Generalized Pólya urns via stochastic approximation

Abstract.

We collect, survey and develop methods of (one-dimensional)

stochastic approximation in a framework

that seems suitable to handle fairly broad generalizations of Pólya urns.

To show the applicability of the results we determine the limiting fraction of balls in an urn with balls of two colors. We consider two models generalizing the Pólya urn, in the first one ball is drawn and replaced with balls of (possibly) both colors according to which color was drawn. In the second, two balls are drawn simultaneously and replaced along with balls of (possibly) both colors according to what combination of colors were drawn.

Key words and phrases:

Stochastic approximation, unstable equilibrium, stable equilibrium, touchpoint, Generalized Pólya urns2000 Mathematics Subject Classification:

60G99, 62L201. Introduction

1.1. Urns

The urn is a common tool in probability theory and statistics and no student thereof can avoid it. Imagine an urn with white and black balls. At a beginners level, urns provide examples of how to calculate probabilities, e.g. the probability of drawing a white ball is the number of white balls divided by the total number of balls, i.e. . If we sample more than one ball, say balls, from the urn and count the number of white ball we get examples of the binomial distribution (with parameters and ) and hypergeometric distributions (with parameters and , depending on whether we sample with or without replacement. These distributions in turn are very important in statistical theory as they are the key to understanding properties of surveys, e.g. voter polls, such as margins of error.

More aspects of probability theory can be illustrated via urns. Suppose we draw two balls without replacement. The question “what is the probability that the second ball is white?” may introduce the concept of conditional probabilities, as the answer depends on the knowledge we have (or lack) regarding the outcome of the first draw. Urns are so useful that it is hard to imagine an introductory text on probability and statistics not ever mentioning urns of any kind. Any reader with a general interest in urns may consult [JK77].

In 1923 Eggenberger and Pólya introduced a new urn model in [EP23], now commonly referred to as a Pólya urn. An urn has one white and one black ball. We sample one ball and replace it along with one additional ball of the same color, and repeat this procedure. It was thought of as a simple model for a contagious disease. The first draw might correspond to a doctor examining the very first patient of the day. She then has a risk of being infected. Now, the essence of a contagious disease is that the more people have it, the more likely you are to get it, and vice versa. This is now reflected in the model in the following way. Say white ball means “infected”. After we draw a white ball we replace at along with one additional white ball. Hence, the probability of drawing a white ball next time has risen to . It basically means that the more infected patients the doctor gets, the more likely it is that there are yet more to come. Of course, the actual numbers in this example is by no means meant to be “realistic”, it is rather a qualitative model.

We can, however, play with the parameters of the model to better fit some specific situation if needed. First, the initial composition of the urn need not be 1 of each color. A rare disease might correspond to black balls and only white. Also, some diseases are more contagious than others. We could incorporate this by stating that we should not add one additional ball, but several, of the same color as the one drawn, corresponding to a faster spread of the disease.

Any reader interested in Pólya urns and generalizations thereof can start with [Mah08].

Our own interest in Pólya-like urn models comes from a similar situation as described above but rather than modelling infectious diseases, it can model how something is learned, e.g. a “brain” trying to learn what to do in a specific situation. Assume for simplicity that there are only two possible ways to act, act 1 and act 2, and that act 1 is the correct way to handle the situation and, as such, leads to a reward of some kind. Act 2 is wrong and has no benefit for our brain. However, at first it is not known to our brain which act is correct (if any). It must somehow learn this by trial and error. A very simple urn model describing how this brain could work is the following. To model an initial state of ignorance, there is one white ball (meaning “do act 1”) and one black ball (meaning “do act 2”) so that the first time it just picks one ball (act) randomly. Then, to model reinforcement learning, there is a rule that if an act is deemed successful, more balls of the color corresponding to the act just performed are added to the urn. In this case; if a white ball is drawn, add, say, one additional white ball and if a black ball is drawn replace it but add no more balls. Now, every time our brain performs the right act it becomes increasingly likely that it will do so again.

As with the previous model, the interest is mainly qualitative. One should not expect that any brain works exactly like an urn. However, it captures some of the dynamics of what one can think of as learning; one tends to be more likely to do things that have proved successful in the past.

Again, we can fine tune the parameters. More colors can mean more ways to act, different reinforcement rules between colors can specify how much benefit the brain gets from the different acts, and so on.

More specifically, it was questions relating to the so called “signaling problems” (communicated by Persi Diaconis and Brian Skyrms) that spawned the authors interest in these matters. These refer to the situation where two (or more) agents try to acquire a common language simultaneously via urns. Recently, one of these problems was solved in [APSV08] which also contains a more thorough description of the problem.

This is some of the motivation behind studying urns evolving along the lines of “draw one or several balls and add more balls according to some prescribed rule depending on the colors of the drawn balls”. It is also the motivation for only looking at the fraction of balls, as these dictate the probabilities of “acting correctly” in models of learning.

1.2. Stochastic approximation algorithms

A stochastic approximation algorithm is usually defined as an -valued stochastic process adapted to a filtration such that

| (1.1) |

holds, where the decreasing “steplengths” satisfy and . The random variables can be considered stochastic or deterministic but in either case it is usually assumed that is a martingale difference sequence, i.e.

| (1.2) |

The origin of this subject is [RM51], in which Robbins and Monro considered the following one-dimensional problem; suppose that given an input to some system in which we get as output, where is an unknown function and only observable through white noise. What we really observe is thus , for some random variable with . We want to find the input so that for some prescribed . For simplicity we might assume that is nondecreasing and that has a unique solution .

A candidate algorithm for finding a sequence that converges (in some sense) to is to start with some initial input . Given a value , with , create the next element by

where is the noise associated with the ’th observation. The algorithm works on an intuitive level since whenever then, on average, takes a step in the direction of .

This describes a stochastic approximation algorithm with drift function and steplengths . Of course, there is nothing in the formulation of the problem that demands us to set the steplengths to . To demand is natural since this basically means that the algorithm can wander arbitrarily far, thus hopefully finding what it is looking for, and not converging in a trivial manner.

Next, since

the requirement makes bounded (under additional assumptions on the error terms and ).

In the multidimensional case the heuristics behind the algorithm (1.1) is that it constitutes a discrete time version of the ordinary differential equation

| (1.3) |

subject to “noise”. If the noise vanishes for large it seems plausible that the interpolation of should estimate some trajectory of a solution of (1.3), an idea made precise in [Ben99], where more references may be found. An overview may also be found in [Pem07]. We are however only concerned with the one-dimensional case.

Any reader interested in other aspects of stochastic approximation and applications may find [Bor08] useful.

1.3. How they fit

Stochastic approximation is very well suited for urn models with reinforcements such as the classical Pólya urn and generalizations thereof. If a ball is drawn from an urn and (a bounded number of) balls are added according to some reinforcement scheme, the difference of the proportion of balls before and after is approximately some function of the proportion times .

As an example, consider the so called Friedman’s urn starting with one ball each of two colors where balls of the same color and balls of the other color are added along with the ball drawn. The proportion of either color then satisfies

with the drift function and where “noise” is a martingale difference sequence. This resembles the situation considered by Robbins and Monro and, as the drift always points towards , it seems intuitive that this is the point of convergence of (in some sense). That this is so will follow from Theorem 1 below. This is “easy” since 1/2 is the unique solution of .

In other urn models may have several roots. There are known results that deal with multiple zeros, although often under the property (1.2). Urn schemes where the total number of balls added each time is not constant tend to lose this property. We will generalize existing results under an assumption slightly weaker than (1.2) and apply the results to generalized Pólya urns.

1.4. A generalized Pólya urn considered as a

stochastic approximation algorithm

First, we will show more precisely how stochastic approximation algorithms fit urn schemes by presenting an application which will be studied in more detail below. Consider an urn with balls of two colors, white and black say. Let and denote the number of balls of each color, white and black respectively, after the ’th draw and consider the initial values and to be fixed. After each draw we notice the color and replace it along with additional balls according to the replacement matrix

| WB | |||

so that, e.g. a white ball is replaced along with additional white and additional black balls. We demand that are nonnegative numbers.

This model is by no means new, chapter 3 of [Mah08] gives a historical overview. Setting , and gives the classical Pólya urn described in the introduction.

We let and denote the indicators of getting a white and black ball in draw , respectively. We set and . Recursively, and evolve as

and hence, with ,

Let denote the history of the process up to time , i.e. the -algebra . We will define

where

In the form of a stochastic approximation algorithm we can write

where and .

Now, is mean-zero “noise” but if then in general . However, as will be shown later, , and (usually) grows like , so this conditional expectation is vanishing fast.

2. The method of stochastic approximation

We will apply the stochastic approximation machinery to fractions and thus limit ourselves to processes in . This naturally restricts the noise and the function to be bounded.

2.1. Definition

Stochastic variables are throughout assumed to be defined on a probability space , although we will find no need to make any reference to the underlying measurable space . We will also consider a filtration to be given.

To simplify notation, let and denote the conditional expectation and probability, respectively, with respect to .

Definition 1.

A stochastic approximation algorithm is a

stochastic process taking values in , adapted

to the filtration , that satisfies

| (2.1) |

where and the following conditions hold a.s.

-

(i)

,

-

(ii)

,

-

(iii)

, and

-

(iv)

,

where the constants are positive real numbers. For future reference, set .

Remark 1.

There is no consensus in the scientific litterature as to exactly what constitutes a stochastic approximation algorithm. The main characteristic is that a relation of type (2.1) holds, although the range, measurability etc. of the ingredients and may differ. In this section we state results concerning ”the” process which throughout is understood to be a stochastic approximation algorithm according to our definition.

Remark 2.

The condition (iv) could, in view of condition (i), equally well have been formulated as , for some positive constant . The formulation above arises naturally for the applications toward the end of this paper.

Condition (iv) replaces the more common requirement (1.2), so that does not necessarily have conditional expectation 0, but this expectation is tending to zero quickly. In what follows, we verify that some results known to be true for condition (1.2) carry over to the present situation, as well as present some new results.

2.2. Limit points

In this section we establish that the accumulation points of the process are a subset of the zeros of , for continuous . This property is well known and the ideas for the proofs of Lemma 2 and Lemma 4 are from [Pem07]. Moreover, Theorem 1 gives an existence result for the limit of the process .

Let so that we may write increments of the process as

Lemma 1.

converges almost surely.

Proof.

Set and and define the martingale . Then

so that is an -martingale and thus convergent. Next, since

we must also have that converges a.s. ∎

Definition 2.

Let

be the set of accumulation points of .

Lemma 2.

Suppose that (or ), for some , whenever . Then

and either or .

Proof.

The proof follows that of Lemma 2.6 of [Pem07].

Let and let be the smallest distance from to a point outside . Let be a (random) number large enough so that implies

which by Lemma 1 is possible a.s. due to the a.s. convergence of . Then we have for any

so that the process after cannot immediately go from a point to the left of to a point on the right of . Also, if , and then

The last step shows that after the process cannot increase by more than while inside , hence cannot escape out to the right. Moreover, since a.s., we must have for some .

Now, once the process is below it will never reach above in one step. Once inside it will never increase by more than . Hence, it will never again reach above . Obviously, we a.s. cannot have both and .

The first results follows from choosing , such that

, so that

The second results follows by an analogous calculation, yielding

and the observation that since we thus must have or , we must in fact have either a.s.

since no accumulation points exist in by the first result.

The case where on is analogous. ∎

Next, we introduce the concept of attainability that we need now and again to rule out trivialities.

Definition 3.

Call a subset attainable if for every fixed there exists an such that

Any ”reasonable” stochastic approximation algorithm on should have and , otherwise it seems that the drift could push the processes out of . The notion of attainability gives a sufficient condition to ensure this.

Lemma 3.

Assume that the drift function is continuous at the boundary points and . If all neighborhoods of the origin are attainable, then . Similarly, if all neighborhoods of are attainable, then .

Lemma 4.

Suppose is continuous and let the zeros of . Then

Proof.

The continuity of makes the sets

open. Hence, each is a countable union of open intervals, each on which is or and hence where no accumulation points may exist.

The only ”loose end” here is the boundary. Suppose e.g. that close to zero (but a priori not at zero). Then it seems that the process might be pushed down to zero (or beyond) even though . This is however ruled out by Lemma 3, since if neighborhoods of the origin are attainable then and if they are not, then the process eventually is bounded away from the origin. Similarly we can not have close to and attainability of this boundary point simultaneously, unless .

It is clear that if close to the origin then the process will eventually be bounded away from there (and similarly if close to then the process will be bounded away from ). ∎

Theorem 1.

If is continuous then exists a.s. and is in .

Proof.

If does not exist, we can find two different rational numbers in the open interval .

Let be two arbitrary different rational numbers. If we can show that

the existence of the limit will be established and the claim of the theorem will follow from Lemma 4.

To do this we need to distinguish between whether or not and are in the same connected component of .

Case 1: and are in not in the same connected component of .

Since is closed and continuous, there must exist such that

is non-zero and of the same sign for all . By Lemma 2

it is impossible to have and .

Case 2: and are in the same connected component of .

Assume that and fix an arbitrary in such

a way that . We aim to show

that .

Recall the notation . We know from Lemma 1 that converges a.s., so for some stochastic , we have that implies . By assumption there is some stochastic such that .

2.3. Categorizing equilibrium points

Any point is called an equilibrium point, or zero, of . In this paper we shall use the following terminology:

-

•

A point is called unstable if there exists a neighborhood of such that whenever .

This means that when is just above and when is just below , hence the drift is locally pushing the process away from (or not pushing at all).

If when we call strictly unstable. If is differentiable then is sufficient to determine that is strictly unstable.

-

•

A point will be called stable if there exists a neighborhood of such that whenever . If is differentiable then is sufficient to determine that is stable.

Locally, the drift pushes the process towards from both directions.

-

•

A point is called a touchpoint if there exists a neighborhood of such that either for all or for all . If is twice differentiable then and is sufficient to determine that is a touchpoint.

A touchpoint may be thought of as having one stable and one strictly unstable side. Note that our definition does not allow touchpoints on the boundary.

2.4. Nonconvergence

In this section we narrow down the set of limit points of the process by excluding certain unstable points.

2.4.1. Unstable points with non-vanishing error terms

Here we exclude the unstable zeros of as possible limit points, given that the error terms do not vanish at these points. For our applications below this is applicable to zeros of in as the noise does vanish at the boundary , a problem addressed in the next section.

Heuristically, the process may arrive at an unstable point by “accident”. To ensure that it does not stay there, we need to know that there is enough noise to push the process out into the drift leading away from .

The main result here, Theorem 2 below, is an adaptation of Theorem 3.5 of [Pem88], a sketch of which can be found in [Pem07] and a corresponding multidimensional result in [Pem90], whereby condition (1.2) is replaced by (iv). For results on nonconvergence to more general unstable sets in the multidimensional case the reader is referred to section 9 of [Ben99] and references there.

To begin with we mention a result which will be used.

Lemma 5.

Let and suppose there is some integer and a real number such that implies . Then .

Proof.

The sequence is an a.s. convergent martingale and a.s., see Th. 35.6 of [Bil95]. If this variable is bounded away from zero it must be 1. ∎

Also, the following will prove to be useful.

Lemma 6.

Let be an integer and be a stopping time with respect to the filtration in Definition 1, such that a.s. Let ,

Suppose that on we have or that we on have , then

| (2.4) |

Proof.

First, we note that for any

so that is an -martingale and hence a.s. convergent. Due to the assumption that on we have strictly positive, or strictly negative, we must have , otherwise we would have . In particular, this assumption means that so that we can make the following calculation

Next, since is true for any random variable ,

∎

Theorem 2.

Assume that there exist an unstable point in , i.e. such that locally, and that

| (2.5) |

holds, for some , whenever is close to . Then

Remark 3.

The local assumptions and (2.5) can without loss of generality be assumed, in the proof, to hold globally. Assume that the theorem is proved with global assumptions but that and (2.5) are only satisfied when is in a neighborhood of . Couple the process after a late time to another process , such that and

If is constructed so as to satisfy the global assumptions of Theorem 2, then so does . Now if , then the same would be true of , contradicting the theorem.

Proof of Theorem 2.

Following Pemantle’s proof there are two steps that need verification:

Step 1: Show that there is a such that for all large enough

| (2.6) |

Step 2: Let

| (2.7) |

Conditional on show that

| (2.8) |

for some not depending on .

Notation: Throughout the proof we will justify inequalities (as they appear in calculations) by stating that they hold if a parameter is sufficiently large. We will denotes this by or if the inequality holds if is sufficiently large, or if it is clear from the context which parameter is referred to, respectively. E.g. , since this is true if .

Verification of Step 1:

First, in view of Remark 3, we assume that and

holds globally.

We aim to show that where is defined in (2.7).

Recall that , so that we have the bounds

We may assume that , otherwise there is nothing to prove. Examine the process for . An upper bound on this quantity is given by

and so

| (2.9) |

Next, we make use of the relation

Since we have so any conditional expectation can be calculated as . Hence,

| (2.10) |

Now, by the assumption we get

| (2.11) |

Also, by the assumption we have that

| (2.12) |

We can now get a lower bound on . Continuing (2.4.1), using (2.4.1) and combining (2.4.1) with the fact that when , we see that

| (2.13) |

where the last inequality is true for any since . Expanding this recursion gives us

Letting and combining this with (2.9) we have

Choosing makes .

Verification of Step 2:

Assume throughout that

, defined by (2.7), is

realized through the event . The case

when is similar. Set

We aim to show that , with .

With notation as in Lemma 6 let and set . Notice that by conditioning on we may consider it fixed (so that Lemma 5 is indeed applicable).

Observe that by the assumption we must have when , since in this case. This gives us

and hence on the event ,

Lemma 6 now gives us

which implies . ∎

2.4.2. Strictly unstable boundary points

In this section we deal with strictly unstable zeros on the boundary. These present a new problem as the error terms tend to vanish, making Theorem 2 inapplicable. This new result motivated a separate paper [Ren09].

Interestingly, the key ingredient here is an upper bound on how fast the error terms are vanishing when the process gets near the unstable point on the boundary. This is quite the opposite to the situation in Theorem 2, which required a lower bound on the error terms. This may at first seem odd. However, the heuristics is that if the process cannot arrive at the boundary in a finite number of steps, knowing that the error terms get small enough means an increasing tendency for the process to follow the drift.

Theorem 3.

Suppose of the process from Definition 1 that for all . Assume that is such that whenever is close to and that there are positive constants such that a.s.

| (2.14) | ||||

| (2.15) | ||||

| (2.16) |

Then .

Remark 4.

Consider the case in Theorem 3. In our applications, is the fraction of white balls in an urn. If and denote the number of white balls and the total number of balls in the urn at time respectively, then . What is usually easy to verify is that , say , which implies so that assumption (2.16) just means that we need that .

Proof of Theorem 3.

We will, for ease of notation, assume in the proof that . Let be a number such that if .

The idea of the proof is to show that should the process ever be close to the origin it is very likely that it doubles its value before it decreases to a fraction of its value. So likely in fact, that it will do this time and time again until it reaches above .

Consider the process after time . Let be a small constant and let . Define

| (2.17) |

Since we assume that for all , we know that and thus . Let and define the two events and . Anticipating an application of Lemma 6, we let and as in that lemma.

On the event we have for any that and hence

Using this estimate gives us, on the event ,

where the last step is justified by assumption (2.16) if .

Next, we use assumptions (2.14) and (2.15) to get

| (2.18) |

where . This in turn gives, since whenever ,

Since on we know from Lemma 2 that eventually must leave , for any , and hence that . So, we can apply Lemma 6 to get

| (2.19) |

Exploiting that , we see that (2.19) is equivalent to, with ,

| (2.20) |

Notice that this estimate decreases if increases.

Next, define stopping times recursively from (2.4.2)

where is some (stochastic) number s.t. and thus since either (in which case ) or

(in which case and ). Define the events and stopping times . Then (2.20) yields, if ,

since and . If then . In either case

holds.

Now, is a subset of the event that the process after reaches above . Hence

This contradicts the assumption that since this requires that there is a positive probability that for every prescribed there is an such that implies . ∎

2.5. Convergence

Now we know when we may exclude some unstable points from the set of limit points. Next, we need to check that stability of a point is in fact enough to ensure positive probability of convergence to . After that we also need to know what happens at a touchpoint. A touchpoint may be thought of as having a “stable side” and an “unstable side”. Intuitively, one may think that convergence to might be possible from the stable side, which is indeed the case.

For the results of the sections to follow we need the notion of attainability, recall Definition 3. This is just to rule out trivialities, as there might exists a stable point in a neighborhood where the process is somehow forbidden to go. Consider e.g. the urn model studied in [HLS80]; an urn has balls of two colors, white and black say, and at each timepoint there is a proportion of white balls and a ball is drawn and replaced along with one additional ball of the same color. The probability of drawing a white ball is not but where . This yields a drift function of . Consider e.g. if and define on in such a way that and a stable zero of exists there. Then the attainability of neighborhoods of this depends on the initial condition . If then can not be reached as (strictly) decreases to zero.

2.5.1. Stable points

That convergence to stable points is possible is known in related models, e.g. [HLS80] has a similar result as Theorem 4 below. For related multidimensional results, see section 7.1 of [Ben99].

Theorem 4.

Suppose is stable, i.e. whenever is close to . If every neighborhood of is attainable then .

Proof.

Case 1: .

We can find and such that

and on and

on . Let

Define . and let be large enough so that , where .

For , define . By attainability there exists an such that . Define

We want to show that is non-zero.

Notice that on we have and if then .

On , for any , we have , so that

Expanding the above recursion gives a bound on the conditional expectation

| (2.21) |

Now,

and this fact in combination with (2.21) yields

Hence, so there is a positive probability that never leaves . On the event Lemma 2 implies that . Since we can repeat our argument with any instead of , and any instead of , this implies that (on the event ).

Case 2:

We will prove the statement for , with being analogous.

Assume that on , for some .

Set so large that ,

,

and

, where is such that .

Analogous to Case 1 we calculate

and

,

so that . We know that

for some by attainability.

So, there is a positive probability of the event for all . By Lemma 2 it follows that on this event we must have . But we may repeat the argument above, choosing any in place of , concluding that . This makes it clear that given the event we must have .

Postponed proof of Lemma 3

We will prove Lemma 3 in the case when the origin is

attainable, the case of the other boundary point, , is analogous.

We assume that is continuous at and we need to prove that .

Assume the contrary, i.e. that and hence, by continuity,

that on , for some .

Recall the notation of Lemma 1 and 2; . Lemma 1 ensures that converges. Hence, for some large (stochastic) we have that implies .

From identical calculations as in Case 2 above, we can conclude that there is a positive probability of for all . Then

with positive probability, which is a contradiction. Hence, . An analogous argument shows that , and Lemma 3 follows. ∎

2.5.2. Touchpoints

Theorem 5 below asserts that as long as the slope toward a touchpoint (from the stable side) is not to steep, convergence is possible. need in fact not be a touchpoint as the proof only shows that convergence to may happen from the stable side. In our applications, the drift function is differentiable and thus the slope tends to zero, making the result applicable.

The method of proof is taken from a similar result of [Pem91], which deals with the same urn model as [HLS80]. The interested reader is adviced to read this article for more, and stronger, results on touchpoints, albeit not in this more general setting of stochastic approximation.

Theorem 5.

Suppose that is such that for some whenever is close to .

Also, assume the following technical condition:

-

Suppose there exists some such that for every and every there exists an such that and .

[Or similarly suppose that for some whenever is close to and assume the existence of a such that for every and every there exists some such that and .]

Remark 5.

Condition states that every point in some neighborhood to the right – the stable side – of can potentially be down-crossed at some “later” time.

Proof.

First, without loss of generality we make the global assumption that for (remember Remark 3). The reason that the origin is not included in the interval where is negative is Lemma 3. These global assumptions are somewhat superfluous, as we will only be concerned with the behavior of the process to the right of . We will however assume that the inequality holds for all .

The idea here is to show that

| (2.22) |

i.e. that it might happen that the process never again reaches below . Given the event that the process stays above , Lemma 2 implies that the process must converge to (from above).

The proof is rather technical and there are numerous constants that needs fine tuning in order for everything to work. First, we will use a sequence of times and a sequence of points starting with an index large enough so that , where is defined by condition .

We define

Notice that by we have , and if for some then all stopping times are bounded, namely , for all .

If we can show that for all , this will imply (2.22).

For reasons that only become apparent later we set

| (2.23) |

where and such that and is to be specified by the demand that

| (2.24) |

If we let , then and , so that we know that there exists an such that . From now on we fix111We may assume that so that , as it is easier to consistently think of as a non-integer. such an . Let

where .

Set

We always have the estimate, due to assuming ,

where , and hence on , for ,

We will begin by bounding

| (2.25) |

Since and means that we can make large enough to ensure that

Set and combine the facts that

so that we can continue the estimates of (2.5.2)

| (2.26) |

Notice that on the event , meaning that implies , we have

Introduce . By the previous bound, given , the events and together imply, first

where is motivated by the fact that if are such that and , then . is motivated by having large enough since tends to 0 as grows. Secondly, by setting ,

where . Notice that

with and , so if is large enough is positive.

We have just shown that on the event we have

If we let then we also have on . An upper bound on can be calculated analogously to the bound on in (2.26). This yields an upper bound on given by

where

as since . Thus we can get the bound

for some constant . So,

since the product converges as

∎

3. Generalized Pólya urns

Now, we will apply these result to determine the limiting fraction of balls in two related urn models. The stochastic approximation machinery makes this fairly easy albeit hard work since the calculations to verify the required properties can be rather lengthy.

3.1. Evolution by one draw

We now return to the model defined in Section 1.4. An urn has white and black balls after the ’th draw. Each draw consists of drawing one ball uniformly from the contents of the urn, noticing the color and replacing it along with additional balls according to the replacement matrix

| WB | ||||

| (3.7) |

so that, e.g. a black ball is replaced along with additional white and additional black balls. The initial values and are considered fixed, although this makes no difference to the distribution of the limiting fraction of white balls, except when and as we will see later.

and denote the indicators of getting a white and black ball in draw , respectively. We define and and implicitly by , which, after rewriting, gives

| (3.8) |

With written on this form it is easy to see that the drift function is given by

| (3.9) |

By defining and we arrive at the stochastic approximation representation

Clearly, and are bounded since , so that conditions (ii) and (iii) of Definition 1 are satisfied.

Condition (i):

Recall that . Define

| (3.10) |

Assume , then

Throughout we will assume that and handle the case separately.

Condition (iv):

To verify condition (iv) of Definition 1 we calculate

the expected value of

for coefficients and . So, there is a constant (depending on ) such that

The error function

In order to apply Theorems 2 and 3 via

verification of condition (2.5) and (2.14) we need to calculate what

we will call the error function

| (3.11) |

One sees from (3.8) and (3.9) that

where so that

3.1.1. Limit points

To determine the limits points of the fraction of white balls in this urn model we know from Theorem 1 that we need to look at zeros of

| (3.12) |

where and . First notice that

| (3.13) |

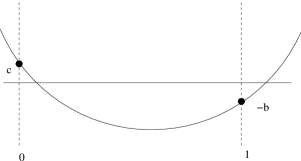

so that, by the continuity and differentiability of , there must be a point such that and , see Fig. 1. A unique zero must be the convergence point of the process and if more than one zero exists, we must check which one is stable (if any).

We will look at the possible difficult zeros , i.e. the ones that are unstable and where the error terms are vanishing, in the sense that , recall (3.11).

First, if and only if and . This is not surprising since there will be no error terms when there is no randomness; this is the urn scheme where white and black balls are added whatever color is drawn. The drift function is then so that is a unique (stable) zero.

It follows from (3.13) that if at most two zeros exist222If there are more than two zeros then is identically zero, since is a polynomial of order at most 2. and one of these is in then that one is stable. Hence, an unstable zero, if it exists, must be at the boundary. By symmetry between colors we need only consider unstable zeros at the origin. To that end set so that , with and , has the property . In order for the origin to be unstable we need parameters to make when is very small. We need to consider two cases:

(i) but . This can only happen if and i.e. . Having makes the sequence a (bounded) martingale and hence a.s. convergent. This is in fact the classical Pólya-Eggenberger urn model where it is well known that converges a.s. to a random variable that has a beta distribution with parameters and , see e.g. Theorem 2.2 of [Fre65] or Theorem 3.2 of [Mah08].

(ii) , i.e. and arbitrary. The origin is an unstable zero and not a convergence point. To see why, we need only notice that certainly can be bounded as (constant) and the same is true of . Considering Remark 4, is clear since does imply that white balls are reinforced infinitely often. Hence, Theorem 3 is applicable.

Loose ends

It remains to check what happens if

(but ).

If then it is clear that a.s. which is the

unique zero of the driftfunction .

The case is symmetric.

So we have proved the following.

Theorem 6.

Consider the Pólya urn scheme with replacement matrix (3.1), starting with a positive number of balls of each color. Then, the limit of the fraction of balls exists a.s. Furthermore, apart from the case when and , in which the fraction of white balls tends a.s. to a beta distribution, the a.s. limiting random variable has a one point distribution at . This point is a zero of (3.12) in and if two such points exists it has the additional property that .

The author does not expect that Theorem 6 is new (although we have never seen it written down). In [Gou89] one finds a similar proposition with less generality as it is demanded that although it has the benefit that and could be negative.

It seems likely that Theorem 3 could be proved using only the embedding method of Athreya and Karlin into multi-type branching processes, see e.g. chapter V of [AK68], but we have not attempted it. However, the model in the next section does not fit this embedding method.

In [HMPS03] a very general extension of the Pólya urn is studied. The urn may have balls of several colors and balls are drawn with a probability according to a function of the urn content. At any stage a replacement policy is randomly selected from a number of different policies, which may include nonbounded random variables, depending on the colors drawn. However, their convergence result (Theorem 2.1) is inapplicable to several cases in our study due to their assumption of a unique zero of the resulting drift function.

3.2. Evolution by two draws

Again, we will consider an urn with balls of two colors but now we turn our attention to an urn scheme where two balls are drawn simultaneously and reinforcement is done according to which of the three possible combinations of colors this results in. and keep their meaning from the previous section but we now assume that so that all 3 combinations of draws have positive probability from the start.

The replacement matrix becomes

| WB | ||||

| (3.22) |

From this we see, e.g. that if we draw a white and a black ball these will be replaced along with additional white and black balls.

This model has been studied e.g. in Chapter 10 of [Mah08], where a central limit theorem for the number of white balls (under parameter constraints, see remark after Theorem 7) is presented as well as applications of the model.

Let and be the indicators of the events that draw results in two white, one black and one white or two black balls, respectively. Since balls are drawn simultaneously we have

| (3.23) | ||||

Remark 6.

If two balls were drawn with replacement we would have the simpler situation

As the rightmost parts of (3.2) suggest that for large there is little difference in sampling the two balls with or without replacement. Sampling without replacement will make the calculations messier but with the added benefit that is it easy to see that the result, Theorem 7 below, will remain valid in the simpler case. In the calculations, terms named “” or “” are terms that would be zero if we drew with replacement.

The number of white balls and the total number of balls evolve recursively as

Hence, the increments of the fraction of white balls can be calculated as

which we again denote as . From the above and (3.2) we calculate

where

with

| (3.24) | ||||

Setting gives us the stochastic approximation representation . It is clear that (ii) and (iii) of Definition 1 are satisfied.

Condition (i): Define

| (3.25) |

Assume , then

Throughout we will assume that and handle the case separately.

Condition (iv):

We write the expectation of as

| (3.26) |

where each in (3.26) has the form

with coefficients given by Table 1. As an example, is calculated from .

| 0 | 0 | 0 | 0 |

|---|---|---|---|

| 1 | 0 | ||

| 2 | |||

| 3 | |||

| 4 | |||

| 5 |

Each is a polynomial in divided by , more precisely

We want to show that . The terms clearly satisfy .

Recalling (3.2), and plugging these in, shows that for each we have . This gives us

| (3.26) | |||

where and are some constants whose exact value is of no importance. This makes it clear that

The error function

In order to apply Theorems 2 and 3 via

verification of condition (2.5) and (2.14) we need to

calculate the second moment of

Excruciating calculations show that the error function is given by

where is a polynomial in divided by (so this term tends to zero for large ) and is a polynomial of order 4 given by

which is too complicated a formula to work with. Working through the expression one can arrive at the form

| (3.27) |

where

and the relation

| (3.28) |

holds.

3.2.1. Limit points

To determine the limiting fraction of white balls we need to examine the zeros of

| (3.29) |

where , and . We see that

| (3.30) |

By continuity and differentiability there will thus exists a point with and . A difference with the previous model, where the urn evolved by a single draw each time, is that we now have more types of equilibrium points. Previously, we only encountered unstable zeros on the boundary, which we resolved with Theorem 3. Now we will also make use of Theorems 2 and 5.

Remark 7.

There will be urn schemes with a unique zero, e.g. the case , where

and is unique. Another example is given by where .

Remark 8.

On attainability and condition of

Theorem 5

Consider the replacement matrix 3.2. Let and

denote the number of times that draws up to time

has resulted in the combinations and

, respectively.

Then

Since

for any combination such that , it follows that any open set in is attainable, where

Hence, if is a stable zero of and then the conditions of Theorem 4 is fullfilled and .

We can also see that condition of Theorem 5 is satisfied if is a touchpoint and . Furthermore, since the drift is continuously differentiable, the slope will tend to zero close to , making Theorem 5 applicable.

We will not attempt to prove that it will always be the case that neighborhoods of stable points are attainable and that condition is satisfied whenever there is a touchpoint. Our attempts to do so yields too messy calculations, but it seems reasonable that this is true.

In any specific situation there is no problem in verifying these conditions.

Remark 9.

There will be urn schemes where the set of stable zeros contains exactly two points and with unstable zeros in . For example the case , where

and is unstable whereas and are stable. Notice that and so that both stable points are possible convergence points by Remark 8.

Remark 10.

Touchpoints may arise. If then

where is a touchpoint and is stable. Notice that so that both the stable point and the touchpoint are possible convergence points by Remark 8.

No unstable equilibrium in with vanishing error terms.

Now we will examine whether there could exist an unstable zero in

such that , i.e. an unstable zero to which we can not apply

Theorem 2. We recall that

where and

is given in (3.27). Hence, we need to look at points such that

.

First, if . It is easy to calculate and intuitive that this can only happen if and , since this is the case when there is no randomness involved in the urn scheme, white and black balls are added whatever is drawn. Then so that is unique.

Next, we need to solve for . We will do this by going through the cases when exactly one of or , or none, is zero. This suffices due to relation (3.28).

Note, since the drift function is a polynomial of order at most with boundary condition (3.30), the only time when an unstable has is when . This case is special and will be treated below. Hence, we need only verify that if is a point where vanishes, then is not strictly unstable, i.e. that .

The case

If , i.e. and , then from (3.28) we have that

. Then

We assume is not identically zero, so if then is never zero. If then for . The drift function is now

so that and thus if . If then

If , then so that or . In the latter case we have .

The case

If then and , and

where has no roots in . We assume that is not identically zero so if then is never zero. If then for . Now

so that if . If then

If then so or . In the latter case we have .

The case

If then , , and

We assume that is not identically zero so if then is never zero. If then for and

so that

The case not

Suppose , , and

. The only chance of having , for ,

is for and to be zero simultaneously.

A common zero of and when none of these is

identically zero imposes

which is the case whenever .

Setting and and using Maple yields the simple expression

which is zero if . The derivative simplifies to

If then so is or . If we can write and

So we can determine that there is no strictly unstable zero of in such that the error terms are vanishing.

Unstable boundary points

Next, we check the boundary. By symmetry of colors we need only consider

an unstable zero of at the origin. To that end set

so that has . We check the cases

where close to the origin:

(a) , and is only possible

if , and so that and hence

. It is then, in some sense, the 2-draw version

of the classical Pólya urn. The special case of

has been studied in [CW05] and they show that

the limiting variable has an absolutely continuous distribution.

They also include a simulation study that indicates that the

limiting distribution “resembles” the beta distribution.

By Theorem 2,

we may only conclude

that the limiting distribution has no point masses on .

(b) and , i.e. and .

(c) , i.e. .

In both (b) and (c)

the conditions of Theorem 3 are satisfied. can

be made arbitrarily big since . In the second case this

is due to . Since the combination will always be drawn

infinitely often, it follows that white balls will tend to infinity.

In the first case, either and we are done, or

and so that the combination will be drawn infinitely

often.

Also, both and behave like (constant) when is close to zero. Thus, convergence to a strictly unstable boundary point is impossible.

Loose ends

Here we examine what happens if .

1. has drift . It is clear that does converge to a.s. (i.e. the stable zero of ) since any draw that alters the urns composition does so by increasing the number of white balls by and the numbers of black balls by .

2. is symmetric to the above case ; will converge to the stable zero of .

3. has

with being the only stable zero. It is clear that converges to this point a.s.

4. and so that nothing happens when two white balls are drawn (except that they are replaced in the urn). Let and for

By looking at the sequence we ignore the times when two white balls are drawn. This makes no difference to the limit since for .

However, since

it is more convenient to define and . It is straightforward to compute where

so that

We also get the error function, with , as

Since we have assumed we know that (i) of Definition (1) is satisfied, and one easily verifies (ii)-(iv).

As and any unstable zero of must be on the boundary . We can apply Theorem 3 to conclude that will not converge to an unstable boundary point.

So, we have the original process described by the driftfunction

and our ”new” process described by

Now, as , the limit and are related as

In particular is equivalent to and is equivalent to .

A straightforward calculations shows that

| (3.31) |

so that and have the same zeros, with the possible exception of .

For we examine two cases:

-

(i)

If then , whereas always, so that , which implies . But so that nonconvergence to is what we would expect..

-

(ii)

If then . We examine the behavior of these close to via the calculations

Hence is stable/unstable simultaneously for and .

Differentiating (3.31) for yields

so that at any point where and vanishes we have

i.e. and have the same stable and strictly unstable points (if any). For any such that and vanishes we also have

so that and have identical touchpoints (if any).

Thus the convergence of to a stable zero of implies the convergence of to a stable zero of . Also, the non-convergence to an unstable zero of implies the non-convergence to an unstable zero of .

5. and is symmetric to 4.

6. and . Define as in the previous section and . Now

is a difficult expression to work with directly, so we rewrite it as

Next, set . Then

so that

Next,

which yields the error function

One may also verify (iv) of Definition (1) by calculating:

which certainly is .

Next we compare with the original process , with drift

It is straightforward to verify that

| (3.32) |

so that and have the same equilibrium points. Differentiating (3.32) yields

so, at any point where we have . Differentiating again at a point where yields . In conclusion, and have ”similar” equilibrium points in that they are stable, strictly unstable, or touchpoints simultaneously.

We have proved the following.

Theorem 7.

Suppose that the Pólya urn scheme of drawing two balls (with or without replacement) according to (3.2) has (or just if drawn with replacement). Then, the limit of the fraction of balls exists a.s. Furthermore, apart from the case , and , in which all we may conclude is that the limiting variable of the fraction of white balls has no point masses in , the limiting random variable has support only on the zeros of , defined in (3.29), such that the derivative is nonpositive there.

In Theorem 10.1 of [Mah08] one can find a central limit theorem for the number of white balls in the urn scheme 3.2 with the added constraints of a constant row sum larger than one (i.e. ) and , which together has the effect that the drift function becomes linear (i.e. in 3.2). It is also noted there (Proposition 10.3) that the fraction of white balls converge (in probability) to .

Acknowledgements

This paper, with minor modifications, has served as my licentiate thesis which was defended 2009-03-06 at Uppsala university. I am indebted to my PhD supervisors Sven Erick Alm and Svante Janson for their encouragement and for providing me with numerous ways to improve this paper, both with the mathematics and clarity of exposition.

The thesis was partly finished while attending the Mittag-Leffler institute. I am indebted to the Royal Swedish Academy of Sciences for financial support towards attending the institute during spring 2009.

In the midst of writing this thesis I became a father. A most loving acknowledgement to my wonderful wife Ida who has looked after both me and our amazing little girl, Emma, during this time.

References

- [AK68] K. B. Athreya, S. Karlin: Embedding of urn schemes into continuous time Markov branching processes and related limit theorems, Ann. Math. Statist., 39 (1968), 1801–1817.

- [APSV08] R. Argiento, R. Pemantle, B. Skyrms, S. Volkov: Learning to signal: analysis of a micro-level reinforcement model. Preprint (2008), 19 pages. To appear in Stoch. Proc. Appl.

- [Ben99] M. Benaïm: Dynamics of stochastic approximation algorithms, Séminaire de Probabilités. Lectures Notes in Mathematics, 1709, Springer (1999), 1-68.

- [Bil95] P. Billingsley: Probability and Measure, 3rd ed. Wiley Series in Probability and Mathematical Statistics (1995).

- [Bor08] V. Borkar: Stochastic approximation. A dynamical systems viewpoint, Cambridge University Press, (2008).

- [CW05] M. Chen, C. Wei: A new urn model, J. Appl. Probab. 42 (2005), 964–976.

- [EP23] F. Eggenberger, G. Pólya: Über die Statistik verketteter Vorgänge, Zeit. Angew. Math. Mech. 3 (1923), 279–289.

- [Fre65] D. Freedman: Bernard Friedman’s urn, Ann. Math. Statist., 36 (1965), 956–970.

- [Gou89] R. Gouet: A martingale approach to strong convergence in a generalized Pólya-Eggenberger urn model, Statist. Probab. Lett., 8 (1989), 225–228.

- [HMPS03] I. Higueras, J. Moler, F. Plo, M. San Miguel: Urn models and differential algebraic equations. J. Appl. Probab., 40 (2003), 401–412.

- [HLS80] B. Hill, D. Lane, W. Sudderth: A strong law for some generalized urn processes, Ann. Probab., 8 No. 2 (1980), 214–226.

- [Jan04] S. Janson: Functional limit theorems for multitype branching processes and generalized Pólya urns, Stochastic Process. Appl., 110 No. 2 (2004), 177–245.

- [Jan06] S. Janson: Limit theorems for triangular urn schemes, Probab. Theory Related Fields, 134 No. 3 (2006), 417–452.

- [JK77] N. Johnsson, S. Kotz: Urn models and their application. An approach to modern discrete probability theory. Wiley (1977).

- [Mah08] H. M. Mahmoud: Pólya urn models, CRC Press (2009).

- [Pem88] R. Pemantle: Random processes with reinforcement, Doctoral Dissertation. M.I.T. (1988).

- [Pem90] R. Pemantle. Nonconvergence to unstable points in urn models and stochastic approximations, Ann. Probab., 18 No. 2 (1990), 698–712.

- [Pem91] R. Pemantle. When are touchpoints limits for generalized Pólya urns?, Proc. Amer. Math. Soc., 113 No. 1 (1991), 235–243.

- [Pem07] R. Pemantle: A survey of random processes with reinforcement, Probab. Surv., 4 (2007), 1–79.

- [Ren09] H. Renlund: Nonconvergence to strictly unstable boundary points in stochastic approximation. Preprint (2009), 9 pages.

- [RM51] H. Robbins, S. Monro: A stochastic approximation method, Ann. Math. Statist. 22 (1951), 400–407.