The unscaled paths of

branching Brownian motion

Abstract

For a set , we give new results on the growth of the number of particles in a branching Brownian motion whose paths fall within . We show that it is possible to work without rescaling the paths. We give large deviations probabilities as well as a more sophisticated proof of a result on growth in the number of particles along certain sets of paths. Our results reveal that the number of particles can oscillate dramatically. We also obtain new results on the number of particles near the frontier of the model. The methods used are entirely probabilistic.

1 Introduction

One of the most natural questions to ask about branching Brownian motion (BBM) concerns the position of the extremal particle — the particle with maximal position at each time . It is well-known that its speed — its position divided by time — converges almost surely to as . In fact, far more precise results are available, such as that given by Bramson [1] via some powerful and explicit analysis of the Brownian bridge.

Once we know the speed of the extremal particle at large times , we might ask about its history: have its ancestors stayed close to the critical speed throughout, or have they hovered around in the mass of particles near the origin and made a late dash as we get close to time ? One way of interpreting this question is to consider branching Brownian motion with absorption. One imagines an absorbing line where is a constant close to the critical value , such that whenever a particle hits the line it disappears and is removed from the system. Are there any particles still present at large times? If so then we may consider them to have stayed “close” to the extremal edge of the system.

This model for BBM with killing on the line was studied by Kesten [10], who discovered asymptotics for extinction probabilities and numbers of particles in intervals of the area above the absorbing line. To choose two examples of particular interest, Kesten shows that if then there is strictly positive probability that never becomes empty; and that in the critical case , the probability that there is at least one particle present at time is approximately for some positive constant . Thus it is possible for particles to stay above the line for all time whenever , and that this is not the case when . Our next question might be: can particles stay within (plus a constant, say) of the critical line for ? Indeed, we could also attempt to generalise by moving away from the critical line — given a path , are there particles that stay close to and, if so, how close? Such questions provide motivation for this article.

The classical scaled path properties of branching Brownian motion (BBM) have now been well-studied: for example, see Lee [13] and Hardy and Harris [3] for large deviation results on “difficult” paths which have a small probability of any particle following them, and Git [2] and Harris and Roberts [6] for the almost sure growth rate of the number of particles near “easy” paths along which we see exponential growth in the number of particles. To give these results, the paths of a BBM are rescaled onto the interval , echoing the approach of Schilder’s theorem for a single Brownian motion.

In this article, as suggested above, we consider a problem similar in theme, but from a more naive viewpoint. We are given a fixed set of paths and we want to know how many particles in a BBM have paths within this set . Similar problems in the case of a single Brownian motion have been considered by Kesten [10] and Novikov [17]. The simplest case is to consider the ball of fixed width about a single continuous path , (we will, however, consider more general sets of paths). Clearly there is a positive probability that no particle will stay within this fixed “tube” — indeed, the very first particle could wander away from before it has the chance to give birth to another — and in this event we say that the process becomes extinct.

The intuition is that the growth of the population due to branching is in constant competition with the “deaths” due to particles failing to follow the function . Thus a natural condition arises: if the gradient of is too large, then the process eventually dies out almost surely and we may ask for the large deviation probabilities of survival up to large times; otherwise, if the gradient of remains sufficiently small, then we may condition on non-extinction and give an almost sure result on the number of particles along the path.

One payoff for our less classical approach is that we immediately see a dramatic oscillation in the number of particles along certain paths. This unusual behaviour (not seen in the existing literature) has a simple explanation which we demonstrate via some illuminating examples in Section 3.

In our proofs, we take advantage of spine techniques to interpret the change of measure given by a carefully chosen martingale. The spine tools give us an intuitive probabilistic handle on the problem, without which we would certainly need substantial extra technical work in several areas. Our particular change of measure involves forcing one particle (the spine) to stay within a tube of varying radius , about a function . This change of measure is the result of a new martingale which we develop in Section 4. We then use the spine decomposition first introduced by Lyons et al. [15], which allows us to bound the growth of the system by looking at the births along the spine.

Even with the spine theory the problem retains significant difficulty inherent in its time-inhomogeneity. This fact is underlined by the observation that even in the case we are essentially considering a one-dimensional branching diffusion with time-dependent drift, and asking how many particles remain within a bounded domain about the origin. It turns out that the main difficulty is in showing that extinction of the process coincides (to within a null set) with the event that the limit of our martingale is zero. Standard tools – analytic or probabilistic – cannot be applied; instead we proceed by our own methods in Section 6, using in particular an identity from Harris and Roberts [7].

For simplicity, we consider only standard one-dimensional binary branching Brownian motion, but we note that our work could be extended to a wide range of other branching diffusions. In particular the spine methods are well-suited to the situation where each particle gives birth to a random number of new particles, and methods similar to those used in the original papers of Lyons et al [11, 14, 15] could be used to extend our result.

Our main theorem concerns only sets of paths away from criticality. However, by adapting the methods from the proof of this theorem, we are able to obtain new results on the number of particles near the extremes of the system (see Theorems 3 and 4). These results answer the questions raised in the above discussion and, as was mentioned there, should be compared to the work of Bramson [1] on the position of the right-most particle, and of Kesten [10] and other authors on BBM with absorption.

2 Main results

2.1 Initial definitions

We consider a branching Brownian motion starting with one particle at the origin, whereby each particle moves independently and undergoes independent dyadic branching at exponential rate . We let the set of particles alive at time be , and for each particle denote its position at time by . We extend this notion of a particle’s position to include the positions of its ancestors; that is, if has ancestor for some , then we set . This setup will be given in more detail in Section 4.

Fix a continuous function , and another . If and are twice continuously differentiable then we define

and

We say that the pair satisfies the usual conditions if:

-

(I)

;

-

(II)

and are twice continuously differentiable;

-

(III)

;

-

(IV)

.

We assume throughout this article that, unless otherwise stated, these conditions hold. We consider initially the class of sets of the form

such that and satisfy the usual conditions. After we obtain our results we will be able to extend them in a natural way to cover more general subsets of — see Section 7 — but for now these conditions will allow us to apply integration by parts theorems without any complications. Although condition (III) may appear unnatural, there are clear reasons behind it, some of which are demonstrated via example in Section 7. There are also similar conditions in the work on a single Brownian motion by Kesten [10] and Novikov [17].

Define

the set of particles that have stayed within distance of the function for all times . We wish to study the number of particles in at large times. Let

We call the extinction time for the process, and say that the process has become extinct by time if . When we talk about survival or non-extinction, we mean the event .

2.2 The non-critical case,

We now state our main result in the non-critical case when . Most of this article will be concerned with proving this theorem.

Theorem 1.

If , then almost surely and

On the other hand, if , then and almost surely on survival we have

As mentioned earlier, this theorem can be extended to cover more general sets, and we give results in this direction in Section 7. The behaviour at criticality (S=0) depends on the finer behaviour of and , but we are able to give some results in particular important cases in Section 2.3 below. We note the following corollary, which is easily deduced from Theorem 1.

Corollary 2.

If , then almost surely on survival we have

and

2.3 The critical case,

At least one obvious question immediately arises: what happens when ? This is an interesting but delicate matter: one must look at the finer behaviour of

Our methods, as they stand, are not always sharp enough to say what will happen, and we are unable to provide a complete theory as we must adapt carefully to the set in question. There are several situations, however, where something can be done. We are able to give results on the behaviour near the critical line in Theorems 3 and 4 below. Proofs of these two theorems will be given in Section 8, as adaptations of our main proof, that of Theorem 1.

Fix , and , and for let

Theorem 3.

If then we have , and

If , we have , and almost surely on survival

It is well-known that the asymptotic speed of the right-most particle in a BBM is . The theorem above concerns asking particles to stay close to this critical line forever: for example, we might ask particles to be in for all times . If then particles manage this with positive probability; if then they do not. What if ? Intuitively this question is “even more critical” than the previous theorem. Indeed, our methods are not able to give a full answer, but they can identify regimes where each behaviour (growth or death) is observed.

Theorem 4.

Consider the case . Let

If and , then ; in fact

and

On the other hand, if and , or if and , then and almost surely on survival

and

Theorems 3 and 4 should be compared with what is currently known about the right-most particle, for example the work of Bramson [1] and Lalley and Sellke [12], results on branching Brownian motion with killing, for example Kesten [10], and work on the branching random walk, for example Hu and Shi [8] and Jaffuel [9]. The recent article by Jaffuel [9], in particular, gives results similar to our Theorems 3 and 4.

3 Examples

We now consider some very simple examples to give the reader a flavour of the implications of Theorem 1. More complex examples will be given in Sections 7 and 8 in order to explore the limits of our method.

Example 1.

Take with and . We have a growth rate of (provided this is non-zero): if this constant is negative, then

and if it is positive then there is a positive probability of survival, and almost surely on that event

Thus taking a fixed introduces an extra “killing” rate of to the system compared to the scaled results of [2, 3, 6, 13].

Example 2.

Again take with but now let be any unbounded monotone non-decreasing function such that satisfies the usual conditions (for example with or ). Then we have a growth rate of : thus while constant severely restricts the growth of the system, as soon as we relax slightly we regain the full growth behaviour seen in [2, 3, 6, 13].

Example 3.

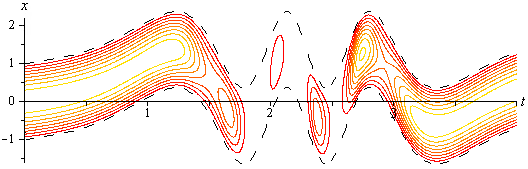

Example 4.

Let and . If is large enough then, on survival, the number of particles alive at time oscillates, with

and

(Note the appearance of the golden ratio.)

The reason for this oscillation on the exponential scale becomes clearer when we consider the following simpler, but perhaps less natural, example.

Example 5.

Define a continuous function by setting for and

Then, provided that , on non-extinction we have

and

The idea here is that the number of particles grows quickly when , but much more slowly when as the steep gradient means that particles have to struggle to follow the path for a long time. As the size of the intervals grows exponentially, the behaviour of the number of particles at time is dominated by the behaviour on the most recent such interval. [We note that this choice of is not twice differentiable; however, it can be uniformly approximated by twice differentiable functions, and it is easily checked that our results still hold - see Section 7.]

4 The spine setup

Consider a dyadic one-dimensional branching Brownian motion, branching at rate , with associated probability measure under which

-

•

we begin with a root particle, , at 0;

-

•

if a particle is in the tree then all its ancestors are also in the tree (if is an ancestor of then we write );

-

•

each particle has a lifetime , which is exponentially distributed with parameter , and a fission time ;

-

•

each particle has a position at each time ;

-

•

at the fission time , has disappeared and been replaced by two children and , which inherit the position of their parent;

-

•

given its birth time and position, each particle , while alive, moves according to a standard Brownian motion started from independently of all other particles.

For convenience, we extend the position of a particle to all times , to include the paths of all its ancestors:

We recall that we defined to be the set of particles alive at time ,

and also that

We choose from our BBM one distinguished line of descent or spine – that is, a subset of the tree such that contains exactly one particle for each and if and then . We make this choice as follows:

-

•

the initial particle is in the spine;

-

•

at the fission time of node in the spine, the new spine particle is chosen uniformly at random from the two children and of .

We denote the position of the spine particle at time by ; however we may also occasionally use to refer to the spine particle itself (that is, the node of the tree that is in the spine at time ) — it should be clear from the context which meaning is intended. We call the resulting probability measure (on the space of marked trees with spines) . We also consider the translated probability measures and for , where under and we start with a single particle at instead of 0.

4.1 Filtrations

We use three different filtrations, , and , to encapsulate different amounts of information. We give descriptions of these filtrations here, but the reader is referred to Hardy and Harris [4] for the full definitions.

-

•

contains all the information about the marked tree up to time . However, it does not know which particle is the spine at any point.

-

•

contains all the information about both the marked tree and the spine up to time .

-

•

contains just the spatial information about the spine up to time ; it does not know anything about the rest of the tree.

We note that and , and also that is an extension of in that .

4.2 Martingales and a change of measure

Under , the path of the spine is a standard Brownian motion. Set

We claim that the process

is a -local martingale.

Lemma 5.

Let

The process

is a -local martingale.

Proof.

By Itô’s formula,

Lemma 6.

The process , is a -local martingale.

Proof.

Again applying Itô’s formula does the trick - or one may simply apply Girsanov’s theorem in series with Lemma 5. ∎

By stopping the process at the first exit time of the spine particle from the tube , we obtain also that

is a -local martingale, and in fact since its size is constrained it is easily seen to be a -martingale. We call this martingale the single-particle martingale.

Definition 7.

We define an -adapted martingale by

where is the generation of the spine at time . The proof that this process is an -martingale can be found in [4].

We note that if is an -measurable function then we can write:

| (1) |

where each is -measurable – intuitively, if is in fact -measurable, one replaces every appearance of with : so for example

It is also shown in [4] that if we define

where is the -adapted process defined via the representation of as in (1), then

and hence that is an -martingale. This martingale is the main object of interest in this article.

Definition 8.

We define a new measure, , via

Also, for convenience, define to be the projection of the measure onto ; then

Lemma 9.

Under ,

-

•

when at position at time the spine moves as a Brownian motion with drift

-

•

the fission times along the spine occur at an accelerated rate ;

-

•

at the fission time of node on the spine, the single spine particle is replaced by two children, and the new spine particle is chosen uniformly from the two children;

-

•

the remaining child gives rise to an independent subtree, which is not part of the spine and which (along with its descendants) draws out a marked tree determined by an independent copy of the original measure shifted to its position and time of birth.

This, again, was covered in [4]. We also use that, under , the spine remains within distance of for all times . To see this explicitly, note that

by definition of . All other particles, once born, move like independent standard Brownian motions but – as under – we imagine them being “killed” instantly upon leaving the tube of radius about . In reality they are still present in the system, but make no contribution to once they have left the tube.

Remark.

Note that , and hence , and various other of our constructions, depend upon the choice of function and radius . Usually these will be implicit, but occasionally we shall write , and (and so on) to emphasise the choice of and in use at the time.

4.3 Spine tools

We now state the spine decomposition theorem, which will be a vital tool in our investigation. It allows us to relate the growth of the whole process to just the behaviour along the spine. For a proof (of a more general version) the reader is again referred to [4].

Theorem 10 (Spine decomposition).

We have the following decomposition of :

The spine decomposition is usually used in conjunction with a result like the following – a proof of a more general form of this lemma can be found in [16].

Lemma 11.

Let . Then

and

Another extremely useful spine tool is the many-to-one theorem. A much more general version of this theorem is proved in [4], but the following version will be enough for our purposes.

Theorem 12 (Many-to-One).

If is -measurable for each with representation (1), then

We have one more lemma, a proof of which can be found in [7]. Although this result is extremely simple — and essential to our study — we are not aware of its presence in the literature before [7].

Lemma 13.

For any (note that infinity is included here), we have

5 Almost sure growth along paths

5.1 Controlling the measure change

Before applying the tools that we have developed, we need the following short lemma to keep the Girsanov part of our change of measure under control.

Lemma 14.

For any , almost surely under both and we have

and hence under

| (2) |

Proof.

From the integration by parts formula for Itô calculus, we know that

From ordinary integration by parts,

We also note that if then for all . Thus

Plugging this estimate into the definition of gives the result. ∎

We are now ready to prove our first real result.

Proposition 15.

Recall that . If , then the process almost surely becomes extinct in finite time (and hence we have ). In this case,

Alternatively, if then .

Proof.

We first recall the spine decomposition and apply inequality (2):

If , then the integrand above is exponentially small for all large (as is the second term); so . It is easy to show that is a positive -supermartingale, and hence converges -almost surely to some (possibly infinite) limit. Thus, applying Fatou’s lemma, we get

We deduce that -almost surely, and Lemma 11 then gives that .

Alternatively, suppose that . Then by the above,

Now, by the tower property of conditional expectation and Jensen’s inequality,

This clearly implies that, for large (using that ),

and it is easy to see that the right-hand side converges to one as . This gives us our upper bound.

For the lower bound (still in the case ), suppose for a moment that we may choose such that

We note that we may choose in this way if (eventually) shows at most linear growth, which we will check later. Then

If then there is at least one particle in ; we may then apply inequality (2) to see that

We repeat our calculations from the upper bound, taking logarithms and dividing by the desired denominator, to give

| (3) |

for large . Thus it remains to check that the right-hand side above has a limsup that is close to 1 when is close to 1. Again it is sufficient that can (eventually) show at most linear growth, and we check that fact now. This is rather fiddly and not interesting in the context of the rest of the proof. Suppose it is not true; that is, suppose

Then since we must have

| (4) |

If we take , then

so differentiating and rearranging we get

Now, we note that , so (4) implies that for all large ,

for some constant . We have just shown that , so for all large ,

contradicting (for large ) the definition of .

We have shown that

which allows us to make the limsup of (3) as close to as we like by letting . This completes the lower bound, which in particular implies (by monotonicity) that the probability of eventual extinction is equal to 1. ∎

5.2 Almost sure growth

Having established, in Proposition 15, the large deviations behaviour of our model, we now turn to the question of what happens when extinction does not occur. The two propositions in this section contain the meat of our results in this direction. Proposition 16 gives a lower bound on the number of particles in for large , and Proposition 17 an upper bound. The former holds only on the event that has a positive limit; as mentioned in the introduction, this set coincides (up to a null event) with the event that no particle manages to follow within of , although we will not prove this fact until Section 6. The proofs of our two propositions are very simple, but we stress again that this is due to the careful choice of martingale.

Proposition 16.

Let be the set on which has a strictly positive limit,

If then -almost surely on we have

Proof.

For any , by inequality (2), almost surely under

Hence (for large , since )

Now, on we have and thus has a non-negative liminf for any ; then since we see that the right-hand side above has liminf at least 1. ∎

Remark.

Recall that under , is a non-negative martingale, and hence -almost surely. If , then by Proposition 15 , so in this case occurs with strictly positive probability.

Proposition 17.

If , then -almost surely we have

Proof.

Fix and let . Since is a non-negative martingale under , we have -almost surely. This implies that for any , almost surely

Now, almost surely under ,

By the definition of above, for any the cosine term in is at least (since the particle is within of at time ). Applying inequality (2) we see that

and hence

As in Proposition 15, we can bound the growth of the term in the numerator so that letting we get the desired result. ∎

Corollary 18.

If , then -almost surely on the event ,

6 Showing that agrees with extinction

We note that we have now established our main result except for one key point: our growth results have so far been on the event , rather than the event of survival of the process, . We turn now to showing that these two events differ only on a set of zero probability.

The approach to proving this is often analytic: one shows that and satisfy the same differential equation with the same boundary conditions, and then shows that any such solution to the equation is unique. There is also sometimes a probabilistic approach to such arguments: one considers the product martingale

On extinction, the limit of this process is clearly 1, and if we could show that on survival the limit is 0, then since is a bounded non-negative martingale we would have

In Harris et al [5], for example, we have killing of particles at the origin rather than on the boundary of a tube – and it is shown that on survival, at least one particle escapes to infinity and its term in the product martingale tends to zero. This is enough to complete the argument (although in [5] the authors favour the analytic approach). In our case we are hampered by the fact that for a single particle the value of is bounded away from zero, and if the particle is close to the edge of the tube, or even possibly in some places in the interior the tube, then this probability takes values arbitrarily close to 1.

The time-inhomogeneity of our problem means that other standard methods also fail. Our alternative approach is based upon similar principles as the probabilistic approach above, but is more direct: we show that if at least one particle survives for a long time, then it will have many births in “good” areas of the tube, and thus with high probability.

Recall that under , we start at time with one particle at position (rather than at the origin) – and similarly for . We assume throughout this section that , otherwise there is nothing to prove — our theorem does not consider the case , and if we have proved that . We now need some more notation.

Definition 19.

Let , and define

and

Now, for any function on , define the -delayed version of for by

Thus for each we have four new functions , , and .

Also, for , define

We think of as the “good” part of the tube — if a particle is born in then it has probability at least of contributing to . Finally, for any particle and , define

is the time spent by particle in the set before .

Our first task is to convert to using and ; the fact that is bounded will prove useful.

Lemma 20.

The pair satisfies usual conditions (II, III, IV), and .

Proof.

We note that is twice continuously differentiable and hence so is , and that whenever , whenever , and for all . We first claim that , working by comparison with . Indeed, when we clearly have and . When ,

so . Also,

so (since the sizes of , and are bounded above by 1)

Each of these terms on the right-hand side above is since

and satisfies our usual conditions. As , and similarly for , we may also bound and simply by using the above estimates along with the triangle inequality and linearity of the integral. Thus, provided that we must have . Clearly also .

Secondly, we claim that . Suppose not; then there exist and such that for each . Setting

if (which must occur for all but finitely many ) then by the mean value theorem we can choose such that . But , so , contradicting the assumption that satisfies the usual conditions (specifically the requirement that ).

Thirdly, we show that . By Minkowski’s inequality,

but

and the same calculation holds for . Similarly by writing out in terms of , and and applying Minkowski’s inequality we get that

Our final claim is that . Indeed, using various facts just established,

so that (since )

as required. ∎

Our next lemma establishes that for sufficiently small , — which we think of as the good part of the tube — stretches to near the top and bottom edges of the -tube for almost proportion of the time. To do this we use the identity given in Lemma 13 combined with the spine decomposition. For and , let

Lemma 21.

Fix and . If then for sufficiently small and large , we have

Proof.

Fix and ; we show that for

and all sufficiently large we have

We begin working with and ; we shall move back to and towards the end of the proof. Let

and define three subsets, , and , of by

and

If is increasing at , then clearly for any

and hence

Thus if then, as in Proposition 15, we can apply the spine decomposition and Lemma 14 to get, for any ,

Using the identity from Lemma 13 together with Jensen’s inequality gives that for any ,

Now, since

we have shown that if then is large enough for all . If then running the same argument as above but using , in place of gives exactly the same result: so we have that is large enough for the half-region and by symmetry for the whole region . Hence it now suffices to show that for large ,

But for all large enough , since increases at rate at most (recall that , which is bounded) and ,

Also, for large enough we must have (otherwise would be negative). Thus for large

finally,

so since we have (again for large )

Hence for all large ,

as required. ∎

We now show that if a particle has remained in the tube for a long time, then it is very likely to have spent a long time in . The idea is that if stretches to within of the edge of the tube for a proportion of time, then in order to stay out of a particle must spend a long time in a tube of radius . We use simple estimates for the time spent by Brownian motion in such a tube and apply these to our problem via the many-to-one theorem (Theorem 12).

Lemma 22.

For any and ,

Proof.

We first claim that if we define by

then

We check, by approximation with functions, that Itô’s formula holds for . Define a function for each by setting

with , . Since , Itô’s formula tells us that

Since Lebesgue-almost everywhere, by bounded convergence

and uniformly so for each , -almost surely. Also, by the Itô isometry

since uniformly, the right hand side above converges to zero, and hence

Thus Itô’s formula does indeed hold for , and since

our claim holds. Now recall that under , the spine’s motion is simply a Brownian motion, so

Thus

establishing the result. ∎

Lemma 23.

Fix and . If then for sufficiently small and large , we have

Proof.

For any , by Lemma 21 we may choose and such that

Then if the spine particle is to have spent less than time in (yet remained within the tube of width ) then it must have spent at least within of the edge of the tube (provided that is large enough). That is, for , if we let

then

In fact, using the fact that if then we may apply two simple Girsanov measure changes and our usual estimates on them. The first will give the spine drift , and the second will give it an extra drift . Letting

we have

Using the estimate given in Lemma 22, and usual condition (III), we get that for large enough

Finally, taking and using the many-to-one theorem (Theorem 12), for large

We now combine the above results to achieve the aim of this section.

Proposition 24.

Recall that is the extinction time for the process. If then

Proof.

We note that , so it suffices to show that for any ,

To this end, fix and choose small enough and large enough that

(this is possible by Lemma 23). Now choose an integer large enough such that . Finally, choose large enough that

Then

Now, if a particle has spent at least time in then (by the choice of , since the births along form a Poisson process of rate ) it has probability at least of having at least births whilst in . Each of these particles born within launches an independent population from a point , so that

where each is a non-negative martingale on the interval with law equal to that of started from for some , and hence satisfying . Thus

which completes the proof. ∎

We draw our results together as follows.

7 Extending the class of functions

As promised, we can extend Theorem 1 to cover more general subsets of in an obvious way: if a set is contained within (or contains) an -tube about a function , then the set of particles with paths in is a subset (respectively, superset) of the set of particles with paths within of , and if satisfies our usual conditions then we have an immediate upper (lower) bound on the number of particles within . That is, for any ,

| (5) |

and

| (6) |

where both suprema are taken over all and such that satisfies our usual conditions and

both infima are taken over all and such that satisfies our usual conditions and

and

The obvious question now is whether this allows us to give growth rates for all sets in . The answer is no: there are still some seemingly reasonable sets that are not covered (which we shall see shortly).

Thus the natural question becomes whether we can instead characterise, in a more succinct way, the class of functions that Theorem 1 does cover, subject to using the extensions provided by (5) and (6). Can we weaken our usual conditions in some way that we can easily write down? The answer again seems to be, more or less, no. We may drop condition (I) as our eventual growth rate does not depend on the initial position of the particle as long as there is a path within our set that starts at the same point as the initial position of the first particle. We may also effectively drop condition (IV) — since it is not possible to get without violating condition (III), and the case can always be covered either by bounding above using (5) and (6) or by using the many-to-one theorem, Theorem 12, more directly. However the interesting conditions (II) and (III) are difficult to shake off, a fact which is best demonstrated by a series of examples.

It is easiest to first consider condition (III).

Example 6.

Take to be constant, and let

then as , converges uniformly to the zero function, . By Theorem 1 we know that on survival,

However, if the result of Theorem 1 held for each then by approximation via (5) and (6) we would have (on survival)

Of course, does not satisfy usual condition (III) and hence this contradiction does not appear – but the example shows that we cannot simply drop the requirement that .

Example 7.

Take and . Intuitively, the sine term oscillates so fast for large that we are effectively constrained within a tube of constant width 1. Thus we expect (and it is not too hard to imagine a hands-on proof using Theorem 1) that we should have a growth rate of . However, one may show (for example by using the periodicity of sine and approximating the integral by a sum) that

so that if the result of Theorem 1 held in this case we would have a growth rate of at least . Again, does not satisfy usual condition (III) and we see that we cannot just drop the requirement that .

Example 8.

Take , , and . Then the growth rate for is ; and since the -tube about is contained in the -tube about , we must have a growth rate for of at least (in fact it is exactly since it is well-known that the growth rate of the entire system is ). If the result of Theorem 1 held for then its growth rate would be ; so we see that we cannot simply drop the condition that .

Now consider condition (II). We can approximate any continuous function with twice continuously differentiable functions, but then how do we approach the conditions on the second derivative (from condition (III))? Even for constant , there are some nowhere-differentiable paths such that we may find a growth rate for using (5) and (6), and some for which we may not. The lack of even a first derivative to work with in these cases precludes the existence of an obvious simple condition to tell us where to draw the line between these two groups. We claim simply that any non-smooth sets are best considered on a case-by-case basis using Theorem 1 together with (5) and (6).

For example, again with constant , we may easily (by approximating by its partial sums) give a growth rate for the function

(where is a positive odd integer, and ), which is a time change of a Weierstrass function and hence, by the chain rule, nowhere differentiable. On the other hand we cannot give an exact growth rate along (almost) any given Brownian path: any uniformly approximating functions must (by the fact that Brownian motion has independent increments) violate our conditions on the second derivative of in (III).

8 The critical case

Of course, it is also possible to ask what happens when , although as we stated in Section 2.3, we are unable to give a general theory. We did, however, state two results in Section 2.3 as examples of what may be achieved by adjusting our earlier methods, and we prove those now.

Proof of Theorem 3.

In the case we may simply mimic the requisite part of the proof of Proposition 15, using the fact that for ,

and

Now suppose that . We proceed in very much the same way as in the main part of the article, leaving out many of the details. Direct calculation reveals that for ,

and

Thus, by the spine decomposition,

which converges as provided that . We deduce that provided that , and indeed for all and since for fixed , increasing can only increase the probability of survival. The same argument as Proposition 17 gives

Now, take and define and . Note that the -tube is contained within the -tube. Define

and note that the same argument as in Proposition 16 gives that on we have

Thus it suffices to show that agrees with up to a set of zero probability.

Following Lemma 23 and Proposition 24, we see that in fact it suffices to show that for any we can bound from below the probability that a particle in which is not within of the edge of the -tube contributes something positive to , in analogy with Lemma 21. But , and so instead we show that a particle in which is not within of the edge of the -tube contributes something positive to .

Now (possibly subject to decreasing further, but this is no problem) we may use the argument given in Lemma 21 to show that for small enough the set for stretches to near the top and bottom of the tube: even when we are distance from the top edge of the tube at time , the smaller tube with radius about fits (for all times ) within the tube of radius about . Then by using the spine decompositon and Jensen’s inequality as in Proposition 15, we can bound the probability of contributing to away from zero (over all ). We may take the same approach when starting from a position closer to the centre of the tube (that is, further than from the edge). Thus, for small enough , for stretches to within of the edge of the tube for all times . By the argument above, this is enough to complete the proof as in Lemma 23 and Proposition 24. ∎

Proof of Theorem 4.

The first part of the proof proceeds exactly as that of Theorem 3, but with

and

the spine decomposition converges if

so if

But increasing makes the right-hand side of this inequality larger as soon as , and increasing can only make larger, so (after some rearrangements) we deduce that provided either and or and .

Under , diverges to infinity if . Since , this is impossible if ; so we need and . If almost surely under , then by Lemma 11, almost surely under .

The calculations of the s and s are standard, as in Propositions 15, 16 and 17. However, we must again take a different approach to show that agrees with up to a set of zero probability. Our proof, below, is specially adapted to this particular case and takes advantage of the convenient — and well-known — fact that .

We can easily show, straight from the spine decomposition and as in previous calculations, that for any , there exists such that stretches to within of the edges of the tube at time for any . Thus (in analogy with Lemma 23) we would like to show, loosely speaking, that with high probability, particles spend a long time outside the tubes of radius , nested just inside the upper and lower boundaries of our main tube about . The idea is that if particles do not want to leave then staying near the boundaries of the tube is a bad tactic. To be more precise about this, following the direction of part of the proof of Lemma 23 and setting

and

we have

Now, by our calculation of above, the exponential part

is at most for some constant and all large . By the many-to-one theorem,

We attempt to show that, for small , the probability

is at most .

For the sake of brevity we make some approximations here: for example we will use instead of in various places, and assume throughout that is large. Let , define

and for let

Then for any ,

which is smaller than when is large. We now ask how many of the occur strictly before . We know that if

then

and

This tells us that

and hence there must be at least of the strictly before . Let be a binomial random variable with parameters . At each , the spine is within distance of the boundary of the tube. If it jumps upwards by too much by time , then it leaves the tube; and it has at least opportunities to do so. Thus we deduce that

By choosing small we can make this smaller than , which is what we required. The rest of the proof follows just as in Proposition 24. ∎

As mentioned in Section 2.3, Theorems 3 and 4 should be compared with the work of Bramson [1], Lalley and Sellke [12], Kesten [10], Hu and Shi [8] and Jaffuel [9]. Kesten [10], if translated into the language of this article, effectively considers a “one-sided” tube with lower boundary the critical line and no upper boundary — he shows that there is extinction almost surely, and that the probability of survival up to time decays like . If we were to consider a tube with lower boundary the line and upper boundary we could obtain, by the above methods, a lower bound for Kesten’s asymptotic for the probability of survival up to time , which would agree with Kesten’s results up to a constant in the exponent. Unfortunately the corresponding upper bound, and more accurate calculations on the right-most particle in the style of Bramson [1], do not seem to be accessible via our current methods: the error term outweighs the fine adjustments necessary to investigate such quantities. We hope to carry out further work on these and other related issues in the future.

References

- [1] M. D. Bramson. Maximal displacement of branching Brownian motion. Comm. Pure Appl. Math., 31(5):531–581, 1978.

- [2] Y. Git. Almost sure path properties of branching diffusion processes. In Séminaire de Probabilités, XXXII, volume 1686 of Lecture Notes in Math., pages 108–127. Springer, Berlin, 1998.

- [3] R. Hardy and S. C. Harris. A conceptual approach to a path result for branching Brownian motion. Stochastic Process. Appl., 116(12):1992–2013, 2006.

- [4] R. Hardy and S. C. Harris. A spine approach to branching diffusions with applications to -convergence of martingales. In Séminaire de Probabilités, XLII, volume 1979 of Lecture Notes in Math. Springer, Berlin, 2009.

- [5] J. W. Harris, S. C. Harris, and A. E. Kyprianou. Further probabilistic analysis of the Fisher-Kolmogorov-Petrovskii-Piscounov equation: one sided travelling-waves. Ann. Inst. H. Poincaré Probab. Statist., 42(1):125–145, 2006.

- [6] S. C. Harris and M. I. Roberts. Branching Brownian motion: almost sure growth along scaled paths. Preprint, http://arxiv.org/abs/0906.0291, 2009.

- [7] S. C. Harris and M. I. Roberts. Measure changes with extinction. Statist. Probab. Lett., 79(8):1129–1133, 2009.

- [8] Y. Hu and Z. Shi. Minimal position and critical martingale convergence in branching random walks, and directed polymers on disordered trees. Ann. Probab., 37(2):742–789, 2009.

- [9] B. Jaffuel. The critical random barrier for the survival of branching random walk with absorption. Preprint, http://arxiv.org/abs/0911.2227, 2009.

- [10] H. Kesten. Branching Brownian motion with absorption. Stochastic Processes Appl., 7(1):9–47, 1978.

- [11] T. Kurtz, R. Lyons, R. Pemantle, and Y. Peres. A conceptual proof of the Kesten-Stigum theorem for multi-type branching processes. In K. B. Athreya and P. Jagers, editors, Classical and modern branching processes (Minneapolis, MN, 1994), volume 84 of IMA Vol. Math. Appl., pages 181–185. Springer, New York, 1997.

- [12] S. P. Lalley and T. Sellke. A conditional limit theorem for the frontier of a branching Brownian motion. Ann. Probab., 15(3):1052–1061, 1987.

- [13] Tzong-Yow Lee. Some large-deviation theorems for branching diffusions. Ann. Probab., 20(3):1288–1309, 1992.

- [14] R. Lyons. A simple path to Biggins’ martingale convergence for branching random walk. In K. B. Athreya and P. Jagers, editors, Classical and modern branching processes (Minneapolis, MN, 1994), volume 84 of IMA Vol. Math. Appl., pages 217–221. Springer, New York, 1997.

- [15] R. Lyons, R. Pemantle, and Y. Peres. Conceptual proofs of criteria for mean behavior of branching processes. Ann. Probab., 23(3):1125–1138, 1995.

- [16] Y. Lyons, R. with Peres. Probability on Trees and Networks. In progress. Available online: http://mypage.iu.edu/ rdlyons/prbtree/prbtree.html.

- [17] A.A. Novikov. On estimates and the asymptotic behavior of nonexit probabilities of a Wiener process to a moving boundary. Math. USSR Sbornik, 38(4):495–505, 1981.