Computational LPPL Fit to Financial Bubbles

Abstract

The log-periodic power law (LPPL) is a model of asset prices during endogenous bubbles. If the on-going development of a bubble is suspected, asset prices can be fit numerically to the LPPL law. The best solutions can then indicate whether a bubble is in progress and, if so, the bubble critical time (i.e., when the bubble is expected to burst). Consequently, the LPPL model is useful only if the data can be fit to the model with algorithms that are accurate and computationally efficient.

In this paper, we address primarily the computational efficiency and secondarily the precision of the LPPL non-linear least-square fit. Specifically, we present a parallel Levenberg-Marquardt algorithm (LMA) for LPPL least-square fit that sped up computation of more than a factor of four over a sequential LMA on historical and synthetic price series. Additionally, we isolate a linear sub-structure of the LPPL least-square fit that can be paired with an exact computation of the Jacobian, give new settings for the Levenberg-Marquardt damping factor, and describe a heuristic method to choose initial solutions.

1 Introduction

Financial bubbles and busts have devastating effect on the economy and on markets. However, the existence and characteristics of bubbles are notoriously hard to ascertain if not with hindsight. This paper contributes to the investigation of financial bubbles within the LPPL framework [17], and specifically improves on its computational efficiency.

Financial bubbles are hard to detect. In the words of the former Federal Reserve chairman Alan Greenspan: “We, at the Federal Reserve recognized that, despite our suspicions, it was very difficult to definitively identify a bubble until after the fact, that is, when its bursting confirmed its existence.” [8]. Yet, if a regulatory agency, such as the Fed, were aware of a developing financial bubble, it could take mitigating steps in the areas of monetary policy, unconventional open market operations (e.g., [16]), or supervisory activities (e.g., [3]). Bubble detection is not only critical to the macro-economic decision makers but it is also helpful to the trader. In particular, a trading system may requires detailed knowledge of the time or the level at which the bubble will burst.

Endogenous financial bubbles have been modeled as a log-periodic power law (LPPL) [17]. The LPPL model has two main characteristics:

-

•

Super-exponential growth, leading to a critical time at which the asset price will burst (power law), and

-

•

Oscillations that become progressively faster as the critical time approaches (log-periodicity).

Super-exponential growth is a sign that price growth are unsustainable. The oscillatory behavior indicates an incipient system failure, and is often associated with increasingly more rapid and pronounced swings in investor sentiment. The main issue in LPPL is the fit of the LPPL function to price time series. Indeed, the LPPL model may be correct, but if it cannot be fit satisfactorily to price data, its usefulness is limited. In this paper, we address the computational efficiency and precision of the LPPL least-square fit, and present:

-

•

A parallel algorithm for LPPL least-square fit, with a justification and analysis of the speed-up afforded by parallelism.

-

•

A linear sub-structure of the LPPL least-square fit that can be paired with an exact computation of the LPPL Jacobian.

-

•

En route to the algorithm development, we also give new settings for the Levenberg-Marquardt damping factor and a heuristic method to choose initial solutions.

-

•

An analysis of historical and synthetic price time series in terms of both computational speed and accuracy.

Previous work has paid considerable attention to fitting the LPPL law to historical time series of financial bubbles, and a recent summary reviews the state of the art [10]. Current methods for LPPL bubble detection are currently being tested in an on-line experiment [18]. Previous work mostly focus on the issues of accuracy and of noise. Noise can complicate the estimation of parameters and even make it hard to distinguish between LPPL (bubble) and exponential (non-bubble) growth [7, 6]. However, if noise has a mean-reverting property, then LPPL can be explain many historical bubbles [13]. No previous paper has investigated the issue of computational efficiency and parallel algorithms specifically for LPPL least-squares.

The paper is organized as follows. Section 2 introduces the LPPL model and defines the weighted LPPL least-square problem. Section 3 gives an heuristic method to set multiple initial solutions to the LPPL least-square problem. Section 4 describes a parallel implementation of the Levenberg-Marquardt algorithm and Section 5 gives a method to dynamically set the algorithm’s damping factor. Section 6 describes a method to alternate the solution of the non-linear least-square problem with the solution of a linear sub-system while ensuring the exact computation of the Jacobian. Section 7 describes the evaluation methodology and reports on the evaluation results. Section 8 concludes the paper.

2 Log-Periodic Power Law (LPPL) and Least Squares

The log-periodic power law is a function:

| (1) |

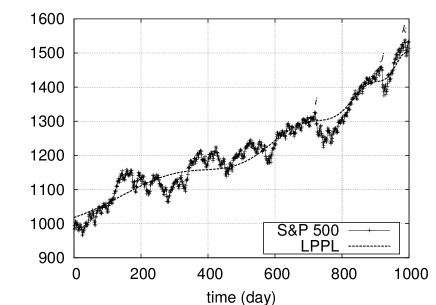

where and . The LPPL function is a model for a time series of prices so that . Figure 1 shows the S&P 500 daily closing prices and an LPPL fit for the four years between July 2003 and June 2007.

If , then LPPL reduces to an exponential fit of the price time series. If , then LPPL grows super-exponentially until the critical time . If , then LPPL exhibits oscillations that become progressively more frequent as approaches the critical time.

Given a time series of prices and weights , the LPPL weighted least-square problem is to find the values of the LPPL parameters () that minimize the weighted sum of squared residuals , where . We will refer to as the error corresponding to the given LPPL parameters, and to as the average error, where is the degrees of freedom of the least-squares problem.

The LPPL weighted least-squares can be solved with various methods, such as the Levenberg-Marquardt algorithm (LMA) [14]. The LMA is an iterative method that maintains a vector of parameters and at each iteration adjusts so as to reduce the error .

Previous work has considered unweighted LPPL least-squares () on sub-intervals [10]. Weighted least-squares generalizes sub-interval fitting since it reduces to sub-interval fitting in the special case

| (2) |

Weighted least-squares make it possible to emphasize recent history over older data. For example, if weights are as in (2) and , then the fit will only depend on the recent interval . As another example, if

| (3) |

the importance of decreases quadratically with its age . The importance of recency can be increased by taking smaller values of . Returning to the case of general weights, recency can be progressively emphasized by decreasing weights more rapidly for progressively older data points.

Recency weighting is relatively less important during the last stages of a bubble. When a bubble is approaching its critical time , recent prices are much larger than older prices. Hence, the residual is much larger for recent data than for older prices, even if the relative error is the same. Thus, the least-square objective is affected more by recent data points than older ones. However, recency weighting is important when the bubble is in its early stages because price values are relatively close to each other.

3 Initial Solutions

Non-linear least-squares is in general a non-convex optimization problem, and a solution algorithm, such as LMA, can reach a local minimum that is not globally optimum. The existence of local minima can be partly obviated by starting LMA from multiple initial solutions. Initial solutions can be selected via Taboo search [10]. Yet, in the presence of a strong LPPL component to price data, initial solutions can also be chosen by inspection of the price series.

In this paper, the initial solutions are determined as follows. First, we find the best fit of prices to an exponential function of the form . The exponential fit is found by linear least-squares, and can be regarded as fitting the LPPL function (1) under the additional constraints that and . The LMA method starts with these exponentially fit parameters and moves on to a general LPPL fit, where the constraints can be violated. However, if the LMA general LPPL fit does not significantly reduce the error, it can be taken as an indication that no LPPL bubble is forming. In other words, the exponential starting point can be interpreted informally as testing for the null hypothesis that prices grow exponentially, i.e., no super-exponential LPPL bubble is developing.

Second, we estimate the initial values of and from price gyrations. We say that two indexes and are consecutive in angle if . The estimation of and relies on the fact that in many cases it is easy to identify visually two indexes that are consecutive in angle. For example, two consecutive peaks of the LPPL function are consecutive in angle (points and in Fig. 1). If two indexes are consecutive in angle, then . Define . Then, and . To estimate , consider three points such that are consecutive in angle and are consecutive in angle. Then, for some integer , and , so that .

An estimate , , and is obtained by selecting three consecutive price peaks (or troughs). It is an open question to automate the selection of , for example, with a visual pattern recognition algorithm. At any rate, each choice of corresponds to a value of , and thus to a different initial solution. The LMA process will be started from multiple initial parameters.

It remains to choose an initial value of . We use the previously chosen initial values of and , and without loss of generality make the assumption that . If , , and are chosen as approximate price peaks, then , and so . Similarly, the LPPL equation (1) can be solved for if , , and are chosen as approximate price troughs, or at any other fixed angle.

Example.

In the 2003-2007 S&P 500 bubble up to 6/30/2007 (Fig. 1), three consecutive peaks are (5/5/2006), (2/20/2007), and (6/4/2007). Hence, , , , and . The initial linear least-squares fit to an exponential function leads to and , with an error of . The initial point is subsequently fit to LPPL, and the final value of the parameters is (11/16/2007), , with an error of . The final parameter values and the substantial error reduction denote that a bubble was likely in progress. The actual S&P 500 peak was on 10/9/2007.

4 Parallel Least-Squares

Modern computer systems provide significant parallelization capabilities: most CPUs have multiple cores, multiple CPUs and co-processors are placed on the same motherboard, general-purpose GPUs execute streams of independent operations on multiple data, and cloud computing makes it possible to gain inexpensive access to a vast number of computational resources. Furthermore, the amount of parallelism is expected to increase in the next few years as current trends solidify: more cores will be placed on a single CPU, and cloud computing will gradually become commonplace. Several programming interfaces (e.g., OpenMP [1]) make it easy to develop parallel programs, especially if the computation involves primarily iterations of independent statements. Previous work describes a general-purpose parallel LMA implementation based on three techniques: solving multiple problems in parallel, parallelizing the computation of the Jacobian, and probing multiple values of the damping factor in parallel [5]. Parallelism offers an opportunity to implement faster LMA especially tailored to the LPPL least-squares.

Parallelism can be exploited at various levels of granularity. At the coarsest level, multiple securities can be analyzed in parallel. Moreover, each security can be analyzed from multiple initial solutions and for different weight functions. Since different securities, initial solutions, and weights lead to independent LMA executions, the analysis can be conducted in parallel. Widespread LMA tools, such as levmar [14], are thread-unsafe, and a single process cannot accommodate concurrent LMA invocations. Hence, multiple securities, weights, and starting points are analyzed by independent processes.

At the other extreme, fine-grained parallelism can be used to speed-up the computation of the LPPL function (1) and associated quantities. Each LMA iteration requires the computation of and of its Jacobian at the current solution . In general, the Jacobian can be computed either analytically or through approximation methods, such as finite differences. Since has a relatively simple closed expression, we compute the LPPL Jacobian analytically. In practice, each step requires the computation of at points and the evaluation of 7 partial derivatives at the same points. The computation at is independent of the computation at , and so its parallelization is a perfect match for the OpenMP “parallel for” construct. The computation of and can be parallelized even if the LMA solver is not thread-safe because it is invoked from within the solver. In this case, the program is sequential except at the very bottom of the invocation tree, where and are calculated by multiple threads.

| Time percentage | Function Name |

|---|---|

| 19.0321 | cos |

| 17.3662 | __ieee754_log |

| 16.1608 | __ieee754_pow |

| 10.7317 | lppl_vector.omp_fn.2 |

| 10.4502 | __exp1 |

| 2.5473 | pow |

| 1.2532 | isnan |

| 1.0655 | log |

| 1.0591 | finite |

| 0.6072 | __mul |

| 0.4087 | dlevmar_L2nrmxmy |

| 0.3768 | /usr/lib64/libblas.so.3.0.3 |

| 0.3049 | levmar_weight |

| 0.2072 | sin |

| 0.1884 | csloww1 |

| 0.1285 | _int_malloc |

The computation of and accounts for most of the program execution time. Table 1 shows a breakdown of the running time: the largest contribution comes from numerical functions (such as raising to power, cosine, logarithm) that appear solely in the evaluation of the LPPL function and of its Jacobian. In summary, the parallelization of and is not only relatively easy, but it is also likely to lead to a large performance improvement. On the other hand, it is not clear a priori that multiple threads speed execution up since the running time depends also on the work overhead needed to manage a thread pool.

The parallel computation of the LPPL function and of its Jacobian requires a parameter that sets the number of concurrent execution threads. The thread pool size depends on the number of cores available to the process. Consequently, the available core count depends not only on the underlying computational resources, but also on the number of securities, starting points, and weight functions that are simultaneously running.

5 Damping Term

The LMA algorithm maintains a damping term , which represents the contribution of the steepest descend method to the next iteration. If is large, then LMA is approximately steepest descent, and if , then LMA reduces to a linear least-square applied to the linearization of the fit function around the current solution. The LMA algorithm dynamically adjusts the value of , it always keeps , and it can increment or decrement at any iteration by multiplying its current value by certain carefully selected factors. The LMA algorithm can terminate with fit parameters because of certain circumstances (e.g., singular matrices) in which the algorithm should be restarted from the current solution with a larger value of . Furthermore, it is possible that the algorithm reaches because of underflow, making it impossible to subsequently increase by multiplying it by any factor. If LMA terminates with or in the other cases that require restarting from a larger value of , then we double the value of a parameter and restart LMA with the initial value of set to . The parameter is also subject to a global upper bound beyond which it cannot be further increased.

6 Linear Sub-System

If , , , are constrained to fixed values, then the least-square problem on , , and is linear. Linear least-squares are typically fast since they require only the computation of one exact Jacobian and the solution of a system of linear equations. However, computation speed must be weighed against solution error. In general, constraining parameters will lead to a solution with a larger error than the unconstrained global optimum. However, the LMA algorithm can fall into a local minimum, and the relation between its final parameters and the linear least-square is not always clear. In particular, when the non-linear LMA terminates at a solution , if the non-linear parameters , , , are fixed at the value, the linear least-square on , , and often leads to a solution that improves on , i.e., its error is smaller. Furthermore, if the non-linear LMA is restarted from , the LMA may be able to further improve on , whereas LMA had not been able to make progress from . In some sense, the linearized system can be viewed as a computationally efficient way to extricate LMA from a local minimum. Alternatively, previous work derived analytical expressions for as a function of the other parameters by expanding the linear least-squares optimality conditions. These expressions for are then substituted in the non-linear least-square problem [10]. Direct substitution reduces the number of parameters in the fit, but it complicates the LPPL expression and especially the analytical calculation of the Jacobian matrix.

To interleave LMA with linear least-squares, we run LMA until either it terminates or it has reached the th iteration, and then solve the linear least-square assuming that , , , are fixed. If the linear least-square improves the error, it is taken as the starting point for another round of the LMA algorithm. The process terminates when the linear least-square fails to improve the current solution and the damping factor cannot be further increased.

The parameter is a bound on the number of LMA iterations and can be supplied by the user. We have also implemented an adaptive method to choose depending on the relative gains made by the linear and the non-linear algorithm. The adaptive method changes the value of depending on which least-square algorithm reduces the error the most during a unit of computation time. In other words, the adaptive method will run LMA longer if LMA reduces the error more than linear least-squares during a unit of computation time, and will run the linear least-square more often if conversely the linear least-square reduces the error more than LMA during a unit of computation time. The method collects the error reduction and the running time of each invocation of both linear least-squares and LMA. In the case of linear least-squares, we estimate the error reduction per unit of time by simply dividing the measured error reduction by the execution time. The LMA unit error reduction is more complicated to estimate because LMA executes various initializations regardless of how many iterations the algorithm executes. The LMA run time is modeled as , where is the time needed to execute the initialization, is the number of iterations, and is the time needed for each iteration. The values of and are adaptively estimated by keeping track of the execution time during the last two invocation of LMA with different values of . We then compute an estimate of the error reduction that would occur if the LMA computation took one more unit of time.

Given the linear and non-linear estimates of error reduction per unit of time, we compare them to choose whether to increase or decrease . The adaptive mechanism proceeds in two phases: a start-up phase and a regime phase. The start-up phase aims at finding quickly an approximate value for the best value of , whereas the regime phase aims toward a more precise value of . The start-up begins with a small user-supplied value of , and doubles it until the marginal unit LMA error improvement is smaller than the unit error improvement of the linear least-squares. The regime phase increases or decreases by one depending on which algorithm leads to the largest unit error reduction.

7 Evaluation

7.1 Methodology

The LPPL least-square fit can be carried out under two main goals: prediction of a bubble prior to its critical time (), or fit of asset prices to LPPL after the fact to verify whether LPPL models the evolution of prices (). The focus of this paper is on prediction ().

The evaluation uses real and synthetic data sets. Real data sets are daily closing values of major securities and stock indexes described in Table 2.

| Series | Period | Data Points |

|---|---|---|

| Dow Jones | June 1921-July 1929 | 2440 |

| S&P 500 | July 1985–July 1987 | 527 |

| S&P 500 | July 2003–June 2007 | 1000 |

| GLD | March 2009–October 2009 | 171 |

Synthetic data sets are generated by adding noise to LPPL price values: , where is the value of a Brownian motion process at time and is a scaling factor [12, 11]. Geometric Brownian motion is commonly used to model price dynamics in an efficient market (e.g., [2]), where is called implied volatility. Thus, synthetic data can be regarded the combination of a super-exponential bubble with an efficient market. Recent work proposes a more sophisticated model based on LPPL plus both Brownian motion and an Ornstein-Uhlbeck process [13]. However, Brownian motion is the most difficult noise component for the LPPL least-square fit [13, 7, 6]. Synthetic data were generated with the parameters shown in table 3.

| Base | Oscillatory | Exponential | |

| 5 | 5 | 5 | |

| 0.02 | 0.02 | 0.005 | |

| 1100 | 1100 | 1100 | |

| .68 | .68 | 1 | |

| .05 | 0.2 | 0 | |

| 9 | 9 | 1 | |

| 0 | 0 | 0 | |

| 1000 | 1000 | 1000 | |

| 0.005 | 0.02 | 0.05 |

Base and oscillatory traces capture a LPPL processes, and exponential traces capture non-LPPL processes. The base case contains a log-periodic term () that is relatively small so that the LPPL function is always increasing over time. The oscillatory model assumes a larger value of that magnifies the log-periodic oscillations. For each stochastic model (base, oscillatory, exponential), five random traces were generated.

7.2 Parallelism

Each least-square LPPL fit was run on an 8-core machine as a process with 8 threads of control. The machine was otherwise unloaded (except for various unavoidable and lightweight system processes), and the LPPL fit achieved close to 100% CPU utilization. The parallel least-square typically took less than 1/4 of the time of the sequential implementation, i.e., we observe a speed up of a factor of four or more. Since the parallel least-square has 8-fold parallelism, the amount of work increased significantly. In particular, more than 1/3 of the running time is taken by OpenMP management (Table 4).

| Time percentage | Function Name |

|---|---|

| 36.1513 | /usr/lib64/libgomp.so.1.0.0 |

| 12.3288 | __ieee754_pow |

| 11.6925 | __ieee754_log |

| 11.3157 | cos |

| 8.4633 | lppl_vector.omp_fn.2 |

| 6.9043 | __exp1 |

| 2.9887 | pow |

| 2.5607 | isnan |

| 1.5655 | log |

| 1.1870 | /no-vmlinux |

| 0.8585 | dlevmar_L2nrmxmy |

| 0.6399 | /usr/bin/oprofiled |

| 0.4110 | /usr/lib64/libblas.so.3.0.3 |

| 0.3673 | levmar_weight |

| 0.3386 | __mul |

| 0.3371 | finite |

| 0.2273 | jac_lppl_vector.omp_fn.1 |

| 0.2170 | sin |

Discussion.

The optimal degree of parallelism depends on the number of jobs and on the number of available cores. For example, while a single job was than 4 times faster on 8 cores, eight distinct jobs complete sooner if each is sequential.

The workload is dominated by the independent execution of the same set of instructions on multiple data. Therefore, it is likely that the computation would benefit from SIMD (single-instruction multiple data) and related hardware architecture, such as GPGPU (General-Purpose computation on Graphics Processing Units) [15]. By contrast, general multi-core architectures, such as the one used in this paper, are easier to program but may have lower performance than specialized SIMD. This paper leaves it as an open problem to implement the LPPL least-square on GPGPU.

Another disadvantage of general multi-core architecture is that the parallelizable data set (the stream) is relatively small. In practice, a price time series has few thousands points at most, and corresponds to a full stream. As a result, the overhead of managing multiple threads over a multi-core architecture is a substantial fraction of the execution time. On the flip side, the algorithm is scalable with the number of data points, so the thread management overhead becomes smaller if more data is available.

7.3 LPPL Least-Square Fit

Historical Time Series.

Table 5 gives the error reduction of the best least-square LPPL fit, and the predicted and actual critical time in the minimum residual error fit. As an example, Figure 1 gives the best fit of the S&P 500 (2007) prices. The substantial error reduction and the final parameter values are strong evidence that an endogenous LPPL bubble was in progress. However, the best fit predicts a critical time that deviates, in some cases significantly, from the actual bubble burst. Critical time overestimation was robust to several choices of a quadratic weight function (3).

| Average Error | |||||||

|---|---|---|---|---|---|---|---|

| Series | Exponential fit | LPPL fit | Fit | Actual | |||

| Dow Jones 1929 | 2784 | 2467 | 0.372 | 0.0414 | 12.23 | ||

| S&P 500 1987 | 658 | 573 | 0.417 | 0.0705 | 9.89 | ||

| S&P 500 2007 | 1105 | 1071 | 0.518 | 0.0438 | 9.87 | ||

| GLD 2009 | 211 | 195 | 18.40 | ||||

The best LPPL solutions were characterized by a strong local correlation between some of the variables. In particular, in the neighborhood of the optimum, had absolute correlation higher than with both and . In other words, even if had been fixed to a value slightly different from the optimum (e.g., [4]), the LPPL fit would still be able to make progress by tweaking the values of and .

Synthetic Time Series.

On the base synthetic traces (Table 3), the best fit almost always predicts larger values of the critical time than in the underlying process. The overestimation was 63 trading periods on average and ranged between -5 and +166 trading periods. On the oscillatory traces, the best fit almost always predicts smaller values of the critical time than in the underlying process. The underestimation was 19 trading periods on average and ranged between -42 and +67 trading periods. We conjecture that in the presence of additive noise such as Brownian motion the best least-square fit tends to overestimate if oscillations are muted ( small) and to underestimate it if oscillations are larger ( large). The hypothesis matches the best fit behavior on the historical price series (Table 5), where is small and comparable to that of the base synthetic trace, oscillations are muted (for example, see Figure 1), and estimated critical times always exceeded actual critical times.

On the exponential synthetic traces, the fit found either , which denotes a nearly exponential fit, or , in which case the log-periodic oscillations were so small that the LPPL fit did not significantly differ from a super-exponential function. Parameter values denote poor statistical significance for the LPPL fit [9].

Discussion.

The least-square LPPL algorithm distinguished clearly between LPPL and non-LPPL growth. In particular, it was sufficient to check for and small (say, ). The implication is that it is possible for, say, a regulatory agency, to distinguish between endogenous bubbles and ordinary exponential growth. However, the estimated parameters differed from their true value, and in particular the critical time is underestimated in the presence of Brownian noise and if the underlying LPPL function lacks strong oscillations. As a consequence, the best LPPL fit was not a workable indicator for technical analysis.

8 Conclusion

In this paper, we have presented methods for the solution of the LPPL weighted least-square fit via the Levenberg-Marquardt algorithm. The method heavily relies on parallelism to cut down on the critical computation path, namely the evaluation of the LPPL function and of its Jacobian. We have described cases that are based on historical price series and where the method cuts the solution time by a factor of four or more. We have also presented a method to dovetail the non-linear LPPL least-square with the solution of the linear LPPL sub-component while preserving the exact computation of the Jacobian. En route, we have described methods for selecting initial solutions to the LPPL fit and a method for setting the LMA damping factor.

The paper leaves a number of open problems. On the computational side, the running time is dominated by the stream computation of the LPPL function and of its Jacobian. When this computation is parallelized on a general-purpose multi-core process, the thread management overhead approached 40% of the process work. Thus, much promise is held by alternative architectures, such as SIMD or GPGPU. On the economics side, the method is a tool for further research on LPPL, and especially for deriving precise fits of LPPL to noisy price data.

References

- [1] OpenMP. http://openmp.org/wp/.

- [2] Fischer Black and Myron Scholes. The pricing of options and corporate liabilities. The Journal of Political Economy, 81(3):637–654, 1973.

- [3] Oliver Blanchard, Giovanni Dell’Ariccia, and Paolo Mauro. Rethinking macroeconomic policy. Technical Report SPN/10/03, International Monetary Fund, 2010.

- [4] David S. Bree and Nathan Lael Joseph. Fitting the Log Periodic Power Law to financial crashes: a critical analysis. Technical Report 1002.1010, arXiv, 2010.

- [5] Jun Cao, Krista A. Novstrup, Ayush Goyal, Samuel P. Midkiff, and James M. Caruthers. A parallel Levenberg-Marquardt algorithm. In ICS’09, pages 450–459, June 2009.

- [6] G. Chang and J. Feigenbaum. A Bayesian analysis of log-periodic precursors to financial crashes. Quantitative Finance, 6(1):15–36, 2006.

- [7] J. A. Feigenbaum. A statistical analysis of log-periodic precursors to financial crashes. Quantitative Finance, 1:346–360, 2001.

- [8] A. Greenspan. Economic volatility. In Jackson Hole, August 2002.

- [9] Y. Huang, A. Johansen, M.W. Lee, H. Saleur, and D. Sornette. Artifactual log-periodicity in finite size data—relevance for earthquake aftershocks. Journal of Geophysical Research, 105(B11):25451–25471, 2000.

- [10] Zhi-Qiang Jiang, Wei-Xing Zhou, Didier Sornette, Ryan Woodard, Ken Bastiaensen, and Peter Cauwels. Bubble diagnosis and prediction of the 2005-2007 and 2008-2009 Chinese stock market bubbles. Economic Behavior and Organization, 74:149–162, 2010.

- [11] A. Johansen, O. Ledoit, and D. Sornette. Crashes as critical points. International Journal of Theoretical and Applied Finance, 3:219–255, 2000.

- [12] A. Johansen, D. Sornette, and O. Ledoit. Predicting financial crashes using discrete scale invariance. Journal of Risk, 1:5–32, 1999.

- [13] L. Lin, R. R. E, and D. Sornette. A Consistent Model of ‘Explosive’ Financial Bubbles With Mean-Reversing Residuals. ArXiv e-prints, May 2009.

- [14] Manolis Lourakis. levmar: Levenberg-Marquardt nonlinear least squares algorithms in C/C++. http://www.ics.forth.gr/~lourakis/levmar/.

- [15] David Luebke, Mark Harris, Naga Govindaraju, Aaron Lefohn, Mike Houston, John Owens, Mark Segal, Matthew Papakipos, and Ian Buck. GPGPU: general-purpose computation on graphics hardware. In SC ’06: Proceedings of the 2006 ACM/IEEE conference on Supercomputing, page 208, New York, NY, USA, 2006. ACM.

- [16] Ricardo Reis. An interpretation of the unconventional U.S. monetary-policy response to the 2007-09 crisis. In Brookings Papers on Economic Activity, September 2009.

- [17] D. Sornette. Critical phenomena in natural sciences: chaos, fractals, selforganization, and disorder: concepts and tools. Springer, 2004.

- [18] Didier Sornette, Ryan Woodard, Maxim Fedorovsky, Stefan Reimann, Hilary Woodard, and Wei-Xing Zhou. The financial bubble experiment: advanced diagnostics and forecasts of bubble terminations, 2009.