The dual optimizer for the growth-optimal portfolio under transaction costs

Abstract.

We consider the maximization of the long-term growth rate in the Black-Scholes model under proportional transaction costs as in Taksar, Klass and Assaf [Math. Oper. Res. 13, 1988]. Similarly as in Kallsen and Muhle-Karbe [Ann. Appl. Probab., 20, 2010] for optimal consumption over an infinite horizon, we tackle this problem by determining a shadow price, which is the solution of the dual problem. It can be calculated explicitly up to determining the root of a deterministic function. This in turn allows to explicitly compute fractional Taylor expansions, both for the no-trade region of the optimal strategy and for the optimal growth rate.

Key words and phrases:

Transaction costs, growth-optimal portfolio, shadow price2000 Mathematics Subject Classification:

91B28, 91B16, 60H101. Introduction

Portfolio optimization is a classical example of an infinite-dimensional concave optimization problem. The first ingredient is a probabilistic model of a financial market, e.g., the Black-Scholes model consisting of a bond modelled as

| (1.1) |

and a stock modelled as

| (1.2) |

Here is a standard Brownian motion and , as well as denote constants. In the sequel, we focus on the Black-Scholes model and assume (without loss of generality for the present purposes) that , and .

In order to model the preferences of an economic agent, the second ingredient is a utility function . In the present paper we will deal with the most tractable specification, namely logarithmic utility

The third ingredient is an initial endowment of units of bonds, as well as a time horizon .

There are essentially two versions of the portfolio optimization problem.

The first version consists of maximizing the expected utility from consumption, which is typically formulated for an infinite horizon:

| (1.3) |

Here, is a discount factor pertaining to the impatience of the investor and runs through all positive consumption plans which can be financed by the initial endowment and subsequent trading in the stock . In Merton’s seminal paper [21], it is shown that – in the Black-Scholes model and for the case of logarithmic or power utility – there are two constants , depending on the model parameters, such that the optimal strategy consists of investing a fraction of the current wealth into the stock and consuming with an intensity which is a fraction of the current wealth.

The second version of the portfolio optimization problem is to choose a time horizon and to maximize expected utility from terminal wealth:

| (1.4) |

Here we maximize over all predictable processes describing the number of stocks which the agent holds at time . We only consider those strategies which are admissible, i.e. lead to a nonnegative wealth process . Again, it turns out that – for the Black-Scholes model (1.2) and logarithmic or power utility – the optimal strategy is to keep the proportion between wealth invested in the stock and total wealth constant. In particular, for logarithmic utility, this Merton rule reads as

| (1.5) |

Here, and denote the the holdings in bond and stock, respectively, which are related via the self-financing condition that no funds are added or withdrawn. In fact, (1.5) holds true much more generally; e.g., for Itô processes with – say – bounded coefficients one just has to replace and with the drift coefficient resp. the diffusion coefficient (cf. e.g. [17, Example 6.4]). This particular tractability of the -utility maximization problem is a fact which we are going to exploit later on.

We now pass to the theme of the present paper, which is portfolio optimization under (small) transaction costs. To this end, we now assume that (1.2) defines the ask price of the stock, while the corresponding bid price is supposed to be given by for some constant . This means that one has to pay the higher price when purchasing the stock at time , but only receives the lower price when selling it.111This notation, also used in [25], turns out to be convenient in the sequel. It is equivalent to the usual setup with the same constant proportional transaction costs for purchases and sales (compare e.g. [7, 14, 24]). Indeed, set and . Then coincides with . Conversely, any bid-ask process with equals for and . Since transactions of infinite variation lead to immediate bankruptcy, we confine ourselves to the following set of trading strategies.

Definition 1.1.

A trading strategy is an -valued predictable finite variation process , where represents the initial endowment in bonds222This assumption is made mainly for notational convenience. An extension to general initial endowments is straightforward. and denote the number of shares held in the bank account and in stock at time , respectively.

To capture the notion of a self-financing strategy, we use the intuition that no funds are added or withdrawn. To this end, we write the second component of a strategy as the difference of two increasing processes and which do not grow at the same time. The proceeds of selling stock must be added to the bank account while the expenses from the purchase of stock have to be deducted from the bank account in any infinitesimal period , i.e., we require

Written in integral terms this amounts to the following notion.

Definition 1.2.

A trading strategy is called self-financing, if

| (1.6) |

where for increasing predictable processes which do not grow at the same time.

Note that since is continuous and is of finite variation, integration by parts yields that this definition coincides with the usual notion of self-financing strategies in the absence of transaction costs if we let .

The subsequent definition requires the investor to be solvent at all times. For frictionless markets, i.e. if , this coincides with the usual notion of admissibility.

Definition 1.3.

A self-financing trading strategy is called admissible, if its liquidation wealth process

is a.s. nonnegative.

Utility maximization problems under transaction costs have been studied extensively. In the influential paper [7], Davis and Norman identify the solution to the infinite-horizon consumption problem (1.3) (compare also [14, 24]). Transaction costs make it unfeasible to keep a fixed proportion of wealth invested into stocks, as this would involve an infinite variation of the trading strategy. Instead, it turns out to be optimal to keep the fraction of wealth in stocks in terms of the ask price inside some interval. Put differently, the investor refrains from trading until the proportion of wealth in stocks leaves a no-trading region. The boundaries of this no-trade region are not known explicitly, but can be determined numerically by solving a free boundary problem.

Liu and Loewenstein [20] approximate the finite horizon problem by problems with a random horizon, which turn out to be more tractable. Dai and Yi [6] solve the finite-horizon problem by characterizing the time-dependent boundaries of the no-trade region as the solution to a double-obstacle problem, where the ODE of [7] is replaced by a suitable PDE. Taksar et al. [25] consider the long-run limit of the finite horizon problem, i.e. the maximization of the portfolio’s asymptotic logarithmic growth rate. As in the infinite-horizon consumption problem, this leads to a no transaction region with constant boundaries. However, these boundaries are determined more explicitly as the roots of a deterministic function. Arguing on an informal level, Dumas and Luciano [9] extend this approach to the maximization of the asymptotic power growth rate. To the best of our knowledge, a rigorous proof of this result still seems to be missing in the literature, though.

From now on, we only consider logarithmic utility and formulate the problem, for given initial endowment in bonds, time horizon and transaction costs , in direct analogy to the frictionless case in (1.4) above.

Definition 1.4 (-optimality for horizon , first version).

An admissible strategy is called -optimal on for the bid-ask process , if

| (1.7) |

for all competing admissible strategies .

It turns out that this problem is rather untractable. To see this, consider the special and particularly simple case . In the frictionless case, Merton’s rule (1.5) tells us what the optimal strategy is: At time , convert the entire initial holdings into stock, i.e., pass from to . Then keep all the money in the stock, i.e., , for the entire period . At the terminal date , this provides a logarithmic utility of , after converting the stocks into bonds (without paying transaction costs).

Let us now pass to the setting with transaction costs . If , it is, from an economic point of view, rather obvious what constitutes a “good” strategy for the optimization problem (1.7): Again convert the initial holdings of bonds at time into stocks and simply hold these stocks until time without doing any dynamic trading. Converting the stocks back into bonds at time , this leads to a logarithmic utility of . Put differently, the difference to the frictionless case is only the fact that at terminal date you once have to pay the transaction costs .

Now consider the case . In this situation, the above strategy does not appear to be a “good” approach to problem (1.7) any more. The possible gains of the stock during the (short) interval are outweighed by the (larger) transaction costs . Instead, it now seems to be much more appealing to simply keep your position of bonds during the interval and not to invest into the stock at all.

These considerations are of course silly from an economic point of view, where only the case is of interest. The economically relevant issue is how the dynamic trading during the interval is affected when we pass from the frictionless case to the case . Paying the transaction costs only once at time (resp. twice if we also model the transaction costs for the purchase at time ) can be discarded from an economic point of view, as opposed to the “many” trades necessary to manage the portfolio during if . This economic intuition will be made mathematically precise in Corollary 6.2 and Proposition 6.3 below, where the leading terms of the relevant Taylor expansions in are of the order and , respectively. The effect of paying transaction costs once, however, is only of order (compare Corollary 1.9 below).

Mathematically speaking, a consequence of the above formulation (1.7) is the loss of time consistency, which we illustrated above for the special case . For , it follows from Merton’s rule (1.5) that the optimal strategy in the problem (1.4) without transaction costs does not depend on the time horizon , i.e., is optimal for all . In the presence of transaction costs, this desirable concatenation property does not hold true any more for Problem (1.7) as we have just seen. There is a straightforward way to remedy this nuisance, namely passing to the limit . This has been done by Taksar, Klass and Assaf [25] and in much of the subsequent literature.

Definition 1.5.

An admissible strategy is called growth-optimal, if

for all competing admissible strategies .

Note that the optimal growth rate does not depend on the initial endowment . Moreover, the above notion does not yield a unique optimizer. As the notion of growth optimality only pertains to a limiting value, suboptimal behaviour on any compact subinterval of does not matter as long as one eventually behaves optimally. While the notion of growth optimality allows to get rid of the nuisance of terminal liquidation costs, the non-uniqueness of an optimizer has serious drawbacks. For example, much of the beauty of duality theory, which works nicely when the primal and dual optimizers are unique, is lost.

In order to motivate our final remedy to the “nuisance problem” (cf. Definition 1.7 below), we introduce, as in [15], the concept of a shadow price which will lead us to the notion of a dual optimizer .

Definition 1.6.

A shadow price for the bid-ask process is a continuous semimartingale with and taking values in , such that the -optimal portfolio for the frictionless market with price process exists, is of finite variation and the number of stocks only increases (resp. decreases) on the set (resp. . Put differently, is the difference of the increasing predictable processes and .

We now pass to the decisive trick to modify the finite-horizon problem. Given a shadow price , formulate the optimization problem such that we only allow for trading under transaction costs during the interval , but at time we make an exception. At the terminal time , we allow to liquidate our position in stocks at the shadow price rather than at the (potentially lower) bid price . Here is the mathematical formulation:

Definition 1.7 (-optimality for horizon , modified version).

Given a shadow price and a finite time horizon , we call an admissible (in the sense of Definition 1.3) trading strategy -optimal for the modified problem if

for every competing admissible strategy , where

denotes the wealth process for liquidation in terms of .

Of course, the above definition is “cheating” by using the shadow price process – which is part of the solution – in order to define the optimization problem. But this trick pays handsome dividends: Suppose that the -optimizer for the frictionless market is admissible for the bid-ask process , i.e., is of finite variation and has a positive liquidation value even in terms of the lower bid price (this will be the case in the present context). Then this process is the optimizer for the modified optimization problem from Definition 1.7:

Proposition 1.8.

Let be a shadow price for the bid-ask process with associated -optimal portfolio . If , this portfolio is also -optimal for the modified problem under transaction costs from Definition 1.7.

Proof.

Since only increases (resp. decreases) on (resp. ), it follows from the definition that the portfolio is self-financing for the bid-ask process . Hence it is admissible in the sense of Definition 1.3 if . Now let be any admissible policy for and set . Then and is an admissible portfolio for , since . Together with the -optimality of for , this implies

which proves the assertion. ∎

As a corollary, we obtain that the difference between the optimal values for the modified and the original problem is bounded by and therefore of order as the transaction costs tend to zero. In particular, this difference vanishes if one considers the infinite-horizon problem studied by [25].

Corollary 1.9.

Let be a shadow price for the bid-ask process with -optimal portfolio satisfying . Then

where the supremum is taken over all , which are admissible for the bid-ask process . Moreover, is growth-optimal for .

Proof.

We formulated the corollary only for positive holdings in bonds and stocks. In the present context, this will only be satisfied if . To cover also the case , we show in Lemma 5.3 below that the assertion of Corollary 1.9 remains true more generally in the present setup, provided that the transaction costs are sufficiently small.

Finally, let us point out that – due to Definition 1.7 – much of the well-established duality theory for frictionless markets (cf. e.g. [13, 16, 22]) carries over to the modified problem. Let denote the unique equivalent martingale measure for the process . Then the pair , which corresponds to a consistent price system in the notation of [12], is the dual optimizer for the modified problem from Definition 1.7 (compare [5]). Recalling that the conjugate function to is , we obtain the equality of the primal and dual values

where the relation between the Lagrange multiplier and the initial endowment is given by . We then also have the first-order condition

as well as several other identities of the duality theory, see e.g. [13, 16, 22, 19]. In other words, the little trick of “allowing liquidation in terms of a shadow price at terminal time ” allows us to use the full strength of the duality theory developed in the frictionless case.

The main contribution of the present article is that we are able to explicitly determine a shadow price process for the bid-ask process in Theorem 5.1. Roughly speaking, the process oscillates between the ask price and the bid price , leading to buying (resp. selling) of the stock when (resp. ). The predictable sets and when one buys (resp. sells) the stock are of “local time type”. Remarkably, our shadow price process nevertheless is an Itô process, whence it “does not move” on the sets and . The reason is that there is a kind of “smooth pasting” when the process touches resp. . When this happens, the processes and (resp. and ) are aligned of first order, see Section 2 for more details. This parallels the results of [15]. These authors determine a shadow price for the infinite-horizon consumption problem. Their characterization, however, involves an SDE with instantaneous reflection, whose coefficients have to be determined from the solution to a free boundary problem.

Here, on the other hand, the relation between the shadow price and the ask price (as well as its running minimum and maximum) is established via a deterministic function , which is the solution of an ODE and known in closed form up to determining the root of a deterministic function. This ODE is derived heuristically from an economic argument in Section 3, namely by applying Merton’s rule to the process . Subsequently, we show in Section 4 that these heuristic considerations indeed lead to well-defined solutions. With our candidate shadow price process at hand, Merton’s rule quickly leads to the corresponding -optimal portfolio in Section 5. This in turn allows us to verify that is indeed a shadow price. Finally, in Section 6, we expound on the explicit nature of our previous considerations. More specifically, we derive fractional Taylor expansions in powers of for the relevant quantities, namely the width of the no-trade region and the asymptotic growth rate. The coefficients of these power series, which are rational functions of and , can all be algorithmically computed. For the related infinite-horizon consumption problem, the leading terms were determined and the second-order terms were conjectured in [14] (compare also [1, 23, 24, 26] for related asymptotic results).

Of course, the very special setting of the paper can be generalized in several directions. One may ask whether similar results can be obtained for more general diffusion processes or, even more generally, for stochastic processes which allow for -consistent price sytems such as geometric fractional Brownian motion. Another natural extension of the present results is the consideration of power utility and/or consumption. This is a theme for future research (compare [10]).

2. Reflection without local time via smooth pasting

In this section, we show how to construct a process that remains within the upper and lower boundaries of the bid-ask spread , yet does not incorporate local time, i.e., is an Itô process (see (2.5) below).

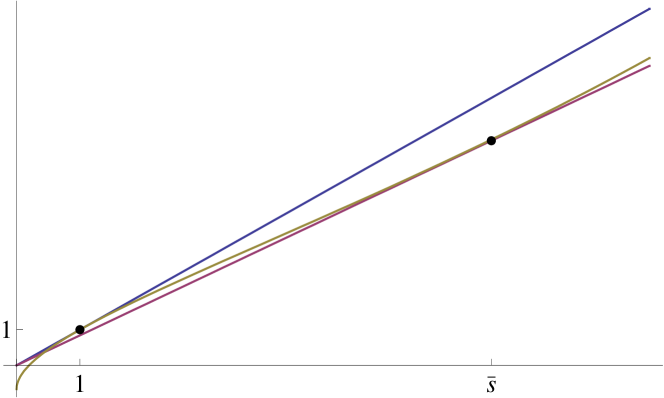

To this end, suppose that there is a real number and a -function

| (2.1) |

such that for and satisfies the smooth pasting condition with the line at the point , i.e.,

| (2.2) |

and with the line at the point i.e.,

| (2.3) |

These conditions are illustrated in Figure 1 and motivated in Remark 2.3 below.

Now define sequences of stopping times and processes and as follows: let and the running minimum process of , i.e.,

where the stopping time is defined as

Next define as the running maximum process of after time , i.e.,

where the stopping time is defined as

For , we again define

where

and, for , we define

where

Continuing in an obvious way we obtain series and of a.s. finite stopping times and , increasing a.s. to infinity, such that (resp. ) are the relative running minima (resp. maxima) of defined on the stochastic intervals (resp. ). Note that

and

We may therefore continuously extend the processes and to by letting

For , we then have as well as , and hence

By construction, the processes and are of finite variation and only decrease (resp. increase) on the predictable set (resp. .

We can now state and prove the main result of this section.

Proposition 2.1.

Under the above assumptions define the continuous process

| (2.4) |

Then is an Itô process starting at and satisfying the stochastic differential equation

| (2.5) |

Moreover, takes values in the bid-ask spread .

Remark 2.2.

We have formulated the proposition only for the Black-Scholes model (1.2). But – unlike the considerations in the following sections – it has little to do with this particular process and can also be formulated for general Itô processes satisfying some regularity conditions.

Remark 2.3.

Formula (2.5) is obtained by applying Itô’s formula to (2.4), pretending that the process were constant. The idea behind this approach is that on the complement of the “singular” set the process indeed “does not move” (the statement making sense, at least, on an intuitive level). On the set , where the process “does move”, the smooth pasting conditions (2.2) and (2.3) will make sure that the SDE (2.5) is not violated either, i.e., the process “does not move” on this singular set. This intuitive reasoning will be made precise in the subsequent proof of Proposition 2.1.

of Proposition 2.1.

We first show that the process defined in (2.4) satisfies the SDE (2.5) on the stochastic interval , where is arbitrary.

Fix where and define inductively the stopping times and by letting and, for ,

Clearly, the sequences and increase a.s. to .

We partition the stochastic interval into (the letters reminding of “local time” and “regular set”), where

As is a predictable set we may form the stochastic integral . Arguing on each of the intervals , we obtain

| (2.6) |

This is a mathematically precise formula corresponding to the intuition that “does not move” on Arguing once more on the intervals Itô’s formula and (2.6) imply that

| (2.7) |

In other words, the SDE (2.5) holds true, when localized to the set

We now show that the process tends to zero, as More precisely, we shall show that

| (2.8) |

where the limit is taken with respect to convergence in probability. This will finish the proof of (2.5) on as (2.8) implies that, for ,

Here the first equality follows from (2.8) and the fact that , with denoting Lebesgue measure on , which gives

in probability. The second equality is just (2.7), and the third one again follows from and the fact that the drift and diffusion coefficients appearing in the above integral are locally bounded.

To show (2.8), fix and such that By the definition of and as well as a second order Taylor expansion of around utilizing , we obtain

where does not depend on and . Likewise, and, in fact

for fixed . Denote by the random variable

Then

| (2.9) |

By Itô’s formula, we have

Since is bounded by , the third term on the right-hand side is a square-integrable martingale, and the first one is of integrable variation. Moreover, the variation of the second term is bounded by times the variation of , which is integrable as well. As , if one can therefore apply a version of Doob’s upcrossing inequality for semimartingales (cf. [2]) to conclude that in and hence in probability. Thus (2.9) implies (2.8) which in turn shows (2.5), for .

Repeating the above argument by considering the function in an -neighborhood of rather than and using that and , we obtain

which implies the validity of (2.5) for

Continuing in an obvious way we obtain (2.5) on . Since was arbitrary, this completes the proof. ∎

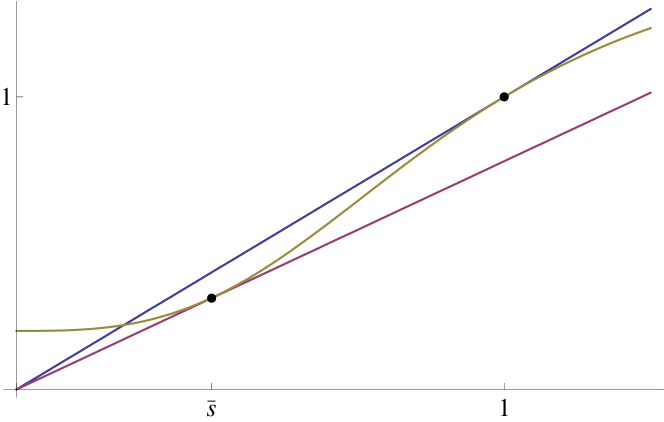

Remark 2.4.

We have made the assumption in (2.1) above. There also is a symmetric version of the above proposition, where and the function

satisfies

See Figure 2 for an illustration.

Define now

as the running maximum process of , where

Likewise, define

as the running minimum process of , where

etc. Continuing in an obvious way, we can again extend continuously to by setting

For

we then again obtain the conclusion of the above proposition, i.e.,

3. Heuristic derivation of the function

We now explain on an intuitive level how to come up with a candidate function that satisfies the smooth pasting conditions from Section 2 and leads to a process , whose -optimal portfolio keeps the positions in stock and bond constant as long as lies in the interior of (resp. in the setting of Remark 2.4).

To this end, suppose we start at with a portfolio such that the proportion of total wealth invested into stocks in terms of the ask price

| (3.1) |

lies on the buying side of the no-trade region.

First suppose that the Merton proportion lies in the interval . This implies that, in the model without transaction costs, the optimal holdings in bonds and in stocks are always strictly positive. We suppose (and shall later prove) that the same holds true under transaction costs. Then if starts a positive excursion from level at time , the processes , and remain constant. The fraction of stocks starts this positive excursion from , too, until reaches some level , where is positioned at the selling boundary of the no-trade region. At this time , the fraction of wealth held in stocks has evolved to

| (3.2) |

Now suppose that, during this time interval , the process is given by

for some -function that we now want to determine. Itô’s formula and (1.2) yield

The mean-variance ratio of the process is therefore given by

| (3.3) |

Let us now consider the fraction of wealth invested in the stock divided by the total wealth at time , if we evaluate the stock at price . We obtain

| (3.4) |

where is defined by

Note that remains constant as long as lies in the interior of the bid-ask spread , i.e., for . Indeed, the idea is to construct in such a way that the frictionless optimizer associated to only moves on the set .

Here comes the decisive argument. Merton’s rule (1.5) tells us that the -optimal portfolio for the (frictionless) process must have the following property: The ratio (3.4) of wealth invested in the stock divided by the total wealth must be equal to the mean-variance ratio (3.3). A short calculation shows that this equality is tantamount to the following ODE for :

| (3.5) |

We still need the corresponding boundary conditions. Since the proportion of wealth held in stocks started at the buying boundary at time , the shadow price must equal the higher ask price there, i.e. . Likewise, since the proportion of wealth held in stocks has moved to the selling boundary when the ask price reaches level , we must have such that coincides with the lower ask price . Since the boundary is not known a priori, we need some additional boundary conditions, which we can heuristically derive as follows. Since we want to remain in the bid-ask spread , the ratio must remain within as moves through . Therefore, its diffusion coefficient should tend to zero as approaches either or . Itô’s formula yields that the diffusion coefficient of is given by . Together with and , this implies that we should have and . These are precisely the smooth pasting conditions from Section 2.

Imposing the two boundary conditions , the general closed-form solution of the ODE (3.5) is given by

| (3.6) |

unless , which is a special case that can be treated analogously (cf. Lemma 4.3 below). For given , it remains to determine and such that and . This is equivalent to requiring and . Plugging (3.6) into the latter condition yields

| (3.7) |

To determine from the Merton proportion and the transaction costs , insert (3.6) and (3.7) into the remaining condition . We find that must solve

| (3.8) |

Once we have determined , this yields and, via (3.1) and (3.2), the lower resp. upper limits and for the fraction of total wealth held in stocks in terms of the ask price . It does not seem to be possible to determine in closed form from (3.8) as a function of . However, the above representation easily leads to fractional Taylor expansions in terms of for , and the lower resp. upper limits and for . This completes the heuristics for the case . As mentioned above, the case can be dealt with in an analogous way except for a different solution of the ODE for (see Lemma 4.3 below).

Now consider a Merton proportion . In this case, the -investor in the price process without transaction costs goes short in the bond, i.e., chooses and . We again suppose (and subsequently verify in Section 5) that this remains true in the presence of transaction costs. Then if starts a negative excursion from level at time , the processes , and remain constant. The fraction of stocks in turn starts a positive excursion from , until reaches some level , where is positioned at the higher selling boundary of the no-trade region (see Figure 2). The remaining arguments from above can now be carried through accordingly, by replacing with . Consequently, one ends up precisely in the setup of Remark 2.4.

Finally, consider the degenerate case . Then the ODE (3.5) for complemented with the boundary conditions already implies and . Since the other boundary condition and cannot hold in this case (except for ), we formally have . This means that the shadow price coincides with the ask price and the corresponding optimal fraction of wealth held in stock evaluated at price is constantly equal to one, since the lower and upper boundaries and both become for and . This is also evident from an economic point of view, since Merton’s rule (1.5) implies that the optimal strategy for without transaction costs consists of refraining from any trading after converting the entire initial endowment into stocks at time zero.

4. Existence of the candidates

To show that the heuristics from the previous section indeed lead to well-defined objects, we begin with the following elementary observations. Their straightforward but tedious proofs are deferred to Appendix Appendix. Proofs of Lemmas 4.1 and 4.2.

Lemma 4.1.

Fix , and let

Then there exists a unique solution to on if , on if , resp. on if .

For fixed and as in Lemma 4.1, we can now define the real number as motivated in the heuristics for .

Lemma 4.2.

Fix . Then for as in Lemma 4.1,

| (4.1) |

is well-defined and lies in if , resp. in if . Moreover, we have if resp. if .

Now we can verify by insertion that the candidate function has the properties derived in the heuristics above.

5. The shadow price process and its log-optimal portfolio

With Proposition 2.1 and the function from Lemma 4.3 at hand, we can now construct a shadow price and determine its -optimal portfolio. To this end, let be the function from Lemma 4.3. Then, for the process as defined in Section 2, Proposition 2.1 yields that

is an Itô process satisfying the stochastic differential equation

| (5.1) |

with drift and diffusion coefficients

Note that we have replaced in Proposition 2.1 with the expression provided by the ODE (4.3) from Lemma 4.3. Also notice that and are continuous and hence bounded on , and is also bounded away from zero.

For Itô processes with bounded drift and diffusion coefficients, the solution to the -optimal portfolio problem is well-known (cf. e.g. [17, Example 6.4]). This leads to the following result.

Theorem 5.1.

Fix and let the stopping times , and the process be defined as in Section 2. For the function from Lemma 4.3, set

Then the -optimal portfolio in the frictionless market with price process exists and is given by , and

as well as

The corresponding optimal fraction of wealth invested into stocks is given by

| (5.2) |

Proof.

By (5.1), is an Itô process with bounded coefficients. Since, moreover, is also bounded, Merton’s rule as in [17, Example 6.4] implies that the optimal proportion of wealth invested into stocks is given by

On the other hand, the adapted process is continuous and hence predictable. By definition,

| (5.3) |

For any , Itô’s formula and (5.3) now yield

on and likewise on . Therefore is self-financing. Again by (5.3), the fraction

of wealth invested into stocks when following coincides with the Merton proportion computed above. Hence is -optimal and we are done. ∎

In view of (5.2) and Lemma 4.3, it is optimal in the frictionless market with price process to keep the fraction of wealth in terms of invested into stocks in the interval . By definition of and , no transactions take place while moves in the interior of this no-trade region in terms of .

As was kindly pointed out to us by Paolo Guasoni, the no-trade region in terms of is symmetric relative to the Merton proportion . Indeed, after inserting , (4.2), and (4.1), rearranging yields that . Hence

| (5.4) |

From Theorem 5.1 we can now obtain that is a shadow price.

Corollary 5.2.

Proof.

First consider the case . In view of Proposition 2.1, takes values in the bid-ask spread . By Theorem 5.1, the -optimal portfolio for exists. Moreover, since only increases (resp. decreases) on (resp. ), the number of stocks only increases (resp. decreases) on (resp. ) by definition of . This shows that is a shadow price.

For , it follows from [17, Example 6.4] that the optimal strategy for the frictionless market transfers all wealth into stocks at time and never trades afterwards, i.e. and for all . Hence it is of finite variation, the number of stocks never decreases and only increases at time where . This completes the proof. ∎

If , Corollary 1.9 combined with Corollary 5.2 shows that is also growth-optimal for the bid-ask process . The corresponding fraction of wealth invested into stocks in terms of the ask price is given by

where we have used for the last equality. Hence, the fraction is always kept in the no-trade-region in term of . Note that this interval always lies in , since and by Lemmas 4.1 and 4.2.

For , the investor always keeps his entire wealth invested into stocks.

If , one cannot apply Corollary 1.9 directly. However, in the present setting a corresponding statement still holds, provided that the transaction costs are sufficiently small.

Lemma 5.3.

Fix and let be the -optimal portfolio for the frictionless market with price process from Theorem 5.1. Then there exists such that, for all , the portfolio is also growth-optimal for the bid-ask process .

Proof.

First note that by Lemma 4.2. Moreover, the function is increasing and maps to by Lemma 4.3. By (5.2), the fraction of wealth in terms of invested into stocks therefore takes values in the interval . Together with , this yields the estimate

| (5.5) |

By Proposition 6.1 below, there exists such that

Since is nonnegative, this shows that is admissible for the bid-ask process , if . The remainder of the assertion now follows as in the proof of Corollary 1.9 by combining the above estimate (5.5) with the obvious upper bound . ∎

If Lemma 5.3 is in force, the growth-optimal portfolio under transaction costs for also keeps the fraction of stocks in terms of the ask price in the interval . In particular, since and , this now entails always going short in the bond, i.e. both boundaries of the no-trade region lie in the interval .

5.1. The optimal growth rate

We now want to compute the optimal growth rate

| (5.6) |

where denotes the -optimal portfolio for the shadow price from Theorem 5.1 and the second equality follows from [17, Example 6.4]. In view of Corollary 1.9 resp. Lemma 5.3, the above constant coincides with the optimal growth rate for the bid-ask process .

It follows from the construction in Section 2 above that the process is a doubly reflected geometric Brownian motion with drift on the interval (resp. on for the case ). Therefore, an ergodic theorem for positively recurrent one-dimensional diffusions (cf., e.g., [3, Sections II.36 and II.37]) and elementary integration yield the following result.

Proposition 5.4.

Remark 5.5.

In the degenerate case , the optimal portfolio leads to . Hence and the optimal growth rate is given by as in the frictionless case.

6. Asymptotic expansions

Similarly to Janeček and Shreve [14] for the infinite-horizon optimal consumption problem, we now determine asymptotic expansions of the boundaries of the no-trade region and the long-run optimal growth rate.

6.1. The no-trade region

We begin with the following preparatory result.

Proposition 6.1.

For fixed and sufficiently small , the functions and have fractional Taylor expansions of the form

| (6.1) | ||||

| (6.2) |

where , and and are rational functions that can be algorithmically computed. (For , the quantity has to be read as .) The first terms of these expansions are

| (6.3) | ||||

| (6.4) | ||||

Proof.

By (4.1), the quantity can be written as , where is analytic at . (We will again suppress the dependence of and on in the notation.) We focus on , since the case is an easy modification.

Expanding the rational function in (4.1) around , and appealing to the binomial theorem (for real exponent), we find that the Taylor coefficients of

| (6.5) |

are rational functions of . An efficient algorithm for the latter step, i.e., for calculating the coefficients of a power series raised to some power, can be found in Gould [11]. Now we insert the series (6.5) into the equation , i.e., into

| (6.6) |

Performing the calculations (binomial series again), we find that the expansion of the right-hand side of (6.6) around starts with the third power of :

Dividing (6.6) by the series (whose coefficients are again computable) therefore yields an equation of the form

| (6.7) |

The series on the left-hand side is an analytic function evaluated at , with real Taylor coefficients Its coefficients are computable rational functions of . Moreover, the first coefficient is non-zero. Hence we can raise (6.7) to the power to obtain

where the power series represents again an analytic function. By the Lagrange inversion theorem (see [8] or [18, § 4.7]), is an analytic function of :

| (6.8) |

This is the expansion (6.2). To see that the coefficients are of the announced form, note that Lagrange’s inversion formula implies that the coefficients in (6.8) are given by

where the operator extracts the -th coefficient of a power series. Since the are rational functions of , and

the expansion of is indeed of the form stated in the proposition.

Once the existence of expansions of and in powers of is established, one can also compute the coefficients by inserting an ansatz

| (6.9) |

into the equations

| (6.10) | ||||

| (6.11) |

and then comparing coefficients (preferably with a computer algebra system). Implementing this seems somewhat easier (but less efficient) than implementing the preceding proof. To give some details, let us look at the expression in the first line of (4.2). Note that, by the binomial theorem (for real exponent), the coefficients of

can be expressed explicitly in terms of the unknown coefficients . Performing the convolution with the ansatz for , and continuing in a straightforward way (multiplying by constant factors, and appealing once more to the binomial series, this time with exponent ), we find that

| (6.12) |

Now insert the ansatz (6.9) into the right-hand side of the first equation (6.10):

| (6.13) |

Comparing coefficients in (6.12) and (6.13) yields an infinite set of polynomial equations for the and . Proceeding analogously for the equation (6.11) yields a second set of equations. It turns out that the whole collection can be solved recursively for the coefficients and . Along these lines the coefficients in (6.3) and (6.4) were calculated.

With the expansions of and at hand, we can now determine the asymptotic size of the no-trade region.

Corollary 6.2.

For fixed , the lower and upper boundaries of the no-trade region in terms of the ask price have the expansions

and

respectively. The size of the no-trade region in terms of satisfies

Note that there is no -term in these expansions. We also stress again that more terms can be obtained, if desired, by using the machinery of symbolic computation.

Proof.

Insert the expansions of and found in Proposition (6.1) into and . A straightforward calculation, using the binomial series and amenable to computer algebra, then yields the desired expansions. ∎

6.2. The optimal growth rate

Proposition 6.3.

Suppose that . As , the optimal growth rate has the asymptotics

| (6.14) |

Note that the - as well as the -term vanish in the above expansion. Moreover, the preceding result can again be extended to a full expansion of in powers of .

6.3. Comparison to Janeček and Shreve (2004)

In order to compare our expansions to the asymptotic results of Janeček and Shreve [14], we rewrite them in terms of a bid-ask spread . As explained in the first footnote in the introduction, we set

Therefore also follows a Black-Scholes model with drift rate and volatility and the fraction of wealth invested into stocks in terms of is given by

where we have again used for the last equality. This yields the expansions

for the lower boundary and

for the upper boundary of the no-trade-region in terms of , respectively. The size of the no-trade region satisfies

Comparing these expansions to the results of [14] for the infinite-horizon consumption problem (specialized to logarithmic utility), we find that the leading -terms coincide. Hence, the relative difference between the size of the no-trade region with and without intermediate consumption goes to zero as .

The higher order terms for the consumption problem are unknown. However, [14] argue heuristically that – in second order approximation – the selling intervention point is closer to the Merton proportion than the buying intervention point. They also point out that, on an intuitive level, this is due to the fact that consumption reduces the position in the bank account. In line with this, the present setup without consumption leads to symmetric second order -terms, which in fact vanish. However, note that the no-trade regions in terms of the mid-price resp. the ask price are only symmetric up to order , unlike the perfectly symmetric no-trade region in terms of the shadow price (cf. Equation (5.4) above).

An extension of the present approach to the infinite-horizon consumption problem as well as to power utility is left to future research.

Appendix. Proofs of Lemmas 4.1 and 4.2

of Lemma 4.1.

First consider the case . By insertion, we find . Moreover, for , such that a solution to exists on by the intermediate value theorem. We now show that it is unique.

Differentiation yields and . On the other hand, we find on for some .

Now notice that is increasing on . Indeed, we have

| (6.15) |

for as in Equation (4.1) and

By tedious calculations or using Cylindrical Algebraic Decomposition [4] (henceforth CAD), it follows that and in turn on .

Consequently, on and on for some . Combining this with and for , we find that there exists such that on and on . Since , this implies that any solution to must lie on and hence is unique, because is strictly increasing there.

Now let . Then is continuous on and as above. Moreover, the first term of grows like for , whereas the second one grows like . Since for , this implies that for . Hence a solution to exists on by the intermediate value theorem, and it remains to show that it is unique.

To see this, first notice that again, either by tedious calculations or using CAD, the function from above turns out to be strictly positive, this time on . The remainder of the assertion now follows as above.

Next, let . In this case, and for . Hence a solution to exists on by the intermediate value theorem. We now show its uniqueness. Indeed,

is strictly positive on . Since and for , this implies that there exists such that on and on . Combined with and for , this shows that there exists such that on and on . Since , any solution to must therefore lie in and is unique, since is strictly increasing there.

Finally, consider the case . Then the third derivative increases on . This time is negative (by CAD), but so is the fraction in front of it in (6.15). We can now reason as above, so that the proof is complete. ∎

of Lemma 4.2.

For , this follows immediately from Lemma 4.1, which yields and

For , one easily shows by CAD that

hence is well-defined. Moreover, is positive for , since and .

Finally, let . Then clearly , and it remains to show that . For , we have

Hence, by (4.1),

We have to show that for . By a discussion similar to the proof of Lemma 4.1, the function has a unique maximum at

and the value of at satisfies

The last quantity has a negative derivative w.r.t. , and equals for . Hence it is smaller than for , so that , which completes the proof. ∎

References

- [1] Barles, G., and Soner, H. M. Option pricing with transaction costs and a nonlinear Black-Scholes equation. Finance Stoch. 2, 4 (1998), 369–397.

- [2] Barlow, M. T. Inequalities for upcrossings of semimartingales via Skorohod embedding. Z. Wahrsch. Verw. Gebiete 64, 4 (1983), 457–473.

- [3] Borodin, A. N., and Salminen, P. Handbook of Brownian motion—facts and formulae, second ed. Probability and its Applications. Birkhäuser Verlag, Basel, 2002.

- [4] Collins, G. E. Quantifier elimination for real closed fields by cylindrical algebraic decomposition. In Automata theory and formal languages (Second GI Conf., Kaiserslautern, 1975). Springer, Berlin, 1975, pp. 134–183. Lecture Notes in Comput. Sci., Vol. 33.

- [5] Cvitanić, J., and Karatzas, I. Hedging and portfolio optimization under transaction costs: a martingale approach. Math. Finance 6, 2 (1996), 133–165.

- [6] Dai, M., and Yi, F. Finite-horizon optimal investment with transaction costs: a parabolic double obstacle problem. J. Differential Equations 246, 4 (2009), 1445–1469.

- [7] Davis, M. H. A., and Norman, A. R. Portfolio selection with transaction costs. Math. Oper. Res. 15, 4 (1990), 676–713.

- [8] de Bruijn, N. G. Asymptotic methods in analysis, third ed. Dover Publications Inc., New York, 1981.

- [9] Dumas, B., and Luciano, E. An exact solution to a dynamic portfolio choice problem under transaction costs. J. Finance 46, 2 (1991), 577–595.

- [10] Gerhold, S., Muhle-Karbe, J., and Schachermayer, W. Asymptotics and duality for the Davis and Norman problem. Preprint, 2010.

- [11] Gould, H. W. Coefficient identities for powers of Taylor and Dirichlet series. Amer. Math. Monthly 81 (1974), 3–14.

- [12] Guasoni, P., Rásonyi, M., and Schachermayer, W. Consistent price systems and face-lifting pricing under transaction costs. Ann. Appl. Probab. 18, 2 (2008), 491–520.

- [13] He, H., and Pearson, N. D. Consumption and portfolio policies with incomplete markets and short-sale constraints: the infinite-dimensional case. J. Econom. Theory 54, 2 (1991), 259–304.

- [14] Janeček, K., and Shreve, S. E. Asymptotic analysis for optimal investment and consumption with transaction costs. Finance Stoch. 8, 2 (2004), 181–206.

- [15] Kallsen, J., and Muhle-Karbe, J. On using shadow prices in portfolio optimization with transaction costs. Ann. Appl. Probab. 20, 4 (2010), 1341–1358.

- [16] Karatzas, I., Lehoczky, J. P., and Shreve, S. E. Optimal portfolio and consumption decisions for a “small investor” on a finite horizon. SIAM J. Control Optim. 25, 6 (1987), 1557–1586.

- [17] Karatzas, I., Lehoczky, J. P., Shreve, S. E., and Xu, G. Martingale and duality methods for utility maximization in an incomplete market. SIAM J. Control Optim. 29, 3 (1991), 702–730.

- [18] Knuth, D. E. The Art of Computer Programming, third ed., vol. 2. Addison Wesley, Reading MA, 1998.

- [19] Kramkov, D., and Schachermayer, W. The asymptotic elasticity of utility functions and optimal investment in incomplete markets. Ann. Appl. Probab. 9, 3 (1999), 904–950.

- [20] Liu, H., and Loewenstein, M. Optimal portfolio selection with transaction costs and finite horizons. Rev. Financ. Stud. 15, 3 (2002), 805–835.

- [21] Merton, R. C. Lifetime portfolio selection under uncertainty: the continuous-time case. Rev. Econ. Statist 51, 3 (1969), 247–257.

- [22] Pliska, S. R. A stochastic calculus model of continuous trading: optimal portfolios. Math. Oper. Res. 11, 2 (1986), 370–382.

- [23] Rogers, L. C. G. Why is the effect of proportional transaction costs ? In Mathematics of finance, vol. 351 of Contemp. Math. Amer. Math. Soc., Providence, RI, 2004, pp. 303–308.

- [24] Shreve, S. E., and Soner, H. M. Optimal investment and consumption with transaction costs. Ann. Appl. Probab. 4, 3 (1994), 609–692.

- [25] Taksar, M., Klass, M. J., and Assaf, D. A diffusion model for optimal portfolio selection in the presence of brokerage fees. Math. Oper. Res. 13, 2 (1988), 277–294.

- [26] Whalley, A. E., and Wilmott, P. An asymptotic analysis of an optimal hedging model for option pricing with transaction costs. Math. Finance 7, 3 (1997), 307–324.