Good-deal bounds in a regime-switching diffusion market

Abstract

We consider option pricing in a regime-switching diffusion market. As the market is incomplete, there is no unique price for a derivative. We apply the good-deal pricing bounds idea to obtain ranges for the price of a derivative. As an illustration, we calculate the good-deal pricing bounds for a European call option and we also examine the stability of these bounds when we change the generator of the Markov chain which drives the regime-switching. We find that the pricing bounds depend strongly on the choice of the generator.

1 Introduction

Regime-switching market models are a way of capturing discrete shifts in market behavior. These shifts could be due to a variety of reasons, such as changes in market regulations, government policies or investor sentiment. First introduced by Hamilton (1989), regime-switching models have been shown in various empirical studies to be better at capturing market behavior than their non-regime-switching counterparts (for example, see Ang and Bakaert (2002), Gray (1996) and Klaassen (2002)).

An example of regime-switching market is one in which there are only two regimes: a bear market regime and a bull market regime. Suppose the market starts in a bull market regime, in which prices are generally rising. It stays in this regime for a random length of time before switching to a bear market regime, in which prices are generally falling. It then stays in the bear market for another random length of time before switching back to the bull market. This cycle continues ad infinitum.

Due to the regime-switching, the market is incomplete and hence there is no unique risk-neutral martingale measure to use for pricing derivatives. In fact, there are infinitely many possible risk-neutral martingale measures. This means that not only is there no unique price for derivatives, but the range of prices which can be obtained from all the possible risk-neutral martingale measures are too wide to be useful in practice.

As prices of derivatives are not unique in incomplete markets, various suggestions have been made either on how to choose a single price or on how to obtain a more restricted, and therefore potentially more useful, range of prices. We focus in this paper on the latter because it is the market which ultimately decides which risk-neutral martingale measure is used for pricing a derivative and so we should take into account our uncertainty about what the market price will be. Therefore, we believe it is better to find a range of prices that the market-determined price might reasonably be expected to lie in, rather than determining a single price.

The idea that we build upon is that of the good-deal bound. This idea is due to Cochrane and Saá Requejo (2000) and is based on the Sharpe Ratio, which is the excess return on an investment per unit of risk. Their idea is to bound the Sharpe Ratios of all possible assets in the market and thus exclude Sharpe Ratios which are considered to be too large. The bound is called a good-deal bound. The method of applying the bound gives a set of risk-neutral martingale measures which can be used to price options. This results in an upper and lower good-deal bound on the prices of an option. The idea was streamlined and extended to models with jumps in Björk and Slinko (2006), and it is their approach that we follow in this paper.

The uncertainty measured by the size of the good-deal bounds reflects the uncertainty within the market model concerning the price of the derivative. It does not measure uncertainty concerning the choice of the model, by which we mean both the model structure - in this case a regime-switching model - and the model parameters. Indeed, as we see concretely in a numerical example, changing the model parameters changes a derivative’s pricing bounds for a fixed good-deal bound. Thus the model choice is still a very important factor in determining the derivative’s good-deal pricing bounds. In summary, the good-deal pricing bounds tell us nothing about model uncertainty itself, only about the uncertainty in the choice of a risk-neutral martingale measure within a particular model.

Cochrane and Saá Requejo (2000) outline various ways that the good-deal pricing bounds can be used, such as a trader using the bounds as buy and sell points and a bank using them as bid and ask prices for non-traded assets. The good-deal pricing bounds enable us to avoid unreasonable prices and also to examine the price sensitivity to changes in the market price of risk.

In Bayraktar and Young (2008), Sharpe Ratios are also used to price options in incomplete markets. However, the perspective is that of an individual seller of one option, rather than that of the entire market. The seller of an option decides the option price via his own risk preferences, as expressed by his own chosen Sharpe Ratio. In other words, the seller of the option chooses the risk-neutral martingale measure under which he prices the option. It is shown in Bayraktar and Young (2008) that the upper and lower good-deal bounds of Cochrane and Saá Requejo (2000) can be obtained; in that case, the seller’s chosen risk-neutral martingale measure coincides with the martingale measure which gives the upper good-deal bound. The lower good-deal bound is obtained in Bayraktar and Young (2008) by considering the buyer of the option.

A utility-based approach to the good-deal bound idea is found in C̆erný (2003), and extended in Klöppel and Schweizer (2007). An alternative approach based on the gain-loss ratio, which is the expectation of an asset’s positive excess payoffs divided by the expectation of its negative excess payoffs, is found in Bernardo and Ledoit (2000).

The aim of this paper is to apply the good-deal bound idea to the pricing of derivatives in a regime-switching diffusion market. The paper is structured as follows. Section 2 details the regime-switching market model. In Section 3 we identify the set of equivalent martingale measures. In Section 4 the Sharpe Ratio of an arbitrary asset in the market is defined and we state the extended Hansen-Jagannathan bound. The definitions of the upper and lower good-deal bounds on the price of a derivative are in Section 5. The stochastic control approach that we use to find them is detailed in Section 6. The minimal martingale measure, which we consider to be a benchmark pricing measure, is given in Section 7. A numerical example illustrating the upper and lower good-deal bounds of a European call option of various maturities is in Section 8. We also examine the stability of the good-deal bounds when we change the market model’s parameters. Finally, we conclude in Section 9 with some remarks.

2 Market model

We consider a regime-switching diffusion market model in which there is one risk-free asset traded asset and a finite number of traded assets. An example of a risk-free asset is a bank account and typical examples of risky assets are equities, bonds or a pooled fund. The full mathematical description of the market is given below.

2.1 Description of the market model

We consider a continuous-time financial market model on a complete probability space where all investment takes place over a finite time horizon , for a fixed . The probability space carries both a Markov chain and an -dimensional standard Brownian motion , where we use to denote the transpose of .

The information available to the investors in the market at time is the history of the Markov chain and Brownian motion up to and including time . Mathematically, this is represented by the filtration

| (2.1) |

where denotes the collection of all -null events in the probability space . We assume that .

Remark 2.1.

As a mathematical consequence of being defined on the same filtered probability space , the Markov chain and the Brownian motion are independent processes. Relating these processes to economic reality, we might think of the Brownian motion as modeling short-term, micro-economic changes in the market, whereas the Markov chain models long-term macro-economic changes. With this interpretation, the implicit assumption in our model that these economic changes are independent is a reasonable approximation to reality. For practical implementation, this means that the number and specification of the market regimes should be chosen to reflect this interpretation.

Remark 2.2.

In our model, an investor knows what regime the market is in at each time . In reality, the market regime is unlikely to be known with certainty, although it could be estimated from market data. This is an important point to note, since the prices of assets in the market are dependent on the initial market regime.

The market is subject to regime-switching, as modelled by the continuous-time Markov chain which takes values in a finite state space , for some integer . For example, suppose we wish to model a market in which there are only two regimes: a bull market regime and a bear market regime. We set and we might identify as corresponding to the market being in the bull market regime at time . We would then identify as corresponding to the market being in the bear market regime at time .

We assume that the Markov chain starts in a fixed state , so that , a.s. The Markov chain has a generator , which is a matrix with the properties , for all and . The interpretation of the off-diagonal element of the generator matrix is as the instantaneous rate of transition from state to state . To avoid states where there are no transitions into or out of, we assume that for each state .

Associated with each pair of distinct states in the state space of the Markov chain is a point process, or counting process,

| (2.2) |

where denotes the zero-one indicator function. The process counts the number of jumps that the Markov chain has made from state to state up to time . Define the intensity process

| (2.3) |

If we compensate by , then the resulting process

| (2.4) |

is a martingale (see Rogers and Williams (2006, Lemma IV.21.12)). We refer to the set of martingales as the -martingales of . They are mutually orthogonal, purely discontinuous, square-integrable martingales which are null at the origin.

We consider a financial market that is built upon a finite number of traded assets, which we call risky assets, and a risk-free asset. The risk-free rate of return in the market is denoted by the scalar stochastic process and the risk-free asset’s price process is governed by

| (2.5) |

The mean rate of return of the th risky asset is denoted by the scalar stochastic process and the volatility process of the th risky asset is denoted by the -dimensional stochastic process . The price process of the th risky asset is then given by

| (2.6) |

with the initial value being a fixed, strictly positive constant in .

3 Martingale measures

3.1 Equivalent martingale measure

From the fundamental theorem of arbitrage-free pricing, it is known that existence of an equivalent martingale measure (“EMM”) is equivalent to absence of arbitrage in the market. Furthermore, the market is complete (in the sense that all claims can be replicated) if and only if the EMM is unique. In our financial market model, while there is no arbitrage, the market is incomplete. This means that while EMMs exist, there is no unique one. This has immediate consequences for the valuation of contingent claims using our model, for example valuing European call options. We can price a European call option by the usual risk-neutral pricing formula. However, as there are infinitely many EMMs, we obtain a range of prices rather than a unique price. The good-deal bound approach is a means of narrowing the range of prices, which can be too wide to be useful in practice. The essential idea is to exclude those EMMs which imply a Sharpe Ratio that is too high.

3.1.1 The Girsanov kernel process and the Girsanov Theorem

Suppose we are given a probability measure on which is equivalent to the (real-world) probability measure . We define the likelihood process corresponding to the measure in the usual way as

We can assume that is a positive -martingale under the measure (see Rogers and Williams (2006, Theorem IV.17.1)) with , -a.s. Recalling that the filtration is generated by both the Brownian motion and the Markov chain , we can apply an appropriate martingale representation theorem (for example, see Elliott (1976, Theorem 5.1)) to obtain predictable and suitably integrable stochastic processes , for and , satisfying

| (3.1) |

In order that the measure is non-negative, the process must satisfy

We call a Girsanov kernel process. As a consequence of the Girsanov theorem (for example, see Protter (2005, Theorem 40, page 135)),

-

•

we have

(3.2) where, by Lévy’s Theorem, is a -Brownian motion; and

-

•

the process

(3.3) is a -martingale, for each . We can interpret as the intensity of the point process under the measure .

The set of martingales are the -martingales of . They are mutually orthogonal, purely discontinuous martingales which are null at the origin. Their integrability depends on the integrability of . Furthermore, substituting from (2.4) into (3.3), we find

| (3.4) |

which is analogous to (3.2).

Remark 3.1.

While retains the Markov property under the measure (this can be shown using martingale problems, for example see Ethier and Kurtz (1986, Theorem 4.4.1)), it is not generally a Markov chain. This is because the intensity of the point process under the measure is not generally deterministic.

Remark 3.2.

The condition that is to ensure that the measure is non-negative. However, if then and are not necessarily equivalent which means that we can have arbitrage. As discussed in Björk and Slinko (2006, Remark 3.3), to avoid any arbitrage possibility we can replace the inequality by , for some fixed or we can regard any good-deal bounds derived with the constraint as open intervals of good-deal bounds. We choose the latter alternative since it is mathematically more convenient.

3.1.2 The martingale condition and admissible Girsanov kernel processes

Given a suitable process , we can generate a corresponding measure by using (3.1) to define the likelihood process and then constructing the measure by

| (3.5) |

Let be the measure generated by the Girsanov kernel process . Consider an arbitrary asset in the market, with price process . Note that this asset is not restricted to the traded risky assets or risk-free asset, but it could be any derivative or self-financing strategy based on them and the Markov chain . If we price this asset using a risk-neutral measure , then the discounted price process is an -martingale under the measure . As the filtration is generated by both the Brownian motion and the Markov chain (recall (2.1)), then using a suitable martingale representation theorem (such as Elliott (1976, Theorem 5.1)) this -martingale can be expressed as the sum of a stochastic integral with respect to the Brownian motion and a stochastic integral with respect to the -martingales of the Markov chain. If we use the Girsanov theorem to obtain the -dynamics of the price process, we still have a term involving the martingales of the Markov chain. This is the reason why the -dynamics of the price process are of the form

| (3.6) |

The processes , and are suitably integrable and measurable with the condition, in order to avoid negative asset prices, that for each . Note that if the asset is not the traded asset then the processes , and depend on the choice of the risk-neutral measure through the corresponding Girsanov kernel process.

Apply (3.2) and (3.4) to (3.6) to obtain the price dynamics of the arbitrarily chosen asset under the measure :

| (3.7) |

The measure is a martingale measure if and only if the local rate of return of the asset under the measure equals the risk-free rate of return . Thus we obtain the following martingale condition.

Proposition 3.3.

Martingale condition The measure generated by the Girsanov kernel process is a martingale measure if and only if

| (3.8) |

and for any asset in the market whose price process has -dynamics given by (3.6), we have

| (3.9) |

We refer to a Girsanov kernel process for which the generated measure is a martingale measure as an admissible Girsanov kernel process.

Remark 3.4.

From (3.9) we have the following economic interpretation of an admissible Girsanov kernel process : the process is the market price of diffusion risk and is the market price of jump risk, for a jump in the Markov chain from state to state .

Suppose we are given a Girsanov kernel process for which the generated measure is a martingale measure. The price dynamics under of the th underlying risky stock are as in (2.6), that is

By Proposition 3.3, we must have that

This means that the market price of diffusion risk is determined by the price dynamics of the underlying risky assets, with the solution given by

where has all entries equal to one. However, as there is no traded asset in the market which is based on the Markov chain, we cannot say anything about the market price of jump risk .

4 The Sharpe Ratio and a Hansen-Jagannathan Bound

4.1 The Sharpe Ratio of an arbitrary asset

We define a Sharpe Ratio process for an arbitrarily chosen asset, with -dynamics as in (3.6). Broadly, the Sharpe Ratio is the excess return above the risk-free rate of the asset per unit of risk. We make this definition precise in our model. Define a volatility process for the asset by

| (4.1) |

where is the angle-bracket process. Substituting for from (3.6) and using to denote the usual Euclidean norm, we obtain

| (4.2) |

Comparing (4.1) and (4.2), we see that the squared volatility process satisfies

Recalling that the state space of the Markov chain is denoted by and the intensity process is given by (2.3), define the norm in the Hilbert space by

Then we can write

Defining the Hilbert space

| (4.3) |

and denoting by the norm in the Hilbert space , we can also express the volatility process as

| (4.4) |

Finally, we are in a position to define the Sharpe Ratio process for the arbitrarily-chosen asset. As is the local mean rate of return of the asset under the measure ,

| (4.5) |

The Sharpe Ratio process depends on the chosen asset’s price process. However, we seek a bound that applies to all assets’ Sharpe Ratio processes. To do this, we use the extended Hansen-Jagannathan inequality, which is derived in Björk and Slinko (2006) and is an extended version of the inequality introduced by Hansen and Jagannathan (1991).

4.2 An extended Hansen-Jagannathan Bound

Lemma 4.1 (An extended Hansen-Jagannathan Bound).

Proof.

The proof follows that of Björk and Slinko (2006, Theorem A.1) and is therefore omitted. ∎

5 The general problem

On the market detailed in Subsection 2.1, we consider the valuation of a general contingent claim. To apply the good-deal bound idea, suppose we are given a contingent claim of the form

| (5.1) |

for a deterministic, measurable function , where is the vector of the risky assets’ price processes. As there is no unique martingale measure in the market, there is no unique price for the contingent claim. Rather than choosing one particular martingale measure to price the contingent claim, we seek instead to find a reasonable range of prices by excluding those martingale measures which imply Sharpe Ratios which are too high.

5.1 The good-deal bound

The key idea is that to restrict the set of martingale measures by way of the Sharpe Ratio, we use the Hansen-Jagannathan bound. Rather than bounding the Sharpe Ratios directly, we bound the right-hand side of (4.6) by a constant. We call the constant a good-deal bound.

Condition 5.1.

There exists such that

Definition 5.2.

A good-deal bound is a constant .

Remark 5.3.

A chosen good-deal bound bounds the Sharpe Ratio process of any asset in the market as follows:

| (5.2) |

In other words, . The economic interpretation is that, under the good-deal bound approach, and are the highest and lowest achievable instantaneous Sharpe Ratio in the market, respectively. However, in the regime-switching diffusion market, we see from (5.2) that the good-deal bound is really a bound on the price of regime change risk, since the price of diffusion risk is determined by the traded assets.

5.2 The good-deal bound price processes

We consider the problem of finding the upper and lower good-deal bounds on the range of possible prices of the contingent claim .

Definition 5.4.

Suppose we are given a good-deal bound . The upper good-deal price process for the bound is the optimal value process for the control problem

| (5.3) |

where the predictable processes are subject to the constraints

| (5.4) |

| (5.5) |

and

| (5.6) |

for all .

Definition 5.5.

Remark 5.6.

The risk-neutral valuation formula in (5.3) implies that the local rate of return of the price process corresponding to the contingent claim equals the risk-free rate under the measure . The equality constraint (5.4) ensures that is consistent with the market price of jump risk. Together with the constraint (5.5), these ensure that the measure generated by is a martingale measure, as in Proposition 3.3. Note that, due to the constant bound on in the constraint (5.6), the measure generated by is a martingale measure, and not just a local martingale measure.

Remark 5.7.

Remark 5.8.

The only unknown in the constraints (5.4)-(5.6) is the market price of jump risk . If we obtain wide good-deal pricing bounds for a derivative then this tells us that the choice of the market price of jump risk has a large impact on the derivative’s price. Thus wide pricing bounds are a signal that we should explore additional ways of further restricting the possible values of the market price of jump risk . This point is also made in Cochrane and Saá Requejo (2000).

The goal is to calculate the upper and lower good-deal bound price processes, which are what we consider to be reasonable bounds on the possible prices of the contingent claim . To calculate them, we use a stochastic control approach.

6 Stochastic control approach

To ensure that the Markovian structure is preserved under the martingale measure , we need the following condition.

Condition 6.1.

Remark 6.2.

We note from the constraint (5.4) that the process is completely determined by the market parameters , and . This means that the requirement is really a requirement that the market parameters are of the form

6.1 The good-deal functions

Under Condition 6.1, the optimal expected value in (5.3) can be written as where the deterministic mapping is known as the optimal value function. From general dynamic programming theory (for example, see Björk (2009, Chapter 19)), the optimal value function satisfies the following Hamilton-Jacobi-Bellman equation

| (6.1) | ||||

where the supremum in (6.1) is subject to the constraints (5.4) - (5.6). An application of Itô’s formula (for example, see Protter (2005, Theorem V.18, page 278)) shows that the infinitesimal operator is given by

| (6.2) |

for all .

Definition 6.3.

Given a good-deal bound , the upper good-deal function for the bound is the solution to the following boundary value problem

| (6.3) | ||||

where is given by (6.2) and the supremum is taken over all functions subject to Condition 6.1 and satisfying

| (6.4) |

| (6.5) |

and

| (6.6) |

for all . We denote the solution to (6.3) by .

Definition 6.4.

Rather than attempting to solve the partial integro-differential equation (“PIDE”) of (6.3) directly, we reduce it to two deterministic problems which we solve for each fixed triple . Moreover, as is completely determined by (6.4), we need to solve only for the optimal .

Therefore, given satisfying (6.4), we do the following.

- 1.

-

2.

Using the optimal found above, solve the PIDE

(6.7) (6.8)

We consider in more detail how to solve the static optimization problem. To solve the PIDE, we can use numerical methods. A concrete example of this, where we find the good-deal bounds for a European call option, is given in Section 8.

6.2 The static optimization problem

As we have seen above, the static optimization problem associated with the upper good-deal function of Definition 6.3 is to find for each triple the optimal that attains the supremum of

| (6.9) |

subject to the constraints

| (6.10) |

with given by (6.4).

The static optimization problem associated with the lower good-deal function of Definition 6.4 is as for the upper good-deal function but taking the infimum of (6.9), rather than the supremum.

As the only term in (6.9) which involves is the last one, we can equivalently consider the problem of finding the optimal which attains the supremum of

| (6.11) |

subject to the constraints in (6.10). This is a linear optimization problem with both linear and quadratic constraints. We consider how the complexity of this problem increases as the number of states of the Markov chain increases.

6.2.1 Markov chain with two states

When there are only two states of the Markov chain, the solution of the linear optimization problem (6.11) subject to the constraints (6.10) is very simple indeed and can be obtained by considering the sign of in (6.11).

Lemma 6.5.

6.2.2 Markov chain with three or more states

For a Markov chain with more than two states, the solution becomes more complicated because the number of constraints increases. If there are states then for each fixed triple there are variables to find, each of which is subject to a lower and upper inequality constraint. Hence there are potential solutions, depending on which of the lower and upper constraints is binding. To see how the complexity increases, we consider a Markov chain with three states. For each , denote by the sign of .

Lemma 6.6.

For a -state Markov chain, fix and define for each , ,

Then for each and , , the solution to the static optimization problem associated with the upper good-deal function of Definition 6.3 is one of the following pairs:

| (6.12) |

| (6.13) |

| (6.14) |

| (6.15) |

and the solution to the static optimization problem associated with the lower good-deal function of Definition 6.4 is one of the following pairs:

| (6.16) |

| (6.17) |

| (6.18) |

| (6.19) |

Proof.

Apply the Kuhn-Tucker method. ∎

Remark 6.7.

The solutions and depend on the value function , just as in the two-state Markov chain case. However, the difficulty involved in solving the PIDE (6.7)-(6.8) numerically has increased since there are four potential solutions which must be checked at each node of the discretized state space. As we increase the number of states in the Markov chain, the number of potential solutions to the static optimization problem increases and hence the complexity involved in solving the PIDE increases too.

7 Minimal martingale measure

Here we leave aside the good-deal bounds and consider the minimal martingale measure, which we consider as a benchmark measure for pricing any derivative in the market.

Definition 7.1.

The minimal martingale measure is the measure generated by , where is the Girsanov kernel process which minimizes

subject to the constraint for .

It is immediate that the minimal martingale measure is generated by

for all , where has all entries equal to one. As , we have that is an admissible Girsanov kernel process.

Remark 7.2.

Under the measure , the process is a Markov chain with the same generator as under the measure . In particular, this means that the measure preserves the martingale property of the process defined by (2.4), so that the -martingales of are also its -martingales.

8 Numerical example

Having applied the good-deal bound idea in a regime-switching diffusion market, the next question is: are they useful? We examine this question by calculating the upper and lower good-deal pricing bounds for a -year European call option in a market where there are two regimes. We calculate them for various initial stock prices and for various choices of the good-deal bound. Finally, we examine how the pricing bounds change as we change the generator of the Markov chain which drives the regime-switching.

8.1 Market model

Suppose that we are in a financial market setting of Section 2 with only two market regimes and one risky asset, so that , and time is measured in years. Assume the values of the market parameters given in Table 1 and take the generator of the Markov chain to be

These figures are based on the estimated parameters found in Hardy (2001) for a -state regime-switching model fitted to data from the S&P 500, an index of 500 U.S. stocks.

| Regime | |||

|---|---|---|---|

| 1 | 0.06 | 0.15 | 0.12 |

| 2 | 0.06 | -0.22 | 0.26 |

From the generator , we see that the average time spent in regime 1 is 2 years and the average time spent in regime 2 is about 2.5 months.

8.2 Calculation and implementation

We wish to calculate the upper and lower good-deal pricing bounds for a European call option with maturity and strike price . To do this, we choose a good-deal bound and fix the initial market regime and initial stock price . Then we calculate the upper and lower good-deal functions of Definitions 6.3 and 6.4. In Section 6, we saw that this involved first

-

•

solving the associated static optimization problem, and then

- •

We have already solved the static optimization problem for a 2-state regime-switching model, with the solution given by Lemma 6.5. Thus it remains to numerically solve the PIDE

| (8.1) | ||||

for , using the optimal values which solve the static optimization problem. Denoting the solution to the above PIDE by for the upper good-deal pricing bound and by for the lower good-deal pricing bound, the good-deal price range for the derivative is . The intervals are open intervals due to the discussion in Remark 3.2.

We implement the numerical solution of the PIDE using a fully implicit, finite-difference method, based on a grid which has the values

where is the grid step-size in the time direction (measured in years), is the grid step-size in the stock price direction and is the grid range in the stock price direction. The grid range in the time direction is . We use the boundary conditions

Note that by Definition 5.2 and using the figures in Table 1 to calculate and , the good-deal bound must satisfy

8.3 Results

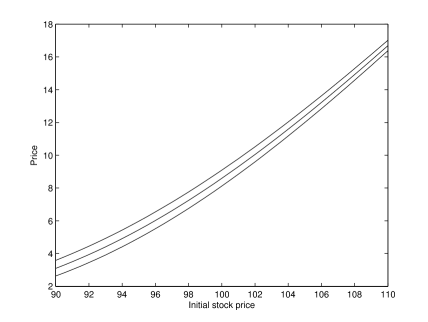

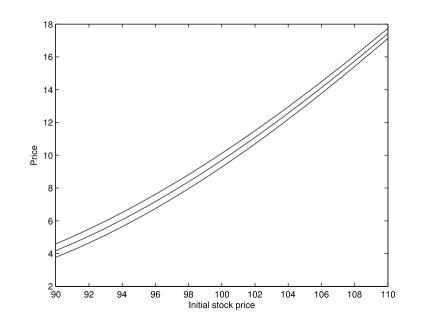

We begin by fixing the good-deal bound and calculating the upper and lower pricing bounds for a range of initial stock prices. The results are shown in Figure 1, with Figure 1(a) and 1(b) corresponding to the market starting in regime 1 and 2, respectively. The middle line in each of the plots corresponds to the minimal martingale measure price, which is the benchmark price. The plots show that, for the choice , the good-deal pricing bounds are reasonably narrow and therefore they are potentially of practical use.

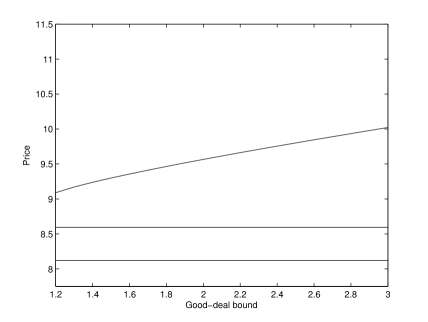

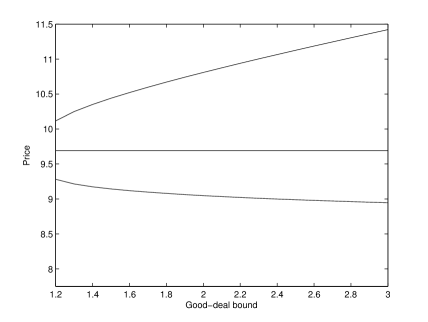

Next we examine exactly how the pricing bounds change as we vary the good-deal bound . We fix the initial stock price and calculate the good-deal pricing bounds for various choices of the good-deal bound . These results are shown in Figure 2, with Figure 2(a) and 2(b) corresponding to the market starting in regime 1 and 2, respectively. Again, the minimal martingale measure prices are the horizontal lines in the middle of each plot.

The plots in Figure 2 show that as we increase the good-deal bound , we increase the upper good-deal pricing bound. However, while the lower good-deal pricing bound decreases in Figure 2(b), it is constant in Figure 2(a). The reason is that, in this particular market, the solution to the static optimization problem for the lower good-deal function is always when starting in regime 1, regardless of the value of the good-deal bound . Setting in the PIDE (8.1), we see immediately that the last term on the left-hand side vanishes and hence the PIDE reduces to the classical Black-Scholes formula for a European call option in a non-regime-switching market with market parameters , and .

8.4 Stability of the good-deal pricing bounds

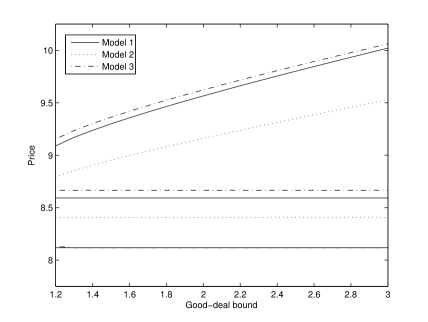

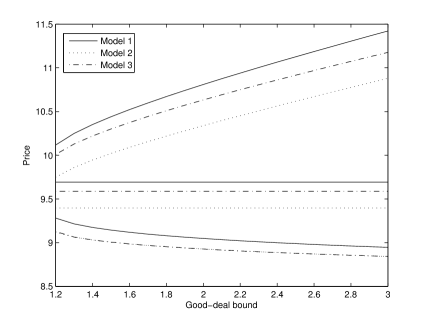

We base the market parameters in Table 1 on figures found in Hardy (2001). However, the analysis in Hardy (2001) gives a large standard error in the estimation of the Markov chain parameters. This leads us to wonder what happens if we have mis-estimated the generator of the Markov chain. Do we have stability of the good-deal pricing bounds? To examine this issue, we consider again a -year European call option with strike price . We find the good-deal pricing bounds for this option for three different models, assuming that the price of the risky stock at time 0 is . In each of the models, the market parameters , and are as in Table 1 but the diagonal elements of the generator of the Markov chain are given in Table 2.

| Model 1 | Model 2 | Model 3 | |

| 0.5 | 0.333 | 0.667 | |

| 5 | 6 | 6 | |

| Avg. time in regime 1 | 2.000 | 3.000 | 1.500 |

| Avg. time in regime 2 | 0.200 | 0.167 | 0.167 |

Note that Model 1 corresponds to the model described in Subsection 8.1. The results are shown in Figure 3, with Figure 3(a) and 3(b) corresponding to the market starting in regime 1 and 2, respectively. The middle horizontal lines in the plots correspond to the minimal martingale measure prices.

The plots show that the good-deal pricing bounds are sensitive to the choice of the generator of the Markov chain. Roughly, the upper good-deal pricing bounds move in tandem with the minimal martingale measure prices. In Figure 3(b), the lower good-deal pricing bounds behave similarly. However, in Figure 3(a), the lower good-deal pricing bounds are nearly all constant. The explanation for the constant lower pricing bounds is as before: the solution to the static optimization problem for the lower good-deal function is when starting in regime 1 in these cases. In Figure 3(a) we see that lower good-deal pricing bound is slightly higher at the good-deal bound because here the solution to the static optimization problem for the lower good-deal function is just above .

9 Conclusion

We have applied the good-deal bound idea of Cochrane and Saá Requejo (2000) to a regime-switching market using the approach of Björk and Slinko (2006) and illustrated it with a numerical example. The good-deal bound idea is a way to measure the uncertainty in the choice of the risk-neutral measure used to price derivatives. However, as our numerical example demonstrates, the good-deal pricing bounds change when the model changes, even though the good-deal bound remains constant. Thus the good-deal pricing bounds are sensitive to the choice of model. It would be interesting to do a wider investigation of the variation of the good-deal pricing bounds over a wider class of models for different derivatives.

We have looked at pricing, but what is a “good-deal hedging” strategy? As Björk and Slinko (2006) say in their conclusion, this is a highly challenging open problem.

Acknowledgments

The author thanks RiskLab, ETH Zurich, Switzerland for financial support. The author is grateful to Tomas Björk for his sound advice and his correction of some errors in an early draft of this paper. Paul Embrechts, Marius Hofert and an anonymous referee made valuable comments on the presentation of the paper. The author thanks Michel Baes for a helpful discussion.

References

- Ang and Bakaert [2002] A. Ang and G. Bakaert. Regime switches in interest rates. Journal of Business and Economic Statistics, 20:163–182, 2002.

- Bayraktar and Young [2008] E. Bayraktar and V. Young. Pricing options in incomplete equity markets via the instantaneous Sharpe ratio. Annals of Finance, 4:399–429, 2008.

- Bernardo and Ledoit [2000] A.E. Bernardo and O. Ledoit. Gain, loss, and asset-pricing. Journal of Political Economy, 108:144–172, 2000.

- Björk [2009] T. Björk. Arbitrage Theory in Continuous Time. Oxford University Press, Oxford, UK, 3rd edition, 2009.

- Björk and Slinko [2006] T. Björk and I. Slinko. Towards a general theory of good-deal bounds. Review of Finance, 10:221–260, 2006.

- C̆erný [2003] J. C̆erný. Generalised Sharpe ratios and asset pricing in incomplete markets. European Finance Review, 7:191–233, 2003.

- Cochrane and Saá Requejo [2000] J. Cochrane and J. Saá Requejo. Beyond arbitrage: good-deal asset price bounds in incomplete markets. Journal of Political Economy, 108:79–119, 2000.

- Elliott [1976] R.J. Elliott. Double martingales. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 34:17–28, 1976.

- Ethier and Kurtz [1986] S.N. Ethier and T.G. Kurtz. Markov Processes: Characterization and Convergence. John Wiley, USA, 1986.

- Gray [1996] S. F. Gray. Modeling the conditional distribution of interest rates as a regime-switching process. Journal of Financial Economics, 42(1):27–62, 1996.

- Hamilton [1989] J. D. Hamilton. A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica, 57:357–384, 1989.

- Hansen and Jagannathan [1991] L.P. Hansen and R. Jagannathan. Implications of security market data for models of dynamic economies. Journal of Political Economy, 99:225–262, 1991.

- Hardy [2001] M. R. Hardy. A regime-switching model of long-term stock returns. North American Actuarial Journal, 5(2):41–53, 2001.

- Klaassen [2002] F. Klaassen. Improving GARCH volatility forecasts with regime-switching GARCH. Empirical Economics, 27:363–394, 2002.

- Klöppel and Schweizer [2007] S. Klöppel and M. Schweizer. Dynamic utility-based good deal bounds. Statistics and Decisions, 25:285–309, 2007.

- Protter [2005] P. E. Protter. Stochastic Integration and Differential Equations. Springer-Verlag, New York, USA, 2nd edition, 2005.

- Rogers and Williams [2006] L.C.G. Rogers and D. Williams. Diffusions, Markov Processes and Martingales Volume 2. Cambridge University Press, Cambridge, UK, 2nd edition, 2006.