Extracting strong measurement noise from stochastic series:

applications to empirical data

P.G. Lind

Center for Theoretical and Computational Physics,

University of Lisbon,

Av. Prof. Gama Pinto 2, 1649-003 Lisbon, Portugal

Departamento de Física, Faculdade de Ciências

da Universidade de Lisboa, 1649-003 Lisboa, Portugal

M. Haase

Institute for High Performance Computing, University of Stuttgart,

Nobelstr. 19, D-70569 Stuttgart, Germany

F. Böttcher

Institute of Physics, University of Oldenburg,

D-26111 Oldenburg, Germany

J. Peinke

Institute of Physics, University of Oldenburg,

D-26111 Oldenburg, Germany

D. Kleinhans

Institute for Marine Ecology, University of Gothenburg,

Box 461, SE-405 30 Göteborg, Sweden

Institute of Theoretical Physics, University of

Münster, D-48149 Münster, Germany

R. Friedrich

Institute of Theoretical Physics, University of

Münster, D-48149 Münster, Germany

Abstract

It is a big challenge in the analysis of experimental data to disentangle

the unavoidable measurement noise from the intrinsic dynamical noise.

Here we present a general operational method to extract measurement noise

from stochastic time series, even in the case when the amplitudes of

measurement noise and uncontaminated signal are of the same order

of magnitude.

Our approach is based on a recently developed method for a nonparametric

reconstruction of Langevin processes.

Minimizing a proper non-negative function the procedure is able to correctly

extract strong measurement noise and to estimate

drift and diffusion coefficients in the Langevin equation describing the

evolution of the original uncorrupted signal.

As input, the algorithm uses only the two first conditional moments

extracted directly from the stochastic series and is therefore

suitable for a broad panoply of different signals.

To demonstrate the power of the method we apply the algorithm to synthetic

as well as climatological measurement data, namely the daily North Atlantic

Oscillation index, shedding new light on the discussion of the nature of its

underlying physical processes.

Recently, much effort has been made to uncover

the dynamical process underlying a given time series of scale and time

dependent complex systemsschreiberbook ; friedrich08 ; abarbanel93 .

In many cases it is possible to describe such systems

by a Langevin equation, extracted directly from the data, which separates

the deterministic and stochastic processes inherent to the

systemfriedrich97 .

Such an approach has already been carried out successfully for instance

for data from turbulent fluid dynamicsnawroth07 , financial

datafriedrich00 , climate indicescollette04 ; lind05

and for electroencephalographic recordings from epilepsy

patientsprusseit08 ; lehnertz09 and additional improvements were proposed

to address the case of low sampling

rateskleinhans05 ; gottschall08 .

However, typically the signal is subject to noise, due to

experimental constraints or due to the measurement or discretization

procedure leading to the data set to be studied.

Such noise is not intrinsic to the system, differing from what

is known as dynamical noise, and therefore one is interested to

separate it from the stochastic process.

We call such non-intrinsic noise measurement noise.

To separate the measurement noise from the dynamics of the measured

variable different predictor models or schemes for noise reduction

may be usedschreiberbook ; abarbanel93 .

In this context, an alternative procedure has been proposedboettcher06

to extract the intrinsic dynamics associated with Langevin processes

strongly contaminated by measurement noise, based solely on the two

conditional moments directly calculated

from the datagottschall08 ; boettcher06 .

In this manuscript we will revisit this nonparametric procedure,

describing it in detail and explaining the main steps for its

implementation, with the aim of applying it to empirical data sets.

Let us consider a one-dimensional Langevin process

(an extension to more dimensions is straightforward) defined as

(1)

where represents a Gaussian -correlated

white noise

and

.

Functions and are the drift and diffusion

coefficients defined as

(2)

for , where denotes the -th order conditional

moment of the data, as explained below.

Further, we consider that is ‘contaminated’ by a Gaussian

-correlated measurement white noise, which leads to the series

of observations

(3)

where denotes the amplitude of the measurement noise.

When there is no measurement noise (), Eq. (3) yields

the particular case , and the evolution

equation underlying the signal can be extracted directly from

the two conditional moments ()

In the presence of measurement noise () the conditional

moments depend on , and . Since generally

the limit

(5)

does not exist, Eq. (3) cannot be applied.

The aim of this paper, however, is to explicitly derive a procedure

which can transform the functional form of the ’noisy conditional

moments’ and

at small

into the ’true’ coefficients and and simultaneously

retrieve the amplitude of the associated measurement noise.

For that, we show that for fixed is typically

linear in for a certain range of values

(see Fig. 4 below). Therefore, even when one

can estimate the quantities

(6)

We start in Sec. II by briefly describing

the procedure to extract Langevin equations from data sets

and show how the drift and diffusion coefficients depend on the

measurement noise strength .

In particular, we will see that the proposed estimatesiefert03

does not

yield the correct value when the measurement noise is too strong.

In Sec. III we then proceed to minimize a proper least

square function using the Levenberg-Marquardt procedurenumrecip .

By applying this algorithm to synthetic data we show that indeed

this approach is able to reliably extract the noise amplitude even in

cases where it is of the same order as the synthetic signal without

noise.

Furthermore, the procedure yields simultaneously more accurate estimates

for the clean signal .

Finally, in Sec. IV, we apply this framework to

an empirical data set, namely the North Atlantic Oscillation daily

indexijbc , giving some insight from the obtained results to

the underlying system.

Discussion and conclusions are given in Sec. V, where further

possible applications are proposed.

All details concerning the implementation of the minimization

procedure to extract strong measurement noise are given as appendices.

II Stochastic time series with strong measurement noise

We consider a time series generated by integrating Eq. (1)

with drift and diffusion coefficient assumed to be linear and quadratic

forms respectively

(7a)

(7c)

and by adding separately to each data point the measurement

term in Eq. (3).

Though we concentrate on the particular expressions for and

given above, it should be stressed that they comprehend a large collection

of different processes, such as Ornstein-Uhlenbeck processesboettcher06 .

Further, some generalizations may be carried out as will be discussed in

Sec. V.

Using Eqs. (7a) and (7b), one has six parameters: five

coefficients defining the evolution equation of the clean signal

and a sixth parameter for the amplitude of the measurement noise.

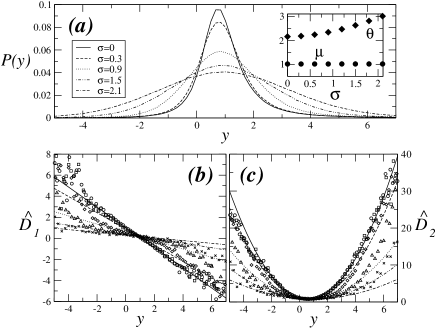

Figure 1: Langevin time series with different measurement

noise strengths. Here we show

(a) the probability density function of the series

with noise (see Eq. (3)), with the corresponding mean value

and standard deviation in the inset, and the

corresponding functions

(b) and

(c) , see Eq. (6).

In all cases, the assumed time series without measurement

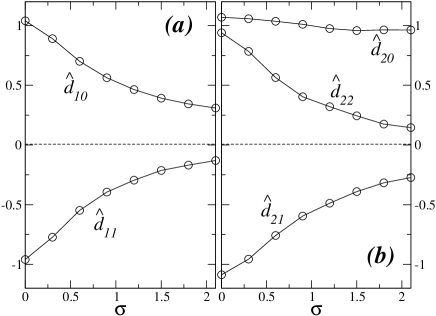

noise uses the coefficients and .Figure 2: Noise dependence of functions and

(see text and Eq. (6))

The underlying Langevin time series without noise

is the same as in Fig. 1.

Figure 1 illustrates this influence of noise for a particular

choice of .

As shown in Fig. 1a, for increasing one obtains

broader probability density functions as one intuitively

expects.

Quantitatively, the standard deviation of varies

quadratically with the measurement noise , while the mean value

of remains constant, as shown in the inset of Fig. 1a.

The estimated functions and

change significantly, as shown in Fig. 1b and 1c

respectively.

Assuming and

,

Fig. 2 shows how the estimated parameters deviate

from the ‘true’ uncontaminated values in Eq. (7)

when measurement noise increases.

Notice that for – see left vertical axis in the plots of

Fig. 2 – the estimated parameter values are approximately

correct.

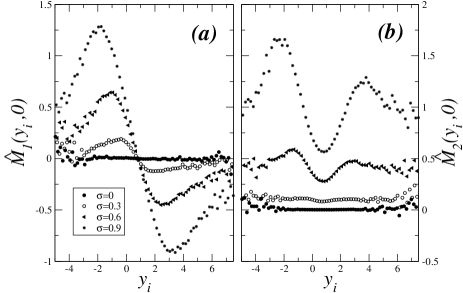

Figure 3: Conditional moments and

as a function of bin , for and different measurement

noise strengths. The asymmetry of is due to

(see Eqs. (7)).

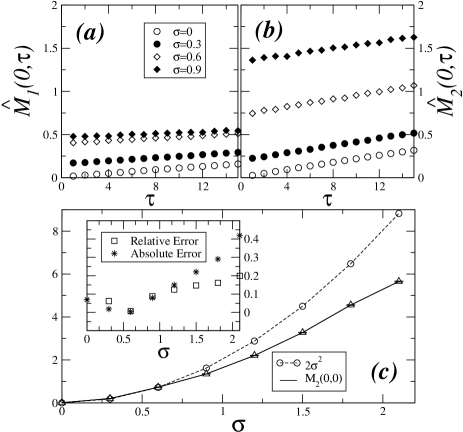

The same as in Fig. 1 was used.Figure 4: Conditional moments

(a) and

(b) as a function of , for

bin and different measurement noise strengths.

In (c) one compares the true measurement noise

with the approximation

given in Eq. (9).

In the inset the corresponding absolute and relative erros are given

by and

respectively. Errors for are negligible.

The same as in Fig. 1 was used.Figure 5: Functions , , and

(symbols) defining the conditional moments in

Eqs. (8).

The underlying Langevin time series without noise is

characterized by a drift coefficient and

a diffusion coefficient .

The measurement noise was fixed at .

Each hat-function is compared with the corresponding

integral form in Eqs. (10) using the first estimate

of parameters values (dashed lines) and the true values (solid lines).

To correctly derive the drift and diffusion coefficients and

when is strong, we consider the measured conditional

moments and , as in

Eq. (4), the hat indicating that they are calculated

from the measured data directly.

Since this conditional moments depend in a non trivial way on both

time and amplitude , we approximate them up to first

order on :

(8a)

(8c)

(8e)

(8g)

where is taken in the range for

each bin , and depends on the binning considered.

Appendix A gives the full derivation of Eqs. (8).

Figure 3 shows both conditional moments for and

with different measurement noise strengths.

Conversely, in Fig. 4a and 4b one sees that the

conditional moments depend linearly on for a fixed amplitude

, which justifies the approximation assumed in Eqs. (8).

Therefore, to study the dependence of the conditional moments on

we will consider the linear decompositions in Eqs. (8), as

done in Fig. 5.

Our simulations with synthetic data have shown that using a to

large range of values yields results for and

deviated from their true values. The best estimation for both

Kramers-Moyal coefficients are obtained using the range .

Notice that for sufficiently

small measurement noise a good estimate of it is given

byboettcher06 ; siefert03

(9)

where is the average value of data points in the

time series. For details see Append. A.

However, as shown in Fig. 4c, this approximation is no longer

valid for sufficiently high measurement noise,

namely when (see inset of Fig. 4c)

and even otherwise coefficients and are not correctly estimated

(see Fig. 2).

Therefore, a better algorithm to estimate such parameters is necessary.

The heart of our procedure to correctly estimate measurement noise

lies in the fact that while the functions and

(i=1,2) are obtained explicitly for each

bin value , functions and depend

generally on the drift and diffusion coefficients as follows:

(10a)

(10c)

(10e)

(10g)

where is the probability for the system to adopt the

value when a measured value is observed.

For details about the derivation of functions in Eqs. (10)

see Append. A and for the explicit expression of

see Append. B.

In Fig. 5 we illustrate both the hat-functions in Eqs. (8)

and their integral form in Eqs. (10).

Due to the measurement noise fixed in this example at the

hat-functions (symbols) are not properly fitted by the integral form

in Eqs. (10)

using the first estimate (dashed lines) of the parameters ,

taken from Fig. 2, and , computed from

Eq. (9).

If instead we use the true parameter values in the integral forms of

our and functions a proper fit is obtained (solid lines).

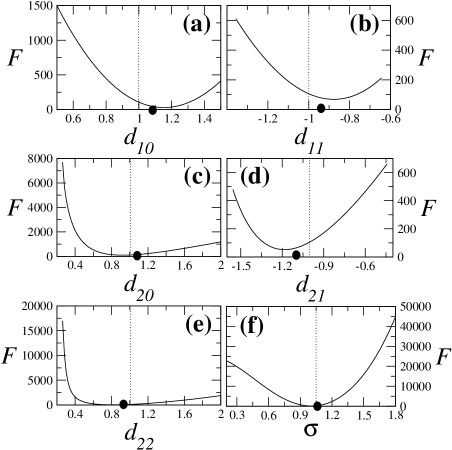

Figure 6: Function in Eq. (17) as a function of

(a) ,

(b) ,

(c) ,

(d) ,

(e) and

(f) .

The same situation as in Fig. 2 is here chosen:

, and .

Dashed lines indicate the true values used for generating the

data series, while the bullet indicates the estimated values

of the Kramers-Moyal coefficients for .

In each plot while varying one parameter, the remaining ones

are fixed at their true values (see text).

Therefore, the problem we want to solve is to determine the parameters

that minimize the function:

(17)

where the summation extends over all bins,

is the error associated to function at the value

and similarly for ,

and .

Notice that the values of such and

are taken directly from the data only.

See Appendix A for details.

Taking again the example illustrated in Fig. (2) with

we plot in Fig. 6 function in Eq. (17)

as function of each one of the parameters keeping all others fixed

at their true values.

Evidently, the estimated values are near the minimum of in each

case. Further, the one-dimensional cuts of function show only one

minimum. One should note however that, for the entire -dimensional

parameter space, several local minima of may appear.

In fact, after minimizing by varying one parameter, function also

changes as a function of the other parameters, i.e. its minimum as a

function of the other parameter changes.

In the next Section we will see how to minimize function , in order to

find good estimates for the correct values for each parameter.

III Optimization procedure

After computing the functions , ,

and as well as the

corresponding errors , etc, directly from

the measured time series

and estimating the coefficients and given by the functional

forms in Eqs. (7)

there are several ways to minimize .

All of them start from the initially estimated set of values for the

parameters and iteratively improve the solution, by finding lower values

of , till convergence is attained.

To proceed the following remark should be considered.

Parameter can be always eliminated with a simple

transformation .

Alternatively, and since we do not know beforehand the

true values of and we can consider also the fact

that averaging Eq. (1) yields

and consider the transformation

.

With these arguments, we henceforth disregard , which reduces the

dimension of parameter space by one. Parameter is computed

from the relations above, only after minimizing .

For simplicity the primes in will be omitted.

The simplest way is to minimize each term in and repeat that a large

number of times starting from different initial conditions for the

parameters, in a sort of a Monte Carlo procedure of random

walks bouchaud90 or Lévy-walksmetzler00 .

The Monte Carlo procedure assures that a substantial number of local

minimal for will be visited, and in the end we take the minimum

of all values found.

Simulations have shown however that a Monte Carlo procedure is too

expensive in this case, since there are different local minima and

the choice of the minimum is strongly path dependent.

We will therefore consider the Levenberg-Marquardt methodnumrecip .

For the Levenberg-Marquardt procedure one computes the first and second

derivative of . Symbolizing the parameters

and by with respectively, these derivatives read

(18)

(27)

(33)

In the right-hand side of Eq. (33) we neglect the terms containing

second derivatives of and functions.

This last approximation of neglecting second derivatives is

acceptable as far as the model is successfulnumrecip .

By symbolizing first and second derivatives as and

respectively the iterative procedure computes

the increments for each parameter (),

which are the solutions of

(34)

Furthermore,

one assumes that , which considering dimensional

analysisnumrecip can be written as:

(35)

where typically .

For a given value, instead of the second derivatives

one assumes for and

otherwise and solves Eq. (34)

for numrecip .

If , the parameter values are updated,

, and is typically decreased by .

Otherwise, if one increases by and

determines new increments .

The procedure stops after attaining the required convergence.

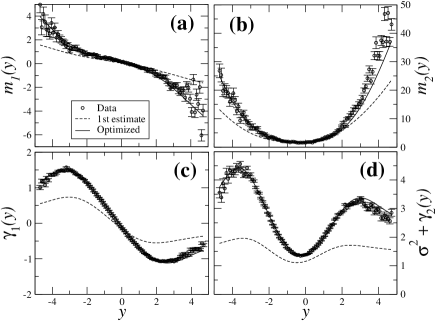

Figure 7: Functions , , and

for the Langevin process with ,

and . Symbols indicate the

functions obtained for the data, dashed line corresponds

to the first estimate of the parameters and solid line

corresponds to the parameter values obtained from the

Levenberg-Marquardt procedure (see text).

In this case, for the first estimate one has

while the final estimate retrieves .

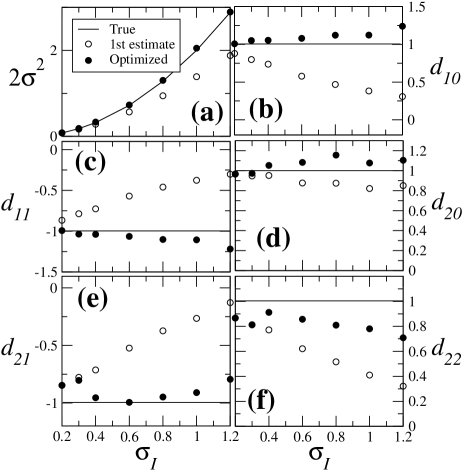

The true minimum is .Figure 8: Comparison of the optimized parameters values (bullet)

with the first estimate and the true values for different

input measurement noise strengths :

(a) ,

(b) ,

(c) ,

(d) ,

(e) ,

(f) .

The measurement noise is correctly extracted as well as

the parameters defining the drift coefficient

which controls the deterministic part of the underlying

evolution equation (see text).

Using the same data as generated in Fig. 5 with , we

now plot in Fig. 7 the functions and

for the data (symbols) and compare them with the integral forms of those

functions

for the first estimate of parameter values (dashed lines) and the optimized

solution obtained with the Levenberg-Marquardt procedure (solid lines).

Clearly, the optimized functions fit better the data and the minimum of

found is very close to its true value

(see caption of Fig. 7).

Notice that the optimized values are obtained for the

transformed data (), assuming

. In practice one obtains ,

typically two orders of magnitude smaller than the other coefficients.

Using , one

obtains the true coefficients according to

,

,

,

and

.

To show the power of the present procedure we next generate several

synthetic data sets from Eq. (1) with different

measurement noise amplitudes in the range .

The same and as in Fig. 2 is used.

Results are shown in Fig. 8.

The circles indicate the obtained parameter values for the first estimate,

as in Fig. 2. The solid lines indicate the true values used to

generate the data, while bullets indicate the value after optimization.

From Fig. 8a one sees that after optimization the value of

is always correctly determined.

Such finding is of major importance and shows the relevance of our

approach for practical applications even for strong measurement noise,

since the uncontaminated series typically lies within the range

, having therefore values close to the amplitude

of the measurement noise.

Figures 8b and 8c also show a very reliable estimate for

the two parameters and respectively, defining the drift

coefficient .

Since this coefficient characterizes the deterministic part of the

evolution equation for , this accurate estimate should provide valuable

insight into the dynamics of the underlying system.

As for the diffusion coefficient , Figs. 8d-f show

that the estimate of is no longer as good as for

the other parameters.

Parameter is reasonably estimated but the optimized estimate

is as good as the first one.

For stronger measurement noise,

namely for ,

one faces the problem that the optimization procedure is

sometimes stucked in a local minimum of the function

leading to unreliable coefficients . This is in principle

a shortcoming of the presently used minimization algorithm.

In addition, the function itself is based on estimated

functions and and therefore itself subject

to errors. A forthcoming study will address the observed issues

in the context of global optimization.

IV The North Atlantic Oscillation: an empirical example

In this section we apply our framework to the North Atlantic Oscillation

daily index, which presents data with strong measurement noise.

Table 1 summarizes the optimized values for all

parameter describing the data set, comparing it with simulations.

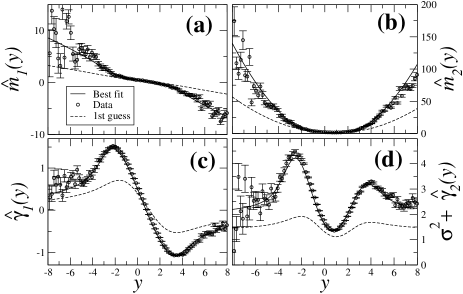

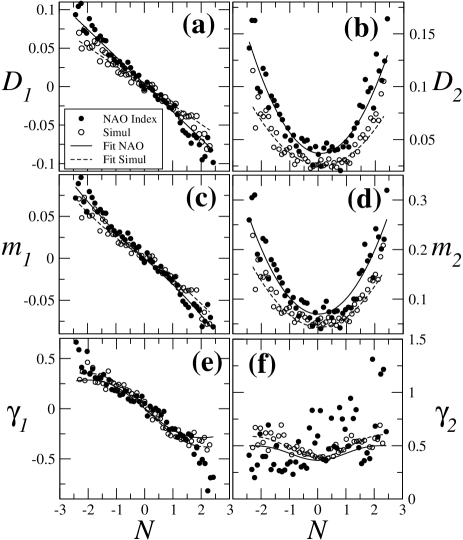

Figure 9: (a)-(b) Estimate of the drift and diffusion coefficients

and of the daily North Atlantic Index

ijbc ( datapoints), together with the corresponding

(c) ,

(d) ,

(e) and

(f) .

Results for the empirical NAO index are represented with bullets

whereas the synthetic data also with datapoints and parameter

values given by Tab. 1 is shown with circles for comparison.

The corresponding fits are given with solid and dashed lines,

respectively.

The North Atlantic Oscillation (NAO) is a source of variability

in the global atmosphere, describing a large-scale vacillation in

atmospheric mass between the anticyclone near the Azores and the

cyclone near Iceland hurrel95 .

The state of the NAO is usually measured by an index , defined

as the normalized pressure difference between the high and the low poles,

where the pressures are averaged over each, day, month or

year lind05 ; hurrel95 .

The NAO index and climate indices in general are receiving much attention

due to their important role in climate change.

Lately, evidences for the stochasticity of this index have been

showncollette04 ; lind05 . In this section we address the problem

of estimating its measurement noise amplitude.

Figures 9a and 9b show the drift and diffusion coefficients

respectively for the NAO daily index (bullets) and the corresponding

fit (solid line). The parameters for both and are

given in Tab. 1 together with the amplitude of the measurement

noise.

Probably due to the small amount of data points ( values) one

observes large scattering of the data, particularly away from the average

value .

To evaluate the reliability of considering the NAO index a Markov

process described by Eq. (1) we also plot in Figs. 9

the results obtained when integrating such equation (circles) using the

coefficient values in Tab. 1 including the amplitude of the

measurement noise. The same sample size was considered.

The corresponding fit is represented with a dashed line.

While the drift coefficient resembles the one observed for the NAO

index, there is a significant shift of the diffusion coefficient, that

only for a very narrow range around the average value is well reproduced.

Indeed, as one sees from Tab. 1, the coefficient values for in

our simulation significantly deviate from the ones found for the

NAO series.

Further, functions and , plotted in Figs. 9c-f,

show also large scattering, particularly for . This feature

raises difficulties in a proper minimum search for .

Param.

Simulations (16801 pts, 10 sim)

NAO Index

(16801 pts)

With noise

No noise

Only noise

()

()

()

()

()

()

Table 1: Optimized parameter values for the daily North Atlantic

Oscillation daily indexijbc compared with the average values

for sets of synthetic data (“With noise”) using the same number

of points and parameter values.

In order to evaluate the reliability of our synthetic data we also

run the optimization procedure for sets of synthetic data with

the same and found in NAO series and

(“No noise”). In the last column we plot the results returned from

the optimization procedure for synthetic data of pure measurement

noise with amplitude , the one obtained for NAO series.

In order to check the reliability of the calculations

we reproduce the synthetic data times and present in Tab. 1

(column “With noise”)

the average values for each parameter, where the error is taken as the largest

deviation from the average over the sample of data sets.

The measurement noise, which dominates all parameters, is well

reproduced. For the drift and diffusion coefficient the order of

magnitude of each parameter is also correct, but for and

and one observes significant deviations from the

estimated values obtained for the NAO series.

This mismatch between the empirical and synthetic series could raise

the question if the NAO Index is indeed suitably described by a

Markovian stochastic process with a perceivable deterministic part.

In fact, since one observes the

series is approximately a pure white noise (i.e.

in Eq. (3)),

which in fact also yields a linear drift and quadratic

diffusion coefficients.

To address this problem we rerun our optimization procedure for synthetic

data, for two additional situations, one where and drift and

diffusion coefficients are given by the NAO index, and another one which

simulates a pure white noise () with equal to the value

found for the NAO series. The results are also given in Tab. 1,

columns “No Noise” and “Only noise” respectively.

For the pure white noise process one obtains as the only non-zero

parameter, apart fluctuations, but with an amplitude different from the

one used to generate the synthetic data, namely , which

corresponds to of the inserted

measurement noise ().

For the synthetic process with no noise, the order of magnitude for the

parameters of and is correctly computed, whereas a non-zero

measurement noise is retrieved

covering the remaining of the inserted measurement noise.

In other words, one can argue that in this situation our procedure

retrieves of the total amount of measurement noise.

In this scope, our results point in the direction of previous arguments

given by some authorsstephenson00 :

differently from other climate indices such as

the ENSO index, the NAO index seems to be an almost

pure white noise process with only a minor contribution from a

stochastic process governed by a Langevin-like equation.

Alternative indices should be therefore considered and studied as

recently suggestedlind05 .

V Discussion and Conclusions

We described in detail a nonparametric procedure to extract measurement

noise in empirical stochastic series with strong measurement noise.

The algorithm is able to accurately extract the strength of measurement

noise and the values of the parameters defining the drift coefficient and

to estimate with good accuracy the diffusion coefficient that

fully describe the evolution equation for the measured quantity

in the time series.

This has been shown by synthetically generated

data sets contaminated by increasing measurement noise.

Additionally, the algorithm was applied to

a set of measured data

providing new insight in the underlying systems.

The data for the climate index shows a large scattering, probably

due to the small amount of data points. Larger data sets for climate

indices are not available up to our knowledge.

It should be noticed that the nonparametric reconstruction of the

Langevin Eq. (1) from measured stationary data sets

generally requires that the process exhibits Markovian properties and

fulfils the Pawula theoremlind05 .

While the second constraint can be relaxed extending the analysis to a

broader class of Langevin-like systems in which the Gaussian

-correlated white noise

Langevin force is replaced by a more general Lévy

noisefriedrich08 ; siegert01 , in general the Markov condition remains

a crucial constraint.

Recently, it has been shown that processes corrupted from measurement

noise may loose their Markov propertieskleinhans07 .

For this reason the proper

analysis of data suffering from strong measurement noise in general is a

complicated task. We, however, would like to point out, that the method

presented here solely relies on Markov properties of the underlying,

undisturbed process . In case of -correlated measurement

noise the method presents a general approach to access the process

and the noise amplitude at the same time.

Therefore, since the algorithm is general for a broad class of

stochastic systems other applications can be proposed.

Particularly in cases where the measurement procedure is subject

to large measurement noise due to the distance between the location

where the measure is taken and the location where the phenomena

occurs. Two important applications in this context are seismographic

datafriedrich08 , where the epicenter can not be predicted before-hand,

and data from surface EEGprusseit08 ; lehnertz09 , which, though having

stronger measurement noise, are much recommended instead of insitu

measurements for the sake and comfort of the patient.

A further application would be the analysis of sensors to which one has

no access, for example sensors being installed in remote systems

showing more and more measurement noise due to aging effects.

Here it

should even be possible to know quite precisely the functional structure of

the underlying process, an assumption of our analysis here.

Such applications however appeal for the extension of the present

procedures to higher dimensions, i.e. more than one time-series, which

implies the consideration of different measurement noise sources and

consequently noise mixing. To ascertain in which conditions and up to

which point can we separate different measurement noise sources is

an open question which we will address elsewhere.

In all simulations a linear function was assumed for the drift coefficient

and a quadratic one for diffusion.

Although such assumptions comprehend already a broad class of

systemsfriedrich08 ; lind05 ; boettcher06

our approach and all expressions may easily be extended to higher

order polynomials for and , as long as the number of

parameters for modelling and is not too high.

In this case the calculations presented in the appendices are valid

if one considers proper higher powers in the integrand of integrals

and (see Eqs. (117) in Append. C).

Furthermore, other possibilities for optimization are possible.

For instance, though in this case we have shown that random Monte Carlo

procedures are computationally expensive consuming, one could think

of a non-local search procedure using for example bigger jumps such as

the ones of a Lévy flight processpavlyukevich07 .

Alternatively one may also study how good would be an optimization

procedure that considers the minimization of a splitted cost function

.

Preliminary results have shown that for a proper decomposition of

our optimization problem may be reduced to a cubic equation

and a lower dimensional system of linear equations.

Another possibility would be to use genetic algorithmsgenetic .

These points will be addressed elsewhere.

Acknowledgements

The authors thank Wilhelm and Else Heraeus Foundation for supporting the

meeting hold in Bad Honnef, where very usefull discussions happened and

also the project DREBM/DAAD/03/2009 for the bilateral cooperation between

Portugal and Germany. PGL thanks Reza M. Baram and Bibhu Biswal for

usefull discussions.

Appendix A The conditional moments of an arbitrary time series

and their linear approximations

Taking a series of measurements as defined in Eq. (3),

its -th order conditional moment reads

(36)

(38)

where is the probability to measure in

the presence of a measurement noise with variance , when the

system (without noise) has the value ,

is the probability for the system to evolve from

a value to a value within a time interval

and

has the inverse meaning of :

it is the probability for the system to adopt the value when a

measured value is observed.

While is unknown, and are related

with each other according to Bayes’ theorem (see App. B).

From such assumptions one easily arrives to the identities

(39a)

(39b)

(39c)

and using these identities the general expression (38)

can be approximated up to first order assuming .

More precisely, the first two moments and yield

(40)

(42)

(44)

(48)

(50)

(52)

(56)

(58)

(60)

(62)

(64)

(66)

(68)

(70)

(76)

(77)

(79)

(81)

(87)

(90)

(94)

(96)

From Eq. (96) one has

where .

Such observations justify the first estimate for the measurement noise

stated in Eq. (9), since

when is small enough, probability density function

is similar to

(see Eq. (39a)) and therefore, one

can take as a first approximation .

Notice that the last equalities in and yield

first order approximations under the assumption that .

In Ref. kleinhans05 another approach is proposed

for the estimation of drift and diffusion coefficients

in the case of low sampling rates.

The errors for , ,

and are just given from the

linear fit of and for each fixed ,

given in Eqs. (8c) and (8g).

The errors of and can be

also directly computed from the data as

(97a)

(97c)

(97e)

(97g)

(97i)

(97k)

(97m)

(97o)

where is the number of data points in bin .

For the optimization procedure it is convenient to simplify the

expressions for functions and (). Namely,

and can be written as expressions of and .

In fact, substituting Eqs. (7a) and (7c) into Eqs. (10e)

and (LABEL:m2), and adding and subtracting properly , yields

(98a)

(98c)

(98e)

(98g)

(98i)

(98k)

(98m)

(98q)

(98s)

Substituting Eqs. (98i) and (98s) into Eq. (17)

yields as a functional depending only on the integrals

and defined in Eqs. (10a) and (10c),

apart the six parameters, and , we want to optimize.

Appendix B The probability density function

To solve the minimization problem we will need to explicitly write

expressions for . This conditional probability density function appears in Eqs. (10a)

and (10c) and according to the Bayes theorem is given by:

(99)

where is the probability density function of the

measurement noise , i.e. a Gaussian function

centered at with variance ,

(100)

and can be written, assuming that the process is stationary, as

(101)

where is some normalized function such that

and

(102)

For an Ornstein-Uhlenbeck process and

one finds

(103)

from which one easily sees that is a necessary condition to

have a well-defined probability density function .

For the general case given by Eqs. (7) one has typically

with , which yields .

In these situations, can also be integrated, yielding

(104)

with

(105)

Appendix C The derivatives of , , and

The minimization problem needs also the expression of the derivatives

for the ’s and ’s.

To compute them one needs first to write the derivatives of

function defined in Eq. (99).

Defining one has in general

(106)

where is some variable on which depends.

Since depends only on parameters and

depends only on , we have

(107a)

(107b)

where for we have

(108)

and for we have

(109)

with

(110)

and therefore

(111)

with one of the parameters.

In the Ornstein-Uhlenbeck case

(112a)

(112b)

(112c)

and in the general case

(113a)

(113b)

(113c)

(113d)

(113e)

where

(114a)

(114b)

(114c)

So, neglecting the parameter as explained in Sec. III,

for the other parameters we have

(115a)

(115c)

and therefore considering Eqs. (10a) and (10c)

that define functions and and also

Eqs. (98i) and (98s) defining functions

and it follows

(116a)

(116c)

(116e)

(116g)

(116i)

(116k)

(116m)

(116o)

(116q)

(116s)

(116u)

(116w)

where

(117a)

(117c)

References

(1) H. Kantz and T. Schreiber,

Nonlinear Time Series Analysis,

(Cambridge University Press, Cambridge, England, 1997).

(2) R. Friedrich, J. Peinke and M.R.R. Tabar,

Complexity in the view of stochastic processes

in

Springer Encyclopedia of Complexity and Systems

Science (Springer, Berlin, 2008).