Shape of Growth Rate Distribution

Determines the Type of Non-Gibrat’s Property

Abstract

In this study, the authors examine exhaustive business data on Japanese firms, which cover nearly all companies in the mid- and large-scale ranges in terms of firm size, to reach several key findings on profits/sales distribution and business growth trends. First, detailed balance is observed not only in profits data but also in sales data. Furthermore, the growth-rate distribution of sales has wider tails than the linear growth-rate distribution of profits in log-log scale. On the one hand, in the mid-scale range of profits, the probability of positive growth decreases and the probability of negative growth increases symmetrically as the initial value increases. This is called Non-Gibrat’s First Property. On the other hand, in the mid-scale range of sales, the probability of positive growth decreases as the initial value increases, while the probability of negative growth hardly changes. This is called Non-Gibrat’s Second Property. Under detailed balance, Non-Gibrat’s First and Second Properties are analytically derived from the linear and quadratic growth-rate distributions in log-log scale, respectively. In both cases, the log-normal distribution is inferred from Non-Gibrat’s Properties and detailed balance. These analytic results are verified by empirical data. Consequently, this clarifies the notion that the difference in shapes between growth-rate distributions of sales and profits is closely related to the difference between the two Non-Gibrat’s Properties in the mid-scale range.

pacs:

I Introduction

Distributions with a power-law tail have been found in various fields of natural and social science. Examples of such studies include, for instance, avalanche sizes in a sandpile model Bak , fluctuations in the intervals of heartbeats Peng , fish school sizes Bonabeau , citation numbers of scientific papers Render , frequency of jams in Internet traffic TTS , city sizes (see the recent review in Ref. Saichev ), land prices Kaizoji –Ishikawa100 , stock market price changes Mantegna , and firm sizes Stanley00 . Here, variables (denoted by ) follow the probability density function (PDF):

| (1) |

over some size threshold . This is called Pareto’s Law, which was first observed in the field of personal income Pareto . The index is called the Pareto index. Refer to Newman Newman for a useful description of Pareto’s Law.

In statistical physics, the study of distributions with a power-law tail (1) is significant because the -th moment diverges in the case of . It is impossible to describe the system by using the variance or the standard deviation in the case of . This feature comes from power-law behavior in the tail. Furthermore, it is worth noting that a large portion of the overall data are included in the power-law tail. For example, approximately of total sales or profits in Japanese firms are included in the power-law tail. In economics (especially in macroeconomics), one of the major issues is the state of the entire economy. In this sense, it is important to clarify the nature of the power-law tail not only in physics but also in economics.

In general, the power-law breaks below the size threshold to suppress the divergence of the PDF Badger , Montroll . There are many distributions that have a power-law tail. These include, for instance, Classical Pareto Distribution (Pareto Type I Distribution), Pareto Type II Distribution, Inverse Gamma Distribution, Inverse Weibull Distribution, –Distribution, A–Distribution and B–Distribution Aoyama book . In addition to these distributions, it has been hypothesized that many other distributions with a power-law tail follow the log-normal distribution for mid-sized variables below the size threshold :

| (2) |

Here, is a mean value and is a variance. A lower bound of the mid-scale range is often related to the lower bound of an exhaustive set of data. A pseudo log-normal distribution is approximately derived from A–Distribution or B–Distribution in the mid-sized range Aoyama book .

The study of distributions in the mid-scale range below the size threshold is as important as the study of the power-law tail. In physics, we are interested not only in the mechanism generating a power-law tail but also in the reason for the tail breaking. In economics, we should note that the majority of firms are mid-sized. For instance, in sales or profits data, more than of the total number of firms are in the mid-scale range. In this study, by examining exhaustive business data of Japanese firms that nearly cover the mid- and large-scale ranges, the authors investigate the relevant distributions with a power-law tail. This research is expected to be useful for understanding phenomena not only in economics but also in physics.

On the one hand, it has been shown that Pareto’s Law and the log-normal distribution can be derived by assuming some model. For example, a multiplicative process with boundary constraints and additive noise can generate Pareto’s Law Levy . On the other hand, by using no model, Fujiwara et al. have recently shown that Pareto’s Law (1) is derived from Gibrat’s Law and from the detailed balance observed in the large-scale range of exhaustive business data Fujiwara . The relations among laws observed in exhaustive business data are important for examining the characteristics of distributions based on firm-size. For instance, in the study of Fujiwara et al., it was found that Pareto index is related to the difference between a positive growth-rate distribution and a negative one. Furthermore, along the lines of their study, one of the authors (A. I) has shown that the log-normal distribution (2) can be inferred from detailed balance and from Non-Gibrat’s Property observed in the profits data of the mid-scale range Ishikawa . The study of the growth-rate distribution is an interesting subject in itself, and an ongoing investigation into this issue has progressed recently Riccaboni .

Detailed balance means that the system is thermodynamically in equilibrium, the state of which is described as

| (3) |

Here, and are firm sizes at two successive points in time. In Eq. (3), the joint PDF is symmetric under the time reversal exchange .

Gibrat’s Law and Non-Gibrat’s Property are observed in the distributions of firm-size growth rate . The conditional PDF of the growth rate is defined as by using the PDF and the joint PDF . Gibrat’s Law, which is observed in the large-scale range, implies that the conditional PDF is independent of the initial value Gibrat :

| (4) |

Sutton Sutton provides an instructive resource for obtaining the proper perspective on Gibrat’s Law.

Non-Gibrat’s Property reflects the dependence of the growth-rate distribution on the initial value . The following properties are observed in the mid-scale range of positive profits data of Japanese firms Ishikawa :

| (5) | |||||

| (6) | |||||

| (7) |

Here, and are positive constants. In this composite Non-Gibrat’s Property (5)–(7), the probability of positive growth decreases and the probability of negative growth increases symmetrically as the initial value increases in the mid-scale range. It is particularly noteworthy that the shape of the growth-rate distribution (5)–(6) uniquely determines the change in the growth-rate distribution (7) under detailed balance (3). Moreover, the rate-of-change parameter appears in the log-normal distribution (2). We designate (5)–(7) as Non-Gibrat’s First Property to distinguish it from another Non-Gibrat’s Property that is observed in sales data.

The shape of the growth-rate distribution (5)–(6) is linear in log-log scale. This type of growth-rate distribution is observed in profits and income data of firms (for instance Okuyama , Ishikawa10 , Economics ). In contrast, it has been reported in various articles that the growth-rate distributions of assets, sales, number of employees in firms, and personal income have wider tails than those of profits and income in log-log scale (for instance Amaral , Fujiwara , Matia , Fu , Buldyrev , Economics ). In this case, the shape of the growth-rate distribution is different from Eqs. (5) and (6). There must be, therefore, another Non-Gibrat’s Property corresponding to this shape. In fact, it has been reported in several studies that a Non-Gibrat’s Property different from Non-Gibrat’s First Property exists in the mid-scale range of assets and sales of firms (for instance Aoyama –Takayasu ).

In this study, we report the following findings by employing the sales data of Japanese firms, which include not only data in the large-scale range but also those in the mid-scale range.

-

1.

Detailed balance (3) is confirmed in the mid- and large-scale ranges of sales data.

-

2.

In not only the large-scale range but also the mid-scale range of sales data, the growth-rate distributions have wider tails than those of profits in log-log scale.

-

3.

Under detailed balance (3), the allowed change of the growth-rate distribution in the mid-scale range is analytically determined by using empirical data. The change is different from that of profits. We call this Non-Gibrat’s Second Property.

-

4.

A log-normal distribution is derived from Non-Gibrat’s Second Property and from detailed balance. This is verified with empirical data.

From these results, we conclude that the shape of the growth-rate distribution determines the type of Non-Gibrat’s Property in the mid-scale range.

II Non-Gibrat’s First Property

In this section, we review the analytic discussion in Ref. Ishikawa and confirm it by applying the results to newly obtained data. In the analytic discussion, detailed balance (3) and the shape of the growth-rate distribution (5)–(6) lead uniquely to a change in the growth-rate distribution (7). In addition, Non-Gibrat’s First Property and detailed balance derive a log-normal distribution (2) in the mid-scale range.

In this study, we employ profits and sales data supplied by the Research Institute of Economy, Trade and Industry, IAA (RIETI) RIETI . In this section we analyze profits data, and sales data are analyzed in the next section. The data set, which was created by TOKYO SHOKO RESEARCH, LTD. TSR in 2005, includes approximately 800,000 Japanese firms over a period of three years: the current year, the preceding year, and the year before that. The number of firms is approximately the same as the actual number of active Japanese firms. This database is considered nearly comprehensive, at least in the mid- and large-scale ranges. In this study, we investigate the joint PDF and the distribution of the growth rate . Therefore, by using data of each firm in the previous three years, we analyze a data set that has two values at two successive points in time as follows: = (data in preceding year, data in current year) (data in year before last, data in preceding year). Here, indicates set-theoretic union. This superposition of data is employed in order to secure a statistically sufficient sample size. This procedure is allowed in cases where the economy is stable, that is, thermodynamically in equilibrium. The validity is checked by detailed balance, as described below.

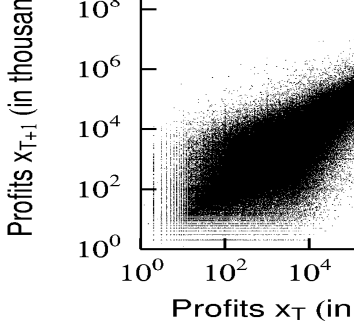

First, detailed balance (3) is observed in profits data. Note that only positive-profits data are analyzed here, since we assume that non-negligible negative profits are not listed in the database. Negative-profits data are thus not regarded as exhaustive. We employ “622,420” data sets that have two positive profits at two successive points in time. Figure. 1 shows the joint PDF as a scatter plot of individual firms. Detailed balance (3) is confirmed by the Kolmogorov–Smirnov (KS), Wilcoxon–Mann–Whitney (WMW), and Brunner–Munzel (BM) tests. In the statistical tests, the range of is divided into bins as to approximately equalize the number of data in each bin “ and .” Here, and are the lower and the upper bounds of , respectively. We compare the distribution sample for “ and ” with another sample for “ and ” () by making the null hypothesis that these two samples are taken from the same parent distribution.

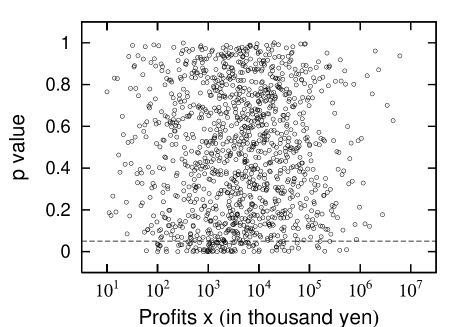

Each value of the WMW test for the case of is shown in Fig. 2. Note that the profits data contain a large number of same-value amounts, which are round numbers: , , , , , , , , . This phenomenon is frequently observed in economic data. A bin with a round-number amount may contain an exceptionally large number of data in this method of division. For the case of , almost all bins typically contain data; however, a bin with the round number of , for instance, contains an exceptional data. In order to generally equalize the average amount of data in bins to the typical value, an appropriate number of empty bins are inserted at such bins of round-number amounts as needed (Fig. 3). In the case of , there are empty bins. values with respect to the remaining bins are depicted in Fig. 2, in which values exceed . Regardless of the division number and the kind of test, values exceed in approximately of bins. This means that the null hypothesis is not rejected within the significance level in approximately of the range. This result does not change in the case where the range of is divided into logarithmically equal bins. Consequently, the detailed balance (3) in Fig. 1 is generally confirmed.

Second, we divide the range of the initial value into logarithmically equal bins as in order to identify the shape of the growth-rate distribution and the change as the initial value increases. The conditional PDFs of the logarithmic growth rate are shown in Figs. 4–6.

In Figs. 5 and 6, the growth-rate distributions in the mid- and large-scale ranges are approximated by a linear function of :

| (8) | |||||

| (9) |

The approximation (8)–(9) is equivalent to Eqs. (5) and (6) by using relations and . From , the normalization coefficient (or the intercept ) is determined as

| (10) |

Following the discussion in a previous work Ishikawa , we derive the change in the growth-rate distribution (7) from the shape of the growth-rate distribution (5)–(6) under detailed balance (3) and then derive the log-normal distribution in the mid-scale range. Under the exchange of variables from to , two joint PDFs and are related to each other as . Substituting the joint PDF for the conditional PDF and using detailed balance (3), we obtain

| (11) |

By substituting the conditional PDF for the shape of the growth-rate distribution (5)–(6), another expression of detailed balance (11) is reduced to

| (12) |

for the case of . Here, we denote . By expanding Eq. (12) around with and , the following three differential equations are obtained:

| (13) |

| (14) |

The same differential equations are obtained for . Equations (14) uniquely fix as Eq. (7). Now, let us verify this by empirical data.

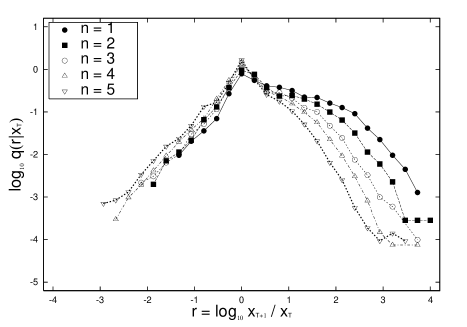

Figure 7 shows and estimated by fitting the approximation (8)–(9) to each growth-rate distribution in Figs. 4–6. In Fig. 7, is fixed as the empirical value and is estimated by using the least-squares method.

In Fig. 4, the linear function (8)–(9) is difficult to approximate for each growth-rate distribution, and the values for in Fig. 7 are untrustworthy. In Fig. 5, however, the linear approximation (8)–(9) is appropriate. Applying the change in the growth-rate distribution (7) to in Fig. 7, we obtain the rate-of-change parameter from and from by using the least-squares method. This coincidence of two estimated values guarantees Non-Gibrat’s First Property (5)–(7) in the empirical data. We regard as the mid-scale range.

In Fig. 6, the growth-rate distribution barely changes as increases. This means that Gibrat’s Law (4) is valid in the large-scale range. In Fig. 7, the values vary in the large-scale range, since the number of data in Fig. 6 is statistically insufficient to estimate by the least-squares method. However, by measuring the positive and negative standard deviations of each growth-rate distribution in Figs. 4–6, we confirmed that the growth-rate distribution only slightly changes in the range (Fig. 8). From Fig. 8, we regard as the large-scale range and set in this range. Strictly speaking, a constant parameter must not take different values. However, in the database, a large number of firms stay in the same range for two successive years. This parameterization is, therefore, generally suitable for describing the PDF.

In Fig. 7, hardly changes in the mid- and large-scale ranges . This is consistent with in Eqs. (7) and (10). Consequently, by approximation we determine that the dependence of on is negligible in the mid- and large-scale ranges. Using (7), Eq. (13) uniquely decides the PDF of as

| (15) |

Here, we regard in as a constant and denote . The solutions (7) and (15) satisfy Eq. (12) beyond perturbation around , and thus these are not only necessary but also sufficient.

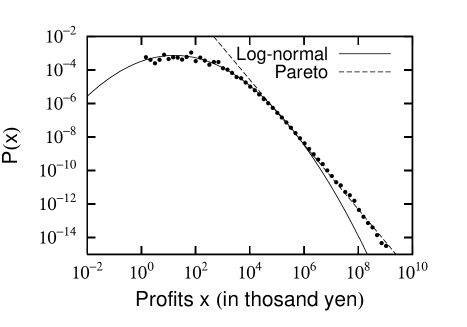

Figure 9 shows that the resultant PDF (15) fits correctly with the empirical profits data. In the large-scale range (), the PDF (15) behaves as Pareto’s Law (1). The Pareto index is estimated as approximately in the large-scale range () of Fig. 9. In the mid-scale range, the PDF (15) behaves as the log-normal distribution (2) with , . Applying the PDF (15) to the mid-scale range () of Fig. 9, we obtain the rate-of-change parameter by using the least-squares method. The error bar is not small because we have applied the least-squares method to the quadratic curve in log-log scale. The estimated value () is, however, consistent with the values estimated by the change in ( or ). From these results, we conclude that Non-Gibrat’s First Property is confirmed by the empirical data.

III Non-Gibrat’s Second Property

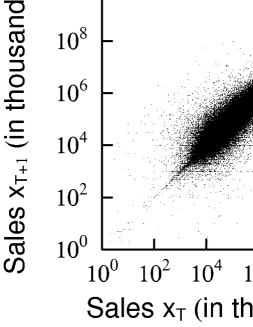

In this section, we investigate another Non–Gibrat’s Property observed in the mid-scale range of sales data. This is the main aim of this study. First, detailed balance (3) is also observed in sales data. Here, we employ “1,505,108” data sets that have two sales at two successive points in time. Figure 10 shows the joint PDF as a scatter plot of individual firms.

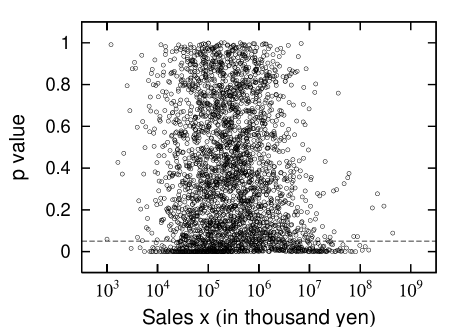

Detailed balance (3) is also confirmed by using the KS, WMW, and BM tests in the same manner as in the previous section. Figure 11 shows each value of the BM test for the case. Regardless of the division number and the kind of test, values exceed in approximately of bins. This means that the null hypothesis is not rejected within the significance level in approximately of the range. Note that the sales data also contain a large number of same-value amounts, which are round numbers. values of the statistical test for bins with a large number of round values are unusually small. In this situation, is acceptable. The percentage is slightly higher in the case where the range of is divided into logarithmically equal bins. We assume, therefore, that detailed balance (3) in Fig. 10 is generally verified.

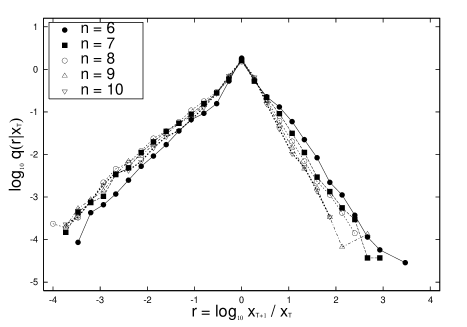

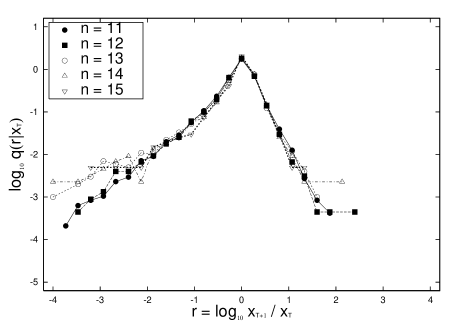

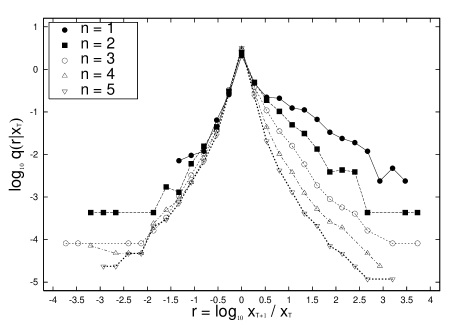

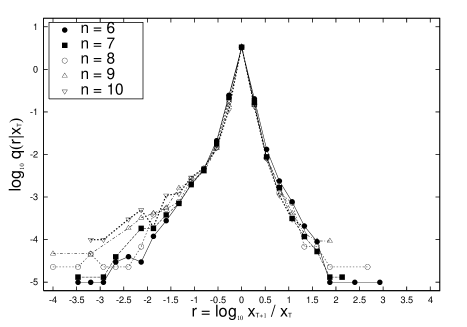

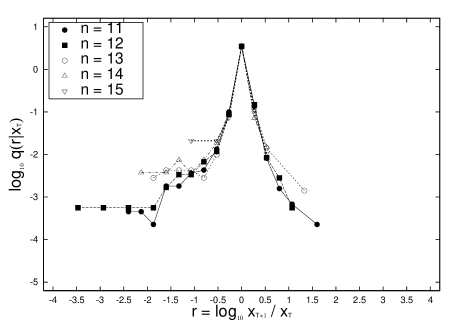

Second, we divide the range of the initial value into logarithmically equal bins as . The conditional growth-rate distributions are shown in Figs. 12–14.

Each growth-rate distribution in Figs. 12–14 has curvatures. It is difficult to approximate the growth-rate distributions by the linear approximation (8)–(9) as in the profits case. As the simplest extension, we have added a second-order term with respect to to express the curvatures as follows:

| (16) | |||||

| (17) |

Note that we must introduce a cut in order to normalize the probability integration as , since Eqs. (16) and (17) are quadratic with respect to . From this normalization condition, can be expressed by using , , and . The expression is quite complicated, and it is later observed that only slightly depends on in the empirical data. Therefore, we do not describe the expression here.

The approximation (16)–(17) is rewritten as

| (18) | |||||

| (19) |

By using this shape, in the case of , detailed balance (11) is reduced to

| (20) |

By expanding Eq. (20) around with and , the following five differential equations are obtained:

| (21) |

| (22) | |||

| (23) | |||

| (24) | |||

| (25) |

The same differential equations are obtained for . Equations (22)–(25) uniquely fix the change in the growth-rate distribution , as follows:

| (26) | |||||

| (27) | |||||

| (28) | |||||

| (29) |

Now, let us confirm these solutions with the empirical data.

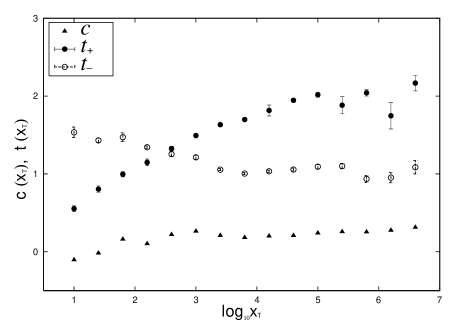

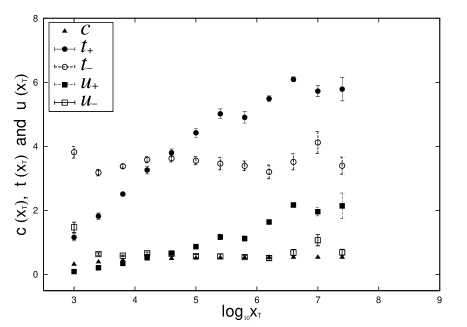

Figure 15 shows , and estimated by fitting the approximation (16)–(17) to each growth-rate distribution in Figs. 12–14. In Fig. 15, is fixed as the empirical value and and are estimated by using the least-squares method. For in Fig. 14, there are not sufficient data points to estimate , for or to estimate the error bar for . Therefore, data points for are not plotted in Fig. 15.

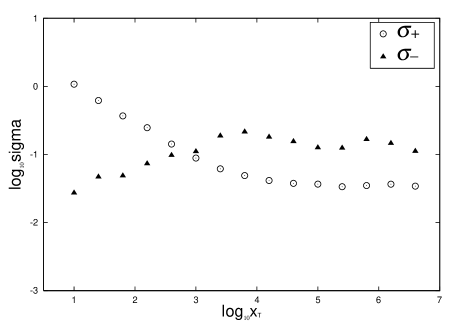

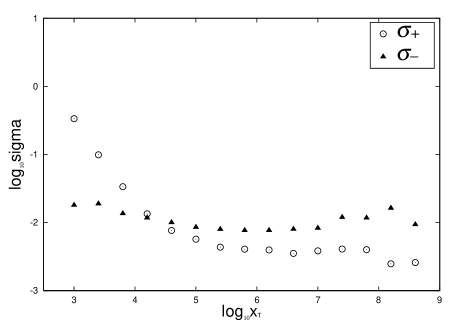

On the one hand, for in Figs. 13 and 14, the growth-rate distribution hardly changes as increases. This means that Gibrat’s Law (4) is verified by the empirical data. We regard as the large-scale range and set in this range because and do not depend on . In Fig. 15, the values of and vary in this range because the number of data in Fig. 14 is statistically insufficient to estimate them by the least-squares method. However, by measuring positive and negative standard deviations of each growth-rate distribution in Figs. 12–14, we confirmed that the growth-rate distribution hardly changes in the large-scale range (Fig. 16).

On the other hand, in Fig. 12, while the negative growth-rate distribution hardly changes as increases, the positive growth-rate distribution gradually decreases. This is Non-Gibrat’s Property in the mid-scale range of sales data. We should estimate parameters and by applying the change in the growth-rate distribution (26)–(29) to Fig. 15. However, there are insufficient data points in Fig. 15 for using the least-squares method by polynomial functions (26)–(29). Consequently, as a first-order approximation, we assume that the negative growth-rate distribution does not depend on , even in the mid-scale range. This approximation is guaranteed by Fig. 16 because the negative standard deviation hardly changes compared with the positive standard deviation .

In this approximation, the parameters are simplified as

| (30) |

Only the change in the positive growth-rate distribution depends on as follows:

| (31) | |||||

| (32) |

We call this Non-Gibrat’s Second Property.

Applying (31) to in Fig. 15, we obtain the rate-of-change parameter by the least-squares method. We regard as the mid-scale range of sales. In this range, and hardly change compared with , so the approximation (32) is considered relevant. Nevertheless, the value estimated by the difference between and disagrees with the value estimated by the change in . Most likely, this comes from a limitation of the second-order approximation with respect to (16)–(17). To fix this discrepancy, we may add a third-order term with respect to . We will consider this point in the conclusion. In addition, we should note that the intercept only slightly depends on in the mid- and large-scale ranges , as in the profits case.

Using (26)–(27), Eq. (21) uniquely determines the PDF of as

| (33) |

Here, we regard in as a constant and denote . The solutions (26)–(29) and (33) satisfy Eq. (20) beyond perturbation around , so these are not only necessary but also sufficient. In the approximation (30), the PDF is reduced to

| (34) |

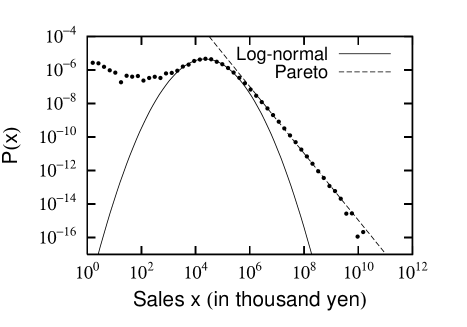

Figure 17 shows that the resulting PDF (34) fits correctly with the empirical sales data. In the large-scale range (), the PDF (34) behaves as Pareto’s Law (1). The Pareto index is estimated as approximately in the large-scale range () of Fig. 17. In the mid-scale range, the PDF (34) behaves as the log-normal distribution (2) in the same manner as in the profits case. Applying the PDF (34) to the mid-scale range () of Fig. 17, we obtain the rate-of-change parameter by using the least-squares method. This is consistent with the value estimated by the change in (). From these results, we conclude that Non-Gibrat’s Second Property is also confirmed by the empirical data.

IV Conclusion

In this study, we have employed exhaustive business data on Japanese firms that nearly cover not only the entire large-scale range but also the entire mid-scale range in terms of firm size. Using this newly assembled database, we first reconfirmed the previous analyses for profits data Ishikawa as described below. In the mid-scale range, the log-normal distribution is derived from detailed balance and from Non-Gibrat’s First Property. In Non-Gibrat’s First Property, the probability of positive growth decreases and the probability of negative growth increases symmetrically as the initial value increases. Under detailed balance, this change is uniquely reduced from the shape of the growth-rate distribution, which is linear in log-log scale.

Second, the following findings were reported with respect to sales data. Detailed balance is also observed in the mid- and large-scale ranges of sales data. The growth-rate distribution of sales has wider tails than the linear growth-rate distribution of profits in log-log scale. In the mid-scale range, while the probability of negative growth hardly changes as the initial value increases, the probability of positive growth gradually decreases. This feature is different from Non-Gibrat’s First Property observed in the profits data. We have approximated the growth-rate distribution with curvatures by a quadratic function. In addition, from an empirical observation, we have imposed the condition that the negative growth-rate distribution does not depend on , even in the mid-scale range. Under detailed balance, these approximations and conditions uniquely lead to a decrease in positive growth. We call this Non-Gibrat’s Second Property. In the mid-scale range, the log-normal distribution is also derived from detailed balance and from Non-Gibrat’s Second Property. These results are confirmed by the empirical data.

In this study, it was clarified that the shape of the growth-rate distribution of sales is different from that of profits. It was also demonstrated that this difference is closely related to the difference between two kinds of Non-Gibrat’s Properties in the mid-scale range. The growth-rate distribution of income of firms is approximated by a linear function in log-log scale as in the profits data. The growth-rate distributions of assets, the number of employees, and personal income have wider tails than a linear function in log-log scale, as in the sales data. If we obtained exhaustive data that include the mid-scale range, Non-Gibrat’s First Property would probably be observed in the income data of firms, while Non-Gibrat’s Second Property would probably be observed in the assets, the number of employees, and the personal income data.

We have not determined what makes the difference between the shapes of the growth-rate distributions. However, this difference is probably related to the following factors Economics . Income and profits of firms are calculated by a subtraction of total expenditures from total sales in a rough estimate. Assets and sales of firms, the number of employees, and personal income are not calculated by any subtraction.

Let us consider the distribution of added values, the sum of which is GDP. Clearly, added values are calculated by some subtraction. If we obtained exhaustive data of added values, Non-Gibrat’s First Property would certainly be observed. It has been reported that the growth-rate distribution of GDPs of countries is linear in log-log scale (for instance Canning ). This report reinforces that speculation. The results in this paper should be carefully considered in cases where governments and firms discuss strategies of growth.

Finally, we consider a method to fix the inconsistency by which the rate-of-change parameter is not estimated by the difference between (32). Let us add not only the second-order term with respect to but also a third-order term as follows:

| (35) | |||||

| (36) |

In the same manner as in the previous section, under detailed balance, coefficients , , and are uniquely obtained as follows:

| (37) | |||||

| (38) | |||||

| (39) | |||||

| (40) | |||||

| (41) | |||||

| (42) |

By imposing the condition that the negative growth-rate distribution does not depend on even in the mid-scale range, these are simplified as follows:

| (43) | |||||

| (44) | |||||

| (45) |

The results in the previous sections (31) and (32) correspond to a special case , in Eqs. (43)–(45). In the previous section, it was difficult to estimate by the difference in . In the expressions (43)–(45), this discrepancy is probably solved with a negative . Note that Eqs. (26)–(29) cannot be reduced to Eqs. (43) and (44) in any parameterization.

It is technically difficult to estimate , , and by approximating the growth-rate distribution by the cubic function (35)–(36) and to estimate and fitting Eqs. (43)–(45) by the least-squares method. At the same time, under the approximation by the cubic function (35)–(36), the integration converges without a cut , as in the linear approximation. Because this work involves difficulties as well as advantages, we will investigate the above issues in the near future.

Acknowledgments

The authors thank the Research Institute of Economy, Trade and Industry, IAA (RIETI) for supplying the data set used in this work. This study was produced from the research the authors conducted as members of the Program for Promoting Social Science Research Aimed at Solutions of Near-Future Problems, “Design of Interfirm Networks to Achieve Sustainable Economic Growth.” This work was supported in part by a Grant-in-Aid for Scientific Research (C) (No. 20510147) from the Ministry of Education, Culture, Sports, Science and Technology, Japan. Takayuki Mizuno was supported by funding from the Kampo Foundation 2009.

References

-

(1)

P. Bak, C. Tang and K. Wiesenfeld, Phys. Rev. Lett. 59 (1987) 381;

P. Bak, C. Tang and K. Wiesenfeld, Phys. Rev. A 38 (1988) 364. - (2) C.-K. Peng, J. Mietus, J. M. Hausdorff, S. Havlin, H. E. Stanley and A. L. Goldberger, Phys. Rev. Lett. 70 (1993) 1343.

- (3) E. Bonabeau and L. Dagorn, Phys. Rev. E 51 (1995) R5220.

- (4) S. Render, Eur. Phys. J. B4 (1998) 131.

- (5) M. Takayasu, H. Takayasu and T. Sato, Physica A 233 (1996) 824.

- (6) A. Saichev, Y. Malevergne and D. Sornette, Theory of Zipf’s law and beyond, Lecture Notes in Economics and Mathematical Systems, p. 632 (Springer, 2009).

- (7) T. Kaizoji, Physica A 326 (2003) 256.

- (8) T. Yamano, Eur. Phys. J. B 38 (2004), 665.

-

(9)

A. Ishikawa, Physica A 371 (2006) 525;

A. Ishikawa, Prog. Theor. Phys. Supple. No. 179 (2009) 103. - (10) R. N. Mantegna and H. E. Stanley, Nature 376 (1995) 46.

- (11) M. H. R. Stanley, S. V. Buldyrev, S. Havlin, R. Mantegna, M. A. Salinger and H. E. Stanley, Economics Lett. 49 (1995) 453.

- (12) V. Pareto, Cours d’Economique Politique (Macmillan, London, 1897).

-

(13)

M. E. J. Newman, Contemporary Physics 46 (2005) 323;

A. Clauset, C. R. Shalizi and M. E. J. Newman, SIAM Review 51 (2009) 661. - (14) W. W. Badger, in B. J. West (ed.) Mathematical Models as a Tool for the Social Science, p. 87 (Gordon and Breach, New York, 1980).

- (15) E. W. Montroll and M. F. Shlesinger, J. Stat. Phys. 32 (1983) 209.

- (16) H. Aoyama, H. Iyetomi, Y. Ikeda, W. Souma and Y. Fujiwara, ECONOPHYSICS (Kyoritsu, Tokyo, 2008 in Japanese).

-

(17)

M. Levy, S. Solomon, Int. J. Mod. Phys. C 7 (1996) 595;

H. Kesten, Acta Math. 131 (1973) 207;

D. Sornette, R. Cont, J. Phys. I 7 (1997) 431;

H. Takayasu, A.-H. Sato, M. Takayasu, Phys. Rev. Lett. 79 (1997) 966. -

(18)

Y. Fujiwara, W. Souma, H. Aoyama, T. Kaizoji and M. Aoki, Physica A 321 (2003), 598;

Y. Fujiwara, C. D. Guilmi, H. Aoyama, M. Gallegati and W. Souma, Physica A 335 (2004), 197. -

(19)

A. Ishikawa, Physica A 367 (2006) 425;

A. Ishikawa, Physica A 383 (2007) 79. - (20) M. Riccaboni, F. Pammolli, S. V. Buldyrev, L. Ponta and H. E. Stanley, Proc. Natl. Accad. Sci. USA 105 (2008) 19595.

- (21) R. Gibrat, Les inegalites economiques (Sirey, Paris, 1932).

- (22) J. Sutton, J. Econo. Lit. 35 (1997) 40.

- (23) K. Okuyama, M. Takayasu and H. Takayasu, Physica A 269 (1999) 125.

- (24) A. Ishikawa, Physica A 363 (2006) 367.

- (25) A. Ishikawa, Economics 3 –Special Issue Reconstructing Macroeconomics, 2009–11.

- (26) L. A. N. Amaral, S. V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M. A. Salinger, H. E. Stanley, and M. H. R. Stanley, J. Phys. I France 7 (1997) 621.

- (27) K. Matia, D. Fu, S. V. Buldyrev, F. Pammolli, M. Riccaboni and H. E. Stanley, Europhys. Lett. 67 (2004) 498.

- (28) D. Fu, F. Pammolli, S. V. Buldyrev, M. Riccaboni, K. Matia, K. Yamasaki and H. E. Stanley, Proc. Natl. Acad. Sci. 102 (2005) 18801.

- (29) S. V. Buldyrev, J. Growiec, F. Pammolli, M. Riccaboni and H. E. Stanley, J. Eur. Economic Association 5 (2-3) (2007) 574.

-

(30)

H. Aoyama, Ninth Annual Workshop on Economic Heterogeneous Interacting Agents (WEHIA 2004);

H. Aoyama, Y. Fujiwara and W. Souma, The Physical Society of Japan 2004 Autumn Meeting. - (31) H. Aoyama, H. Iyetomi, Y. Ikeda, W. Souma and Y. Fujiwara, Pareto Firms (Nihon Keizai Hyouronsha, Tokyo, 2007 in Japanese).

- (32) H. Takayasu, New way of financing firms based on the fat-tailed distribution of growth rate. APFA7 Tokyo Tech. Hitotsubashi Interdisciplinary Conference (2009).

- (33) Research Institute of Economy, Trade and Industry, IAA (RIETI), http://www.rieti.go.jp/en/index.html.

- (34) TOKYO SHOKO RESEARCH, LTD., http://www.tsr-net.co.jp/.

- (35) D. Canning, L. A. N. Amaral, Y. Lee, M. Meyer and H. E. Stanley, Economics Lett. 60 (1998) 335.