22institutetext: Centre for Atom Optics and Ultrafast Spectroscopy, Swinburne University of Technology, Hawthorn, VIC 3122, Australia

A note on the theory of fast money flow dynamics

Abstract

The gauge theory of arbitrage was introduced by Ilinski in ilinski1997physics and applied to fast money flows in ilinskaia1999reconcile ; ilinski2001physics . The theory of fast money flow dynamics attempts to model the evolution of currency exchange rates and stock prices on short, e.g. intra-day, time scales. It has been used to explain some of the heuristic trading rules, known as technical analysis, that are used by professional traders in the equity and foreign exchange markets. A critique of some of the underlying assumptions of the gauge theory of arbitrage was presented by Sornette in sornette1998gauge . In this paper, we present a critique of the theory of fast money flow dynamics, which was not examined by Sornette. We demonstrate that the choice of the input parameters used in ilinski2001physics results in sinusoidal oscillations of the exchange rate, in conflict with the results presented in ilinski2001physics . We also find that the dynamics predicted by the theory are generally unstable in most realistic situations, with the exchange rate tending to zero or infinity exponentially.

pacs:

11.15.HaLattice gauge theory and 11.10.EfLagrangian and Hamiltonian approach and 89.65.-sSocial and economic systems and 89.65.GhEconomics; econophysics, financial markets, business and management and 89.75.-kComplex systems1 Introduction

Fast money flows are analyzed in ilinskaia1999reconcile ; ilinski2001physics in terms of the lattice gauge theory of arbitrage developed in ilinski1997physics . The main idea of the theory is that the dynamics should only depend on gauge invariant quantities rather than the exchange rates themselves. Changing the units in which stocks of currency are denominated obviously changes the nominal exchange rate. However, it is obvious that such changes of scale, i.e. gauge transformations, should have no effect on its dynamics. Some assumptions of the theory have been criticized in sornette1998gauge ; for example, the lack of justification for the exponential form of the weight of a given market configuration. However, the results of the theory reported in ilinskaia1999reconcile ; ilinski2001physics seem impressive, reproducing in particular some of the phenomenological rules of technical trading employed by professional traders. Hence the theory appears to be a promising tool for analyzing the markets.

In this note, we present our analysis of the theory of fast money flow dynamics and re-examine the results presented in ilinskaia1999reconcile ; ilinski2001physics . In Sect. 2, we present the derivation of the dynamical equations of the theory. In Sect. 3, we examine the dynamics predicted by the theory for various initial conditions. We highlight certain inconsistencies in the theory, the unstable dynamics for most realistic values of the parameters and initial conditions, and the resulting problems in applying the theory to technical trading. In Sect. 4, we revisit the action and demonstrate that the expression used in ilinskaia1999reconcile ; ilinski2001physics is inconsistent with the evolution operator resulting from the lattice formulation.

2 Lattice gauge theory and fast money flow dynamics

In analogy with quantum electrodynamics, Ilinski identified the exchange rate between two currencies with the field and the trading agents with matter. In general, the exchange rate dynamics depends on the interest rates of the underlying currencies. However, since we are interested in intra-day dynamics only, we consider the special case of zero interest rates. Ilinski tacitly assumed that the interest rates of the two currencies are identical, i.e . In this paper we set and assume that transaction costs are zero.

The part of the action that describes the dynamics of the field on its own is formulated by identifying arbitrage on the lattice with the curvature, which gives

| (1) |

In Eq. (1), is the investment horizon and is the volatility (presumed to be constant in the interval ). This expression is equivalent to a Gaussian random walk in .

The effect of the field on “matter”, i.e. the trading agents, is described by the Hamiltonian

| (2) |

where and are creation and annihilation operators for agents in currency (), and the coefficients and depend on . According to Ilinski, and , where and are constants (we discuss the motivation behind these formulas in Sect. 4). Following the standard treatment of a quantum harmonic oscillator (see, e.g. slavnov1980gauge ), Ilinski ilinski2001physics derived a path-integral expression for the evolution operator in terms of the coherent states and , which are the eigenstates of the annihilation operators and respectively. From the evolution operator one can obtain the expression for the part of the action that represents the field’s effect on matter:

| (3) |

where the overbar denotes complex conjugation.

Finally, departing from the electrodynamics analogy, Ilinski introduced Farmer’s term to describe the effect of matter on the field. As a result, the action is replaced by

| (4) |

where

| (5) |

is the total number of agents, and is a constant (ilinski2001physics uses in place of ).

The total action is given by

| (6) |

Following Ilinski, we introduce new variables and , and replace complex-valued with and , defined by () and . Ilinski identifies with the number of agents in currency ; the total number of agents is conserved. The action can be written as

| (7) |

where the Lagrangian is given by

| (8) |

with , , , . A prime denotes a derivative with respect to . Due to the unique structure of the Lagrangian (8), the resulting Euler-Lagrange equations can be simplified to the following first order differential equations:

| (9) | ||||

| (10) | ||||

| (11) | ||||

However, some of the second-order nature of the Euler-Lagrange equations is retained in the constant , whose value depends explicitly on the derivatives and . The equation for is trivial and we omit it. To solve Eqs. (9–11), one needs to specify the initial conditions , , , and , which uniquely determine (note that is given by Eq. (11)). Alternatively, one can set , , , and , which uniquely determine .

3 Analysis of the Euler-Lagrange equations

3.1 Missing coefficient

By introducing new variables, and , and linearizing (, ), we obtain and

| (12) |

For , the general solution is

| (13) | |||

| (14) |

with ( and are found from the initial conditions). This is inconsistent with the solutions presented in ilinskaia1999reconcile ; ilinski2001physics , which exhibit oscillations decaying slowly with time. The origin of this inconsistency can be traced to a simple algebraic mistake in the derivation of the equations of motion given in ilinskaia1999reconcile ; ilinski2001physics . On page 168 of ilinski2001physics , the second term on the right-hand side of the equation for is missing a factor . The same coefficient is also missing in the equations given in ilinskaia1999reconcile . This is essentially equivalent to replacing in our Eq. (10) with unity, while keeping in our Eq. (9) intact.

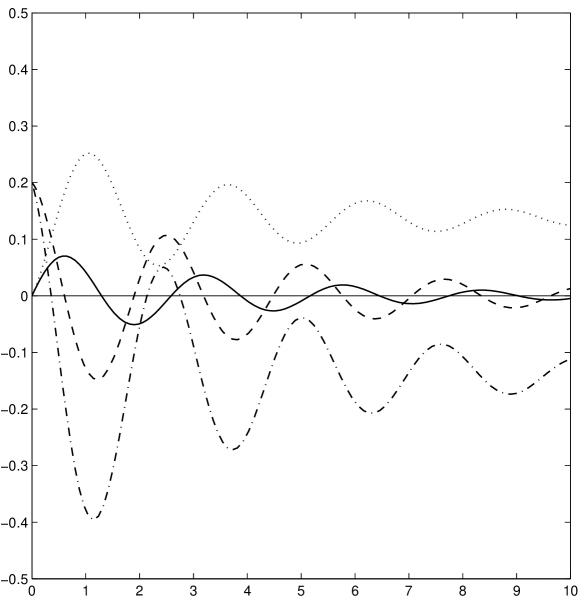

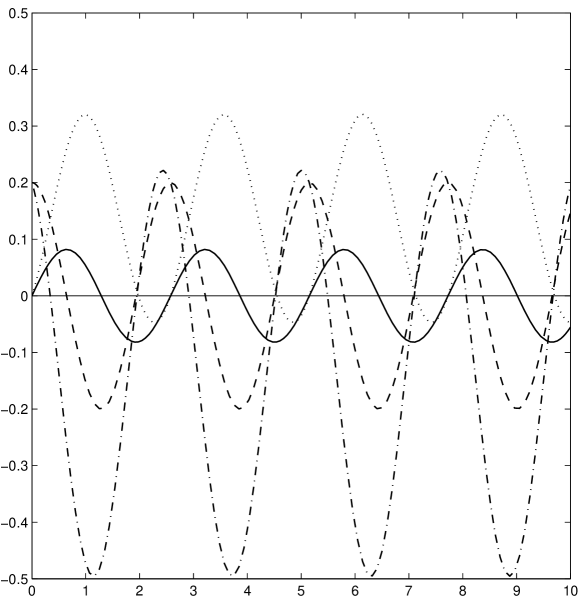

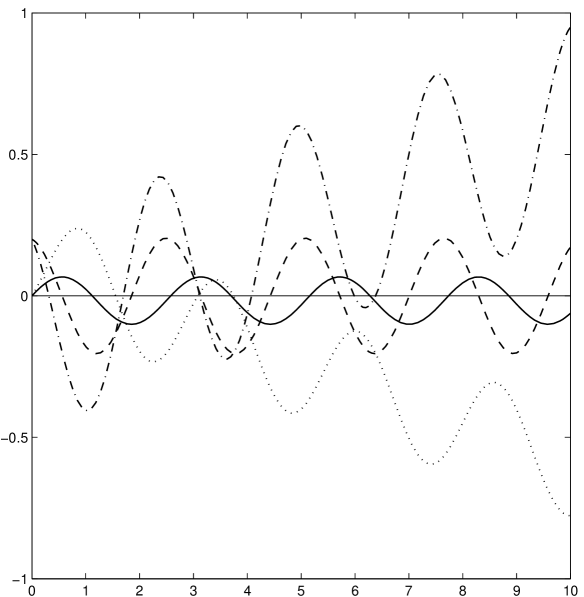

We verify the above by numerically solving Eqs. (9–11) in their incorrect form (with missing from one of the equations as in ilinskaia1999reconcile ; ilinski2001physics ) and in their correct form derived in this paper. We are able to perfectly reproduce111In the caption of figure 7.2 in ilinski2001physics , it is claimed that one of the quantities displayed is ( in Ilinski’s notation), but actually is plotted. the plots presented on page 169 of ilinski2001physics by solving the incorrect equations (see Fig. 1). Note that we have and for the parameters used in ilinski2001physics . Ilinski claimed to set ( in his notation), but this is obviously incorrect; the solutions he presented are obtained for , which gives . As anticipated by the linearized analysis, the correct nonlinear equations of motion do not show any decay in the oscillation amplitude (see Fig. 2).

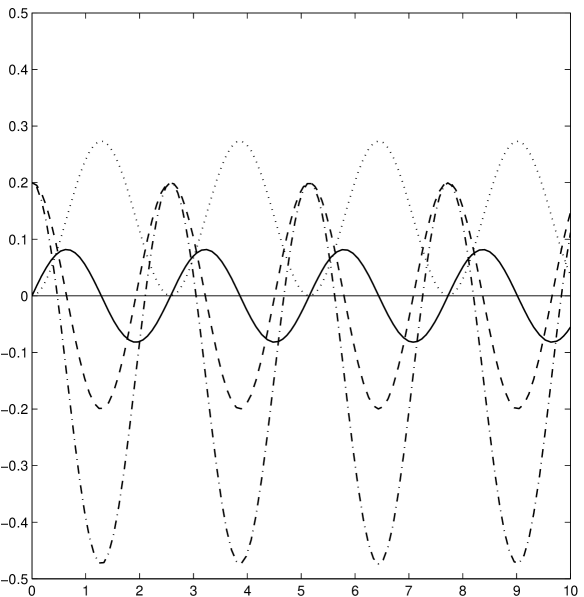

Furthermore, we do not observe any enhancement of oscillations for smaller values of , as Farmer’s term becomes less important. In fact, the solutions for plotted in Fig. 3 are only slightly different from those for (cf. the plots given on page 171 of ilinski2001physics ). After some exploration, we conclude that Farmer’s term does not have any critical effect on the dynamics of the system; it only affects the amplitude of oscillations of and , and their phase shift from .

3.2 Unstable solutions

In Sect. 3.1, we explored the dynamics of in the case . However, there is no a priori reason why the initial conditions should conspire to give . In this section, we briefly examine the dynamics of in the more general case .

Linearizing Eqs. (9) and (10) gives

| (15) | |||

| (16) |

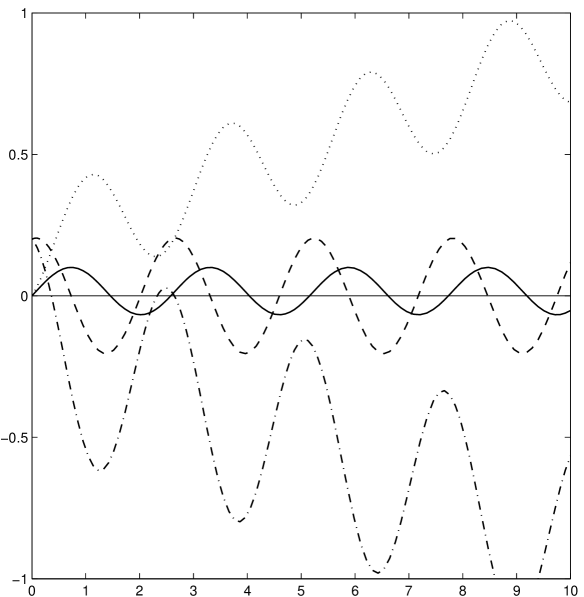

We find that the solutions for and are also harmonic oscillations plus an extra term linear in time. The average value of changes linearly with time at a rate , while the average of changes at the same rate but with the opposite sign. This behaviour is illustrated in Figs. 4 and 5 (note that and remain small, so the linearization assumption is not broken). Thus, for , the exchange rate decays exponentially to zero, whereas for , it grows exponentially. In both cases the exponential time-scale is given by .

3.3 Technical trading

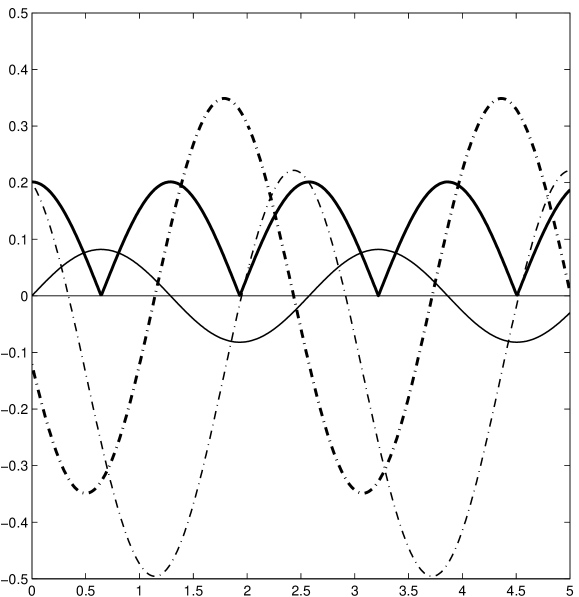

Ilinski justified certain rules employed in technical trading (see ilinskaia1999reconcile and pages 170–173 of ilinski2001physics ), e.g., the use of positive and negative volume indices (PVI and NVI respectively), by appealing to the solutions of the equations of motion. The relevant figures are presented in ilinski2001physics on pages 170 (figure 7.3) and 172 (figure 7.7). We identify the trading volume with and the return with . In ilinski2001physics , the derivative of is used incorrectly instead of to compute the return (see also footnote 1). For comparison, we plot the volume and the return curves in Fig. 6, computed using the correct equations of motion and . The quantities plotted in figure 7.7 of ilinski2001physics are not specified, nor are the parameters and initial conditions, so we do not comment on that figure’s validity.

Ilinski used the trading volume and the return curves to construct continuous222In technical trading, these quantities are discrete and defined by recursive formulas. versions of PVI and NVI. The details of the construction are left unspecified. However, the PVI and NVI are usually computed from daily returns, not from continuous intra-day variables. In any event, the resulting construction must depend strongly on the time-scale that is chosen, since the indices are defined recursively. Examining figure 7.7 in ilinski2001physics , one observes that, for instance, the continuous PVI is constant if the trading volume is decreasing with time and changes linearly if is increasing, with a slope of where the return curve is positive and where is negative. However, this simple trend is inconsistent with the recursive definitions of the PVI and NVI employed in technical trading.

Moreover, the constant-amplitude solutions we employed in this section only exist for . In all other cases, the exchange rate converges to zero or diverges to infinity exponentially on a short time scale. The condition requires precise alignment between the initial values , , , and . There is no reason to expect that such a precise alignment will be observed at any time in the real market. Therefore, the lattice gauge model predicts unrealistic behaviour (e.g., exponential divergence if ) of the exchange rate under most circumstances. Given the issues raised in this section, it is premature to conclude that the technical trading schemes employed by market participants can be justified by the lattice gauge model.

4 Revisiting the action

We conclude by re-examining the derivation of the action given by Eq. 6. Consider two currencies, referred to as currency 1 and currency 2, linked by an exchange rate that depends on time , such that the amount of currency 2 at time corresponds to the amount of currency 1. We assume that the currencies can only be exchanged at the discrete times () and define . At any given time , an agent can decide to either exchange his stock of currency for the counterpart currency or keep his position, in which case his stock of currency remains unchanged (recall that we neglect interest rates completely since we are interested in the intra-day dynamics). We display these possibilities in Fig. 7, showing part of the lattice from time to time .

The returns on arbitrage along the closed loops of the elementary plaquette shown in Fig. 7 are given by for the clockwise loop and for the counter-clockwise loop. The total return is identified in ilinski1997physics with the curvature on the lattice and, therefore, the corresponding discrete action is given by

| (17) |

Assuming that for any we have in the limit , we obtain the continuous action given by (1). No justification is given in ilinski1997physics ; ilinski2001physics for why the limit of must be finite. The expression for Farmer’s term was derived in ilinski2001physics , but we omit it because its inclusion has no critical effect on the dynamics (see Sect. 3.1).

In order to derive the Hamiltonian given by Eq. (2) and the expressions for the coefficients and , Ilinski considered the case of a single trader first and then generalized to multiple traders by using creation and annihilation operators. In the case of a single trader, Ilinski postulated that the probability of a given path through the lattice from to is exponentially weighted with respect to , where are the parallel transport coefficients on the lattice (note that for most paths). Thus, for a given path , the probability is given by

| (18) |

Depending on the path, a given can be , , or unity (note that Ilinski introduces a new gauge, under which the exchange rates remain unchanged, except at and where they equal unity; see pages 131–132 of ilinski2001physics for more details). The state of the trader is characterized by the probabilities and of being in currency 1 and currency 2 respectively. The evolution of the state vector can be described by the transition matrix

| (19) |

which Ilinski essentially identifies333 In the case of non-zero interest rates, is related to by a simple matrix transform (see page 132 of ilinski2001physics ); however, if and the transaction costs are zero. with the discrete version of the continuous evolution operator that satisfies

| (20) |

where is the Hamiltonian and is the identity matrix. Ilinski claim that the expression for the transition matrix (19) and the formula (20) result in

| (21) |

Finally, identifying the parameter with , we obtain the expressions for and , the Hamiltonian given by (2), and the action .

In deriving the action Ilinski considered a more general case of non-zero interest rates, but this does not nullify the two issues pointed out below. Firstly, we note that the Hamiltonian given by (21) becomes infinite in the limit . It is stated in ilinski2001physics that in the continuous-time calculations “stands for the smallest time-scale of the theory, the time cut-off” (see page 133). However, if is retained in the finite form in the Hamiltonian and, therefore, the action , it must also appear in the finite form in the expression for the action for consistency. Secondly, we observe that the transition matrix is degenerate; its determinant is zero. Therefore, it cannot possibly be identified with the evolution operator. We conclude that the justification provided for the Hamiltonian (2) in ilinski2001physics is insufficient.

5 Conclusions

We have examined the theory of fast money flow dynamics developed in ilinskaia1999reconcile ; ilinski2001physics and uncovered errors in 1) the derivation and the analysis of the equations of motion based on the theory, and 2) the justification of the action based on the lattice gauge formalism.

The equations of motion presented in ilinskaia1999reconcile ; ilinski2001physics are missing the coefficient in one term, crucially modifying the dynamics of the system. We also find that most of the solutions of the equations of motion, in their correct form derived in this paper, are unstable with respect to the initial conditions, resulting in unrealistic behaviour of the exchange rate. We show that the justification of the technical trading given in ilinski2001physics is based on an erroneous interpretation of the variables related to the exchange rate and on the stability predicted by the incorrect equations of motion.

The theory of fast money flows relies on a particular form of the Hamiltonian that describes the effect of the exchange rate on the actions of the agents. We demonstrate that this form is not consistent with the lattice gauge formulation and diverges in the continuum limit.

Acknowledgement

AS thanks the Portland House Foundation for their generous financial support.

References

- (1) K. Ilinski, Arxiv preprint hep-th/9710148 (1997)

- (2) A. Ilinskaia, K. Ilinski, Arxiv preprint cond-mat/9902044 (1999)

- (3) K. Ilinski, Physics of finance: gauge modelling in non-equilibrium pricing (Wiley, 2001)

- (4) D. Sornette, International Journal of Modern Physics C 9(3), 505 (1998)

- (5) A. Slavnov, L. Faddeev, Gauge Fields, Introduction to Quantum Theory (Frontiers in Physics, Vol. 50) (1980)