random Fragmentation and Coagulation Processes, vol. 102 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge. URL http://dx.doi.org/10.1017/CBO9780511617768.

- Billingsley [1972] Billingsley, P. (1972). On the distribution of large prime divisors. Period. Math. Hungar., 2 283–289. Collection of articles dedicated to the memory of Alfréd Rényi, I.

- Borgs et al. [1999] Borgs, C., Chayes, J. T., Frieze, A., Kim, J. H., Tetali, P., Vigoda, E. and Vu, V. H. (1999). Torpid mixing of some Monte Carlo Markov chain algorithms in statistical physics. In 40th Annual Symposium on Foundations of Computer Science (New York, 1999). IEEE Computer Soc., Los Alamitos, CA, 218–229. URL http://dx.doi.org/10.1109/SFFCS.1999.814594.

- Borodin et al. [2000] Borodin, A., Okounkov, A. and Olshanski, G. (2000). Asymptotics of Plancherel measures for symmetric groups. J. Amer. Math. Soc., 13 481–515 (electronic). URL http://dx.doi.org/10.1090/S0894-0347-00-00337-4.

- Brémaud [1999] Brémaud, P. (1999). Markov Chains, vol. 31 of Texts in Applied Mathematics. Springer-Verlag, New York. Gibbs fields, Monte Carlo simulation, and queues.

- Ceccherini-Silberstein et al. [2008] Ceccherini-Silberstein, T., Scarabotti, F. and Tolli, F. (2008). Harmonic Analysis on Finite Groups, vol. 108 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge. Representation theory, Gelfand pairs and Markov chains.

- Cherednik [1992] Cherednik, I. (1992). Double affine Hecke algebras, Knizhnik–Zamolodchikov equations, and Macdonald’s operators. Int. Math. Res. Notices, 1992 171–180. http://imrn.oxfordjournals.org/cgi/reprint/1992/9/171.pdf, URL http://imrn.oxfordjournals.org.

- Diaconis and Anderson [2007] Diaconis, P. and Anderson, H. C. (2007). Hit and run as a unifying device. J. Soc. Francaise Statist., 148 5–28.

- Diaconis and Hanlon [1992] Diaconis, P. and Hanlon, P. (1992). Eigen-analysis for some examples of the Metropolis algorithm. In Hypergeometric Functions on Domains of Positivity, Jack Polynomials, and Applications (Tampa, FL, 1991), vol. 138 of Contemp. Math. Amer. Math. Soc., Providence, RI, 99–117.

- Diaconis and Holmes [2002] Diaconis, P. and Holmes, S. P. (2002). Random walks on trees and matchings. Electron. J. Probab., 7 no. 6, 17 pp. (electronic).

- Diaconis et al. [2004] Diaconis, P., Mayer-Wolf, E., Zeitouni, O. and Zerner, M. P. W. (2004). The Poisson–Dirichlet law is the unique invariant distribution for uniform split-merge transformations. Ann. Probab., 32 915–938.

- Diaconis and Ram [2000] Diaconis, P. and Ram, A. (2000). Analysis of systematic scan Metropolis algorithms using Iwahori–Hecke algebra techniques. Michigan Math. J., 48 157–190. Dedicated to William Fulton on the occasion of his 60th birthday.

- Diaconis and Shahshahani [1981] Diaconis, P. and Shahshahani, M. (1981). Generating a random permutation with random transpositions. Z. Wahrsch. Verw. Gebiete, 57 159–179.

- Edwards and Sokal [1988] Edwards, R. G. and Sokal, A. D. (1988). Generalization of the Fortuin–Kasteleyn–Swendsen–Wang representation and Monte Carlo algorithm. Phys. Rev. D, 38 2009–2012.

- Fristedt [1993] Fristedt, B. (1993). The structure of random partitions of large integers. Trans. Amer. Math. Soc., 337 703–735. URL http://dx.doi.org/10.2307/2154239.

- Fulman [2002] Fulman, J. (2002). Random matrix theory over finite fields. Bull. Amer. Math. Soc. (N.S.), 39 51–85. URL http://dx.doi.org/10.1090/S0273-0979-01-00920-X.

- Garsia and Remmel [2005] Garsia, A. and Remmel, J. B. (2005). Breakthroughs in the theory of Macdonald polynomials. Proc. Natl. Acad. Sci. USA, 102 3891–3894 (electronic). URL http://dx.doi.org/10.1073/pnas.0409705102.

- Ghosh and Ramamoorthi [2003] Ghosh, J. K. and Ramamoorthi, R. V. (2003). Bayesian Nonparametrics. Springer Series in Statistics, Springer-Verlag, New York.

- Goncharov [1944] Goncharov, V. (1944). Du domaine d’analyse combinatoire. Bull. Acad. Sci. URSS Ser. Math, 8 3–48. Amer. Math. Soc. Transl. 19 (1950).

- Gordon [2003] Gordon, I. (2003). On the quotient ring by diagonal invariants. Invent. Math., 153 503–518. URL http://dx.doi.org/10.1007/s00222-003-0296-5.

- Haglund et al. [2005a] Haglund, J., Haiman, M. and Loehr, N. (2005a). A combinatorial formula for Macdonald polynomials. J. Amer. Math. Soc., 18 735–761 (electronic). URL http://dx.doi.org/10.1090/S0894-0347-05-00485-6.

- Haglund et al. [2005b] Haglund, J., Haiman, M. and Loehr, N. (2005b). Combinatorial theory of Macdonald polynomials. I. Proof of Haglund’s formula. Proc. Natl. Acad. Sci. USA, 102 2690–2696 (electronic). URL http://dx.doi.org/10.1073/pnas.0408497102.

- Haglund et al. [2008] Haglund, J., Haiman, M. and Loehr, N. (2008). A combinatorial formula for nonsymmetric Macdonald polynomials. Amer. J. Math., 130 359–383. URL http://dx.doi.org/10.1353/ajm.2008.0015.

- Haiman [2006] Haiman, M. (2006). Cherednik algebras, Macdonald polynomials and combinatorics. In International Congress of Mathematicians. Vol. III. Eur. Math. Soc., Zürich, 843–872.

- Hanlon [1992] Hanlon, P. (1992). A Markov chain on the symmetric group and Jack symmetric functions. Discrete Math., 99 123–140. URL http://dx.doi.org/10.1016/0012-365X(92)90370-U.

- Hoppe [1987] Hoppe, F. M. (1987). The sampling theory of neutral alleles and an urn model in population genetics. J. Math. Biol., 25 123–159.

- Hora and Obata [2007] Hora, A. and Obata, N. (2007). Quantum Probability and Spectral Analysis of Graphs. Theoretical and Mathematical Physics, Springer, Berlin. With a foreword by Luigi Accardi.

- Jiang and Zhao [2010] Jiang, J. and Zhao, J. T. (2010). Multiplicative measures on partitions, asymptotic theory. Preprint, Department of Mathematics, Stanford University.

- Kerov [2003] Kerov, S. V. (2003). Asymptotic Representation Theory of the Symmetric Group and its Applications in Analysis, vol. 219 of Translations of Mathematical Monographs. American Mathematical Society, Providence, RI. Translated from the Russian manuscript by N. V. Tsilevich, With a foreword by A. Vershik and comments by G. Olshanski.

- Knop and Sahi [1997] Knop, F. and Sahi, S. (1997). A recursion and a combinatorial formula for Jack polynomials. Invent. Math., 128 9–22. URL http://dx.doi.org/10.1007/s002220050134.

- Levin et al. [2009] Levin, D. A., Peres, Y. and Wilmer, E. L. (2009). Markov Chains and Mixing Times. American Mathematical Society, Providence, RI. With a chapter by James G. Propp and David B. Wilson.

- Logan and Shepp [1977] Logan, B. F. and Shepp, L. A. (1977). A variational problem for random Young tableaux. Advan. Math., 26 206–222.

- Macdonald [1995] Macdonald, I. G. (1995). Symmetric Functions and Hall Polynomials. 2nd ed. Oxford Mathematical Monographs, The Clarendon Press Oxford University Press, New York. With contributions by A. Zelevinsky, Oxford Science Publications.

- Macdonald [2000/01] Macdonald, I. G. (2000/01). Orthogonal polynomials associated with root systems. Sém. Lothar. Combin., 45 Art. B45a, 40 pp. (electronic). URL arXiv:math.QA/0011046.

- Macdonald [2003] Macdonald, I. G. (2003). Affine Hecke algebras and orthogonal polynomials, vol. 157 of Cambridge Tracts in Mathematics. Cambridge University Press, Cambridge. URL http://dx.doi.org/10.1017/CBO9780511542824.

- Newman and Barkema [1999] Newman, M. E. J. and Barkema, G. T. (1999). Monte Carlo Methods in Statistical Physics. The Clarendon Press Oxford University Press, New York.

- Okounkov [1999] Okounkov, A. (1999). Infinite wedge and random partitions. ArXiv Mathematics e-prints. arXiv:math/9907127.

- Okounkov [2003a] Okounkov, A. (2003a). Symmetric functions and random partitions. ArXiv Mathematics e-prints. arXiv:math/0309074.

- Okounkov [2003b] Okounkov, A. (2003b). The uses of random partitions. ArXiv Mathematical Physics e-prints. arXiv:math-ph/0309015.

- Olshanski [2010] Olshanski, G. (2010). Random permutations and related topics. In The Oxford Handbook on Random Matrix Theory (G. Akermann, J. Baik and P. Di Francesco, eds.). Oxford University Press. To appear.

- Pitman [2006] Pitman, J. (2006). Combinatorial Stochastic Processes, vol. 1875 of Lecture Notes in Mathematics. Springer-Verlag, Berlin. Lectures from the 32nd Summer School on Probability Theory held in Saint-Flour, July 7–24, 2002, With a foreword by Jean Picard.

- Ram and Yip [2008] Ram, A. and Yip, M. (2008). A combinatorial formula for Macdonald polynomials. To appear Advan. Math. ArXiv e-prints 0803.1146, URL http://dx.doi.org/10.1016/j.aim.2010.06.022.

- Saloff-Coste [1997] Saloff-Coste, L. (1997). Lectures on finite Markov chains. In Lectures on Probability Theory and Statistics (Saint-Flour, 1996), vol. 1665 of Lecture Notes in Math. Springer, Berlin, 301–413.

- Stanley [1989] Stanley, R. P. (1989). Some combinatorial properties of Jack symmetric functions. Advan. Math., 77 76–115. URL http://dx.doi.org/10.1016/0001-8708(89)90015-7.

- Veršik and Kerov [1977] Veršik, A. M. and Kerov, S. V. (1977). Asymptotic behavior of the Plancherel measure of the symmetric group and the limit form of Young tableaux. Dokl. Akad. Nauk SSSR, 233 1024–1027.

- Yakubovich [2009] Yakubovich, Y. (2009). Ergodicity of multiplicative statistics. ArXiv e-prints. 0901.4655.