Revenue Optimal Auction for Single-Minded Buyers

Abstract

We study the problem of characterizing revenue optimal auctions for single-minded buyers. Each buyer is interested only in a specific bundle of items and has a value for the same. Both his bundle and its value are his private information. The bundles that buyers are interested in and their corresponding values are assumed to be realized from known probability distributions independent across the buyers. We identify revenue optimal auctions with a simple structure, if the conditional distribution of any buyer’s valuation is nondecreasing, in the hazard rates ordering of probability distributions, as a function of the bundle the buyer is interested in. The revenue optimal auction is given by the solution of a maximum weight independent set problem. We provide a novel graphical construction of the weights and highlight important properties of the resulting auction.

1 Introduction

Consider buyers competing for a certain set of items offered by a seller. A buyer has a value for each combination of the items (henceforth referred to as a bundle) that he is interested in. This is the maximum price that he is willing to pay for the bundle. The seller’s objective is to maximize his revenue from the sale. If the seller knew these values exactly, he could maximize his revenue by simply finding an allocation of the items among the buyers that has the maximum total value, and charging each buyer the exact value of the bundle allocated to him. However, the values that the buyers have for different bundles are their private information; the seller has imperfect information about these values. The seller’s task is complicated further by the strategic behavior of the buyers; a buyer might misreport the values of the bundles he is interested in, if it is beneficial for him to do so. Combinatorial auctions (henceforth CAs) offer a solution. CAs allow buyers the freedom to compete for any bundle of items and provide them incentives to report their private values truthfully. The allocation and the payments are determined by the competition among the buyers. However, the inherent problems of CAs limit their appeal.

Often there are complementarities among the items - a buyer can have a higher value for a bundle as a whole than the sum of values of the parts of the bundle. Different buyers may have different forms of complementarity. Because of complementarity, allocation of items in a CA requires solving a hard combinatorial optimization problem; a naive implementation can lead to the exposure problem for the winners - a winner might end up getting only a part of his desired bundle, while still paying a high price for it. Moreover, the goal of revenue maximization (referred to as optimality) is very different from the much studied goal of social welfare maximization (referred to as efficiency) in auction theory, e.g., the VCG mechanism [1, 2, 3]. Theoretical results on revenue maximization are known only under simple settings, e.g., [4, 5, 6]. Characterizing revenue optimal CAs in full generality with multiple buyers, multiple items, and different values for the different bundles, still remains a challenging open problem, even if the complexity considerations are ignored.

This paper aims to address the issues of (1) dealing with complementarity, and (2) maximizing revenue, for CAs. The key to designing CAs with desirable properties is to understand and handle complementarity among the items. An extreme case of complementarity is when buyers are single minded [7]. Here, each buyer is interested only in a specific bundle and has a value for the same. Any allocation of items to a buyer that does not contain his desired bundle has zero value for him. Both the bundle that a buyer is interested in and its value are his private information. CA problems with single-minded buyers are more tractable than if buyers have general valuations. While the single-minded buyers model might appear as a simplifying assumption, no general result on revenue maximization is known even for this extreme case. Here a buyer has two dimensions for misreporting his preference - the bundle he is interested in, and the value of the bundle. Most of the existing literature on revenue optimal auctions studies problems which are one dimensional - a buyer has only one real number for misreporting his preference, e.g., Myerson’s single item auction [4], the single-parameter buyers model described in [5], and single-minded buyers with known bundles111Single-minded buyers with known bundles is also an instance of the single-parameter buyers. [8]. Thus, the single-minded buyer model can be thought of as an initial step towards solving the general CA problems. Also, see [7] for some real examples where buyers are single minded. Hence, we focus on the CAs with single-minded buyers.

In addition, we take a departure from the continuous variable models of economics and assume that the set of possible values that a buyer can have for his bundle is finite. While working with finite valuation sets is clearly relevant from the implementation point of view, it is interesting in its own right; e.g., we show later in this paper that the revenue equivalence result of [4] does not hold true when the valuation sets are finite. A related work was done by [9] where a Bayesian optimal auction, when buyers’ valuation sets are finite, is characterized. However, [9] deals only with single item auctions.

We make the following contributions in this paper. We modify and extend the framework of [9] for multiple item auctions with single-minded buyers. We then find a sufficient condition under which a revenue optimal auction can be characterized for single-minded buyers. This sufficient condition is the monotonicity of the conditional distribution of any buyer’s valuation, in the hazard rate ordering, as a function of the bundle the buyer is interested in. An interpretation of this condition is as follows: if there are two bundles where one contains the other, then the larger bundle is likely to have a higher value. Such monotonicity property is intuitive for single-minded buyers. Such monotonicity property is intuitive for single-minded buyers. A similar hazard rate ordering condition appears in [10] in the context of dynamic knapsack problem. However, [10] (as well as [8]) assumes that the distributions also satisfy Myerson’s nonintuitive regularity assumption [4]. An important contribution of our paper is to show that such assumption is unnecessary. We present an algorithm for optimal auction as a solution of a maximum weight independent set problem, where weights are an appropriate mapping of buyers’ valuations, called virtual valuations. We also provide a novel graphical construction of the virtual valuations.

2 Model and Notation

Consider buyers competing for items that a seller wants to sell. The set of buyers is denoted by , and the set of items for sale is denoted by . Buyers are single minded - each buyer is interested only in a specific bundle and has a value for any bundle such that , while he has zero value for any other bundle. Here denotes the power set of . Notice that single-minded buyers enjoy free disposal of the items. We refer to the tuple as the type of buyer . The type of a buyer is known only to him and constitutes his private information.

For each buyer , the seller and the other buyers have imperfect information about his type; they describe the bundle that buyer is interested in by a random set , and its value by a discrete random variable . The random set takes values from the collection , where is the collection of all bundles that buyer can possibly be interested in. The random variable is assumed to take values from the set of cardinality , where . The joint probability distribution of and is common knowledge. The probability that is denoted by , and conditioned on , the probability that is equal to is denoted by ; i.e., , and . Assume that and for all , , and . Note that can be interpreted as a specific realization of the random variables . Let be the random vector describing the type of buyer . Random vectors are assumed to be independent222This is referred to as the independent private value model. It is a fairly standard model in auction theory..

Denote a typical reported type (henceforth referred to as a bid) of a buyer by , where and . Define the vector of bids as , where is the vector of reported bundles, and is the vector of reported values. The seller can only allocate the items to a set of buyers whose reported bundles are disjoint. Given a vector of bundles , define as follows:

| (1) |

This is the collection of all feasible allocations; i.e., the collection of all subsets of buyers who can be allocated their respective bundles simultaneously. Trivially, and is downward closed; i.e., if and , then .

Define , , and . We use and interchangeably. Let and . We use the standard game theoretic notation of and . Similar interpretations are used for , , , , , and . Henceforth, in any further usage, , , and are always in the sets , , and respectively; and , , and are always in the sets , , and respectively.

3 Revenue Optimal Auction

In this section, we formally describe the optimal auction problem, formulate the objective and the constraints explicitly, and provide an optimal algorithm for solving the problem. We will be focusing only on the auction mechanisms where buyers are asked to report their types directly (referred to as direct mechanism). By the revelation principle333Revelation principle says that, given a mechanism and a Bayes-Nash equilibrium (BNE) for that mechanism, there exists a direct mechanism in which truth-telling is a BNE, and allocation and payment outcomes are same as in the given BNE of the original mechanism. [4], the restriction to direct mechanisms is without any loss of optimality.

3.1 Characterization

An auction mechanism is specified by an allocation rule , and a payment rule . Given a bid vector , the allocation rule is a probability distribution over the power set of . For each , is the probability that the set of buyers get their reported bundles simultaneously. The payment rule is defined as , where is the payment (expected payment in case of random allocation) that buyer makes to the seller when the bid vector is . Let be the probability that buyer gets his reported bundle when the bid vector is ; i.e,

| (2) |

Given that the type of a buyer is , and the bid vector is , the payoff (expected payoff in case of random allocation) of the buyer is:

| (3) |

So buyers are assumed to be risk neutral and have quasilinear payoffs (a standard assumption in auction theory). The mechanism and the payoff functions induce a game of incomplete information among the buyers. We use Bayes-Nash equilibrium (BNE) as the solution concept. The seller’s goal is to design an auction mechanism to maximize his expected revenue at a BNE of the induced game. Again, using the revelation principle, seller can restrict only to the auctions where truth-telling is a BNE (referred to as incentive compatibility) without any loss of optimality.

For the above revenue maximization problem to be well defined, assume that the seller cannot force the buyers to participate in an auction and impose arbitrarily high payments on them. Thus, a buyer will voluntarily participate in an auction only if his payoff from participation is nonnegative (referred to as individual rationality). In addition, the auction mechanism that the seller uses must always produce feasible allocations; i.e., for any bid vector, the set of winners must have disjoint bundles. The seller too is assumed to have free disposal of the items and may decide not to sell some or all items for certain bid vectors.

The idea now, as in [4], is to express incentive compatibility, individual rationality, and feasible allocations as mathematical constraints, and formulate the revenue maximization objective as an optimization problem under these constraints. To this end, for each , , and , define the following functions:

| (4) |

| (5) |

Here, is the expected probability that buyer gets his bundle given that he reports his type as while everyone else is truthful. The expectation here is over the type of everyone else; i.e., over . Similarly, is the expected payment that buyer makes to the seller. The constraints can be expressed mathematically as follows

-

1.

Feasible allocation (FA): For any and ,

(6) -

2.

Incentive compatibility (IC): For any , , , and ,

(7) Notice that, given , and , the left side of (7) is the payoff of buyer from reporting his type truthfully, assuming everyone else is also truthful, while the right side is the payoff from misreporting his type to .

-

3.

Individual rationality (IR): For any , , and ,

(8)

Under IC, all buyers report their true types. Hence, the expected revenue that the seller gets is . The expectation here is over the distribution of the random vector . Thus, the seller’s optimization problem is given by:

Optimal auction problem (OAP)

| (9) |

Instead of solving the OAP, we solve a modified problem obtained by relaxing the IC constraint. We then find a sufficient condition under which the solution of the modified problem is also the solution of OAP. The relaxed IC constraint is obtained by assuming that buyers report their bundles truthfully, or equivalently, the bundles that the buyers are interested in are known to everyone. Mathematically, the relaxed IC constraint is:

| (10) |

for any , , and . The modified optimization problem is given by:

Modified optimal auction problem (MOAP)

| (11) |

For the MOAP, using the relaxed IC constraint (10) and the IR constraint (8), we relate the expected payment of a buyer to his expected allocation probability . The framework used is similar to [9]. We first define the virtual-valuation function, , of buyer as:

| (12) |

Definition 1.

The virtual-valuation function is said to be regular if for all , and .

Proposition 1.

Let be an allocation rule and and be obtained from by (2) and (4). A payment rule satisfying the relaxed IC constraint (10) and the IR constraint (8) exists for if and only if for all , , and . Given such and a payment rule satisfying the IC and IR constraints, the seller’s revenue satisfies:

| (13) |

Moreover, a payment rule achieving this bound exists and any such satisfies:

for all , , and , where we use the notational convention .

Proof.

The proof is given in Appendix A. ∎

3.2 Solution of the MOAP

We now describe an algorithm for finding a solution of the MOAP. As mentioned in Section 1, this is related to [5], [8], and [9].

From (2), for all and , we have:

| (14) |

Proposition 1 and (14) suggest that a solution of the MOAP can be found by selecting the allocation rule that assigns nonzero probabilities only to the set of buyers in with the maximum total virtual valuations for each bid vector . If all ’s are regular, then it can be verified that such an allocation rule satisfies the monotonicity condition on the ’s needed by Proposition 1. However, if ’s are not regular, the resulting allocation rule would not necessarily satisfy the required monotonicity condition on the ’s. This problem can be remedied by using another function, , called the monotone virtual valuation (henceforth MVV), constructed graphically as follows.

For all , , and , define:

| (15) |

where we use the notational convention of , , and . Then, is given by the slope of the line joining the point to the point ; i.e.,

| (16) |

Find the lower convex hull of the points . Let be the point on this convex hull corresponding to . Then, is defined as the slope of the line joining the point to the point ; i.e.,

| (17) |

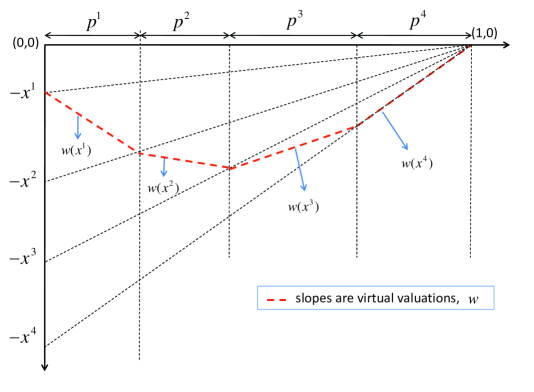

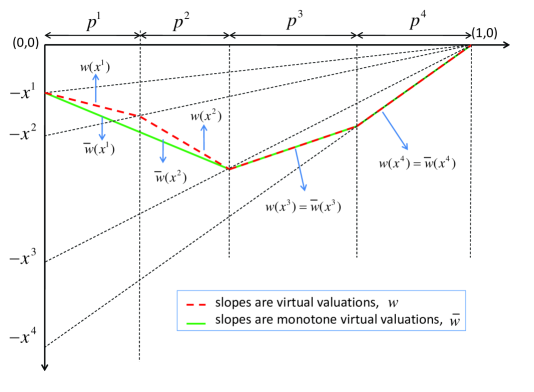

To find the points graphically, draw vertical lines separated from each other by distances . For each , join the point on the y-axis to the x-axis at (sum of probabilities) and call such line as line . The intersection of line with y-axis is the point . The intersection of line with the first vertical line is the point . Similarly, the intersection of the line with the second vertical line is the point , and so on. Notice that if is regular, is equal to .

Figure 1(a) shows this construction for a typical random variable taking four different values with corresponding probabilities , where we have dropped the subscripts corresponding to the buyers and the bundle information for the ease of notation. This is the case of virtual valuation being regular. Since the slopes of the graph are nondecreasing, the function graphed is convex. In Figure 1(b), , and hence, the virtual-valuation function is not regular. Here, the the lower convex hull of the points ’s is taken. The slopes of individual segments of this convex hull give the MVV function . This is equivalent to replacing and by their weighted mean; i.e., .

The following lemma that is a straightforward consequence of the construction of as the slopes of a convex function:

Lemma 1.

for all , , and .

The next proposition establishes the significance of the allocation rule obtained by using ’s.

Proposition 2.

Proof.

The maximum weight algorithm (henceforth MWA) for the MOAP is described in Algorithm 1. The set is the collection of all feasible subsets of buyers with maximum total MVVs for the given bid vector . Since is downward closed and , no buyer with is included in the set of winners . In step of the MWA, for each , is computed recursively by treating as the input bid vector and repeating steps .

Given a bid vector :

-

1.

Compute for each .

-

2.

Take to be any probability distribution on the collection defined as:

Obtain the set of winners by sampling from according to .

- 3.

Proposition 3.

The MWA gives a solution of the MOAP.

Proof.

Let be the solution given by the MWA and let and be obtained from by (2) and (4). Since , satisfy the FA constraint.

The MWA can be interpreted as follows. Given a bid vector , construct a graph with a node for each buyer , and an edge if . Thus, is the conflict graph of the buyers, where an edge denotes that buyers corresponding to its endpoints cannot be allocated their bundles simultaneously. The collection of all independent sets of this graph is precisely . Let be the weight of node . Then the set of winners is a maximum weight independent set of this graph.

In the subsequent discussion, we will be using the MWA with a deterministic tie-breaking rule (henceforth deterministic MWA). Here, in step of the MWA, the set of winners is selected by a deterministic rule. For example, the set of winners can be the first allocation set in under the lexicographic order defined over the set of all allocations .

Let be the solution given by the deterministic MWA. Then for all , , and . Also, from the proof of Proposition 3, is nondecreasing in , keeping and constant. This, along with the payment rule in step of MWA, implies that a winner pays the price that is the minimum value he needs to report to still win, keeping his bundle and the bids of everyone else fixed.

3.3 Solution of the OAP

We now give a sufficient condition under which a solution of MOAP is also the solution of OAP. To this end, define the hazard rate ordering [11] on two random variables as follows:

Definition 2.

A nonnegative random variable is said to be smaller than a nonnegative random variable under the hazard rate order, denoted by , if and have the same support, and

| (19) |

for all such that , and are in the common support of and .

Notice that, if , then is also smaller than under the first order stochastic dominance (FOSD) [11]. In the FOSD, (19) is replaced by simply for all in the common support of and . Hence, the hazard rate order is stricter than the FOSD.

It is natural to expect that if there are two bundles where one contains the other, then the larger bundle is likely to have a higher value. This is precisely captured by Assumption 1 below.

Assumption 1.

For any with , the conditional random variable is smaller than the conditional random variable under the hazard rate order. Equivalently, for all , such that , and ,

| (20) |

Proposition 4.

Let be such that . Then under Assumption 1, for .

Proof.

The proof is given in Appendix C. ∎

Proposition 5.

A deterministic MWA gives a solution of the OAP under Assumption 1.

Proof.

Notice that OAP and MOAP differ only in their constraints, and the relaxed IC constraint (10) is a subset of the IC constraint (7). Hence, we only need to verify that the solution given by the deterministic MWA satisfies the IC constraint. We show that, under the deterministic MWA, the truthful declaration of the types is a weakly dominant strategy for the buyers.

Let the bid vector be . Based on the reported bundles , the conflict graph is constructed. The weights of the nodes of are the MVVs for the bid vector . Consider a buyer . Let his true type be . Since buyers are single minded, it can be assumed that , otherwise the payoff from misreporting a bundle can be at most zero, which is less than or equal to the payoff from reporting the bundle truthfully. Also, if buyer does not get his bundle by bidding (and hence payoff equal to zero) then truthful bidding (payoff at least zero) cannot be worse. Hence, we only need to analyze the case where buyer wins by bidding such that . Since buyer is a winner, there is a maximum weight independent set (henceforth MWIS) in that contains node . Because of a deterministic tie-breaking rule, buyer pays the minimum value he needs to report to win. This is his value at which the value of the MWIS containing node exceeds the value of all MWIS not containing node . Now, if instead buyer reports , it can result in deletion of some edges incident on node in , but cannot add any new edge. At the same time, from Proposition 4, the weight of node (or the MVV of buyer ) can possibly increase but cannot decrease. Hence, the value of the MWIS containing node can possibly go up but cannot decrease, while the value of the MWIS not containing node does not change. Buyer still wins and the payment if he declares cannot be more than what he pays when he declares . Thus, truthful reporting of the bundle is a weakly dominant strategy.

We can now assume that buyer reports his bundle truthfully. Since the price that he pays only depends on his reported bundle and the bids of everyone else, but not on his reported value, truthful reporting of the value is a weakly dominant strategy. This completes the proof. ∎

4 Discussion

In this section, we highlight some of the important properties of the optimal auction characterized in Section 3.

-

(a)

Some special cases: A special case of interest is when the bundle that a buyer is interested in is known to everyone. This is equivalent to containing only one bundle. Here, OAP and MOAP are identical. More generally, if is such that no bundle in is a superset of another bundle in , then a buyer will report his bundle truthfully, and hence OAP and MOAP are identical. If and are independent then Assumption 2 trivially holds true. In all these cases, an optimal auction is given by the deterministic MWA.

Auctions with identical items can be thought of as single minded buyers with substitutes and is closely related to the case with known bundles. Here, the seller has identical items for sale. A buyer is interested in any one of the items. The analysis of Section 3 is easily extended to this case by simply defining the collection of feasible allocations as:

This is the collection of all subsets of with cardinality less than or equal to . The optimal auction is given by the MWA with replaced by .

-

(b)

Continuous OAP: The results of this paper easily extend to the continuous version of the OAP where buyers’ valuation sets are continuous. Here, is a nonnegative interval of , and the random variable is specified by the probability density function (pdf) for all . Let be the corresponding cumulative distribution (CDF) function. Denote the conditional pdf and conditional CDF of , given , by and respectively. Then the MWA again gives the solution of the continuous OAP after the following modifications:

The continuous OAP, however, has one key difference from the discrete OAP. In the continuous case, given an allocation rule , under the IC and relaxed IR constraints, the expected payment that a buyer makes is determined up to an additive constant (the revenue equivalence principle of [4]); i.e., is a known function of . However, in the discrete case, is fixed to within an interval of values. The expected revenue is maximized by taking the upper value of this interval, and the optimal auction in Section 3 is characterized this way.

-

(c)

Reserve prices: Given a bid vector , no buyer with is included in the set of winners, , by the MWA. Depending on the tie-breaking rule, a buyer with may or may not be included in the set of winners. Assume that only buyers with are considered. Since , the seller equivalently sets reserve prices for each buyer and does not sell any item to a buyer if his reported value is less than his reserve price. The reserve price for a buyer depends only on the probability distribution of his valuations, conditioned on his bundle, and might be different for different buyers. Let be the reserve price for a buyer as a function of his bundle. If , then for . As ’s are the slopes of the lines joining the points , we get . From the property of convex hull, . Thus, using the definition of ’s, an equivalent formulation of the reserve price is:

(21) Graphically, this corresponds to the y-intercept of the line through the lowermost point of the graph and the point ( in Figures 1(a) and 1(b)).

-

(d)

Implementation complexity: The optimal allocation rule for auctions with single-minded buyers requires finding a maximum weight independent set in the conflict graph. This problem is NP-hard. However, similar to [7], a greedy scheme can be obtained that is easy to implement, and achieves approximation555Any approximation better than is again NP-Hard. of the revenue generated by the deterministic MWA. The greedy scheme allocates the bundles to the buyers according to the order induced by the normalized virtual valuations . The price charged to a buyer who gets his desired bundle is the minimum value he needs to report to still win, keeping his bundle and the bids of everyone else fixed.

-

(e)

On the hazard rate order assumption: In the absence of Assumption 1, the solution given by the MWA (under any tie-breaking rule) need not satisfy the IC constraint. The following example shows this. Consider two buyers and two items . Buyer is interested in bundle and has value for it. Buyer can be interested in bundle or bundle , each with probability . Conditioned on buyer being interested in bundle , his values can be or $, each with probability . Conditioned on him being interested in bundle , his values can be or , with probabilities and respectively. Clearly, Assumption 1 does not hold true for buyer . The virtual-valuation function for buyer is . For buyer , the virtual-valuation function is , , , and . Under the MWA, if buyer bids he loses, and if he bids then he gets bundle at the price . However, if buyer bids or then he gets bundle at the price . Thus, if the true type of buyer is , he will misreport it to or .

5 Conclusions

We characterized a Bayesian revenue optimal multiple items auction with single-minded buyers under a partial hazard rate order assumption on the conditional distribution of any buyer’s valuation. This assumption is intuitive for single-minded buyers and imply that the larger bundle is likely to have higher value. The resulting auction has a simple structure - the set of winners are the maximum weight independent set of the conflict graph of the buyers, and the payment made by a winner is the minimum value he needs to report to win. Single-minded buyers have two dimensional private information. The contributions here provide a step towards understanding optimal auction problems where buyers’ private information is multidimensional.

Appendix A Proof of Proposition 1

The proof of Proposition 1 follows from the lemmas given below.

Lemma 2.

Under the relaxed IC constraint (10), for all , , and .

Proof.

The proof follows easily from (10) by considering the case where the true value of the bundle for buyer is but he reports instead, and the case where the true value is but he reports instead. ∎

Lemma 3.

Proof.

Trivially, the relaxed IC constraint (10) implies (22). To show that (22) implies (7), first consider the case . Using (22),

where the first inequality follows from Lemma 2 and . Thus, (10) holds for . Similarly, starting with the left inequality of (22), it can easily be shown that (22) implies (10) for , and the proof is complete. ∎

Lemma 4.

Proof.

Lemma 3 and the IR constraint easily imply:

| (25) |

where . Using (25),

where the second last equality is obtained by rearranging the terms and using (12). It is straightforward to verify that the above holds with equality for given by (24). The final step is show that this particular choice of satisfies the relaxed IC and the IR constraints. The relaxed IC constraint is trivially satisfied using Lemma 3. The IR constraint is satisfied since:

∎

Appendix B Proof of Proposition 2

To prove (18), it is sufficient to show that:

| (26) |

Similarly,

| (29) |

Since is the point corresponding to on the convex hull of , we must have , , and . This, along with , and (B)-(29), gives:

Let be the allocation rule that maximizes for each bid vector , subject to the FA constraint. Given , if are such that , for , and (recall that ), then lies on the line joining and . Hence, for ; i.e., is constant in this interval. This in turn implies that if such that , then is constant in the interval , given and . Let and be obtained from by (2) and (4). Then is also constant in the interval . Moreover, from the construction of ,

Thus, for all and , we have:

| (30) |

where the last equality follows from (27). This completes the proof of the equality.

Appendix C Proof of Proposition 4

Define . Notice that this is the left continuous cumulative distribution function (CDF) of the conditional random variable . We start with the following lemmas:

Lemma 5.

For all and , for , and .

Proof.

If , then this is trivially true. Given , if are such that , for , and , then is constant in the interval . Hence, This completes the proof of inequality. Also, , for any . Thus, the convex hull of points always contains the line connecting to (recall the construction of in Section 3.2). Hence, , and the proof is complete. ∎

Lemma 6.

For all , , and ,

| (31) |

with the convention that if more than one value of minimizes the maximum, then the largest such is selected.

Proof.

From (15), for any ,

| (32) |

Let for . Consider the plot of points ’s. The convex hull of the points is same as that of the points . Note that, from the proof of Lemma 5, the convex hulls of the points and differ from each other by just the line segment connecting to . Hence, ’s for are obtained as the slopes of the convex hull of points ’s. Fix for some . Call the line from to the line for . Given and , consider the line through the point with slope , and let be the point of intersection of this line with the line for . Then, is the horizontal distance of from the vertical line at . Taking the maximum over corresponds to the point which is the intersection of the line of slope that is tangent to the plot, and the line for . Then the minimizing is the slope of the tangent at the point where the convex hull of intersects the line for , and hence, same as . If there is more than one intersection point, the largest is selected. From Lemma 5, the minimum is achieved by . This completes the proof. ∎

For , define:

Notice that is nonincreasing in .

Lemma 7.

Let be such that . Then under Assumption 1, is nonincreasing in .

Proof.

Fix . We need to prove that:

Under Assumption 1, is nonincreasing in . Let and denote the values of achieving the maximum in the definition of and respectively. Clearly, and . If ,

On the other hand, if ,

In either case, the required inequality is proved. ∎

References

- [1] E. H. Clarke, “Multipart pricing of public goods,” Public Choice, vol. V11, no. 1, pp. 17–33, 1971.

- [2] T. Groves, “Incentives in teams,” Econometrica, vol. 41, no. 4, pp. 617–631, 1973.

- [3] W. Vickrey, “Counterspeculation, auctions, and competitive sealed tenders,” The Journal of Finance, vol. 16, no. 1, pp. 8–37, 1961.

- [4] R. Myerson, “Optimal auction design,” Mathematics of Operations Research, vol. 6, no. 1, pp. 58–73, 1981.

- [5] J. D. Hartline and A. R. Karlin, “Profit maximization in mechanism design,” in Algorithmic Game Theory (N. Nisan, T. Roughgarden, E. Tardos, and V. V. Vazirani, eds.), ch. 13, pp. 331–361, New York, NY, USA: Cambridge University Press, 2007.

- [6] M. Armstrong, “Optimal multi-object auctions,” The Review of Economic Studies, vol. 67, no. 3, pp. 455–481, 2000.

- [7] D. Lehmann, L. I. Oćallaghan, and Y. Shoham, “Truth revelation in approximately efficient combinatorial auctions,” J. ACM, vol. 49, no. 5, pp. 577–602, 2002.

- [8] J. O. Ledyard, “Optimal combinatoric auctions with single-minded bidders,” in EC ’07: Proceedings of the 8th ACM conference on Electronic commerce, (New York, NY, USA), pp. 237–242, ACM, 2007.

- [9] E. Elkind, “Designing and learning optimal finite support auctions,” in SODA ’07: Proceedings of the eighteenth annual ACM-SIAM symposium on Discrete algorithms, (Philadelphia, PA, USA), pp. 736–745, Society for Industrial and Applied Mathematics, 2007.

- [10] A. G. Deniz Dizdar and B. Moldovanu, “Revenue maximization in the dynamic knapsack problem.” Working paper, University of Bonn, 2009.

- [11] M. Shaked and J. G. Shanthikumar, Stochastic Orders (Springer Series in Statistics). New York: Springer-Verlag, October 2006.