Consider a linear regression model with

regression parameter and independent normal

errors.

Suppose the parameter of interest is , where is specified.

Define the -dimensional parameter vector , where

and are specified.

Suppose that we carry out a preliminary F test of

the null hypothesis against the alternative hypothesis .

It is common statistical practice to then construct

a confidence interval for with

nominal coverage , using the same data,

based on the assumption that the selected model had been given to us a priori

(as the true model).

We call this the naive confidence interval for . This assumption is false and

it may lead to this confidence interval having

minimum coverage probability far

below , making it completely inadequate. Our aim is to compute this minimum

coverage probability.

It is straightforward to find

an expression for the coverage probability of this confidence interval

that is a multiple integral of dimension .

However, we derive a new elegant and computationally-convenient formula for this coverage probability.

For this formula is a sum of a

triple and a double integral and for all this formula is a sum of a quadruple and a double integral.

This makes it easy to compute the minimum coverage probability of the naive confidence interval,

irrespective of how large is.

A very important practical application of this formula is to the analysis of covariance.

In this context, can be defined so that

expresses the hypothesis of “parallelism”.

Applied statisticians commonly recommend carrying out

a preliminary F test of this hypothesis.

We illustrate the application of our formula with a real-life

analysis of covariance data set and a preliminary F test for “parallelism”.

We show that the naive 0.95 confidence interval has minimum coverage probability 0.0846,

showing that it is completely inadequate.

Keywords: analysis of covariance, naive confidence interval, preliminary F test, test for parallelism.

1. Introduction

Consider the linear regression model

,

where is a random -vector of responses, is a known matrix with linearly

independent columns, is an unknown parameter -vector and

where is an unknown positive parameter.

Suppose that the parameter of interest is where is a given

-vector (). We seek a confidence interval for .

Let the -dimensional parameter vector be defined to be where is a specified matrix ()

with linearly independent columns and is a specified -vector.

Suppose that does not belong to the linear subspace spanned by the columns

of .

Also suppose that we carry out a preliminary F test of

the null hypothesis against the alternative hypothesis .

It is then common statistical practice to construct a confidence interval for with

nominal coverage , using the same data, based on the assumption

that the selected model had been given to us a priori (as the true model).

We call this the naive confidence interval for .

In Section 2, we provide a convenient description of this confidence interval.

This assumption is false and it can lead to the naive confidence interval

having minimum coverage probability far below , making it completely inadequate.

Our aim is to compute this minimum

coverage probability.

For , the preliminary F test is equivalent to a t test. The case of a single preliminary t test

has been dealt with by Kabaila and Giri (2009, Theorem 3). So, in the present paper,

we restrict attention to the case that .

Straightforward application of the methodology of Farchione (PhD thesis,

2009, Section 5.7) leads to

an expression for the coverage probability of the naive confidence interval, for a

given value of an -dimensional parameter vector, that is a multiple integral of dimension .

Finding the minimum coverage probability using this formula becomes increasingly cumbersome

as increases due to both the need to (a) evaluate multiple integrals of dimension and

(b) the need to search for the minimum over a space of dimension .

In Section 3, by a careful consideration of the geometry of the

situation, we derive a new elegant and computationally-convenient formula for the coverage probability

of this confidence interval for given parameter values.

For this formula is a sum of a

triple and a double integral and for all this formula is a sum of a quadruple and a double integral.

This formula also shows that the coverage probability is a function of a two-dimensional parameter

vector, irrespective of how large is. This makes it easy to compute the minimum coverage probability of the naive confidence interval,

irrespective of how large is. Another important aspect of this formula is that it

can be used to delineate general categories of , and for which the naive confidence interval

has poor coverage properties.

A very important practical application of this formula is to the analysis of covariance.

In this context, can be defined so that

expresses the null hypothesis of “parallelism”.

In the applied statistics literature on the analysis of covariance it is commonly recommended

that a preliminary F test of the null hypothesis of “parallelism” be carried out.

See, for example, Kuehl (2000, p.563), Milliken and Johnson (2002, pp. 14 – 17) and

Freund et al (2006, pp. 363 – 368).

For an analysis of covariance, we can choose so that the parameter

is the difference in expected responses for two specified treatments, for the same specified values of the covariates.

In Section 4, we illustrate the application of the results of the paper with a real-life

analysis of covariance data set and a preliminary F test for “parallelism”.

We define

to be

,

evaluated at the same specified value of the covariate.

We show that

the naive 0.95 confidence interval for has minimum coverage probability 0.0846,

for this specified value of the covariate. This shows that this

confidence interval is completely inadequate, for this specified value of the covariate.

2. Description of the naive confidence interval

In this section we provide a convenient description of the naive confidence

interval constructed after

the preliminary F test.

Let denote the least squares estimator of .

Define . Let .

Define .

Also, define and .

We suppose that the columns of the matrix are linearly independent.

We also suppose that does not belong to the linear subspace spanned by the

columns of .

Now define the matrix

Note that , and .

Define to be the value of minimizing subject to the restriction that

. As is well known (see e.g. Graybill, 1976, p.222)

The standard test statistic for testing against is

This test statistic has an distribution under .

Suppose that we reject when and accept otherwise, where

is a specified positive number.

Define .

Also define the quantile by the requirement that

for .

The naive confidence interval for is obtained as follows.

Suppose that . The confidence interval is constructed on the assumption that

is not necessarily true. In this case, the naive confidence interval

is the usual confidence interval for based on fitting the full model,

Now suppose that . The confidence interval is constructed on the assumption that

. If then and

Var.

Note that and are independent random variables.

We use the notation for the interval ().

In this case, the naive confidence interval for is

(1)

3. The coverage probability of the naive confidence interval

Define and

.

Let denote the probability density function of .

Define .

Thus

Since Var,

.

The assumption that the vector does not belong to the linear subspace spanned by the columns

of implies that . So, we may assume that .

Now define

where , and

Define to be the probability density function of when .

Let denote the beta function.

Define the probability density function to be

For , define the probability density function to be

Let .

Define to be the probability density function of a noncentral chi squared distribution

with degrees of freedom and noncentrality parameter .

Also define

Define the unit vector . When , define and then

. Also define when . Now, when , define

The following is the main result of the paper.

Theorem 1.

The coverage probability of the naive confidence interval for is

. A computationally-convenient

expression for the second term in this sum is

(2)

and computationally-convenient expressions for

are as follows.

Let . For ,

(3)

For and ,

is equal to

(4)

For , and ,

For and ,

Note that for given (which is determined by , and ) and , , and ,

the coverage probability of the naive confidence interval is a function of

.

The proof of this theorem is presented in Appendix A.

The formulas given in Theorem 1 have three attractive features. The first of these is that, irrespective of

how large is, these formulas involve, at most, a 4-dimensional integral.

The second of these features is that

the numerical evaluation of these integrals, reviewed in Appendix B, is very straightforward.

Thirdly, for given , , , and , the coverage probability of the naive confidence

interval

is a function of the two-dimensional parameter vector . These features make

it is easy to compute the minimum coverage probability of the naive confidence interval for

given , , , and .

Finally, Theorem 1 has the following corollary

Corollary 1.

For given , , and ,

the infimum over of the coverage probability of the naive confidence interval

for is a function of .

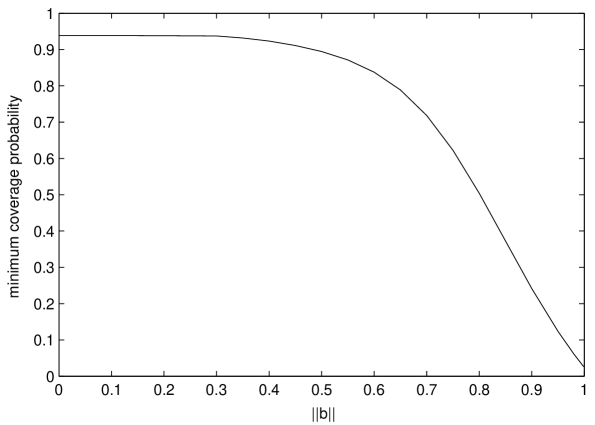

For the numerical example described in the next section, , ,

(corresponding to a 0.05 level of significance of the preliminary F test)

and .

For these values of , and , the minimum coverage

probability of the naive 0.95 confidence interval, as a function of

, is as shown in Figure 1. All of the computations presented in the present

paper were performed with programs written in MATLAB, using the optimization and

statistics toolboxes. We note the decrease in the minimum coverage probability

of this naive confidence interval with increasing .

We can use Corollary 1 to delineate

general categories of , and (via their relationship to )

for which this naive 0.95 confidence interval

has poor coverage properties. Specifically, this naive confidence interval

will have poor coverage properties for those values of , and

such that

is greater than 0.7, say.

Figure 1: Plot of the minimum coverage

probability of the naive 0.95 confidence interval, as a function of

, for , ,

and .

4. Application to a real-life data set

In this section we consider the real-life analysis of covariance

data set due to Chin et al (1994)

and analysed by Yandell (1997, Chapter 17), who makes this data available at the

website http://www.stat.wisc.edu/yandell/pda/. This data is listed in the

Table 1. It consists of the observed response (weight gain) for a given

treatment and value of the covariate (feed intake). There are 4 possible treatments,

numbered 1 to 4.

treatment

weight gain

feed intake

1

1416.1

2451.75

1

1447.0

2546.00

1

1509.6

2657.00

2

1497.8

2452.10

2

1469.9

2404.90

2

1469.4

2479.90

3

1510.1

2788.70

3

1423.0

2655.50

3

1295.9

2366.40

4

1354.8

2578.80

4

1326.8

2384.40

4

1335.1

2477.50

Table 1: The observed response (weight gain) for a given

treatment and value of the covariate (feed intake).

Source: http://www.stat.wisc.edu/yandell/pda/.

We use the following linear regression model for this data:

where is the response of the th experimental unit ()

that is receiving the th treatment (), when the covariate takes the

value . The are independent and identically

distributed and is an unknown positive parameter.

The and () are unknown

parameters. Also,

denotes the mean of the ().

We express this model in the form

, where

and is the obvious matrix.

As considered by Yandell (1997, p.271), we carry out a preliminary test of the null hypothesis

against the alternative

hypothesis that the are not all the same, using an F test. Suppose that we use

a 0.05 level of significance for this preliminary test. We express as

and as , where

and

Define the parameter of interest as follows. Let and denote

the responses of two experimental units, receiving treatments 1 and 2 respectively, for

the same value of the covariate. In other words,

where and are independent and identically

distributed random variables. Let

.

Thus, where

.

We suppose that , which is the maximum value of

for the data.

For this situation, and so the minimum coverage

probability of the naive 0.95 confidence interval is 0.0846.

This shows that this confidence interval is completely inadequate,

in this situation.

5. Discussion

The poor coverage properties of naive confidence intervals found in this paper

are presaged by the poor coverage properties of naive confidence intervals

found in the context of a preliminary best subset variable selection by minimizing an

AIC-type criterion, see e.g. Kabaila (2005), Kabaila & Leeb (2006) and Kabaila & Giri

(2009). Apart from the form of preliminary model selection used, minimum AIC versus an F test,

these papers differ from the present paper in that the present paper provides a method

for computing the minimum coverage probability, whereas Kabaila (2005), Kabaila & Leeb (2006) and Kabaila & Giri

(2009) provide only upper bounds on the minimum coverage probability of the naive

confidence interval.

Appendix A: Proof of Theorem 1

In this appendix, we prove Theorem 1.

Define and .

Let denote the probability density function of .

Note that

(5)

where denotes the identity matrix. Thus the distribution of , conditional

on , is . Note that and are

independent random vectors.

We use the notation

where is an arbitrary statement. This is similar to the Iverson bracket notation

(Knuth, 1992).

By the law of total probability, the coverage probability of the naive confidence interval is

We divide the remainder of the proof into 2 parts.

Part 1: expression for

Suppose that . We prove the validity of the expressions

(3) and (4) for .

The proofs of the validity of the other expressions for

(given in Theorem 1) are similar and are omitted, for the sake of brevity.

Now

and .

Thus

(6)

Note that

Thus

(7)

We now find a simple formula for this expected value.

Since , where is a nonnegative random variable and is a random

-vector with the following distributions. The random vectors and are independent, with

and is distributed uniformly on the surface of the unit sphere

in . Thus , where .

Also, , where .

Hence

Note that , and are independent random vectors.

Define the random vector

to be such that , , and are independent and and have the probability density functions

and respectively, defined in Section 3.

Define the unit -vectors and as follows.

The vector has 1 as its first component and zeros for the remaining components.

The vector has first component , second component

and zeros for the remaining components.

Because is distributed uniformly on the surface of the unit sphere

in , has the same distribution as .

It follows from Fang and Wang (1994, p.49, pp.306–306 and p.308) that has the same distribution as

(a) for , (b)

for and

for .

Thus, has the same distribution as

for ,

for and

for .

Thus is

for and

(8)

for .

This leads to the expressions (3) and (4)

for given in the theorem.

Part 2: expression for

The derivation of the expression for

is based on (S0.Ex6) and the fact that , and

are independent random vectors. Define

and note that has a noncentral chi squared distribution with degrees of freedom and

noncentrality parameter . Note that

where , and are independent random variables and . Also

Thus

by a method similar to that used in Part 1.

Appendix B: Numerical evaluation of the integrals in

Theorem 1

We evaluate the integrals

(2) and (3)

in the statement of Theorem 1 as follows.

We approximate (2) by

(9)

for an appropriately chosen value of .

We bound the error of this approximation as follows.

Since is a probability,

We choose sufficiently large that the right hand side is less than, say, .

To evaluate (9), we transform the region of integration to a rectangle as follows.

Change the variable of integration in (9) to ,

so that (9) is equal to

The integrand is a smooth function of

and so this double integral is easily evaluated by numerical integration.

for an appropriately chosen value of .

We bound the error of this approximation as follows.

Since is a probability,

We choose sufficiently large that the right hand side is less than, say, .

To evaluate (10), we transform the region of integration to a rectangle as follows.

Change the variable of integration in (10) to ,

so that (10) is equal to

The integrand is a smooth function of

and so this triple integral is easily evaluated by numerical integration.

The evaluation of the other integrals in the statement of Theorem 1 is similar to the evaluation

of the integrals (2) and (3).

The evaluation of (4) using MATLAB requires special

comment. In MATLAB, the highest dimensional integral that one can evaluate using a built-in MATLAB

function is a triple integral. We evaluate the quadruple integral (4) using MATLAB

as follows. As before, let . Define

The integrand on the right-hand-side is a very smooth function of . We evaluate ,

to a good approximation, using a compound Simpson’s rule with a specified number of subdivisions

of the interval . The quadruple integral (4) is approximated by

which is evaluated using the MATLAB built-in function triplequad.

References

Chin, S.F., Storkson, J.M., Albright, K.J., Cook, M.E. & Pariza, M.W.: Conjugate linoleic

acid is a growth factor for rats as shown by enhanced weight gain and improved feed efficiency.

Journal of Nutrition 124, 2344 – 2349 (1994)

Fang, K.-T. & Wang, Y.: Number-theoretic Methods in Statistics.

Chapman & Hall, London (1994)

Farchione, D.: Interval estimators that utilize uncertain prior information. Unpublished Ph.D. thesis,

Department of Mathematics and Statistics, La Trobe University (2009)

Freund, R.J., Wilson, W.J. & Sa, P.: Regression Analysis: Statistical Modeling

of a Response Variable, 2nd ed.. Elsevier, Academic Press, Burlington, Mass. (2006)

Graybill, F.A.: Theory and Application of the Linear Model. Duxbury, Pacific Grove, CA (1976)

Kabaila, P.: On the coverage probability of confidence intervals

in regression after variable selection. Australian & New Zealand Journal of Statistics

47, 549–562 (2005).

Kabaila, P., Leeb, H.: On the large-sample minimal coverage

probability of confidence intervals after

model selection. Journal of the American Statistical Association 101, 619–629 (2006)

Kabaila, P., Giri, K.: Upper bounds on the minimum coverage probability of confidence

intervals in regression after model selection. Australian & New Zealand Journal of Statistics

51, 271 – 288 (2009)

Knuth, D.E.: Two notes on notation. American Mathematical Monthly 99, 403–422 (1992)

Kuehl, R.O.: Design of Experiments: Statistical Principles of Research Design and Analysis,

2nd ed.. Brooks/Cole,Pacific Grove, CA (2002)

Milliken, G.A., Johnson, D.E.: Analysis of Messy Data, Volume III: Analysis of

Covariance. Chapman & Hall/CRC, Boca Raton, Fl. (2002)

Yandell, B.S.: Practical Data Analysis for Designed Experiments.

Chapman & Hall, London, New York (1997).