Meromorphic Lévy processes and their fluctuation identities

Abstract

The last couple of years has seen a remarkable number of new, explicit examples of the Wiener-Hopf factorization for Lévy processes where previously there had been very few. We mention in particular the many cases of spectrally negative Lévy processes in [21, 32], hyper-exponential and generalized hyper-exponential Lévy processes [24], Lamperti-stable processes in [9, 10, 13, 39], Hypergeometric processes in [35, 31, 11], -processes in [29] and -processes in [30].

In this paper we introduce a new family of Lévy processes, which we call Meromorphic Lévy processes, or just -processes for short, which overlaps with many of the aforementioned classes. A key feature of the -class is the identification of their Wiener-Hopf factors as rational functions of infinite degree written in terms of poles and roots of the Laplace exponent, all of which are real numbers. The specific structure of the -class Wiener-Hopf factorization enables us to explicitly handle a comprehensive suite of fluctuation identities that concern first passage problems for finite and infinite intervals for both the process itself as well as the resulting process when it is reflected in its infimum. Such identities are of fundamental interest given their repeated occurrence in various fields of applied probability such as mathematical finance, insurance risk theory and queuing theory.

Keywords: Lévy processes, Wiener-Hopf factorization, exit problems, fluctuation theory.

AMS 2000 subject classifications: 60G51, 60G50.

1 Introduction

The theory of Lévy processes forms the cornerstone of an enormous volume of mathematical literature which supports a wide variety of applied and theoretical stochastic models. One of the most obvious and fundamental problems that can be stated for a Lévy process, particularly in relation to its role as a modelling tool, is the distributional characterization of the time at which a Lévy process first exists either an infinite or finite interval together with its overshoot beyond the boundary of the interval. As a family of stochastic processes, Lévy processes are now well understood and the exit problem has seen many different approaches dating back to the 1960s. See for example [2, 6, 8, 16, 41, 19, 13, 35] to name but a few.

Despite the maturity of this field of study it is surprising to note that, until very recently, there were less than a handful of examples for which explicit analytical detail concerning the first exit problem could be explored. Given the closeness in mathematical proximity of the first exit problem to the characterization of the Wiener-Hopf factorization, one might argue that the lack of concrete examples of the former was a consequence of the same being true for the latter. The landscape for both the Wiener-Hopf factorization problem and the first exit problem has changed quite rapidly in the last couple of years however with the discovery of a number of new, mathematically tractable families of Lévy processes. We mention in particular the many cases of spectrally negative Lévy processes in [21, 32], hyper-exponential and generalized hyper-exponential Lévy processes [24], Lamperti-stable processes in [9, 10, 13], Hypergeometric processes in [35, 31], -processes in [29] and -processes in [30].

In this paper we introduce a new family of Lévy processes, which we call Meromorphic Lévy processes, or just -class for short, that overlaps with many of the aforementioned classes. Our definition of the -class of processes will allow us to drive features of their Wiener-Hopf factors through to many of the fluctuation identities which are of pertinence for a wide variety of applications. In the theory of actuarial mathematics, the problem of first exit from a half-line is of fundamental interest with regard to the classical ruin problem and is typically studied within the context of an expected discounted penalty function. The latter is also known as the Gerber-Shiu function following the first article [18] of a long series of papers found within the actuarial literature. In the setting of financial mathematics, the first exit of a Lévy process, as well as a Lévy process reflected in its infimum, from an interval is of interest in the pricing of barrier options and American-type options, [1], as well as certain credit risk models, [20, 33]. In queueing theory exit problems for Lévy processes play a central role in understanding the trajectory of the workload during busy periods as well as in relation to buffers, [17, 27]. Many optimal stopping strategies also turn out to boil down to first passage problems for both Lévy processes and Lévy processes reflected in their infimum; classic examples of which include McKean’s optimal stopping problem, [38], as well as the Shepp-Shiryaev optimal stopping problem, [2, 3] .

It is not our purpose however to dwell on these applications. As alluded to above, the main objective will be expose a comprehensive suite of fluctuation identities in explicit form for the -class of Lévy processes. We thus conclude the introduction with an overview of the paper.

In the next section we give a formal definition of meromorphic Lévy processes, dwelling in particular on their relationship with discrete completely monotone functions. In Section 3 we consider several classes of existing families of Lévy processes that have appeared in recent literature. Next, in Section 4 we establish explicit identities for the exponentially discounted first passage problem. In particular we deal with (what is known in the actuarial literature as) the Gerber-Shiu measure describing the discounted joint triple law of the overshoot, undershoot and undershoot of the maximum at first passage over a level as well as the marginal thereof which specifies the law of the discounted overshoot. It is important to note that the discounting factor which appears in all of the identities means that one is never more than a Fourier transform away from the naturally associated space-time identity in which the additional law of the time to first passage is specified. This last Fourier inversion appears to be virtually impossible to produce analytically within the current context, but the expressions we offer are not difficult to work with in conjunction with straightforward Fourier inversion algorithms.

In Section 5 we look at the more complicated two-sided exit problem. Inspired by a technique of Rogozin [41] we solve a system of equations which characterize the discounted overshoot distribution on either side of the interval in question. The same technique also delivers explicit expressions for the discounted entrance law into an interval. In Section 6 we look in analytical detail at what can be said of the ascending and descending ladder variables. In particular we offer expressions for their joint Laplace exponent and jump measure. Section 7 mentions some additional examples of fluctuation identities which enjoy explicit detail and finally in Section 8 we describe some numerical experiments in order to exhibit the genuine practical applicability of our method.

2 Meromorphic Lévy processes

Recall that a general one-dimensional Lévy process is a stochastic process issued from the origin with stationary and independent increments and almost sure right continuous paths. We write for its trajectory and for its law. As is necessarily a strong Markov process, for each , we will need the probability to denote the law of when issued from with the understanding that . The law of Lévy processes is characterized by its one-time transition probabilities. In particular there always exist a triple where , and is a measure on satisfying the integrability condition , such that, for all

| (1) |

where the Laplace exponent is given by the Lévy-Khintchine formula

| (2) |

Here is the cutoff function which is usually taken to be . However, everywhere in the present paper we will work with the Lévy measures which have exponentially decaying tails, thus we will take . Note, that the exponential decay of the tails of the Lévy measure also implies that the Laplace exponent can be analytically continued into some vertical strip for .

Everywhere in this paper we will denote the tails of the Lévy measure as and for . Let us define the supremum/infimum processes , and denote by an independent, exponentially distributed random variable with rate . Finally, the first passage time above is defined as , and similarly .

Let us recall some basic facts about completely monotone functions. A function is called completely monotone if and for all and . According to Bernstein theorem (see Theorem 1.4 in [42]), the function is completely monotone if and only if it can be represented as the Laplace transform of a positive measure on :

| (3) |

Note that if , then is a probability measure and is the cumulative distribution function of a positive infinitely divisible random variable , whose distribution is a mixture of exponential distributions. We will denote the class of completely monotone functions as .

Next, let us introduce a subclass of completely monotone functions, which will be important for us later. We will call a discrete completely monotone function if the measure in the representation (3) is discrete, and the support of the measure is infinite and does not have finite accumulation points. This implies that the measure is an infinite mixture of atoms of size at the points

where denotes the Dirac measure at , for all we have , and as (without loss of generality we can also assume that the sequence is strictly increasing). From (3) it follows then that any discrete completely monotone function can be represented as an infinite series of exponential functions

| (4) |

We will denote the class of discrete completely monotone functions as .

Definition 1 (-class).

A Lévy process is said to belong to the Meromorophic class (-class) if .

We see that according to our definition of the discrete completely monotone functions, the process is Meromorphic if and only if the Lévy measure has a density with respect to the Lebesgue measure, given by

| (5) |

where all the coefficients , , , are positive, the sequences and are stricly increasing, and and as .

Proposition 1.

Assume that is given by (5). The integral converges if and only if both series and converge.

Proof.

Recall, that a function is called meromorphic if it does not have any other singularities in the open complex plane except for poles. A function is called real meromorphic function if it is meromorphic and for all , or equivalently, if .

Theorem 1.

The following conditions are equivalent:

-

(i)

is Meromorphic.

-

(ii)

and the Laplace exponent is meromorphic.

-

(iii)

For some (and then, for every ) the functions and restricted to belong to the class .

-

(iv)

For some (and then, for every ) the functions and restricted to belong to the class .

-

(v)

For some (and then, for every ) we have the factorization

(6) where all roots of are real and interlace with the poles

(7) -

(vi)

The Laplace exponent is a real meromorphic function, which satisfies for all in the half-plane .

Proof.

The main ideas and tools needed for the proof of this theorem come from the proofs of Theorem 2 in [40] and Theorem 1 in [30].

(i)(ii) Using (5) and (2) we find that

| (8) |

which shows that is a meromorphic function. Since this proves (ii).

(ii)(vi) We know that is a meromorphic function, and that , therefore is analytic in some neighbourhood of zero. From the proof of Theorem 2 in [40] we find that (a) can be analytically continued in the half-planes and , (b) for all in the half-plane . Since we conclude that is a real meromorphic function. Using this fact and the above statement (b) we obtain (vi).

(vi)(v), . For and it is true that , thus (vi) implies that for all in the half-plane . Using Theorem 1 on page 220 in [36] (the statement of this result can also be found in the proof of Theorem 1 in [30]) we find that (v) is valid for all .

(v)(iii) This follows from Theorem 1 in [30].

(iii)(iv) One can also check that if two functions and belong to the class , then the same is true for and , where is the convolution. The result (iv) then follows easily from this fact and the Wiener-Hopf decomposition which says that , where the random variables and are independent, and .

(iv)(i) From (iv) and the definition of the class we know that for some there exist and positive constants , , , such that

| (9) |

Note that the condition implies that both series and converge. Let us define . Using (9) we obtain

Comparing the above formula with (8) we conclude that is a Laplace exponent of a Meromorphic Lévy process. We have already proved that (i) implies (vi), therefore for all in the half-plane .

Next, using the definition of the Laplace exponent (1) it is easy to verify that . Therefore

As we have already established, for all in the half-plane . Using this fact and the above identity we conclude that . Applying Theorem 1 on page 197 in [14] (the statement of this result can also be found in the proof of Theorem 1 in [30]) we find that admits a representation of the form (8), which in turn implies that the process is meromorphic.

Finally, note that if (v) is true for some , then (iii) and (iv) are valid for the same value of . But as we have already demonstrated, any of the conditions

(iii), (iv), (v) implies (i) which is equivalent to (v) being valid for all . Thus, if one of the conditions (iii), (iv), (v) is valid for some ,

then it must be valid for all .

Statement (ii) in Theorem 1 shows that the -class of Lévy processes might also be called ”processes with completely-monotone Lévy measure and meromorphic Laplace exponent”, which explains the origin of the name ”Meromorphic Lévy processes”. Note, however, that there exist Lévy processes with meromorphic Laplace exponent but not completely monotone Lévy measure.

The following technical result on partial fraction decomposition of infinite products will be very important for us later.

Lemma 1.

Assume that we have two increasing sequences and of positive numbers, such that as and the following interlacing condition is satisfied:

| (10) |

Define

| (11) |

Then for all

| (12) | |||||

| (13) |

where

| (14) | |||||

| (15) |

Moreover, , and for all we have , .

Proof.

The convergence of the infinite product in (11) and the partial fraction decomposition (12) follow from Theorem 1 in [30]. To prove the second partial fraction decomposition, rewrite the infinite product as

and note that sequences and satisfy interlacing condition, thus we can apply the same method. The details are left to the reader.

Using Monotone Convergence Theorem one can show that formulas (12) and (13) are equivalent to

| (16) | |||||

| (17) |

Before stating our next result we recall that a Lévy process creeps upwards if for some (and then all) , . Moreover, we say that is irregular for if and only if . (Note that this probability can only be 0 or 1 thanks to the Blumenthal zero-one law). We refer to Bertoin [5], Doney [15] or Kyprianou [34] for more extensive discussion of these subtle path properties.

We also need to introduce some more notation. In the forthcoming text everything will depend on the coefficients defined using (14) and defined using (15). We define for convenience a column vector

and similarly for , and . Next, given a sequence of positive numbers , we define a column vector as a vector of distributions

where is the Dirac delta function at .

From here on, unless otherwise stated, we shall always assume that is a Lévy process belonging to the -class and that is not a compound Poisson process.

Theorem 2 (Properties of Meromorphic processes).

-

(i)

The Wiener-Hopf factors are given by

(18) -

(ii)

For

(19) -

(iii)

() is nonzero if and only if is irregular for (correspondingly, ).

-

(iv)

() is nonzero if and only if the process creeps upwards (correspondingly, downwards).

-

(v)

For every

(20)

Proof.

Parts (i) and (ii) were established in Theorem 1 in [30], these results also follow easily from formulas (6), (16) and the structure of the Wiener-Hopf factorization. Let us prove (iii). We note that is irregular for if and only if, for any , has an atom in its distribution at . From part (ii) this is clearly the case if and only if is non-zero. For part (iv) of the proof, we note that we may necessarily write

where is the Laplace exponent of the bivariate subordinator which describes the ascending ladder process of . It is also known that a Lévy process creeps upwards if and only if the subordinator describing its ladder height process has a linear drift component. The drift coefficient is then described by where the limit is independent of the value of . Inspecting (17) we see that the required drift coefficient is non-zero if and only if is non-zero. The conclusion thus follows.

Finally, let us prove (v). From part (iv) of Theorem 1 we know that can be written in the form (9), where due to our assumption that is not a compound Poisson process. Combining this fact and the identity we conclude that

| (21) |

We see that the function on the right-hand side of the above equation has poles at the points and , while the left hand side has poles at and (this follows from (6)). Therefore we conclude that and . Comparing the residues of both sides of (21) at the pole we see that

Similarly we find

We would like to emphasize the importance of statement (v) of Theorem 2. It is well known that there exist only a few specific examples of Lévy processes (such as Variance Gamma or Normal Inverse Gaussian processes) for which the law of is known explicitly (for every ). While we do not know the law of for Meromorphic processes, the result in Theorem 2 (v) shows that Meromorphic processes have an advantage that at least the distribution of can be easily computed (for every ). The formula is given in terms of the roots and , but as we will see in Section 8, computing these numbers is a rather simple task and it can be done very efficiently.

As the next corollary shows, the Lévy measure of a Meromorphic process can be easily reconstructed from zeros and poles of . This has the spirit of Vigon’s theory of philanthropy (cf. [43]) in that we construct the Lévy measure from the Wiener-Hopf factors.

Corollary 1.

Proof.

The fact that is Meromorphic was already established in part (iii) of Theorem 1. Assume that the density of the Lévy meausre is given by (5), then as we have established in the proof of Theorem 1, the Laplace exponent can be expressed in the form (8). Comparing this equation with (6) we conclude that the exponents and in (5) must coincide with the poles of .

Note that the coefficients and given in (22) (which define the Lévy measure via (5)) depend on on the right hand side but not on the left hand side. It is therefore tempting to take limits as on the right hand side. This is not as straightforward as it seems as the limits of and are not easy to compute. It would be more straightforward to start with the Wiener-Hopf factorization for the case that and then perform the same analysis as in Corollary 1. The next corollary provides us with the aforementioned Wiener-Hopf factorization. We recall that (resp. ) denote the non-negative solutions to equation (resp. ).

Corollary 2.

-

(i)

Assume that . As we have and for

We have the Wiener-Hopf factorization , where

(24) -

(ii)

Assume that . As we have , and for

We have the Wiener-Hopf factorization , where

(25)

Proof.

Let us prove part (i). Since we know that and as , and also that with probability one. Therefore, if the Wiener-Hopf factor must converge to as while must converge to as . Since all roots and have nonzero limits as if (this is true due to the interlacing condition (7) and the fact that is a meromorphic function) we conclude that must go to zero while . The function is analytic in the neighbourhood or , and it’s derivative , thus using the Implicit Function Theorem we conclude that is an analytic function of in some neighbourhood of , and taking derivative with respect to of the equation we find that

Since we conclude that as . Using this fact and the formulae in (18) for the Wiener-Hopf factors we obtain expressions (24).

The proof of part (ii) is very similar. We use the fact that and to conclude that

as . This implies that when is small and positive, the equation has two solutions in the neighbourhood of zero, and

. Using this information, the uniquenes of the Wiener-Hopf factorization and taking the limit as in (6) we obtain (25).

3 Examples of Meromorphic processes

There are four particular families of Lévy processes which have featured in recent literature, all of which have proved to have relevance to a number of applied probability models, all of which have exhibited some degree of mathematical tractability in the context that they have occurred. These processes are as follows.

-

•

Hyper-exponential Lévy processes: The elementary but classical Kou model, [28], consists of a linear Brownian motion plus a compound Poisson process with two-sided exponentially distributed jumps. The natural generalization of this model (which therefore includes the Kou model) is the hyper-exponential Lévy process for which the exponentially distributed jumps are replaced by hyper-exponentially distributed jumps. That is to say, the density of the Lévy measure is written

where , , and are positive numbers and , are positive integers. One can verify that the Laplace exponent is a rational function of the form (8), where we have finite sums instead of infinite series, and that hyper-exponential Lévy processes have finite activity jumps and paths of bounded variation unless .

Strictly speaking, the Hyper-exponential Lévy processes do not belong to the class of Meromorphic processes, as in this case the Laplace exponent has only finite number of poles , . However, all the results presented in this paper are still correct when we have a process with positive and/or negative hyper-exponential jumps, provided that the results are interpreted in the correct way, see Remark 1 below.

-

•

-class Lévy processes: The -class of Lévy processes was introduced by Kuznetsov [29]. The Laplace exponent is given by

where is the Beta function, with parameter range , , and . The corresponding Lévy measure has density

With the help of binomial series one can check that is of the form (5), thus -processes are Meromorphic.

The large number of parameters allows one to choose Lévy processes within the -class that have paths that are both of unbounded variation (when at least one of the conditions , or holds) and bounded variation (when all of the conditions , and hold) as well as having infinite and finite activity in the jump component (accordingly as both or ). The -class of Lévy processes includes another recently introduced family of Lévy processes known as Lamperti-stable processes, cf. [9, 10, 13].

-

•

-class Lévy processes:

The -class of Lévy processes was also introduced by Kuznetsov [30] as a family of processes with Gaussian component and two-sided jumps, characterized by the density of the Lévy measure

where is the -th order (fractional) derivative of the theta function :

The parameter corresponds to the exponent of the singularity of at , and when () the Laplace exponent of is given in terms of trigonometric (digamma) functions. Again, due to the fact that the density of the Lévy measure is of the form (5) we conclude that -processes are Meromorphic.

-

•

Hypergeometric Lévy processes: These processes were introduced in Kyprianou et al. [35, 31] as an example of how to use Vigon’s theory of philanthropy. Their Laplace exponent is given by

(26) where and are the Laplace exponents of two subordinators from the -class of Lévy processes. Note that such Laplace exponents necessarily take the form

(27) Compared with the previous examples, it is less obvious that hypergeometric processes are Meromorphic, however it is not hard to establish this result with the help of Theorem 1. We know that -processes are meromorphic, thus the process with the Laplace exponent is Meromorphic (this is due to part (v) of Theorem 1). Finally, the hypergeometric process defined by the Laplace exponent via (26) and the process have the same Lévy measure, therefore is also Meromorphic.

Remark 1.

Within the scope of Definition 1, when the process has hyper-exponential positive jumps (a mixture of exponentials), we have only a finite sequence and either (or ) negative roots . All the formulas presented in this paper are still valid in this case if we adopt notation for and for (or ). For example, expression (18) for the Wiener-Hopf factor becomes a finite product

depending on whether we have or negative roots . The same remark holds true when we have hyper-exponential negative jumps.

Remark 2.

When the process has hyper-exponential positive jumps, calculation of coefficients and is much easier, since the corresponding expressions in (14) and (15) are just finite products. Moreover, calculation of the coefficients and is also simplified considerably even if the sequence is infinite, since we can use Wiener-Hopf factorization (23) and the fact that and are simple roots (poles) of function . For example we can compute coefficients as follows:

and this last expression is more convenient than (14), since usually we know explicitly and is just a rational function.

4 One-sided exit problem

Doney and Kyprianou [16] have given a detailed characterization of the one-sided exit problem through the so-called quintuple law. The latter can be easily integrated out to give the following discounted triple law which is also known in the actuarial mathematics literature as the Gerber-Shiu measure (cf. [7]). The following result holds for general Lévy processes.

Lemma 2.

Fix . Define

For all and we have

Taking account of formulas (19) this gives us the following immediate corollary for the -class of Lévy processes.

Corollary 3.

Fix . For all and we have

Often, one is only interested in the discounted overshoot distribution. In principle this can be obtained from the above formula by integrating out the variables and . However, it turns out to be more straightforward to prove this directly, particularly as otherwise it would require us to specify in more detail the Lévy measure in terms of poles and roots for the -class (cf. Corollary 1). The following result does precisely this, but in addition, it also gives us the probability of creeping.

Theorem 3.

Define a matrix as

| (28) |

Then for and we have

| (29) |

5 Entrance/exit problems for a finite interval

The two sided exit problem is a long standing problem of interest from the theory of Lévy processes and there are very few cases where explicit identities have been be extracted for the (discounted) overshoot distribution on either side of the interval. Classically the only examples with discounting which have been analytically tractable are those of jump diffusion processes with (hyper)-exponentially distributed jumps (see for example [26, 44]) and, up to knowing the so-called scale function, spectrally negative processes, [34]. Otherwise, the only other examples, without discounting, are those of stable processes, [41], and Lamperti-stable processes, [13].

Recall that

For , the space of positive, measurable and uniformly bounded functions on , and , define the following operators

| (31) | |||||

and for any subset define

| (32) | |||||

These are bounded operators from into . Note also that if then and similarly if then . For example, when , and when , .

Following similar reasoning to Rogozin [41] (see also [25]), an application of the Markov property tells us that for all we have

Thus we have the following operator identities:

| (33) |

Consider a space of bounded linear operators on with the norm

In the next theorem, which holds for general Lévy processes, we give a series representation for in terms of and a similar one for . In the case of stable processes and general Lévy processes respectively, Rogozin [41] and Kadankov and Kadankova [25] have shown similar series representations. The presentation we give above only differs in that it takes the form of linear operators. This turns out to be more convenient for the particular application to the -class of processes.

Theorem 4.

Assume . A pair of operators given by (31) is the unique solution in to the system of equations (33). Moreover, this solution can also be represented in series form

| (34) |

and

where, in both cases, convergence is exponential in the following sense. There exist and a constant such that if is the sum of the first terms in the series describing then with a similar statement holding for .

Proof.

It suffices to prove the result for , the proof for follows by duality. For uniqueness, we note first that the norm of operators is stricly less than one:

and similarly we find . Uniqueness also follows from the latter fact. Indeed if we assume that we have another pair of solutions , then using the system of equations (33) we find that the difference must satisfy the equation

Thus we find

and since we conclude that and . To establish the series representation (34) we use (33) to find

By iterating this equation we obtain series representation (34), which converges at an exponential rate as described in the statement of the theorem with

.

The next theorem converts the above general setting to the specific setting of -processes.

Theorem 5.

(First exit from a finite interval) Let and define a matrix with

| (35) |

and similarly .There exist matrices , and , such that for we have

| (36) |

These matrices satisfy the following system of linear equations

| (37) |

where and are defined by (28). The system of linear equations (37) can be solved iteratively with exponential convergence with respect to the matrix norm , where for any square matrix ,

| (38) |

Before proceeding to the proof of the above theorem, there is one technical lemma we must first address.

Lemma 3.

Let . Then .

Proof.

Using definitions (28) and (35) of and we find that for

Our first goal is to prove that are positive for all (note that for all ). Let us consider a random variable , where as usual is an exponentially distributed random variable with rate , independent of and . The Laplace transform of is given by

and using the partial fraction decomposition (12), after some algebraic manipulations we find that has a probability density function

This proves that are all positive. To prove that are positive one can use identity

Next we need to prove that . Define a row vector as the -th row of the matrix . Using Theorem 3 we check that

where and is independent and exponentially distributed with parameter . Thus we have

and using the already established fact that are positive we conclude that .

Proof of Theorem 5. The operator is an integral operator, with kernel

(see Theorem 3). We also have a similar formula for . Using the infinite series representation (34) we find that there exist some matrices of coefficients , and , so that integral kernels of operators and can be represented in the form (5). Matrix equations (37) follow from operator identities (33) and the fact that

Equations (37) can be solved iteratively as follows:

and the convergence and is exponential because of Lemma 3.

Once we find and we find and .

Remark 3.

Assume that within the -class the positive (negative) jumps come from a mixture of () exponential distributions. Then matrices and have size and , while matrices and have sizes and and can be found by the relations

The idea of writing down a pair of simultaneous equations (31) also works when considering the problem of first entrance into an interval. This problem has been considered earlier by [41] for the setting of stable processes and [26] for two sided Lévy processes whose upwards jumps are exponentially distributed.

Theorem 6 (First entrance into a finite interval).

Let and define . Define a matrix and similarly (see (35)). There exist matrices , and , such that for we have

| (39) |

These matrices satisfy the following system of linear equations

| (40) |

where and are defined by (28). This system of linear equations (40) can be solved iteratively with exponential convergence with respect to the matrix norm

The proof of this Theorem is very similar to the proof of Theorem 5, and we leave the details to the reader.

6 Ladder processes

In this Section we derive several results related to the Laplace exponent of the bivariate ladder process . We are interested in numerical evaluation of this object since it is the key to many important fluctuation identities, such as the quintuple law at the first passage which was introduced in [16].

Everywhere in this section we will denote the characteristic exponent of the Lévy process by . Note, that the Laplace exponent can be expressed in terms of the characteristic exponent as , this fact easily follows from (1).

The following Theorem, which holds for general Lévy processes, is a generalization of the expression for the Wiener-Hopf factors which can be found in Lemma 4.2 in [37].

Theorem 7.

Assume that for some and for all large enough we have

| (41) |

for some , and

| (42) |

exists for some (and then for all) . Then for and we have

| (43) |

Proof.

We start with the following integral representation for (see Theorem 6.16 in [34])

Assume that the process has a non-zero Gaussian component (), then has a density which can be obtained as the inverse Fourier transform of the right hand side of (1). Using this fact and assuming that we obtain

| (44) | |||||

Applying Fubini Theorem and performing integration in we find that the above integral is equal to

| (45) | |||||||

where in the last step we have used the fact that for and

(which can be easily verified by residue calculus). Next, we apply Fubini Theorem and Frullani integral to the last integral in (45) and combining this result with (44) we obtain

| (46) |

Next we need to take the limit of the above identity as . For small the integrand in the right hand side of (46) is bounded by

uniformly in for each , and for large it can be bounded by

again uniformly in . Using the above two estimates and assumption (41) we conclude that the integrand in the right hand side of (46) is bounded by

for some uniformly in , and the above function is integrable on due to assumption

(42). Thus we can apply the Dominated Convergence Theorem on the right hand side of (46) together with the Monotone Convergence Theorem on the left hand side whilst taking limits as . To finish the proof we only

need to take the limit , which can be justified in exactly the same way using the Dominated Convergence Theorem on the right hand side of (46) and weak convergence on the right hand side of (46). Note in particular that the characteristic exponent of is continuous in the Gaussian coefficient and hence, by the Continuity Theorem for Fourier transforms, the law of is weakly continuous in the Gaussian coefficient.

Assumption (42) is a very mild one. It is satisfied by all processes except those which have unusually heavy tails of the Lévy measure. It is satisfied by all processes in -class, and more generally, by all processes for which there exists an such that as (for example, all stable processes have this property). While condition (41) is more restrictive, one can see that it only excludes compound Poisson processes and some processes of bounded variation which are equal to the sum of its jumps. One example of such a process is a pure jump Variance Gamma process with no linear drift , which satisfies as . One can see that condition (41) is satisfied for the processes of bounded variation with non-zero drift, processes with non-zero Gaussian component and all processes with the Lévy measure satisfying as for some . In particular this condition is satisfied for all processes in the -, -, hypergeometric or hyperexponential family excluding compound Poisson processes.

Theorem 7 allows us to derive an expression for the Laplace exponent of the bivariate ladder process .

Theorem 8.

Assume that belongs to -, -, hyper-exponential or hypergeometric family of Levy processes and that is not a compound Poisson process. Then

| (47) |

Proof.

If belongs to -, - or hypergeometric family of Levy processes, we can use asymptotics for as (see [29], [30] and [31]) to find that and , which implies that both infinite products

converge. Next, using the same technique as in the proof of Lemma 6 in [29], one can prove that

as , . Using the Wiener-Hopf factorization and (18) we obtain

Since is not a compound Poisson process, we have as , , thus we finally conclude that

The next step is to use the Wiener-Hopf factorization , (18) and the above identity to rewrite as

Now we can use the above factorization and the following integral identity (which can be proved by shifting the contour of integration in the complex plane)

to deduce that for

which is equivalent to (47).

Corollary 4.

Let be the Lévy measure of the ascending ladder process . Then for we have

| (48) |

7 More Fluctuation identities

We offer some more fluctuation identities. Although they are slightly more complex, they are still equally straightforward for the purpose of numerical work.

We assume throughout this section that is regular for both and . Equivalently, we assume that . This is the case if, for example, has paths of unbounded variation. It will be clear from the proofs of the results given below how this assumption may be removed.

For and for we define resolvent for killed on leaving as

Theorem 9.

Define a matrix as follows

Then if we have

Proof.

From the proof of Theorem 20 on p176 of [5], it can be seen that

Thus we obtain an alternative representation of the Spitzer-Bertoin identity

To finish the proof we have to use the formulas in (19) and perform the integration in the above expression (noting that some terms are lost on account of the fact that we have assumed ).

Next define

Theorem 10.

Proof.

Remark 4.

The previous result also allows us to write down the discounted joint overshoot, undershoot distribution for the two-sided exit problem:

(Again this relates to the so-called Gerber-Shiu measure for classical risk theory). Indeed, for and , using the compensation formula we have

Remark 5.

Define the reflected process and its resolvent when killed on exiting ,

where . According to [4] one may write for all ,

where . Moreover, note that we may continue the computations in a similar way to before with the help of the compensation formula,

and hence

8 Numerical Results

For all our numerical examples we will use a process from the -family (see the introduction or [29]) having parameters

Here and is the Gaussian coefficient, the other parameters define the density of a Lévy measure, which has exponentially decaying tails and singularity at , thus this process has jumps of infinite activity but finite varation. We define the following four parameter sets

As the first illustration of the efficiency of our algorithms we will compute the following three quantities related to the double exit problem:

-

(i)

density of the overshoot one the event that the process exists at the upper boundary

-

(ii)

probability of exiting from the interval at the upper boundary

-

(iii)

probability of exiting the interval by creeping across the upper boundary

In order to compute these expressions we use methods described in Theorem 5. We truncate all the matrices so that they have size (this corresponds to truncating coefficients and at and coefficients and at ). In order to compute coefficients , , and we truncate infinite products in (14) and (15) at , thus all the computations depend on precomputing for . All the code was written in Fortran and the computations were performed on a standard laptop (Intel Core 2 Duo 2.5 GHz processor and 3 GB of RAM).

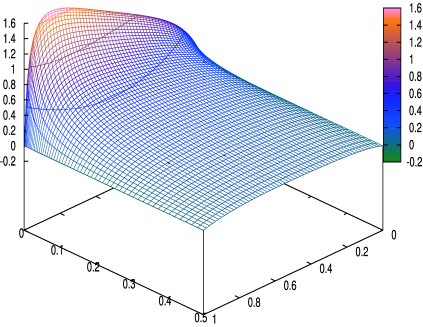

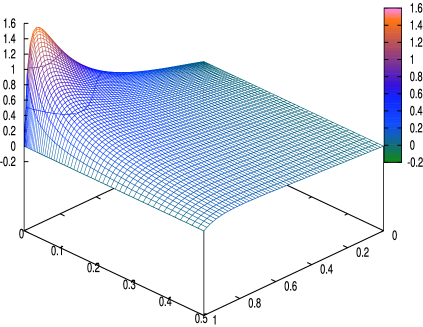

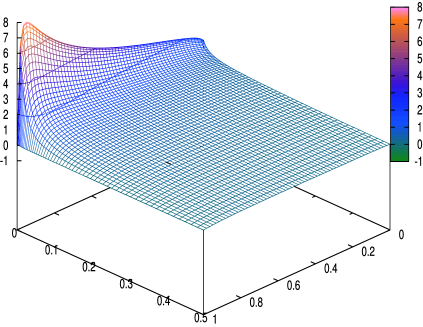

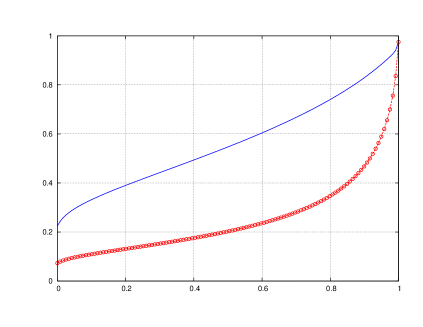

We present the results for in Figures 1 and 2. Computations required to produce graphs for each parameter set took around 0.15 seconds. The numerical results clearly show the effects that we would expect to see. In Figures 1b, 1d and 2b we see a positive probability of creeping, which is expected since the process has a Gaussian component in the first two cases and a bounded variation and positive drift in the third case. Parameter Set 4 corresponds to a process with bounded variation and negative drift, thus we do not have any upward creeping, and this is exactly what we obtain in Figure 2d. Also, figures 1a, 1c and 2a show that as , which confirms our expectation, as in this case the upper half line is regular and as the process will cross the barrier at 1 by creeping, not by jumping over it. This is different from figure 2c, where, because of bounded variation and negative drift, the upper half line is irregular and the only way to cross the barrier at 1 is by jumping over it. Next, Figures 1b and 1d show that as and as , which again agrees with the theory, as for parameter Sets 1 and 2 the process has a Gaussian component, therefore is regular for and . This is not so for parameter Sets 3 and 4, since now the process has bounded variation and drift, and depending on the sign of the drift, is regular for either or , and this is what we observe on figures 2b and 2d.

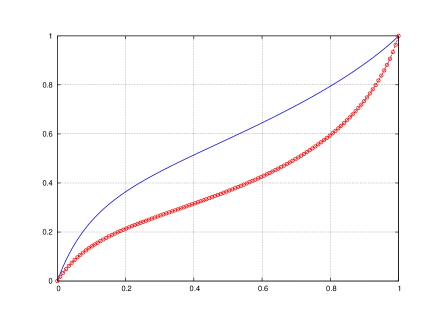

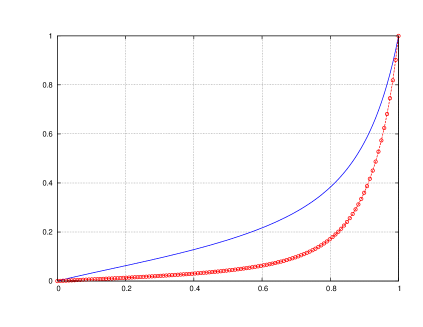

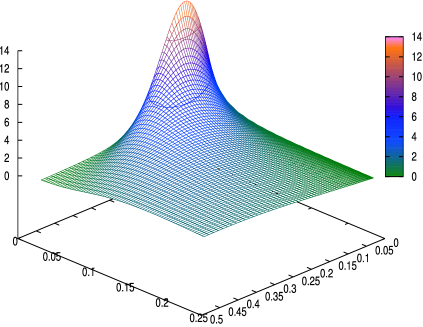

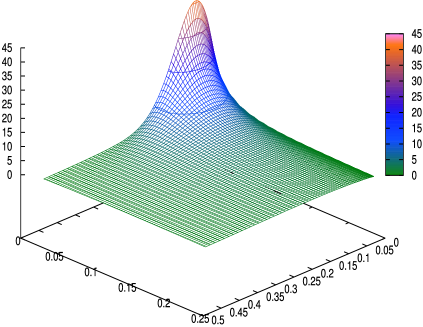

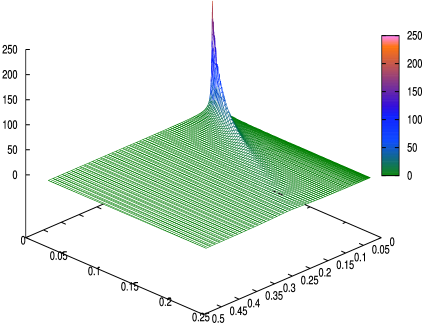

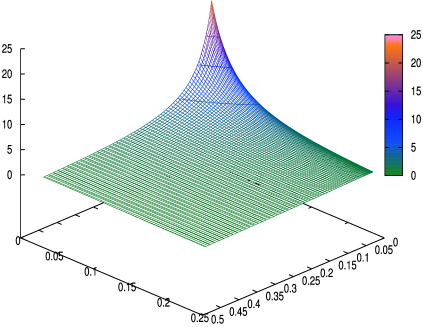

For the next example, we compute the density of the bivariate renewal measure defined by

where is the ascending ladder process, see [16], [34] and [35]. This measure is a very important object, as it gives us full knowledge of the quintuple law at the first passage, see [16]. Using formulas 6.18 and 7.10 in [34] we see that satisfies

therefore using Theorem 8 and (19) we find that the density of can be computed as

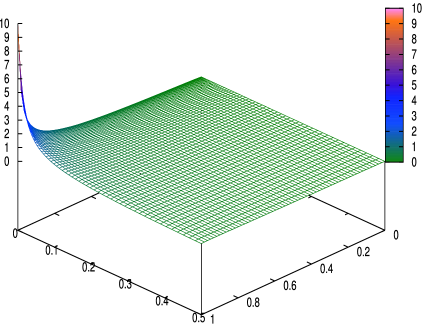

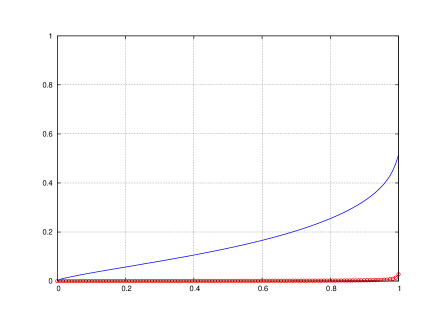

for any . It turns out that it is quite easy to compute the above integral numerically using technique discussed in [29] coupled with a Filon-type method (see [23]). Producing each graph on Figure 3 takes around seconds. In order to compute we truncated at and used roots to compute these coefficients using formulas (14). We chose , truncated integal in at . The numerical results are presented in Figure 3. Note that both the ascending ladder height and time processes behind Figure 3 (c) have a linear drift where as in Figure 3 (d) they are both driftless compound Poisson processes. In the former case this explains the strong concentration of mass around a linear trend, and in the latter case there exists an atom at , which is not visible on the graph since we are only plotting the absolutely continuous part.

As we have mentioned in the introduction, all expressions related to fluctuation identities presented in this paper have the following property: (i) they are computed explicitly in terms of roots/poles of and possibly some linear algebra operations, (ii) all of them have the law of the space variables (for example, overshoot or location of the last maximum) in closed form and (iii) they involve Laplace transform of the first passage time or . The third condition implies that if we want to compute joint distribution of both space and time functionals of the process (for example, joint density of the first passage time and the overshoot) we would have to perform a Fourier transform in the -variable, and it has to be done numerically. See [29] and [31] for examples of application of this technique. It turns out, that using exactly the same method we can also be used to obtain similar reults for Lévy processes with stochastic volatility, which are very popular models in Mathematical Finance, see for example [12]. We will briefly present this technique for the case of the two-sided exit problem considered above. Let be an increasing continuous process satisfying . We require that is known in closed form, a classical example is the integral of the Cox-Ingersoll-Ross diffusion process, however one can also choose several other processes, see [22]. Define a time-changed process , , where we assume that is independent of . As before, define to be the first passage time of process below {above }. Since is continuous we have , thus we obtain for any positive

where we have used the fact that

which follows from (49) by inverting the Laplace transform in . Thus we see that if we choose the time change process for which the Laplace transform is known in closed form, then computing quantities for the time-changed process is essentially identical to computing the same quantities for the process itself.

References

- [1] L. Alili and A.E. Kyprianou, Some remarks on first passage of Lévy processes, the American put and pasting principles, Ann. Appl. Probab., 15 (2005), pp. 2062–2080.

- [2] F. Avram, A. E. Kyprianou, and M. R. Pistorius, Exit problems for spectrally negative Lévy processes and applications to (Canadized) Russian options, Ann. Appl. Probab., 14 (2004), pp. 215–238.

- [3] E. Baurdoux and A.E. Kyprianou, The Shepp-Shiryaev stochastic game driven by a spectrally negative Lévy process., Theory of Probability and Its Applications (Teoriya Veroyatnostei i ee Primeneniya), 53 (2009), pp. 481–499.

- [4] E.J. Baurdoux, Some excursion calculations for reflected lévy processes, ALEA Lat. Am. J. Probab. Math. Stat., 6 (2009), pp. 149–162.

- [5] J. Bertoin, Lévy Processes, Cambridge University Press, 1996.

- [6] , Exponential decay and ergodicity of completely asymmetric Lévy processes in a finite interval, Ann. Appl. Probab., 7 (1997), pp. 156–169.

- [7] E. Biffis and A. E. Kyprianou, A note on scale functions and the time value of ruin for Lévy insurance risk processes, Insurance Math. Econom., 46 (2010), pp. 85–91.

- [8] A. A. Borovkov, Stochastic processes in queueing theory, Springer-Verlag, New York, 1976. Translated from the Russian by Kenneth Wickwire, Applications of Mathematics, No. 4.

- [9] M.E. Caballero and L. Chaumont, Conditioned stable Lévy processes and the Lamperti representation, J. Appl. Probab., 43 (2006), pp. 967–983.

- [10] M.E. Caballero, J.C. Pardo, and J.L. Perez, On the Lamperti stable processes, Probab. Math. Statist., 30 (2010), pp. 1–28.

- [11] , Explicit identities for Lévy processes associated to symmetric stable processes, Bernoulli, 17 (2011), pp. 34–59.

- [12] P. Carr, H. Geman, D.B. Madan, and M. Yor, Stochastic volatility for lévy processes, Mathematical Finance, 13 (2003), pp. 345–382.

- [13] L. Chaumont, A.E. Kyprianou, and J.C. Pardo, Some explicit identities associated with positive self-similar Markov processes, Stoch. Proc. Appl., 119 (2009), pp. 980–1000.

- [14] N.G. Chebotarev and N.N. Meiman, The Routh-Hurwitz problem for polynomials and entire functions, Trudy Mat. Inst. Steklov. (in Russian), 26 (1949), pp. 3–331, available online at http://mi.mathnet.ru/eng/tm1039.

- [15] R. A. Doney, Fluctuation theory for Lévy processes, vol. 1897 of Lecture Notes in Mathematics, Springer, Berlin, 2007. Lectures from the 35th Summer School on Probability Theory held in Saint-Flour, July 6–23, 2005, Edited and with a foreword by Jean Picard.

- [16] R.A. Doney and A.E. Kyprianou, Overshoots and undershoots of Lévy processes, Ann. Appl. Probab., 16 (2006), pp. 91–106.

- [17] A. Es-Saghouani and M. Mandjes, On the correlation structure of a Lévy-driven queue, J. Appl. Probab., 45 (2008), pp. 940–952.

- [18] H. U. Gerber and E. S. W. Shiu, The joint distribution of the time of ruin, the surplus immediately before ruin, and the deficit at ruin, Insurance Math. Econom., 21 (1997), pp. 129–137.

- [19] R. K. Getoor, First passage times for symmetric stable processes in space, Trans. Amer. Math. Soc., 101 (1961), pp. 75–90.

- [20] B. Hilberink and L. C. G. Rogers, Optimal capital structure and endogenous default, Finance Stoch., 6 (2002), pp. 237–263.

- [21] F. Hubalek and A.E. Kyprianou, Old and new examples of scale functions for spectrally negative Lévy processes, in Sixth Seminar on Stochastic Analysis, Random Fields and Applications, eds R. Dalang, M. Dozzi, F. Russo., (2011), pp. 119–146.

- [22] T.R. Hurd and A. Kuznetsov, Explicit formulas for Laplace transform of stochastic integrals, Markov Processes Relat. Fields, 14 (2008), pp. 277–290.

- [23] A. Iserles, On the numerical quadrature of highly-oscillating integrals I: Fourier transforms, IMA J. Numer. Anal, 24 (2004), pp. 365–391.

- [24] M. Jeannin and M.R. Pistorius, A transform approach to calculate prices and greeks of barrier options driven by a class of Lévy processes, Quantitative Finance, 10 (2010), pp. 629–644.

- [25] V. Kadankov and T. Kadankova, On the distribution of the first exit time from an interval and the value of overshoot through the boundaries for processes with independent increments and random walks, Ukr. Math. J., 57 (2005), pp. 1359–1384.

- [26] T. Kadankova and N. Veraverbeke, On several two-boundary problems for a particular class of Lévy processes, J. Theor. Prob., 24 (2007), pp. 1073–1085.

- [27] T. Konstantopoulos, A. E. Kyprianou, P. Salminen, and M. Sirviö, Analysis of stochastic fluid queues driven by local-time processes, Adv. Appl. Probab., 40 (2008), pp. 1072–1103.

- [28] S. Kou, A jump diffusion model for option pricing, Management Science, (2002), pp. 1086–1101.

- [29] A. Kuznetsov, Wiener-Hopf factorization and distribution of extrema for a family of Lévy processes, Ann. Appl. Probab., 20 (2010), pp. 1801–1830.

- [30] , Wiener-Hopf factorization for a family of Lévy processes related to theta functions, J. Appl. Probab., 47 (2010), pp. 1023–1033.

- [31] A. Kuznetsov, A.E. Kyprianou, J.C. Pardo, and K. van Schaik, A Wiener-Hopf Monte Carlo simulation technique for Lévy processes, Ann. Appl. Probab., to appear, (2009).

- [32] A. E. Kyprianou and V. Rivero, Special, conjugate and complete scale functions for spectrally negative Lévy processes, Electron. J. Probab., 13 (2008), pp. no. 57, 1672–1701.

- [33] A. E. Kyprianou and B. A. Surya, Principles of smooth and continuous fit in the determination of endogenous bankruptcy levels, Finance Stoch., 11 (2007), pp. 131–152.

- [34] A.E. Kyprianou, Introductory Lectures on Fluctuations of Lévy Processes with Applications, Springer, 2006.

- [35] A.E. Kyprianou, J.C. Pardo, and V. M. Rivero, Exact and asymptotic n-tuple laws at first and last passage, Ann. Appl. Probab., 20 (2010), pp. 522–564.

- [36] B.Ya. Levin, Lectures on entire functions, no. 150 in Translations of Mathematical Monographs, Amer. Math. Soc., 1996.

- [37] A.L. Lewis and E. Mordecki, Wiener-Hopf factorization for Lévy processes having positive jumps with rational transforms, J. Appl. Probab., 45 (2008), pp. 118–134.

- [38] H. McKean, Appendix: A free boundary problem for the heat equation arising from a problem of mathematical economics., Ind. Manag.Rev., 6 (1965), pp. 32–39.

- [39] P. Patie, Exponential functional of a new family of Lévy processes and self-similar continuous state branching processes with immigration, Bull. Sci. Math., 133 (2009), pp. 355–382.

- [40] L. C. G. Rogers, Wiener-Hopf factorization of diffusions and Lévy processes, Proc. London Math. Soc. (3), 47 (1983), pp. 177–191.

- [41] B.A. Rogozin, The distribution of the first hit for stable and asymptotically stable walks on an interval., Theor. Probab. Appl., 17 (1972), pp. 332 – 338.

- [42] R. L. Schilling, R. Song, and Z. Vondracek, Bernstein Functions: Theory and Applications, vol. 37 of de Gruyter Studies in Mathematics 37, De Gruyter, 2010.

- [43] V. Vigon, Simplifiez vos Lévy en titillant la factorisation de Wiener-Hopf., Thèse de doctorat de l’INSA de Rouen, 2002.

- [44] S. Wang and C. Zhang, First-exit times and barrier strategy of a diffusion process with two-sided jumps, Preprint, (2007).