Micro-Macro Relation of Production

– The Double Scaling Law for Statistical Physics of Economy –

Abstract

We show that an economic system populated by multiple agents generates an equilibrium distribution in the form of multiple scaling laws of conditional PDFs, which are sufficient for characterizing the probability distribution. The existence of the double scaling law is demonstrated empirically for the sales and the labor of one million Japanese firms. Theoretical study of the scaling laws suggests lognormal joint distributions of sales and labor and a scaling law for labor productivity, both of which are confirmed empirically. This framework offers characterization of the equilibrium distribution with a small number of scaling indices, which determine macroscopic quantities, thus setting the stage for an equivalence with statistical physics, bridging micro- and macro-economics.

pacs:

02.50.-r, 05.70.-a, 89.65.-s, 89.75.DaEconomics is in crisis. Although there exists a mainstream approach kydland1982time ; gali2008monetary , its internal coherence and ability in explaining empirical evidences are increasingly questioned. The causes of the present state of affairs go back to the mid of the XVIII century, when new figures of social scientist (economists) borrowed the method (mathematics) of the most successful hard science (physics) allowing for the mutation of political economy into economics. It was, and still is, the Newtonian mechanical physics of the XVII century, which rule economics.

From then on, economics lived its own evolution based on the classical physics assumptions (reductionism, determinism and mechanicism). Quite remarkably, Keynes adopted the approach of statistical physics, which deeply affected physical science at the turn of the XIX century by emphasizing the difference between micro and macro, around the mid 1930s keynes1936general . However, after decades of extraordinary success it was rejected by the neoclassical school around the mid 1970s, which framed the discipline into the old approach and ignored, by definition, any interdependence among economic agents (firms, banks, households) and difference between microscopic individual behavior and macroscopic aggregate behavior.

The ideas of natural laws and equilibrium were transplanted into economics sic et simpliciter. As a consequence of the adoption of the classical mechanics paradigm, behavior of macro-economic systems are treated as a scaled-up version of one individual agent, who is called Representative Agent (RA), and complexity that emerges from aggregation was lost. Any learned physicist knows that this is entirely wrong for physical systems with many constituents: macroscopic behavior of gas is qualitatively different from that of a single molecule. Likewise, economy of a country is not explained by analysing a single RA as if he is on a deserted island all by himself, like Robinson Crusoe without even Friday, and multiplying the number of population to the results.

Another quite a dramatic example is the concept of equilibrium. In many economic models equilibrium is described as a state in which (individual and aggregate) demand equals supply. The notion of statistical equilibrium, in which the aggregate equilibrium is compatible with stochastic behavior of the constituents, is outside the box of tools of mainstream economists. Again, physics teaches us that the equilibrium of a system does not require that every single element be in equilibrium by itself, but rather that the statistical distributions describing macroscopic aggregate phenomena be stable.

What modern physics can do for economics is, then, to open a way to a proper treatise of macro economy as an aggregation of individual economic agents, which is one main theme of econophysics on real economy gatti2006em ; bible2010 . Such a thought is not totally unfamiliar to open-minded economists, whose keyword is Heterogeneous Interacting Agents (HIA) blume2006economy , where ‘heterogeneity’ implies that each has different characteristics; different financial profile like different energy and momentum, and ‘interaction’ is trade with exchange of money, goods, workers, information, etc. just as physical particles interact with each other.

In this letter we will show that a system populated by many HIA generates equilibrium distribution in the form of scaling laws. In particular, economic literature has shown the existence of large and persistent differences in labour productivity across industries and countries aoyama2008 ; ikeda2009iclpd ; aoyama2008b . Productivity is often measured in terms of the ratio between firms’ revenues and the number of employees. It can be expected to be a unique value only within a very straightjacket hypothesis, such as the Representative Agent. If agents are heterogeneous and interact, then scaling laws emerge, and dispersion is nothing but a consequence of it. Using Japanese data we empirically demonstrate it. The conclusive remarks points out that a thermodynamical approach (see also foley1994statistical ; aoki2006rmp ) may be what economics needs if HIA are the actors of the drama.

For the purpose to study properties in probability distributions, it is essential to observe a large portion of the entire population of firms and workers. A database of only listed firms, for example, is insufficient to analyze properties of distributions. We employ the largest database of Credit Risk Database (CRD) in Japan (years 1995 to 2009), which includes a million firms and fifteen million workers in the year 2006, covering the large portion of the whole domestic population. Below we give our analysis for the year 2006, but note that the qualitative results are valid for other years as well.

We measure the value added and the labor of each firm to have the information of output and input in the production at the individual level. We use simply the business sales/profits as a proximity to the value added, and the end-of-year number of workers (excluding managers) as the labor in order to calculate distributions for and and to uncover their properties.

To understand how workers are distributed among different levels of output and productivity, we shall study the distributions of and using the following probability density functions (PDFs). The joint PDF, , the conditional PDFs, and , and the marginal PDFs, and , are defined by

| (1) |

The conditional average of is defined by

| (2) |

for an arbitrary function , and similarly for .

As we shall see, since the PDFs are heavy-tailed for and , it is convenient for the purpose of statistical analysis to take the logarithms of variables:

| (3) |

where and are arbitrary scales.

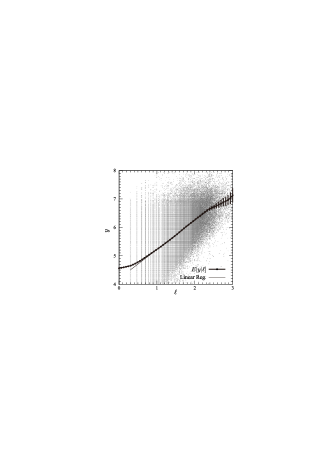

Fig. 1 shows the scatter plot for . To reveal statistical structure in data, which can be easily missed by parametric methods, we employ a kernel-based nonparametric methods li2007ne . Fig. 1 depicts a nonparametric regression curve with error bars (95% significance level) for . We can observe that there exists a range for which the relation:

| (4) |

holds where is a constant. In fact, the goodness of fit for nonparametric regression (; see hayfield2008ne for the definition) has a same level as that for linear regression () for the range, the estimation of which gives the estimation, (shown by a straight line in Fig. 1).

Similarly, for the range of , we have another relation, namely

| (5) |

with a constant . The validity for this relation is checked by the nonparametric () and linear () regressions, the latter of which gives the estimation, .

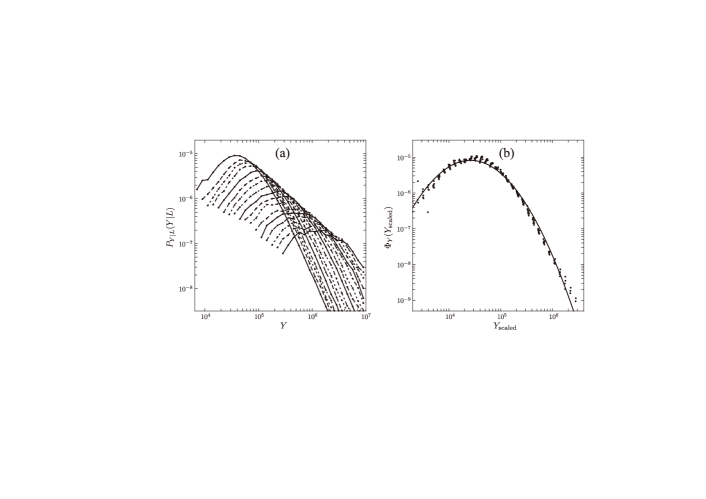

We find that these relations are simple consequences from two scaling relations for the conditional PDFs, and . Fig. 2 (a) depicts the conditional PDF, , with the conditioning values of are chosen at a logarithmically equal interval corresponding to the range in terms of histograms. By using the values of estimated above, we find that the conditional PDF obeys a scaling relation:

| (6) |

where and is a scaling function, as shown by the fact that the PDFs for different values of fall onto a curve depicted in Fig. 2 (b). It is straightforward to show that Eq. (4) follows from Eq. (6).

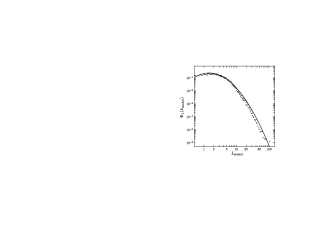

Similarly, we have another scaling relation for

| (7) |

where and is a scaling function, as shown by Fig. 3. And also Eq. (5) immediately follows from Eq. (7).

The two scaling laws, Eqs. (6) and (7), which we collectively call the double scaling law (DSL) have strong consequences to the function form of the joint PDF. Let us briefly describe them in the following.

Let us choose the reference scales and to be within the region of the -plane where DSL is valid. Then by substituting , into Eqs. (1), (6) and (7), We obtain the marginal PDFs, and in terms of the invariant functions, and :

| (8) | ||||

| (9) |

From Eqs. (6) and (7) and the above, we arrive at the following equation for the s:

| (10) |

This equation puts strong constraints the form of ’s. We have converted the above to differential equations and have derived complete solutions of Eq. (10).111Since the proof is too lengthy for this letter, it will be published elsewhere in near future. Depending on whether or not, the solution is qualitatively different, which we shall explain below.

When , we find the following relation between ’s is necessary and sufficient for Eq. (10):

| (11) |

In other words, we have one arbitrary function in the solution. In this case, Eqs. (8) and (9) implies that

| (12) | ||||

| (13) |

with

| (14) |

This result is straightforward to understand: Due to , we have

| (15) |

Therefore, an arbitrary function of is a function of as far as dependence on and is concerned. This is why an arbitrary function is left in the solution. Also the marginal PDFs in Eqs. (12) and (13) results from the relation (1).

For , we obtain,

| (16) | ||||

| (17) | ||||

| (18) | ||||

| (19) |

The joint PDF is given by the following:

| (20) |

We find that in the limit we obtain the power laws for and , which is consistent with the results (12) and (13) above.

The parameter of is estimated in two ways: The best fit of the theoretical expression (16) in Fig. 2 (b) yields , while Eq. (16) in Fig. 3 yields . These measured values of agree with each other very well, with combined value , assuming equal weight and no correlation. The marginal PDF and in Eqs. (18) and (19) agrees with empirical data very well with these values of . These analysis show that our theoretical results above are in good agreement with data.

We stress that the above results are proven in the local region of the -plane where DSL is valid. On the other hand, if the lognormal PDF (20) is valid everywhere on the plane, one may obtain the marginal PDFs and s as given in Eq. (17)–(19), as can be obtained by integrating Eq. (20) over , and then obtain in Eq. (17) from Eqs. (6) and (7), and so forth, which constitute easy checks of the relation between various functions.

Let us now study the labor productivity in case of , as such is the reality as shown empirically. The joint PDF of , is given by the following:

| (21) |

Substituting the expression (20) into the above, we find that is express, we obtain that too is of lognormal form like the r.h.s. of (20) with replaced by

| (22) | ||||

| (23) |

respectively. By substituting empirical values found for and (the average of the two central values of found above), we find that they are , , . By comparing this with Eq. (19), we find the following marginal PDF for the productivity :

| (24) | ||||

| (25) |

where with and the measured values of yield . Also, the conditional PDF satisfies the scaling law;

| (26) | ||||

| (27) |

while the average of the labor for a given productivity is given by the following;

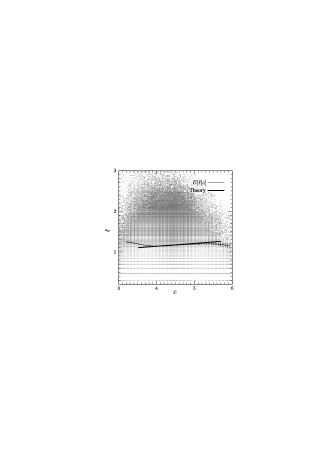

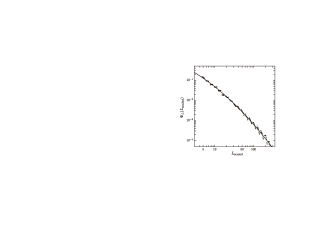

| (28) |

Fig. 4 checks the result of Eq. (28) with the parameter estimated from the relation in Eq. (27), where the thick straight line is the theoretical calculation. Fig. 5 depicts the scaling function , where the curve is given by the fitting in Eq. (27). Both of these results confirm our results in the region where the scaling relations are valid.

In this paper, we have shown that the Japanese data for some one million firms show that the firm distribution in plane satisfy the double scaling law (DSL). We have shown that DSL leads to either power-law for the marginal PDF of and , or the lognormal PDF for the joint PDF of and . Although we have concentrated on these specific two variables because of their importance for the labour productivity, we believe that other financial quantities obey DSL. Furthermore, joint PDF of more than two variables are expected to obey the similar scaling laws, which yield extensions of the results explained above, including multi-variate lognormal distributions, yielding simple relations such as Eq. (25) between scaling exponents. These laws offer straightforward guidance to the method of aggregation: the macroscopic quantities are now expressed in terms of just a few parameters in the PDFs, conditioned by DSL. Thus scaling laws and the resulting lognormal distributions should be the basic ingredient of economics of HIA, which is an equivalence of the statistical physics, bridging micro and macro economy.

Acknowledgements.

We would like to thank Hiroshi Iyetomi, Yuichi Ikeda, Wataru Souma and Hiroshi Yoshikawa for discussions, support and encouragements. We also would like to thank Mr. Shigeru Hikuma, the President of the CRD Association for providing us with their database. The present work was supported in part by the Program for Promoting Methodological Innovation in Humanities and Social Sciences, and by Cross-Disciplinary Fusing of the Japan Society for the Promotion of Science, Grant-in-Aid for Scientific Research (B) 20330060 (2008-10), and Invitation Fellowship Program for Research in Japan (Short term) ID No.S-09132 of the Ministry of Education, Science, Sports and Culture, Japan.References

- (1) F. Kydland and E. Prescott, Econometrica: Journal of the Econometric Society, 1345(1982)

- (2) J. Galí, Monetary Policy, Inflation, and the Business Cycle (Princeton University Press, 2008)

- (3) J. Keynes, The General Theory (McMillan, London, 1936)

- (4) D. Delli Gatti, E. Gaffeo, M. Gallegati, G. Giulioni, and A. Palestrini, Emergent Macroeconomics: An Agent-based Approach to Business Fluctuations (Springer, 2008)

- (5) H. Aoyama, Y. Fujiwara, Y. Ikeda, H. Iyetomi, and W. Souma, Econophysics and Companies: Statistical Life and Death in Complex Business Networks (Cambridge University Press, Cambridge, U.K., 2010)

- (6) L. Blume and S. Durlauf, eds., Economy as an evolving complex system III, Current perspectives and future directions (Oxford University Press, 2006)

- (7) H. Aoyama, H. Yoshikawa, H. Iyetomi, and Y. Fujiwara, RIETI Discussion Paper Series, 08-E-035(2008)

- (8) Y. Ikeda and W. Souma, Progress of Theoretical Physics Supplement 179, 93 (2009)

- (9) H. Aoyama, H. Yoshikawa, H. Iyetomi, and Y. Fujiwara, Progress of Theoretical Physics Supplement 179, 80 (2009)

- (10) K. Foley Duncan, Journal of Economic Theory 62, 321 (1994)

- (11) M. Aoki and H. Yoshikawa, Reconstructing Macroeconomics: A Perspective from Statistical Physics and Combinatorial Stochastic Processes (Cambridge University Press, New York, 2007)

- (12) Q. Li and J. S. Racine, Nonparametric Econometrics: Theory and Practice (Princeton University Press, 2007)

- (13) T. Hayfield and J. S. Racine, Journal of Statistical Software 27 (2008)

- (14) Since the proof is too lengthy for this letter, it will be published elsewhere in near future.