A copula based approach to adaptive sampling

Abstract

Our article is concerned with adaptive sampling schemes for Bayesian inference that update the proposal densities using previous iterates. We introduce a copula based proposal density which is made more efficient by combining it with antithetic variable sampling. We compare the copula based proposal to an adaptive proposal density based on a multivariate mixture of normals and an adaptive random walk Metropolis proposal. We also introduce a refinement of the random walk proposal which performs better for multimodal target distributions. We compare the sampling schemes using challenging but realistic models and priors applied to real data examples. The results show that for the examples studied, the adaptive independent Metropolis-Hastings proposals are much more efficient than the adaptive random walk proposals and that in general the copula based proposal has the best acceptance rates and lowest inefficiencies.

Keywords: Antithetic variables; Clustering; Metropolis-Hastings; Mixture of normals; Random effects.

1 Introduction

Bayesian inference using Markov chain Monte Carlo simulation methods is used extensively in statistical applications. In this approach, the parameters are generated from a proposal distribution, or several such proposal distributions, with the generated proposals accepted or rejected using the Metropolis-Hastings method; see for example Tierney (1994).

In adaptive sampling the parameters of the proposal distribution are tuned by using previous draws. Our article deals with diminishing adaptation schemes, which means that the difference between successive proposals converges to zero. In practice, this usually means that the proposals themselves eventually do not change. Important theoretical and practical contributions to diminishing adaptation sampling were made by Holden (1998), Haario et al. (2001), Gåsemyr (2003), Andrieu and Robert (2001), Andrieu, Moulines, and Doucet (2005), Andrieu and Moulines (2006), Roberts and Rosenthal (2007) and Roberts and Rosenthal (2006). The adaptive random walk Metropolis method was proposed by Haario et al. (2001) with further contributions by Atchadé and Rosenthal (2005), Andrieu, Moulines, and Doucet (2005) and Roberts and Rosenthal (2006). Giordani and Kohn (2008) propose an adaptive independent Metropolis-Hastings method with a mixture of normals proposal which is estimated using a clustering algorithm.

Although there is now a body of theory justifying the use of adaptive sampling, the construction of interesting adaptive samplers and their empirical performance on real examples has received less attention. Our article aims to fill this gap by introducing a -copula based proposal density. An antithetic version of this proposal is also studied and is shown to increase efficiency when the acceptance rate is above 70%. We also refine the adaptive Metropolis-Hastings proposal in Roberts and Rosenthal (2006) by adding a heavy tailed component to allow the sampling scheme to traverse multiple modes more easily. As well as being of interest in its own right, in some of the examples we have also used this refined sampler to initialize the adaptive independent Metropolis-Hastings schemes. We study the performance of the above adaptive proposals, as well as the adaptive mixture of normals proposal of Giordani and Kohn (2008), for a number of models and priors using real data. The models and priors produce challenging but realistic posterior target distributions.

Silva et al. (2008) is a longer version of our article that considers some alternative versions of our algorithms and includes more details and examples.

2 Adaptive sampling algorithms

Suppose that is the target density from which we wish to generate a sample of observations, but that it is computationally difficult to do so directly. One way of generating the sample is to use the Metropolis-Hastings method, which is now described. Suppose that given some initial we have generated the iterates . We generate from the proposal density which may also depend on some other value of which we call . Let be the proposed value of generated from . Then we take with probability

| (1) |

and take otherwise. If does not depend on , then under appropriate regularity conditions we can show that the sequence of iterates converges to draws from the target density . See Tierney (1994) for details.

In adaptive sampling the parameters of are estimated from the iterates . Under appropriate regularity conditions the sequence of iterates , converges to draws from the target distribution . See Roberts and Rosenthal (2007), Roberts and Rosenthal (2006) and Giordani and Kohn (2008).

We now describe the adaptive sampling schemes studied in the paper.

2.1 Adaptive random walk Metropolis

The adaptive random walk Metropolis proposal of Roberts and Rosenthal (2006) is

| (2) |

where is the dimension of and is a multivariate dimensional normal density in with mean and covariance matrix . In (2), for , with representing the initial iterations, for with ; is a constant covariance matrix, which is taken as the identity matrix by Roberts and Rosenthal (2006) but can be based on the Laplace approximation or some other estimate. The matrix is the sample covariance matrix of the first iterates. The scalar is meant to achieve a high acceptance rate by moving the sampler locally, while the scalar is considered to be optimal (Roberts et al. 1997) for a random walk proposal when the target is multivariate normal. We note that the acceptance probability (1) for the adaptive random walk Metropolis simplifies to

| (3) |

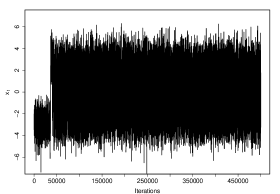

We refine the two component random walk Metropolis proposal in (2) by adding a third component with and with . We take if , for and . Alternatively, the third component can be a multivariate distribution with small degrees of freedom. We refer to this proposal as the three component adaptive random walk. The purpose of the heavier tailed third component is to allow the sampler to explore the state space more effectively by making it easier to leave local modes.

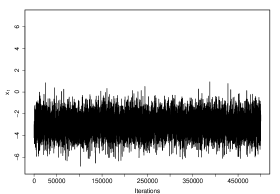

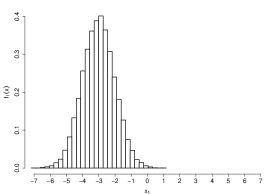

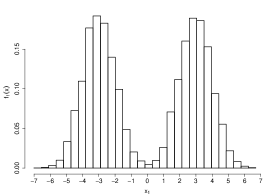

To illustrate this issue we consider the performance of the two and three component adaptive random walk samplers when the target distribution is a two component and five dimensional multivariate mixture of normals. Each component in the target has equal probability, the first component has mean vector and the second component has mean vector . Both components have identity covariance matrices. For the three component adaptive random walk we choose . The starting value is for both adaptive random walk samplers.

Figure 1 compares the results and shows that the two component adaptive random walk fails to explore the posterior distribution even after 500, 000 iterations, whereas the three component adaptive random walk can get out of the local modes.

2.2 A mixture of normals based proposal density

The proposal density of the adaptive independent Metropolis-Hastings approach of Giordani and Kohn (2008) is a mixture with four terms of the form

| (4) |

with the parameter vector for the density . The sampling scheme is run in two stages, which are described below. Throughout each stage, the parameters in the first two terms are kept fixed. The first term is an estimate of the target density and the second term is a heavy tailed version of . The third term is an estimate of the target that is updated or adapted as the simulation progresses and the fourth term is a heavy tailed version of the third term. In the first stage is a Laplace approximation to the posterior if it is readily available and works well; otherwise, is a Gaussian density constructed from a preliminary run of 1000 iterates or more of the three component adaptive random walk. Throughout, has the same component means and probabilities as , but its component covariance matrices are ten times those of . The term is a mixture of normals and is also a mixture of normals obtained by taking its component probabilities and means equal to those of , and its component covariance matrices equal to 20 times those of . The first stage begins by using and only with, for example, and , until there is a sufficiently large number of iterates to form . After that we set and . We begin with a single normal density for and as the simulation progresses we add more components up to a maximum of four according to a schedule that depends on the ratio of the number of accepted draws to the dimension of . See Appendix A.

In the second stage, is set to the value of at the end of the first stage and and are constructed as described above. The heavy-tailed densities and are included as a defensive strategy, as suggested by Hesterberg (1995), to get out of local modes and to explore the sample space of the target distribution more effectively.

It is too computationally expensive to update (and hence ) at every iteration so we update them according to a schedule that depends on the problem and the size of the parameter vector. See Appendix A.

Our article estimates the multivariate mixture of normals density for the third component using the method of Giordani and Kohn (2008) who identify the marginals that are not symmetric and estimate their joint density by a mixture of normals using k-harmonic means clustering. We also estimated the third component using stochastic approximation but without first identifying the marginals that are not symmetric. We studied the performance of both approaches to fitting a mixture of normals and found that the clustering based approach was more robust in the sense that it does not require tuning for particular data sets to perform well, whereas for the more challenging target distributions it was necessary to tune the parameters of the stochastic approximation to obtain optimal results. The results for the stochastic approximation approach are reported in Silva et al. (2008). We note that estimating a mixture of normals using the EM algorithm also does not require tuning; see McLachlan and Peel (2000), as well as Titterington (1984) for the online EM. However, the EM algorithm is more sensitive to starting values and is more prone to converge to degenerate solutions, particularly in an MCMC context where small clusters of identical observations arise naturally; see Giordani and Kohn (2008) for a discussion.

2.3 A mixture of a copula and a multivariate proposal distribution

The third proposal distribution is a mixture of a copula and a multivariate distribution. We use the copula as the major component of the mixture because it provides a flexible and fast method for estimating a multivariate density. In our applications this means that we assume that after appropriately transforming each of the parameters, the joint posterior density is multivariate . Or more accurately, such a proposal density provides a more accurate estimate of the posterior density than using a multivariate normal or multivariate proposal. The second component in the mixture is a multivariate distribution with low degrees of freedom whose purpose is to help the sampler move out of local modes and explore the parameter space more effectively.

Joe (1997) and Nelsen (2006) provide an introduction to copulas, with details of the copula given in Demarta and McNeil (2005).

Let be a -dimensional density with location , scale matrix and degrees of freedom and let be the corresponding cumulative distribution function. Let and be the probability density function and the cumulative distribution function of the th marginal, with its parameter vector. Then the density of the copula based distribution for is

| (5) |

where is determined by , . For a given sample of observations, or in our case a sequence of draws, we fit the copula by first estimating each of the marginals as a mixture of normals. For the current degrees of freedom, , of the copula, we now transform each observation to using

| (6) |

This produces a sample of dimensional observations which we use to estimate the scale matrix as the sample correlation matrix of the ’s. Given the estimates of the marginal distributions and the scale matrix , we estimate the degrees of freedom by maximizing the profile likelihood function given by (5) over a grid of values , with representing the Gaussian copula. We could use instead the grid of values in (6), but this is more expensive computationally and we have found our current procedure works well in practice.

The second component of the mixture is a multivariate distribution with its degrees of freedom fixed and small, and with its location and scale parameters estimated from the iterates using the first and second sample moments. The copula component of the mixture has a weight of 0.7 and the multivariate component a weight of 0.3.

To draw an observation from the copula, we first draw from the multivariate distribution with location 0 and scale matrix and degrees of freedom . We then use a Newton-Raphson root finding routine to obtain for a given from (6) for . The details of the computation for the copula and the schedule for updating the proposals is given in Appendix A.

Using antithetic variables in simulations often increases sampling efficiency; e.g. Rubinstein (1981). Tierney (1994) proposes using antithetic variables in Markov chain Monte Carlo simulation when the target is symmetric. We apply antithetic variables to the copula based approach which generalizes Tierney’s suggestion by allowing for nonsymmetric marginals. To the best of our knowledge, this has not been done before. The antithetic approach is implemented as follows. As above, we determine probabilistically whether to sample from the copula component or the multivariate component. If the copula component is chosen, then is generated as above and is also computed. The values and are then transformed to and respectively and are accepted or rejected one at a time using the Metropolis-Hastings method. If we decide to sample from the multivariate component to obtain , we also compute , where is the mean of the multivariate , and accept or reject each of these values one at a time using the Metropolis-Hastings method.

We note that to satisfy the conditions for convergence in Giordani and Kohn (2008) we would run the sampling scheme in two stages, with the first stage as above. In the second stage we would have a three component proposal, with the first two components the same as above. The third component would be fixed throughout the second stage and would be the second component density at the end of the first stage. The third component would have a small probability, e.g. 0.05. However, in our examples we have found it unnecessary to include such a third component as we achieve good performance without it.

3 Algorithm comparison

This section studies the five algorithms discussed in Section 2. The two component adaptive random walk metropolis (RWM) and the three component adaptive random walk Metropolis (RWM3C) are described in Section 2.1. The adaptive independent Metropolis-Hastings with a mixture of normals proposal distribution fitted by clustering (IMH-MN-CL) described in Section 2.2. The adaptive independent Metropolis-Hastings which is a mixture of a copula and a multivariate proposal, with the marginal distributions of the copula estimated by mixtures of normals that are fitted by clustering (IMH-TCT-CL). The fifth sampler is the antithetic variable version of IMH-TCT-CL, which we call IMH-TCT-CL-A. These proposals are described in Section 2.3.

Our study compares the performance of the algorithms in terms of the acceptance rate of the Metropolis-Hastings method, the inefficiency factors (IF) of the parameters, and an overall measure of effectiveness which compares the times taken by all samplers to obtain the same level of accuracy. We define the acceptance rate as the percentage of accepted values of each of the Metropolis-Hastings proposals. We define the inefficiency of the sampling scheme for a given parameter as the variance of the parameter estimate divided by its variance when the sampling scheme generates independent iterates. We estimate the inefficiency factor as

| (7) |

where is the estimated autocorrelation at lag and the truncated kernel function if and 0 otherwise (Andrews 1991). As a rule of thumb, the maximum number of lags is given by the lowest index such that with being the sample size use to compute . We define the equivalent sample size as , where , which can be interpreted as iterates of the dependent sampling scheme are equivalent to independent iterates. The acceptance rate and the inefficiency factor do not take into account the time taken by a sampler. To obtain an overall measure of the effectiveness of a sampler, we define its equivalent computing time , where is the time per iteration of the sampler and . We interpret as the time taken by the sampler to attain the same accuracy as that attained by independent draws of the same sampler. For two samplers and , is the ratio of times taken by them to achieve the same accuracy.

We note that the time per iteration for a given sampling algorithm depends to an important extent on how the algorithm is implemented, e.g. language used, whether operations are vectorized, which affects but not the acceptance rates nor the inefficiencies.

3.1 Logistic Regression

This section applies the adaptive sampling schemes to the binary logistic regression model

| (8) |

using three different priors for the vector of coefficients . The first is a non-informative multivariate normal prior,

| (9) |

The second is a normal prior for the intercept , and a double exponential, or Laplace prior, for all the other coefficients,

| (10) |

The regression coefficients are assumed to be independent a priori. We note that this is the prior implicit in the lasso (Tibshirani 1996). The prior for is , where means an inverse gamma density with shape and scale . The double exponential prior has a spike at zero and heavier tails than the normal prior. Compared to their posterior distributions under a diffuse normal prior, this prior shrinks the posterior distribution of the coefficients close to zero to values even closer to zero, while the coefficients far from zero are almost unmodified. In the adaptive sampling schemes we work with rather than as it is unconstrained.

The third prior distribution takes the prior for the intercept as and the prior for the coefficients as the two component mixture of normals,

| (11) |

with the regression coefficients assumed a priori independent. George and McCulloch (1993) suggest using this prior for Bayesian variable selection, with and small and large variances that are chosen by the user. In our article their values are given for each of the examples below. The prior for is uniform. In the adaptive sampling we work with the logit of because it is unconstrained.

Labor force participation by women

This section models the probability of labor force participation by women, , in 1975 as a function of the covariates listed in Table 1. This data set is discussed by Wooldridge (2004), p. 537 and has a sample size of 753.

| 1 if the woman is in labor force in 1975 and 0 otherwise; | |

| 1 if kids are with less than 6 years and 0 otherwise; | |

| 1 if kids are between 6 and 18 years and 0 otherwise; | |

| Age of the woman; | |

| Years of schooling; | |

| Hours worked by husband in 1975; | |

| Husband’s hourly wage in 1975; | |

| Federal marginal tax rate facing woman; | |

| Actual labor market experience; and | |

| family income () in 1975 minus wage times hour divided by 1000 | |

| (). |

We ran all the adaptive sampling schemes presented in Section 2 for all three prior distributions. Our targets are 12 dimensional (normal diffuse prior) and 13 dimensional (double exponential prior and mixture of normals prior) posterior distributions. Our starting values and initial proposal distributions for all the adaptive algorithms were obtained by fitting a generalized linear model using the function glmfit in MATLAB. We used and for the mixture of normals prior. Table 2 summarizes the posterior distributions for the three priors.

| Parameter | Normal | Double Exponential | Mixture of Normals | |||

|---|---|---|---|---|---|---|

| Mean | S. Dev. | Mean | S. Dev. | Mean | S. Dev. | |

| - | - | 0.6107 | 0.3973 | 1.3208 | 0.7118 | |

| intercept | 22.4612 | 3.1836 | 16.5521 | 3.7459 | 23.6789 | 2.8201 |

| -1.0685 | 0.2200 | -1.0885 | 0.2157 | -1.1618 | 0.2168 | |

| 0.3347 | 0.0862 | 0.2864 | 0.0884 | 0.1763 | 0.0649 | |

| -0.0688 | 0.0164 | -0.0703 | 0.0158 | -0.0790 | 0.0151 | |

| 0.1521 | 0.0492 | 0.1612 | 0.0480 | 0.1225 | 0.0424 | |

| -0.0010 | 0.0002 | -0.0009 | 0.0002 | -0.0008 | 0.0002 | |

| -0.2587 | 0.0522 | -0.2220 | 0.0530 | -0.1851 | 0.0436 | |

| -23.2281 | 3.5870 | -16.2031 | 4.3158 | -25.1363 | 3.0601 | |

| 0.7621 | 0.1584 | 0.8448 | 0.1648 | 0.1944 | 0.0584 | |

| -0.1355 | 0.0241 | -0.1074 | 0.0254 | -0.1211 | 0.0212 | |

| -0.0030 | 0.0012 | -0.0029 | 0.0012 | -0.0026 | 0.0011 | |

| -0.8276 | 0.2219 | -0.9472 | 0.2312 | -0.0419 | 0.0781 | |

Table 3 shows the acceptance rates, inefficiencies, the equivalent sample sizes and the equivalent computing times of the adaptive sampling schemes for the three prior distributions.

| Inefficiency | Equivalent sample size | ECT | ||||||||

| Algorithm | A. Rate | Min | Median | Max | Min | Median | Max | Min | Median | Max |

| Normal Prior | ||||||||||

| RWM | 16.9 | 63.149 | 66.419 | 69.542 | 144 | 151 | 158 | 1696 | 1784 | 1868 |

| RWM3C | 30.4 | 45.098 | 46.744 | 48.685 | 205 | 214 | 222 | 1219 | 1264 | 1316 |

| IMH-MN-CL | 67.1 | 1.981 | 2.188 | 2.426 | 4121 | 4571 | 5049 | 191 | 211 | 234 |

| IMH-TCT-CL | 76.5 | 1.695 | 1.761 | 1.918 | 5213 | 5680 | 5900 | 161 | 167 | 182 |

| IMH-TCT-CL-A | 79.2 | 0.749 | 0.836 | 0.938 | 10655 | 11959 | 13349 | 202 | 226 | 253 |

| Double exponential Prior | ||||||||||

| RWM | 16.7 | 68.437 | 71.198 | 75.024 | 133 | 140 | 146 | 1907 | 1984 | 2090 |

| RWM3C | 30.1 | 47.749 | 50.993 | 52.587 | 190 | 196 | 209 | 1340 | 1431 | 1476 |

| IMH-MN-CL | 66.6 | 2.080 | 2.185 | 2.415 | 4140 | 4578 | 4807 | 258 | 271 | 299 |

| IMH-TCT-CL | 76.2 | 1.753 | 1.874 | 2.614 | 3826 | 5336 | 5706 | 277 | 296 | 413 |

| IMH-TCT-CL-A | 77.7 | 1.007 | 1.182 | 1.896 | 5273 | 8460 | 9935 | 263 | 308 | 495 |

| Mixture of Normals Prior | ||||||||||

| RWM | 25.9 | 36.243 | 44.711 | 46.234 | 216 | 224 | 276 | 1230 | 1517 | 1568 |

| RWM3C | 29.7 | 49.411 | 52.163 | 79.618 | 126 | 192 | 202 | 1681 | 1774 | 2708 |

| IMH-MN-CL | 68.6 | 1.986 | 2.126 | 2.642 | 3786 | 4703 | 5036 | 204 | 218 | 271 |

| IMH-TCT-CL | 76.7 | 1.643 | 1.776 | 2.030 | 4926 | 5630 | 6085 | 352 | 381 | 435 |

| IMH-TCT-CL-A | 81.8 | 0.661 | 0.733 | 1.136 | 8800 | 13651 | 15120 | 164 | 182 | 282 |

Although the acceptance rates for the three component adaptive random walk are higher than for the two component adaptive random walk, the results are more ambiguous when comparing their inefficiencies. The inefficiencies for all the adaptive independent Metropolis-Hastings schemes are much lower than the two adaptive random walk Metropolis schemes. The copula based proposal distribution performed the best in terms of the acceptance rates and the inefficiency factors, and its antithetic version performed even better.

Home mortgage disclosure act

The home mortgage disclosure act (HMDA) data set relates to mortgage applications in Boston in 1990. It is discussed in Section 11.4 of Stock and Watson (2007) and has been analyzed by many authors, e.g. Megbolugbe and Carr (1993). The dependent variable is deny, which is 1 if a mortgage application is denied and 0 otherwise. The sample size is 2380 with the covariates listed in Table 4.

| Scaled total obligation to income ratio; | |

| 1 if African-American and 0 otherwise; | |

| Credit history of consumer payments: | |

| 1 if no slow pay, | |

| 2 if one or two slow pay accounts, | |

| 3 if more than two slow pay accounts, and | |

| 4 if insufficient credit history; | |

| Mortgage history: | |

| 1 if no late mortgage payments, | |

| 2 if no mortgage payment history, | |

| 3 if one or more late mortgage payments, and | |

| 4 if More than two late mortgage payments; | |

| 1 if there is a bankruptcy public record and 0 otherwise; | |

| 1 if a private mortgage insurance has been denied and 0 otherwise; | |

| 1 if self employed and 0 otherwise; | |

| 1 if married and 0 otherwise; | |

| 1 if number of years of schooling 12 and 0 otherwise; | |

| (loan-to-value 80%) (loan-to-value 95%); | |

| loan-to-value 95%; | |

| 1 if credit history of consumer payments is equal to 3 and 0 otherwise; | |

| 1 if credit history of consumer payments is equal to 4 and 0 otherwise; | |

| 1 if credit history of consumer payments is equal to 5 and 0 otherwise; and | |

| 1 if credit history of consumer payments is equal to 6 and 0 otherwise. |

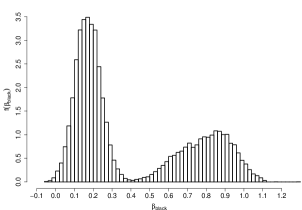

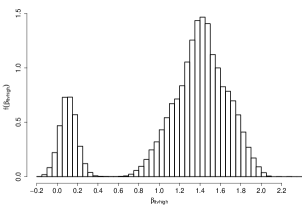

Our starting values and initial proposal distributions for all the adaptive algorithms were obtained by fitting a generalized linear model using the function glmfit in MATLAB. We used and for the mixture of normals prior. Table 5 summarizes the estimation results and Figure 2 shows the two marginals that are bimodal under the mixture of normals prior.

| Parameter | Normals | Double Exponential | Mixture of Normals | |||

|---|---|---|---|---|---|---|

| Mean | S. Dev. | Mean | S. Dev. | Mean | S. Dev. | |

| - | - | 0.1637 | 0.2890 | 0.8536 | 0.5573 | |

| intercept | -4.9153 | 0.6744 | -4.4802 | 0.6342 | -5.0159 | 0.3489 |

| 4.8068 | 0.7904 | 4.2074 | 0.7831 | 4.8814 | 0.7589 | |

| 0.6042 | 0.1797 | 0.5955 | 0.1766 | 0.4081 | 0.3190 | |

| 0.7326 | 0.2134 | 0.4498 | 0.1464 | 0.2718 | 0.0403 | |

| 0.2215 | 0.1456 | 0.2125 | 0.1428 | 0.1079 | 0.0797 | |

| 1.2814 | 0.2132 | 1.2360 | 0.2118 | 1.3572 | 0.1976 | |

| 4.7761 | 0.5888 | 4.4736 | 0.5510 | 4.6734 | 0.5538 | |

| 0.6645 | 0.2160 | 0.6388 | 0.2143 | 0.1012 | 0.0912 | |

| -0.3971 | 0.1544 | -0.3799 | 0.1520 | -0.1290 | 0.0831 | |

| -1.1721 | 0.4276 | -0.9786 | 0.4315 | -0.0507 | 0.0968 | |

| 0.4933 | 0.1616 | 0.4686 | 0.1614 | 0.1451 | 0.0906 | |

| 1.5686 | 0.3193 | 1.4515 | 0.3235 | 1.2000 | 0.5342 | |

| -0.6192 | 0.4683 | -0.1229 | 0.3454 | 0.0157 | 0.0917 | |

| -0.6872 | 0.6469 | 0.0544 | 0.4433 | 0.0556 | 0.0954 | |

| -1.7431 | 0.8103 | -0.6463 | 0.5597 | -0.0086 | 0.0906 | |

| -2.1088 | 1.0084 | -0.7534 | 0.6892 | 0.0003 | 0.0923 | |

Table 6 shows the acceptance rates, inefficiencies, the equivalent sample sizes and the equivalent computing time of the adaptive sampling schemes for the three prior distributions. Both adaptive random walk Metropolis algorithms have much higher inefficiencies than the adaptive independent Metropolis-Hastings algorithms, especially under the mixture of normals prior distribution. The copula based proposal has the highest acceptance rates and lowest inefficiencies, especially for the mixture of normals prior. The reason for this may be that this prior produces a multimodal posterior distribution.

| Inefficiency | Equivalent sample size | ECT | ||||||||

| Algorithm | A. Rate | Min | Median | Max | Min | Median | Max | Min | Median | Max |

| Normal Prior | ||||||||||

| RWM | 28.5 | 49.974 | 52.714 | 54.216 | 184 | 190 | 200 | 2872 | 3030 | 3116 |

| RWM3C | 30.0 | 59.084 | 61.101 | 63.796 | 157 | 164 | 169 | 3405 | 3521 | 3676 |

| IMH-MN-CL | 69.2 | 1.974 | 2.040 | 2.211 | 4522 | 4903 | 5067 | 302 | 312 | 338 |

| IMH-TCT-CL | 76.8 | 1.612 | 1.821 | 2.136 | 4682 | 5490 | 6205 | 332 | 375 | 439 |

| IMH-TCT-CL-A | 63.9 | 1.762 | 2.503 | 4.095 | 2442 | 3995 | 5676 | 519 | 737 | 1206 |

| Double exponential Prior | ||||||||||

| RWM | 27.5 | 53.770 | 57.625 | 60.116 | 166 | 174 | 186 | 3153 | 3379 | 3525 |

| RWM3C | 29.5 | 61.348 | 63.907 | 68.001 | 147 | 156 | 163 | 3609 | 3760 | 4001 |

| IMH-MN-CL | 63.8 | 2.244 | 2.401 | 2.968 | 3369 | 4164 | 4457 | 195 | 208 | 257 |

| IMH-TCT-CL | 65.0 | 2.266 | 2.468 | 2.743 | 3645 | 4052 | 4412 | 712 | 775 | 862 |

| IMH-TCT-CL-A | 65.1 | 1.665 | 1.865 | 2.626 | 3807 | 5361 | 6006 | 627 | 702 | 989 |

| Mixture of Normals Prior | ||||||||||

| RWM | 15.8 | 66.962 | 96.965 | 159.411 | 63 | 103 | 149 | 4309 | 6240 | 10258 |

| RWM3C | 20.1 | 91.179 | 104.422 | 159.808 | 63 | 96 | 110 | 5886 | 6741 | 10316 |

| IMH-MN-CL | 22.4 | 15.066 | 26.898 | 109.568 | 91 | 372 | 664 | 1108 | 1978 | 8057 |

| IMH-TCT-CL | 59.0 | 3.041 | 3.293 | 13.016 | 768 | 3037 | 3288 | 1520 | 1647 | 6508 |

| IMH-TCT-CL-A | 55.7 | 3.096 | 3.476 | 13.193 | 758 | 2877 | 3230 | 1934 | 2172 | 8241 |

We remark that we monitored the updates of the proposal distributions through all iterates of all algorithms using the copula based sampler and noted that most of the time the degrees of freedom was generated as 1 000, effectively giving a Gaussian copula.

3.2 Bayesian Quantile Regression

In classical quantile regression the vector of coefficients is estimated by minimizing the function

for for a given , where . We can turn this into a likelihood function based on the asymmetric Laplace distribution, i.e.

| (12) |

See for example Yu and Moyeed (2001) and references therein for a discussion of Bayesian quantile regression. In the example below, we use the same three priors for the regression parameters as in Section 3.1, an prior for and take and for the mixture of normals prior distribution.

Current population survey

We consider a data set of full-time male workers given by the U.S. current population survey of March 2000. The dependent variable is the logarithm of wage and salary income and the covariates are listed in Table 7. The sample size is 5149 observations. Similar data are analyzed by Donald, Green and Paarsch (2000). We carry out Bayesian quantile regression for this data set for . Similar analyses for and are reported in Silva et al. (2008). The target distributions in this example are 24 and 25 dimensional. Our initial proposal distributions for the adaptive independent samplers were obtained by first running the 3 component adaptive random walk for 20 000 iterations for the normal and double exponential priors and 100 000 iterations for the mixture of normals prior. In all cases we initialized the random walks using linear regression estimates. Table 8 summarizes the marginal posterior distributions of the parameter estimates.

| Age of worker in years; | |

| Square of age | |

| Education: | |

| 1 if incomplete high school and 0 otherwise; | |

| 1 if some post-secondary and 0 otherwise; | |

| 1 if completed college or university and 0 otherwise; | |

| (Omitted category is completed high school.) | |

| Coverage: | |

| 1 if covered by a union negotiated collective agreement and 0 otherwise; | |

| Employment: | |

| 1 if works in public sector and 0 otherwise; | |

| Occupation: | |

| white collar professional (e.g. managers) | |

| while collar other (e.g. clerical) | |

| (Omitted category is blue collar.) | |

| Industry: | |

| 1 if primary and 0 otherwise; | |

| 1 if transport and commn and 0 otherwise; | |

| 1 if trade and 0 otherwise; | |

| 1 if services and 0 otherwise; | |

| 1 if public admin and 0 otherwise; | |

| (Omitted category is manufacturing sector.) | |

| Location: | |

| 1 if location in metropolitan area and 0 otherwise; | |

| Region: | |

| 1 if mid-west and 0 otherwise; | |

| 1 if south and 0 otherwise; | |

| 1 if west and 0 otherwise; | |

| (Omitted category is north east.) | |

| Marital: | |

| 1 if never married and 0 otherwise; | |

| 1 if separated, divorced or widowed and 0 otherwise; | |

| (Omitted category is married.) | |

| Dependents: | |

| 1 if kids are with less than 6 years and 0 otherwise; | |

| 1 if kids are between 6 and 18 years and 0 otherwise; and | |

| Race: | |

| 1 if visible minority and 0 otherwise. |

| Parameter | Normals | Double Exponential | Mixture of Normals | |||

|---|---|---|---|---|---|---|

| Mean | S. Dev. | Mean | S. Dev. | Mean | S. Dev. | |

| - | - | -5.43902 | 0.21692 | 3.70487 | 1.28372 | |

| 0.01032 | 0.00014 | 0.01032 | 0.00014 | 0.01032 | 0.00014 | |

| intercept | 0.02686 | 0.00825 | 0.03108 | 0.00806 | 0.03299 | 0.00745 |

| 0.02286 | 0.00420 | 0.02056 | 0.00412 | 0.01956 | 0.00377 | |

| -0.00205 | 0.00052 | -0.00176 | 0.00051 | -0.00164 | 0.00047 | |

| -0.01448 | 0.00196 | -0.01437 | 0.00188 | -0.01435 | 0.00186 | |

| 0.00599 | 0.00161 | 0.00571 | 0.00158 | 0.00582 | 0.00155 | |

| 0.01696 | 0.00191 | 0.01657 | 0.00190 | 0.01675 | 0.00185 | |

| 0.01478 | 0.00199 | 0.01420 | 0.00207 | 0.01424 | 0.00197 | |

| -0.00301 | 0.00291 | -0.00168 | 0.00259 | -0.00208 | 0.00270 | |

| 0.02694 | 0.00204 | 0.02640 | 0.00198 | 0.02586 | 0.00196 | |

| 0.00268 | 0.00166 | 0.00215 | 0.00158 | 0.00200 | 0.00158 | |

| -0.00835 | 0.00206 | -0.00764 | 0.00199 | -0.00767 | 0.00198 | |

| -0.00216 | 0.00229 | -0.00138 | 0.00211 | -0.00135 | 0.00222 | |

| -0.01902 | 0.00205 | -0.01803 | 0.00198 | -0.01780 | 0.00195 | |

| -0.01753 | 0.00199 | -0.01677 | 0.00192 | -0.01647 | 0.00188 | |

| 0.00711 | 0.00420 | 0.00631 | 0.00385 | 0.00715 | 0.00382 | |

| 0.00767 | 0.00134 | 0.00734 | 0.00134 | 0.00748 | 0.00132 | |

| 0.00442 | 0.00194 | 0.00387 | 0.00188 | 0.00412 | 0.00191 | |

| -0.00102 | 0.00167 | -0.00126 | 0.00157 | -0.00119 | 0.00163 | |

| 0.00270 | 0.00197 | 0.00208 | 0.00179 | 0.00226 | 0.00187 | |

| -0.00496 | 0.00168 | -0.00475 | 0.00167 | -0.00508 | 0.00165 | |

| -0.00733 | 0.00216 | -0.00661 | 0.00217 | -0.00687 | 0.00212 | |

| -0.00234 | 0.00124 | -0.00207 | 0.00117 | -0.00233 | 0.00120 | |

| 0.00157 | 0.00069 | 0.00154 | 0.00067 | 0.00163 | 0.00067 | |

| -0.00865 | 0.00218 | -0.00821 | 0.00214 | -0.00842 | 0.00208 | |

Table 9 shows the acceptance rates, inefficiencies, the equivalent sample sizes and the equivalent computing times of the adaptive sampling schemes for the three prior distributions. The adaptive independent Metropolis-Hastings algorithms have lower inefficiencies than the adaptive random walk Metropolis algorithms, and the copula based proposals have in general the highest acceptance rates and lowest inefficiencies.

| Inefficiency | Equivalent sample size | Timing | ||||||||

| Algorithm | A. Rate | Min | Median | Max | Min | Median | Max | Min | Median | Max |

| Normal Prior | ||||||||||

| RWM | 18.0 | 93.934 | 99.926 | 102.211 | 98 | 100 | 106 | 2757 | 2933 | 3000 |

| RWM3C | 25.2 | 88.069 | 90.182 | 92.733 | 108 | 111 | 114 | 2598 | 2661 | 2736 |

| IMH-MN-CL | 47.3 | 3.855 | 4.321 | 4.957 | 2017 | 2315 | 2594 | 128 | 143 | 164 |

| IMH-TCT-CL | 54.2 | 3.353 | 3.609 | 4.049 | 2470 | 2770 | 2982 | 849 | 914 | 1025 |

| IMH-TCT-CL-A | 51.7 | 3.125 | 3.642 | 4.376 | 2285 | 2746 | 3200 | 889 | 1036 | 1245 |

| Double exponential Prior | ||||||||||

| RWM | 15.5 | 102.917 | 106.161 | 108.036 | 93 | 94 | 97 | 3551 | 3662 | 3727 |

| RWM3C | 22.4 | 93.033 | 95.986 | 98.044 | 102 | 104 | 107 | 3227 | 3329 | 3401 |

| IMH-MN-CL | 41.6 | 4.971 | 5.452 | 16.263 | 615 | 1834 | 2012 | 188 | 206 | 614 |

| IMH-TCT-CL | 47.8 | 4.273 | 4.568 | 4.993 | 2003 | 2189 | 2340 | 1452 | 1552 | 1697 |

| IMH-TCT-CL-A | 46.3 | 4.166 | 4.623 | 5.859 | 1707 | 2163 | 2401 | 1732 | 1923 | 2437 |

| Mixture of Normals Prior | ||||||||||

| RWM | 22.8 | 81.008 | 83.060 | 92.968 | 108 | 120 | 123 | 3006 | 3083 | 3450 |

| RWM3C | 23.2 | 84.279 | 86.135 | 92.548 | 108 | 116 | 119 | 3157 | 3226 | 3466 |

| IMH-MN-CL | 46.0 | 4.227 | 4.688 | 8.217 | 1217 | 2133 | 2366 | 205 | 227 | 398 |

| IMH-TCT-CL | 54.4 | 3.507 | 3.722 | 6.412 | 1560 | 2687 | 2852 | 2066 | 2193 | 3777 |

| IMH-TCT-CL-A | 49.7 | 3.938 | 4.365 | 9.977 | 1002 | 2291 | 2540 | 4939 | 5475 | 12514 |

4 Binary random effects model

This section considers adaptive sampling in a binary random effects model where the random effects are integrated out using importance sampling. However, the same ideas can be applied to other random effects models.

Suppose there are groups with observations in the th group, such that the probability of the th binary response is given by the probit model,

| (13) |

and is the standard normal cumulative distribution function. Let be the parameter vector, are the vectors of observations on the th group, is the vector of all the observations and is the vector of all the covariates. Then

| (14) |

We form proposals for the posterior with the random effects integrated out because in many applications there are too many random effects to include in the adaptation. We use importance sampling to integrate out the random effects with the importance density based on previous iterates. Let and be estimates of the posterior mean and variance of . We use the importance density to efficiently integrate out in (14), with , using

| (15) |

where the are generated from . We obtain by first writing , so that

| (16) | ||||

| (17) |

where the are iterates from the adaptive sampling and is constructed by the right side of (4). The estimate is obtained similarly and is then computed as .

We update the importance density after every accepted values of the adaptive sampling scheme, with given in appendix A

Pap smear data

We applied the probit random effects model (13) to data collected in a discrete choice experiment designed to study factors that may determine whether a woman chooses to have a Pap smear test to detect cervical cancer. The study is described by Fiebig and Hall (2005) and is based on Australian women, where each woman was presented with different scenarios and for each scenario asked whether she would choose to have a Pap smear test. Thus, there are 32 repeated binary observations for each woman. Table 10 lists the covariates in the study.

| 1 if the GP is known to the patient and 0 otherwise; | |

| 1 if the GP is male and 0 otherwise; | |

| 1 if the patient is due or overdue for a Pap test and 0 otherwise; and | |

| 1 if GP recommends that the patient has a Pap test and 0 otherwise. | |

| Cost of the Pap test in AU$ (2 levels). |

We fitted the binary random effects model with 7 parameters and 79 random effects to the data with

an prior for . For the double exponential prior for , the prior for is . For the mixture of normals prior, we set and .

and the prior for is uniform on (0,1). In the adaptive sampling scheme we generated because it was unconstrained.

The initial values and proposal distributions for the adaptive independent Metropolis-Hastings algorithms were obtained by running the 3 component adaptive random walk for 2 000 iterations.

To initialize all the adaptive random walk algorithms we first used the MATLAB function

glmfit to estimate the regression coefficients and their standard

errors with the random effects set identically to zero. To integrate out the random effects in the

adaptive random walk proposals we began with the proposal importance density , with initially.

Table 11 summarizes the posterior distributions of the parameters.

| Parameter | Normals | Double Exponential | Mixture of Normals | |||

|---|---|---|---|---|---|---|

| Mean | S. Dev. | Mean | S. Dev. | Mean | S. Dev. | |

| - | - | -0.5683 | 0.4488 | -1.0691 | 0.8988 | |

| 0.5792 | 0.2081 | 0.5598 | 0.2151 | 0.5680 | 0.1976 | |

| constant | 0.2914 | 0.1797 | 0.2646 | 0.1865 | 0.2808 | 0.1833 |

| -0.3052 | 0.0633 | -0.2882 | 0.0658 | -0.2846 | 0.0934 | |

| 0.6582 | 0.0656 | 0.6483 | 0.0677 | 0.6591 | 0.0690 | |

| -1.1794 | 0.0750 | -1.1688 | 0.0807 | -1.1769 | 0.0773 | |

| -0.4978 | 0.0737 | -0.4772 | 0.0739 | -0.4941 | 0.0725 | |

| 0.0091 | 0.0028 | 0.0091 | 0.0030 | 0.0085 | 0.0028 | |

Table 12 shows the acceptance rates, inefficiencies, equivalent sample sizes, and equivalent computing times for each algorithm. The copula based sampling schemes have the highest acceptance rates and the smallest inefficiency factors, with the antithetic proposal being the best for the normal and double exponential priors, where the acceptance rates are at least 70%.

| Inefficiency | Equivalent sample size | ECT | ||||||||

| Algorithm | A. Rate | Min | Median | Max | Min | Median | Max | Min | Median | Max |

| Normal Prior | ||||||||||

| RWM | 28.6 | 18.210 | 23.039 | 32.306 | 310 | 434 | 549 | 618517 | 782509 | 1097268 |

| RWM3C | 28.8 | 22.623 | 24.766 | 33.667 | 297 | 404 | 442 | 750806 | 821899 | 1117299 |

| IMH-MN-CL | 62.1 | 2.356 | 2.590 | 2.999 | 3334 | 3862 | 4244 | 77641 | 85324 | 98824 |

| IMH-TCT-CL | 71.6 | 1.803 | 2.086 | 2.226 | 4493 | 4793 | 5548 | 59834 | 69253 | 73879 |

| IMH-TCT-CL-A | 70.9 | 0.968 | 1.453 | 1.893 | 5282 | 6884 | 10329 | 32002 | 48017 | 62580 |

| Double exponential Prior | ||||||||||

| RWM | 26.8 | 25.337 | 30.855 | 39.939 | 250 | 325 | 395 | 833790 | 1015358 | 1314306 |

| RWM3C | 26.8 | 24.894 | 30.907 | 36.229 | 276 | 324 | 402 | 821509 | 1019936 | 1195573 |

| IMH-MN-CL | 57.9 | 2.656 | 2.860 | 3.542 | 2823 | 3502 | 3765 | 86895 | 93583 | 115885 |

| IMH-TCT-CL | 71.8 | 1.922 | 2.151 | 2.514 | 3978 | 4650 | 5202 | 63124 | 70627 | 82551 |

| IMH-TCT-CL-A | 70.7 | 0.974 | 1.526 | 2.209 | 4527 | 6555 | 10272 | 32187 | 50462 | 73036 |

| Mixture of Normals Prior | ||||||||||

| RWM | 25.4 | 27.979 | 32.678 | 90.248 | 111 | 307 | 357 | 1014949 | 1185408 | 3273811 |

| RWM3C | 24.2 | 26.739 | 34.183 | 52.536 | 190 | 293 | 374 | 1004583 | 1284255 | 1973767 |

| IMH-MN-CL | 58.4 | 2.369 | 3.058 | 3.720 | 2688 | 3271 | 4221 | 82817 | 106888 | 130032 |

| IMH-TCT-CL | 71.5 | 2.011 | 2.244 | 3.364 | 2973 | 4462 | 4971 | 73396 | 81889 | 122746 |

| IMH-TCT-CL-A | 62.2 | 2.365 | 2.635 | 6.221 | 1607 | 3794 | 4229 | 88108 | 98204 | 231813 |

5 Summary

Our article proposes a new copula based adaptive sampling scheme and a generalization of the two component adaptive random walk designed to explore the target space more efficiently than the proposal of Roberts and Rosenthal (2006). We studied the performance of these sampling schemes as well as the adaptive independent Metropolis-Hastings sampling scheme proposed by Giordani and Kohn (2008) which is based on a mixture of normals. All the sampling schemes performed reliably on the examples studied in the article, but we found that the adaptive independent Metropolis-Hastings schemes had inefficiency factors that were often much lower and acceptance rates that were much higher than the adaptive random walk schemes. The copula based adaptive scheme often had the smallest inefficiency factors and highest acceptance rates. For acceptance rates over 70% the antithetic version of the copula based approach was the most efficient. Our results suggest that the copula based proposal provides an attractive approach to adaptive sampling, especially for higher dimensions. However, the mixture of normals approach of Giordani and Kohn (2008) also performed well and is useful for complicated and possibly multimodal posterior distributions.

Acknowledgment

The research of Robert Kohn, Ralph Silva and Xiuyan Mun was partially supported by an ARC Discovery Grant DP0667069. We thank Professor Garry Barret for the CPS data and Professor Denzil Fiebig for the Pap smear data.

Appendix A Details of the Simulation

All the computations were done on Intel Core 2 Quad 2.6 Ghz processors, with 4GB RAM (800Mhz) on a GNU/Linux platform using MATLAB 2007b. However, in the TCT algorithm we computed the univariate cumulative distribution functions and inverse cumulative distribution functions of the , normal and mixture of normals distributions using MATLAB mex files based on the corresponding MATLAB code. In addition, to speed up the computation, we tested each marginal for normality using the Jarque-Bera test at the 5% level. If normality was not rejected then we fitted a normal density to the marginal. Otherwise, we estimated the marginal density by a mixture of normals.

In Stage 1 of the adaptive sampling schemes IMH-MN-CL and IMH-MN-SA that use a multivariate mixture of normals, the number of components () used in the third term of the mixture (4) is determined by the dimension of the parameter vector () and the number of accepted draws () to that stage of the simulation. In particular, if , if , if and if .

We now give details of the number of iterations, burn-in and updating schedules for all the adaptive independent Metropolis-Hastings schemes in the paper. In addition, we update the proposal in Stage 1 if in 100 successive iterations the acceptance rate is lower than 0.01.

Logistic regression, HMDA data

-

•

Normal prior: end of first stage = 5 000; burn-in = 75 000; number of iterations: 100 000; updates = [50, 100, 150, 200, 300, 500, 700, 1000, 2000, 5000, 10000, 20000, 30000, 50000, 75000].

-

•

Double exponential prior: end of first stage = 5 000; burn-in = 100 000; number of iterations: 150 000; updates = [50, 100, 150, 200, 300, 500, 700, 1000, 2000, 5000, 10000, 20000, 30000, 50000, 75000, 100000].

-

•

Mixture of normals prior: end of first stage = 100 000; burn-in = 300 000; number of iterations: 400 000; updates = [100, 150, 200, 300, 500, 700, 1000, 2000, 3000, 5000, 7500, 10000, 15000, 20000, 30000, 50000, 75000, 100000, 125000, 150000, 175000, 200000, 225000, 250000, 300000].

Bayesian quantile regression, CPS data.

-

•

Normal and double exponential priors, quantiles 0.1, 0.5 and 0.9: end of first stage = 3 000; burn-in = 150 000; number of iterations: 200 000; updates = [100, 150, 200, 300, 500, 700, 1000, 2000, 3000, 5000, 7500, 10000, 15000, 20000, 30000, 50000, 75000, 100000, 150000].

-

•

Mixture of normals prior, quantiles 0.1, 0.5 and 0.9: end of first stage = 200 000; burn-in = 400 000; number of iterations: 500 000; updates = [100, 150, 200, 300, 500, 700, 1000, 2000, 3000, 5000, 7500, 10000, 15000, 20000, 30000, 50000, 75000, 100000, 125000, 150000, 175000, 200000, 225000, 250000, 275000, 300000, 325000, 350000, 375000, 400000].

Probit random effects model, Pap smear data. For all three priors, end of first stage = 5 000; burn-in = 10 000; number of iterations: 20 000; updates = [20, 50, 100, 150, 200, 300, 400, 500, 600, 700, 800, 900, 1000, 1100, 1200, 1300, 1400, 1500, 2000, 2500, 3000, 3500, 4000, 4500, 5000, 6000, 7000, 8000, 9000, 10000, 12000, 15000].

In this example the importance sampling density is updated every iterations.

We now give the details of the sampling for both adaptive random walk Metropolis algorithms. For the HMDA data the number of burn-in iterations was 300 000 and the total number of iterations was 500 000 for all three priors. The corresponding numbers for the CPS data with normal and double exponential priors are 500 000 and 1000 000, and for the mixture of normals prior 1000 000 and 1500 000. The corresponding numbers for the Pap smear data are 30 000 and 50 000.

References

- Andrews (1991) Andrews, D. W. K. (1991). Heteroskedasticity and autocorrelation consistent covariance matrix estimation. Econometrica, 59(3), 817-858.

- Andrieu and Moulines (2006) Andrieu, C. and Moulines, D. (2006). On the ergodicity properties of some adaptive MCMC algorithms. Annals of Applied Probability, 16, 1462-1505.

- Andrieu and Robert (2001) Andrieu, C. and Robert, C. P. (2001). Controlled MCMC for optimal sampling. Technical Report, cahier du Ceremade 0125, Université Paris-Dauphine, 2001.

- Andrieu, Moulines, and Doucet (2005) Andrieu, C., Moulines, D., and Doucet, A. (2005). Stability of stochastic approximation under verifiable conditions. SICON, 44, 283-312.

- Andrieu and Moulines (2006) Andrieu, C. and Moulines, D. (2006), On the ergodicity properties of some adaptive MCMC algorithms. Annals of Applied Probability, 16(3), 1462-1505.

- Atchadé and Rosenthal (2005) Atchadé, Y. and Rosenthal, J. (2005). On adaptive Markov chain Monte Carlo algorithms. Bernoulli, 11, 815-828.

- Demarta and McNeil (2005) Demarta, S. and McNeil, A. (2005). The t copula and related copulas. International Statistical Review, 9, 111-129.

- Donald, Green and Paarsch (2000) Donald, S.G., Green, D.A. and Paarsch, H.J. (2000). Differences in wage distributions between Canada and the United States: An application of a flexible estimator of distribution functions in the presence of covariates. Review of Economic Studies, 67(4), 609-633.

- Fiebig and Hall (2005) Fiebig, D. G., and Hall, J. (2005). Discrete choice experiments in the analysis of health policy in Quantitative Tool for Microeconomic Policy Analysis, 119-136.

- Gåsemyr (2003) Gåsemyr, J. (2003). On an adaptive version of the Metropolis-Hastings algorithm with independent proposal distribution. Scandinavian Journal of Statistics, 30, 159-173.

- George and McCulloch (1993) George, E. I. and McCulloch, R. E. (1993). Variable selection via Gibbs sampling. Journal of the American Statistical Association, 88, 881-889.

- Giordani and Kohn (2008) Giordani, P. and Kohn, R. (2008). Adaptive Independent Metropolis-Hastings by Fast Estimation of Mixture of Normals. Prepint. http://arxiv.org/PS_cache/arxiv/pdf/0801/0801.1864v1.pdf

- Giordani et al. (2008) Giordani, P., Kohn, R. and Mun, X. (2008). Flexible multivariate density estimation with marginal adaptation. Prepint.

- Haario et al. (2001) Haario, H., Saksman, E. and Tamminen, J. (2001). An adaptive Metropolis algorithm. Bernoulli, 7, 223-242.

- Hesterberg (1995) Hesterberg, T. C. (1995). Weighted average importance sampling and defensive mixture distributions. Technometrics, 37(2), 185-194.

- Holden (1998) Holden, L. (1998). Adaptive chains. Technical Report, Norwegian Computing Center. http://citeseer.ist.psu.edu/holden98adaptive.html

- Joe (1997) Joe, H. (1997). Multivariate Models and Dependence Concepts. London: Chapman & Hall/CRC.

- McLachlan and Peel (2000) McLachlan, G. and Peel, D. (2000). Finite Mixture Models. John Wiley and Sons, New York.

- Megbolugbe and Carr (1993) Megbolugbe, I. and Carr, J. (1993). Federal Reserve Bank of Boston study on Mortgage lending revisited. Journal of Housing Research, 4(2), 277-314.

- Nelsen (2006) Nelsen, R. B. (2006). An Introduction to Copulas, 2nd edn. New York: Springer-Verlag.

- Roberts et al. (1997) Roberts, G. O., Gelman, A. and Gilks, W. R. (1997). Weak convergence and optimal scaling of random walk Metropolis algorithms. Annals of Applied Probability, 7, 110-120.

- Roberts and Rosenthal (2006) Roberts, G. O. and Rosenthal, J. S. (2006). Examples of adaptive MCMC. To appear in Journal of Computational and Graphical Statistics. http://probability.ca/jeff/ftpdir/adaptex.pdf

- Roberts and Rosenthal (2007) Roberts, G. O. and Rosenthal, J. S. (2007). Coupling and ergodicity of adaptive MCMC. Journal of Applied Probability, 44, 458-475.

- Rubinstein (1981) Rubinstein. Y. (2003). Simulation and the Monte Carlo Method. New York: Wiley.

- Silva et al. (2008) Silva, R., Kohn, R., Giordani, P. and Mun, X. (2008) A comparison of adaptive sampling schemes. Prepint.

- Stock and Watson (2007) Stock, J.H. and Watson, M.W. (2007). Introduction to Econometrics, 2nd edition. Pearson Education, New York.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society, Series B 58(1), 267-288.

- Tierney (1994) Tierney, L. (1994). Markov Chains for Exploring Posterior Distributions. Annals of Statistics 22(1), 1701-1728.

- Titterington (1984) Titterington, D. M. (1984). Recursive Parameter Estimation Using Incomplete Data. Journal of the Royal Statistical Society, Series B 46, 257-267.

- Wooldridge (2004) Wooldridge, J. M. (2004). Introductory Econometrics: A Modern Approach South-Weestern College Publishing.

- Yu and Moyeed (2001) Yu, K. and Moyeed, R. A. (2001). Bayesian quantile regression. Statistics and Probability Letters, 54, 437-447.