Neyman-Pearson Detection of a

Gaussian Source

using Dumb Wireless Sensors

Abstract

We investigate the performance of the Neyman-Pearson detection of a stationary Gaussian process in noise, using a large wireless sensor network (WSN). In our model, each sensor compresses its observation sequence using a linear precoder. The final decision is taken by a fusion center (FC) based on the compressed information. Two families of precoders are studied: random iid precoders and orthogonal precoders. We analyse their performance in the regime where both the number of sensors and the number of samples per sensor tend to infinity at the same rate, that is, . Contributions are as follows. 1) Using results of random matrix theory and on large Toeplitz matrices, it is proved that the miss probability of the Neyman-Pearson detector converges exponentially to zero, when the above families of precoders are used. Closed form expressions of the corresponding error exponents are provided. 2) In particular, we propose a practical orthogonal precoding strategy, the Principal Frequencies Strategy (PFS), which achieves the best error exponent among all orthogonal strategies, and which requires very few signaling overhead between the central processor and the nodes of the network. 3) Moreover, when the PFS is used, a simplified low-complexity testing procedure can be implemented at the FC. We show that the proposed suboptimal test enjoys the same error exponent as the Neyman-Pearson test, which indicates a similar asymptotic behaviour of the performance. We illustrate our findings by numerical experiments on some examples.

I Introduction

The design of powerful tests allowing to detect the presence of a stochastic signal using large WSN’s is a crucial issue in a wide range of applications. We investigate the Neyman-Pearson detection of a Gaussian signal using a wireless network of sensors. Each sensor observes a finite sample of the signal of interest, corrupted by additive noise, and then forwards some information towards the FC which takes the final decision. Neyman-Pearson detection of Gaussian signals using large sensor networks has been thoroughly investigated in the literature (see for instance [1, 2] and references therein). In such works, the FC is assumed to have a perfect knowledge of the observation sequence of each sensor. Unfortunately, in a WSN, the amount of information forwarded by each sensor node to the FC is usually limited, due to channel capacity constraints. Thus, in practice, each sensor node must compress its information in some way before transmission to the FC. This compression step of course degrades the performance of the detection. A large number of works has been devoted to the determination of relevant compression strategies, essentially within the framework of distributed detection [3, 4]. In these works, the data is locally processed by each sensor: Typically, a local Neyman-Pearson test is made by each node, based on the knowledge of the probabilistic law of the source to be detected. Unfortunately, such approaches require at the same time that each sensor possesses a significant computational ability allowing involved processing of its data, and that each sensor has a full knowledge of the source statistics. On the opposite, this paper investigates the case of dumb WSN. By this term, we refer to the case where:

-

•

Individual sensor nodes are not aware of their mission and their environment. They process the observed data with no or few instructions from the central processor.

-

•

The processing abilities of each sensor node are limited due either to hardware or energy constraints.

Dumb WSN are of practical interest because they are simple, flexible (i.e., easily reconfigurable as a function of the sensor network’s mission) and avoid an excess of signaling overhead in the network.

The aim of this paper is to propose and to study different compressing strategies which satisfy the above constraints and which are attractive in terms of detection performance. The paper is organized as follows. Section II introduces the signal model. Each sensor is assumed to observe noisy samples of a stationary (correlated) Gaussian source. The spectral density of the source is known at the FC but is unknown at the sensor nodes. The aim is to detect the presence of the source. To that end, each node forwards a compressed version of its observed sequence to the FC. In our model, the latter compression is achieved through simple (linear) processing of the data, allowing this way for low cost implementation. We refer to this step as linear precoding. Section III introduces the problem of the detection of the presence of the source (hypothesis ) versus the hypothesis that only thermal noise is observed (hypothesis ). It is well known that a uniformly most powerful (UMP) test is obtained by the celebrated Neyman-Pearson procedure. The corresponding test is derived in Subsection III-A. Intuitively, the good detection performance of the Neyman-Pearson test fundamentally relies on the relevant selection of the linear precoders used at the sensor nodes. Useful families of linear precoders are introduced, namely random iid precoders and orthogonal precoders. The detection performance associated with each of these families is studied in the asymptotic regime where both the number of sensors and the number of observations per sensor tend to infinity at the same rate (, where ). More precisely, we show in Section IV that for any fixed , the miss probability of the NP test of level converges exponentially to zero. Error exponents are characterized and compared for the precoding strategies of interest. In particular, it is proved that the so-called Principal Frequencies Strategy (PFS) achieves the best error exponent among all orthogonal strategies. Numerical computations of all the obtained error exponents on some examples conclude this section. In the case where PFS is used, a suboptimal (non UMP) test is proposed in Section V. Based on the proof of a Large Deviation Principle governing the proposed test statistics, it is shown that our suboptimal test achieves the same error exponent as the Neyman-Pearson test. Finally, Section VI is devoted to the simulations.

Notations

Column vectors are represented by bold symbols. Notation denotes the Euclidean norm of vector . We denote by the Lebesgue measure restricted to . For any function , we use notation for the inverse image of , and we denote by the image measure of by , i.e. which composes with . For any square matrix , denotes its spectral radius. Finally, denotes the identity matrix.

II The Framework

II-A Observation model at the sensor nodes

Consider a set of sensors whose aim is to detect the presence of a certain source signal . Each sensor collects noisy samples of the source signal. We assume that . Denote by the data vector observed by sensor . For each , we consider the following signal model:

| (1) |

where contains the time samples extracted from a zero mean stationary Gaussian process with known spectral density function , . Vector is a zero mean white Gaussian process which stands for the thermal noise of sensor . We denote by the variance of which is assumed to be the same for all . Random vectors , are supposed to be independent. In the usual framework of Gaussian source detection, the aim is to detect whether the signal of interest is present. Formally, this reduces to the following hypothesis testing problem:

In this paper, we make the following technical assumptions on the spectral density :

- A1.

-

The spectral density is continuous on .

- A2.

-

Measure does not put mass on points.

Assumption A2 says that cannot be constant over a set of positive Lebesgue measure (say, an interval of positive length). This e.g. rules out a white noise for . On the other hand any ARMA process that is not a white noise satisfies Assumptions A1 and A2.

II-B Assumptions and constraints on the network

We assume that the decision is taken by a distant node (the fusion center). The latter is supposed to have a perfect knowledge of the noise variance and of the spectral density of the signal to be detected. In this paper, we are interested in WSN satisfying the following constraints.

II-B1 Communication constraint

In an ideal WSN architecture, each sensor would transmit all available observations to the FC. Unfortunately, perfect forwarding of the whole information sequence by each sensor is impractical in a large number of situations, the amount of information transmitted by each sensor node to the fusion center being usually limited. In this paper, we consider the case where only a compressed version of is likely to be forwarded. More precisely, we assume that each sensor forwards a single scalar to the fusion center, where is a certain mapping of the sequence received by sensor .

II-B2 Signaling overhead constraint

Depending on the particular mission of the network or on the particular spectral density to be detected, the network should be easily reconfigurable using a limited number of feedback bits from the fusion center to the sensors. In the sequel we assume that the spectral density is known at the fusion center but is unknown (or at most partially known) at the sensor nodes.

II-B3 Complexity constraint

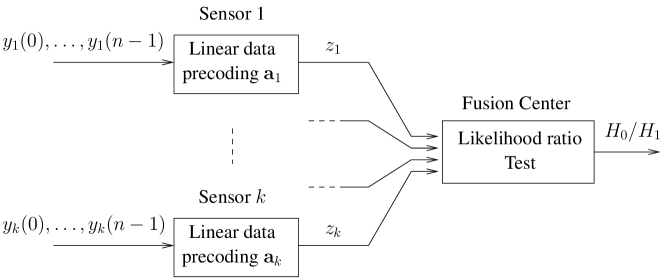

Only low complexity data processing is likely to be implemented at the sensors’ side. More precisely, we assume that each sensor node forwards a linear combination

| (2) |

of its observation sequence to the fusion center, where is a vector to be determined. Figure 1 provides an illustration of the sensing scheme.

Such a set of vectors will be refered to as a linear precoder. The matrix will be refered to as the precoding matrix.

III Likelihood Ratio Test

III-A Expression of the Likelihood Ratio

We denote by and the probability under and and by and the corresponding expectations. Denote by the available observation vector at the fusion center, where for each , is defined by (2). We denote by and the joint probability density function of under hypotheses and respectively. Due to the celebrated Neyman-Pearson’s Lemma, the Likelihood Ratio Test (LRT) is uniformly most powerful. The LRT rejects the null hypothesis for large values of the log-likelihood ratio (LLR) defined by:

| (3) |

In the above definition, the lowerscript has been introduced to recall that the distribution of the random variable depends on the particular choice of the precoding matrix . We now derive a closed form expression of the LLR . It is worth noting that multiplying each by a non-zero constant does not modify the performance of the likelihood ratio test. Hence we may normalize so that for each in the following. In this case, is a zero mean Gaussian random vector with covariance matrix

under hypothesis , where represents the covariance matrix of vector . Matrix is the Toeplitz matrix associated to the spectral density of process , namely,

| (4) |

Under , the covariance matrix of vector simply coincides with . Using these remarks, it is straightforward to show that

| (5) |

In the sequel, we assume as usual that the threshold of the test, say , is fixed in such a way that the probability of false alarm (PFA) does not exceed a level (), which reads

| (6) |

We now analyze the miss probability of the above LLR test as a function of .

III-B Introduction to error exponents

Let denote the miss probability of the LLR test with level based on the observation :

where the inf is taken over all threshold values verifying the PFA constraint (6). The miss probability is generally the key metric to characterize the performance of hypothesis tests. Unfortunately, an exact expression of the miss probability as a function of is difficult to obtain in the general case. Following [5], we thus analyze the asymptotic behaviour of the miss probability as the number of available observations tends to infinity. More precisely, we study the asymptotic regime where both the number of sensors and the number of observations per sensor tend to infinity at the same rate:

| (7) |

where . Any sequence of precoding matrices will be refered to as a linear strategy. Loosely speaking, we will prove that, at least for certain linear strategies of interest, the miss probability behaves as

in the asymptotic regime (7), where is a certain constant which depends on the linear strategy but, as a matter of fact, does not depend on the level . Such a constant is called the error exponent. It is a key indicator of the way the power of the test is influenced by the chosen linear strategy. More formally, we define for each ,

| (8) | |||||

| (9) |

and we define the error exponent of as as soon as (8) and (9) coincide. In the sequel, our aim is therefore to determine linear precoding strategies having a large error exponent (and for which is well-defined, of course). The following Lemma (see [5]) provides a practical way to evaluate error exponents.

Lemma 1 ([5]).

The following inequalities hold:

In particular if, under hypothesis , converges in probability to a deterministic constant , then is necessary equal to this limit.

According to the above lemma, the asymptotic performance analysis of the LLR test reduces to the characterization of the limit in probability of the normalized LLR as , as soon as this limit exists. Moreover, in this case, the error exponent is independent from level .

III-C Some families of precoders

A natural approach to design relevant precoders would be to characterize the linear strategies which maximize the limit in probability (if it exists) of the LLR as . Ideally, this would lead to the strategies with maximal error exponent. Unfortunately, such a characterization is difficult and would moreover lead to linear strategies which would deeply depend on the spectral density of the signal to be detected. The practical implementation of such optimal linear strategies would typically require to communicate the whole function to each sensor via a feedback link from the central processor. In this paper, we focus on the opposite on the case of “dumb” sensors i.e., sensors which are able to process information with few or no knowledge of their mission or their environment. More precisely, we separately study the following linear strategies.

-

1.

Random iid precoders: A natural way to design dumb sensor networks is to select each sensor’s precoder at random, independently from the network’s mission. Motivated by first by the simplicity of the approach and second by its widespread use in compressive sensing applications [6], we assume that matrix is one realization of a random matrix with zero mean iid entries. In the case of random iid precoders, sensors are able to precode their information without any instructions from the fusion center.

-

2.

Orthogonal precoders: In this case, matrix is such that i.e., the precoders are orthogonal. Orthogonal precoders will reveal useful for the design of dumb but nevertheless efficient sensor networks. Indeed, under this constraint, we are able to exhibit strategies that achieve the best error exponent. In addition, when such precoders are used, we will show that a low complexity testing procedure can be implemented as an alternative to the costly Likelihood Ratio Test, without decreasing the error exponent.

IV Error Exponents

IV-A Case of random iid precoders

Before stating the main result of this subsection, remark that the performance of the test is of course expected to depend on the covariance matrix of the signal to be detected. In particular, it is useful to recall some well known results on the behaviour of the eigenvalues of . From classical results on large Toeplitz matrices [7], it is known that can be approximated by a circulant matrix with eigenvalues . More precisely, for any Hermitian matrix , we denote by the distribution function associated with the empirical distribution of the eigenvalues of (the corresponding probability measure is often refered to as the spectral measure of ). Szegö’s Theorem ([7], p.64) states that, provided that Assumption holds, converges weakly to the distribution function defined by:

| (10) |

where we recall that is the measure which composes the Lebesgue measure on with (the inverse image under ). The error exponent merely depends on the latter limiting spectral measure , as stated by the following Theorem.

Theorem 1.

Suppose that (7) holds for some and assume . For each , let be a real random matrix such that for all are iid zero mean random variables with finite second order moment. Consider any fixed level . Then the linear strategy admits an error exponent given by:

| (11) |

where is the unique solution to the following equation:

| (12) |

The proof is provided in Appendix A-A.

IV-B Case of orthogonal precoders

We now focus on the case where . Our aim is first to prove that among all orthogonal strategies, we may determine some that achieve the maximum error exponent and second, to determine this maximum error exponent. Results are provided below in Theorem 2. We first provide some definitions along with some insights on the results.

Loosely speaking, it is easy to think of a relevant orthogonal strategy as follows. Focus on one given sensor for the sake of simplicity. Under , the received sequence corresponds to a white Gaussian noise of variance . Therefore the law of is . Under , it is straightforward to show that , where we recall that is the signal covariance matrix. Clearly, the best way for the sensor to discriminate versus is to chose the precoder which maximizes the variance . This is achieved when coincides with the eigenvector of associated with the largest eigenvalue. Generalizing this remark to sensors, it is natural to introduce the strategy for which the precoders coincide with the eigenvectors of associated with the largest eigenvalues. We shall refer to this strategy as the Principal Component Strategy (PCS).

Definition 1 (principal components strategy (PCS)).

Let be the eigenvectors of and be the corresponding eigenvalues, ordered in such a way that . The principal component strategy is defined as the sequence of matrices given by:

As will be stated by Theorem 2 below, PCS achieves the maximum error exponent among all orthogonal strategies. Unfortunately, exact PCS might be difficult to implement in a dumb sensor network, as each node needs to be informed of a whole eigenvector of the covariance matrix . This requires involved cooperation between the nodes and the fusion center. In order to reduce the amount of overhead in the network, we propose an alternative strategy which turns out to achieve the same error exponent as PCS. Let denote the real-valued orthogonal Fourier basis matrix, that is , where the columns are defined, up to a normalizing constant by

The main idea is to remark that for large , the covariance matrix can be approximated by the matrix

| (13) |

see [7, 8] for more details. As a consequence, it seems reasonable to propose a strategy inspired of PCS, only substituing the above matrix (13) with the true covariance matrix . This leads to the following definition.

Definition 2 (principal frequencies strategy (PFS)).

For each , denote by any permutation of such that . The principal frequencies strategy is defined as the sequence of matrices given by:

| (14) |

where are the columns of matrix .

Note that PFS only requires to transmit one of the indices corresponding to the principal frequencies of to each sensor. In return, each sensor computes the scalar product between the th column of Fourier matrix and its received sequence . In other words, it computes the value of the (real) periodogram of at frequency . The following result proves furthermore that both PCS and PFS achieve the best error exponent among all orthogonal strategies.

For any denote by the following set of frequencies:

| (15) |

It is worth noting that the Lebesgue measure of is equal to (see Lemma 5).

Theorem 2.

Suppose that (7) holds for some . and assume and . Let and respectively denote the PCS and PFS as defined above. For any , the error exponents and associated with and exist, and are such that where

| (16) |

where denotes the Kullback-Leibler contrast. Moreover, for any orthogonal strategy ,

| (17) |

The proof is provided in Appendix A-B. Let us briefly comment the best error exponent formula (16). First we recall that for any ,

which is increasing as gets away from 1 from above or below. Since is nondecreasing, we see that the frequencies lying in are those that maximize in . Thus can be interpreted as some distance between the two spectral densities (corresponding to ) and (corresponding to ) restricted to a set of frequencies where these two spectral densities are the furthest apart.

IV-C Illustration and comparisons

Error exponents and defined in sections IV-B and IV-A depends on the following parameters: the spectral density , the noise level , along with the sensors growth ratio . When using the orthogonal strategy, one can expect that the more peaky is, the more efficient the compression will be. That is, by using only a few sensors configured at the peak frequencies, one will get a attractive exponent error. This should also lead to a sharp increase of the error exponent curve for small . On the contrary, when is nearly flat (with a small range of values), there are no priviledged frequencies for the sensors to forward and the error exponent should increase slowly as gets larger. Let us illustrate these intuitive arguments with numerical experiments. We consider two spectral densities corresponding to ARMA processes. The corresponding plots are depicted in Fig. 2.

Fig. 3 represents and for . For comparison, we also plotted another error exponent curve, corresponding to an orthogonal, yet suboptimal strategy which uses precoding matrices . This strategy amounts to keep only the first values of the signal, independently of . It is straightforward to prove that the corresponding error exponent writes .

One can notice several numerical facts on Fig. 3. First, as expected from section IV-B, is always below . Remark that, as expected, has a sharper increase near when used with than when used with . The fact that the random iid strategy seems to behave better for close to is more surprising but it reveals the following interesting fact: in some circumstances, a non-orthogonal strategy may outperform an optimal orthogonal strategy. Let us try to interpret this result. When setting up the sensor network design, one faces a tradeoff. Either use an extra sensor over the same frequency that the previous sensor in order to denoise their common measurment, or use this extra sensor over a new frequency in order to discover another part of the spectral density . At small levels of noise, it is always more interesting to discover at new frequencies than to denoise ones already used by other sensors; indicating that the orthogonal strategy is always the best. But for high levels of noise, it may become more efficient to repeat (and thus denoise) key frequencies than to discover less important ones. To support this claim, we refer to Fig. 4 where we chose two levels of noise, one that is larger () than the one used in Fig. 3, and one that is smaller (). One can see that when , the best orthogonal strategy outperforms the two others, whereas for the upcrossing of over near is more important than on Fig. 3. The same conclusions hold for both spectral densities and .

V A PFS-based low complexity test

Results of the previous section indicate that the principal frequencies strategy is a good candidate for implementation in dumb sensor networks. Indeed it requires only few cooperation between the nodes and the fusion center, and is attractive from an error exponent perspective. In this section, we prove furthermore that when PFS is used, then a test procedure can be proposed which is much less complex than the LRT, and which achieves nevertheless the same error exponent.

We assume throughout this section that PFS is used i.e., each precoding matrix is given by where is defined by (14).

V-A A low complexity test

Recall that the LRT rejects the null hypothesis when the LLR (5) is above a threshold. As the terms and are constant w.r.t. the observation , it is clear that the LRT reduces to the test which rejects the null hyopthesis for large values of the statistics:

| (18) |

Unfortunately, the evaluation of the above statistics is computationally demanding as gets larger, since it requires the inversion of the matrix . In order to avoid this, we propose to replace matrix in (18) with its circulant approximation given by (13). In other words, product is replaced by:

This leads directly to the following procedure.

PFS low complexity (PFSLC) Test: Reject hypothesis when the statistics defined by:

| (19) |

is larger than a threshold.

Although this statistics cannot give rise to a better test than the LRT, its numerical simplicity makes it worth to be considered. In the next paragraph, we study the performance of the test and we prove that it performs as well as the LRT in terms of error exponent.

V-B Asymptotic optimality of the PFSLC test

As the statistics (19) is no longer a likelihood ratio, Lemma 1 cannot be used to evaluate the error exponent associated with the test (19). Instead, we must resort to arguments of large deviations theory. Specifically, we shall study the large deviation behaviour of the test associated to this statistic, that is the limit of where is the -quantile of the statistic under , . Under mild assumptions, we show below that this limit is given by the error exponent of the PFS. Hence, as far as error exponents are considered, there is no loss in the performance in using the statistic defined in (19) rather than the likelihood ratio.

Theorem 3.

Assume that and hold true. For any level , the statistics defined in (19) satisfies the following property. For such that , the miss probability satisfies

The proof of this result is provided in Appendix A-C.

VI Simulations

The error exponent theory is inherently asymptotic. In this section we provide numerical experiments to analyze the performance of the PFS on simulated data for finite since we have already proved that the error exponent curve is the same. The point here is to test how well the error exponent theory is relevant for finite .

We use the same spectral density functions and as in section IV-C, whose error exponents are displayed in Fig. 3. We now compare, for a couple of values for , the finite sample performances of the LRT with the iid, PFS and PCS Strategies by using their empirical Receiver Operating Characteristic (ROC) curves. When the PFS is used, we also consider the PFSLC test of section V. We have shown that the LRT with the PFS or the PCS and the PFSLC test share the same error exponent curve. How well this measure of the performance impacts the whole ROC curves at finite samples is displayed in Fig. 5. It turns out that the PCS, the PFS and the PFSLC have similar ROC curves, as indicated by the error exponent analysis. One can also notice the good performance of the PFS, PFSLC and PCS when , and for , which confirms the conclusions drawn from the error exponent curves in Fig. 3. For , and , one can notice that error exponent curves also provide a good prediction: the iid strategy slightly outperforms the PFS, PCS and PFSLC.

VII Conclusion

In this paper, we studied the performance of the Neyman-Pearson detection of a stationary Gaussian process in noise, using a large wireless sensor network (WSN). Our results are relevant for the design of sensor networks which are constrained by limited signaling and communication overhead between the fusion center and the sensor nodes. We studied the case where each sensor compresses its observation sequence using either a random iid linear precoder or an orthogonal precoder. In the random precoder case, we determined the error exponent governing the asymptotic behaviour of the miss probability, when and . In the orthogonal precoder case, we exhibit strategies (PCS and PFS) that achieve the best error exponent among all orthogonal strategies. The PFS has moreover the attractive property of being well suited for WSN with signaling overhead constraints. In addition, we proved that when the PFS is used, a low complexity test can be implemented at the FC as an alternative to the Likelihood Ratio (Neyman-Pearson) test. Interestingly, the proposed test performs as well as the LRT in terms of error exponents.

Acknowledgments

We thank Jamal Najim for helpful comments and for bringing useful references to our attention.

Appendix A Proofs of main results

Observe that we may set without loss of generality, since it amounts to divide by and the data by . Hence in the following proof sections, we assume . In particular the LLR in (5) for a precoding matrix with normalized precoders , is given by

| (20) |

A-A Proof of Theorem 1

We assume without restriction that . Due to Lemma 1, it is sufficient to prove that the normalized LLR associated to strategy converges in probability to the rhs of equation (11) under . Expression (20) of the LLR relies on the assumption that each precoder has unit norm, which is generally not the case for defined as in Theorem 1. Since the false alarm and miss probabilities of this LRT do not depend on the norms , , it is equivalent to consider precoders defined by the matrix

| (21) |

where . With this definition, we may use expression (20) which is valid for normalized precoders. In order to prove Theorem 1, it is now sufficient to show that converges to the constant defined in (11).

The main issue lies in the asymptotic study of the two terms and . This can be done by successively using the results of [9], [10] and [11]. The crucial point is to characterize the limiting spectral measure of matrix . Define:

First, we prove (see Lemma 2 below) that the spectral measure of is asymptotically close to the one of in a sense which is made clear below. Second, we apply the results of [12, 10] along with [7] to determine the limiting spectral measure of . Finally, closed form expressions of the desired quantities follow from the results of [11].

Denote by the Lévy distance on the set of distribution functions. We recall that denotes the distribution function of the spectral measure of (see Section IV-A).

Lemma 2.

As , converges to zero in probability.

Proof.

The proof relies on Bai’s formula (see [13] and [9]) which provides the following bound on the Lévy distance:

| (22) |

for any real matrices , where denotes the Frobenius norm of . We now use equation (22) with and . Using (21) and introducing , it is straightforward to show that:

| (23) |

Note that , where denotes the spectral radius of . Similarly, . Finally, . Putting all pieces together,

| (24) |

where

From [7], converges to . By the law of large numbers, converges almost surely (a.s.) to . From [14], converges a.s. to . Therefore, converges a.s. to . In order to prove that converges in probability to zero, it is sufficient, by equation (24), to prove that converges in probability to zero. We write as follows:

where . Note that for a fixed , are iid for all . Let . By Markov inequality,

| (25) |

As converges a.s. to zero, we conclude that tends to zero. This completes the proof of Lemma 2.

Thanks to Lemma 2, it is sufficient to study the asymptotic behaviour of . The latter is provided by [12, 10]. In order to introduce this result, we need to recall some definitions. For any distribution function , the Stieltjes transform of is given by:

for each , where with denoting the imaginary part of . Recall that, from the results of [7], the spectral distribution function of converges weakly to given by (10). By straightforward application of the results of [12, 10], we obtain that, with probability one, converges weakly to a deterministic measure whose Stieltjes transform is the unique solution in of:

| (26) |

for each . The above result along with Lemma 2 implies that

| (27) |

We are now in a position to study the limit of the LLR. We obtain immediately from (20):

| (28) |

where

Using (27), and respectively converge in probability to the constants and defined by:

Recalling that under , the term in the rhs of (28) converges a.s. to one. Since is independent of and since the spectral radius of is bounded, it is straightforward to show that (use for instance Lemma 2.7 in [15]). Finally, converges in probability to:

| (29) |

Constant coincides with the Stieltjes transform of at point , that is where we defined for each , . Constant is thus the unique solution to (12). A closed form expression for can as well be obtained using (for instance) [11]. Using the fact that the limiting spectral measure associated with has a bounded support, the dominated convergence Theorem applies to the function . One easily obtains after some algebra:

Following [11], we conclude that where is the function defined for each by:

This statement can simply be proved by noting that (where is the derivative of ) and . Plugging the above expression of into (29), we obtain the claimed error exponent .

A-B Proof of Theorem 2

We start with some useful definitions and technical preliminaries. Let . Denote so that, by definition of in (10), for all and for all . We define the set

By assumptions A1 and A2, is continuously strictly increasing from to , we denote by its inverse continuous function defined from to . Hence . Moreover, using again A2, we obtain that is almost surely continuous with respect to . By the uniform mapping theorem, this implies that, for any sequence of probability measures weakly converging to , we have, for all continuous function , as ,

| (30) |

where the last equality follows from the definition of in (15) by setting .

A-B1 The PCS case

The outline of the proof is the following.

- Step 1.

-

Step 2.

Strategy with any sequence satisfying (7) also has the error exponent .

- Step 3.

Step 31. Let denote the empirical spectral measure of defined in (4). Szegö’s Theorem states that converges weakly to ([7], p.64). Applying (30) and then Lemma 5 then gives

That is, defined by (31) satisfies (7). Recall that here is given in Definition 1 with given by in (31). The empirical spectral measure of is thus given by . Hence we have as above that

| (32) | ||||

| (33) |

The spectral radius is bounded by . Using eqs (20), (32)–(33), Lemma 3 and (16), we obtain that, under , . As a consequence of Lemma 1, we obtain the assertion of Step 1.

Step 2. Observe that the error exponent associated to a strategy is increasing with . Now let be a sequence satisfying (7). For any and such that , define and by (31) with replaced by and respectively. Then, as seen in Step 31, and also satisfy (7) with replaced by and respectively. Thus, eventually, , and, applying Step 31, the error exponent of belongs to . This, with the continuity of , yields the assertion of Step 2.

Step 3. Assume now denotes any orthogonal, that is is a orthogonal matrix for all , where satisfies (7). Let us prove that the bound (17) holds. By Lemma 1, for all real , we have

| (34) |

Let . Using Markov inequality, we have for large enough,

Using (20), we have

where the convergence follows from Lemma 3 by noticing that has eigenvalues in and, under (recall that we set ), . The last two displays show that as for all . With (34), we get that

To conclude the proof, it thus only remains to show that . We have, by (20),

Since is nondecreasing on , Lemma 4 thus implies that . We proved in Step 31 that . Hence the proof is achieved.

A-B2 The PFS case

We now prove that the PFS strategy also achieves the error exponent under the condition (7). Using the same argument as in Step 2 of the PCS case, we can in fact take as defined by

| (35) |

where is given in Definition 2, which we assume in the following.

It is known ([16], Lemma 4.6) that defined in (4) is asymptotically equivalent to where denotes the diagonal matrix with entries , . As in [17], we denote asymptotic equivalence between matrices and by . Asymptotic equivalence is preserved by elementary matrix operations ([17], Proposition 2.1). Hence, being unitary,

Also, from the definition of ,

where is a selection matrix the columns of which belong to the canonical basis. Hence, being unitary,

| (36) |

We then conclude as in Step 31 of the PCS case.

A-C Proof of Theorem 3

Again we can take defined by (31) without loss of generality.

Let denote the diagonal matrix with entries , , where we defined the function

Then by Definition 2 and (19), we have

where and is a -sample of a centered stationary Gaussian process with spectral density under and under . We shall apply [18, Propostion 2] which provides a large deviation principle (LDP) for quadratic forms of stationary Gaussian processes. Recall that we denote by the covariance matrix associated to the spectral density (see (4)). Let denote the set of eigenvalues of . Since is non-negative, to apply this result, we successively show that for or ,

-

(i)

is bounded above by ,

-

(ii)

the following weak convergence holds ,

-

(iii)

as .

Observe that the eigenvalues of are given by , with , and those of are bounded by . Hence we have (i). Assertion (ii) is a consequence of Lemma 5 in [16] and Theorem 2.1 in[17]. By (i) and (ii), we have

Thus Assertion (iii) follows by observing that , and achieve their maxima at the same points, thus for or . Since Assertions (i)–(iii) hold, Propostion 3 and Corollary 2 in [18] give that for , under , satisfies a LDP with good rate function

| (37) |

with or under or , respectively. As in [18], we assume for convenience that when .

Assertion (ii) above also implies that with the same convention for . Hence the sequence in Theorem 3 satisfies . Thus the LDP under gives

and

By Lemma 6, we conclude that

To conclude the proof, it only remains to show that and is nonincreasing on . By definition of and , we have , where

Using the definition of , we further have and hence with

For any , it is straightforward to show that is maximized at at which it takes value . Since the maximizing does not depend on we obtain

We now consider . By differentiating , the maximizing satisfies

Note that is non-negative and has a positive integral on hence the right-hand side of the previous display has a strictly positive derivative w.r.t. . It follows that , defined as the maximizing , is strictly increasing with . On the other hand, we know from above that . Thus, for all , we have . Now observe that for all and all we have . It follows that is nonincreasing on , which achieves the proof.

Appendix B Technical lemmas

Lemma 3.

Assume that for each , where has bounded spectral radius ; and assume is a family of quadratic forms with bounded spectral radius . Then,

If, moreover,

Then converges in the sense towards .

Proof:

One has . Let us estimate .

with a standard centered gaussian vector and diagonal and congruent to .

where is a constant. Thus we have, as sought,

Lemma 4 ([19], p. 189).

Let be a symmetric matrix, and be a -dimensional subspace of . Denote by the restriction of to , , , the eigenvalues of in increasing order and , , the eigenvalues of in increasing order. Then, for all , we have .

Lemma 5.

Under A1-A2, we have for any , , where is defined by (15).

Proof:

We have , where denotes the inverse image under . Observe that . Moreover as we have seen in the preamble of Appendix A-B, is continuously and strictly increasing from to and constant on , hence , where here denotes the inverse function from to . Hence . Now since is the distribution function of the probability measure and using again that it is continuously and strictly increasing from to , we get that , which concludes the proof.

Lemma 6.

Let be defined for by (37) with values in for some non-negative bounded function . Then is finite and continuous for .

Proof:

Let so that . Let denote the essential sup of . Then for all . Let . Note that and for all and , as . Thus there exists only depending on such that for all and . From these facts, it follows that for all , . Finally we observe that for all , which now yields the result.

References

- [1] Y. Sung, L. Tong, and V. Poor, “Neyman-pearson detection of gauss-markov signals in noise: Closed-form error exponent and properties,” IEEE Trans. Information Theory, vol. 52, no. 4, pp. 1354–1365, 2006.

- [2] W. Hachem, E. Moulines, and F. Roueff, “Error exponents for neyman-pearson detection of a continuous-time gaussian markov process from noisy irregular samples,” submitted to IEEE Trans. on Inform. Theory, 2009.

- [3] R.S. Blum, S.A. Kassam, and H.V. Poor, “Distributed detection with multiple sensors ii. advanced topics,” Proc. of the IEEE, vol. 85, no. 1, pp. 64–79, 1997.

- [4] J.J. Xiao, Z.Q. Ribeiro, A.and ZQ Luo, and G.B. Giannakis, “Distributed compression-estimation using wireless sensor networks,” IEEE Sign. Process. Magaz., vol. 23, no. 4, pp. 27–41, 2006.

- [5] P.-N. Chen, “General Formulas For The Neyman-Pearson Type-II Error Exponent Subject To Fixed And Exponential Type-I Error Bounds,” IEEE Transactions on Information Theory, vol. 42, no. 1, pp. 316–323, 1996.

- [6] E.J. Candes and T. Tao, “Decoding by linear programming,” IEEE Trans. on Inform. Theory, vol. 51, no. 12, pp. 4203–4215, December 2005.

- [7] U. Grenander and G. Szegö, Toeplitz Forms and Their Applications (2nd Ed.), Chelsea Publishing Co, 1984.

- [8] H Widom, Studies in Real and Complex Analysis, vol. 3 of MAA Studies in Mathematics, Prentice Hall, 1965.

- [9] W. Hachem, Ph. Loubaton, and J. Najim, “The empirical eigenvalue distribution of a gram matrix: From independence to stationarity,” Markov Process, Related Fields, vol. 11, pp. 629–648, 2005.

- [10] J. Silvertein, “Strong convergence of the empirical distribution of eigenvalues of large dimensional random matrices,” Journal of Multivariate Analysis, vol. 55, no. 2, pp. 175–192, 1995.

- [11] W. Hachem, Ph. Loubaton, and J. Najim, “Deterministic equivalents for certain functionals of large random matrices,” Ann. Appl. Prob., vol. 17, no. 3, pp. 875–930, 2007.

- [12] Y. Q. Yin, “Limiting spectral distribution for a class of random matrices,” J. Multivariate Anal., vol. 20, no. 1, pp. 50–68, 1986.

- [13] Z.D. Bai, “Convergence rate of expected spectral distributions of large random matrices part ii: Sample covariance matrices,” Ann. Prob., vol. 21, no. 2, pp. 649–672, 1993.

- [14] Y. Q. Yin, Z. D. Bai, and P. R. Krishnaiah, “On the limit of the largest eigenvalue of the large-dimensional sample covariance matrix,” Probab. Theory Related Fields, vol. 78, no. 4, pp. 509–521, 1988.

- [15] Z.D. Bai and J. Silverstein, “No eigenvalues outside the suppport of the limiting spectral distribution of large dimensional random matrices,” Ann. Prob., vol. 26, no. 1, pp. 316–345, 1998.

- [16] J. Gutiérrez-Gutiérrez and P. M. Crespo, “Asymptotically equivalent sequences of matrices and hermitian block toeplitz matrices with continuous symbols: Applications to mimo systems,” IEEE Transactions on Information Theory, vol. 54, no. 12, pp. 5671–5680, 2008.

- [17] R. M. Gray, Toeplitz And Circulant Matrices: A Review, Now Publishers, 2006.

- [18] B. Bercu, F. Gamboa, and A. Rouault, “Large deviations for quadratic forms of stationary Gaussian processes,” Stochastic Process. Appl., vol. 71, no. 1, pp. 75–90, 1997.

- [19] R. A. Horn and C. R. Johnson, Matrix Analysis, Cambridge University Press, 1990.