Constructing Time-Homogeneous Generalised Diffusions Consistent with Optimal Stopping Values

Abstract

Consider a set of discounted optimal stopping problems for a one-parameter family of objective functions and a fixed diffusion process, started at a fixed point. A standard problem in stochastic control/optimal stopping is to solve for the problem value in this setting.

In this article we consider an inverse problem; given the set of problem values for a family of objective functions, we aim to recover the diffusion. Under a natural assumption on the family of objective functions we can characterise existence and uniqueness of a diffusion for which the optimal stopping problems have the specified values. The solution of the problem relies on techniques from generalised convexity theory.

Keywords: optimal stopping, generalised convexity, generalised diffusions, inverse American option problem

1 Introduction

Consider a classical optimal stopping problem in which we are given a discount parameter, an objective function and a time-homogeneous diffusion process started at a fixed point, and we are asked to maximise the expected discounted payoff. Here the payoff is the objective function evaluated at the value of the diffusion at a suitably chosen stopping time. We call this problem the forward optimal stopping problem, and the expected payoff under the optimal stopping rule the (forward) problem value.

The set-up can be generalised to a one-parameter family of objective functions to give a one-parameter family of problem values. In this article we are interested in an associated inverse problem. The inverse problem is, given a one-parameter family of objective functions and associated optimal values, to recover the underlying diffusion, or family of diffusions, for which the family of forward stopping problems yield the given values.

The approach of this article is to exploit the structure of the optimal control problem and the theory of generalised convexity from convex analysis to obtain a duality relation between the Laplace transform of the first hitting time and the set of problem values. The Laplace transform can then be inverted to give the diffusion process.

The generalised convexity approach sets this article apart from previous work on this problem, see [2, 1, 6]. All these papers are set in the realm of mathematical finance where the values of the stopping problems can be identified with the prices of perpetual American options, and the diffusion process is the underlying stock process. In that context, it is a natural question to ask: Given a set of perpetual American option prices from the market, parameterised by the strike, is it possible to identify a model consistent with all those prices simultaneously? In this article we abstract from the finance setting and ask a more general question: When can we identify a time-homogeneous diffusion for which the values of a parameterised family of optimal stopping problems coincide with a pre-specified function of the parameter.

Under restrictive smoothness assumptions on the volatility coefficients, Alfonsi and Jourdain [2] develop a ‘put-call parity’ which relates the prices of perpetual American puts (as a function of strike) under one model to the prices of perpetual American calls (as a function of the initial value of the underlying asset) under another model. This correspondence is extended to other payoffs in [1]. The result is then applied to solve the inverse problem described above. In both papers the idea is to find a coupled pair of free-boundary problems, the solutions of which can be used to give a relationship between the pair of model volatilities.

In contrast, in Ekström and Hobson [6] the idea is to solve the inverse problem by exploiting a duality between the put price and the Laplace transform of the first hitting time. This duality gives a direct approach to the inverse problem. It is based on a convex duality which requires no smoothness on the volatilities or option prices.

In this article we consider a general inverse problem of how to recover a diffusion which is consistent with a given set of values for a family of optimal stopping problems. The solution requires the use of generalised, or -convexity (Carlier [4], Villani [14], Rachev and Rüschendorf [11]). The log-value function is the -convex dual of the log-eigenfunction of the generator (and vice-versa) and the -subdifferential corresponds to the optimal stopping threshold. These simple concepts give a direct and probabilistic approach to the inverse problem which contrasts with the involved calculations in [2, 1] in which pdes play a key role.

A major advantage of the dual approach is that there are no smoothness conditions on the value function or on the diffusion. In particular, it is convenient to work with generalised diffusions which are specified by the speed measure (which may have atoms, and intervals which have zero mass).

Acknowledgement: DGH would like to thank Nizar Touzi for suggesting generalised convexity as an approach for this problem.

2 The Forward and the Inverse Problems

Let be a class of diffusion processes, let be a discount parameter, and let be a family of non-negative objective functions, parameterised by a real parameter which lies in an interval . The forward problem, which is standard in optimal stopping, is for a given , to calculate for each , the problem value

| (2.1) |

where the supremum is taken over finite stopping times , and denotes the fact that . The inverse problem is, given a fixed and the family , to determine whether could have arisen as a solution to the family of problems (2.1) and if so, to characterise those elements which would lead to the value function . The inverse problem, which is the main object of our analysis, is much less standard than the forward problem, but has recently been the subject of some studies ([2, 1, 6]) in the context of perpetual American options. In these papers the space of candidate diffusions is , where is the set of price processes which, when discounted, are martingales and is the put option payoff (slightly more general payoffs are considered in [1]). The aim is to find a stochastic model which is consistent with an observed continuum of perpetual put prices.

In fact it will be convenient in this article to extend the set to include the set of generalised diffusions in the sense of Itô and McKean [8]. These diffusions are generalised in the sense that the speed measure may include atoms, or regions with zero or infinite mass. Generalised diffusions can be constructed as time changes of Brownian Motion, see Section 5.1 below, and also [8], [10], [13], and for a setup related to the one considered here, [6].

We will concentrate on the set of generalised diffusions started and reflected at , which are local martingales (at least when away from zero). We denote this class . (Alternatively we can think of an element as the modulus of a local martingale whose characteristics are symmetric about the initial point zero.) The twin reasons for focusing on rather than , are that the optimal stopping problem is guaranteed to become one-sided rather than two-sided, and that within there is some hope of finding a unique solution to the inverse problem. The former reason is more fundamental (we will comment in Section 6.2 below on other plausible choices of subsets of for which a similar approach is equally fruitful). For , 0 is a reflecting boundary and we assume a natural right boundary but we do not exclude the possibility that it is absorbing. Away from zero the process is in natural scale and can be characterised by its speed measure, and in the case of a classical diffusion by the diffusion coefficient . In that case we may consider to be a solution of the SDE (with reflection)

where is the local time at zero.

We return to the (forward) optimal stopping problem: For fixed define , where is the first hitting time of level . Let

| (2.2) |

Clearly . Indeed, as the following lemma shows, there is equality and for the forward problem (2.1), the search over all stopping times can be reduced to a search over first hitting times.

Lemma 2.1.

and coincide.

Proof.

See Appendix. ∎

The first step in our approach will be to take logarithms which converts a multiplicative problem into an additive one. Introduce the notation

Then the equivalent -transformed problem (compare (2.2)) is

| (2.3) |

where the supremum is taken over those for which is finite. To each of these quantities we may attach the superscript if we wish to associate the solution of the forward problem to a particular diffusion. For reasons which will become apparent, see Equation (2.5) below, we call the eigenfunction (and the log-eigenfunction) associated with .

In the case where , and are convex duals. More generally the relationship between and is that of -convexity ([4], [14], [11]). (In Section 3 we give the definition of the -convex dual of a function , and derive those properties that we will need.) For our setting, and under mild regularity assumptions on the functions , see Assumption 3.6 below, we will show that there is a duality relation between and via the -payoff function which can be exploited to solve both the forward and inverse problems. In particular our main results (see Proposition 4.4 and Theorems 5.1 and 5.4 for precise statements) include:

Forward Problem: Given a diffusion , let and . Set . Then the solution to the forward problem is given by , at least for those for which there is an optimal, finite stopping rule. We also find that is locally Lipschitz over the same range of .

Inverse Problem: For to be logarithm of the solution of (2.1) for some it is sufficient that the -convex dual (given by ) satisfies , is convex and increasing, and for all .

Note that in stating the result for the inverse problem we have assumed that contains its endpoints, but this is not necessary, and our theory will allow for to be open and/or unbounded at either end.

If is a solution of the inverse problem then we will say that is consistent with . By abuse of notation we will say that (or ) is consistent with (or ) if, when solving the optimal stopping problem (2.1) for the diffusion with eigenfunction , we obtain the problem values for each .

The main technique in the proofs of these results is to exploit (2.3) to relate the fundamental solution with . Then there is a second part of the problem which is to relate to an element of . In the case where we restrict attention to , each increasing convex with is associated with a unique generalised diffusion . Other choices of subclasses of may or may not have this uniqueness property. See the discussion in Section 5.6.

The following examples give an idea of the scope of the problem:

Example 2.2.

Forward Problem: Suppose . Let and suppose that solves for . For such a diffusion . Then for , .

Example 2.3.

Forward Problem: Let be reflecting Brownian Motion on the positive half-line with a natural boundary at . Then . Let so that -convexity is standard convexity, and suppose . Then

It is easy to ascertain that the supremum is attained at where

| (2.4) |

for . Hence, for

with limits and . For we have .

Example 2.4.

Inverse Problem: Suppose that and . Suppose also that for

Then is reflecting Brownian Motion.

Note that is uniquely determined, and its diffusion coefficient is specified on . In particular, if we expand the domain of definition of to then for consistency we must have for .

Example 2.5.

Inverse Problem: Suppose and . Then for and, at least whilst , solves the SDE . In particular, does not contain enough information to determine a unique consistent diffusion in since there is some indeterminacy of the diffusion co-efficient on .

Example 2.6.

Inverse Problem: Suppose , and . Then the -dual of is given by , and is a candidate for . However is not convex. There is no diffusion in consistent with .

Example 2.7.

Forward and Inverse Problem: In special cases, the optimal strategy in the forward problem may be to ‘stop at the first hitting time of infinity’ or to ‘wait forever’. Nonetheless, it is possible to solve the forward and inverse problems.

Let be an increasing, differentiable function on with , such that is convex; let be a positive, increasing, differentiable function on such that ; and let be a non-negative, increasing and differentiable function on with .

Suppose that

Note that the cross-derivative is non-negative.

Consider the forward problem. Suppose we are given a diffusion in with log-eigenfunction . Then the log-problem value is given by

Conversely, suppose we are given the value function on . Then

is the log-eigenfunction of a diffusion which solves the inverse problem.

A generalised diffusion can be identified by its speed measure . Let be a non-negative, non-decreasing and right-continuous function which defines a measure on , and let be identically zero on . We call a point of growth of if whenever and denote the closed set of points of growth by . Then may assign mass to 0 or not, but in either case we assume . We also assume that if then . If then either is an absorbing endpoint, or does not reach in finite time.

The diffusion with speed measure is defined on and is constructed via a time-change of Brownian motion as follows.

Let be a filtration supporting a Brownian Motion started at with a local time process . Define to be the left-continuous, increasing, additive functional

and define its right-continuous inverse by

If we set then is a generalised diffusion which is a local martingale away from 0, and which is absorbed the first time that hits .

For a given diffusion recall that is defined via . It is well known (see for example [13, V.50] and [5, pp 147-152]) that is the unique increasing, convex solution to the differential equation

| (2.5) |

Conversely, given an increasing convex function with and , (2.5) can be used to define a measure which in turn is the speed measure of a generalised diffusion .

If then the process spends a positive amount of time at . If is an isolated point, then there is a positive holding time at , conversely, if for each neighbourhood of , also assigns positive mass to , then is a sticky point.

If and has a density, then where is the diffusion coefficient of and the differential equation (2.5) becomes

| (2.6) |

In this case, depending on the smoothness of , will also inherit smoothness properties. Conversely, ‘nice’ will be associated with processes solving (2.6) for a smooth . However, rather than pursuing issues of regularity, we prefer to work with generalised diffusions.

3 u-convex Analysis

In the following we will consider -convex functions for a function of two variables and . There will be complete symmetry in role between and so that although we will discuss -convexity for functions of , the same ideas apply immediately to -convexity in the variable . Then, in the sequel we will apply these results for the function , and we will apply them for -convex functions of both and .

For a more detailed development of -convexity, see [11], [14], [4] and the references therein. Proofs of the results below are included in the Appendix.

Let and be sub-intervals of . We suppose that is well defined, though possibly infinite valued.

Definition 3.1.

is -convex iff there exists a non-empty such that for all

Definition 3.2.

The -dual of is the -convex function on given by

A fundamental fact from the theory of -convexity is the following:

Lemma 3.3.

A function is -convex iff .

The function (the -convexification of ) is the greatest -convex minorant of (see the Appendix). The condition provides an alternative definition of a -convex function, and is often preferred; checking whether is usually more natural than trying to identify the set .

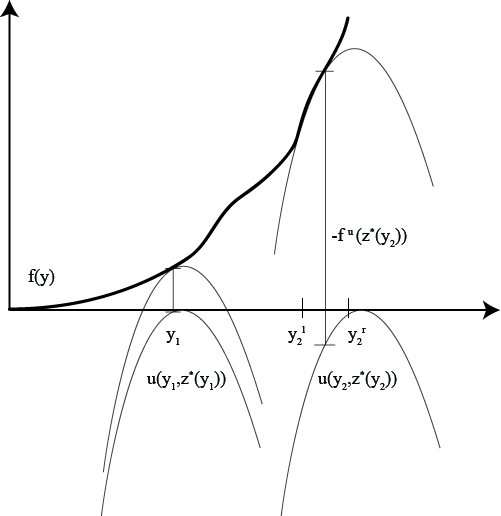

Diagrammatically (see Figure 1.), we can think of as the vertical distance between and . Thus when for all .

The following description due to Villani [14] is helpful in visualising what is going on: is -convex if at every point we can find a parameter so that we can caress from below with .

The definition of the -dual implies a generalised version of the Young inequality (familiar from convex analysis, e.g [12]),

for all . Equality holds at pairs where the supremum

is achieved.

Definition 3.4.

The -subdifferential of at is defined by

or equivalently

If is a subset of then we define to be the union of -subdifferentials of over all points in .

Definition 3.5.

is -subdifferentiable at if . is -subdifferentiable on if it is -subdifferentiable for all , and is -subdifferentiable if it is -subdifferentiable on .

In what follows it will be assumed that the function is satisfies the following ‘regularity conditions’.

Assumption 3.6.

-

(a)

is continuously twice differentiable.

-

(b)

as a function of , and as a function of , are strictly increasing.

Remark 3.7.

Remark 3.8.

The following results from -convex analysis will be fundamental in our application of -convex analysis to finding the solutions of the forward and inverse problems.

Lemma 3.9.

Suppose is -subdifferentiable, and satisfies

Assumption 3.6.

Then is monotone in the following

sense:

Let , .

Suppose and .

Then .

Definition 3.10.

We say that a function is strictly -convex, when its -subdifferential is strictly monotone.

Proposition 3.11.

Suppose that satisfies Assumption 3.6.

Suppose is a.e differentiable and -subdifferentiable. Then there exists a map such that if is differentiable at then and

| (3.1) |

Moreover, is such that is non-decreasing.

Conversely, suppose that is a.e differentiable and equal to the integral of its derivative. If (3.1) holds for a non-decreasing function , then is -convex and -subdifferentiable with .

Note that the subdifferential may be an interval in which case may be taken to be any element in that interval. Under Assumption 3.6, is non-decreasing

We observe that since we have and so that may be defined directly as an element of . If is strictly increasing then is just the inverse of .

Remark 3.12.

Proposition 3.13.

Suppose that satisfies Assumption 3.6.

Suppose is -subdifferentiable in a neighbourhood of . Then is continuously differentiable at if and only if is continuous at .

4 Application of -convex analysis to the Forward Problems

Now we return to the context of the family of optimal control problems (2.1) and the representation (2.3).

Lemma 4.1.

Let be a diffusion in natural scale reflected at the origin with a finite or infinite right boundary point . Then the increasing -eigenfunction of the generator

is locally Lipschitz continuous on .

Proof.

is increasing, convex and finite and therefore locally Lipschitz on . , and since is locally Lipschitz on , is locally Lipschitz on . ∎

Henceforth we assume that satisfies Assumption 3.6, so that is twice differentiable and satisfies the Spence-Mirrlees condition. We assume further that is non-decreasing in . Note that this is without loss of generality since it can never be optimal to stop at if , since to wait until the first hitting time of involves greater discounting and a lower payoff.

Consider the forward problem. Suppose the aim is to solve (2.3) for a given with associated -eigenfunction for the family of objective functions . Here is assumed to be an interval with endpoints and , such that .

Now let

| (4.1) |

Then is the -convex dual of .

By definition is the (set of) level(s) at which it is optimal to stop for the problem parameterised by . If is empty then there is no optimal stopping strategy in the sense that for any finite stopping rule there is another which involves waiting longer and gives a higher problem value.

Let be the infimum of those values of such that

. If is nowhere -subdifferentiable then we set .

Lemma 4.2.

The set where is -subdifferentiable forms an interval with endpoints and .

Proof.

Suppose is -subdifferentiable at , and suppose . We claim that is -subdifferentiable at .

Fix . Then and

| (4.2) |

and for if . We write the remainder of the proof as if we are in the case ; the case involves replacing with .

Fix . We want to show

| (4.3) |

for then

and since is continuous in the supremum is attained.

Lemma 4.3.

is locally Lipschitz on .

Proof.

On is -convex, -subdifferentiable and is monotone increasing.

Fix such that . Choose and and suppose has Lipschitz constant (with respect to ) in a neighbourhood of .

Then and so that

and a reverse inequality follows from considering . ∎

Note that it is not possible under our assumptions to date ( satisfying Assumption 3.6, and monotonic in ) to conclude that is continuous at , or even that exists. Monotonicity guarantees that even if we can still define . For example, suppose and for let . Then if is the -convex dual of we have , where . If and are such that exists and is finite, then choosing any bounded for which does not exist gives an example for which does not exist. It is even easier to construct modified examples such that is infinite.

Denote . Then for , . We have shown:

Proposition 4.4.

If satisfies Assumption 3.6, is increasing in and if is a reflecting diffusion in natural scale then the solution to the forward problem is .

Remark 4.5.

We close this section with some examples.

Example 4.6.

Recall Example 2.5, but note that in that example was restricted to take values in . Suppose , and . Then and for , . Further, for

and for .

Note that is continuous on , but not on .

Example 4.7.

Suppose and . Suppose is a diffusion on , with a natural boundary and diffusion coefficient . Then and

It is straightforward to calculate that and then that is given by

| (4.5) |

5 Application of -convex analysis to the Inverse Problem

Given an interval with endpoints and and a value function defined on we now discuss how to determine whether or not there exists a diffusion in that solves the inverse problem for . Theorem 5.1 gives a necessary and sufficient condition for existence. This condition is rather indirect, so in Theorem 5.4 we give some sufficient conditions in terms of the -convex dual and associated objects.

Then, given existence, a supplementary question is whether contains enough information to determine the diffusion uniquely. In Sections 5.3, 5.4 and 5.5 we consider three different phenomena which lead to non-uniqueness. Finally in Section 5.6 we give a simple sufficient condition for uniqueness.

Two key quantities in this section are the lower and upper bound for the range of the -subdifferential of on . Recall that we are assuming that the Spence-Mirrlees condition holds so that is increasing on . Then, if is somewhere -subdifferentiable we set , or if , . Similarly, we define , or if , , and . If is nowhere -subdifferentiable then we set .

5.1 Existence

In the following we assume that is -convex on , which means that for all ,

Trivially this is a necessary condition for the existence of a diffusion such that the solution of the optimal stopping problems are given by . Recall that we are also assuming that is increasing in and that it satisfies Assumption 3.6.

The following fundamental theorem provides necessary and sufficient conditions for existence of a consistent diffusion.

Theorem 5.1.

There exists such that if and only if there exists such that , is increasing and convex and is such that on .

Proof.

If then and is increasing and convex. Set . If then

Conversely, suppose satisfies the conditions of the theorem, and set . Let . Note that if then

and the maximiser satisfies .

For define a measure via

| (5.1) |

Let for , and, if is finite for . We interpret (5.1) in a distributional sense whenever has a discontinuous derivative. In the language of strings is the length of the string with mass distribution . We assume that . The case is a degenerate case which can be covered by a direct argument.

Let be a Brownian motion started at 0 with local time process and define via

Let be the right-continuous inverse to . Now set . Then is a local martingale (whilst away from zero) such that . When , we have .

We want to conclude that . Now, is the unique increasing solution to

with the boundary conditions and . Equivalently, for all with , solves

By the definition of above it is easily verified that is a solution to this equation. Hence and our candidate process solves the inverse problem. ∎

Remark 5.2.

Since is -convex a natural candidate for is , at least if and is convex. Then is the eigenfunction of a diffusion .

Our next example is one where is convex but not twice differentiable, and in consequence the consistent diffusion has a sticky point. This illustrates the need to work with generalised diffusions. For related examples in a different context see Ekström and Hobson [6].

Example 5.3.

Let and let the objective function be . Suppose

Writing we calculate

Note that is increasing and convex, and . Then jumps at and since

we conclude that . Then includes a multiple of the local time at 1 and the diffusion is sticky there.

Theorem 5.1 converts a question about existence of a consistent diffusion into a question about existence of a log-eigenfunction with particular properties including . We would like to have conditions which apply more directly to the value function . The conditions we derive depend on the value of .

As stated in Remark 5.2, a natural candidate for is . As we prove below, if this candidate leads to a consistent diffusion provided and is convex and strictly increasing. If then the sufficient conditions are slightly different, and need not be globally convex.

Theorem 5.4.

Assume is -convex. Each of the following is a sufficient condition for there to exist a consistent diffusion:

-

1.

, and is convex and increasing on .

-

2.

, , is convex and increasing on , and on , where

is the straight line connecting the points and .

-

3.

and there exists a convex, increasing function with such that for all and

where .

Proof.

We treat each of the conditions in turn. If then Theorem 5.1 applies directly on taking , with for (we use the fact that is -convex and so ).

Suppose . The condition on implies . Although the left-derivative need not equal the right-derivative the arguments in the proof of Proposition 3.11 show that . This implies that the function

is convex at and hence convex and increasing on .

Setting and for we have a candidate for the function in Theorem 5.1.

It remains to show that on . We now check that is consistent with on , which follows if the -convex dual of is equal to on .

Since we have . We aim to prove the reverse inequality. By definition, we have for

| (5.2) |

Now fix . For we have by the definition of the -subdifferential

Hence .

Similarly, if we have for all ,

and .

Finally, suppose . By the definition of and the condition we get

On the other hand

Hence on . ∎

Remark 5.5.

Case 1 of the Theorem gives the sufficient condition mentioned in the paragraph headed Inverse Problem in Section 2. If then if and only if for all , , where we use the fact that, by supposition, .

5.2 Non-Uniqueness

Given existence of a diffusion which is consistent with the values , the aim of the next few sections is to determine whether such a diffusion is unique.

Fundamentally, there are two natural ways in which uniqueness may fail. Firstly, the domain may be too small (in extreme cases might contain a single element). Roughly speaking the -convex duality is only sufficient to determine (and hence the candidate ) over and there can be many different convex extensions of to the real line, for each of which . Secondly, even when and , if is discontinuous then there can be circumstances in which there are a multitude of convex functions with . In that case, if there are no for which it is optimal to stop in an interval , then it is only possible to infer a limited amount about the speed measure of the diffusion over that interval.

In the following lemma we do not assume that is -convex.

Lemma 5.6.

Suppose is -convex and on . Let . Then, for each , , and for , . Further, for we have .

Proof.

Note that if is any function, with then .

If then

Hence there is equality throughout, so and .

For the final part, suppose and fix . From the Spence-Mirrlees condition, if ,

and hence

In particular, for , and

This last supremum is attained so that is non-empty.

∎

5.3 Left extensions

In the case where and there exists a diffusion consistent with then it is generally possible to construct many diffusions consistent with . Typically contains insufficient information to characterise the behaviour of the diffusion near zero.

Suppose that . Recall the definition of the straight line from Theorem 5.4.

Lemma 5.7.

Suppose that and that there exists consistent with .

Suppose that and that and is continuous and differentiable to the right at . Suppose further that for each .

Then, unless either for some or , there are many diffusions consistent with .

Proof.

Let be the log-eigenfunction of a diffusion which is consistent with

If then by Lemma 5.6. Otherwise the same conclusion holds on taking limits, since the convexity of necessitates continuity of .

Moreover, taking a sequence , and using we have

In particular, the conditions on translate directly into conditions about .

Since the straight line is the largest convex function with and we must have .

Then if for some or , then convexity of guarantees on .

Otherwise there is a family of convex, increasing with and such that for and for .

For such a , then by the arguments of Case 2 of Theorem 5.1 we have and then implies .

Hence each of is the eigenfunction of a diffusion which is consistent with . ∎

Example 5.8.

Recall Example 2.5, in which we have , and . We can extend to by (for example) drawing the straight line between and (so that for , ). With this choice the resulting extended function will be convex, thus defining a consistent diffusion on . Note that any convex extension of (i.e. any function such that and , for ) solves the inverse problem, (since necessarily on ). The most natural choice is, perhaps, for .

Our next lemma covers the degenerate case where there is no optimal stopping rule, and for all it is never optimal to stop. Nevertheless, as Example 5.10 below shows, the theory of -convexity as developed in the article still applies.

Lemma 5.9.

Suppose , and that there exists a convex increasing function with and such that and .

Suppose that exists in and write . If then is the unique diffusion consistent with if and only if for some or . If then there exist uncountably many diffusions consistent with .

Proof.

The first case follows similar reasoning as Lemma 5.7 above. Note that is the largest convex function on such that and .

If for any , or if then there does not exist any convex function lying between and on . In particular is the unique eigenfunction consistent with .

Conversely, if lies strictly below the straight line , and if then it is easy to verify that we can find other increasing convex functions with initial value 1, satisfying the same limit condition and lying between and the line.

In the second case define for . Then since we have

Hence is the eigenfunction of another diffusion which is consistent with . We conclude that there exist uncountably many consistent diffusions. ∎

Example 5.10.

Suppose and on . For this example we have that is nowhere -subdifferentiable and . Then and each of ,

and for any is an eigenfunction consistent with .

5.4 Right extensions

The case of is very similar to the case , and typically if there exists one diffusion which is consistent with , then there exist many such diffusions. Given consistent with , the idea is to produce modifications of the eigenfunction which agree with on , but which are different on .

Lemma 5.11.

Suppose . Suppose there exists a diffusion such that agrees with on . If then there are infinitely many diffusions in which are consistent with .

Proof.

It is sufficient to prove that given convex increasing defined on with and on , then there are many increasing, convex with defined on with for which .

The proof is similar to that of Lemma 5.7. ∎

Example 5.12.

Let , and .

Consider the forward problem when is a reflecting Brownian motion, so that the eigenfunction is given by . Suppose .

Then attains its maximum at the solution to

| (5.3) |

It follows that but where is the positive root of and .

Now consider an inverse problem. Let and be as above, and suppose . Let be the solution to (5.3) and let . Then the diffusion with speed measure (reflecting Brownian motion), is an element of which is consistent with . However, this solution of the inverse problem is not unique, and any convex function with for is the eigenfunction of a consistent diffusion. To see this note that for , so that any convex with for satisfies .

Remark 5.13.

If then one admissible choice is to take . This was the implicit choice in the proof of Theorem 5.1.

Example 5.14.

The following example is ‘dual’ to Example 2.3.

Suppose , , and . Then , for . For we have that is infinite. Since is convex, and -duality is convex duality, we conclude that is -convex. Moreover, is convex. Setting we have that , is convex and . Hence is associated with a diffusion consistent with , and this diffusion has an absorbing boundary at .

For this example we have and , but the left-derivative of is infinite at and is infinite to the right of . Thus there is a unique diffusion in which is consistent with .

5.5 Non-Uniqueness on

Even if is the positive real line, then if fails to be continuous it is possible that there are multiple diffusions consistent with .

Lemma 5.15.

Suppose there exists a diffusion which is consistent with .

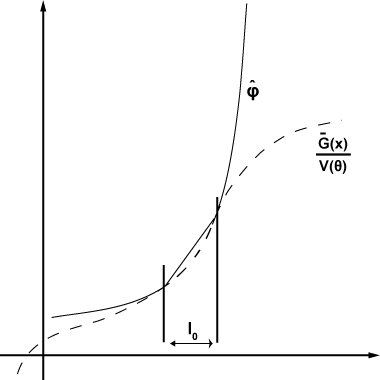

Suppose the -subdifferential of is multivalued, or more generally that is not continuous on . Then there exists an interval where the -subdifferential of is constant, so that . If is strictly convex in on some subinterval of of then the diffusion is not the unique element of which is consistent with .

Proof.

First note that if , is continuous then is nowhere constant and hence strictly monotone and thus = is strictly -convex (recall 3.10).

Suppose is strictly convex on . Then we can choose such that

on ,

is linear on ,

is continuous.

Then .

By definition we have

Then on , see Figure 2.

Let be given by

Then is convex and , so that they are associated with different elements of . Let .

It remains to show that . It is immediate from that . For the converse, observe that

∎

Example 5.16.

Suppose , and . Suppose that is such that is given by

It follows that

Then is multivalued, and there are a family of diffusions which give the same value functions as .

In particular we can take

Then and is a log-eigenfunction.

5.6 Uniqueness of diffusions consistent with V

Proposition 5.17.

Suppose is such that is continuous on , with range the positive real line.

Then there exists at most one diffusion consistent with .

Proof.

The idea is to show that is the only function with -convex dual . Suppose is such that on . For each there is a with , and moreover . Then by Lemma 5.6, and . ∎

Recall that we define and if set .

Theorem 5.18.

Suppose is such that is continuously differentiable on and that and .

Then there exists at most one diffusion consistent with .

Proof.

The condition on the range of translates into the conditions on and , so it is sufficient to show that is continuous at if and only if is differentiable there. This follows from Proposition 3.13. ∎

Corollary 5.19.

If the conditions of the Theorem hold but either is not convex or , then there is no diffusion which is consistent with .

Example 5.20.

Recall Example 2.6. For this example we have , which on is continuous and strictly increasing. Then and by the above corollary there is no diffusion consistent with .

6 Further examples and remarks

6.1 Birth-Death processes

We now return to and consider the case when is made up of isolated points only; whence is a birth-death process on points indexed by , with associated exponential holding times . We assume , is increasing, and write .

For a birth-death process the transition probabilities are given by

where of course , with . By our assumption that, away from zero, is a martingale, we must have . Then we can write . Let

Then it is easy to verify, but see [7], that (2.5) can be expressed in terms of a second-order difference operator

| (6.1) |

with boundary conditions and .

Let . In the language of strings, the pair is known as the Stieltjes String. If the string is called regular and is a regular boundary point, while otherwise the string is called singular, in which case we assume that is natural (see Kac [9]).

In this section we consider the call option payoff, defined for . This objective function is straight-forward to analyse since the -duality corresponds to straight lines in the original coordinates. It follows that for the forward problem is decreasing and convex in . is easily seen to be piecewise linear.

Our focus is on the inverse problem. Note that the solution of this problem involves finding the space and the jump rates . Suppose that is decreasing, convex and piecewise linear. Let be a sequence of increasing real valued parameters with and increasing to infinity, and suppose that has negative slope on each interval . Then is increasing in and

| (6.2) |

We assume that .

Since is convex, is convex. Let . By Proposition 3.11, for

so that . Note that is constant on . We find that for

and hence . Then, for ,

| (6.3) |

We proceed by determining the -matrix for the process on . For each , let denote the probability of jumping to state and the probability of jumping to . Then and are determined by the martingale property (and ). Further is determined either through (6.1) or from a standard recurrence relation for first hitting times of birth-death processes:

Example 6.1.

Suppose that so that , and . It follows that . We find (this example has been crafted to ensure that the birth-death process has the integers as state space, and this is not a general result). Also ( is piecewise linear with kinks at the integers) and the holding time at is exponential with rate .

6.2 Subsets of and uniqueness

So far in this article we have concentrated on the class . However, the methods and ideas translate to other classes of diffusions.

Let denote the set of all diffusions reflected at . Here denotes the speed measure, and the scale function. With the boundary conditions as in (2.5), is the increasing, but not necessarily convex solution to

| (6.4) |

In the smooth case, when has a density and is continuous, (6.4) is equivalent to

| (6.5) |

where

see [3].

Now suppose is given such that , and is increasing, then we will be able to find several pairs such that solves (6.5) so that there is a family of diffusions rather than a unique diffusion in consistent with .

It is only by considering subsets of , such as taking as in the majority of this article, or perhaps by setting the diffusion co-efficient equal to unity, that we can hope to find a unique solution to the inverse problem.

Example 6.2.

Consider Example 2.6 where we found . Let be the set of diffusions with unit variance and scale function (which are reflected at 0). Then there exists a unique diffusion in consistent with . The drift is given by

7 Applications to Finance

7.1 Applications to Finance

Let be the set of diffusions with the representation

In finance this SDE is often used to model a stock price process, with the interpretation that is the interest rate, is the proportional dividend, and is the level dependent volatility. Let denote the starting level of the diffusion and suppose that is an absorbing barrier.

Our aspiration is to recover the underlying model, assumed to be an element of , given a set of perpetual American option prices, parameterised by . The canonical example is when is the strike, and , and then, as discussed in Section 6.2, the fundamental ideas pass over from to . We suppose and are given and aim to recover the volatility .

Let be the convex and decreasing solution to the differential equation

| (7.1) |

(The fact that we now work with decreasing does not invalidate the method, though it is now appropriate to use payoffs which are monotonic decreasing in .) Then is determined by the Black-Scholes equation

| (7.2) |

Let be a family of payoff functions satisfying assumption 3.6. Under the additional assumption that is decreasing in (for example, the put payoff) Lemma 2.1 shows that the optimal stopping problem reduces to searching over first hitting times of levels . Suppose that is used to determine a smooth, convex on via the -convex duality

Then the inverse problem is solved by the diffusion with volatility given by the solution of (7.2) above. Similarly, given a diffusion such that is -convex on , then the value function for the optimal stopping problem is given exactly as in Proposition 4.4. See Ekström and Hobson [6] for more details.

Remark 7.1.

The irregular case of a generalised diffusion requires the introduction of a scale function, see Ekström and Hobson [6]. That article restricts itself to the case of the put/call payoffs for diffusions , using arguments from regular convex analysis to develop the duality relation. However, the construction of the scale function is independent of the form of the payoff function and is wholly transferable to the setting of -convexity used in this paper.

7.2 The Put-Call Duality; -dual Processes

In [2], Alfonsi and Jourdain successfully obtain what they

term

an American Put-Call duality (see below) and in doing so, they solve

forward and inverse problems for diffusions .

They consider objective functions corresponding to

calls and puts:

and .

In

[1] the procedure is generalised slightly to payoff functions

sharing ‘global properties’ with the put/call payoff. In our notation the

assumptions they

make are the following:

[1, (1.4)]

Let be a continuous function such

that on

the space ,

is

and further for all

Subsequently, they assume [1, (3.4)]

| (7.3) |

Condition (7.3) is precisely the Spence-Mirrlees condition applied to . Note that unlike Alfonsi and Jourdain [1] we make no concavity assumptions on G. We also treat the case of the reverse Spence-Mirrlees condition, and we consider classes of diffusions other than . Further, as in Ekström and Hobson [6] we allow for generalised diffusions. This is important if we are to construct solutions to the inverse problem when the value functions are not smooth. Moreover, even when is smooth, if it contains a -section, the diffusion which is consistent with exists only in the generalised sense. When contains a -section we are able to address the question of uniqueness. Uniqueness is automatic under the additional monotonicity assumptions of [1].

In addition to the solution of the inverse problem, a further aim of Alfonsi and Jourdain [2] is to construct dual pairs of models such that call prices (thought of as a function of strike) under one model become put prices (thought of as a function of the value of the underlying stock) in the other. This extends a standard approach in optimal control/mathematical finance where pricing problems are solved via a Hamilton-Jacobi-Bellman equation which derives the value of an option for all values of the underlying stock simultaneously, even though only one of those values is relevant. Conversely, on a given date, options with several strikes may be traded.

The calculations given in [2] are most impressive, especially given the complicated and implicit nature of the results (see for example, [1, Theorem 3.2]; typically the diffusion coefficients are only specified up to the solution of one or more differential equations). In contrast, our results on the inverse problem are often fully explicit. We find progress easier since the -convex method does not require the solution of an intermediate differential equation. Furthermore, the main duality ([1, Theorem 3.1]) is nothing but the observation that the -subdifferentials (respectively and ) are inverses of each other, which is immediate in the generalised convexity framework developed in this article. Coupled with the identity, the main duality result of [2] follows after algebraic manipulations, at least in the smooth case where and are strictly increasing and differentiable, which is the setting of [2] and [1].

Appendix A Proofs

A.1 The Forward and Inverse Problems

Proof of Lemma 2.1 Clearly , since the supremum over first hitting times must be less than or equal to the supremum over all stopping times.

A.2 u-convexity

Lemma A.1.

For every function , is the largest -convex minorant of .

Proof.

Note that is always a -convex minorant and by Definition 3.1 a function defined as the supremum of a collection of -convex functions is -convex.

Hence we can define , the largest -convex minorant of by

where is the set of -convex functions on . Then by the Fenchel Inequality, and since is -convex, it follows that .

Since is -convex there exists such that

For fixed , is -convex and it is easy to check that .

We note that if , then . Since , we therefore have . Taking the supremum over pairs , we get . ∎

Proof of Lemma 3.3 If is -convex then is its greatest -convex minorant, so . On the other hand if then since is -convex, so is .

Proof of Lemma 3.9 Let . For any and any , the following pair of inequalities follow from -convexity (see especially the second part of Definition 3.4):

Adding and re-arranging we get,

and hence,

| (A.1) |

Since (by Assumption 3.6(b)) is strictly increasing in the second argument it follows that .

Proof of Proposition 3.11 Suppose is -convex and -subdifferentiable. Let be a point of differentiability of and . Then for , we have both and

From the definition of -convexity and , so taking and putting all this together,

Dividing by on both sides and letting we get

If instead we take above then we get the reverse inequality and hence

| (A.2) |

By the Spence-Mirrlees condition is injective with respect to . Hence, the last equation determines uniquely; thus whenever is differentiable the sub-differential is a singleton set. We set . Then, since we have as required.

To prove the converse statement, suppose that for any point of differentiability of ,

where non-decreasing.

Define

Then is -convex: to see this define

and then

Clearly . We want to show that . By the assumptions on we have

Hence

Thus and so is -convex.

The following Corollary is immediate from 3.11.

Corollary A.2.

Suppose is differentiable at . Then is twice-differentiable at if and only if is differentiable at .

Proof of Proposition 3.13

Suppose is -subdifferentiable in a neighbourhood of . Then for small enough ,

and .

For the reverse inequality, if is continuous at then for small enough that we have

and .

Inequalities for the left-derivative follow similarly, and then which is continuous.

Conversely, if is multi-valued at so that is discontinuous at , then

where the strict middle inequality follows immediately from Assumption 3.6.

References

- [1] A. Alfonsi and B. Jourdain. General duality for perpetual American options. International Journal of Theoretical and Applied Finance, 11(6):545–566, 2008.

- [2] A. Alfonsi and B. Jourdain. Exact volatility calibration based on a Dupire-type call-put duality for perpetual American options. Nonlinear Differ. Equa. Appl, 16(4):523–554, 2009.

- [3] A.N. Borodin and P. Salminen. Handbook of Brownian Motion - Facts and Formulae. Birkhäuser, 2nd edition, 2002.

- [4] G. Carlier. Duality and existence for a class of mass transportation problems and economic applications. Adv. in Mathematical economy, 5:1–22, 2003.

- [5] H. Dym and H.P. McKean. Gaussian Processes, Function Theory, and the Inverse Spectral Problem. Academic Press, Inc., 1976.

- [6] E. Ekström and D. Hobson. Recovering a time-homogeneous stock price process from perpetual option prices. Preprint, 2009. http://arxiv.org/abs/0903.4833.

- [7] W. Feller. The birth and death processes as diffusion processes. J. Math. Pures Appl., 38:301–345, 1959.

- [8] K. Itô and H.P McKean. Diffusion Processes and their Sample Paths. Springer-Verlag, 1974.

- [9] I.S. Kac. Pathological Birth-and-Death Processes and the Spectral Theory of Strings. Functional Analysis and Its Applications, 39(2):144–147, 2005.

- [10] S. Kotani and S. Watanabe. Krein’s spectral theory of strings and generalized diffusion processes. Functional Analysis in Markov Processes, (ed. M. Fukushima), Lecture Notes in Math., 923:235–259, 1982.

- [11] S.T Rachev and L. Rüschendorf. Mass Transportation Problems, volume 1. Springer-Verlag, 1998.

- [12] R.T. Rockafellar. Convex Analysis. Princeton University Press, 1970.

- [13] L.C.G. Rogers and D. Williams. Diffusions, Markov Processes and Martingales, volume 2. Cambridge University Press, 2000.

- [14] C. Villani. Optimal Transport: Old and New. Springer-Verlag, 2009.