On the Eigenvalue Density of Real and Complex Wishart Correlation Matrices

Christian Recher, Mario Kieburg and Thomas Guhr

Fakultät für Physik, Universität Duisburg–Essen, Lotharstraße 1,

47048 Duisburg, Germany

Abstract

Wishart correlation matrices are the standard model for the

statistical analysis of time series. The ensemble averaged

eigenvalue density is of considerable practical and theoretical

interest. For complex time series and correlation matrices, the

eigenvalue density is known exactly. In the real case, however, a

fundamental mathematical obstacle made it forbidingly complicated to

obtain exact results. We use the supersymmetry method to fully

circumvent this problem. We present an exact formula for the

eigenvalue density in the real case in terms of twofold integrals

and finite sums.

Time series analysis is an indispensable tool in the study of complex

systems with numerous applications in physics, climate research,

medicine, signal transmission, finance and many other

fields Chatfield (2004); Müller et al. (2005); Šeba (2003). A time series is an observable such

as the water level of a river, the temperature, the intensity of

transmitted radiation, the neuron activity in electroencephalography

(EEG), the price of a stock, etc., measured at usually equidistant

times . Suppose we measure such time series , for example, in the case of EEG, at electrodes

placed on the scalp or, in the case of temperatures, at different

locations. Our data set then consists of the rectangular

matrix with entries . The time series are usually

real (labeled ), but in some applications they can be

complex (). Often, one is interested in the correlations between

the time series. To estimate them, one normalizes the time series

to zero mean and unit variance. The correlation coefficient

between the time series and is then given as the sample

average

(1)

is the correlation matrix. For real time series (), the

complex conjugation is not needed and the adjoint is simply the

transpose. We notice that is a real–symmetric

() or Hermitean () matrix.

The eigenvalues of provide important information, see recent

examples in Refs. Laurent et al. (1999); Sprik et al. (2008). As the empirical information is

limited, it is desirable to compare the measured eigenvalue density

with a “null hypothesis” that results from a statistical ensemble.

The ensemble is defined Muirhead (1982) by synthetic real or complex time

series which yield the empirical

correlation matrix upon averaging over the probability density

function

(2)

that is, we have by construction

(3)

where the measure is the product of the differentials of all

independent elements in . To ensure that is invertible, we

always assume . When going to higher order statistics, the

Gaussian assumption (2) is not necessarily justified, but it

often is a good approximation. This multivariate statistical approach

is closely related to Random Matrix Theory Guhr et al. (1998), and the

matrices are referred to as Wishart correlation

matrices. One is interested in the ensemble averaged eigenvalue

density of these matrices. In terms of the resolvent, it reads

(4)

where is the unit matrix. The argument

carries a small positive imaginary increment ,

indicated by the notation . The limit

is implicit in our notation. Due to the invariance

of the trace and the measure, the ensemble averaged eigenvalue density

only depends on the eigenvalues of . Hence we may replace in Eq. (4) by the

diagonal matrix . We

notice that the eigenvalues are positive definite, .

A large body of literature is devoted to the eigenvalue

density (4). Its asymptotic form for large and has

been studied in great detail, see Refs. Silverstein (1995); Vinayak and Pandey (2010). However,

an exact closed–form result for finite and is only available

in the complex case Alfano et al. (2004); Simon and Moustakas (2004). Unfortunately, a deep,

structural mathematical reason made it up to now impossible to derive

such a closed–form result in the real case which is the more relevant

one for applications. We have three goals: We, first, introduce the

powerful supersymmetry method Efetov (1983); Verbaarschot et al. (1985); Efetov (1997) to Wishart

correlation matrices for arbitrary . This has, to the best of our

knowledge, not been done before. We, second, use the thereby achieved

unique structural clearness to derive a new and exact closed–form

result for the eigenvalue density in the real case for finite and

. We, third, show that our results are easily numerically tractable

and compare them with Monte Carlo simulations.

Why does the real case pose such a substantial problem? — This is

best seen by going to the polar decomposition , where for and for and where is the

matrix containing the singular values or radial coordinates . In particular, one has , with .

When inserting into (4), one sees that the non–trival group

integral

(5)

has to be done to obtain the joint probability density function of the

radial coordinates . Here, is the invariant Haar measure.

For , this integral is the celebrated

Harish-Chandra–Itzykson–Zuber integral and known

explicitly Harish-Chandra (1958); Itzykson and Zuber (1980). For , however,

, is not a Harish-Chandra spherical

function, it rather belongs to the Gelfand class Gelfand (1950) and a

closed–form expression is lacking. The only explicit form known is a

cumbersome, multiple infinite series expansion in terms of zonal or Jack

polynomials Muirhead (1982); Macdonald (1998). This inconvenient feature then carries over

to the eigenvalue density (4), but we will arrive at

a finite series over twofold integrals.

The supersymmetry method is based on writing

(6)

as the derivative of the generating function

(7)

with respect to the source variable at . One has the

normaliziation at . We consider the real and the

complex case and use the latter as test. We map onto

superspace using steps which are by now standard, see

Refs. Verbaarschot et al. (1985); Efetov (1997). A particularly handy approach for

applications such as the present one is given in Ref. Kieburg et al. (2009), we

use the same conventions and find

(8)

The merit of this transformation is the drastic reduction in the

number of degrees of freedom, because the variables to be intergrated

over form the Hermitean supermatrix

(9)

For , and are scalar, real commuting

variables and is a complex anticommuting scalar variable.

For , is a real symmetric matrix,

has to be multiplied with and we have

(10)

where and denote anticommuting variables

and their complex conjugates, respectively. We also introduced the

matrix and the

supersymmetric Ingham–Siegel integral

(11)

where has the same form as . The supertrace and

superdeterminant Berezin (1987) are denoted by str and sdet.

Starting from the generating function (8) we first consider

the complex case . By introducing eigenvalue–angle

coordinates for the supermatrix , we rederive in a

straightforward calculation the eigenvalue density as found

in Ref. Alfano et al. (2004). In the real case , the analogous

approach leads to inconvenient Efetov–Wegner terms Efetov (1997), and

we thus proceed differently. Since the generating function remains

invariant under rotations of the matrix , we introduce its

eigenvalues and the diagonalizing angle as new

coordiantes. This yields the Jacobian .

The next step is to evaluate the Ingham–Siegel integral .

The supermatrix in Eq. (11) has the same form as

in Eq. (9). Doing the integral over followed

by an expansion in the anticommuting variables of according to

Eq. (10) gives

(12)

In a simple, direct calculation, we also expand the product of the

superdeterminats in Eq. (8) in the anticommuting variables of

. We collect everything and do the integration over

the anticommuting variables. With the notation , we obtain

(13)

According to Eq. (6) we have to take the derivative with respect to

. This leads to the three relations

(14)

where denotes the elementary symmetric polynomial of

order in the variables with

and omitted,

(15)

We finally arrive at

(16)

where the constant reads .

Due to the –distribution, the integral over are

elementary. Hence we end up with an expression for the eigenvalue

density which essentially is a twofold integral.

The integrals in Eq. (16) can be numerically evaluated by

using a regularisation technique of the type

(17)

Here we assume an ordering of the eigenvalues such that with

and . The real function

is independent of and has no singularities.

The singularties at the boundaries of the domain are integrable. Using

the commercial software Mathematica® Wolfram Research Inc. (2008), we evaluate

our formula (17) numerically. For independent comparison, we

also carry out Monte Carlo simulations with ensembles of matrices.

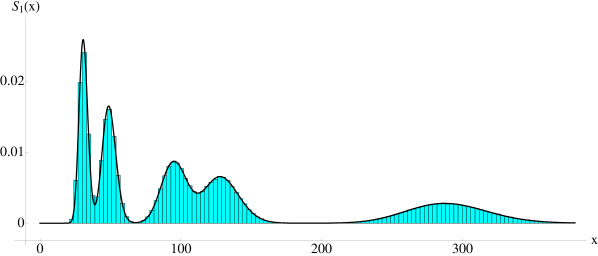

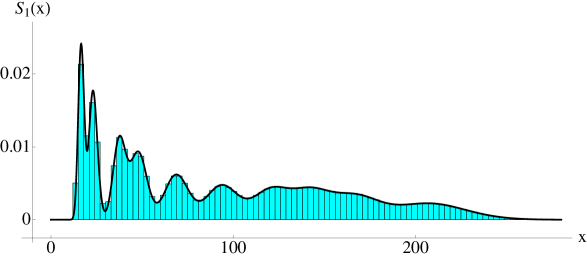

In Figs. 1 and 2, we show the

Figure 1: Eigenvalue density for and : analytical

formula (solid lines) and Monte Carlo simulations (histogram with bin width 3).

Figure 2: Eigenvalue density for and : analytical

formula (solid lines) and Monte Carlo simulations (histogram with bin width 3).

results for and and with the chosen empirical eigenvalues

, of and

, of , respectively. The agreement is perfect.

In conclusion, we introduced the supersymmetry method for the first

time to Wishart correlation matrices. We thereby derived exact

expressions for the eigenvalue density in terms of low–dimensional

integrals. This is a drastic reduction, as the original order of

integrals is . Our approach solves a serious mathematical

obstacle in the real case. A presentation for a mathematics audience

will be given elsewhere Recher et al. (2010). Here, we derived and discussed

the formulae needed for applications. In the real case (), we

obtained the previously unknown exact solution in terms of a finite sum

of twofold integrals. We evaluated our formula numerically and

confirmed it by comparing to Monte Carlo simulations.

We thank R. Sprik for fruitful discussions as well as A. Hucht,

H. Kohler, and R. Schäfer for helpful comments. One of us (TG)

greatly benefitted from the Program on High Dimensional Inference and

Random Matrices in 2006 at SAMSI, Research Triangle Park, North

Carolina (USA). We acknowledge support from Deutsche

Forschungsgemeinschaft (Sonderforschungsbereich Transregio 12).

References

Chatfield (2004)

C. Chatfield,

The Analysis of Time Series

(Chapman and Hall/CRC, Boca Raton,

2004), 6th ed.

Müller et al. (2005)

M. Müller,

G. Baier,

A. Galka,

U. Stephani, and

H. Muhle,

Phys. Rev. E 71,

046116 (2005).

Šeba (2003)

P. Šeba, Phys. Rev. Lett.

91, 198104

(2003).

Sprik et al. (2008)

R. Sprik,

A. Tourin,

J. de Rosny, and

M. Fink,

Phys. Rev. B 78,

012202 (2008).

Laurent et al. (1999)

L. Laurent,

P. Cizeau,

J. Bouchaud, and

M. Potters,

Phys. Rev. Lett. 83,

1467 (1999).

Muirhead (1982)

R. Muirhead,

Aspects of Multivariate Statistical Theory

(Wiley, New York,

1982), 1st ed.

Guhr et al. (1998)

T. Guhr,

A. Müller-Groeling,

and

H. Weidenmüller,

Phys. Rep. 299,

189 (1998).

Silverstein (1995)

J. Silverstein,

Multivariate Anal. 55,

331 (1995).

Vinayak and Pandey (2010)

Vinayak and

A. Pandey,

Phys. Rev. E 81,

036202 (2010).

Alfano et al. (2004)

G. Alfano,

A. Tulino,

A. Lozano, and

S. Verdu,

Proc. IEEE Int. Symp. on Spread Spectrum Tech. and

Applications (ISSSTA ’04) (2004).

Simon and Moustakas (2004)

S. Simon and

A. Moustakas,

Phys. Rev. E 69,

065101 (2004).

Efetov (1983)

K. Efetov,

Adv. Phys. 32,

53 (1983).

Verbaarschot et al. (1985)

J. Verbaarschot,

H. Weidenmüller,

and

M. Zirnbauer,

Phys. Rep. 129,

367 (1985).

Efetov (1997)

K. Efetov,

Supersymmetry in Disorder and Chaos

(Cambridge University Press,

Cambridge, 1997), 1st

ed.

Harish-Chandra (1958)

Harish-Chandra, Am. J. Math.

80, 241 (1958).

Itzykson and Zuber (1980)

C. Itzykson and

J. Zuber, J.

Math. Phys. 21, 411

(1980).

Gelfand (1950)

I. Gelfand,

Dokl. Akad. Nauk. SSSR 70,

5 (1950).

Macdonald (1998)

I. Macdonald,

Symmetric Functions and Hall Polynomials

(Clarendon Press, Oxford,

1998), 2nd ed.

Kieburg et al. (2009)

M. Kieburg,

J. Grönqvist,

and T. Guhr,

J.Phys. A 42,

275205 (2009).

Berezin (1987)

F. Berezin,

Introduction to Superanalysis (D.

Reidel Publishing Company, Dordrecht,

1987), 1st ed.

Wolfram Research Inc. (2008)

Wolfram Research Inc.,

Mathematica Version 7.0,

Champaign, Illinois (2008).

Recher et al. (2010)

C. Recher,

M. Kieburg, and

T. Guhr, in

preparation (2010).