Consistent Valuation of Bespoke CDO Tranches

Abstract

This paper describes a consistent and arbitrage-free pricing methodology for bespoke CDO tranches. The proposed method is a multi-factor extension to the [self] model, and it is free of the known flaws in the current standard pricing method of base correlation mapping. This method assigns a distinct market factor to each liquid credit index and models the correlation between these market factors explicitly. A low-dimensional semi-analytical Monte Carlo is shown to be very efficient in computing the PVs and risks of bespoke tranches. Numerical examples show that resulting bespoke tranche prices are generally in line with the current standard method of base correlation with TLP mapping. Practical issues such as model deltas and quanto adjustment are also discussed as numerical examples.

1 Introduction

Base correlation mapping is the current market standard for pricing bespoke CDO tranches111 [bcmap] is a detailed review of representative base correlation mapping methods.. Most market participants have implemented certain variations of the base correlation mapping method to price and risk manage bespoke tranches. Given the illiquid nature and wide bid/ask range of bespoke tranches, only rough agreements on the valuation of bespoke tranches between market participants are needed to facilitate trading. The standard base correlation mapping method played such a crucial role of providing the pricing consensus. The base correlation mapping method also produces stable risk measures, which allows a market participant to hedge bespoke tranches with index tranches and single name CDS contracts. The hedging activity of bespoke tranches in turn spurred further growth of the index tranche market. The base correlation mapping method therefore is a key enabler in the explosive growth of the bespoke and index tranche markets in the years prior to the credit crisis.

When the credit crisis hits in 2008, the bespoke tranche market rapidly froze because of the disappearing of the “rating arbitrage” and the lack of demand for illiquid and complex derivatives. However, the base correlation mapping method is still critical in practice for the risk management of the existing bespoke tranche positions. The losses from synthetic CDO tranche positions in major banks has been minuscule comparing to the write-downs from cash instruments such as ABS, MBS and CMBS bonds, which is a testimony of the effective risk management practice enabled by the base correlation model when comparing to the risk management practice in cash instruments.

Despite its popularity and practical importance, the base correlation mapping method is known to have serious flaws. The main problems include the lack of pricing consistency, existence of arbitrage and counter-intuitive risk measures. Some of the flaws are well documented in [bcdelta]. The pricing of bespoke tranches are still of great practical interests because 1) there are a large number of legacy bespoke tranche positions that require risk management; 2) the standard index tranches remain liquid, and a bespoke tranche model is required for trading the standard index tranches since the index tranches eventually lose liquidity and behave like bespoke tranches as time goes by; 3) the consistent pricing of bespoke tranches is also important for developing relative value trading strategies between index tranches from different indices and series.

In this paper, we propose a consistent pricing method for bespoke CDO tranches that is free of the flaws in the base correlation model. This paper is organized as follows, we first review the base correlation mapping method; then we introduce the consistent pricing method for bespoke tranches based on the [self] model; then we present the numerical results with special focuses on important practical issues such as tranche and single name deltas.

2 Review of Base Correlation Mapping

It is well known that the base correlation model cannot produce a consistent joint distribution of default time or default indicators (abbreviated as and respectively following the notation in [self]); therefore its practical application is limited to the computation of portfolio loss distributions. The lack of consistent and in the base correlation model has been frequently criticized by both practitioners and academics; however the base correlation model remains the market standard because it is a simple and flexible method to construct the portfolio loss distribution, which is by far the most important metric in practice.

The base correlation model is a very reliable interpolation method to price non-standard tranches on a liquid index portfolio, for example, an IG9 5-7% tranche at 4Y maturity. Even though arbitrage could arise from the base correlation interpolation and extrapolation, the arbitrages on non-standard tranches on liquid index portfolios are usually very small in practice since the base correlation interpolation and extrapolation methods have been exhaustively tweaked to minimize the arbitrage. The remaining small arbitrage across index tranche strikes and maturities are usually not exploitable because of the wide bid/ask of the non-standard index tranches. Therefore, if we calibrate a base correlation model to standard index tranches, then use it to price tranches with non-standard strikes or maturities on the same index, the resulting prices are very consistent and reliable. Different dealers usually reach very similar non-standard index tranche prices even if their implementations of base correlation models differ in model assumptions and parameters222For example, different banks are likely to use different stochastic recovery specifications, and base correlation interpolation and extrapolation schemes.

In contrast, the bespoke tranches are priced with the more ad hoc base correlation mapping procedure, which leads to inconsistent loss distributions across different bespoke portfolios. This inconsistency is very difficult to control and mitigate within the base correlation framework. The bespoke tranche pricing from base correlation mapping methods are therefore much less reliable than the non-standard index tranches, and the risk measures computed from the base correlation mapping methods can be very misleading and counter-intuitive.

Here we briefly review the base correlation mapping methodology to setup further discussions. We assume that a base correlation surface has been calibrated to index tranches, where is the standard index strike. The superscripts are used to denote index portfolio and the bespoke portfolio. The correlation surface of a bespoke portfolio can be found via a mapping function :

| (1) |

Where represents the index and bespoke portfolios, including the notional amounts, default probabilities and recovery rates of all underlying names. Note that are the same on both side. Since is determined by and are all known, (1) defines an implicit function between and at time . The mapping function is usually monotonic in both and to ensure the uniqueness of the mapping between and . A bespoke tranche is then priced with the base correlation of the mapped index strike: . At-the-money (ATM), tranche loss proportion (TLP) and probability match (PM) are popular choices for the mapping function , readers are referred to [bcmap] for more details of these mapping functions.

Currently there are multiple credit indices representing different regions, such as CDX for the US and iTraxx for Europe. If a bespoke portfolio contains names from multiple geographical regions, the typical practice is to apply mapping to the credit indices of different regions separately, then the final price (or correlation) of the bespoke tranche is computed as the notional or risk weighted average of the prices (or correlations) of the different credit indices.

The main problem of this base correlation mapping procedure is the lack of identity consistency across portfolios. By “identity consistency”, we mean that an issuer’s default behavior should be the same no matter which portfolio it appears in; it should not change by merely moving from one portfolio to another portfolio. When computing the loss distribution of the bespoke portfolio, the base correlation mapping method clearly violates the identity consistency because the mapping function depends on all the names in the portfolio. The “weighting” procedure to credit indices of multiple regions also violates the identity consistency because the weighting factors also depend on all other names in the bespoke portfolio. The loss contribution from a unit notional of a specific name is therefore different across different portfolios because of the differences in the mapped bespoke correlation surfaces and the index weighting factors. The lack of identity consistency manifests itself as a number of practical problems.

The first common problem from the lack of identity consistency is the arise of negative single name deltas. Intuitively a buy-protection position on tranche should increase in value if an underlying single name spread widens; however the change in correlation caused by the base correlation mapping could result in larger changes in the tranche’s value than the change in spread, resulting in decrease in value of the buy-protection position. Negative single name delta is a serious challenge to risk management, as it leads to the absurd situation of needing to buy more protection on single names in order to hedge a buy-protection bespoke tranche position.

The dilemma of pricing fixed recovery tranche is another common problem. The protection payout in a fixed recovery tranche are computed using the recovery rate specified in the trade contract instead of the market recovery rate determined by the dealer auction process after the name’s default event. It has become a common practice to model the market recovery rate as stochastic; whereas the fixed tranche has to be modeled as deterministic recovery by definition. There can be (at least) two possible ways to price the fixed recovery tranche under base correlation mapping:

-

1.

apply the mapping with the stochastic market recovery, then use the resulting correlation surface to price the fixed recovery tranche.

-

2.

apply the mapping with the fixed recovery rate, the mapping function thus uses the stochastic market recovery for the index portfolio and the fixed recovery for the bespoke portfolio.

The rationale of the first method is to price the stochastic market recovery tranche consistently with the fixed recovery tranche on the same bespoke portfolio. On the other hand, the fixed recovery portfolio could differ significantly in overall riskiness and dispersion from the same portfolio with stochastic market recovery. The rationale of the second method is to price the fixed recovery tranches consistently with other stochastic market recovery tranches whose underlying portfolios have similar riskiness and dispersion as the fixed recovery portfolio. Both of these methods seem plausible but they give different prices. The cause of this dilemma is that the identity consistency is important when comparing the market recovery tranche with the fixed recovery tranche. Recognizing this, method 1 attempts to preserve the identity consistency by using the same correlation between the market and fixed recovery bespoke tranche, which results in incompatible prices from the direct application of the base correlation mapping as in method 2, which only considers the portfolio riskiness and dispersion, but not the identity consistency.

3 Methodology

The flaws in the base correlation mapping method described in the previous section have been well known among researchers and practitioners. A number of attempts have been made to develop better models to address the shortcomings of the base correlation model. As pointed out in [self], the minimum requirement for a model to price bespoke tranches consistently is to produce the joint distribution of default indicators (). Traditional default time copulas, such as random factor loading in [rfl] and the implied copula in [impliedcopula] and [skarke], produce the joint distributions of default time () whose marginal distribution is the 333Readers are referred to [self] for more discussion on the and .. Even though traditional default time copulas can be used for bespoke tranche pricing, they are very difficult to calibrate across multiple maturities because the global nature of the induces strong coupling between different maturities. [self] proposed the default indicator copula that models the instead of , the advantage of default indicator copula is that it is loosely coupled in time therefore it is much easier to calibrate across multiple maturities. [self] has shown that the default indicator copula can be easily calibrated to index tranches across multiple maturities even near the peak of the credit crisis. In this section, we propose a consistent method to price bespoke tranches based on the default indicator copulas. The same methodology can be applied to default time copulas even though the default indicator copula and the are sufficient for bespoke CDO pricing.

Once we have calibrated a default indicator copula to index tranches, it is a very natural step to take the calibrated copula and apply it to a bespoke portfolio. If there were only one liquid credit index in the market, the resulting bespoke pricing from this simple procedure would have been arbitrage free and had the desired property of identity consistency. However in reality, there are multiple credit indices whose tranches are traded liquidly, for example, CDX-IG, CDX-HY, and iTraxx are three main indices that each contains useful market information. A mixed bespoke portfolio that contains both investment grade and high yield names from the US and Europe should be priced using the market information from all three indices. The default indicator (or default time) copulas are typically one factor for numerical efficiency, which is adequate for a single well-diversified credit index, but it is clearly inadequate in dealing with bespoke portfolios that contain names of different geographical regions and credit qualities. The one factor default indicator copulas have to be extended to multiple factors in order to properly price bespoke tranches.

Recently there are several papers on the multi-factor approach to price bespoke tranches. [mcbspk] proposed a multi-factor default time copula that can be calibrated via a weighted Monte Carlo simulation method; [halpbspk] proposed a hybrid multi-factor model that mixes the top-down and bottom-up approach. Both of these methods assumes there are multiple common market factors behind each credit index. In [mcbspk], the factors are economic factors, such as geographical region, industry and sector. In [halpbspk], the factors are associated with whether a name appear in the bespoke tranche we want to price. Under these multi-factor extensions, the calibration to index tranches becomes more time-consuming because of the additional factors. [mcbspk] used a weighted Monte Carlo simulation to calibrate the joint distribution of all factors; [halpbspk] used a two step approach that a bottom up model is used to compute the prior loss distribution first; then a top-down method is used to adjust the prior distribution to match the observed index tranche prices. Both of these methods are still subjected to certain practical limitations: for example, [mcbspk] only showed calibration and pricing results for a single maturity; it is difficult numerically to extend the same Monte-Carlo based calibration method to multiple maturities because of the strong coupling of the default time copula across different maturities. The [halpbspk] approach, on the other hand, is not fully bottom-up, so the identity consistency is not fully preserved, and it can be cumbersome in dealing with real “bespoke” names that do not belong to any credit index.

3.1 Multi-factor Extension

In this section, a very simple and efficient multi-factor extension to the [self] model is described. This method is fully consistent and arbitrage free across both time and capital structure; and it preserves identity consistency by construction. This pricing method is free of all the flaws in the standard base correlation mapping methods, for example: its single name deltas are always positive and there is no ambiguity in the pricing of fixed recovery tranches.

Even though it is very important for a model to produce arbitrage free prices, there are other requirements that are also important in practice, for example: the model has to produce reasonable index tranche deltas for market making purposes, and the model’s bespoke and off-the-run index tranche prices should not be too far away from the current market consensus as determined by the base correlation model with the TLP mapping (abbreviated as BC-TLP). Even if a model can produce intrinsically consistent and arbitrage free prices, its acceptance would be difficult if its prices and tranche deltas are too far away from the current market observations and consensus. Also, the model has to be fast enough to compute the PVs and risks of a large number of bespoke tranches in a reasonable time before it can be used in practice. Later in this article, we will show that the proposed method does meet these practical requirements.

Readers are assumed to be familiar with the modelling framework described in [self], where it showed how a one-factor default indicator copula can be calibrated to index tranches across multiple maturities. Unlike the [mcbspk] and [halpbspk] where each credit index can be affected by multiple market factors, here we make the assumption that there is a single distinct market factor for each credit index. The reason behind this assumption is that the index portfolios such as CDX and iTraxx are well diversified therefore its tranche prices only reflect the broad market factor rather than any of the specific sector or industry factors. The same argument is also made in [mcbspk]. The advantage of this one-to-one mapping between market factors and liquid credit indices is that it does not add any complexity to the calibration procedure to index tranches, each credit index can be calibrated separately. Itraxx-S9, CDX-IG9 and CDX-HY9 are the three most important liquid credit indices in the current market444The most liquid series may not be the latest series, for example, CDX-IG9 is still the most liquid CDX series while the CDX-IG13 is the latest series.; we need to consider at least these three market factors in order to cover most bespoke tranches in practice. Because of the one-to-one mapping between market factor and liquid indices, this approach is easily extensible if other credit indices become liquid.

Given the globalization of world economy, the market factors behind these different credit indices are expected to be highly correlated: if US issuers are suffering large number of defaults we expect the same in European issuers, and vise versa. The correlation between different market factors (denoted as for the -th market factor) is a key risk factor for the mixed bespoke portfolios containing names across multiple regions. There are many possible ways to generate correlated processes from their calibrated marginal distributions. Since we only need the joint distribution of market factors at each time grid for the purpose of bespoke tranche pricing, we can take a very simple approach that models the correlation between market factors using a static copula function (e.g., the classic Gaussian Copula). Under the [self] framework, the marginal distribution of a single market factor is known from the calibration to its associated index tranches. Therefore, the joint distribution of the market factors is fully specified once the copula function is chosen. The time consistency is also preserved by construction as long as the same copula function is applied to all times.

Since the identities and the joint distributions of common market factors are fully specified by the liquid credit indices and the copula function, the bespoke tranche prices are fully determined if we can establish a fixed relationship between every issuer and every market factors. The fixed relationship between issuers and market factors ensures the identity consistency because this relationship does not depend on any other names; therefore a given issuer behaves the same way no matter which portfolio it appears. Given the one-to-one mapping between market factors and liquid indices, issuers that are part of a liquid index can only be exposed to the market factor of that index. But issuers that are not part of any liquid indices can be exposed to multiple market factors in the general case. For example, a conglomerate that operates in both the US and Europe may be sensitive to both of the CDX and iTraxx market factors. A multi-factor extension to the [self] model is therefore needed. The following is a multi-factor version of the conditional default probability function that can be used in Definition 3.4 of [self]:

| (2) |

where the subscript identifies the issuer and the superscript identifies the market factor. We use to denote the vector of all the market factors. The are constant factors that controls the relative exposure weights to different market factors. The is a time-dependent scaling factor so that the overall systemic contribution is a constant fraction of the unconditional cumulative hazard:

| (3) |

where is the unconditional default probability extracted from single name CDS curve; the is the cumulative hazard of the -th name at time ; the is a time-varying fraction for the systemic factor contribution. The is the idiosyncratic factor contribution which makes up the rest of the cumulative hazard:

Because the market factors are correlated, the expectation on the LHS of (3) has to be computed via a multi-dimensional integration, which may require a Monte Carlo simulation if the number of market factors are more than two. Therefore, the calibration of factor is more time-consuming than in the single factor case. However, the only needs to be computed once for each issuer, we can improve the computational efficiency by pre-computing and caching all the factors before valuing all the bespoke tranches. Under this multi-factor extension, the default indicators are independent conditioned on the vector of .

The specification in (2) has a simple econometric explanation if we re-write it in a different form:

| (4) |

which is simply a multi-factor linear regression of a name’s cumulative hazard (the LHS) using market factors as explanatory variables, the is the factor loading to the market factor and the is the residual idiosyncratic error that is specific to the j-th name.

Once we established the fixed relationship between all the issuers and market factors (i.e.: all the s and s), all the bespoke tranche prices are uniquely determined. This method of pricing bespoke tranches is fully bottom-up, and it does not involve any ad hoc mapping method. With this pricing method, the only sources of uncertainty in the bespoke tranche prices are the relative factor loadings of , the systemic fraction , and the correlation between market factors. All of these parameters have clear meanings and are closely related to market observables, therefore they can be easily estimate from the historical data. For example, the correlation between market factors can be estimated from historical spread movements of their corresponding indices; the relative factor loading can be estimated by regressing the single name’s spread movement to spread movements of relevant credit indices.

3.2 Semi-analytical Monte Carlo

A straight-forward Monte Carlo simulation of default time can be used to price bespoke tranches under the multi-factor extension. The easiest way to run a default time simulation is to use a co-monotonic555See [losslinker] for more details on co-monotonic Markov Chain. Markov Chain on the common market factors:

Monte Carlo Simulation of Default Time

-

1.

Draw a set of correlated uniform random numbers from the copula function of market factors; note that the has the same dimensionality as .

-

2.

At each time horizon , invert each element of the correlated to the corresponding market factor using the marginal distributions of the market factor. Because the same is used for all time horizon, the resulting market factor paths over time are effectively co-monotonic. Note that the market factor paths drawn this way are always monotonically increasing, therefore, the time consistency is fully preserved.

-

3.

Draw the individual name’s default time from the conditional default probabilities in (2) separately as the default times are independent conditioned on the path of over time. Also draw the recovery rate if stochastic recovery model is used.

-

4.

Compute the tranche payoff from the simulated default times, and average over many paths to get the tranche PV.

The modelling framework of [self] guarantees that we would obtained the same tranche prices using other Markov chains since the tranche price only depends on the , which is not affected by the choice of the Markov chain.

This default time simulation procedure is of theoretical interest since it evidenced that the suggested multi-factor extension is fully consistent and arbitrage free; however it is notoriously slow in computing single name risk measures because of the digital nature of the default event. The small perturbation in a single-name’s default probability only causes meaningful change in the tranche payoff if it happened to move the default time across the trade maturity. For vast majority of the simulated paths, small perturbation in a single name’s default probability does not cause any difference in the tranche payoff, therefore it requires a huge number of simulation paths for the single name risks to converge. Given the importance of single name risks, this default time simulation is clearly inadequate for practical purposes.

A better Monte Carlo simulation procedure can be devised by extending the standard one-factor semi-analytical pricing technique as described in [semianalytical] to multiple factors. Since the default indicators are independent conditioned on , the conditional tranche losses at time can be computed analytically (for example, using normal approximation). For the given time , the unconditional ETL under the multi-factor model can therefore be obtained by integrating the conditional ETL over the joint distribution of market factors, which requires a low-dimensional Monte Carlo simulation. We call this method the Semi-analytical Monte Carlo method. The following is the detailed steps of computing the ETL at a given time horizon using the semi-analytical Monte Carlo simulation:

Semi-Analytical Monte Carlo Simulation

-

1.

Draw a vector of at the time according to the copula function of the market factors.

-

2.

For each issuer, compute the conditional default probability from (2), and the conditional recovery rate if stochastic recovery is used.

-

3.

Compute the conditional mean and variance of portfolio losses, and use normal approximation to compute the conditional ETL, see [self] for more details on the normal approximation.

-

4.

Average the conditional ETL over many draws of to obtained the unconditional ETL

The above procedure can be repeated for each quarterly time grid to construct the full ETL curve of the tranche, and the tranche price immediately follows. This semi-analytical Monte Carlo simulation is a very natural extension from the typical one factor semi-analytical method. A similar simulation technique is also used in [mcbspk].

This semi-analytical Monte Carlo method is much more efficient than the simple Monte Carlo simulation of default indicators since its dimensionality (which is the number of market factors) is much smaller than the dimensionality of the default time simulation (which is the number of names in the bespoke portfolio). This semi-analytical Monte Carlo method can compute single name deltas very efficiently because the effects of single name perturbation are analytically captured in the conditional mean and variance of portfolio, which leads to a steady change in the conditional ETL for each simulated path.

3.3 Many-to-One Restriction

A even more efficient semi-analytical Monte Carlo method can be devised if we adopt the restriction that each issuer can only be associated with a single market factor, ie, the relationship between issuers and market factors is many-to-one instead of many-to-many. The many-to-one restriction is acceptable in practice because 1) most issuers’ main operations are within one geographical region, 2) the market factors are highly correlated to each other therefore those issuers operating in multiple regions can be well approximated using the market factor of its main operation. The second argument is more apparent with the regression form of the conditional default probability specification in (4): in a multi-factor regression analysis, there is only a small impact to the fit quality if we ignore factors that are highly correlated to existing factors.

The following is a possible procedure to associate issuers to a single market factor:

-

1.

Issuers that are part of a liquid index are only sensitive to the market factor of that index.

-

2.

Issuers whose main business is in Europe are only sensitive to the market factor of iTraxx.

-

3.

For issuers whose main business is in US, the investment grade names are only sensitivity to the CDX-IG9, and the high yield issuers are only sensitivity to CDX-HY9.

With the many-to-one restriction, the bespoke tranches can be priced extremely fast. First, we no longer need to run Monte Carlo simulation to calibrate the in (3). Secondly, we can greatly improve the efficiency of the semi-analytical Monte Carlo as the follows:

Semi-Analytical Monte Carlo Simulation with Many-to-One Restriction

-

1.

Divide he bespoke portfolio into sub-portfolios according to market factors. Each name can only appear in one sub-portfolio because of the many-to-one restriction.

-

2.

We use to denote the loss in the sub-portfolio associated with the th market factor. Since names in each sub-portfolio are exposed to the same market factor, the conditional mean and variance of each sub-portfolio’s loss (denoted as and ) can be pre-computed and cached for each possible value of (here we assume that the distribution of market factors can be discretely sampled).

-

3.

The conditional loss distribution of the total portfolio can then be constructed from the conditional loss distribution of the sub-portfolios. Since the loss of the whole portfolio is the sum of the losses from sub-portfolio () and the sub-portfolio losses are independent conditioned on , the conditional mean and variance of the whole portfolio loss are simply the summation of those of the sub-portfolios: , . The conditional expected tranche loss (ETL) of the whole portfolio can then be obtained using normal approximation.

-

4.

The unconditional ETL can then be computed by integrating the conditional ETL over the multi-dimensional distribution of the market factors via a low-dimensional Monte Carlo simulation.

Since the conditional mean and variance are pre-computed and cached for each sub-portfolio, the above Monte Carlo simulation is extremely fast. The many-to-one restriction may seem restrictive for issuers that operate in multiple regions. However, given that the majority of issuers mainly operate in one geographical region, it is a good trade off in practice since this restriction leads to an extremely simple and efficient method to price bespoke tranches, and it still captures the main risk factors in bespoke tranches.

In the following discussions, we use the abbreviation DIC and SAMC to refer to the default indicator copula and the semi-analytical Monte Carlo pricing method for bespoke tranches.

4 Numerical Results

In this section, we present some numerical results of bespoke tranche pricing with DIC-SAMC, with special attention to practical issues such as deltas and comparisons to the BC-TLP model.

The market data is taken from Dec. 31st, 2009. The DIC is calibrated to the expected tranche loss of CDX-IG9, iTraxx-S9 and CDX-HY9 separately. The details of the calibration procedure is described in [self]. Since the standard maturities of iTraxx-S9 are half year longer than those of CDX-IG9 and CDX-HY9, for the purpose of illustrating the bespoke pricing with mixed portfolios, we calibrated the iTraxx-S9 tranches at the standard maturities of CDX-IG9 and CDX-HY9. Since the ETLs are not directly observable, a standard base correlation model is used to extract the ETLs from index tranche prices; the ETLs are then used as calibration input to the DIC model. For the rest of this paper, all tenors refer to those of the CDX-IG9 index, e.g. 5Y means Dec 20, 2012, and 7Y means Dec 20, 2014.

4.1 and Model Calibration

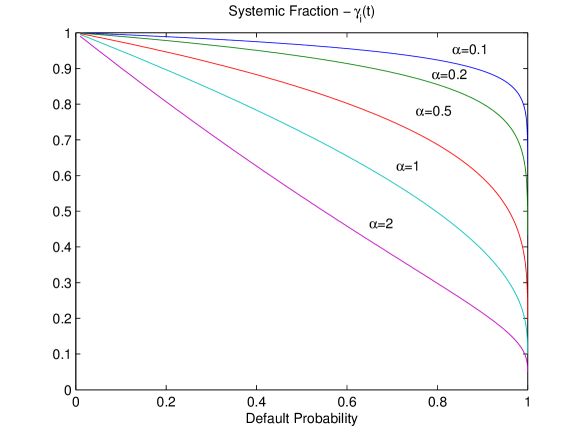

Before we discuss the bespoke tranche pricing, we need to choose the in (2) which is the fraction of systemic factors’ contribution to the overall cumulative hazard. This parameter is of importance because it affects the calibration and resulting bespoke prices. Instead of estimating from historical time series, we choose a very simple functional form for the parameter. It is a common belief that riskier names are more sensitive to idiosyncratic risk and safer names are more sensitive to the systemic risk; therefore we choose the marginal systemic fraction to be a decreasing function of the cumulative hazard. We denote the cumulative hazard as for the -th name. A simple exponential function is convenient for the marginal systemic fraction since it is always within 0 and 1; and the is a free parameter that controls how fast the marginal systemic faction decrease with the cumulative hazard. Then , being the cumulative systemic fraction, can be computed from the marginal systemic fraction:

| (5) |

For simplicity, we choose to use the same parameter for all issuers even though they could be name specific. Figure 1 showed the for different values.

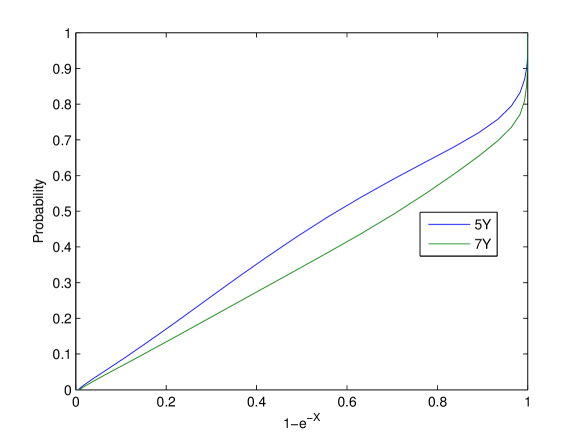

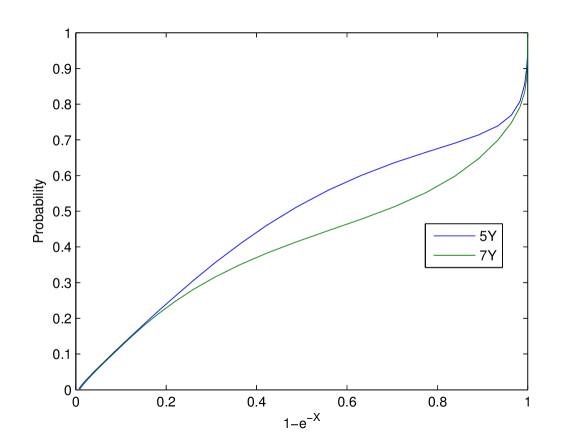

The DIC is calibrated to both the 5Y and 7Y ETL of CDX-IG9, CDX-HY9 and iTraxx-S9 with two different values of and . Only the 5Y and 7Y tenors are used in this study because all three indices trade liquidly at these two tenors. The model can be calibrated very closely to input ETLs of all three indices with either value, table 1 showed the ETL input and the DIC model fit. Figure 2 showed the calibrated distribution of the common factor for the CDX-IG9 index. The calibrated distributions of are well behaved for both values. The calibrated CDF curves at the two maturities never cross each other because the common factor in the [self] framework has to be an increasing process, and this monotonic constraint is built into the calibration procedure.

| CDX-IG9 | Market ETL | Fit with | Fit with | ||||

|---|---|---|---|---|---|---|---|

| Att | Det | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y |

| 0.0% | 2.4% | 67.15% | 82.14% | 67.23% | 82.18% | 67.22% | 82.41% |

| 2.4% | 6.5% | 23.20% | 42.42% | 23.24% | 42.40% | 23.24% | 42.56% |

| 6.5% | 9.6% | 7.52% | 21.79% | 7.53% | 21.71% | 7.53% | 21.86% |

| 9.6% | 14.8% | 3.17% | 10.30% | 3.18% | 10.19% | 3.18% | 10.24% |

| 14.8% | 30.3% | 0.81% | 2.68% | 0.83% | 2.80% | 0.83% | 2.92% |

| 30.3% | 61.2% | 0.23% | 1.90% | 0.33% | 1.86% | 0.33% | 1.77% |

| iTraxx-S9 | Market ETL | Fit with | Fit with | ||||

|---|---|---|---|---|---|---|---|

| Att | Det | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y |

| 0.0% | 3.0% | 35.59% | 56.69% | 35.60% | 55.72% | 35.60% | 56.77% |

| 3.0% | 6.0% | 7.73% | 22.06% | 7.73% | 21.70% | 7.73% | 22.19% |

| 6.0% | 9.0% | 4.56% | 13.46% | 4.56% | 13.12% | 4.56% | 13.55% |

| 9.0% | 12.0% | 2.27% | 7.31% | 2.27% | 7.05% | 2.27% | 7.39% |

| 12.0% | 22.0% | 0.80% | 3.02% | 0.80% | 3.06% | 0.80% | 3.01% |

| 22.0% | 60.0% | 0.51% | 1.84% | 0.53% | 1.97% | 0.53% | 1.84% |

| CDX-HY9 | Market ETL | Fit with | Fit with | ||||

|---|---|---|---|---|---|---|---|

| Att | Det | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y |

| 0.0% | 4.0% | 78.29% | 91.76% | 78.29% | 91.67% | 78.29% | 92.15% |

| 4.0% | 15.6% | 36.47% | 62.78% | 36.47% | 62.54% | 36.48% | 62.54% |

| 15.6% | 27.2% | 13.20% | 32.05% | 13.20% | 31.81% | 13.20% | 32.00% |

| 27.2% | 56.3% | 4.55% | 21.63% | 4.55% | 21.42% | 4.55% | 21.49% |

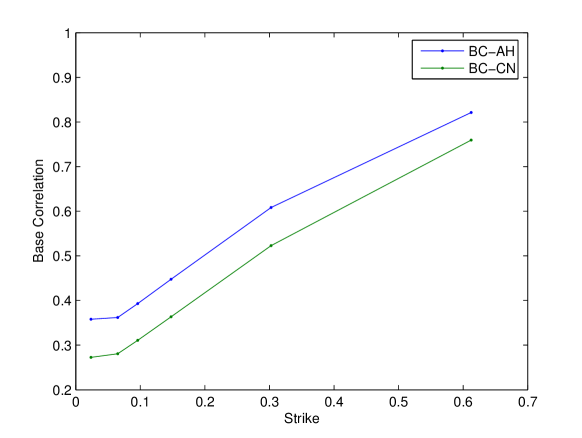

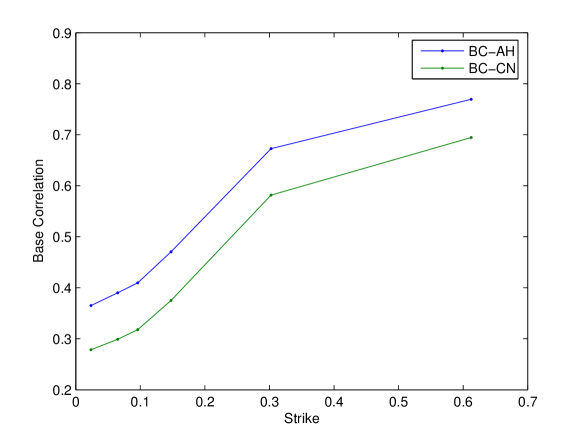

For comparison purposes, the base correlation model is also calibrated to the three indices. Two different stochastic recovery specifications are used, the first is the [hitier] method with a recovery markdown factor of 0.01, the second is the cumulative normal recovery proposed in the [rfl]. With different stochastic recovery specifications, the calibrated base correlation curves are different, as shown in Figure 3, where BC-AH and BC-CN represents the two different stochastic recovery models.

5Y

7Y

4.2 Index Tranche Delta

A practical concern of moving away from the market standard BC-TLP model is the changes in model deltas. We first give a brief description on the index tranche delta for readers who are not familiar with the index tranche market. The index tranches are commonly traded in a delta-hedged package, i.e., when a client enters a tranche trade with a dealer, he also trades a hedging index swap with the same dealer; so the dealer’s book is delta hedged with the new trade. The hedge ratio is published by the dealer as part of the index tranche quote, which is normally referred as the “tranche delta” or “leverage ratio”. The index swaps are much more liquid than the index tranches, and their prices are updated much more frequently throughout a trading day. With this delta-exchange mechanism, an index tranche trader does not need to publish new index tranche quotes every time when the index swap spread moves; he only need to do so if his current level is different from the delta-adjusted prices of the previous quote. This delta exchange mechanism implies that the index tranche prices are the delta-adjusted levels for small movements in the index swap spreads.

We use “market delta” to refer to the index tranche deltas quoted by the market makers and “model delta” to refer to the tranche delta calculated by a model. The model delta is usually computed by bumping the index swap spreads, re-applying the swap adjustment and keeping the model’s correlation parameters constant666The market index swap spread is usually different from the “intrinsic” spread computed from the the underlying single name CDS spreads. This basis between intrinsic and market index swap spread can be quite large when market is in distress. Before index tranche pricing and calibration, the underlying single name spreads are usually adjusted to match the current market index swap spread because the market index swap spread is more liquid than the underlying single names’ CDS spreads. This procedure is commonly referred as “index swap adjustment”.. [bardelta] has shown that the model delta is dependent upon how the single name spreads are bumped during the index swap adjustment. For example, an additive bump where the bump sizes are constant across all names produces very different model deltas from a multiplicative bump where the bump sizes are proportional to the current spread levels. Currently the CDX and iTraxx market deltas are closer to the base correlation model deltas with additive bumps than the multiplicative bumps.

The market tranche deltas are typically determined by a dealer poll process: each major dealer submits their market delta quotes to a dealer poll at the market open, and the averages of all dealers’ submission are then used by all the dealers as the market deltas for that day. Individual dealer usually submit their model delta to the dealer poll, which can be quite different from each other due to difference in model and swap adjustment assumptions. This dealer poll process helps improve the transparency in the index tranche market by ensuring that all major dealers are trading with similar tranche deltas despite their model differences. Therefore, market makers are generally experienced in dealing with the difference between their model deltas (which is their submission to the dealer poll) and market deltas (which is the average of the dealer poll).

| CDX-IG9 | BC-AH | BC-CN | DIC | DIC | |||||

|---|---|---|---|---|---|---|---|---|---|

| Att | Det | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y |

| 0.0% | 2.4% | 4.20 | 1.78 | 4.21 | 1.75 | 5.10 | 2.17 | 4.92 | 1.98 |

| 2.4% | 6.5% | 7.83 | 4.67 | 7.70 | 4.58 | 8.53 | 5.44 | 8.17 | 5.13 |

| 6.5% | 9.6% | 4.58 | 4.28 | 4.54 | 4.20 | 5.96 | 5.56 | 6.75 | 6.02 |

| 9.6% | 14.8% | 2.39 | 2.70 | 2.41 | 2.64 | 2.93 | 5.12 | 2.64 | 4.96 |

| 14.8% | 30.3% | 0.68 | 1.11 | 0.68 | 1.13 | 1.01 | 1.07 | 1.09 | 1.18 |

| 30.3% | 61.2% | 0.20 | 0.55 | 0.23 | 0.59 | 0.06 | 0.13 | 0.05 | 0.10 |

| iTraxx-S9 | BC-AH | BC-CN | DIC | DIC | |||||

|---|---|---|---|---|---|---|---|---|---|

| Att | Det | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y |

| 0.0% | 3.0% | 11.37 | 5.98 | 11.18 | 5.84 | 16.26 | 8.59 | 16.20 | 8.47 |

| 3.0% | 6.0% | 5.22 | 5.04 | 5.12 | 4.93 | 4.15 | 5.43 | 4.10 | 5.39 |

| 6.0% | 9.0% | 3.37 | 3.70 | 3.30 | 3.71 | 4.12 | 5.27 | 4.19 | 5.22 |

| 9.0% | 12.0% | 1.80 | 2.52 | 1.96 | 2.33 | 3.85 | 4.84 | 3.85 | 5.00 |

| 12.0% | 22.0% | 0.92 | 1.22 | 0.92 | 1.17 | 0.84 | 1.12 | 0.86 | 1.27 |

| 22.0% | 60.0% | 0.35 | 0.58 | 0.38 | 0.64 | 0.07 | 0.26 | 0.07 | 0.24 |

| CDX-HY9 | BC-AH | BC-CN | DIC | DIC | |||||

|---|---|---|---|---|---|---|---|---|---|

| Att | Det | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y |

| 0.0% | 4.0% | 2.03 | 0.62 | 1.96 | 0.60 | 1.92 | 0.53 | 1.96 | 0.60 |

| 4.0% | 15.6% | 2.90 | 1.63 | 2.86 | 1.62 | 3.33 | 2.22 | 3.05 | 1.88 |

| 15.6% | 27.2% | 1.74 | 1.49 | 1.74 | 1.48 | 2.11 | 1.37 | 2.40 | 1.63 |

| 27.2% | 56.3% | 0.79 | 1.63 | 0.83 | 1.65 | 0.69 | 1.29 | 0.66 | 1.34 |

Table 2 showed the additive model deltas from the calibrated DIC model computed by keeping the marginal distribution of constant, as well as the model deltas from the base correlation model. The deltas in table 2 is the ratio between the change in tranche ETL and the change in index swap expected loss. This ratio is different from the usual tranche delta definition as the ratio of PV changes. We choose to compare the models’ expected loss deltas since they do not depend on the coupon payments of the tranche, thus making it easier to compare across capital structure.

Different stochastic recovery models only make a very small difference on the model deltas under the base correlation model, so is different values under the DIC model. The model deltas from the DIC model are roughly in line with the model deltas from the base correlation except that the DIC deltas tend to be lower for senior tranches and higher for equity tranches for the two investment grade indices. Certain tweaks to the DIC model can bring its model deltas closer to the BC-TLP model deltas. For example, a “armageddon” event can be introduced, under which all the credits in a portfolio default together. If a portion of the index swap spread bump is attributed to the increase in the probability of the armageddon event, then the deltas in the senior tranches would become higher and equity tranche would become lower, which brings the DIC model deltas closer to the BC-TLP delta. The idea of armageddon event is not new, for example, it appeared in an early work of [compbasket]. However, it is questionable whether the practical benefits from such a tweak, whose sole purpose is to bring the DIC model deltas closer to the BC-TLP model deltas, would outweigh the added complexity to the model, especially given that the market makers are already experienced in dealing with the difference between model deltas and market deltas.

4.3 Price Index Tranches as Bespoke

| iTraxx-S9 | Market ETL | Difference from Market ETL if Priced as Bespoke | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| BC-AH | BC-CN | DIC | DIC | ||||||||

| Att | Det | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y |

| 0.0% | 3.0% | 35.59% | 56.69% | -1.08% | -1.54% | -0.79% | -1.60% | -0.31% | -2.54% | -0.82% | -2.89% |

| 3.0% | 6.0% | 7.73% | 22.06% | 4.20% | 4.05% | 4.21% | 4.31% | 2.25% | 2.18% | 2.80% | 3.06% |

| 6.0% | 9.0% | 4.56% | 13.46% | 0.63% | 1.82% | 0.46% | 1.96% | -0.21% | -0.65% | -0.32% | -0.53% |

| 9.0% | 12.0% | 2.27% | 7.31% | 0.23% | 1.85% | 0.25% | 1.72% | 0.25% | -0.78% | 0.35% | -0.57% |

| 12.0% | 22.0% | 0.80% | 3.02% | 0.24% | 0.36% | 0.21% | 0.33% | 0.25% | -0.12% | 0.27% | 0.07% |

| 22.0% | 60.0% | 0.51% | 1.84% | -0.33% | -0.64% | -0.33% | -0.63% | -0.16% | 0.05% | -0.16% | -0.03% |

| RMS | 0.00% | 0.00% | 1.80% | 2.08% | 1.77% | 2.18% | 0.94% | 1.43% | 1.21% | 1.75% | |

| CDX-HY9 | Market ETL | Difference from Market ETL if Priced as Bespoke | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| BC-AH | BC-CN | DIC | DIC | ||||||||

| Att | Det | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y |

| 0.0% | 4.0% | 78.29% | 91.76% | 0.44% | 2.36% | 0.70% | 2.18% | -1.75% | -0.52% | 0.93% | 2.58% |

| 4.0% | 15.6% | 36.47% | 62.78% | 3.63% | 5.63% | 3.66% | 5.47% | -1.04% | 0.24% | -2.02% | -1.17% |

| 15.6% | 27.2% | 13.20% | 32.05% | 0.07% | 5.95% | -0.05% | 5.92% | 2.72% | 6.26% | 3.76% | 8.07% |

| 27.2% | 56.3% | 4.55% | 21.63% | -1.72% | -11.08% | -1.71% | -10.98% | 0.47% | -2.64% | 0.10% | -3.17% |

| RMS | 0.00% | 0.00% | 2.02% | 6.99% | 2.05% | 6.90% | 1.71% | 3.41% | 2.18% | 4.56% | |

Standard tranches on one index can also be viewed as bespoke tranches to another index, it is interesting to compare the observed index tranche prices against the model prices if they were valued as bespoke tranches to another index. It is certainly preferable if the market prices are close to the “as bespoke” model prices since it means that the model’s response to changes in the underlying credit portfolio is similar to the market’s response.

In this study, we priced the CDX-HY9 and iTraxx-S9 as bespoke tranches to the CDX-IG9 using both the DIC model and the standard BC-TLP model. CDX-IG9 is chosen to be the “index” because it has similar properties to both iTraxx-S9 and CDX-HY9: the CDX-IG9 and iTraxx-S9 are both investment grade indices and the CDX-IG9 and CDX-HY9 are both north American names. In comparison, the iTraxx-S9 and CDX-HY9 indices are more dissimilar to each other.

Table 3 showed the difference between the market ETLs and the ETLs priced as bespoke tranches to the CDX-IG9. Interestingly, the differences between the market and “as bespoke” ETL from the DIC model are generally smaller than those from the BC-TLP model. The performance of DIC model is quite promising in this study considering that the BC-TLP method has been long established as the market standard.

4.4 Bespoke Tranche Pricing

In this example, we show the bespoke pricing results for a super mixed portfolio, which is a union of the CDX-IG9, iTraxx-S9 and CDX-HY9 portfolios. Each standard index portfolio makes up 1/3 of the total notional in the super mixed portfolio. Since all the names in this super mix portfolio appear in standard indices, the many-to-one restriction is satisfied therefore we can use the fast simulation method described in section 3.3. Table 4 showed the prices from the DIC-SAMC and the BC-TLP. The DIC-SAMC method uses , and the BC-TLP method uses the stochastic recovery model from [hitier].

5Y Bespoke ETL

| SuperMix | DIC-SAMC: Market Factor Correlations | BC-TLP with Different Mapping | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Att | Det | 0 | 0.2 | 0.4 | 0.6 | 0.8 | 1 | CDX | ITX | HY9 | N_WA | R_WA |

| 0% | 3% | 82.97% | 80.50% | 78.16% | 76.00% | 74.07% | 72.25% | 71.04% | 75.48% | 69.88% | 72.13% | 70.78% |

| 3% | 7% | 36.68% | 36.12% | 35.32% | 34.37% | 33.46% | 32.53% | 35.76% | 29.93% | 32.05% | 32.58% | 32.56% |

| 7% | 10% | 15.42% | 16.09% | 16.44% | 16.54% | 16.47% | 16.12% | 18.88% | 14.22% | 16.58% | 16.56% | 16.77% |

| 10% | 15% | 7.49% | 8.00% | 8.40% | 8.71% | 8.94% | 8.88% | 8.80% | 7.95% | 9.26% | 8.67% | 9.01% |

| 15% | 30% | 2.92% | 3.14% | 3.31% | 3.45% | 3.53% | 3.69% | 2.52% | 2.39% | 3.73% | 2.88% | 3.33% |

| 30% | 60% | 0.05% | 0.13% | 0.26% | 0.46% | 0.65% | 0.77% | 0.52% | 1.56% | 0.93% | 1.00% | 0.92% |

7Y Bespoke ETL

| SuperMix | DIC-SAMC: Market Factor Correlations | BC-TLP with Different Mapping | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Att | Det | 0 | 0.2 | 0.4 | 0.6 | 0.8 | 1 | CDX | ITX | HY9 | N_WA | R_WA |

| 0% | 3% | 96.22% | 94.49% | 92.80% | 91.13% | 89.52% | 88.05% | 89.32% | 91.60% | 86.14% | 90.26% | 87.46% |

| 3% | 7% | 70.88% | 67.94% | 65.25% | 62.86% | 60.76% | 58.81% | 62.97% | 61.03% | 57.47% | 60.90% | 58.99% |

| 7% | 10% | 42.93% | 41.97% | 40.73% | 39.36% | 37.92% | 35.63% | 43.06% | 38.07% | 36.27% | 37.68% | 37.81% |

| 10% | 15% | 30.99% | 30.62% | 29.95% | 29.16% | 28.50% | 27.43% | 27.85% | 24.26% | 23.26% | 26.95% | 24.27% |

| 15% | 30% | 12.99% | 13.57% | 13.92% | 14.14% | 14.62% | 15.37% | 8.61% | 8.66% | 16.63% | 12.72% | 14.05% |

| 30% | 60% | 0.58% | 1.04% | 1.57% | 2.07% | 2.45% | 2.31% | 3.79% | 4.95% | 3.52% | 3.11% | 3.76% |

In the DIC-SAMC method, we assumed the pair-wise correlation between the three market factors are the same even though it is very easy to accommodate a full correlation matrix. It is very intuitive in table 4 that the DIC-SAMC produces lower equity tranche ETLs and higher senior tranche ETLs with higher correlations between market factors. In the BC-TLP section of table 4, we reported the resulting ETLs from mappings to each individual index, as well as the notional and risk weighted average ETL in the “N_WA” and “R_WA” columns. The notional and risk weighted average of the BC-TLP ETLs are very close to the DIC-SAMC results with very high correlation between 80% and 100%. This is somewhat expected because the BC-TLP is still a one factor model even though it is mapped to three indices separately. The effects of lower correlations between market factors cannot be produced from such a one-factor model. On the other hand, the DIC-SAMC method is able to produce the pricing effects of lower correlations between market factors. The one-factor limitation of BC-TLP is not yet a problem in practice since market participants do expect different market factors to be highly correlated. For example, table 5 showed the correlations between the index swap spread returns estimated from historical weekly index spreads from Mar 2008 to Feb 2010. The correlations are all in the mid 90% between the three main indices. However, being able to price with low market factor correlation is certainly an important advantage in DIC-SAMC since it helps the market participants to gauge the correlation risk between market factors, and allows them to manage or trade such risk.

| CDX-IG9 | CDX-HY9 | Itraxx-S9 | |

|---|---|---|---|

| CDX-IG9 | 1 | 0.9328 | 0.9625 |

| CDX-HY9 | 0.9328 | 1 | 0.9531 |

| Itraxx-S9 | 0.9625 | 0.9531 | 1 |

Since the normal approximation in the DIC-SAMC could result in a pricing error of up to 0.1%777see [self] for more details., there is no benefit to run the DIC-SAMC method with higher accuracy than 0.1%. It only takes about 250K simulation paths in DIC-SAMC for the pricing error to be less than 0.1% for all tranches even without using any variance reduction technique. The left half in table 6 showed the simulation error with 250K path and no variance reduction, in which case the simulation error is almost the same for different correlation values among market factors. With 250K path, the DIC-SAMC takes less than a second to compute the ETL at a given time horizon on a regular PC; thus a typical bespoke tranche pricing only takes a few seconds with DIC-SAMC assuming that the simulation needs to be run on every quarterly date.

| SuperMix | Regular DIC-SAMC | DIC-SAMC w/ Control Variate | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Absolute Err | Relative Err | Absolute Err | Relative Err | ||||||

| Att | Det | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y | 5Y | 7Y |

| 0.00% | 3.00% | 0.056% | 0.036% | 0.077% | 0.041% | 0.019% | 0.016% | 0.026% | 0.018% |

| 3.00% | 7.00% | 0.080% | 0.078% | 0.245% | 0.133% | 0.027% | 0.026% | 0.083% | 0.044% |

| 7.00% | 10.00% | 0.067% | 0.089% | 0.413% | 0.251% | 0.028% | 0.036% | 0.175% | 0.100% |

| 10.00% | 15.00% | 0.050% | 0.088% | 0.567% | 0.320% | 0.023% | 0.046% | 0.256% | 0.169% |

| 15.00% | 30.00% | 0.032% | 0.056% | 0.858% | 0.362% | 0.016% | 0.021% | 0.442% | 0.139% |

| 30.00% | 60.00% | 0.009% | 0.020% | 1.168% | 0.875% | 0.007% | 0.014% | 0.973% | 0.606% |

A number of variance reduction techniques could be applied to further improve the computational speed, for example the quasi-random sequence and importance sampling could be effective. In particular, the 100% correlation case can be used as an effective control variate for the DIC-SAMC. With 100% correlation, the multiple market factors reduce to a single market factor, therefore bespoke tranches can be priced using a regular one-factor semi-analytical method without simulation. This control variate is particularly effective if the correlations between market factors are high, which is indeed the case in practice. The right half in Table 6 showed the simulation error with 90% correlation between market factors using the control variate. The simulation error has been significantly reduced by the control variate, which translates to roughly 3-5 times reduction in computation time.

4.5 Single Name Deltas

The single name deltas are the most time consuming risk measures to compute for bespoke tranches. Using the DIC-SAMC method, the path-wise single name deltas can be computed analytically from the normal approximation, therefore, it is very fast to compute the single name deltas by integrating the path-wise deltas directly within the DIC-SAMC simulation. In the SuperMix portfolio of the previous example, the path-wise delta integration method only takes about 5 seconds to achieve reasonable convergence for all the single name deltas at a given tenor. Overall, the PV and single name risks for a single tranche only take several minutes to compute on a regular PC, therefore the DIC-SAMC method is fast enough to support a large trading book in practice with a small server farm. For example, a trading book of 2,000 bespoke trades would take about 4 hours to compute PVs and single name risks using a server farm with 40 CPUs.

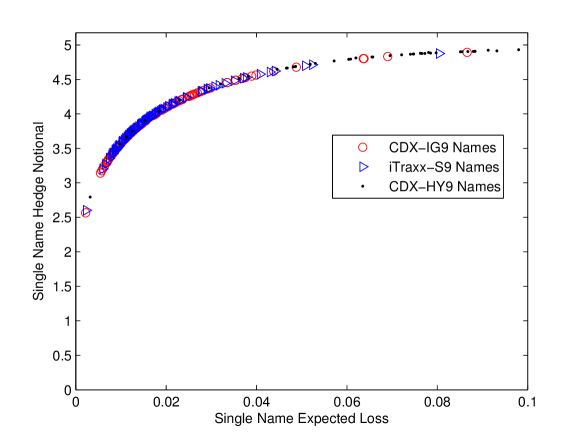

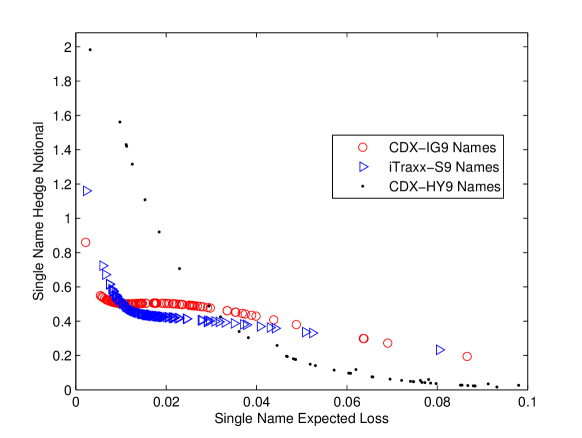

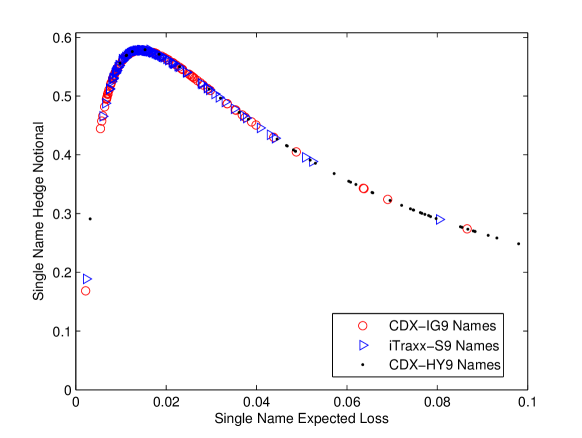

DIC-SAMC 5Y 0-3%

BC-TLP 5Y 0-3%

DIC-SAMC 5Y 7-10%

BC-TLP 5Y 7-10%

DIC-SAMC 5Y 30-60%

BC-TLP 5Y 30-60%

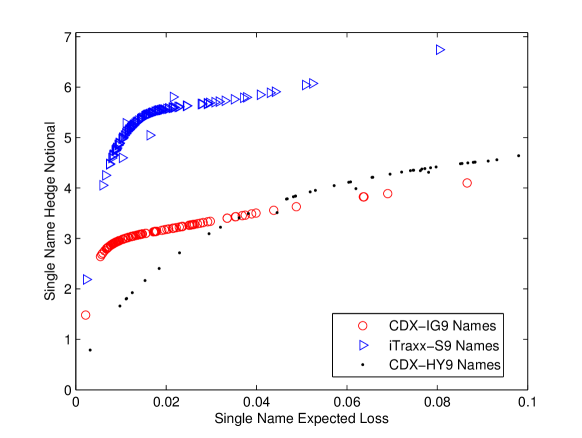

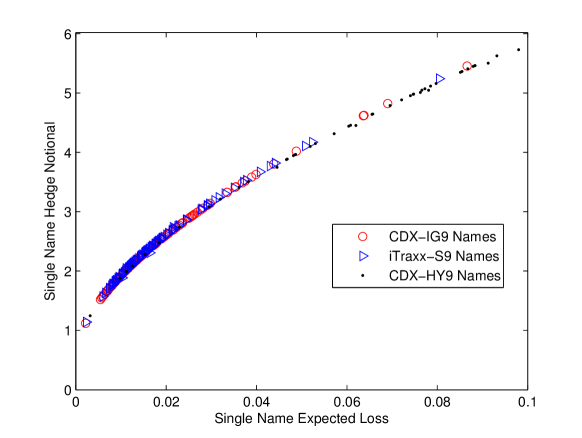

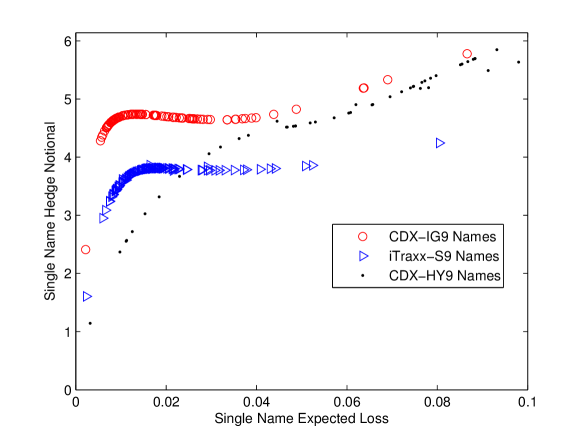

Figure 4 showed the single name hedge ratios from both the DIC-SAMC and BC-TLP mothods for a few tranches on the SuperMix portfolio with 90% correlation between market factors. The hedge ratios are computed as the ratio of change in tranche expected loss over the single name expected loss for a small perturbation in the single name default probability. Since the single name notionals are not uniform in the SuperMix portfolio, we normalized the resulting hedge ratios by each single name’s notional amount in the SuperMix portfolio in order to compare the risk contribution from a unit amount of single name notional. A few interesting observations can be made from figure 4:

-

•

The single name risks from the DIC-SAMC methods depend on the name’s associated market factor. Names from different credit indices can have different single name risks even if their default probability and recovery rates are identical. This is a natural consequence of the multiple market factors and the identity consistency in the DIC-SAMC model. The BC-TLP single name deltas do not depends on the credit index association as BC-TLP is a one-factor model without identity consistency.

-

•

In DIC-SAMC, the junior tranches are more sensitive to riskier names and senior tranches are more sensitive to safer names, which is quite intuitive. In BC-TLP, the 30-60% tranche is much more sensitive to names with expected loss between 1-2%, which is rather counter-intuitive and difficult to explain.

-

•

The deltas in DIC-SAMC are always positive by construction (subject to the Monte Carlo simulation error), while the BC-TLP could produce negative deltas. Even though there is no negative single name deltas shown in table 4, the BC-TLP model did produce some negative deltas for the SuperMix portfolio when mapped to the iTraxx-S9 index.

DIC-SAMC 5Y

| SuperMix | Mkt Factor Corr = 0.8 | Mkt Factor Corr = 1 | |||||

|---|---|---|---|---|---|---|---|

| Att | Det | Rec = 0.2 | Rec = 0.4 | Rec = 0.6 | Rec = 0.2 | Rec = 0.4 | Rec = 0.6 |

| 0% | 3% | 80.50% | 74.47% | 63.84% | 78.70% | 72.68% | 62.20% |

| 3% | 7% | 43.39% | 32.78% | 19.51% | 42.27% | 31.89% | 19.05% |

| 7% | 10% | 23.02% | 15.08% | 7.15% | 22.66% | 14.73% | 7.32% |

| 10% | 15% | 12.77% | 7.55% | 3.50% | 12.64% | 7.62% | 3.76% |

| 15% | 30% | 4.57% | 2.47% | 0.83% | 4.86% | 2.78% | 0.98% |

| 30% | 60% | 0.83% | 0.33% | 0.04% | 1.03% | 0.43% | 0.11% |

BC-TLP 5Y

| SuperMix | Map with Stoch Recovery | Map with Fixed Recovery | |||||

|---|---|---|---|---|---|---|---|

| Att | Det | Rec = 0.2 | Rec = 0.4 | Rec = 0.6 | Rec = 0.2 | Rec = 0.4 | Rec = 0.6 |

| 0% | 3% | 80.57% | 76.50% | 65.03% | 80.29% | 74.78% | 65.22% |

| 3% | 7% | 42.44% | 32.25% | 20.45% | 40.12% | 32.65% | 21.36% |

| 7% | 10% | 22.82% | 14.65% | 7.28% | 17.21% | 15.44% | 7.62% |

| 10% | 15% | 12.31% | 7.06% | 2.83% | 6.84% | 7.54% | 2.75% |

| 15% | 30% | 4.07% | 1.98% | 0.58% | 7.94% | 2.27% | 0.31% |

| 30% | 60% | 1.20% | 0.54% | 0.03% | 0.70% | 0.35% | 0.00% |

4.6 Fixed Recovery Tranches

Table 7 showed the 5Y ETLs of the SuperMix portfolio priced with fixed recovery rates of 20%, 40% and 60% using both the DIC-SAMC and BC-TLP. The BC-TLP uses the [hitier] stochastic recovery model and notional weighted average for mappings to different indices. Table 7 showed the DIC-SAMC prices with two different market factor correlations and BC-TLP prices using both mapping methods described in section 2. The first method uses stochastic market recovery rate in the TLP mapping, then prices the fixed recovery tranche with the same base correlation surface as the regular market recovery tranche; the second method uses the fixed recovery rate directly for the bespoke tranche in the TLP mapping. The DIC-SAMC prices of the fixed recovery trades are generally closer to the first BC-TLP method, which is not surprising because the first BC-TLP method preserves the identity consistency between the market and fixed recovery tranches. Also notable is that the second BC-TLP mapping method produces an obvious arbitrage between the 10-15% and 15-30% tranches for 20% fixed recovery.

4.7 Quanto Adjustment

The consistent DIC model can be useful in a number of practical situations where BC-TLP meets its limitations. In this example, we show how to compute the quanto adjustment for index tranches denominated in a different currency from the index currency. The key factor in the quanto adjustment is the correlation between defaults and the exchange rates, which is difficult to capture properly under the base correlation framework.

We have been ignoring the quanto adjustment for iTraxx names in the previous examples of the SuperMix portfolio. In this example, we’ll show that the quanto adjustment can be easily incorporated into the DIC-SAMC method by adding the exchange rate as another market factor.

We use CDX-IG9 tranches whose protection notional is denominated in EUR as an example. These quanto tranches are easier to price in the US risk neutral measure since the underlying single name CDS curves in the CDX portfolio are constructed in this measure. The USD is expected to appreciate against EUR if the US economy is doing better than the European economy, and vise versa. Since what’s important is the relative health of the two economy, it is a rather natural idea to correlate the USD/EUR exchange rate with the difference between the CDX market factor and the iTraxx market factor. However, since market factor in (2) does not have an absolute scale as the DIC remains the same if we scale up and scale down by the same factor, we instead choose to correlate the USD/EUR exchange rate with the difference between the conditional expected losses in the CDX and iTraxx portfolio with unit notional amounts, which is a metric with an absolute scale. The difference between conditional expected portfolio loss (DCEPL) can be written as:

The DCEPL appears rather peculiar since the difference between the portfolio loss (i.e., ) seems to be a more natural quantity to correlate with the exchange rate. However, the DPL depends on idiosyncratic dynamics, which requires the full default time simulation. The DCEPL, on the other hand, does not depends on the idiosyncratic dynamics, thus it can be easily incorporated into the DIC-SAMC procedure. Therefore, it is much more efficient numerically to use DCEPL instead of DPL.

The calculation for quanto adjustment using DCEPL thus involves two steps: the first step runs a DIC-SAMC simulation with both iTraxx and CDX portfolios to construct the distribution of the DCEPL; the 2nd step runs the DIC-SAMC simulation again and uses a Gaussian Copula to generate the correlated USD/EUR exchange rate based on the DCEPL for each draw of ; the exchange rate is then used to convert the ETL from EUR to USD. The distribution of the DCEPL from the first step is used as marginal distribution in the Gaussian Copula to draw the correlated USD/EUR exchange rate in the second step.

Table 8 showed the quanto adjustment amounts for CDX-IG9 5Y tranches assuming the USD/EUR exchange rate is lognormal with a cumulative volatility of 30% at the 5Y maturity. The general features of the quanto adjustment from the DIC-SAMC simulation are quite intuitive: the quanto adjustments are generally positive and is more significant for senior tranches in relative scale because when CDX-IG9 suffers large losses, it is more likely that USD would depreciate, thus leading to more value in the protection denominated in EUR. Table 8 also showed that the quanto adjustment is bigger with larger correlation between the EUR/USD exchange rate and the DCEPL.

| CDX-IG9 | USD | Quanto Adj by Corr(FX, DCEPL) | |||||

|---|---|---|---|---|---|---|---|

| Att | Det | ETL | 0.0 | 0.2 | 0.4 | 0.6 | 0.8 |

| 0% | 2.4% | 67.23% | 0.00% | 1.26% | 2.39% | 3.85% | 4.81% |

| 2.4% | 6.5% | 23.24% | 0.00% | 0.97% | 1.84% | 3.00% | 3.92% |

| 6.5% | 9.6% | 7.53% | 0.00% | 0.45% | 0.82% | 1.36% | 1.83% |

| 9.6% | 14.8% | 3.18% | 0.00% | 0.29% | 0.48% | 0.81% | 1.04% |

| 14.8% | 30.3% | 0.83% | 0.00% | 0.10% | 0.18% | 0.30% | 0.33% |

| 30.3% | 61.2% | 0.33% | 0.00% | 0.05% | 0.11% | 0.15% | 0.20% |

| 0% | 100% | 3.23% | 0.00% | 0.15% | 0.27% | 0.43% | 0.55% |

5 Conclusion

This DIC-SAMC method proposed in this paper is fully consistent and arbitrage free. It preserves the single name’s identity consistency across all the index and bespoke tranches. All the modelling flaws in the current standard BC-TLP mapping method are addressed in the DIC-SAMC approach. The single name risks from DIC-SAMC are arguably better than those from the BC-TLP because of the absence of arbitrage and the explicit modelling of multiple market factors. The DIC-SAMC method is also computationally efficient, making it a viable alternative to the standard BC-TLP method.

In the DIC-SAMC model setup, we assumed that there is a distinct market factor for each liquid index. This one-to-one mapping between market factors and liquid indices greatly improves the numerical efficiency of the model calibration because each liquid index can be calibrated separately. It is also easier to estimate the correlation between market factors from historical market data because of this one-to-one association. The downside of this choice is that the market factors are not granular enough to capture industry and sector information, it may not be suitable to price bespoke tranches that are concentrated in certain industries or sectors. However, bespoke portfolios are usually well diversified because they are constructed to achieve better ratings. The rating agency’s rating criteria severely penalize non-diversified portfolios, therefore we rarely see any bespoke tranche with very concentrated portfolios in practice.

Interestingly, this study also showed that the current standard method of BC-TLP, despite its many flaws, is actually a reasonable approach to manage bespoke tranches as it produces acceptable prices and risk measures under most practical situations. In the current market environment, the DIC-SAMC method only offers marginal improvements over BC-TLP for the pricing and risk management of ordinary bespoke tranches. Given the wide acceptance and large existing investments in BC-TLP, we don’t foresee market participants to migrate away from the BC-TLP method in the near future. However, the DIC-SAMC method does provide a more consistent view of the prices and risks that can be very useful for risk management and for finding relative value trading opportunities. The DIC-SAMC can also be used when the BC-TLP fails due to its intrinsic limitations. Quanto adjustment for tranches and the pricing effects of lower correlation between market factors are two such examples we discussed in this study.

The DIC-SAMC has less pricing uncertainty when comparing to the very ad hoc BC-TLP. The bespoke tranche pricing uncertainties under DIC-SAMC are mainly from two factors: the first is the correlation between market factors, the second is the factor loadings between bespoke names and index tranches. The meaning and effects of these two factors are very intuitive and they can be easily estimated from historical time series of market observations. The BC-TLP method, on the other hand, has much more uncertainty in pricing because it depends on many ad hoc model parameters and assumptions, such as the interpolation and extrapolation methods on the base correlation curve, the weighting methods across indices etc. The TLP mapping itself is also questionable as alternative mapping methods such as ATM or PM could also be feasible in practice. Most of the parameters and model assumptions in the BC-TLP method do not have intuitive meaning; and their effects on the model price can be quite difficult to understand; and we can’t directly estimate them from historical time series of market observations.

The DIC-SAMC method has the potential to bring much more pricing transparency to bespoke CDO tranches, and hopefully the added pricing transparency will encourage more active trading in the bespoke tranche market.

References

- [1] \harvarditemAmraoui \harvardand Hitier2008hitier Amraoui, S. \harvardand S. Hitier. 2008. “Optimal Stochastic Recovery for Base Correlation.” defaultrisk.com .

- [2] \harvarditemAndersen \harvardand Sidenius2004rfl Andersen, L. \harvardand J. Sidenius. 2004. “Extensions to the Gaussian Copula: Random Recovery and Random Factor Loadings.” Journal of Credit Risk .

- [3] \harvarditem[Andersen, Sidenius \harvardand Basu]Andersen, Sidenius \harvardand Basu2003semianalytical Andersen, L., J. Sidenius \harvardand S. Basu. 2003. “All your hedges in one basket.” Risk .

- [4] \harvarditemBaheti \harvardand Morgan2007bcmap Baheti, P. \harvardand S. Morgan. 2007. “Base Correlation Mapping.” Lehman Brothers: Quantitative Credit Research Quarterly .

- [5] \harvarditem[Epple, Morgan \harvardand Schloegl]Epple, Morgan \harvardand Schloegl2007losslinker Epple, F., S. Morgan \harvardand L. Schloegl. 2007. “Joint Distribution of Portfolio Losses and Exotic Portfolio Products.” International Journal of Theoretical and Applied Finance 10(4).

- [6] \harvarditemHalperin2009halpbspk Halperin, I. 2009. “Implied Multi-factor Model for Bespoke CDO Tranches and Other Portfolio Credit Derivatives.” defaultrisk.com .

- [7] \harvarditemHull \harvardand White2006impliedcopula Hull, J. \harvardand A. White. 2006. “Valuing Credit Derivatives Using an Impplied Copula Approach.” Journal of Derivatives .

- [8] \harvarditemLi2009self Li, Y. 2009. “A Dynamic Correlation Modelling Framework with Consistent Recovery.” defaultrisk.com .

- [9] \harvarditemMorgan \harvardand Mortensen2007bcdelta Morgan, S. \harvardand A. Mortensen. 2007. “CDO Hedging Anomalies in the Base Correlation Approach.” Lehman Brothers: Quantitative Credit Research Quarterly pp. 49–59.

- [10] \harvarditemRosen \harvardand Sanders2009mcbspk Rosen, D. \harvardand D. Sanders. 2009. “Valuing CDOs of Bespoke Portfolios with Implied Multi-factor models.” Journal of Credit Risk .

- [11] \harvarditemSkarke2005skarke Skarke, H. 2005. “Remarks on Pricing Correlation Products.” defaultrisk.com .

- [12] \harvarditem[Tavares et al.]Tavares, Nguyen, Chapovsky \harvardand Vaysburd2004compbasket Tavares, P., T. Nguyen, A. Chapovsky \harvardand I. Vaysburd. 2004. “Composite Basket Model.” defaultrisk.com .

- [13] \harvarditemWillemann \harvardand Leeming2008bardelta Willemann, S. \harvardand M Leeming. 2008. “Are 12-22% Tranches Wide?” Barclays Capital Structured Credit Research Report .

- [14]