Finite-size effect and the components of multifractality in financial volatility

Abstract

Many financial variables are found to exhibit multifractal nature, which is usually attributed to the influence of temporal correlations and fat-tailedness in the probability distribution (PDF). Based on the partition function approach of multifractal analysis, we show that there is a marked finite-size effect in the detection of multifractality, and the effective multifractality is the apparent multifractality after removing the finite-size effect. We find that the effective multifractality can be further decomposed into two components, the PDF component and the nonlinearity component. Referring to the normal distribution, we can determine the PDF component by comparing the effective multifractality of the original time series and the surrogate data that have a normal distribution and keep the same linear and nonlinear correlations as the original data. We demonstrate our method by taking the daily volatility data of Dow Jones Industrial Average from 26 May 1896 to 27 April 2007 as an example. Extensive numerical experiments show that a time series exhibits effective multifractality only if it possesses nonlinearity and the PDF has impact on the effective multifractality only when the time series possesses nonlinearity. Our method can also be applied to judge the presence of multifractality and determine its components of multifractal time series in other complex systems.

pacs:

05.45.Df, 05.45.Tp, 89.65.GhI Introduction

Turbulent flows exhibit multifractal nature. Two main pictures of multifractal analysis in the turbulence literature deal with the velocity fluctuations using the structure function approach and the energy dissipation rates using the partition function approach Frisch (1996). The difference between the two pictures is remarkable and there are a lot of efforts trying to relate the two sequences of scaling exponents. In addition, the power-law dependence of the structure function is more or less not perfect.

It is well known that there are many similarities between turbulent flows (velocity time series) and financial markets (equity prices) Ghashghaie et al. (1996); Mantegna and Stanley (1996); Mantegna and Stanley (1997, 2000). For instance, multifractality is one of the most elusive stylized facts in financial markets Ghashghaie et al. (1996); Mantegna and Stanley (1996); Mandelbrot (1999). Many different methods have been applied to characterize the hidden multifractal behavior of different financial variables, such as the fluctuation scaling analysis Eisler et al. (2005); Eisler and Kertész (2007); Jiang et al. (2007a), the structure function method Ghashghaie et al. (1996); Vandewalle and Ausloos (1998); Ivanova and Ausloos (1999); Schmitt et al. (1999, 2000); Calvet and Fisher (2002); Ausloos and Ivanova (2002); Górski et al. (2002); Alvarez-Ramirez et al. (2002); Balcilar (2003); Lee and Lee (2005a); Lee et al. (2006), the multifractal detrended fluctuation analysis (MF-DFA) Kantelhardt et al. (2002); Matia et al. (2003); Kwapień et al. (2005); Lee and Lee (2005b); Oświȩcimka et al. (2005a); Moyana et al. (2006); Jiang et al. (2007b); Lee and Lee (2007); Lim et al. (2007); Su et al. (2009), the partition function method Sun et al. (2001a, b); Ho et al. (2004); Wei and Huang (2005); Gu et al. (2007); Du and Ning (2008); Zhuang and Yuan (2008); Wei and Wang (2008); Zhou (2010); Jiang and Zhou (2008); Su and Wang (2009), the multiplier method Jiang and Zhou (2007), and the wavelet transform approaches Struzik and Siebes (2002); Turiel and Pérez-Vicente (2003, 2005); Oświȩcimka et al. (2005b), some of which are borrowed from the multifractal analysis of turbulence data. When the return time series is concerned, the structure function method and the MF-DFA method apply. For volatility time series, the partition function approach and the multiplier approach can be utilized.

The extracted multifractal nature has potential applications in financial engineering. Some researchers report that the width of the estimated multifractal spectrum is correlated to the price fluctuation in the future and thus can be used to predict price fluctuations Sun et al. (2001b); Wei and Huang (2005); Su and Wang (2009). In a similar vein, the so-called multifractal volatility has been introduced to measure stock market risks, which can be used to estimate the dynamic Value-at-Risk of an asset Wei and Wang (2008). There is also empirical evidence suggesting that multifractal analysis can be used to quantify the degree of inefficiency of markets in the sense that more developed stock markets have weaker multifractality Zunino et al. (2008, 2009) and an emerging market evolves to be more efficient with narrowing singularity width Wang et al. (2009).

However, understanding the origin of multifractality in financial markets and its components is still a subtle and open problem. For instance, standard multifractal analysis of an exactly monofractal financial model gives artificial multifractal behaviors Bouchaud et al. (2000). It is usually argued that the fat tails and the long-term power-law correlations are two possible sources of multifractal nature in financial time series Kantelhardt et al. (2002). It is obvious that possessing only linear correlations is not sufficient for the presence of multifractality and a nonlinear process with long-memory is necessary to have multifractality Saichev and Sornette (2006). Numerical investigations show that the reported multifractal nature in many real cases is stemmed from the large fluctuations of prices Lux (2004).

Empirically, the problem has been studied based on the multifractal detrended analysis of financial returns Zhou (2009). One conventional measure for quantifying the degree of multifractality is the width of singularity spectrum

| (1) |

Alternative measures are also used in some cases Zunino et al. (2008); de Souza and Queirós (2009). In this way, one can quantitatively determine the contribution of the correlation and PDF components Jin and Lu (2006); de Souza and Queirós (2009). In order to investigate the influence of temporal correlations in return series, one can randomly shuffle the original data and compare their singularity spectra Matia et al. (2003); Oświȩcimka et al. (2005b); Lee and Lee (2005b); Kwapień et al. (2005); Jin and Lu (2006); Kumar and Deo (2009); de Souza and Queirós (2009). All these studies show that the shuffled data have non-shrinking singularity width , comparable to the original width . These observations imply that the heavy-tailed distribution of the returns has a crucial impact on the singularity width. To understand the impact of the distribution, one can either remove large returns Oh et al. (2010) or generate surrogate data having a Gaussian distribution while keeping the linear correlation of the original data Norouzzadeh and Rahmani (2006); Lim et al. (2007); Su et al. (2009). In addition, the temporal correlations can be further separated into linear and nonlinear components, which have different effects on the multifractal spectrum Zhou (2009).

In this work, based on the partition function method of multifractal analysis, we propose that the apparent multifractality can be decomposed into three components caused by the nonlinear correlation, the linear correlation (long-term power-law memory) and the fat-tailed PDF, which can be characterized by the following expression:

| (2) |

We find for the first time that the linear correlation component is the outcome of the finite-size effect and thus the intrinsic multifractal nature is characterized by the effective multifractality composing of the nonlinearity component and the PDF component . These properties are very different from those of the MF-DFA results in Ref. Zhou (2009).

We will develop a systemic procedure to quantitatively determine the components of multifractality. The analysis is carried out based on the daily volatility data of the Dow Jones Industrial Average (DJIA) from 26 May 1896 to 27 April 2007 (totally 30147 trading days). The logarithmic returns is defined as

| (3) |

where is the price at time , and the volatility is computed as the absolute value of :

| (4) |

This simple definition is widely adopted in the Econophysics community.

This paper is organized as follows. Section II gives a brief description of the partition function approach for multifractal analysis and its numerical implementation. Section III designs a numerical procedure to confirm the presence of finite-size effect in the detection of multifractality in time series with a prescribed probability distribution. In Sec. IV, the three multifractal components are determined for the daily DJIA volatility, where the nonlinear correlation component and the fat-tail component are determined by comparing with surrogate time series with normal distributions. The impact of the fat-tailedness of the probability distribution on the apparent multifractality is further investigated in Sec. V using Student’s distributions and the Weibull distributions. We find that the fat-tailed PDF per se has no effect on the multifractality and its impact is due to its coupling with the nonlinear correlations. We finally provide some concluding remarks in Sec. VI.

II Multifractal analysis based on partition functions

The multifractal analysis in this paper is based on the partition function formalism Halsey et al. (1986). Our procedure is slightly different from the conventional algorithm in the calculation of the partition functions. Consider a time series . For a given integer time scale , we choose randomly integers uniformly distributed in . Then the measure enclosed in the interval is calculated

| (5) |

The -th partition function is calculated as follows

| (6) |

If the time series is power-law long-term correlated, we have

| (7) |

If the scaling exponent is a nonlinear function of , the time series possess multifractal nature. The singularity strength and its spectrum can be computed according to the Legendre transform of Halsey et al. (1986),

| (8) |

The advantage of using Eq. (6) is twofold. First, it gives better statistics when is close to . Second, it does not need to deal with the situation in which is not integer.

III Finite-size effect

The finite-size effect in the detection of multifractality has been documented for several uncorrelated time series. One example is time series having an exponential distribution, whose -order moment can be derived as von Hardenberg et al. (2000)

| (9) |

When the length of the time series is small, a spurious multifractal spectrum is detected, where the singularity width is significantly larger than zero. Only for sufficiently long time series with and for , the moment is approximated by . It follows immediately that , and . Therefore, the finite-size effect results in a spurious detection of multifractality from a monofractal signal if the length of the signal is short or the “scaling range” locates at small scales.

Another example is exponentially truncated Lévy flights with characteristic parameter , which exhibit a bifractal behavior such that when and when Nakao (2000). The multifractal spectrum shrinks into two points and . Extensive numerical experiments using uncorrelated time series obeying -Gaussian distributions with different tail exponents unveil a convergence to monofractalilty in the Gaussian attraction basin and to bifractality in the Lévy attraction basin Drożdż et al. (2009), which is consistent with the analytic results for exponentially truncated Lévy flights Nakao (2000).

More generally, according to the law of large numbers, the sum of i.i.d. random variables with mean and standard deviation converges to with much smaller fluctuations Hsu and Robbins (1947). Let be a sequence of independent random variables with mean and variance and

| (10) |

Denoting that

| (11) |

and

| (12) |

we have

| (13) |

According to the law of large numbers Hsu and Robbins (1947), converges to , if

| (14) |

where is the cumulative distribution of . Hence, converges to . In addition, according to the Central Limit Theorem, the distribution of is Gaussian:

| (15) |

We have

| (16) | |||||

where and for most are used. It follows immediately that , and . It indicates that the time series is monofractal and its “singularity spectrum” shrinks to a single point . A direct consequence is that any degree of multifractality observed in real uncorrelated time series is caused by a finite-size effect.

However, the impact of linear long-term correlations on the finite-size effect has not been investigated. It is well-known that financial volatility exhibits strong long-term memory Ding and Granger (1993); Mantegna and Stanley (2000). The Hurst index of the daily DJIA volatility is . In order to show that there is a finite-size effect in the detection of multifractality introduced by linear correlations in the volatility time series, we generate surrogate data that have the same probability distribution as the original time series of volatility, which can be done with the transformation method Press et al. (1996). We first construct the empirical cumulative distribution of volatility, which is the occurrence frequency of volatility less than . A sequence of random numbers are drawn from a uniform distribution. In order not to introduce very large values in the surrogate data of volatility caused by the edge effect, we perform the following map

| (17) |

The sequence of numbers are calculated according to the following transformation

| (18) |

which can be done numerically by linear or spline interpolations. The sample has the same distribution as the volatility .

We then introduce long memory (linear correlations) in the time series using an improved amplitude adjusted Fourier transform (IAAFT) algorithmSchreiber and Schmitz (1996), which is based on a simple iteration scheme and an improved version of the amplitude adjusted Fourier transform algorithm Theiler et al. (1992). The volatility data are sorted resulting in a new sequence , and we obtain the squared amplitudes of the Fourier transform of , denoted as . The initial sequence of the iteration is a random shuffle of . In the -th iteration, the squared amplitudes of the Fourier transform of are obtained and replaced by , which are transformed back, and then the the resulting series are replaced by but keeping the rank order.

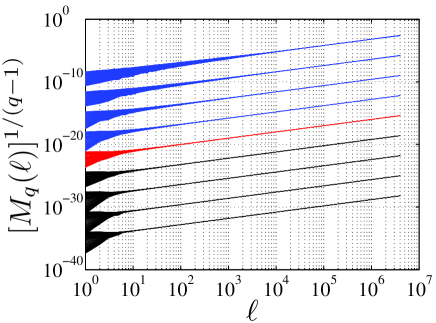

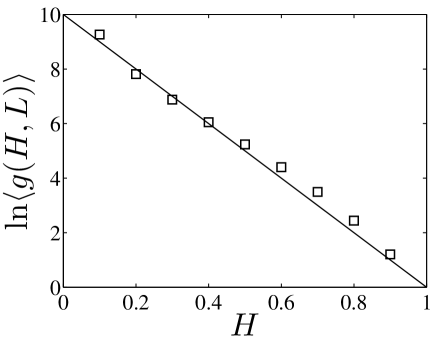

In our numerical experiments, we have investigated different Hurst indexes with . The length of the surrogate data ranges from to . Figure 1 shows the dependence of as a function of for different surrogate time series with different linear correlations. According to Eq. (7), the slope of linear lines in Fig. 1 is . For monofractal time series, these lines should be parallel and have identical slopes. For short time series, the scaling range locates on the left of plot and the lines are not parallel. Only when the time series is sufficiently long, the monofractality can be detected. More data points are needed to reach a decisive conclusion for strongly correlated time series with large Hurst index .

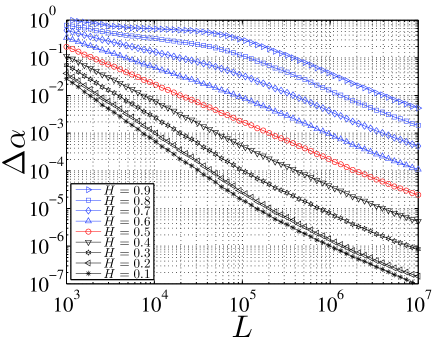

For each surrogate time series with Hurst index and size , a multifractal spectrum is determined within the scaling range . Figure 2 illustrates the finite-size effect in the detection of multifractality. For a given , the singularity width is a decreasing function of the series length . It is shown that the observed non-vanishing singularity spectrum in the surrogate data with only linear correlations is just the outcome of a finite-size effect,

| (19) |

Therefore we can define an effective singularity width

| (20) |

which accounts for the contribution of the nonlinear correlations and the fat tails to the apparent multifractal spectrum width.

According to Fig. 2, there is a power-law dependence between the singularity width and the length for each Hurst index when is not large:

| (21) |

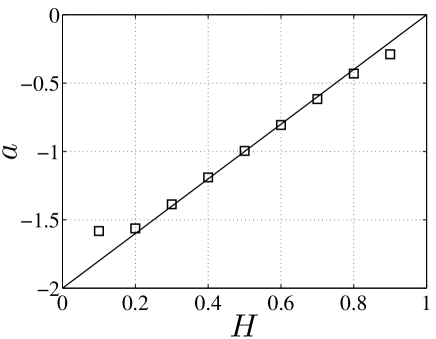

where is a function of . For each , we calculate in the scaling range . The dependence of the exponent on the Hurst index is shown in Fig. 3. We find a nice linear relation

| (22) |

except for . It is interesting to note that, for , we have and thus .

We assume that can be factorized as follows

| (23) |

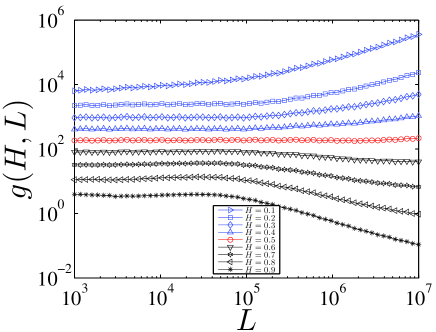

Figure 4 plots as a function of for each . We find that is almost independent of , in the scaling range. For the special case with the Hurst index , it is observed that the curve is horizontal in the whole range of .

According to Fig. 4, we can assume that is independent of in the scaling range. We calculate the average of in the scaling range

| (24) |

where is the number of scales in the scaling range. Figure 5 plots as a function of . We observe a linear relation

| (25) |

which is obtained based on the linear least-squares regression.

Combining Eqs. (22), (23) and (25), we obtain

| (26) |

when is not large. It is interesting to note that for in the whole range of . Note that this expression (26) is valid only for not large . Also, in the quantitative assessment of finite-size effect in correlated signals, one should use Fig. 2, rather than the above expression. For other applications, one need to conduct numerical simulations to produce a finite-size effect figure as Fig. 2 based on the sample distribution under investigation.

IV Determining the singularity width components

We now try to determine the components of the apparent singularity width . Figure 6 shows the multifractal spectrum of the original daily DJIA volatility time series. The apparent singularity width is found to be .

In order to determine the finite-size effect component caused by the linear long-term correlations in the volatility series, we use the iteration scheme Schreiber and Schmitz (1996) to generate surrogate data which have the same distribution and linear long-term correlations as the original volatility time series, while any underlying nonlinear correlations have been eliminated. One hundred surrogate time series have been generated and the average multifractal spectrum is shown in Fig. 6. The finite-size effect component is found to be

| (27) |

For the shuffled data , the resulting multifractal spectrum shrinks to a point as expected and the singularity spectrum width is close to zero, which confirms that the fat-tailedness of PDF alone cannot produce any multifractality. This finding is very different from that in the multifractal detrended fluctuation analysis of financial returns. It follows that the effective width of singularity is

| (28) |

which is significantly smaller than the apparent singularity width .

In order to determine the PDF component , we need to generate surrogate data in which the linear and nonlinear correlations are preserved while the original PDF is replaced by a reference PDF such that the PDF of the surrogate data has no impact on the resulting multifractality. It is not irrational to assume that the PDF component of Gaussian signals is negligible, that is, . We generate surrogate data for the returns which are drawn from a normal distribution

| (29) |

where and (in units of one trading day) are the sample mean and standard deviation of the daily DJIA returns . The surrogate volatility is thus , which has no temporal correlation and can be regarded as being shuffled.

The random numbers are rearranged to have the same rank ordering as so that the surrogate time series preserves the linear and nonlinear correlations of the original volatility Bogachev et al. (2007); Zhou (2008, 2009). The approach is to replace the raw data by random numbers drawn from a prescribed distribution, which is described as follows. For a given distribution, we generate a sequence of random numbers , which are rearranged such that the resulting series has the same rank ordering as the volatility series . In other words, should rank in the sequence if and only if ranks in the sequence Bogachev et al. (2007); Zhou (2008, 2009).

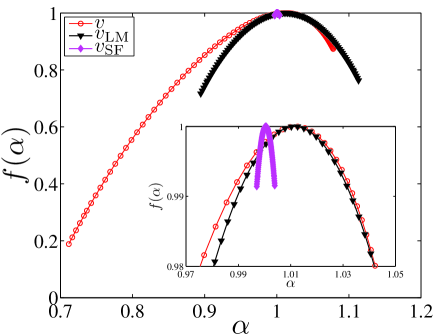

We generate 100 surrogates . For each time series , we further destroy its nonlinear correlations but keep its linear correlations to generate based on the iterated amplitude adjusted Fourier transformation algorithm Schreiber and Schmitz (1996). The average multifractal spectra for , , and are illustrated in Fig. 7. We find that, in the Gaussian surrogate case, the apparent singularity width is

| (30) |

for , its finite-size effect component is

| (31) |

for , and

| (32) |

for . Therefore, the effective width of singularity for the Gaussian surrogates is

| (33) |

Taking into account the assumption that , it follows immediately that the two components of the effective multifractality of the original volatility are

| (34) |

and

| (35) |

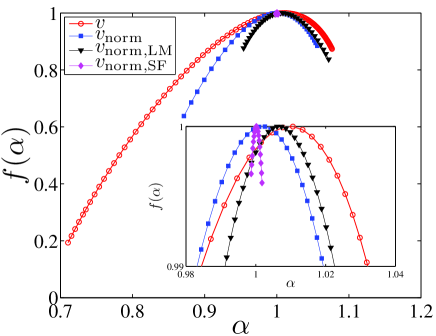

We note that, in the above framework, the nonlinearity component does not change when the PDF is replaced.

V Impact of PDF

In order to further confirm that the PDF of the time series has crucial influence on the multifractality, we investigate two families of distributions with fat tails. The first one is a family of Student’s t distributions

| (36) |

which have power-law tails with exponent . In our simulation, ranges from 3 to 10 with a spacing step of 0.5. For each tail exponent , we generate three types of surrogates for the volatility denoted as which has the same temporal correlations as , which has the same linear correlations as while any nonlinear correlations are eliminated, and which is the shuffled data of . We have generated 100 series of which has the same length as . For each , we generate two surrogates and . The multifractal spectrum of each time series is determined.

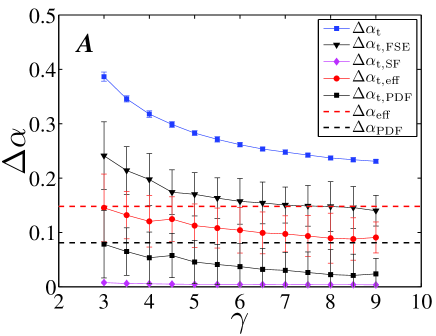

The apparent singularity width , the finite-size effect component , the effective singularity width , the PDF component are calculated and illustrated in Fig. 8 as a function of the tail exponent . All the quantities decreased with , implying that the multifractality is stronger when the distribution is fatter (characterized by smaller ). We also plot and for the original volatility as horizontal lines, both of which intersect with the and curves at . For , we have for , for , for , and . This striking feature is consistent with the inverse cubic law of financial returns Gopikrishnan et al. (1998), which also holds for daily DJIA returns Malevergne and Sornette (2006).

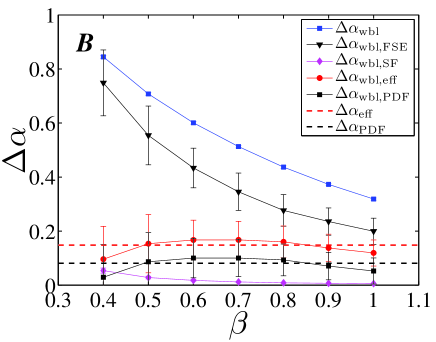

The second one is a family of Weibull distributions

| (37) |

where the shape parameter describes the heaviness of the tails and we require that . In our simulation, varies from 0.4 to 1.0 with a spacing step of 0.1. For each , 100 time series of the same length of are generated, which are manipulated to generate with the same rank ordering of and only with linear correlations.

The results are shown in Fig. 9. We find that , and decrease with , while and are concave functions with respect to . For small values, and increase with , which may be caused by the fact that there is a lack of statistics so that the fluctuations of are markedly large. Indeed, the error bar decreases with increasing . It is worth noting that the fluctuations of and are much less than the corresponding and . The large error bars of the PDF components and the nonlinearity components are caused by the large error bars of the corresponding finite-size effect components. In addition, in the case of exponential distribution with , we have for , for , and for . It follows that and .

VI Summary

We have proposed a method to decompose the apparent multifractality into three components associated with the finite-size effect, the nonlinearity, and the fat-tailed PDF. The finite-size effect component can be determined by the singularity width of surrogate data with the same PDF and linear correlations as the original time series after eliminating its nonlinear correlations. The PDF component can be calculated as the difference between the effective multifractality of the original series and the surrogate data drawn from a normal distribution with the linear and nonlinear correlations preserved. The impact of the fat-tailed PDF on the effective multifractality is the outcome of the coupling of the PDF and the nonlinearity since the shuffled data are monofractal with vanishing singularity width. The method proposed in this paper can be applied to investigate the presence of multifractality in time series and, if any, determine its components.

It is necessary to clarify the marked differences between the current work and Ref. Zhou (2009). First, the current work investigates financial volatility, while Ref. Zhou (2009) investigates financial returns, although the same data set of the daily DJIA index is used in both papers. Second, the partition function approach is used in this work, while the multifractal detrended fluctuation analysis is adopted in Ref. Zhou (2009). Third, the results are quite different. Ref. Zhou (2009) shows that the multifractal spectrum width of the shuffled data is comparable to the apparent singularity width , which means that the long-term correlations have minor impact on and the fat-tailed PDF plays a major role. In contrast, in Figs. 6, 7, 8 and 9 of the current paper, we have shown that

| (38) |

for shuffled time series with different PDFs. It is clear that

| (39) |

where is the singularity width of the shuffled data and is the shuffled data . This suggests that the contribution of the PDF is coupled with the nonlinearity. If there is no nonlinearity, the fat-tailedness of the PDF will not introduce any multifractality. In addition, with the presence of nonlinearity, the PDF does have impact on the effective multifractality.

As a last note, it is well-established that the phase-randomized surrogates of heartbeat series from healthy subjects have a narrower width of singularity () compared to its apparent multifractal width () based on the wavelet transform method Ivanov et al. (1999, 2001), which is in excellent agreement with our results.

Acknowledgements.

We are grateful to Stanislaw Drożdż for invaluable discussions. This work was partially supported by the “Shu Guang” project supported by Shanghai Municipal Education Commission and Shanghai Education Development Foundation under grant 2008SG29 and the Program for New Century Excellent Talents in University sponsored the Ministry of Education of People’s Republic of China under grant NCET-07-0288.References

- Frisch (1996) U. Frisch, Turbulence: The Legacy of A.N. Kolmogorov (Cambridge University Press, Cambridge, 1996).

- Ghashghaie et al. (1996) S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, and Y. Dodge, Nature 381, 767 (1996).

- Mantegna and Stanley (1996) R. N. Mantegna and H. E. Stanley, Nature 383, 587 (1996).

- Mantegna and Stanley (1997) R. N. Mantegna and H. E. Stanley, Physica A 239, 255 (1997).

- Mantegna and Stanley (2000) R. N. Mantegna and H. E. Stanley, An Introduction to Econophysics: Correlations and Complexity in Finance (Cambridge University Press, Cambridge, 2000).

- Mandelbrot (1999) B. B. Mandelbrot, Sci. Am. 298, 70 (1999).

- Eisler et al. (2005) Z. Eisler, J. Kertész, S.-H. Yook, and A.-L. Barabási, Europhys. Lett. 69, 664 (2005).

- Eisler and Kertész (2007) Z. Eisler and J. Kertész, EPL 77, 28001 (2007).

- Jiang et al. (2007a) Z.-Q. Jiang, L. Guo, and W.-X. Zhou, Eur. Phys. J. B 57, 347 (2007a).

- Vandewalle and Ausloos (1998) N. Vandewalle and M. Ausloos, Eur. Phys. J. B 4, 257 (1998).

- Ivanova and Ausloos (1999) K. Ivanova and M. Ausloos, Eur. Phys. J. B 8, 665 (1999).

- Schmitt et al. (1999) F. Schmitt, D. Schertzer, and S. Lovejoy, Appl. Stoch. Models Data Anal. 15, 29 (1999).

- Schmitt et al. (2000) F. Schmitt, D. Schertzer, and S. Lovejoy, Int. J. Theoret. Appl. Financ. 3, 361 (2000).

- Calvet and Fisher (2002) L. Calvet and A. Fisher, Rev. Econ. Stat. 84, 381 (2002).

- Ausloos and Ivanova (2002) M. Ausloos and K. Ivanova, Comput. Phys. Commun. 147, 582 (2002).

- Górski et al. (2002) A. Z. Górski, S. Drożdż, and J. Speth, Physica A 316, 496 (2002).

- Alvarez-Ramirez et al. (2002) J. Alvarez-Ramirez, M. Cisneros, C. Ibarra-Valdez, and A. Soriano, Physica A 313, 651 (2002).

- Balcilar (2003) M. Balcilar, Emerging Markets Financ. Trade 39, 5 (2003).

- Lee and Lee (2005a) K. E. Lee and J. W. Lee, J. Korean Phys. Soc. 46, 726 (2005a).

- Lee et al. (2006) J. W. Lee, K. E. Lee, and P. A. Rikvold, Physica A 364, 355 (2006).

- Kantelhardt et al. (2002) J. W. Kantelhardt, S. A. Zschiegner, E. Koscielny-Bunde, S. Havlin, A. Bunde, and H. E. Stanley, Physica A 316, 87 (2002).

- Matia et al. (2003) K. Matia, Y. Ashkenazy, and H. E. Stanley, Europhys. Lett. 61, 422 (2003).

- Kwapień et al. (2005) J. Kwapień, P. Oświȩcimka, and S. Drożdż, Physica A 350, 466 (2005).

- Lee and Lee (2005b) K. E. Lee and J. W. Lee, J. Korean Phys. Soc. 47, 185 (2005b).

- Oświȩcimka et al. (2005a) P. Oświȩcimka, J. Kwapień, and S. Drożdż, Physica A 347, 626 (2005a).

- Moyana et al. (2006) L. G. Moyana, J. de Souza, and S. M. D. Queiros, Physica A 371, 118 (2006).

- Jiang et al. (2007b) J. Jiang, K. Ma, and X. Cai, Physica A 378, 399 (2007b).

- Lee and Lee (2007) K. E. Lee and J. W. Lee, Physica A 383, 65 (2007).

- Lim et al. (2007) G. Lim, S. Kim, H. Lee, K. Kim, and D.-I. Lee, Physica A 386, 259 (2007).

- Su et al. (2009) Z.-Y. Su, Y.-T. Wang, and H.-Y. Huang, J. Korean Phys. Soc. 54, 1395 (2009).

- Sun et al. (2001a) X. Sun, H.-P. Chen, Z.-Q. Wu, and Y.-Z. Yuan, Physica A 291, 553 (2001a).

- Sun et al. (2001b) X. Sun, H.-P. Chen, Y.-Z. Yuan, and Z.-Q. Wu, Physica A 301, 473 (2001b).

- Ho et al. (2004) D.-S. Ho, C.-K. Lee, C.-C. Wang, and M. Chuang, Physica A 332, 448 (2004).

- Wei and Huang (2005) Y. Wei and D.-S. Huang, Physica A 355, 497 (2005).

- Gu et al. (2007) G.-F. Gu, W. Chen, and W.-X. Zhou, Eur. Phys. J. B 57, 81 (2007).

- Du and Ning (2008) G.-X. Du and X.-X. Ning, Physica A 387, 261 (2008).

- Zhuang and Yuan (2008) X.-T. Zhuang and Y. Yuan, Physica A 387, 511 (2008).

- Wei and Wang (2008) Y. Wei and P. Wang, Physica A 387, 1585 (2008).

- Zhou (2010) W.-X. Zhou, J. Manag. Sci. China (in Chinese) 13, in press (2010).

- Jiang and Zhou (2008) Z.-Q. Jiang and W.-X. Zhou, Physica A 387, 3605 (2008).

- Su and Wang (2009) Z.-Y. Su and Y.-T. Wang, J. Korean Phys. Soc. 54, 1385 (2009).

- Jiang and Zhou (2007) Z.-Q. Jiang and W.-X. Zhou, Physica A 381, 343 (2007).

- Struzik and Siebes (2002) Z. R. Struzik and A. P. J. M. Siebes, Physica A 309, 388 (2002).

- Turiel and Pérez-Vicente (2003) A. Turiel and C. J. Pérez-Vicente, Physica A 322, 629 (2003).

- Turiel and Pérez-Vicente (2005) A. Turiel and C. J. Pérez-Vicente, Physica A 355, 475 (2005).

- Oświȩcimka et al. (2005b) P. Oświȩcimka, J. Kwapień, S. Drożdż, and R. Rak, Acta Phys. Pol. B 36, 2447 (2005b).

- Zunino et al. (2008) L. Zunino, B. M. Tabak, A. Figliola, D. G. Pérez, M. Garavaglia, and O. A. Rosso, Physica A 387, 6558 (2008).

- Zunino et al. (2009) L. Zunino, A. Figliola, B. M. Tabak, D. G. Pérez, M. Garavaglia, and O. A. Rosso, Chaos, Solitons & Fractals 41, 2331 (2009).

- Wang et al. (2009) Y.-D. Wang, L. Liu, and R.-B. Gu, Int. Rev. Financ. Anal. 18, 271 (2009).

- Bouchaud et al. (2000) J.-P. Bouchaud, M. Potters, and M. Meyer, Eur. Phys. J. B 13, 595 (2000).

- Saichev and Sornette (2006) A. Saichev and D. Sornette, Phys. Rev. E 74, 011111 (2006).

- Lux (2004) T. Lux, Int. J. Modern Phys. C 15, 481 (2004).

- Zhou (2009) W.-X. Zhou, EPL 88, 28004 (2009).

- de Souza and Queirós (2009) J. de Souza and S. M. D. Queirós, Chaos, Solitons & Fractals 42, 2512 (2009).

- Jin and Lu (2006) H. Jin and J.-Z. Lu, Il Nuovo Cimento B 121, 987 (2006).

- Kumar and Deo (2009) S. Kumar and N. Deo, Physica A 388, 1593 (2009).

- Oh et al. (2010) G. Oh, C. Eom, S. Havlin, W.-S. Jung, F.-Z. Wang, H. E. Stanley, and S. Kim, Phys. Rev. E XXX, XXX (2010).

- Norouzzadeh and Rahmani (2006) P. Norouzzadeh and B. Rahmani, Physica A 367, 328 (2006).

- Halsey et al. (1986) T. C. Halsey, M. H. Jensen, L. P. Kadanoff, I. Procaccia, and B. I. Shraiman, Phys. Rev. A 33, 1141 (1986).

- von Hardenberg et al. (2000) J. von Hardenberg, R. Thieberger, and A. Provenzale, Phys. Lett. A 269, 303 (2000).

- Nakao (2000) H. Nakao, Phys. Lett. A 266, 282 (2000).

- Drożdż et al. (2009) S. Drożdż, J. Kwapień, P. Oświecimka, and J. Speth (2009), arXiv: 0907.2866.

- Hsu and Robbins (1947) P. L. Hsu and H. Robbins, Proc. Natl. Acad. Sci. U.S.A. 33, 25 (1947).

- Ding and Granger (1993) Z.-X. Ding and C. W. J. Granger, J. Emp. Financ. 73, 185 (1993).

- Press et al. (1996) W. Press, S. Teukolsky, W. Vetterling, and B. Flannery, Numerical Recipes in FORTRAN: The Art of Scientific Computing (Cambridge University Press, Cambridge, 1996).

- Schreiber and Schmitz (1996) T. Schreiber and A. Schmitz, Phys. Rev. Lett. 77, 635 (1996).

- Theiler et al. (1992) J. Theiler, S. Eubank, A. Longtin, B. Galdrikian, and J. D. Farmer, Physica D 58, 77 (1992).

- Bogachev et al. (2007) M. I. Bogachev, J. F. Eichner, and A. Bunde, Phys. Rev. Lett. 99, 240601 (2007).

- Zhou (2008) W.-X. Zhou, Phys. Rev. E 77, 066211 (2008).

- Gopikrishnan et al. (1998) P. Gopikrishnan, M. Meyer, L. A. N. Amaral, and H. E. Stanley, Eur. Phys. J. B 3, 139 (1998).

- Malevergne and Sornette (2006) Y. Malevergne and D. Sornette, Extreme Financial Risks: From Dependence to Risk Management (Springer, Berlin, 2006).

- Ivanov et al. (1999) P. C. Ivanov, L. A. N. Amaral, A. L. Goldberger, S. Havlin, M. G. Rosenblum, Z. R. Struzik, and H. E. Stanley, Nature 399, 461 (1999).

- Ivanov et al. (2001) P. C. Ivanov, L. A. N. Amaral, A. L. Goldberger, S. Havlin, M. G. Rosenblum, H. E. Stanley, and Z. R. Struzik, Chaos 11, 641 (2001).