MM Algorithms for Minimizing Nonsmoothly Penalized Objective Functions

Abstract

The use of regularization, or penalization, has become increasingly common in high-dimensional statistical analysis over the past decade, where a common goal is to simultaneously select important variables and estimate their effects. It has been shown by several authors that these goals can be achieved by minimizing some parameter-dependent “goodness of fit” function (e.g., a negative loglikelihood) subject to a penalization that promotes sparsity. Penalty functions that are nonsmooth (i.e. not differentiable) at the origin have received substantial attention, arguably beginning with LASSO (Tibshirani, 1996).

The current literature tends to focus on specific combinations of

smooth data fidelity (i.e., goodness-of-fit) and nonsmooth penalty

functions. One result of this combined specificity has been a

proliferation in the number of computational algorithms designed to

solve fairly narrow classes of optimization problems involving

objective functions that are not everywhere continuously

differentiable. In this paper, we propose a general class of

algorithms for optimizing an extensive variety of nonsmoothly

penalized objective functions that satisfy certain regularity

conditions. The proposed framework utilizes the

majorization-minimization (MM) algorithm as its core optimization

engine. The resulting algorithms rely on iterated soft-thresholding,

implemented componentwise, allowing for fast, stable updating that

avoids the need for any high-dimensional matrix inversion. We

establish a local convergence theory for this class of algorithms

under weaker assumptions than previously considered in the

statistical literature. We also demonstrate the exceptional

effectiveness of new acceleration methods, originally proposed for

the EM algorithm, in this class of problems. Simulation results and

a microarray data example are provided to demonstrate the

algorithm’s capabilities and versatility.

Keywords: Iterative Soft Thresholding, MIST, MM algorithm.

1 Introduction

Variable selection is an important and challenging issue in the rapidly growing realm of high-dimensional statistical modeling. In such cases, it is often of interest to identify a few important variables in a veritable sea of noise. Modern methods, increasingly based on the principle of penalized likelihood estimation applied to high dimensional regression problems, attempt to achieve this goal through an adaptive variable selection process that simultaneously permits estimation of regression effects. Indeed, the literature on the penalization of a “goodness of fit” function (e.g., negative loglikelihood), with a penalty singular at the origin, is quickly becoming vast, proliferating in part due to the consideration of specific combinations of data fidelity (i.e., goodness-of-fit) and penalty functions, the associated statistical properties of resulting estimators, and the development of several combination-specific optimization algorithms, (e.g., Tibshirani, 1996; Zou, 2006; Zou and Hastie, 2005; Zou and Zhang, 2009; Fan and Li, 2001; Park and Hastie, 2007; Friedman et al., 2008).

In this paper, we propose a unified optimization framework that appeals to the Majorization-Minimization (MM) algorithm (Lange, 2004) as the primary optimization tool. The resulting class of algorithms is referred to as MIST, an acronym for Minimization by Iterative Soft Thresholding. The MM algorithm has been considered before for solving specific classes of singularly penalized likelihood estimation problems (e.g., Daubechies et al., 2004; Hunter and Li, 2005; Zou and Li, 2008); to a large extent, this work is motivated by these ideas. A distinct advantage of the proposed work is the exceptional versatility of the class of MIST algorithms, their associated ease of implementation and numerical stability, and the development of a fixed point convergence theory that permits weaker assumptions than existing papers in this area. We emphasize here the focus of this paper is on the development of a stable and versatile class of algorithms applicable to a wide variety of singularly penalized estimation problems. In particular, the consideration of asymptotic and oracle properties of estimators derived from particular combinations of fidelity and penalty functions, as well as methods for effectively choosing associated penalty parameters, are not focal points of this paper. A comprehensive treatment of these results may be found in Johnson et al. (2008), where asymptotics and oracle properties for estimators derived from a general class of penalized estimating equations are developed in some detail.

The paper is organized as follows. In Section 2, we introduce notation and provide sufficient conditions for local convergence of the MM algorithm applied to a large class of data-fidelity and non-smooth penalty functions. In Section 3, we present a specialized version of this general algorithm, demonstrating in particular how the minimization step of the MM algorithm can be carried out using iterated soft-thresholding. In its most general form, iterated soft-thresholding is required at each minimization step; we further demonstrate how to carry out this minimization step in one iteration through a judicious choice of majorization function. As a consequence, we present a simplified class of iterative algorithms that are applicable to a wide class of singularly penalized, generalized linear regression models.

Simulation results are provided in Section 4, while an application in survival analysis to Diffuse Large B Cell Lymphoma expression data (Rosenwald et al., 2002) is presented in Section 5. We conclude with a discussion in Section 6. Proofs and other relevant results are collected in the Appendix.

2 MM algorithms for nonsmooth objective functions

Let denote a real-valued objective function to be minimized for in some convex subset of . Let denote a real-valued “surrogate” objective function, where . Define the minimization map

| (1) |

Then, if majorizes for each , a generic MM algorithm for minimizing takes the following form (e.g., Lange, 2004):

-

1.

Initialize

-

2.

For , compute iterating until convergence.

Provided that the objective function, its surrogate and the mapping satisfy certain regularity conditions, one can establish convergence of this algorithm to a local or global solution. Lange (2004, Ch. 10) develops such a theory assuming that the objective functions and are twice continuously differentiable. For problems that lack this degree of smoothness (e.g., all singularly penalized regression problems, including lasso, Tibshirani (1996); adaptive lasso, Zou (2006); and SCAD, Fan and Li (2001)), a more general theory of local convergence is required. One such theory is summarized in Appendix A.1; related results for the EM algorithm may be found in Wu (1983), Tseng (2004) and Chrétien and Hero (2008).

Let denote the usual Euclidean vector norm. Based on the theory summarized in Appendix A.1, we propose a new and general class of algorithms for minimizing penalized objective functions of the form

| (2) |

where and are respectively data fidelity (e.g., negative loglikelihood) and penalty functions that satisfy regularity conditions to be delineated below. As will be shown later, the class of problems represented by (2) contains all of the penalized regression problems commonly considered in the current literature. It also covers numerous other problems by expanding the class of permissible fidelity and penalty functions in a substantial way.

We assume throughout that is convex and coercive for , where is an open convex subset of . We further assume that

| (3) |

where the vector and denotes the block of associated with It is assumed that each has dimension greater than or equal to one, that all blocks have the same dimension, and that the for each . Evidently, the case where dim for simply corresponds to the setting in which each coefficient is penalized in exactly the same way; permitting the dimension of to exceed one allows the penalty to depend on additional parameters (e.g., weights, such as in the case of the adaptive lasso considered in Zou (2006)). We are interested in problems with penalization; therefore, is assumed bounded and strictly positive throughout this paper. Several specific examples will be discussed below. For any bounded with as the first element, and the remainder of collecting any additional parameters used to define the penalty, the scalar function is assumed to satisfy the following condition:

-

(P1)

for ; is a continuously differentiable concave function with for , and, for some finite .

Evidently, (P1) implies that for where may be finite or infinite. The combination of the concavity and nonnegative derivative conditions thus imply that the penalty increases away from the origin, but with a decreasing rate of growth that may become zero. The case where (3) is identically zero for is ruled out by the positivity of the right derivative at the origin imposed in (P1); similarly, the concavity assumption also rules out the possibility of a strictly convex penalty term. Neither of these restrictions is particularly problematic. Our specific interest lies in the development of algorithms for estimation problems subject to a penalty singular at the origin. Were (3) absent, or replaced by a strictly convex penalty term, the convexity of implies (2) can be minimized directly using any suitable convex optimization algorithm, such as that discussed in Theorem 3.2 below.

Theorem 2.1 establishes local convergence of the indicated class of MM algorithms for minimizing objective functions of the form (2). A proof is provided in Appendix A.2, where it is shown that conditions imposed in the statement of the theorem are sufficient conditions for the application of the general MM local convergence theory summarized in Appendix A.1.

Theorem 2.1.

Let be convex and coercive and assume satisfies both (3) and condition (P1). Let be a real-valued, continuous function of and that is continuously differentiable in for each and satisfies when . Let

| (4) |

where for , and define

Assume the set of stationary points for is finite and isolated. Then:

-

(i)

in (2) is locally Lipschitz continuous and coercive;

-

(ii)

is either identically zero or non-negative for all

-

(iii)

majorizes and the MM algorithm derived from converges to a stationary point of if is uniquely minimized in for each and at least one of or is strictly positive for each

Condition (iii) of Theorem 2.1 establishes convergence under the assumption that strictly majorizes and has a unique minimizer in for each . Such a uniqueness condition is shown by Vaida (2005) to ensure convergence of the EM and MM algorithms to a stationary point under more restrictive differentiability conditions. Importantly, the assumption of globally strict majorization is only a sufficient condition for convergence; this condition is only important insofar as it guarantees a strict decrease in the objective function at every iteration. As can be seen from the proof, it is possible to relax this condition to locally strict majorization, in which majorizes with strict majorization being necessary only in an open neighborhood containing .

The use of the MM algorithm and selection of (4) are motivated by the results Zou and Li (2008); we refer the reader to Remark 3.1 below for further comments in this direction. The assumptions on clearly cover the case of the linear and canonically parameterized generalized linear models upon setting where denotes the corresponding loglikelihood function. Estimation under the semiparametric Cox regression model (Cox, 1972) and accelerated failure time models are also covered upon setting to be either the negative logarithm of the partial likelihood function (e.g., Andersen et al., 1993, Thm VII.2.1) or the Gehan objective function (e.g., Fygenson and Ritov, 1994; Johnson and Strawderman, 2009).

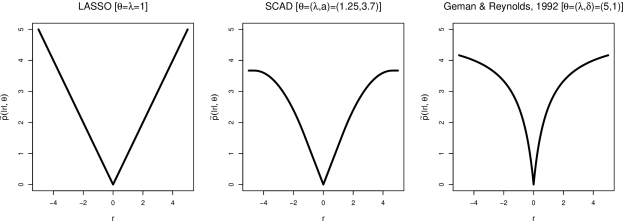

The assumption (P1) on the penalty function covers a wide variety of popular and interesting examples; see Figure 1 for illustration. For example, the lasso (LAS; e.g., Tibshirani, 1996), adaptive lasso (ALAS; e.g., Zou, 2006), elastic net (EN; e.g., Zou and Hastie, 2005), and adaptive elastic net (AEN; e.g., Zou and Zhang, 2009) penalties are all recovered as special cases upon considering the combination of (3) and the ridge-type penalty Specifically, with for , taking in (3) gives LAS ALAS , EN and the AEN penalties. It is easy to see that selecting also implies the equality of (3) and (4), a result relevant in both (ii) and (iii) of Theorem 2.1 above.

The proposed penalty specification also covers the smoothly clipped absolute deviation (SCAD; e.g., Fan and Li, 2001) penalty upon setting for each , where is defined as the definite integral of

| (5) |

on the interval and some fixed value of (e.g., ). The resulting penalty function is continuously differentiable and concave on . The concavity of on combined with and the fact that is finite, implies

| (6) |

for each , the boundary cases for and/or following from Hiriart-Urruty and Lemaréchal (1996, Remark 4.1.2, p. 21). In other words, can be majorized by a linear function of

The lasso penalty, its variants, and SCAD have received the greatest attention in the literature. More recently, Zhang (2007) introduced the minimax concave penalty (MCP), which similarly to SCAD is defined in terms of its derivative. Specifically, one takes for each in (3), where is defined for as the definite integral of

| (7) |

on the interval and some fixed value of (e.g., as in Fan et al., 2009b). Further examples of differentiable concave penalties include for

| (8) |

(e.g. Geman and Reynolds, 1992; Nikolova, 2000); and for

| (9) |

(e.g. Antoniadis et al., 2009). These penalties represent just a small sample of the set of possible penalties satisfying (P1) that one might reasonably consider.

3 MIST: Minimization by Iterated Soft Thresholding

3.1 The MIST algorithm

In general, the statistical literature on penalized estimation has proposed optimization algorithms tailored for specific combinations of fidelity and penalty functions. The class of MM algorithms suggested by Theorem 2.1 provides a very general and useful framework for proposing new algorithms, the key to which is a methodology for solving the minimization problem (1), a step repeated with each iteration of the MM algorithm. In this regard, it is helpful to note that the problem of minimizing for a given is equivalent to minimizing

| (10) |

in . In particular, if is strictly convex for each bounded , which clearly occurs if both and are convex in and at least one is strictly convex, then (10) is also strictly convex and the corresponding minimization problem has a unique solution.

Remark 3.1.

For and for with a twice continuously differentiable loglikelihood function, the majorizer used by the MM algorithm induced by the surrogate function (10) corresponds (up to sign) to the minorizer employed in the LLA algorithm of Zou and Li (2008), an improvement on the so-called LQA algorithm proposed in Hunter and Li (2005). Zou and Li (2008, Proposition 1) assert convergence of their LLA algorithm under imprecisely stated assumptions and are additionally unclear as to the nature of convergence result actually estabished. For example, while Zou and Li (2008, Theorem 1) demonstrate that the LLA algorithm does indeed have an ascent property, their result appears to be insufficient to ensure that the proper analog of condition Z3(ii) of Theorem A.1 holds in the case of the SCAD penalty. As a consequence, it is unclear whether even weak “subsequence” convergence results (cf. Wu, 1983) hold with useful generality in the case of the LLA algorithm. In contrast, Theorem 2.1 shows that strict majorization, under a few precisely stated conditions, is sufficient to ensure local convergence of the resulting MM algorithm to a stationary point of (2) In Section 3.2, it is further demonstrated how a particular choice of yields a strict majorizer that permits both closed form minimization and componentwise updating at each step of the MM algorithm, even in the case of penalties that fail to be strictly concave.

Numerous methods exist for minimizing a differentiable convex objective function (e.g., Boyd and Vandenberghe, 2004). However, because (10) is not differentiable, such methods do not apply in the current setting. Specialized methods exist for nonsmooth problems of the form (10) in settings where has a special structure; a well-known example here is LARS (Efron et al., 2004), which can be used to efficiently solve lasso-type problems in the case where is replaced by a least squares objective function. Recently, Combettes and Wajs (2005, Proposition 3.1; Theorem 3.4) proposed a very general class of fixed point algorithms for minimizing where are each convex and takes values in some real Hilbert space . Hale et al. (2008, Theorem 4.5) specialize the results of Combettes and Wajs (2005) to the case where is some subset of and . The collective application of these results to the problem of minimizing (10) generates an iterated soft-thresholding procedure with an appealingly simple structure. Theorem 3.2, given below, states the algorithm, along with conditions under which the algorithm is guaranteed to converge; a proof is provided in Appendix A.3. The resulting class of procedures, that is, MM algorithms in which the minimization of (10) is carried out via this iterated soft-thresholding procedure, is hereafter referred to as MIST, an acronym for (M)inimization by (I)terated (S)oft (T)hresholding. Two important and useful features of MIST include the absence of high-dimensional matrix inversion and the ability to update each individual parameter separately.

Theorem 3.2.

Suppose the conditions of Theorem 2.1 hold. Let be strictly convex with a Lipschitz continuous derivative of order for each bounded Then, for any such and a constant , the unique minimizer of (10) can be obtained in a finite number of iterations using iterated soft-thresholding:

-

1.

Set and initialize

-

2.

Compute

-

3.

Compute , where for any vectors

(11) denotes the unit vector for

(12) is the univariate soft-thresholding operator, and

-

4.

Stop if converged; else, set and return to Step 2.

The proposed algorithm, as originally developed in Combettes and Wajs (2005), is suitable for minimizing the sum of a differentiable convex function and another convex function; hence, under similar conditions, one could employ this algorithm directly to minimize (2) in cases where the penalty (3) is derived from some convex function . Theorem 3.4 of Combettes and Wajs (2005) further shows that the update in Step 3 can be generalized to

where, for every , and is a suitable sequence of relaxation constants. Judicious selection of these constants, possibly updated at each step, may improve the convergence rate of this algorithm.

Theorem 3.2 imposes the relatively strong condition that the gradient of is -Lipschitz continuous. The role of this condition, also imposed in Combettes and Wajs (2005, Proposition 3.1; Theorem 3.4), is to ensure that the update at each step of the proposed algorithm is a contraction, thereby guaranteeing its convergence to a fixed point. To see this, note that the update from to in the algorithm of Theorem 3.2 involves the mapping For any bounded and , it is easily shown that

When , the right-hand side reduces to , and the resulting mapping is only nonexpansive (i.e., not necessarily contractive). However, under strict convexity, this situation can occur only if In particular, suppose that then, and, using the mean value theorem,

where . The assumption that the gradient of is -Lipschitz continuous now implies that choosing as indicated guarantees , thereby producing a contraction.

In view of the generality of the Contraction Mapping Theorem (e.g., Luenberger and Ye, 2008, Thm. 10.2.1), it is possible to relax the requirement that is globally -Lipschitz continuous provided that one selects a suitable starting point. The relevant extension is summarized in the corollary below; one may prove this result in a manner similar to Theorem 4.5 of Hale et al. (2008).

Corollary 3.3.

Let the conditions of Theorem 2.1 hold. Suppose is a bounded vector and assume that is strictly convex and twice continuously differentiable. Then, for a given bounded , there exists a unique minimizer . Let be a bounded convex set containing and define to be the largest eigenvalue of . Then, the algorithm of Theorem 3.2 converges to in a finite number of iterations provided that , and .

Some useful insight into the form of the proposed thresholding algorithm can be gained by considering the behavior of the penalty derivative term As suggested earlier, (P1) implies that decreases from its maximum value towards zero as moves away from the origin. For some penalties (e.g., SCAD, MCP), this derivative actually becomes zero at some finite value of , resulting in situations for which for at least one . If this occurs for component , then component of the vector simply reduces to the component of the argument vector . In the extreme case where , the proposed update reduces to an inexact Newton step in which the inverse hessian matrix is replaced by , denoting the identity matrix, and with step-size chosen to ensure that this update yields a contraction. Hence, if each of the components of are sufficiently large in magnitude, the proposed algorithm simply takes an inexact Newton step towards the solution; otherwise, one or more components of this Newton-like update are subject to soft-thresholding.

3.2 Penalized estimation for generalized linear models

The combination of Theorems 2.1, 3.2 and Corollary 3.3 lead to a useful and stable class of algorithms with the ability to deal with a wide range of penalized regression problems. In settings where is strictly convex and twice continuously differentiable, one can safely assume that for all choices of and provided that in (P1) is strictly positive for ; important examples of statistical estimation problems here include many commonly used linear and generalized linear regression models, semiparametric Cox regression (Cox, 1972), and smoothed versions of the accelerated failure time regression model (cf. Johnson and Strawderman, 2009). The SCAD and MCP penalizations, as well as other penalties having for can also be used; however, additional care is required. In particular, and as pointed out in an earlier remark, if one sets for all and then convergence of the resulting algorithm to a stationary point is no longer guaranteed by the above results due to the resulting failure of these penalties to induce strict majorization.

The need to use an iterative algorithm for repeatedly minimizing (10) is not unusual for the class of MM algorithms. However, it turns out that for certain choices of , a suitable choice of in Theorem 3.2 guarantees both strict majorization and permits one to minimize (10) in a single iteration, resulting in a single soft-thresholding update at each iteration. Below, we demonstrate how the MIST algorithm simplifies in settings where corresponds to the negative loglikelihood function of a canonically parameterized generalized linear regression model having a bounded hessian function. The result applies to all penalties satisfying condition (P1), including SCAD and MCP. A proof is provided in Appendix A.4.

Theorem 3.4.

Let y be and suppose the probability distribution of y follows a generalized linear model with a canonical link and linear predictor , where is and is with denoting an intercept. Assume that , where

denotes the corresponding loglikelihood; here, and for for strictly convex and twice continuously differentiable. Let the penalty function be defined as in (3) and satisfy (P1); note that remains unpenalized. Define

| (13) |

where is , and is defined as in Corollary 3.3. Then:

In view of previous results, the result in # 3 of Theorem 3.4 shows that the resulting MM algorithm takes a very simple form: given the current iterate ,

-

1.

update the unpenalized intercept

-

2.

update the remaining parameters :

(17) where .

The specific choice of function clearly serves two useful purposes: (i) it leads to componentwise-soft thresholding; and, (ii) it leads to strict majorization, as is required in condition (iii) of Theorem 2.1, allowing one to establish the convergence of MIST for SCAD and other penalties having at some finite

Evidently, the algorithm above immediately covers the setting of penalized linear regression. For example, suppose that y has been centered to remove from consideration and that the problem has also been rescaled so that X, which is now satisfies the indicated conditions. Then, the results of the Theorem 3.4 apply directly with

where is defined as in Corollary 3.3. For the class of adaptive elastic net penalties (i.e., in (3)), the resulting iterative scheme is exactly that proposed in (De Mol et al., 2008, pg. 17), specialized to the setting of a Euclidean parameter. In particular, we have and in Theorem 3.4, and the proposed update reduces to

where Setting and yields the iterative procedure proposed in Daubechies et al. (2004), provided that is scaled such that is positive definite. The proposed MIST algorithm extends these iterative componentwise soft-thresholding procedures to a much wider class of penalty and data fidelity functions.

The restriction to canonical generalized linear models in Theorem 3.4 is imposed to ensure strict convexity of the negative loglikelihood. Our results are easily modified to handle non-canonical generalized linear models, provided the negative loglikelihood remains strictly convex in and the hessian can be appropriately bounded. Interestingly, not all canonically parameterized generalized linear models satisfy the regularity conditions of Theorem 3.4. One such important class of problems is penalized likelihood estimation for Poisson regression models. For example, in the classical setting of independent Poisson observations with for a known set of constants , we have (i.e., up to irrelevant constants) where

It is easy to see that hence is locally but not globally Lipschitz continuous; hence, it is not possible to choose a matrix such that (14) everywhere majorizes . Nevertheless, progress remains possible. For example, Corollary 3.3 implies that that one can still use a single update of the form (17) provided that a suitable hence and can be identified. Alternatively, using results summarized in Becker et al. (1997), one can instead majorize for any bounded using

where, for every , are any sequence of constants satisfying and if Of importance here is the fact is a strictly convex function of and does not depend on for . One may now take in Theorem 2.1 as being equal to leading to the minimization of

| (18) |

In particular, componentwise soft-thresholding is replaced by componentwise minimization of (18), the latter being possible using any algorithm capable of minimizing a continuous nonlinear function of one variable.

Remark 3.5.

The Cox proportional hazards model (Cox, 1972), while not a generalized linear model, shares the essential features of the generalized linear model utilized in Theorem 3.4. In particular, the negative log partial likelihood, say is strictly convex, twice continuously differentiable, and has a bounded hessian (e.g., Bohning and Lindsay, 1988; Andersen et al., 1993). Consequently, Theorem 3.4 and its proof are easily modified for this setting upon taking as indicated, setting and taking as defined as in Corollary 3.3.

3.3 Accelerating Convergence

Similarly to the EM algorithm, the stability and simplicity of the MM algorithm frequently comes at the price of a slow convergence rate. Numerous methods of accelerating the EM algorithm have been proposed in the literature; see McLachlan and Krishnan (2008) for a review. Recently, Varadhan and Roland (2008) proposed a new method for EM called SQUAREM, obtained by “squaring” an iterative Steffensen-type (STEM) acceleration method. Both STEM and SQUAREM are structured for use with iterative mappings of the form hence applicable to both the EM and MM algorithms. Specifically, the acceleration update for SQUAREM is given by

| (19) | |||||

where and for an adaptive steplength Varadhan and Roland (2008) suggest several steplength options, with preference for choice Roland and Varadhan (2005) provide a proof of local convergence for SQUAREM under restrictive conditions on the EM mapping , while Varadhan and Roland (2008) outline a proof for global convergence for versions of SQUAREM that employ a back-tracking strategy. We study the effectiveness of SQUAREM applied to the simplified form of the MIST algorithm, hereafter denoted SQUAREM2, in Section 4.3.

4 Simulation Results

The simulation results summarized below are intended to compare the estimates of obtained from existing methods to those obtained using the simplified MIST algorithm of Theorem 3.4. In particular, we consider the performance of MIST for the class of penalized linear and generalized linear models, demonstrating its capability of recovering the solutions provided by existing algorithms when both algorithms are forced to use the same set of “tuning” parameters (i.e., penalty parameter(s), plus any additional parameters required to define the penalty itself). In cases where multiple local minima can arise, we further show that the MIST algorithm often tends to find solutions with lower objective function evaluations in comparison with existing algorithms, provided these algorithms utilize the same choice of starting value.

4.1 Example 1: Linear Model

Let and respectively denote -dimensional vectors of ones and zeros. Then, following Zou and Zhang (2009), we generated data from the linear regression model

| (20) |

where is a -dimensional vector with intrinsic dimension and x follows a -dimensional multivariate normal distribution with zero mean and covariance matrix having elements We considered and for independent observations.

Penalized least squares estimation is considered for five popular choices of penalty functions, all of which are currently implemented in the R software language (R Development Core Team, 2005): LAS, ALAS, EN, AEN, and SCAD. The LAS, ALAS, EN and AEN penalties are all convex and lead to unique solutions under mild conditions; the SCAD penalty is concave and the resulting minimization problem may have multiple solutions. In each case, we used existing software for computing solutions subject to these penalizations and compared those results to the solutions computed using the MIST algorithm.

Regarding existing methods, we respectively used the lars (Hastie and Efron, 2007) and elasticnet (Zou and Hastie, 2008) packages for computing solutions in the case of the LAS and EN penalties. For the ALAS and AEN penalties, we used software kindly provided by Zou and Zhang (2009) that also makes use of the elasticnet package. The weights for the AEN penalty are computed using where is an EN estimator and is a positive constant. Using EN-based weights in the AEN fitting algorithm necessitates tuning parameter specification for both EN and AEN. As in Zou and Zhang (2009), the parameters ( in their notation) are allowed to differ, whereas the parameters ( in their notation) are forced to be the same. Evidently, setting () results in the ALAS solution. For the SCAD penalty, we considered the estimator of Kim et al. (2008) (HD), as well the one-step SCAD (1S) and LLA estimators of Zou and Li (2008). The code for the first two methods was kindly provided by their respective authors; the LLA estimator was computed using the R package SIS. The choice was used for all implementations of SCAD.

We considered finding solutions using penalties in the set In particular, for LAS and SCAD, For EN, both and For simplicity, we fixed the weights for AEN for a given by selecting the ‘best’ among the six estimators involving based on a BIC-like criteria. Likewise for ALAS, the weights were computing using the ‘best’ among the six estimators involving . The parameter for the ALAS and AEN penalties was respectively set to three and five for and .

For the strictly convex objective functions associated with the LAS, ALAS, EN, and AEN penalties, we simply used a starting value of For SCAD, three different starting values for the MIST, HD, and LLA SCAD algorithms were considered: (i.e., the unpenalized least squares estimate), and (i.e., the one-step estimate computed using the penalty ). As in Zou and Li (2008), the one-step estimator 1S is computed using , an appropriate choice when .

The convergence criteria used by the existing software packages were used without alteration in this simulation study. The convergence criteria used for MIST were as follows: the algorithm stopped if either (i) the normed difference of successive iterates was less than (convergence of coefficients); or, (ii) the difference of the objective function evaluated at successive iterates was less than and the number of iterations exceeded (convergence of optimization). Due to the large number of comparisons and highly intensive nature of the computations, we ran simulations for each choice of , , and . We report the results for the convex penalties in Table 1 and those for the SCAD penalty in Tables 2 and 3.

In Table 1, we summarize the average normed difference between the solution obtained using existing software and that obtained using MIST, over the simulations; in particular, we report in the two leftmost panels the maximum value of this difference, computed across all combinations of tuning parameters. These maximum differences (all of which are multiplied by ) are remarkably small for all (A)LAS and (A)EN penalties, indicating that MIST recovers the same (unique) solutions as the existing algorithms. Interestingly, the values for LAS are slightly larger than the rest, where the maximum differences all resulted from the smallest value of considered (. In these cases, the algorithm tended to stop using the objective function criteria rather than the (stricter) coefficient criteria, resulting in slightly larger differences on average.

| 0 | 0.5 | 0.75 | 0 | 0.5 | 0.75 | 0 | 0.5 | 0.75 | |

|---|---|---|---|---|---|---|---|---|---|

| LAS | 0.10 | 0.35 | 1.45 | 0.10 | 0.37 | 1.56 | 0.07 | 4.28 | 6.17 |

| ALAS | 0.03 | 0.14 | 0.64 | 0.05 | 0.21 | 1.00 | 1.84 | 2.86 | 3.76 |

| EN | 0.07 | 0.19 | 0.50 | 0.07 | 0.20 | 0.51 | 2.30 | 5.61 | 8.68 |

| AEN | 0.03 | 0.10 | 0.33 | 0.04 | 0.13 | 0.36 | 1.47 | 3.35 | 5.27 |

| LAS | 1.73 | 3.82 | 11.76 | 2.33 | 5.78 | 18.99 | 0.10 | 6.97 | 9.94 |

| ALAS | 0.12 | 0.38 | 1.58 | 0.35 | 1.03 | 4.39 | 1.34 | 2.55 | 3.30 |

| EN | 0.31 | 0.49 | 0.87 | 0.31 | 0.49 | 0.88 | 2.35 | 4.64 | 6.56 |

| AEN | 0.14 | 0.22 | 0.56 | 0.16 | 0.26 | 0.56 | 1.27 | 2.29 | 2.85 |

The results for SCAD are reported in Tables 2 () and 3 () and display (i) the average normed differences, multiplied by for each combination of , , , and starting value; and, (ii) the proportion of simulated datasets in which the MIST solution yields a lower evaluation of the objective function in comparison with the solution obtained using another method for the indicated choice of starting value. The results for are not shown, as the solution was in all cases. In comparison with the convex penalties, larger normed differences are observed, even when controlling for the use of the same starting value. Such differences are a result of two important features of the SCAD optimization problem: (i) the possible existence of several local minima; and, (ii) the fact that the MIST, HD, and LLA algorithms each take a different path from a given starting value towards one of these solutions. For example, while each of the LLA, MIST, and HD algorithms involve majorization of the objective function using a lasso-type surrogate objective function, both the majorization and minimization of the resulting surrogate function are carried out differently in each case. In particular, the LLA algorithm, as implemented in SIS, majorizes only the penalty term and adapts the lasso code in glmpath in order to minimize the corresponding surrogate objective function at each step. The HD algorithm is similar in spirit, but instead decomposes the penalty term into a sum of a concave and convex function and utilizes the the algorithm of Rosset and Zhu (2007) to minimize the corresponding surrogate objective function. The MIST algorithm instead uses the same penalty majorization as the LLA algorithm, but additionally majorizes the negative loglikelihood term in a way that permits minimization of the surrogate function in a single soft-thresholding step. Each procedure therefore takes a different path towards a solution, even when given the same starting value.

We remark here that differences must also expected between any of LLA, HD, MIST and the one-step solution 1S; from an optimization perspective, the one-step estimate is the result of running just one iteration of the LLA algorithm, starting from the unpenalized least squares estimator (Zou and Li, 2008), and only provides an approximation the solution to the desired minimization problem. All other methods (LLA, MIST, HD) iterate until some local minimizer (or stationary point) is reached. For example, when using either or as the starting value, MIST always found a solution that produced a lower evaluation of the objective function in comparison to . However, when using the null starting value of , the one-step estimator did occasionally result in a lower objective function evaluation in cases involving smaller values of . This behavior is not terribly surprising; with small the one-step solution should generally be close to the unpenalized least squares solution, as the objective function itself is likely to be dominated by the least squares term.

Of all the SCAD algorithms considered here, MIST and LLA tended to find the most similar solutions (i.e., have the smallest normed differences). For the cases in which the LLA solution had lower objective function evaluations, all of the MIST solutions were also LLA solutions; i.e, when starting the LLA algorithm with the MIST solution, the algorithm terminated at the starting value (i.e., the LLA solution coincides with the MIST solution). With the exception of three of these cases, starting the MIST algorithm with the LLA solution also resulted in the same behavior. For the most part, the HD and MIST algorithms also gave similar results, with one source of difference being the respective stopping criteria used. The stopping criteria for HD, assessed in order, are as follows: (1) ‘convergence of optimization’: stop if the absolute value of the difference of the objective evaluated at successive iterates is less than 1e-6; (2) ‘convergence of penalty gradient’: stop if the sum of the absolute value of the differences of the derivative of the centered penalty evaluated at successive iterates is less than 1e-6, (3) ‘convergence of coefficients:’ stop if the sum of the absolute value of the differences of successive iterates is less than 1e-6, and (4) ‘jump-over’ criteria: stop if the objective at the previous iterate plus 1e-6 was less than the objective at the current iterate. After careful analysis of the results, we can assert the following:

-

•

The MIST solution usually has the same or a lower evaluation of the objective function in comparison with HD, regardless of starting value.

-

•

HD tends to have the greatest difficulty in cases of high correlation between predictors, a likely result of the fact that this algorithm relies on the variance of the unpenalized least squares estimator, hence matrix inversion, to take steps towards solution. In contrast, MIST requires no matrix inversion.

On balance, the MIST algorithm performs as well or better than LLA and HD in locating minimizers in nearly all cases. As suggested above, variation in the solutions found can be traced to the path each algorithm takes towards a solution and differences in stopping criteria. Remarkably, in cases when the correlation among predictors was low, the choice of starting value made little difference for MIST; either the same solution was found for all starting values or none of the starting values dominated in terms of finding the lower or equivalent objective evaluations. In settings involving higher correlation, however, using either or the starting values tended to result in the lower evaluations of the objective function in comparison with using the unpenalized least squares solution. Similar behavior was observed for the LLA algorithm. In contrast, the choice of starting value had a much larger impact on the performance of the HD estimator; in particular, the use of as a starting value typically resulted in the lowest objective function evaluations when compared to using a non-null starting value.

| method | avg | prop | avg | prop | avg | prop | avg | prop | avg | prop | avg | prop | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | HD | 15.71 | 1.00 | 15.41 | 1.00 | 17.93 | 1.00 | 468.55 | 1.00 | 2076.40 | 1.00 | 55.17 | 1.00 |

| 1S | 99.13 | 1.00 | 99.13 | 1.00 | 99.13 | 1.00 | 211.17 | 1.00 | 211.16 | 1.00 | 211.16 | 1.00 | |

| LLA | 0.43 | 1.00 | 0.46 | 1.00 | 0.46 | 1.00 | 2.07 | 1.00 | 1.96 | 1.00 | 2.02 | 1.00 | |

| 0.5 | HD | 7.07 | 0.99 | 10.72 | 1.00 | 2.04 | 1.00 | 269.85 | 0.97 | 218.94 | 0.94 | 130.76 | 0.98 |

| 1S | 192.22 | 1.00 | 192.01 | 1.00 | 192.00 | 1.00 | 483.89 | 0.98 | 421.17 | 1.00 | 419.15 | 1.00 | |

| LLA | 6.65 | 0.99 | 0.62 | 1.00 | 0.60 | 1.00 | 57.87 | 0.96 | 12.84 | 0.99 | 2.37 | 1.00 | |

| 0.75 | HD | 29.25 | 0.99 | 105.39 | 0.92 | 66.83 | 0.96 | 2335.23 | 1.00 | 2758.43 | 0.98 | 2731.10 | 0.99 |

| 1S | 575.09 | 1.00 | 488.09 | 1.00 | 486.19 | 1.00 | 1417.97 | 0.86 | 604.26 | 1.00 | 629.21 | 1.00 | |

| LLA | 23.81 | 0.98 | 23.34 | 0.99 | 1.67 | 0.99 | 558.56 | 0.73 | 69.30 | 0.96 | 44.87 | 0.98 | |

| 0 | HD | 6.22 | 1.00 | 22.87 | 1.00 | 19.99 | 1.00 | 9.44 | 1.00 | 35.16 | 1.00 | 14.65 | 1.00 |

| 1S | 694.59 | 1.00 | 694.57 | 1.00 | 694.57 | 1.00 | 844.68 | 1.00 | 844.67 | 1.00 | 844.67 | 1.00 | |

| LLA | 1.64 | 1.00 | 1.71 | 1.00 | 1.74 | 1.00 | 1.47 | 1.00 | 1.47 | 1.00 | 1.43 | 1.00 | |

| 0.5 | HD | 300.62 | 0.98 | 34.09 | 1.00 | 115.76 | 0.98 | 303.98 | 0.96 | 140.26 | 1.00 | 94.90 | 1.00 |

| 1S | 4489.01 | 1.00 | 4276.77 | 1.00 | 4261.64 | 1.00 | 3547.69 | 1.00 | 3254.16 | 1.00 | 3254.16 | 1.00 | |

| LLA | 296.53 | 0.98 | 7.10 | 1.00 | 88.14 | 0.98 | 248.82 | 0.96 | 2.66 | 1.00 | 2.66 | 1.00 | |

| 0.75 | HD | 3083.00 | 0.68 | 1980.40 | 0.89 | 1138.53 | 0.96 | 1476.59 | 0.84 | 1669.60 | 0.93 | 868.21 | 0.97 |

| 1S | 7224.77 | 1.00 | 5491.09 | 1.00 | 5622.21 | 1.00 | 5682.04 | 0.96 | 3835.30 | 1.00 | 3748.35 | 1.00 | |

| LLA | 2802.66 | 0.66 | 1121.80 | 0.85 | 293.50 | 0.96 | 1365.76 | 0.83 | 918.63 | 0.89 | 433.66 | 0.96 | |

| 0 | HD | 18.18 | 1.00 | 18.18 | 1.00 | 18.18 | 1.00 | 17.73 | 1.00 | 17.73 | 1.00 | 17.73 | 1.00 |

| 1S | 48.23 | 1.00 | 48.23 | 1.00 | 48.23 | 1.00 | 63.63 | 1.00 | 63.63 | 1.00 | 63.63 | 1.00 | |

| LLA | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| 0.5 | HD | 0.01 | 1.00 | 0.01 | 1.00 | 0.01 | 1.00 | 0.01 | 1.00 | 0.01 | 1.00 | 0.01 | 1.00 |

| 1S | 3696.85 | 1.00 | 3696.85 | 1.00 | 3696.85 | 1.00 | 3751.96 | 1.00 | 3751.96 | 1.00 | 3751.96 | 1.00 | |

| LLA | 0.02 | 1.00 | 0.09 | 1.00 | 0.08 | 1.00 | 0.03 | 1.00 | 0.14 | 1.00 | 0.08 | 1.00 | |

| 0.75 | HD | 0.27 | 1.00 | 0.27 | 1.00 | 98.05 | 1.00 | 19.20 | 0.99 | 19.21 | 0.99 | 99.95 | 0.99 |

| 1S | 3977.93 | 1.00 | 3977.93 | 1.00 | 4045.81 | 1.00 | 4170.49 | 1.00 | 4170.49 | 1.00 | 4180.79 | 1.00 | |

| LLA | 0.27 | 1.00 | 0.45 | 1.00 | 98.35 | 1.00 | 19.00 | 0.99 | 19.20 | 0.99 | 100.05 | 0.99 | |

| 0 | HD | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 |

| 1S | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| LLA | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| 0.5 | HD | 57.33 | 1.00 | 57.33 | 1.00 | 57.33 | 1.00 | 53.80 | 1.00 | 53.80 | 1.00 | 53.80 | 1.00 |

| 1S | 501.86 | 1.00 | 501.86 | 1.00 | 501.86 | 1.00 | 497.87 | 1.00 | 497.87 | 1.00 | 497.87 | 1.00 | |

| LLA | 0.01 | 1.00 | 0.03 | 1.00 | 0.01 | 1.00 | 0.01 | 1.00 | 0.04 | 1.00 | 0.01 | 1.00 | |

| 0.75 | HD | 0.41 | 1.00 | 0.41 | 1.00 | 0.41 | 1.00 | 0.53 | 1.00 | 0.53 | 1.00 | 0.53 | 1.00 |

| 1S | 4206.65 | 1.00 | 4206.65 | 1.00 | 4206.65 | 1.00 | 4261.12 | 1.00 | 4261.12 | 1.00 | 4261.12 | 1.00 | |

| LLA | 0.09 | 1.00 | 0.30 | 1.00 | 0.14 | 1.00 | 0.07 | 1.00 | 0.36 | 1.00 | 0.10 | 1.00 | |

| 0 | HD | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 |

| 1S | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| LLA | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| 0.5 | HD | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 |

| 1S | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| LLA | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| 0.75 | HD | 33.90 | 1.00 | 33.90 | 1.00 | 33.90 | 1.00 | 35.46 | 1.00 | 35.46 | 1.00 | 35.46 | 1.00 |

| 1S | 47.21 | 1.00 | 47.21 | 1.00 | 47.21 | 1.00 | 46.90 | 1.00 | 46.90 | 1.00 | 46.90 | 1.00 | |

| LLA | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.06 | 1.00 | 0.00 | 1.00 | |

| method | avg | prop | avg | prop | avg | prop | avg | prop | avg | prop | avg | prop | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | HD | 828.22 | 1.00 | 1211.97 | 1.00 | 962.10 | 1.00 | 4615.10 | 1.00 | 5414.49 | 1.00 | 5350.54 | 1.00 |

| 1S | 753.85 | 1.00 | 753.84 | 1.00 | 753.84 | 1.00 | 2836.29 | 0.90 | 1314.46 | 1.00 | 1366.62 | 1.00 | |

| LLA | 1.60 | 1.00 | 1.67 | 1.00 | 1.64 | 1.00 | 1181.62 | 0.76 | 382.17 | 0.82 | 223.32 | 0.94 | |

| 0.5 | HD | 5992.88 | 1.00 | 6008.14 | 1.00 | 5994.86 | 1.00 | 8002.08 | 1.00 | 9530.30 | 1.00 | 9546.21 | 1.00 |

| 1S | 1217.02 | 1.00 | 1202.01 | 1.00 | 1201.30 | 1.00 | 4619.22 | 0.88 | 1473.61 | 1.00 | 1403.36 | 1.00 | |

| LLA | 24.78 | 0.97 | 1.33 | 1.00 | 8.50 | 0.99 | 2123.22 | 0.57 | 576.65 | 0.83 | 232.10 | 0.91 | |

| 0.75 | HD | 12018.61 | 1.00 | 12042.97 | 1.00 | 12042.90 | 1.00 | 13582.93 | 1.00 | 16580.85 | 1.00 | 16569.80 | 1.00 |

| 1S | 2492.18 | 1.00 | 2327.76 | 1.00 | 2330.54 | 1.00 | 8204.45 | 0.60 | 1215.98 | 1.00 | 1181.16 | 1.00 | |

| LLA | 36.95 | 0.98 | 90.89 | 0.97 | 90.69 | 0.96 | 3517.93 | 0.50 | 607.08 | 0.78 | 252.75 | 0.89 | |

| 0 | HD | 1421.70 | 1.00 | 3595.88 | 1.00 | 2296.03 | 1.00 | 1552.11 | 0.98 | 3258.39 | 1.00 | 2231.63 | 1.00 |

| 1S | 7121.11 | 1.00 | 6977.35 | 1.00 | 6976.16 | 1.00 | 7485.99 | 1.00 | 7182.76 | 1.00 | 7182.76 | 1.00 | |

| LLA | 50.48 | 0.99 | 64.69 | 0.99 | 4.59 | 1.00 | 231.48 | 0.97 | 107.36 | 1.00 | 140.97 | 1.00 | |

| 0.5 | HD | 4505.31 | 0.93 | 6764.71 | 0.88 | 4973.51 | 0.98 | 4571.62 | 0.97 | 6473.05 | 0.89 | 6150.70 | 0.96 |

| 1S | 11973.29 | 1.00 | 10301.59 | 1.00 | 10238.21 | 1.00 | 12411.82 | 1.00 | 9674.64 | 1.00 | 9781.43 | 1.00 | |

| LLA | 1622.24 | 0.89 | 661.69 | 0.95 | 622.25 | 0.96 | 1682.66 | 0.89 | 1785.73 | 0.86 | 517.91 | 0.97 | |

| 0.75 | HD | 11166.35 | 0.75 | 16786.90 | 0.57 | 11642.59 | 0.84 | 12834.39 | 0.81 | 14964.11 | 0.66 | 10110.16 | 0.90 |

| 1S | 16953.51 | 1.00 | 9125.82 | 1.00 | 9225.76 | 1.00 | 17174.91 | 0.99 | 8828.81 | 1.00 | 8549.86 | 1.00 | |

| LLA | 6379.56 | 0.50 | 4295.69 | 0.63 | 787.30 | 0.93 | 6904.11 | 0.52 | 3637.68 | 0.74 | 812.28 | 0.94 | |

| 0 | HD | 12.35 | 1.00 | 12.35 | 1.00 | 12.35 | 1.00 | 13.00 | 1.00 | 13.00 | 1.00 | 13.00 | 1.00 |

| 1S | 1072.70 | 1.00 | 1072.70 | 1.00 | 1072.70 | 1.00 | 1114.13 | 1.00 | 1114.13 | 1.00 | 1114.13 | 1.00 | |

| LLA | 0.01 | 1.00 | 0.05 | 1.00 | 0.01 | 1.00 | 0.01 | 1.00 | 0.07 | 1.00 | 0.01 | 1.00 | |

| 0.5 | HD | 28.71 | 1.00 | 28.71 | 1.00 | 28.71 | 1.00 | 0.43 | 1.00 | 0.42 | 1.00 | 0.43 | 1.00 |

| 1S | 6793.73 | 1.00 | 6793.73 | 1.00 | 6793.73 | 1.00 | 6831.01 | 1.00 | 6831.01 | 1.00 | 6831.01 | 1.00 | |

| LLA | 0.38 | 1.00 | 0.54 | 1.00 | 0.49 | 1.00 | 0.43 | 1.00 | 0.58 | 1.00 | 0.57 | 1.00 | |

| 0.75 | HD | 4998.08 | 0.88 | 4963.08 | 0.88 | 4292.65 | 0.97 | 5753.61 | 0.92 | 5772.76 | 0.95 | 5192.19 | 0.98 |

| 1S | 11191.83 | 1.00 | 11188.02 | 1.00 | 12029.12 | 1.00 | 11917.77 | 1.00 | 11971.47 | 1.00 | 12485.14 | 1.00 | |

| LLA | 1217.39 | 0.90 | 1252.65 | 0.89 | 1060.08 | 0.99 | 861.72 | 0.95 | 937.76 | 0.94 | 1018.59 | 0.98 | |

| 0 | HD | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 |

| 1S | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| LLA | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| 0.5 | HD | 6.69 | 1.00 | 6.69 | 1.00 | 6.69 | 1.00 | 5.80 | 1.00 | 5.80 | 1.00 | 5.80 | 1.00 |

| 1S | 2883.52 | 1.00 | 2883.52 | 1.00 | 2883.52 | 1.00 | 2906.35 | 1.00 | 2906.35 | 1.00 | 2906.35 | 1.00 | |

| LLA | 0.03 | 1.00 | 0.20 | 1.00 | 0.03 | 1.00 | 0.02 | 1.00 | 0.20 | 1.00 | 0.02 | 1.00 | |

| 0.75 | HD | 122.19 | 1.00 | 122.19 | 1.00 | 122.19 | 1.00 | 107.93 | 1.00 | 107.93 | 1.00 | 107.93 | 1.00 |

| 1S | 8835.88 | 1.00 | 8835.88 | 1.00 | 8835.87 | 1.00 | 8874.85 | 1.00 | 8874.85 | 1.00 | 8874.84 | 1.00 | |

| LLA | 0.08 | 1.00 | 0.54 | 1.00 | 0.32 | 1.00 | 0.10 | 1.00 | 0.53 | 1.00 | 0.35 | 1.00 | |

| 0 | HD | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 |

| 1S | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| LLA | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| 0.5 | HD | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 |

| 1S | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| LLA | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| 0.75 | HD | 21.76 | 1.00 | 21.76 | 1.00 | 21.76 | 1.00 | 17.70 | 1.00 | 17.70 | 1.00 | 17.70 | 1.00 |

| 1S | 3997.88 | 1.00 | 3997.88 | 1.00 | 3997.88 | 1.00 | 4014.29 | 1.00 | 4014.30 | 1.00 | 4014.29 | 1.00 | |

| LLA | 0.05 | 1.00 | 0.43 | 1.00 | 0.06 | 1.00 | 0.07 | 1.00 | 0.38 | 1.00 | 0.08 | 1.00 | |

4.2 Example 2: Binary Logistic Regression

As in Example 1, we considered the LAS, ALAS, EN, AEN, and SCAD penalties. There are at least two R packages that allow penalization using the LAS and EN penalties: glmpath (Park and Hastie, 2007), which handles binomial and poisson regression using a “predictor-corrector” method, and glmnet (Friedman et al., 2008), which handles binomial and multinomial regression using cyclical coordinate descent. Both methods can be tuned to find the same solutions, so for ease of presentation we only consider the results of glmnet for comparison in the tables and analysis below. The SIS package (Fan et al., 2009a) permits computations with the ALAS, AEN, and SCAD penalties using modifications of the Park and Hastie (2007) code. For SCAD, we compared the results of MIST to the results from the one-step (1S) algorithm (GLM version, Zou and Li, 2008) using the code provided from the authors and the LLA algorithm as implemented in Fan et al. (2009a).

As before, we only considered comparing solutions that use the same combination of tuning parameters; for the present example, the set considered here is , reflecting a need to accommodate the different scaling of the problem. The data generation scheme for this example was loosely based on the simulation study found in Friedman et al. (2008). Binary response data were generated according to a logistic (rather than linear) regression model using , , where is a vector with elements and the remaining components set to zero. Here, follows a -dimensional multivariate normal distribution with zero mean and covariance where correlation matrix P is such that each pair of predictors has the same population correlation We considered three such correlations,

For the simulations, the maximum (across different tuning parameters) average normed difference between the existing and proposed methods, multiplied by are reported for each of the strictly convex cases in the right-most panel of Table 1. As before, these maximums are generally remarkably small, indicating that MIST can recover the same (unique) solutions as the existing algorithms. The results for SCAD are reported in Table 4, which displays the same information as in the corresponding tables from Example 1; the HD comparisons are omitted here as the methodology and code were only developed for the case of penalized least-squares. In the GLM setting, the 1S estimator is computed by applying the LARS (Efron et al., 2004) algorithm to a quadratic approximation of the negative loglikelihood function evaluated at the MLE. Thus, 1S takes ‘one step’ towards minimizing the objective function; in contrast, both MIST and LLA iterate until a stationary point, usually a local minimizer, is found. As in the linear model case, LLA uses glmpath to minimize the surrogate at each step, whereas the MIST algorithm uses a single application of the soft thresholding operator to minimize the surrogate at each step.

In this example, the starting value carried even greater importance in comparison with the linear model setting. In particular, in the case of MIST, the combination of a starting value and small penalty parameter led to solutions with objective function evaluations that were substantially larger in comparison with those obtained using either and Such behavior may be directly attributed to the fact that the ML and 1S starting values either minimize or nearly minimize the negative loglikelihood portion of the objective function, the dominant term in the objective function when is “small.” In contrast, a starting value led to the best minimization performance for “large” ; upon reflection, this is also not very surprising, since large penalties induce greater sparsity and is the sparsest possible solution.

There were a few settings in which the 1S estimator resulted in a lower objective function evaluation in comparison with applying MIST started at . This reflects the fact that several local minima can exist for non-convex penalties like SCAD. In addition, and as was observed before, using the 1S solution as a starting value always led to MIST finding a solution with a lower evaluation of the objective function in comparison with that provided by the 1S solution. Regarding the use of LLA, which also requires a starting value specification, we again examined the cases for which LLA resulted in lower objective function evaluations. For these cases, all MIST solutions were LLA solutions, and all LLA solutions were MIST solutions with the exception of one. Hence, both methods find valid, if often different, solutions, a behavior that we again attribute to the differences in paths taken towards a solution.

| method | avg | prop | avg | prop | avg | prop | avg | prop | avg | prop | avg | prop | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1S | 26.50 | 0.27 | 0.39 | 1.00 | 0.39 | 1.00 | 31.70 | 0.42 | 0.22 | 1.00 | 0.18 | 1.00 |

| LLA | 18.55 | 0.68 | 0.15 | 1.00 | 0.13 | 1.00 | 17.31 | 0.76 | 0.22 | 1.00 | 0.11 | 1.00 | |

| 0.5 | 1S | 33.90 | 0.15 | 0.08 | 1.00 | 0.07 | 1.00 | 35.43 | 0.26 | 0.10 | 1.00 | 0.07 | 1.00 |

| LLA | 27.65 | 0.64 | 0.01 | 1.00 | 0.00 | 1.00 | 18.45 | 0.82 | 0.10 | 1.00 | 0.00 | 1.00 | |

| 0.75 | 1S | 56.29 | 0.04 | 0.06 | 1.00 | 0.05 | 1.00 | 42.85 | 0.23 | 0.05 | 1.00 | 0.04 | 1.00 |

| LLA | 46.48 | 0.71 | 0.05 | 1.00 | 0.00 | 1.00 | 26.05 | 0.82 | 0.04 | 1.00 | 0.00 | 1.00 | |

| 0 | 1S | 945.60 | 0.11 | 30.65 | 1.00 | 31.42 | 1.00 | 1318.20 | 0.02 | 8.61 | 1.00 | 8.61 | 1.00 |

| LLA | 416.15 | 0.64 | 5.49 | 0.93 | 1.86 | 0.99 | 406.62 | 0.72 | 0.98 | 1.00 | 0.49 | 1.00 | |

| 0.5 | 1S | 1082.65 | 0.00 | 23.60 | 1.00 | 22.97 | 1.00 | 1088.23 | 0.01 | 5.62 | 1.00 | 5.75 | 1.00 |

| LLA | 427.10 | 0.72 | 1.33 | 0.99 | 0.03 | 1.00 | 398.05 | 0.74 | 0.56 | 0.99 | 0.16 | 1.00 | |

| 0.75 | 1S | 1462.74 | 0.00 | 16.81 | 0.98 | 17.37 | 1.00 | 1629.73 | 0.00 | 5.53 | 0.99 | 4.97 | 1.00 |

| LLA | 548.07 | 0.79 | 1.71 | 0.97 | 0.82 | 1.00 | 578.09 | 0.79 | 1.73 | 0.99 | 0.06 | 1.00 | |

| 0 | 1S | 1845.64 | 0.99 | 501.45 | 1.00 | 530.14 | 1.00 | 9575.27 | 0.82 | 252.36 | 1.00 | 263.41 | 1.00 |

| LLA | 75.94 | 0.99 | 93.46 | 0.73 | 76.33 | 0.98 | 97.80 | 0.91 | 27.73 | 0.96 | 13.86 | 0.99 | |

| 0.5 | 1S | 4351.14 | 0.33 | 433.10 | 1.00 | 473.27 | 1.00 | 8323.46 | 0.98 | 171.08 | 1.00 | 181.11 | 1.00 |

| LLA | 394.16 | 0.60 | 125.51 | 0.74 | 74.17 | 0.94 | 106.69 | 0.87 | 15.59 | 0.96 | 9.10 | 1.00 | |

| 0.75 | 1S | 5041.69 | 0.97 | 359.74 | 1.00 | 379.26 | 1.00 | 7907.54 | 1.00 | 156.65 | 0.99 | 164.34 | 1.00 |

| LLA | 337.48 | 0.90 | 124.48 | 0.67 | 46.58 | 0.91 | 24.37 | 0.98 | 31.31 | 0.95 | 2.19 | 1.00 | |

| 0 | 1S | 4095.33 | 1.00 | 818.64 | 1.00 | 815.48 | 1.00 | 8626.86 | 1.00 | 834.01 | 1.00 | 832.92 | 1.00 |

| LLA | 0.00 | 1.00 | 0.04 | 1.00 | 15.14 | 1.00 | 0.00 | 1.00 | 73.78 | 0.89 | 149.55 | 0.98 | |

| 0.5 | 1S | 4330.64 | 1.00 | 660.87 | 1.00 | 682.83 | 1.00 | 7626.58 | 1.00 | 628.29 | 1.00 | 718.12 | 1.00 |

| LLA | 4.56 | 1.00 | 32.36 | 0.93 | 34.80 | 0.99 | 0.00 | 1.00 | 115.84 | 0.85 | 121.60 | 0.98 | |

| 0.75 | 1S | 4536.24 | 1.00 | 626.38 | 1.00 | 693.65 | 1.00 | 7457.80 | 1.00 | 550.76 | 1.00 | 618.94 | 1.00 |

| LLA | 0.00 | 1.00 | 81.21 | 0.87 | 87.10 | 0.99 | 0.00 | 1.00 | 88.95 | 0.86 | 62.41 | 0.98 | |

| 0 | 1S | 3712.07 | 1.00 | 2888.10 | 0.81 | 3712.07 | 1.00 | 4346.96 | 1.00 | 4346.96 | 1.00 | 4346.96 | 1.00 |

| LLA | 0.00 | 1.00 | 0.04 | 1.00 | 0.01 | 1.00 | 0.00 | 1.00 | 0.01 | 1.00 | 0.01 | 1.00 | |

| 0.5 | 1S | 3768.77 | 1.00 | 3167.21 | 0.98 | 3602.53 | 1.00 | 3781.29 | 1.00 | 3781.29 | 1.00 | 3781.29 | 1.00 |

| LLA | 0.00 | 1.00 | 42.80 | 0.99 | 70.75 | 1.00 | 0.00 | 1.00 | 0.01 | 1.00 | 0.01 | 1.00 | |

| 0.75 | 1S | 3825.82 | 1.00 | 2542.80 | 0.97 | 3076.24 | 1.00 | 4331.74 | 1.00 | 4331.74 | 1.00 | 4331.74 | 1.00 |

| LLA | 0.00 | 1.00 | 404.72 | 0.83 | 387.72 | 0.86 | 0.00 | 1.00 | 0.01 | 1.00 | 0.01 | 1.00 | |

| 0 | 1S | 54.18 | 1.00 | 54.18 | 1.00 | 54.18 | 1.00 | 61.54 | 1.00 | 61.54 | 1.00 | 61.54 | 1.00 |

| LLA | 0.00 | 1.00 | 0.01 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.02 | 1.00 | 0.00 | 1.00 | |

| 0.5 | 1S | 40.38 | 1.00 | 40.38 | 1.00 | 40.38 | 1.00 | 49.01 | 1.00 | 49.01 | 1.00 | 49.01 | 1.00 |

| LLA | 0.00 | 1.00 | 0.01 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

| 0.75 | 1S | 32.85 | 1.00 | 32.85 | 1.00 | 32.85 | 1.00 | 38.36 | 1.00 | 38.36 | 1.00 | 38.36 | 1.00 |

| LLA | 0.00 | 1.00 | 0.01 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | |

4.3 Effectiveness of SQUAREM2

We explored the effectiveness of SQUAREM2, defined in Section 3.3, when applied to several simulated datasets taken from the previous two simulation studies. Table 5 indicates the relative reduction in elapsed time (‘RRT’) and numbers of MM updates, i.e., invocations of mapping , required for the original and SQUAREM2-accelerated algorithms to converge for five randomly chosen simulation datasets across the five penalty functions. The SQUAREM2 algorithm converged without difficulty in these cases and required substantially fewer MM updates than the original algorithm; the percent reduction in time was as high as 96%. We remark here that the regularity conditions imposed in Roland and Varadhan (2005) and Varadhan and Roland (2008), particularly smoothness conditions, are not satisfied in this particular class of examples. Hence, while the simulation results are certainly very promising, the question of convergence (and its associated rate) of SQUAREM2 in this class of problems continues to remain an interesting open problem.

| LAS | ALAS | EN | AEN | SCAD | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Dataset | RRT | #orig | #sqm2 | RRT | #orig | #sqm2 | RRT | #orig | #sqm2 | RRT | #orig | #sqm2 | RRT | #orig | #sqm2 |

| 62 | 0.67 | 260 | 62 | 0.81 | 169 | 44 | 0.63 | 46 | 26 | 0.82 | 42 | 23 | 0.91 | 485 | 68 |

| 71 | 0.76 | 221 | 59 | 0.75 | 163 | 41 | 0.67 | 49 | 29 | 0.62 | 44 | 29 | 0.83 | 302 | 65 |

| 86 | 0.67 | 271 | 68 | 0.70 | 149 | 44 | 0.67 | 51 | 29 | 0.75 | 43 | 26 | 0.93 | 987 | 104 |

| 95 | 0.86 | 317 | 74 | 0.88 | 187 | 41 | 0.92 | 49 | 29 | 0.73 | 46 | 26 | 0.90 | 500 | 71 |

| 88 | 0.88 | 330 | 68 | 0.87 | 162 | 41 | 0.78 | 51 | 29 | 0.77 | 45 | 26 | 0.90 | 528 | 77 |

| 62 | 0.90 | 2059 | 242 | 0.89 | 589 | 92 | 0.65 | 68 | 35 | 0.75 | 64 | 29 | 0.88 | 594 | 101 |

| 71 | 0.93 | 1426 | 164 | 0.93 | 838 | 83 | 0.76 | 77 | 32 | 0.70 | 71 | 32 | 0.94 | 2608 | 215 |

| 86 | 0.90 | 1351 | 212 | 0.92 | 956 | 98 | 0.59 | 77 | 38 | 0.79 | 69 | 32 | 0.92 | 1038 | 110 |

| 95 | 0.93 | 1500 | 167 | 0.86 | 367 | 71 | 0.67 | 72 | 35 | 0.74 | 68 | 29 | 0.90 | 663 | 92 |

| 88 | 0.92 | 1547 | 185 | 0.90 | 716 | 101 | 0.60 | 70 | 32 | 0.68 | 66 | 32 | 0.92 | 1798 | 203 |

| 62 | 0.93 | 4928 | 431 | 0.96 | 6227 | 272 | 0.89 | 3201 | 359 | 0.93 | 3316 | 236 | 0.95 | 22044 | 1442 |

| 71 | 0.92 | 4195 | 416 | 0.95 | 5045 | 239 | 0.90 | 2796 | 281 | 0.94 | 2843 | 170 | 0.95 | 16225 | 1052 |

| 86 | 0.92 | 4488 | 470 | 0.95 | 5449 | 242 | 0.92 | 2971 | 257 | 0.93 | 3044 | 206 | 0.95 | 20133 | 1193 |

| 95 | 0.93 | 4553 | 374 | 0.94 | 5419 | 341 | 0.92 | 3059 | 269 | 0.95 | 3096 | 152 | 0.95 | 15250 | 1064 |

| 88 | 0.92 | 5212 | 527 | 0.95 | 6850 | 371 | 0.91 | 3237 | 314 | 0.94 | 3393 | 203 | 0.96 | 26477 | 1367 |

| 62 | 0.88 | 4334 | 674 | 0.91 | 3573 | 377 | 0.85 | 3055 | 575 | 0.90 | 2435 | 293 | 0.95 | 88994 | 5687 |

| 71 | 0.91 | 3805 | 446 | 0.92 | 3046 | 281 | 0.85 | 2761 | 536 | 0.89 | 2194 | 281 | 0.94 | 82615 | 5588 |

| 86 | 0.87 | 3615 | 602 | 0.91 | 2900 | 329 | 0.87 | 2653 | 434 | 0.92 | 2110 | 185 | 0.93 | 42652 | 3686 |

| 95 | 0.89 | 3870 | 554 | 0.90 | 3121 | 380 | 0.90 | 2820 | 338 | 0.89 | 2264 | 314 | 0.94 | 40002 | 3095 |

| 88 | 0.88 | 4177 | 641 | 0.94 | 3395 | 251 | 0.87 | 2972 | 482 | 0.91 | 2415 | 242 | 0.94 | 77484 | 5885 |

5 Example: Identifying genes associated with the survival of lymphoma patients

Diffuse large-B-cell lymphoma (DLBCL) is an aggressive type of non-Hodgkins lymphoma and is one of the most common forms of lymphoma occurring in adults. Rosenwald et al. (2002) utilized Lymphochip DNA microarrays, specialized to include genes known to be preferentially expressed within the germinal centers of lymphoid organs, to collect and analyze gene expression data from 240 biopsy samples of DLBCL tumors. For each subject, 7399 gene expression measurements were obtained. The expression profiles along with corresponding patient information can be downloaded from their supplemental website http://llmpp.nih.gov/DLBCL/. Since the original profiles had some missing expression measurements, we used the dataset subsequently analyzed by Li and Gui (2004) which estimated the missing values using a nearest neighbor approach. During the time of followup, 138 patient deaths were observed with median death time of 2.8 years.

Rosenwald et al. (2002) used hierarchical clustering to group the genes into four gene-expression signatures: Proliferation (PS), which includes cell-cycle control and checkpoint genes, and DNA synthesis and replication genes; Major Histocompatibility Complex ClassII (MHC), which includes genes involved in antigen presentation; Lymph Node (LNS), which includes genes encoding for known markers of monocytes, macrophages, and natural killer cells; and Germinal Center B (GCB), which includes genes that are characteristic of germinal center B cells; see Alizadeh et al. (2000) for more information on gene signatures. Based on the gene clusters, they built a Cox proportional hazards model (Cox, 1972, 1975) to predict survival outcomes in the DLBCL patients. Subsequently, this dataset has been analyzed numerous times, typically to evaluate methods related to subgroup identification and/or survival prediction (e.g., Li and Gui, 2004; Gui and Li, 2005b, a; Li and Luan, 2005; Annest et al., 2009; Engler and Li, 2009; Tibshirani, 2009).

Here, we instead focus on the performance of two different penalties, namely SCAD and MCP, with regard to the identification of genes associated with DLBCL survival. The simulation results of Zhang (2007) suggest that MCP has superior selective accuracy over the SCAD penalty, at least for the case of a linear model. There, selection accuracy was measured as the proportion of simulation replications with correct classification of both the zero and non-zero coefficients, with MCP outperforming SCAD in all simulation settings. To illustrate the utility and flexibility of the MIST algorithm, we reanalyzed the DLBCL data, fitting a penalized Cox regression model respectively using SCAD and MCP penalty functions, and running these procedures in combination with the Iterative Sure Independence Screening procedure (ISIS, Fan et al., 2009b) in order to ensure that the dimension of the parameter space was maintained at a manageable level. For SCAD, we considered both the 1S and LLA estimators. The existing optimization functions provided in the SIS package for the ISIS procedure were used for the 1S estimator, whereas relevant modifications to the ISIS code were made in order to accommodate the fully iterative LLA and MCP estimators. Optimization at each step of the ISIS algorithm in the case of the MCP penalty utilized the MIST algorithm, as we are aware of no other algorithm capable of fitting the Cox regression model subject to MCP penalization. The default settings in the SIS package were used to determine the maximum number of predictors () and to define the additional ISIS parameters (e.g., use of the unpenalized MLE as a starting value, ranking method, tuning parameter selection) for all three analyses (1S-SCAD, LLA-SCAD, MIST-MCP). The parameter was set to 3.7 for all analyses; hence, only the selection of required any tuning.

Table 6 displays the 11 genes identified by at least one of the three analyses. The x’s in a given column indicate the genes with non-zero coefficients resulting from the corresponding penalization. The final column provides references for genes previously linked to DLBCL in the literature. Genes belonging to the original Rosenwald et al. (2002) gene expression signatures are indicated with parenthetical initials. Note that the references provided are not meant to be an exhaustive list, but instead to demonstrate the relevance of certain genes and/or their altered expression levels in DLBCL survival.

Interestingly, the LLA-SCAD and MIST-MCP penalizations selected the same subset of genes, with a nearly a complete overlap with those selected from the 1S-SCAD penalization. The number of genes selected in each case is 10, the maximum specified by ISIS; 9 of these were shared across the three penalizations. According to NCBI Entrez Gene search (http://www.ncbi.nlm.nih.gov/), many of these genes are biologically relevant. For example, CDK7 codes for a protein that regulates cell cycle progression and is represented in the Proliferation Signature, although reported under a different Lymphochip ID as this gene was spotted multiple times on the array. Also members of the Proliferation Signature are SEPT1, coding for a protein involved in cytokinesis, and BUB3, coding for a mitotic checkpoint protein. DNTTIP2 regulates transcriptional activity of DNTT, a gene for a protein expressed in a restricted population of normal and malignant pre-B and pre-T lymphocytes during early differentiation. HLA-DRA, a member of the MHC Signature, plays a central role in the immune system and is expressed in antigen presenting cells, such as B lymphocytes, dendritic cells, macrophages. From the GCB Signature, the ESTs weakly similar to thyroxine-binding globulin precursor is highly cited. Additionally, RFTN1 plays a pivotal role in regulating B-cell antigen receptor-mediated signaling (Saeki et al., 2003).

A description of AI568329 was not provided in the original dataset, thus its function is unknown. Similarly, although cited at least twice, a description for AA830781 was also not provided in the original dataset. However, both of these may be related to lymphoma or risk of death from lymphoma, as it is possible that these genes (and potentially others) were selected because of coexpression or correlation with other relevant genes.

Interestingly the two genes not commonly identified across the three penalizations were both cited in Martinez-Climent et al. (2003). They found altered gene expression of TSC22D3 and ITGAL (both involved in a variety of immune phenomena) in one case who initially presented with follicle center lymphoma and subsequently transformed to DLBCL.

| ID | Name (Symbol) | SCAD | MCP | References | |

| 1S | LLA | ||||

| 27774 | cyclin-dependent kinase 7 (CDK7) | x | x | x | Rosenwald et al. (2002) (PS), Ma and Huang (2007) |

| Binder and Schumacher (2008, 2009) | |||||

| 31242 | acidic 82 kDa protein mRNA (DNTTIP2) | x | x | x | Binder and Schumacher (2008, 2009) |

| 31981 | septin 1 (SEPT1) | x | x | x | Rosenwald et al. (2002) (PS), Li and Luan (2005) |

| Sinisi et al. (2006), Sha et al. (2006) | |||||

| Zhang and Zhang (2007),Annest et al. (2009) | |||||

| Binder and Schumacher (2008, 2009) | |||||

| 29652 | BUB3 budding uninhibited by benzimidazoles 3 (BUB3) | x | x | x | Rosenwald et al. (2002) (PS) |

| 27731 | major histocompatibility complex, | x | x | x | Rosenwald et al. (2002) (MHC),Li and Luan (2005) |

| class II, DR alpha (HLA-DRA) | Gui and Li (2005a, b),Sohn et al. (2009) | ||||

| Binder and Schumacher (2009) | |||||

| 24376 | ESTs, Weakly similar to A47224 | x | x | x | Rosenwald et al. (2002) (GCB),Ando et al. (2003) |

| thyroxine-binding globulin precursor | Gui and Li (2005a, b),Li and Luan (2005) | ||||

| Annest et al. (2009), Sohn et al. (2009) | |||||

| Binder and Schumacher (2008, 2009) | |||||

| 22162 | delta sleep inducing peptide, immunoreactor (TSC22D3) | x | x | Martinez-Climent et al. (2003) | |

| 23862 | (AI568329) ESTs | x | x | x | |

| 24271 | integrin, alpha L (ITGAL) | x | Martinez-Climent et al. (2003) | ||

| 33358 | (AA830781) | x | x | x | Li and Luan (2005) |

| Binder and Schumacher (2009) | |||||

| 32679 | KIAA0084 protein (RFTN1) | x | x | x | Gui and Li (2005b), Sha et al. (2006) |

| Zhang and Zhang (2007),Annest et al. (2009) | |||||

| Binder and Schumacher (2008, 2009) | |||||

The results of this analysis demonstrate equivalence in selection performance between MCP and LLA-SCAD for the case of Cox proportional hazards model. Increasing the maximum number of predictors to again resulted in equivalent selection performance between MCP and LLA-SCAD, with 21 predictors ultimately selected (results not shown). The 1S estimator also resulted in the selection of 21 predictors, but with increased dissimilarity between MCP/LLA-SCAD and 1S: only 13 of the 21 genes were selected by all three methods. It should be noted that Zhang (2007) did not use any form iterative variable selection (e.g., ISIS) in his comparisons between SCAD and MCP for the case of the linear model; in addition, Zhang (2007) fixed values for both penalty parameters in his simulations and also did not use . Thus, use of the ISIS procedure, the particular method used for selecting , and the use of (as suggested in Fan et al. (2009b)) in both the MCP and SCAD penalties may all play a role in the results summarized above.

6 Discussion

This paper proposed a versatile and general algorithm capable of dealing with a wide variety of nonsmoothly penalized objective functions, including but not limited to all presently popular combinations of data fidelity and penalty functions. We established a suitable convergence theory, as well as new results on the convergence of general MM algorithms. We also demonstrated the remarkable effectiveness of the SQUAREM2 acceleration procedure in these problems as tool for accelerating the slow but steady convergence of the proposed class of MM algorithms. Beyond specification of the penalty parameter(s) virtually no effort was expended in tuning or otherwise specializing the MIST algorithm for solving a given problem. Thus, at the expense of greater analytical work, the convergence rate of the MIST algorithm can likely be improved. Through the use relaxation techniques and other methods for controlling the step-size behavior (e.g., line-searches) of MIST, we further expect that the local nature of the convergence theory presented here can be made global in nature.

The simulation results of this paper highlight the fact that nonconvex penalties tend to endow the corresponding objective function with multiple local minima. The resulting sensitivity of computational algorithms to the choice of starting value, while known, has arguably been deemphasized in the current literature. In this regard, the one-step method of Zou and Li (2008) provides a meritorious choice of starting value for fully iterative SCAD-based algorithms. In addition to being unique under mild regularity conditions, it is easily generalized to other nonconvex penalties, such as MCP. Unfortunately, the utility of this approach for identifying starting values is also limited to settings where , for the justification of the 1S estimator relies heavily on the use of the unpenalized MLE as its starting value.

The simulated examples in this paper only consider settings with , mainly to ensure that is strictly convex. Specifying in the ridge-like penalty term ensures that is strictly convex provided only that is convex, as might be encountered in cases where . Thus, for example, one might consider combining the ridge term with any penalty satisfying condition (P1) (e.g., SCAD), providing alternatives to the elastic net penalty; our results on the convergence of the proposed algorithms to some stationary point of the objective function would continue to apply in this setting. It would be interesting to investigate the statistical properties of estimators derived under such combinations in settings where but , with denoting the number of “important” predictors.

References

- Alizadeh et al. (2000) Alizadeh, A. A., Eisen, M. B., Davis, R. E., Ma, C., Lossos, I. S., Rosenwald, A., Boldrick, J. C., Sabet, H., Tran, T., Yu, X., Powell, J. I., Yang, L., Marti, G. E., Moore, T., Hudson, J., Lu, L., Lewis, D. B., Tibshirani, R., Sherlock, G., Chan, W. C., Greiner, T. C., Weisenburger, D. D., Armitage, J. O., Warnke, R., Levy, R., Wilson, W., Grever, M. R., Byrd, J. C., Botstein, D., Brown, P. O. and Staudt, L. M. (2000). Distinct types of diffuse large B-cell lymphoma identified by gene expression profiling. Nature, 403 503–511.

- Andersen et al. (1993) Andersen, P. K., Borgan, O., Gill, R. D. and Keiding, N. (1993). Statistical Models Based on Counting Processes. Springer-Verlag, New York.

- Ando et al. (2003) Ando, T., Suguro, M., Kobayashi, T., Seto, M. and Honda, H. (2003). Multiple fuzzy neural network system for outcome prediction and classification of 220 lymphoma patients on the basis of molecular profiling. Cancer Sci., 94 906–913.

- Annest et al. (2009) Annest, A., Bumgarner, R., Raftery, A. and Yeung, K. Y. (2009). Iterative Bayesian Model Averaging: a method for the application of survival analysis to high-dimensional microarray data. BMC Bioinformatics, 10 72.

- Antoniadis et al. (2009) Antoniadis, A., Gijbels, I. and Nikolova, M. (2009). Penalized likelihood regression for generalized linear models with nonquadratic penalties. Annals of the Instutute of Statistical Mathematics.

- Becker et al. (1997) Becker, M. P., Yang, I. and Lange, K. (1997). EM algorithms without missing data. Statistical Methods in Medical Research, 6 38–54.

- Binder and Schumacher (2008) Binder, H. and Schumacher, M. (2008). Allowing for mandatory covariates in boosting estimation of sparse high-dimensional survival models. BMC Bioinformatics, 9 14.

- Binder and Schumacher (2009) Binder, H. and Schumacher, M. (2009). Incorporating pathway information into boosting estimation of high-dimensional risk prediction models. BMC Bioinformatics, 10 18.

- Bohning and Lindsay (1988) Bohning, D. and Lindsay, B. (1988). Monotonocity of quadratic-approximation algorithms. Ann. Inst. Statist. Math., 40 641–663.

- Boyd and Vandenberghe (2004) Boyd, S. and Vandenberghe, L. (2004). Convex Optimization. Cambridge University Press.

- Chrétien and Hero (2008) Chrétien, S. and Hero, A. O. (2008). On EM algorithms and their proximal generalizations. ESAIM Journ. on Probability and Statistics, 12 308–326.

- Combettes and Wajs (2005) Combettes, P. and Wajs, V. (2005). Signal recovery by proximal forward-backward splitting. Multiscale Model. Simul.

- Cox (1972) Cox, D. R. (1972). Regression models and life-tables (with discussion). J. Roy. Statist. Soc. Ser. B, 34 187–220.

- Cox (1975) Cox, D. R. (1975). Partial likelihood. Biometrika, 62 269–276.

- Daubechies et al. (2004) Daubechies, I., Defreise, M. and De Mol, C. (2004). An iterative thresholding algorithm for linear inverse problems with a sparsity constraint. Communications on Pure and Applied Mathematics 1413–1457.

- De Mol et al. (2008) De Mol, C., De Vito, E. and Rosasco, L. (2008). Elastic-net regularization in learning theory. arXiv.