Resilience of Volatility

Abstract

The problem of non-stationarity in financial markets is discussed and related to the dynamic nature of price volatility. A new measure is proposed for estimation of the current asset volatility. A simple and illustrative explanation is suggested of the emergence of significant serial autocorrelations in volatility and squared returns. It is shown that when non-stationarity is eliminated, the autocorrelations substantially reduce and become statistically insignificant. The causes of non-Gaussian nature of the probability of returns distribution are considered. For both stock and currency markets data samples, it is shown that removing the non-stationary component substantially reduces the kurtosis of distribution, bringing it closer to the Gaussian one. A statistical criterion is proposed for controlling the degree of smoothing of the empirical values of volatility. The hypothesis of smooth, non-stochastic nature of volatility is put forward, and possible causes of volatility shifts are discussed.

1 Introduction

Non-stationarity is arguably the most characteristic feature of financial markets. It is generally accepted that statistical parameters of price dynamics vary with time. This fact is unpleasant both for researchers and practitioners, because any discovered regularities and elaborated trading systems quickly lose their relevance as time passes. The best solution to the problem of non-stationarity would be to include it into a probabilistic model of market operation.

One of the most important characteristics of returns of a financial instrument is its volatility. There is no doubt that volatility varies over time, and this phenomenon is the subject of voluminous literature, for example Schwert:1989 , as well as a more recent collection in Shephard:2005 . There are ’quiet’ periods of market behavior and periods of increased volatility. One can say that volatility characterizes the market ’temperature’, the degree of its emotional tension. Forecasting future values of volatility is extremely important; it plays a crucial role, among other issues, in determining the pricing of options and assessing the risk for portfolio investors (see Poon:2003 for an extensive review). Understanding the causes and nature of non-stationary volatility would also lead to a deeper insight into the essence of the financial market processes. Various models were suggested, encompassing such diverse fields as theory of chaos applied by Hsieh:1991 , and multi-agent systems studied by Watanabe:2008 . This task became especially relevant in recent years, during the unfolding financial disturbances, as well as dramatic events of Internet bubble (relevant discussion can be found in Battalio:2006 ).

The term volatility comprises at least four different meanings: 1) the emotional characteristic of the market; 2) sample mean square deviation of logarithmic returns; 3) the ’true’ unobservable variance of the underlying distribution of returns; and 4) the implied volatility in option contracts. In this paper, we use the term volatility in the second and third senses, which are usually referred to as realized and latent volatility, respectively. We refer the reader to reviews by McAleer:2008 and by Shephard:2008 for good overview of the field. The choice of robust volatility estimator is important for producing correct inferences from the available data (see Broto:2004 ). One of the questions we focus on in our research is, which choice of estimator of sample volatility leads to a minimum error for a certain model of a random process. ’True’ volatility is, of course, non-observable, and the question of its nature is further complicated by the non-stationary nature of the markets.

The generally accepted approach is to consider the volatility as a stochastic variable (see, for example, Andersen:1998 , Shephard:2005 and the collection in Forecasting:2007 ). One of the chief motivations for this is the presence of high autocorrelations in volatility and squared returns, as discussed in Engle:2001 . Compared to the near-zero autocorrelations in logarithmic returns, the detection of such long-memory pattern creates striking impression.

In the probabilistic models with variable volatility, the price random process is described either by discrete or continuous equations, parameters of which are random variables. In this context, GARCH() model first introduced by Engle:1982 gained wide popularity, as well as its various generalizations (see Engle:2002 ). In this case, the timeline is divided into finite time intervals (lags) of duration , and then only ’closing’ prices of these intervals are considered , where is an integer. Logarithmic returns are independent random variables, with variable volatility , the square of which linearly depends on the previous squared returns and volatilities:

| (1) |

Here and below is uncorrelated normalized random (i.i.d.) process with zero mean and unit variance: , , . A line over a symbol, as usual, denotes the average of all the possible realizations of .

In the continuous framework, the stochastic Ito’s equation is widely used for both price and volatility dynamics. The price is modeled (for an example, see a paper by Alizadeh:2002 ) by the ordinary logarithmic walk, and volatility is described by the Ornstein–Uhlenbeck equation:

| (2) |

where , are uncorrelated Wiener variables . Indeed, the term ’stochastic’ volatility is usually reserved for this class of models, although we here use in a somewhat broader sense, to include the GARCH-type models.

Sometimes, both in the discrete and the continuous models, one or more ’hidden’ stochastic variables are introduced, and volatility is considered as a function of such variables. Other, sometimes rather sophisticated approaches, exist in the literature (see Eraker:2004 as an example). What unites them all is the probabilistic description of the local dynamics of volatility (either discrete or continuous).

There is an extensive body of empirical research devoted to testing of predictive power of GARCH-type stochastic models over the last twenty years, surveyed in Canina:1993 , Forecasting:2007 , as well as the discussion of correct methodology for forecast estimation Andersen:1998 . In general, certain skepticism regarding the predictive capabilities of such models is present in ongoing research. Recently, certain considerations were expressed that explain the persistence of autocorrelations of positively determined variables as the result of their non-stationarity; Mikosch:2004 , Granger:1999 and Diebold:2001 are just a few examples of related research.

The effect of non-stationarity is also directly related to the problem of searching for the probability distribution of returns of financial instrument. It is well known that this distribution is non-Gaussian; it has heavy tails and, consequently, manifests high kurtosis and high probability of excessively large or small returns. Starting with the seminal work by Mandelbrot:1963 , this fact has gradually become a standard in financial engineering (see Jondeau:2007 for a modern view upon the subject). However, most approaches to constructing the probability distribution of random variables implicitly suppose their stationarity, which we do not observe at real financial markets.

The idea that non-stationarity in the random process can cause the non-Gaussian behavior of returns distribution goes back as far as the classical work by Fama:1965 ; it was therein tested and was not confirmed. Nevertheless, the question about the type of distribution and the effect of non-stationarity requires further careful consideration.

In this paper we provide the arguments in support of the hypothesis that volatility is a smooth, rather than stochastic, function of time. The explanation of origin of high long-term autocorrelations and the non-Gaussian nature of returns distribution will be given. Our hypothesis also implies that the volatility manifests the property of resilience: under the impact of irregular, relatively rare and completely unpredictable shocks to the market, it gradually deforms; after such influences cease to act, the relaxation process takes over and volatility gradually decreases.

The remainder of the paper is organized as follows. First, we discuss a new measure of volatility and demonstrate its effectiveness. After that, the empirical stylized facts of autocorrelations associated with the volatility are listed, and a simple non-stationary model, in which such properties naturally arise, is proposed. A very clear graphic representation is provided for the mechanism of appearance of autocorrelations, and a simple mathematical formalism for performing the necessary calculations is proposed.

The evidence that such a mechanism is actually realized in financial markets is provided by calculation of the autocorrelation function (ACF) for two modifications of original series; namely, the autocorrelations are vanishing for both the first differences of volatility of consecutive days, and for the residual series obtained by elimination of its smooth part . The empirical tests of these facts are carried out utilizing sample data of both stock market and exchange rate dynamics.

Next, we show that normalizing the returns series by leads to significant reduction in kurtosis of distribution, in some cases restoring it to the normal form. Statistical criteria for controlling the degree of data smoothing are elaborated. We consider the arguments concerning the local constancy of ’true’ volatility. In Conclusion, a number of inferences about the possible properties of the dynamics of volatility are formulated. Various technical details are compiled in self-contained Appendices, which complement and detail the calculations presented in the body of the paper.

2 Measurement of volatility

Historical prices for various financial instruments are usually available as discrete time series, with a certain period of time (lag) between consecutive points. Most widely available are data with daily lags, hourly lags can be observed less frequently, and minute lags are even more seldom. In addition to the closing price (the latest value within a lag), other commonly utilized parameters are: opening quotes (first price of a lag), maximal and minimal price values. By means of these four price points one can construct three independent relative values, which we will call the basis of a lag.

| (3) | |||||

The height of price ascent and the depth of price descent are both positive values. Out of these measures the amplitude of price range can be defined (see, for example Parkinson:1980 and Garman:1980 for early examples of its use). The asset return can be both positive and negative.

If one considers the models of additive Wiener random walk , the values are asset prices. For the logarithmic random walk they are logarithms of price values . Thus, in the latter case, for example, the range would be equal to the logarithm of the ratio of maximum price to minimum price , the corresponding equal to the logarithmic return , and so on.

We define volatility of a lag with duration as an average of asset return deviation from the mean over a sufficiently large number of lags: . If volatility is constant, the values of positive entities in certain sense serve as its measure. The higher is the market volatility, the more probable are their high values. In particular, in absence of drift (), their men values are proportional to volatility: (see Appendix A).

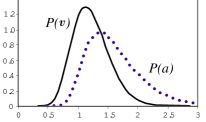

However, the informational content of each parameter, and of their possible combinations, varies. The distributions of the probability density for and , , , in the case of Wiener process, are plotted in Fig. 2 (dotted lines mark the distributions’ mean for ).

As we see, among the basis components only the range has a sufficiently narrow maximum around the mean value. The density of probability of the other three values are strictly decreasing functions, which allows for , and to take, with high probability, values close to zero. The range , on the contrary, avoids going to zero, the probability that being as low as 0.002. Indeed, it often happens that the market closes with a near-zero change in price , while its volatility during the day was significant. In general, the narrower the distribution of probability for volatility measure, the better is this measure. For some positively determined value , the relative degree of distribution narrowness can be characterized by a ratio , where is mean squared deviation from the mean . For the range we have , which signifies more than twice as narrow distribution peak than, for instance, for the height (). A natural question arises: is there a combination of the basis values that has a narrower distribution than the price range ? This topic is the subject of extensive research (see e.g. Parkinson:1980 ,Garman:1980 , Rogers:1991 ,Rogers:2008 , Yang:2000 ).

In the present article we define a simple, but efficient, modification of the price range, which is motivated as follows. If the price dynamics within the lag is accompanied by a significant trend (whether it is going up or down), the volatility may appear lower than for the same price range, but in the absence of trend (). Therefore there are good reasons to decrease the value of the range, as a measure of volatility, in the case when is large. We achieve this by introducing the following volatility estimator, which we call modified price range (see Appendix B):

| (4) |

Its statistical parameters – mean (), standard deviation (), skewness () and its kurtosis () for are listed in Table 1.

| 0.798 | 0.603 | 1.00 | 0.87 | 0.76 | |

| 1.596 | 0.476 | 0.97 | 1.24 | 0.30 | |

| 1.197 | 0.300 | 0.53 | 0.26 | 0.25 |

One can see that the relative width of the distribution of modified range , which is better than that of simple range . The statistical parameters also show that the distribution for is more symmetrical around the maximum and has a lower kurtosis than . The form of distribution for together with (dotted line) are plotted in Fig. 3, and there we also provide the expressions for the average and its square for the case of the Brownian walk.

Thus, the modified price range provides a better measure of volatility than the simple range, and significantly better than absolute logarithmic returns. In Appendix B, we compare the modified range with several other ways of volatility measurement utilized by other authors. Providing for the same or lower error of volatility estimation, the measure has a significantly more simple definition, and is unbiased for the small number of lags, so we will use it extensively throughout this paper.

3 Intraday volatility

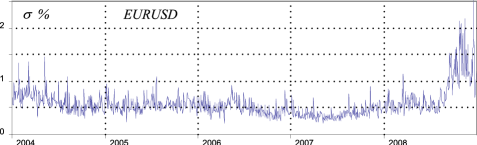

We shall demonstrate the effectiveness of modified amplitude of range on the available realized volatility data. Here we consider 15-minute quotes at the Forex market for the period from 2004 to 2008 for EURUSD currency pair. We shall make them aggregated into daily points, calculating, beside minimum and maximum meanings, intraday volatility basing on logarithmic returns of 15-minute lags:

| (5) |

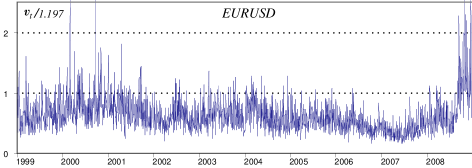

During a day, we have 15-minute lags. Multiplier in (5) turns 15-minute volatility into the daily value. The evolution of intraday volatility is given in the Fig. 4 (data for 1250 trading days, excluding weekends and major holidays):

One can observe that since the fall of 2008, volatility of the currency market, as well as of other financial markets, has increased dramatically, due to the worsening financial crisis. However, even in the pre-crisis period, volatility has a clear-cut non-stationary component.

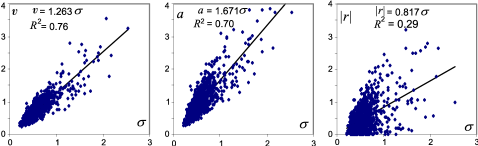

It is natural to assume that realized volatility obtained from a sample of characterizes the ’true’ volatility better than does a daily basis of three values (see Barndorff:2002 , Biais:2005 , Andersen:2003 ) even though there are various high-frequency effects that one has to take into account (discussed in detail by Madhavan:2000 , Bandi:2006 , and Bollerslev:1993 ). To find a more robust measure of volatility, based on the basis, one should look for a value stronger correlated with the intraday volatility. Let us chart the scatter plots of dependence of daily values of , and on intraday volatility (EUR/USD for period 2004-2008, Fig. 5).

It can be easily seen that and are substantially more correlated with , than with . The transition from logarithmic range to modified range makes the correlation more pronounced, but the difference is not significant.

Similar results are observed for other currencies. The slope of regression lines and for six currency pairs are given in Table 2. In each case the error of linear approximation for is lower than for , and significantly lower than for .

| eurusd | gbpusd | usdchf | usdjpy | usdcad | audusd | average | |

|---|---|---|---|---|---|---|---|

| 1.263 | 1.260 | 1.289 | 1.251 | 1.241 | 1.243 | 1.258 | |

| 1.671 | 1.665 | 1.692 | 1.640 | 1.621 | 1.660 | 1.658 | |

| 0.817 | 0.809 | 0.807 | 0.776 | 0.761 | 0.834 | 0.801 |

Despite the noticeable variation, the values of , and are close to their theoretical values for Wiener random walk, 1.197, 1.596 and 0.798, respectively. Nevertheless, we must keep in mind that, for example, the expression holds only for the Brownian random walk with normal distribution of returns. In reality, this condition is not fully satisfied, so the ratio may be equal to some constant different from , and its exact value we will discuss below.

Another indication of significance of modified price range are autocorrelation coefficients that will now be the object of our interest:

| (6) |

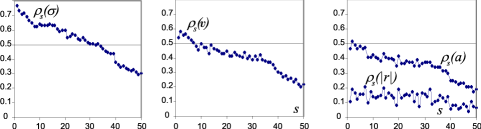

where the averaging is carried out for all the observed values of . For interdaily rates of EUR/USD (2004-2008) we obtain (as shown in Fig. 6) the autocorrelation charts as a function of shift (in days) parameter . As can be observed from Figure 6, autocorrelations of intraday volatility are the highest, followed by modified price ranges , then by simple range , and the weakest correlations are those of absolute logarithmic returns .

High autocorrelations appear for a variety of financial instruments and are quite an intriguing fact (Cont:2001 provides the list of other so-called stylized facts, as well as an excellent compilation of references to relevant research). In contrast, the first autocorrelation coefficient of EUR/USD rate returns is equal to , which corresponds to the absence of correlation, if one takes into account that rule gives an error band of 0.06 (for 1250 trading days). This unpredictability of the market returns is one of manifestations of its market effectiveness.

However, the situation is quite different for absolute returns, and even more so for volatilities, which have slowly decaying long-range ACF function. Basing on this fact a huge number of stochastic models have been constructed, which claim the ability to predict the future values of volatility (see Shephard:2008 for a recent review). The majority of these models have empirical nature, and do not explain the causes of high autocorrelations. One of our tasks in the present paper will be to propose such an explanation

4 Empirical features of autocorrelations

We now extend our analysis by outlining a number of features of autocorrelation coefficients pertinent for volatility.

1. Autocorrelations decay monotonically and very slowly.

This is a well-known result (see Ding:1993 , Breidt:1998 ). A number of papers were devoted to attempts on determining the functional dependence of autocorrelation coefficients from the shift parameter . Usually, autocorrelations are approximated by a power law , where the parameter turns out to be small.

2. The longer is the time interval, the higher are autocorrelations.

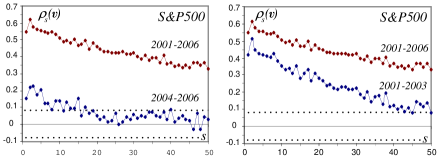

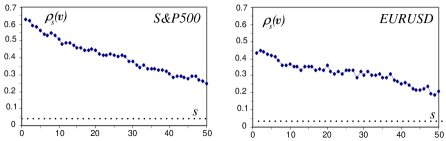

Let us consider the behavior of ACF for daily modified range for S&P500 stock index for the period from 2001 to 2006. We split this interval into two three-year periods, namely, from 2001 to 2003 and from 2004 to 2006. During the first one there were trading days, while during the second - . We calculate autocorrelation coefficients separately for each period, as well as the autocorrelation of combined data series.

The resulting autocorrelograms are represented in Fig. 7 (the combined ACF is repeated on both plots). As can be noticed, the summarized correlogram goes above the correlograms of each period. However, this behavior is not observed for any asset in any circumstances, and the conditions that are required for this to occur will be clarified during further discussion below.

Here and below the dotted horizontal lines in the correlograms mark the double standard error band , where is the number of points involved into the calculation. Table 3 shows the main statistical parameters of daily logarithmic returns of S&P500 index for different periods.

| Period | ||||||||

|---|---|---|---|---|---|---|---|---|

| 2004-2006 | 755 | 0.032 | 0.659 | -0.02 | 0.25 | 55.9 | 69.4 | 0.16 |

| 2001-2003 | 752 | -0.023 | 1.376 | 0.20 | 1.27 | 48.9 | 71.4 | 0.42 |

| 2001-2006 | 1507 | 0.005 | 1.078 | 0.15 | 2.84 | 52.4 | 75.7 | 0.55 |

In addition to the mean (), daily volatility , skewness() and kurtosis(), we also present here the percentage of positive returns and a share of returns falling within one sigma of the mean: .

Table 3 illustrates the fact that when the market is calm (2004-2006: ), the distribution of asset returns is close to normal (). However, the normality deteriorates significantly after we extend the time interval under consideration. Simultaneously the autocorrelation of volatilities starts to increase .

| Period | |||||

|---|---|---|---|---|---|

| 2004Q1 .. 2008Q4 | 1302 | 0.80 | 0.54 | 0.47 | 0.11 |

| 2004Q1 .. 2008Q3 | 1215 | 0.51 | 0.25 | 0.16 | 0.01 |

A similar situation can be observed in the foreign exchange market. Discarding the data from recessionary fourth quarter of 2008 reduces significantly the autocorrelation coefficients of data series related to the volatility of EUR/USD pair, as illustrated in Table 4. We note that dropping the 2008Q4 data reduces the number of days for which the autocorrelation coefficients are calculated by merely 7%.

3. Scatter plot of volatility has a ’comet-like’ shape.

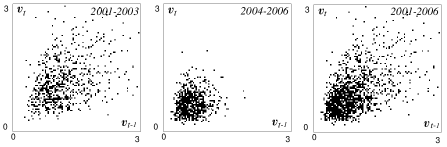

Let us consider the scatter plots for modified range parameter , illustrating the ’existence of memory’ of volatility for the three periods of index, discussed above.

As can be seen from Fig. 8, data points fill the region of a distinctive ’comet-like’ shape, its tail fanning out into the positive values of both axes. Naturally, the higher the autocorrelation coefficients are, the more distinctive is the form of the dot cloud.

The shape of region is completely independent of the shift and the utilized volatility measure. For EUR/USD currency pair over 2004-2008 period, we have the scatter plots of intraday volatilities, obtained from 15-minute lags, are presented in Fig. 9. There, three values of the shift are presented: one day (), one week (), and two weeks (). It can be seen that the form of ’comet-like’ shape doesn’t change qualitatively, but rather spreads out gradually along with the decrease of autocorrelation coefficient.

5 When autocorrelations do not decay

Actually, slowly decreasing autocorrelation coefficients as a function of the shift parameter, ought to be a cause for alert. There are very simple models that exhibit similar long-correlations effects without employing the notion of stochastic volatility (see Granger:1999 for one ingenuous example).

Let us consider, for example, an ordinary logarithmic walk:

| (7) |

and simulate 20 years (5000=20250 trading days) of price evolution; volatility is defined as constant equal to for the first 10 years, and changes to another constant value of in the second half of the period. Wiener’s process is represented as , where is normally distributed random variable with zero mean and unit variance. We choose one second as a small time interval .

The dynamics of daily values of the modified price range during ’critical’ 10th and 11th years has the shape plotted in Fig. 10 (where time is in ’days’).

Such data series with a one-time shock non-stationarity exhibits noticeable autocorrelation coefficients for the absolute returns (plotted in the second panel of Fig. 11), and even higher autocorrelations for the price range (third panel).

The decay of ACF is very slow with the increase of shift parameter . In contrast to and , the correlations of price returns (the first plot above) lie within two standard errors, and thus are practically absent.

Therefore, correlation regularities arise in the considered toy model, despite the statistical independence of the two consecutive days. We stress that not only the returns are independent, but so are the absolute returns , and amplitudes of price . If volatility were constant for the whole modeled period, all the correlograms and would be equal to zero. It is when we introduce non-stationarity that the picture is qualitatively changed.

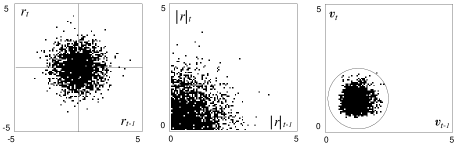

The cause of this effect can be easily understood. Fig. 11 contains three scatter plots that represent values of logarithmic returns, their absolute values and modified price ranges of two consecutive days during the first decade of evolution with constant volatility .

In the first plot, the dots form an almost symmetrical cloud, and the correlation is evidently equal to zero. In the second and third plots, there is symmetry is reduced, in agreement with the corresponding symmetry features of the probability densities and . However, due to the independence of consecutive days, the correlation coefficient is equal to zero. For example, if , and , the independence means that the joint density of distribution is equal to the product of probability densities . Therefore, for any distribution the covariance will be equal to zero: .

It is important to emphasize the fact that for the returns the center of the data cloud is located at the origin of coordinates, whereas for the positively determined values and it is displaced to the right and up to the region of positive values.

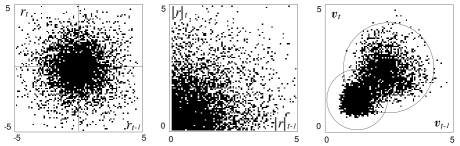

Now let us add the dots corresponding to the data of the second decade to the diagram (see Fig. 13).

For logarithmic returns (first diagram) two clouds with the same center overlay. The resulting cloud remains symmetrical, that is why the autocorrelation is still equal to zero. In the case of the price range (third diagram), there are two non-concentric clouds, one of which corresponds to and second one to (we remind that ). The overlapping area between the clouds dithers, and a figure of a characteristic comet-like shape appears as a result (the upper cloud is larger). Using the least-squares criterion, one can draw a line through it, the slope which will be proportional to the correlation coefficient.

The shape of diagrams do not change if we plot the data for the case of two days’ shift . Indeed, with the exception of few transitional points around the volatility jump, all the data for each decade will still be clustered in its cloud.

The situation with the second diagram for the absolute returns is somewhat more complicated. Visually, it is not qualitatively different from the corresponding one for the first decade; nevertheless, the non-zero correlation is present. In order to understand this phenomenon, it is necessary to extend the standard statistical relations to the case of non-stationary data.

6 Non-stationary statistics

Let the distribution parameters of a random variable vary smoothly with time. If we calculate the mean of over a given time interval without taking the above mentioned statement into account, we will actually obtain the following expression for :

| (8) |

In other words, in every fixed moment of time we calculate a local mean , and then average all such local mean values over the time interval (denoted by angle brackets). Similarly, let us define local variance as:

| (9) |

The variance calculated on all dataset will be equal to:

| (10) |

where the angle brackets, as above, denote averaging over time interval . Thus, is made up of two distinct parts, namely, it is a sum of weighted local variance and time variance of mean (second and third terms in equation (10)).

In the special case of parametric non-stationarity, can be represented as , where represents stationary independent random process with zero mean and unit variance (, ). The mean value of is equal to , and variance is given by: .

Let us now consider two locally independent variables and . Their independence means that the density of joint probability in any fixed moment of time decomposes into product , and

| (11) |

However, when averaged over all data, these variables cease being independent. Indeed, the time mean of the product :

| (12) |

and this expression is not equal to the product of time means: . In general, if local means , are non-zero, the correlation coefficient is non-zero as well. As we observed from the example of the previous section, the mean of returns in each decade was equal to zero, that is why the autocorrelation did not arise for . In contrast, for the positively determined variables and the mean is non-zero, and autocorrelation is present, despite the independence of two consecutive days.

Thus, locally independent variables that have similar long-term non-stationarity, become dependent when we take into account their evolution in time. However, such dependence does not have stochastic nature, but rather ’deterministic’, smooth one, related to time synchronization.

For example, if the non-stationarity of volatility has a shape of a step-function with equal duration of both periods, the mean and variance of the whole dataset are equal to:

| (13) |

where replaced either or , and statistical parameters of the first and second decades are given by , , and , . If the shift in the calculation of the autocorrelation coefficient is small compared to the length of , in the first approximation one can neglect the boundary effects, and assume that and are independent. Their covariance is equal to:

| (14) |

As , we receive for the autocorrelation coefficient:

| (15) |

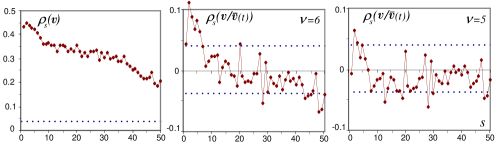

We can see that such ’correlation’ for non-stationary data appears only for variables with different means. For and , mean and variance are proportional to volatility of logarithmic returns , . For absolute returns, , , while for the modified price range , . If volatility of the market changes, so do the mean values of positively determined variables and . For our model, the volatility of logarithmic return is increased by factor of 2, and the corresponding correlation is given by . For absolute returns this is equal to 0.15, and for the modified range, 0.61. This agrees exactly with what we have observed in the numerical experiment.

In general case, in order to obtain the autocorrelation coefficients as function of shift , we should use their definition as sums. However, the presentation in continuous time is more compact. Let us assume and shift to be continuous variables. In case of lags with duration of each we have , and , where . Let us consider a positively determined variable , related to volatility, which is modulated by a non-stationary component , where is a stationary random variable with a unit mean. For example, for the modified amplitude, . Since random variables at different times are non-correlated and positively determined, we obtain that is equal to 1 for , and to for . Let us define the covariance for the case as follows:

| (16) |

We note that this is not the only possibility in the case of a finite sample with duration . In any case, we require that the covariance(16) is equal to zero if . The variance of a positive variable equals to . Accordingly, the autocorrelation coefficient allows to find the shift parameter dependence for different forms of non-stationarity.

We thus see that autocorrelations of various measures of volatility can arise due to smooth non-stationarity in data, rather than because of the stochastic nature of volatility. At this point, a natural question comes up: does such a mechanism represent the reason why noticeable autocorrelations of volatility are observed in various financial markets?

7 Autocorrelation of differences

The easiest way to eliminate the relatively smooth non-stationarities in a time series is to switch to the differences of the data series. If undergoes a locally constant drift, autocorrelations for this process are present. If one considers the differences of two consecutive data points, the drift is effectively cancelled. Even if the trend in slowly changes its direction, within the ascending and descending parts the values of differences change only slightly and become locally quasi-stationary.

Let us shall consider the change in the modified price range:

| (17) |

Our data sample is represented by daily statistics on S&P500 stock index for the period of 1990-2008 (4791 trading days), and daily data on EURUSD exchange rate (1999-2008, 2495 days, excluding holidays). Let us start with obtaining the autocorrelation coefficients of the amplitudes of daily price range , with result plotted in Fig. 14. As usual, the coefficients are considerably high; the autocorrelations for S&P500 index are more significant than those for EUR/USD exchange rate, and manifest weaker fluctuations.

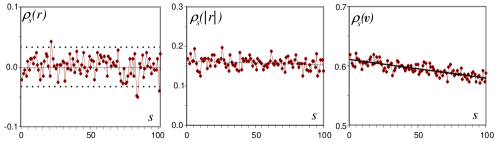

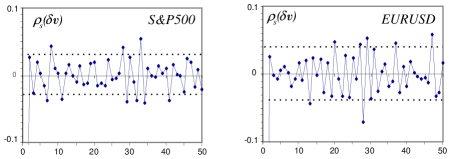

Let us now consider the differences the price range of two consecutive days; we find that for differentiated series, the autocorrelation drops sharply, as can be seen from Fig. 15.

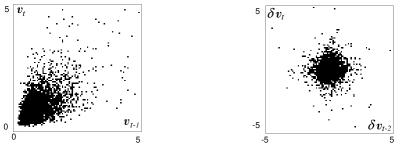

The dissimilarity between these two behaviors is striking. The second autocorrelation coefficient for S&P500 index is reduced by factor of 24, from the value of 0.618 to 0.026. For the EUR/USD rate the decline is 17-fold – from 0.449 to 0.027. Dotted lines in all figures indicate the double standard error, equal to for S&P500 index and for EUR/USD. The disappearance of correlation can be manifestly demonstrated by means of the scatter plots of consecutive values of and .

The two diagrams plotted in Fig. 16 clearly show the presence of correlations between of S&P500 index, and their absence for . In the left chart dots fill the area with a characteristic comet-like shape, while in the right one they form a symmetrical cloud of zero correlation. The similar results, with autocorrelation coefficients being equal to zero, are also obtained for absolute logarithmic returns , as well as for other financial instruments.

We note, however, that for the differences a high negative autocorrelation appears for a shift of one day, . In the above example it is equal to -0.49 for S&P500 index and -0.53 for EUR/USD. However, its origin is not due to the stochastic dynamics of volatility, but rather caused by the overlapping effect. We now elucidate it by way of example. Let us assume that the following simple model governs the price process:

| (18) |

where , and are stationary independent positive random variable that arises because of the errors caused by the finiteness of the sample that is used for volatility measurement. In this case, the differences have zero mean . The first autocorrelation coefficient equals to

| (19) |

where is the variance of . The mean of square arises in the term , which is the one responsible for the effect of overlap. In the same way, the variance of difference is obtained. Thus, first autocorrelation coefficient is exactly equal to , as we have seen above. Correlations with shifts of will be equal to zero, because there is no overlap in this case.

The fact that for the autocorrelations of differences the relations and () hold with a good degree of accuracy corroborates the model (18). However, if the parameter were a constant, there would be no correlation between consecutive values of volatility (due to the independence of ). The correlation may occur, as we have shown above, as a consequence of gradual change in over time. Therefore, actually is a smooth function of time.

Both for the conclusive clarification of the situation with , and for the purposes of further research, we need a method for extracting of the smooth non-stationary component of volatility.

8 Filtering smooth non-stationarity

For the extraction of slowly varying component in the process we will use the Hodrik-Prescott filter Hodrick:1997 (referred to as HP-filter below). The smooth component of the series can be found by way of minimizing the squares of its deviations from empirical data , along with the requirement of curvature minimality for :

| (20) |

where the second difference is given by . The higher parameter is, the more smooth shape one receives as the result. The value of can vary in a very wide range, so it is convenient to use it’s decimal logarithm instead, so that .

When one deals with heavily noisy data, there is always certain freedom in the choice of parameter. If is small, there is a danger of detecting bogus non-stationarity where it does not exist. With little smoothing, component will follow any local fluctuations, which do not have any relation to non-stationarity. On the other hand, with strong smoothing we risk missing important details of the process dynamics that is the focus of our interest.

Therefore, we need a certain statistical criteria of the degree of smoothing in order to reduce the possible arbitrariness. As usual, we will use the random walk as the yardstick.

The mean value of logarithmic returns is equal to the relative change in price within the time lag . We measure the volatility basing on a smoothed mean of modified range within a lag . Here, when using the term ’volatility’, we always assume volatility of a lag (whether it is minute, hour, day, etc.).

If the number of discrete price ticks within a lag is sufficiently large, then regardless of the intra-lag distribution, logarithmic returns will be uncorrelated Gaussian random numbers. Let us smooth their mean value using the HP-filter with different parameters and calculate the typical value of for fluctuations around the average for all empirical data:

| (21) |

Similarly, we determine the error of calculation of smoothed volatility of a lag. Our numerical simulations show that these errors, with a good degree of accuracy, decrease as the parameter grows, as follows:

| (22) |

and manifest no noticeable dependency on the number of empirical points . Moreover, the errors do not depend on the type of distribution (for a discrete model of random walk). The rather small power exponent of 1/8 clarifies the reason why one needs to vary parameter over a wide range of values.

The expressions (22) define a typical corridor of oscillations for the smoothed variables and , which are fluctuations and are not statistically significant for constant volatility. Therefore, we use them as criteria of statistical significance, at least for the sections of data where is approximately constant.

Let us consider a typical example of a numerical simulation (, ) for the three values of (). The boldest line in Fig. 17 corresponds to (), and the thinner one to (). The solid horizontal ’significance levels’ define the double error band in case of , and similar dotted lines, for and . In contrast to significance levels of correlation coefficients, we have a smooth variable , which may for some time dwell outside the band defined by the statistical error. Nevertheless, the relations (22) indeed characterize the behavior of typical fluctuations of a smoothed variable for random data.

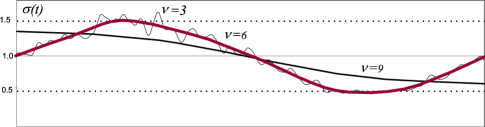

However, in the non-stationary situation, which is a matter of our main interest, we should keep the smoothing factor on the balance. For example, if we model the process , where is the total duration of the simulated data series, we get the following behaviors of volatility smoothing (where volatility is measured by way of modified price range).

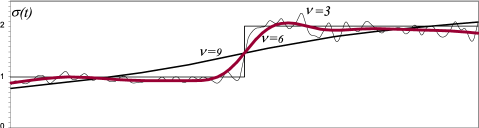

One can see from Fig. 18 that in this case the optimal value is , as follows too closely the noisy fluctuations around the true volatility, while simply does not ’catch’ the periodic nature of . However, the situation deteriorates dramatically, if volatility suffers a shock jump. Thus, let us consider the process, where for half of ’trading days’ the volatility is , and for the second half . For this model, HP-smoothing with different gives the results plotted in Fig. 19.

We see that in this case the choice of blurs the step significantly. On the other hand, smoothing with approximates the jump in volatility much better, but produces noisy and spurious fluctuations for constant .

9 Autocorrelation of normalized volatility

Let us now use the HP-filter to separate the smooth non-stationary part of volatility and filter it out from the data. We will focus on the higher-frequency component of volatility that remain after such filter is applied, as well as on the corresponding autocorrelation coefficients.

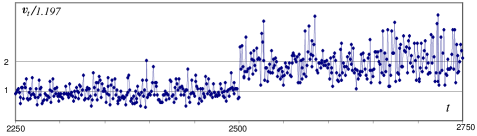

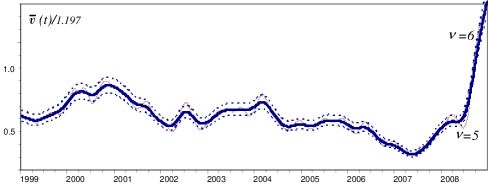

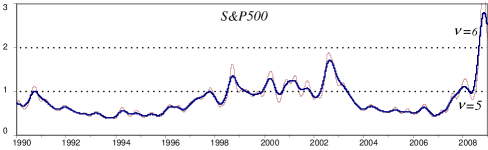

Let us consider the daily modified price range for EUR/USD exchange rate for the period from 1999 to 2008. Using this empirical data, we now estimate daily volatility and plot it in Fig. 20.

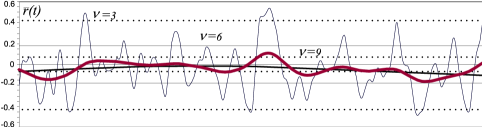

We extract the non-stationarity from the price process using HP-filter. The bold line at the chart below represents the volatility smoothed with (). The double error band, according with the equation (22), for the value of volatility of 0.5 (the average for years 2004-2007), will have the width of . In fact, it is only slightly wider than the width of the line. Therefore, the curves in the graph of non-stationary volatility for can be regarded as statistically significant (see Fig. 21)

The picture changes when smoothing is performed with parameter. Let us take the graph for smoothed with , and plot the double error band around it (marked by dotted lines), which corresponds to the significance levels for . As can be observed from the chart, the smoothed volatility (thin line) is more curvy than the one for ; however, all the bends of the graph lie within the double-error corridor, and thus one could assume they are not statistically significant. On the other hand, the smoothed volatility models noticeably better the behavior of the empirical data around the shock point in fall of 2008.

As can be seen from the previous section, the HP-filter keeps the curvature of the whole curve as low and as constant, as possible. Therefore, it gives good results for relatively quiet intervals, while producing larger distortion when the process goes through abrupt changes.

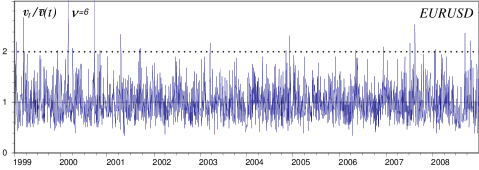

Now we proceed to eliminate the smooth trend from the data. We do this not by subtracting it, as is common practice in the time series processing, but rather divide by it:

| (23) |

The meaning of this procedure is clear; it ensures that the volatility is normalized for the entire data series. As a result of this procedure, the volatilities adjust not only their average, equal to 1, but also their variance, as can be readily seen from Fig. 22.

Let us now compare the autocorrelation coefficients before the normalization procedure (23) is applied (Fig. 23, left), and after it is applied (Fig. 23, center and right). As can be seen, the normalization reduces autocorrelations by nearly 10-fold. The same is true for the first correlation coefficient, which for the price range differences is equal to -0.50. Thus, its origin is indeed related to the effect of overlap discussed above.

We note that during the normalization procedure we divide all daily amplitudes by the smoothed variable . However, when we calculate it, we use a set of values at and around the current time . As a result, the neighboring values of could appear significantly correlated. This may lead to small autocorrelation present after normalization; nevertheless, the value of is very small.

Thus, both simple transition to first differences of the data series, and removal of the smooth component of volatility by means of HP-filter, make correlation coefficients of the adjusted process statistically insignificant. This fact, combined with the discussed above simple explanation for the origin of autocorrelation under non-stationarity, raises doubts about the stochastic nature of volatility. However, one still needs to explore in more depth the noisy component of the volatility. We will return to this issue in the last section of the paper.

10 Back to normal distribution

As was already mentioned in the Introduction, there is a large body of research that study the probability distribution of logarithmic returns. The fact of its being non-Gaussian has become generally accepted (see, for example Jondeau:2007 , Barndorff:2001 ). However, when we speak of the density of probability as function of single variable , we obviously assume the stationarity of random numbers , as we do not involve time dependency. To obtain sufficiently reliable statistical results when inferring , one chooses the widest possible interval containing a large amount of data points .

However, under non-stationarity such approach significantly distorts the ’true’ type of distribution. If statistical parameters depend on time, the density of distribution will not be stationary either . Let us assume that the non-stationarity is parametric and concentrated only in the volatility . Suppose also that is governed by the Gaussian distribution ():

| (24) |

Second and forth moments are equal to, respectively: , and in general case, despite the Gaussian distribution, its ’aggregated’ kurtosis, estimated without taking into account the non-stationarity, becomes different from zero:

| (25) |

In our toy model of a 20-year walk with shock volatility doubling, the kurtosis of data equals to 27/25 = 1.08. In a more general case, the non-Gaussian nature may be affected by other types of non-stationarity, for example, the drift of returns: .

Let us see what happens with the empirical data after eliminating of the non-stationarity. In order to do this we divide all by the value of volatility at a given moment of time. We obtain its current value by smoothing daily modified amplitudes of range using the HP-filter. Thus, we apply the following transformation to initial logarithmic returns:

| (26) |

Such normalization makes random numbers , modulated by function, stationary.

Table 5 contains statistical parameters of S&P500 index logarithmic returns for the period 1990-2008. The total number of trading days is equal to , the share of positive returns is 52.8% for all cases.

| 0.020 | 1.137 | -0.23 | 10.18 | 78.9 | |

| 0.051 | 1.199 | -0.15 | 1.19 | 71.1 | |

| 0.055 | 1.187 | -0.12 | 0.82 | 70.4 | |

| 0.059 | 1.177 | -0.08 | 0.51 | 69.5 |

The first line presents the statistics before the transformation of normalization (26). The other lines contain statistic parameters after transformation, where smoothing with differing parameter is used.

Special attention should be paid to the columns and . We see that smoothing reduces drastically the values of these parameters. This is true even for a sufficiently smooth function , corresponding to . In Fig. 24 it is represented by the bold line:

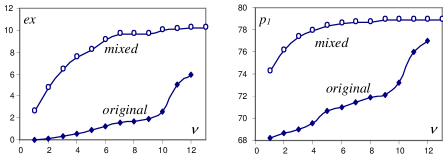

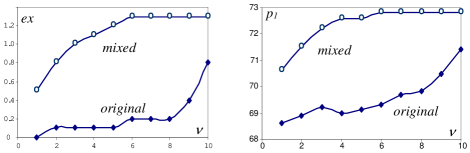

The smaller parameter is, the more intensive the flections of volatility are, because the fluctuations of returns start affecting the average. Obviously, in this case a decrease in kurtosis takes place, even for stationary non-Gaussian random process. To control this effect, we perform the following simulation experiment. We randomly mix the initial pairs of daily returns and volatility in order to eliminate non-stationarity. After that, we apply smoothing with HP-filter, and normalization (26) both to initial data (original), and to mixed ones (mixed). The charts in Fig. 25 present the dependence of the kurtosis (left) and the probability of the fact that returns fall within one sigma (right) as functions of the smoothing parameter . It can be easily noticed that to the right of the kurtosis and probability for mixed data decrease insignificantly. At the same time, statistical parameters characterizing the non-Gaussian property of initial data decrease rapidly.

Thus, as the criterion for the optimal meaning of , one may choose the point where the difference between the statistics of mixed and initial data reaches its maximum.

Another argument for importance of non-stationarity contribution into the non-Gaussian property of distribution is the break out of 2008 financial crisis. As can be seen from Table 5, the kurtosis over the period 1990-2008 is equal to . However, it is enough to eliminate just one volatile year of 2008, in order to make the kurtosis decrease threefold to . The number of trading days for this calculation is reduced in this case by only 5% to 4528.

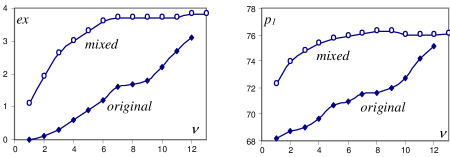

The charts in Fig. 26 depict the dependency of kurtosis and probability on the smoothing parameter for mixed and initial data of S&P500 index daily returns for the period 1990-2007. One can notice that, although the initial value of kurtosis is relatively small, it nevertheless decreases statistically significantly as a result of elimination of non-stationarity from the data. For normalized data, the value of kurtosis can be considered as significant, which is four times smaller than for initial data.

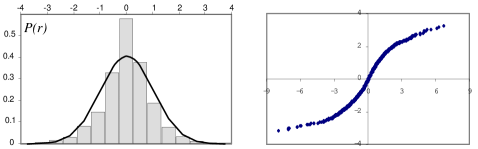

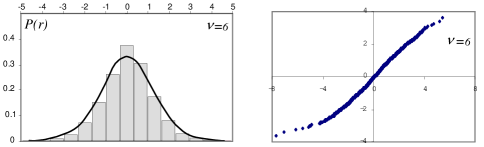

Let us plot (see Fig. 27) the histograms of probability density distribution and a graph of normal probability (in a way similar to Fama:1965 ), formally based on the initial non-stationary data, as well as the same quantities after the normalization procedure (26) is applied to the data (Fig. 28).

The unmarked line in the charts corresponds to the Gaussian distribution. A graph of normal probability represents dependency of relation , where is an integral normal distribution, and is empirical integral distribution for returns. If the empirical distribution of is Gaussian, this graph should be a straight line. We see that after normalization the density of probability becomes much more close to normal. Deviations from the straight line are particularly evident for the excessively large negative returns because of the rare negative shock impacts to the market.

Let us consider, for comparison, the probability distribution of currency market daily returns using the EUR/USD rate for the period 1999-2008 as sample. Basic statistical parameters before normalization (first line) and after smoothing with different parameters are given in Table 6. We see that the initial data has relatively small kurtosis, but after smoothing it decreases even further. The mean value of volatility after normalization is close to one. This confirms that is a good unbiased estimation of the daily volatility of rate returns.

| 0.008 | 0.652 | 0.05 | 1.3 | 72.7 | |

| 0.017 | 1.022 | 0.03 | 0.8 | 71.5 | |

| 0.022 | 0.995 | 0.00 | 0.1 | 69.3 | |

| 0.022 | 0.993 | 0.01 | 0.1 | 69.0 |

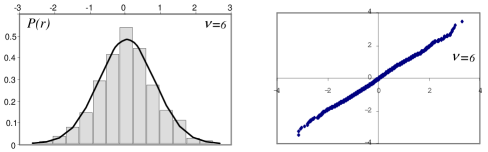

Testing statistical significance of the decrease in kurtosis and the probability shows practically zero kurtosis of normalized returns (Fig. 29).

The corresponding histogram and normal probability graph are plotted in Fig. 30.

As a result we receive a virtually canonical normal distribution with deviations that are rather typical for a relatively small sample ().

We shall not conduct a more detailed statistical analysis of distribution form, limiting the argumentation to these illustrative examples. We infer (see Conclusion) that the observed data is composed of the mixture of normally distributed fluctuations of the market, modulated with non-stationary volatility, and rare shock impacts. Therefore, even after the elimination of non-stationarity there may remain shock outliers, which make the total distribution weakly non-Gaussian.

11 Quasi-stationarity of volatility

Vanishing autocorrelation coefficients between consecutive values of volatility, generally speaking, do not exclude the possibility of its stochastic description. In particular, we can write down the following simple discrete process:

| (27) |

where and are independent random variables, while , are constants. However, within this model the interpretation of volatility as a random variable becomes rather superfluous. In fact, we come back to the usual stationary model , where . In particular, if and are normally distributed, the distribution for would no more be normal with kurtosis equal to . Nevertheless, the question of local stationarity of ’true’ volatility remains open.

Let us conduct several statistical estimations. First, we consider a modified amplitude of range. The spread of its values under constant volatility occurs due to finite width of distribution density . One can obtain its analytical form from the equation (A5) of Appendix A, and present it as the following infinite series:

where , are non-normalized Gaussian functions (see Appendix A). Below we list the integral probabilities of the fact that variable falls within the interval (the first line contains values of , the second, corresponding probabilities measured in percent points):

| 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 | 1.1 | 1.2 | 1.3 | 1.4 | 1.5 | 1.6 |

| 0.6 | 3.3 | 10.4 | 22.5 | 37.8 | 53.7 | 68.1 | 79.5 | 87.7 | 93.1 | 96.4 | 98.2 |

The modified price range should remain within the interval about 96.4% of days; it very rarely drops below 0.5.

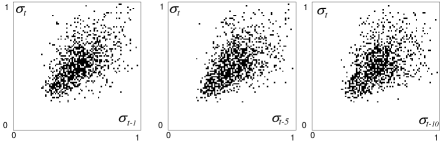

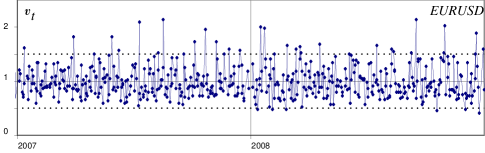

If we eliminate (26) by smoothing procedure with the non-stationarity in daily modified ranges for EURUSD in 2007-2008 years, the residual series has dynamics as shown in Fig. 31.

In case of Brownian random walk, dotted lines correspond to the probability 96% of staying within the interval . We see that, except for rather rare outliers, most of daily volatilities estimated by modified amplitude of probability, fell into the dotted corridor. The number of outliers is slightly higher than expected 4% (as there is 250 trading days in a year, 250*4%=10). This small excess of extremal values may be interpreted (especially in 2008, a crisis year) as occasional shock impacts to the market, not related to its ’typical’ intrinsic dynamics.

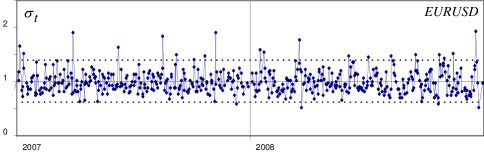

As we have discussed above, the ’daily’ volatility can be estimated not only by means of modified amplitudes of range, but also by calculating its value on the base on intraday lags, i.e. 15-minute ticks. In Fig. 32, the dynamics of volatility is presented, after the elimination of non-stationarity, obtained by the latter method for the period of 2007-2008 for EUR/USD exchange rate.

In this case the spread of values is related to the finiteness of the sample that is used for volatility calculations. In order to determine the significance level, one has to know the corresponding distribution of probability. As we know, the error of stationary volatility calculation is determined by fourth moments and, in case of large kurtosis, it will be quite large.

The intraday 15-minute data distribution has significant kurtosis. Straightforward computation of kurtosis for EURUSD during 2004-2008 yields the value of 20, which is due to the long-term non-stationarity, the substantial cyclic effects in intraday activity, as well as several other specific reasons (see Biais:2005 , Madhavan:2000 for a detailed discussion), into which we will not delve here.

In order to obtain the significance levels, we will conduct the following simple experiment with the data. Let us calculate the logarithmic return basing on 15-minute lags of EUR/USD rate. Then, to preserve the intraday periodicity, we shall mix data points with the same intraday time. In other words, we randomly shuffle all lags at 00:00, then apart from them we mix lags of 00:15, etc. For these synthetic data, that are free of any memory effects except the intraday cycles, we calculate the meaning of intraday volatility. Then we normalize the series so that the mean is equal to 1, and plot the corresponding distribution of probability. It turns out that about 96% of data stays within the corridor. It is these levels, which characterize the ’typical’ range of volatility due to the finiteness of data, that are marked at the above chart with dashed lines. We see that the data fits into the corridor quite well.

We stress that the computations performed above are rather a qualitative estimation than a strict statistical analysis; such analysis might not be appropriate at all without constructing a complete model of non-stationarity of data at different time scales. However, an assumption about the local constancy of volatility of daily lag returns appears rather plausible. In other words, the daily volatility of the market most probably is described by a smooth, rather slowly varying function of time. At any moment, its value can be considered locally constant, and it determines the stochastic dynamics of price returns for a financial instrument.

12 Conclusion

Let us reiterate the main inference that we argued for in this paper:

Volatility and other statistical parameters should be regarded as gradually changing functions of time. They determine locally quasi-stationary stochastic dynamics of prices for financial instruments. There are rare and irregular shock impacts that influence the markets, resulting in shifts in daily returns, and as they accumulate, affect the value of long-term volatility.

The situation resembles the deformation of a plastic material after a series of impacts, and the gradual restoration of form after external influence is terminated. The study of properties of such resilience of volatility are of great importance, especially for forecasting the time of its reversal to the long-term typical levels.

Therefore, the stochastic nature of markets is determined by the following two components: 1) intrinsically Gaussian-distributed daily returns with slowly changing volatility; and 2) rarely occurring shock impacts. These shocks are assumed to be essentially unpredictable, but their impact on the volatility as well as its subsequent evolution should be the subject of research.

Actually, shocks are quite inconspicuous; in reality it is quite difficult to separate the ’unnatural’ behavior of the market as a result of shocks from ’normal’ volatility. Financial analysts and economic commentators never fail to find the piece of news to account for all price spikes and crashes. On the other hand, such events as Lehman’s bankruptcy can hardly be considered everyday news.

Volatility can also gradually increase as a result of relatively insignificant negative news background, provided that such background lasts for long enough. Thus, a gradual increase in volatility since the beginning of 2007 was a result of precisely such ’soft’ pressure on the markets from the real estate sector. Since the autumn of 2008, this growth has been explosive and unprecedented for the modern history of financial markets. As we know, it originated from financial sector, and triggered an avalanche-like effect of confidence crisis and widespread panic. All this, eventually, delivered a blow to the real sector of economy.

Finally, an increase in volatility usually accompanies ’unmotivated’ booms in the market, when a financial bubble starts to inflate. High volatility also persists in the period of its collapse. When market goes into a ’quiet’ phase of growth, volatility usually slowly decreases.

Peaks typically observed in the charts of non-stationary volatility bring up the analogy with resonance phenomena in physics. Such connection implies the existence of certain equations describing the system dynamics. There is no doubt that a relaxation mechanism exists, ensuring that a decay of system excitations happens after a certain period, determined by the life time of the resonance.

When one speaks about a gradual course of change in volatility, one should keep in mind that it refers to the ’typical’ long-term market situations. Sometimes, however, jump-like changes in statistical parameters occur, which determine the stochastic dynamics of the price process. It seems plausible that such a qualitative shift in market behavior happened in September 2008. In contrast, the exit from this instability, and return to equilibrium, is likely to be quite gradual and prolonged.

We infer that the non-Gaussian nature of markets stems from two origins. First, it is the artifact of uncritical postulation of stationarity under conditions when it doesn’t really exist. This component can be removed, at least in theory. After the data is transformed into a stationary form, the non-Gaussian features reduce significantly. However, the rare shock impacts, which are the second origin, even when combined with stationary Gaussian returns, still render the distribution weakly non-Gaussian. This is particularly evident in the case of stock market, which has the after-hours periods when negative or positive news accumulate. When the markets open, a possibility appears of a ’single emission’ of accumulated emotions. Around-the-clock foreign exchange markets can respond to the development of such shocks in more ’subdued’ way.

Autocorrelation coefficients in various volatility measures also arise due to the non-stationarity of the data and disappear after it is eliminated. In this sense, they are indeed the evidence of long-term memory, but do not have anything to do with the short-term stochastic properties of volatility, which are assumed in corresponding autoregressive models. Therefore, further research should focus on forecasting the smooth dynamics of volatility, rather the stochastic theories of volatility behavior.

Acknowledgement

I am grateful to Alexander Zaslavsky, Igor Chavychalov, Andrej Tishchenko, Oleg Orlyansky, Leonid Savtchenko, Alexander Ferludin and Anna Gorbatova for many useful comments. Any remaining errors are my own.

Appendix Appendix A Brownian walk

In this appendix we provide the basic expressions for Brownian motion described by the stochastic equation . Let us first consider the case of driftless process (). Without any loss of generality, we may assume that at the initial moment of time . The maximal and minimal values of for the period are equal to and , respectively, and . The height of ascent and the depth of descent are always positive, and . The amplitude of range is equal to . Below we consider the case of unit volatility and unit time interval . To restore the original notation, it is necessary to substitute for the dimensionfull variables , , , . The same should be done in the differentials , etc. in the integrals containing the probability densities. In order to make the formulae more concise, we use this notation for the normal distribution function: .

We start with the relation for probability that does not rise above and does not fall below , when the closing return is :

| (A1) |

This formula was first received by Feller:1951 . We also note an exclusively useful reference book by Borodin:2000 . Distributions for other variables are derived from the probability (A1). For the return, height and depth we have:

| (A2) |

The density of probability for the range is expressed in the form of an infinite series over Gaussian basis:

| (A3) |

This series converges rather quickly for all . A characteristic property of Feller’s distribution is an extremely rapid decline in the density of probability for large values of . Here is a sample of values of integral probabilities :

| 0.750 | 1.000 | 1.500 | 2.000 | 2.500 | 3.000 | 3.500 | 4.000 | |

| 0.002 | 0.063 | 0.487 | 0.819 | 0.950 | 0.989 | 0.998 | 1.000 |

The parameter is smaller than 0.75 () only in 2 cases out of 1000. The mean value is , the variance is . The one sigma interval ( = [1.120 .. 2.071]) contains 71.6% of all values, while the double sigma interval ( = [0.645 .. 2.547]) contains 95.6%; and data points outside of the latter interval should, in reality, occur only for above the mean.

The joint densities of probability for height (), depth () and range () have the following form:

| (A4) |

| (A5) |

Note also that , and .

Let us provide a table of mean values for different variables (where ):

where is a Rieman -function. The mean values for and are the same as for . The means of certain cross-products are given below:

Expressions for other mean values, as well as their generating function, can be found in Garman:1980 .

For a process with a non-zero drift , we shall use the above-determined driftless densities. In order to restore time and variance , we should additionally substitute the shift as follows: . The density of probability for returns is equal to:

Expressions for joint probability densities Borodin:2000 :

Thus, the densities corresponding to are always multiplied by a factor . In the presence of drift we obtain:

Exact expressions for mean values of other variables are rather cumbersome. However, as for financial data the condition holds, it is acceptable to decompose a factor into a series and to use means for the case . As a result we receive:

| (A6) |

| (A7) |

The mean values of height and depth are linear in , and only even powers of are present in the tail of expansion. The means of lag range and absolute returns contain only even powers of . Note also the following simple relations, available in closed form:

, , , .

Appendix Appendix B Measures of volatility

The width of probability distribution of a positive random variable can be characterized with a relative error , where as usual denotes the standard deviation .

Note that the relative width of distributions for and are different, and thus actually there are different criteria for optimality of volatility measurement. For example, in order to calculate the stationary volatility one usually uses averaging of either squared returns, or the squares of the lag ranges Parkinson:1980 :

| (B8) |

As in this paper we examine the non-stationary nature of volatility and use the non-linear HP-filter for smoothing, it is more convenient to average volatilities proper, rather than their squares; the latter, as we will see below, yield a biased value of for small . Nevertheless, considering the various measures of volatility, we will calculate the relative width of both the value its square.

Let us recite some well-known volatility estimators. We shall use a Parkinson measure (1980) Parkinson:1980 as a base; it is equal to the amplitude of range . Garman and Klass (1980) Garman:1980 , working in the class of analytic functions of , , , proposed the following optimal combination, which is a better measure than that of Parkinson:

| (B9) |

A simpler and drift-independent measure is suggested by Rogers and Satchell (1991) Rogers:1991 :

| (B10) |

Let us show that the simplest linear modification of Parkinson’s measure

| (B11) |

where is a constant, leads to a narrower distribution than the amplitude of range. If we use relative volatility as a criterion of narrowness, it is not difficult to find the optimal value of the coefficient using the means from the Appendix A:

| (B12) |

However, is not the only criterion, and due to the low sensitivity of the relative volatility to change in , we use in this paper the value and notation . In what follows we denote .

We note that there is another simple measure of volatility, comparable in its effectiveness to (B11), namely:

| (B13) |

Although the probability of zero value for finite duration of a lag is vanishingly small, it is still necessary to define the corresponding value for . Actually, the relations (B11) and (B13) are not analytic functions on and , and thus are not governed by the lemma from Appendix B of Garman:1980 .

In addition to the width of distribution, sometimes absent or weak dependence on the drift are used as a criterion. Note that for daily, or shorter, lags ; therefore, this criterion is not that significant. The above proposed measure of the modified lag range, as well as the price range itself, depends on . However, this dependence is significantly weaker for than for the amplitude . If we use the presentations (A6), (A7), we can write the following expression for :

| (B14) |

It can be seen that the factor beside for is four times smaller than for (). Consequently, the dependence on is four times weaker as well. When (denoted below) the coefficient at becomes equal to zero, and the dependence on is weakening still, although it disappears completely only for the measure by Rogers and Satchell.

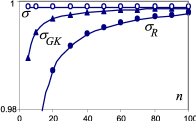

Let us now compare the statistical parameters of different volatility measures shown in Table 7.

| Measure | ||||||||

|---|---|---|---|---|---|---|---|---|

| 1.596 | 2.773 | 0.476 | 0.97 | 1.24 | 70.6 | 0.298 | 0.638 | |

| 0.960 | 0.998 | 0.275 | 0.46 | 0.42 | 69.5 | 0.287 | 0.576 | |

| 1.064 | 1.217 | 0.292 | 0.52 | 0.29 | 68.4 | 0.275 | 0.557 | |

| 0.968 | 0.998 | 0.245 | 0.60 | 0.39 | 68.6 | 0.253 | 0.519 | |

| 1.254 | 1.673 | 0.316 | 0.53 | 0.28 | 68.4 | 0.252 | 0.513 | |

| 1.197 | 1.523 | 0.300 | 0.53 | 0.26 | 68.2 | 0.251 | 0.511 | |

| 1.233 | 1.615 | 0.308 | 0.55 | 0.29 | 68.3 | 0.250 | 0.510 |

We use italic font to mark the values obtained by Monte Carlo simulation for 3.5 million lags, each being a random walk of 1 million ticks. In this case, for means and volatility an error of order of is possible in the last significant digit. The other values (in upright font) are derived through analytical calculations.

For non-stationary data it is often necessary to conduct the averaging over a relatively small number of observations . In this case, a bias becomes apparent in quadratic measures for volatility . Even if one calculates the classical squared volatility by means of the unbiased formula (B8), the value will be biased; indeed, when averaging over large numbers of samples of size , we have , but . If we are interested in the value of volatility itself rather than its square, it is better to use linear rather than quadratic measures for non-stationary data.

To illustrate the effect of drift we provide charts of mean values of volatility (Fig. 33), obtained by averaging a large number of samples of values each, for standard definition of and measure (B9) compared to a linear measure of .

Thus, the measure has a relatively narrow distribution and consecutively results in smaller error in volatility measurement. Simplicity is its obvious advantage, as compared with the measures and . In addition, it is unbiased in case of small sample size, which is significant in examining the effects of non-stationarity.

References

- [1] G William Schwert. Why does stock market volatility change over time? Journal of Finance, 44(5):1115–53, December 1989.

- [2] Neil Shephard, editor. Stochastic volatility: selected readings. Oxford Univ. Press, 2005.

- [3] Ser-Huang Poon and Clive W. J. Granger. Forecasting volatility in financial markets: A review. Journal of Economic Literature, 41(2):478–539, June 2003.

- [4] D.A. Hsieh. Chaos and nonlinear dynamics: application to financial markets. Journal of Finance, 46(5):1839–1877, 1991.

- [5] M. Watanabe. Price Volatility and Investor Behavior in an Overlapping Generations Model with Information Asymmetry. The Journal of Finance, 63(1):229–272, 2008.

- [6] R. Battalio and P. Schultz. Options and the Bubble. Journal of Finance, 61(5):2071, 2006.

- [7] Michael McAleer and Marcelo Medeiros. Realized volatility: A review. Econometric Reviews, 27(1-3):10–45, 2008.

- [8] Neil Shephard and Torben Andersen. Stochastic volatility: Origins and overview. Economics Papers 2008-W04, Economics Group, Nuffield College, University of Oxford, May 2008.

- [9] C. Broto and E. Ruiz. Estimation methods for stochastic volatility methods: a survey. Journal of Economic Surveys, 18(5):613–649, 2004.

- [10] Torben G Andersen and Tim Bollerslev. Answering the skeptics: Yes, standard volatility models do provide accurate forecasts. International Economic Review, 39(4):885–905, November 1998.

- [11] J.Knight and S. Satchell, editors. Forecasting Volatility in the Financial Markets. Elsevier, third edition, 2007.

- [12] Robert F Engle and Andrew J Patton. What good is a volatility model. Quantitative Finance, 1(2):237–245, 2001.

- [13] Robert F Engle. Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica, 50(4):987–1007, July 1982.

- [14] Robert Engle. New frontiers for arch models. Journal of Applied Econometrics, 17(5):425–446, 2002.

- [15] Sassan Alizadeh, Michael W. Brandt, and Francis X. Diebold. Range-based estimation of stochastic volatility models. Journal of Finance, 57(3):1047–1091, 06 2002.

- [16] Bjørn Eraker. Do stock prices and volatility jump? reconciling evidence from spot and option prices. Journal of Finance, 59(3):1367–1404, 06 2004.

- [17] Linda Canina and Stephen Figlewski. The informational content of implied volatility. Review of Financial Studies, 6(3):659–81, 1993.

- [18] Thomas Mikosch and Cătălin Stărică. Nonstationarities in financial time series, the long-range dependence, and the igarch effects. The Review of Economics and Statistics, 86(1):378–390, 01 2004.

- [19] Clive W. J. Granger and Timo Terasvirta. A simple nonlinear time series model with misleading linear properties. Economics Letters, 62(2):161–165, February 1999.

- [20] F.X. Diebold and A. Inoue. Long memory and regime switching. Journal of Econometrics, 105(1):131–159, 2001.

- [21] Benoit Mandelbrot. The variation of certain speculative prices. Journal of Business, 36:394, 1963.

- [22] Eric Jondeau, Ser-Huang Poon, and Michael Rockinger. Financial Modelling under non-Gaussian Distributions. Springer, 2007.

- [23] Eugene F. Fama. The behavior of stock-market prices. The Journal of Business, 38(1):34–105, 1965.

- [24] Michael Parkinson. The extreme value method for estimating the variance of the rate of return. Journal of Business, 53(1):61–65, January 1980.

- [25] Mark B Garman and Michael J Klass. On the estimation of security price volatilities from historical data. Journal of Business, 53(1):67–78, January 1980.

- [26] L.C.G. Rogers and S.E. Satchell. Estimating variance from high, low and closing prices. Annals of Applied Probability, 1(4):504–512, 1991.

- [27] L. C. G. Rogers and Fanyin Zhou. Estimating correlation from high, low, opening and closing prices. ANNALS OF APPLIED PROBABILITY, 18:813, 2008.

- [28] Dennis Yang and Qiang Zhang. Drift-independent volatility estimation based on high, low, open, and close prices. Journal of Business, 73(3):477–91, July 2000.

- [29] Ole E. Barndorff-Nielsen and Shephard. Econometric analysis of realized volatility and its use in estimating stochastic volatility models. Journal Of The Royal Statistical Society Series B, 64(2):253–280, 2002.

- [30] Bruno Biais, Larry Glosten, and Chester Spatt. Market microstructure: A survey of microfoundations, empirical results, and policy implications. Journal of Financial Markets, 8(2):217–264, May 2005.

- [31] Torben G. Andersen, Tim Bollerslev, Francis X. Diebold, and Paul Labys. Modeling and forecasting realized volatility. Econometrica, 71(2):579–625, March 2003.

- [32] Ananth Madhavan. Market microstructure: A survey. Journal of Financial Markets, 3(3):205–258, August 2000.

- [33] Federico M. Bandi and Jeffrey R. Russell. Separating microstructure noise from volatility. Journal of Financial Economics, 79(3):655–692, March 2006.

- [34] Tim Bollerslev and Ian Domowitz. Trading patterns and prices in the interbank foreign exchange market. Journal of Finance, 48(4):1421–43, September 1993.

- [35] R. Cont. Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1(2):223–236, 2001.

- [36] Zhuanxin Ding, Clive W. J. Granger, and Robert F. Engle. A long memory property of stock market returns and a new model. Journal of Empirical Finance, 1(1):83–106, June 1993.

- [37] F. Jay Breidt, Nuno Crato, and Pedro de Lima. The detection and estimation of long memory in stochastic volatility. Journal of Econometrics, 83(1-2):325–348, 1998.

- [38] Robert J Hodrick and Edward C Prescott. Postwar u.s. business cycles: An empirical investigation. Journal of Money, Credit and Banking, 29(1):1–16, February 1997.

- [39] Ole E. Barndorff-Nielsen and Neil Shephard. Non-gaussian ornstein-uhlenbeck-based models and some of their uses in financial economics. Journal Of The Royal Statistical Society Series B, 63(2):167–241, 2001.

- [40] William Feller. The asymptotic distribution of the range of sums of independent random variables. The Annals of Mathematical Statistics, 22:427–432, September 1951.

- [41] A.N. Borodin and P. Salminen. Handbook of Brownian Motion - Facts and Formulae. Basel: Birkhauser, 2000.