A test for second order stationarity of a time series based on the Discrete Fourier Transform (Technical Report)

Abstract

We consider a zero mean discrete time series, and define its discrete Fourier transform at the canonical frequencies. It is well known that the discrete Fourier transform is asymptotically uncorrelated at the canonical frequencies if and if only the time series is second order stationary. Exploiting this important property, we construct a Portmanteau type test statistic for testing stationarity of the time series. It is shown that under the null of stationarity, the test statistic is approximately a chi square distribution. To examine the power of the test statistic, the asymptotic distribution under the locally stationary alternative is established. It is shown to be a type of noncentral chi-square, where the noncentrality parameter measures the deviation from stationarity. The test is illustrated with simulations, where is it shown to have good power. Some real examples are also included to illustrate the test.

Keywords and phrases Discrete Fourier Transform, linear time series, local stationarity, Portmanteau test, test for second order stationarity.

1 Introduction

An important assumption that is often made when analysing time series is that it is at least second order stationary. Most of the linear time series literature is based on this assumption. If the assumption is not properly tested and the analysis is performed, the resulting models are considered to be misspecified and any forecasts obtained are not appropriate. Therefore, it is important to check whether the time series is second order stationary.

In recent years several statistical tests have been proposed. Many of the proposed tests are based on comparing spectral densities over various segments (? (?), ? (?), ? (?), ? (?) and ? (?)) comparing covariance structures over various segments of the data (? (?), ? (?) and ? (?)), or comparisons of wavelet coefficients (? (?), ? (?)). The underlying important assumption, on which these tests are based, is on a delicate, subjective, choice of segments of the data. In this paper we propose a test based on the discrete Fourier transforms based on the entire length of data, thus avoiding a subjective choice of segment length.

In Section 2 we define the Discrete Fourier transform and show that the Discrete Fourier transforms are asymptotically uncorrelated at the canonical frequencies if and only if the time series is second order stationary. This motivates the test statistics, which is based on the discrete Fourier transform. The Portmanteau type test statistics we propose is based on the covariance function calculated using the discrete Fourier transform at the canonical frequencies. The asymptotic sampling distribution of the test statistic is obtained in Section 3. Further we show that the asymptotic sampling distribution is approximately distributed as a central chi-square under the null hypothesis that the time series is second order stationary. To examine the power of the test, we consider the case of locally stationary time series (see ? (?), ? (?), ? (?), ? (?), ? (?), and ? (?)), and derive the distribution of the test statistic under this class of alternatives. In Section 4 we show the distribution under this class of alternatives, is a type of non-central chi-square, where the noncentrality parameter is in some sense a measure of departure of nonstationarity. In Section 5, through simulations, we examine the power of the test, and show that for various types of alternatives the power is very high. We end this section with various comments on the types of nonstationary behaviour the test can detect. In Section 6 we illustrate the test with two real data examples.

An outline of important aspects of some proofs can be found in the appendix, and the full details can be found in the accompanying technical report.

2 The Test Statistic, motivation and sampling distribution

2.1 Motivation

Let be a zero mean time series. Suppose we observe and let be its Discrete Fourier Transform defined as

where are the canonical frequencies. It is well known that if is a second order stationary time series, whose covariances are absolutely summable then for and we have Therefore in the case of stationary processes, the discrete Fourier transform is asymptotically uncorrelated. Let

where is the complex conjugate of the complex variable . From the above we observe if for or , then we have for . In other words, an uncorrelated discrete Fourier transform sequence implies that the original time series is second order stationary, up to lag .

Let us consider a simple example to show that even if the time series are independent, but not stationary, then are not uncorrelated. Let us suppose , where is a deterministic, time dependent function and are independent identically distributed random variables with and . In this case, the covariance of the discrete Fourier transform at the canonical frequencies is

From the above, it is clear that for some . If we suppose that is a sample from a smooth function , that is , then by using the rescaling methods often used in nonparametric statistics we have

2.2 The test statistic

The above observations lead us to the following test statistic. We note that, if the the time series is second order stationary, then and as , where is the spectral density of the original time series (see ? (?) and ? (?)). Therefore by standardising with , under the null of stationarity, is close to an uncorrelated, second order stationary sequence. Therefore to test for stationarity of we will test for randomness of the sequence . The proposed test will be a type of Portmanteau test (see ? (?) for applications of the Portmanteau test in time series analysis). Of course, in reality the spectral density is unknown, therefore we will replace with the estimated spectral density function , where

| (1) |

is a positive, continuous, symmetric kernel function which satisfies and and is a bandwidth.

We define the empirical covariance at lag , which is complex valued, of the discrete Fourier transform as

| (2) |

The proposed test statistic is based on . In the technical report we show that if is a stationary time series and then both the variance of the real and imaginary parts of converge to

| (3) |

as , where , is the fourth order cumulant spectra. Furthermore, under the null hypothesis of second order stationarity, we show in Lemma 3.1, that the empirical covariances at different lags are asymptotically uncorrelated and . Therefore we define the test statistic

where and or . For example, we can choose , and use consecutive lags. We note, that unlike the classical Portmanteau tests, using covariances with a large lag is not problematic as the discrete Fourier transform is periodic.

We derive the asymptotic distribution of the test statistic in Section 3, under the null hypothesis that statisfies the MA representation

| (4) |

where are independent, identically distributed random variables with , and . Under these assumptions we will show in Corollary 3.1, below, that and converges in distribution to . Therefore we reject the null of second order stationarity at the significance level if . We proved the above result under the assumption that the time series is stationary, linear and has absolutely summable covariances. But we believe this result is true even if the process is nonlinear, but stationary or has long memory but is stationary. The proof is beyond the scope of this paper. We need strong mixing condition to prove this general result.

In the case of linearity, (3) has an interesting form. It can be shown that

where

Hence in the case of linearity, the test statistic is equivalent to

| (5) |

Morever, if is small and small lags are used (ie. ) then the test statistic can be approximated by .

Remark 2.1 (Estimation of the tri-spectra)

We observe that the test statistic requires estimates of the the parameter

Therefore to estimate the above parameter we require estimators of the tri-spectra and spectral density and respectively. ? (?) propose a consistent estimator of the tri-spectra , which we denote as . Therefore an estimator of the above integral is

where is defined in (1). Since is a consistent estimator of , replacing in the test statistic with , does not alter the asymptotic sampling distribution.

Remark 2.2 (Practical issues)

The asymptotic distribution under the null is derived under the assumptions that the spectral density of the time series is bounded away from zero. In practice, even if this assumption holds, the estimated spectral density may be quite close to zero. Therefore, in this case, to prevent falsely rejecting the null, we suggest adding a small ridge to the spectral density estimator to bound it away from zero.

2.3 The power of the test

In Section 4 we obtain the asymptotic sampling properties of the test statistic , under the alternative of local stationarity. In order to understand what nonstationary behaviour the test statistic can detect and how to select the lag in the test statistic, we will now outline some of the results in Section 4. Suppose that is a nonstationary time series, where in a small neighbourhood of the observations are close to stationary and has the local spectral density . In Lemma 4.1 we show that , where

| (6) |

and that has asymptotically a type of non-central chi squared distribution where the noncentrality parameters are given by . Hence, the test statistic is more likely to reject the null, the further , is from from zero. Studying the above we see that if the dynamics change slowly over time, then a small lag , should yield a large . On the other hand, if there is a rapid change in the behaviour, a large , leads to a large . Therefore, in this case, by using a large , we are more likely to reject the null.

3 Sampling properties of the test statistic under the null

We now derive the asymptotic distribution under the null of stationarity. We will use the following assumptions.

Assumption 3.1

Let us suppose that satisfies (4).

Let and define the spectral density . Assume

-

(i)

(noting that this implies ).

-

(ii)

.

-

(iii)

and .

-

(iv)

Either (a) or (b) the derivative of the spectrum is piecewise montone on the interval (in other words can be partitioned into a finite number of intervals which is either nonincreasing or nondecreasing).

We use Assumption 3.1(i,ii) to show asymptotic normality if (in fact Assumption 3.1(ii) is used to obtain the error when replacing , with , defined below). We use Assumption 3.1(iv) to obtain the rate of decay of the Fourier coefficients of the function .

To simplify the analysis of the test statistic we replace the denominator in the covariance with its deterministic limit. To do this, we define the unobserved covariance

| (7) |

and obtain the asymptotic distribution of .

In the following lemma we show that the difference between is negligible.

Theorem 3.1

In the following lemma we derive the asymptotic variance of , and show that is asymptotically uncorrelated at different lags , and at the real and imaginary parts.

Lemma 3.1

PROOF. See Appendix A.3.

We now show normality of , which we use to obtain the distribution of .

Theorem 3.2

Suppose Assumption 3.1 holds. Then for fixed we have

| (10) |

as and , where is the identity matrix and .

PROOF. See Appendix A.4.

By using the above we are able to obtain the asymptotic distribution of .

Corollary 3.1

Suppose Assumption 3.1 holds. Then for fixed we have

with

,

as .

PROOF. The result immediately follows from Theorem 3.2.

Hence we have shown under the null, that the test statistics has asymptotically a distribution.

4 Sampling properties of the test statistic under the alternative of local stationarity

It is useful to investigate the behaviour of the test statistic in the case that the null does not hold. If the covariance structure varies over time, then the limit of will not be zero. This suggests that the test statistic will have a type of non-central distribution. However, in the case that time-varying covariance has no structure it is not clear what the limit of will be. For example, consider the simple example of a time-varying AR process, , where are iid random variables. Without any structure on the AR coefficient, , it is not clear what the spectral density estimator, , defined in (1) should converge to. Hence it is not possible to obtain the limit of . On the other hand, let us suppose that , varies slowly over time and is a sample from a function , that is for some , , and the time series satisfies . Now in this set up, as we let , varies less and is observed on a finer grid, which in reality can never be realised. Hence, by supposing that varies slowly over time we have imposed some structure on the time-varying parameter and we are using an infill asymptotic argument (see ? (?)). In this case, we will show, below, that is an estimator of the integrated spectrum, this can also be viewed as the average of local spectrums. The model described above, is an example of a locally stationary linear time series considered in ? (?) and ? (?). Therefore, following ? (?), we define a locally stationary linear time series as

| (11) |

where are iid random variables, , . Therefore we will consider the behaviour of the test statistic under the alternative of local stationarity.

In order for to be a locally stationary time series, we will assume that closely approximates the smooth function . Hence the time-varying MA parameters vary slowly over time. It can be shown that in this case, is a locally stationary time series because it can locally be approximed by a stationary time series. We will use the following assumptions.

Assumption 4.1

Let us suppose that satisfies (11). Suppose, there exists a sequence of functions , such that is Lipschitz continuous and , where is a positive monotonically decreasing function which satisfies . Let (hence ).

-

(i)

and (hence ).

-

(ii)

.

-

(iii)

Define the integrated spectral density , and assume that .

-

(iv)

Either (a) (hence ) or (b) and are piecewise monotone functions with respect to .

We will show in Lemma 4.1, below, that in the locally stationary case the spectral density estimator defined in (1) estimates the integrated spectrum , where is defined in Assumption 4.1(iii). Roughly speaking, one can consider the integrated spectrum as the average of the locally stationary spectrums.

As in Section 3, it is difficult to directly obtain the distribution of . Instead we replace the random denominator with its deterministic limit (that is with ), and define

| (12) |

where is the integrated spectrum. The following result is the locally stationary analogue of Theorem 3.1.

Theorem 4.1

From the lemma above we see that in order for the sampling properties of and to coincide, we require that .

We now obtain the mean and variance of under the alternative hypothesis of local stationarity.

Lemma 4.1

PROOF. See Appendix A.3.

We use the above to obtain the asymptotic distribution of under the alternative. First we recall that we estimated the standardisation of , , in Remark 2.1. It is worth noting that in the case that of local stationarity, is an estimator of

where is the integrated spectral density and and , with .

Theorem 4.2

Furthermore define , where

Then we have

with as , where is a normally distributed random vector with and . Note the small abuse of notation, when we say , we mean that the distribution of random variable converges to the distribution of random variable .

Remark 4.1

We observe that if the matrix , define in the

theorem above, were the identity matrix, then the limiting distribution of

, is a non-central

where the noncentrality parameter

is determined by the limit of (for ).

Hence the power of the

test depends on the deviation of

from zero,

for each of the lags . We see that term depends on the Fourier

coefficient

and

the magnitude of depends on whether the frequency of the

nonstationary variation matches .

However, in the case that is s second order nonstationary time series, will not be a diagonal time series, because there is correlation between the real and imaginary parts of and also correlation at different lags . Thus the limiting distribution of will not be a classical non-central , due to the correlations in . However, the conclusions discussed above still hold, namely the power of the test is determined, mainly, by the magnitude of mean vector .

5 Simulations

We now consider a simulation study. We compare the results of the test statistic for both stationary and nonstationary time series. In each case, we replicate the time series 1000 times, and for each replication we do the test. We do the test for sample sizes and . We do the test for and . The percentage of time the test statistic exceeds , that is is given in the tables, we also give plots of the empirical density of the test statistic.

5.1 Stationary time series

We first investigate the behaviour of the test statistic under the null hypothesis of stationarity.

-

(i)

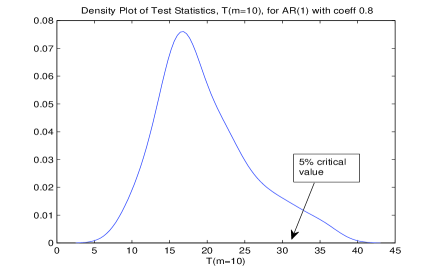

Model 1: , where are iid Gaussian random variables. We do the test for consecutive lags , the results can be found in the table below. A plot of the estimated finite sample density of the test statistic is given in Figure 3.

% reject 6 5 8 % reject 5.3 6.4 6.5 -

(ii)

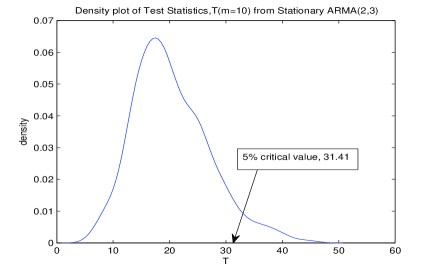

Model 2: , are Gaussian. We do the test for consecutive lags , the results can be found in the table below. A plot of the estimated finite sample density of the test statistic is given in Figure 3.

% reject 4.9 5.9 6.3 % reject 8.33 4.67 3.33

We observe that under the null of stationarity, the percentage rejects, in the tables, and the plots of the empirical density in Figure 3 suggest that the -distribution approximates well the distribution of the test statistic .

5.2 Nonstationary time series

We now investigate the performance of the test statistic under different types of nonstationary behaviour.

-

(i)

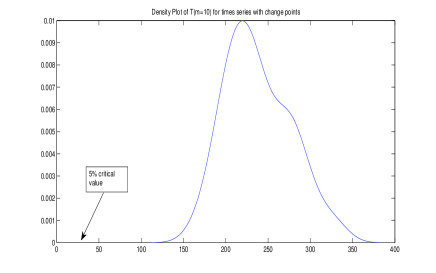

Model 3: In this model there is a change point occuring in the later part of the time series: for and for . We do the test for consecutive lags , the results can be found in the table below. A plot of the estimated finite sample density of the test statistic is given in Figure 3.

m=1 m=5 m=10 % reject 100 100 100 m=1 m=5 m=10 % reject 100 100 100 -

(ii)

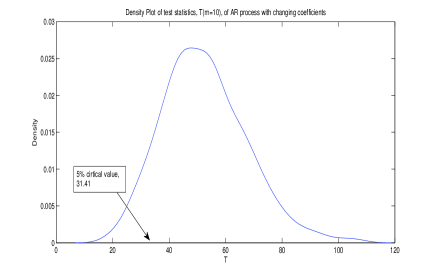

Model 4: In this model the variance of the innovation changes smoothly over time: where , where are Gaussian. We do the test for consecutive lags , the results can be found in the table below. A plot of the estimated finite sample density of the test statistic is given in Figure 3.

T=256 m=1 m=5 m=10 % reject 6.6 16.9 26.6 T=512 m=1 m=5 m=10 % reject 99.9 98 94.6 We mention, that for , function defined above, does not vary much, which explains why the rejection rate for is relatively low.

-

(iii)

Model 5: In this model there is a change point, but the change is quite small: for and for , where are Gaussian. We do the test for consecutive lags , the results can be found in the table below.

T=256 m=1 m=5 m=10 % reject 52 35.6 25.2 T=512 m=1 m=5 m=10 % reject 82 66 52 -

(iv)

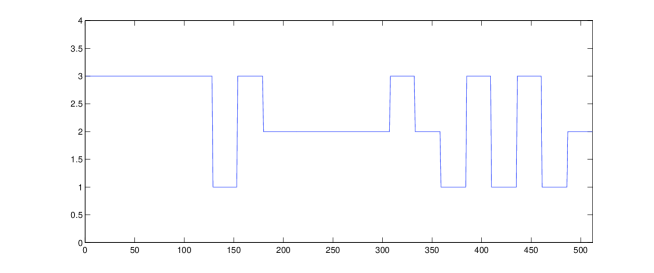

Model 6: In this model, the time series is independent with time-varying variance. Define the piecewise varying function

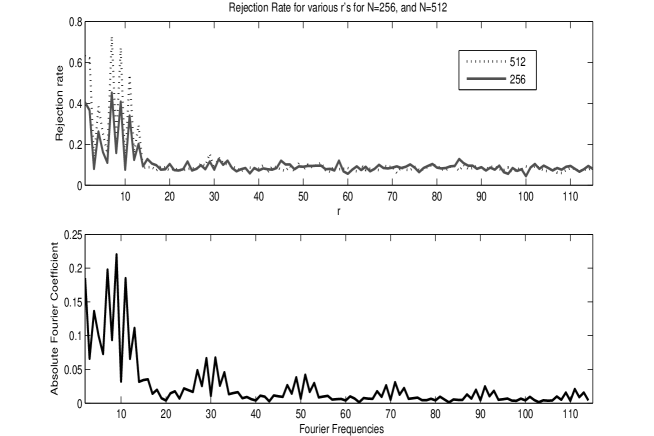

and the time series , where are iid Gaussian random variables. A plot of a realisation of the time series and the function is given in Figure 5. We do the test for consecutive lags , the results can be found in the table below.

T=256 m=1 m=5 m=10 % reject 39 59 79 T=512 m=1 m=5 m=10 % reject 62 85 99 We observe that the rejection rate increases as the number of lags used in the test grows. We now investigate why. In Figure 5, we plot the rejection rate of (hence one lag) at lags , we do this for both sample sizes and and we also plot the absolute values of the Fourier coefficients of the function for (ie. , where , which are estimated with ). We observe that with one lag (in the test statistic) the rejection rate is greatest at the frequencies that the Fourier coefficients are largest. This illustrates well the theory of the test statistic under the alternative. More precisely, for this model, the time-varying spectral density is approximately , and the noncentrality parameter is largest when the Fourier coefficient is largest.

We observe that for various types of nonstationary behaviour the test has good power. Moreover, we observe that for many types of nonstationarity, by using a few small number of lags , we are still able to reject the null hypothesis.

6 Real data analysis

To illustrate the test for second order stationarity we consider two real data examples. For both data sets we will use the test statistic . We choice , because the simulations in the previous section show that most nonstationary behaviour appears to be captured in the first four lags. We recall that under the null asymptotically has a chi squared distribution with eight degrees of freedom.

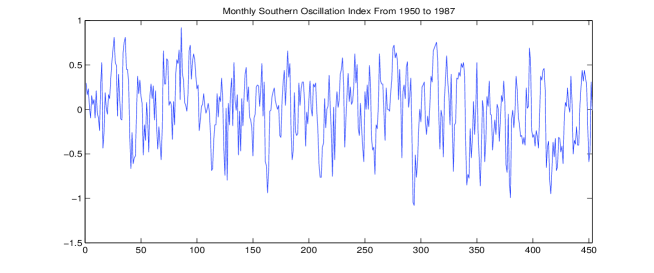

We first test for second order stationarity of the monthly southern oscillation index time series observed between January 1950 to December 1987 (). The data can be found at http://www.stat.pitt.edu/stoffer/tsa2/, a plot is given in Figure 6. The test statistic gives the value , which corresponds to a p-value of , hence there is no evidence to reject the null of second order stationarity.

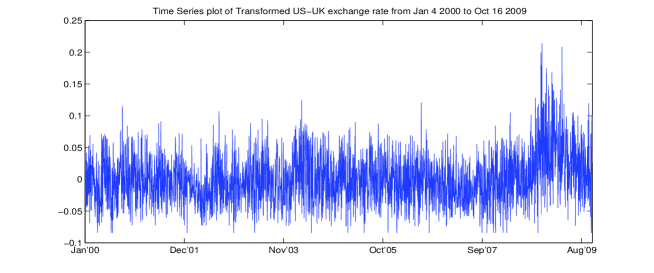

In our second data example we consider the daily British pound/US dollar exchange rate data observed between January 2000 to October 2009. This data was obtained from http://federalreserve.gov/releases/h10/Hist. In order to ensure the existence of moments we tranformed the data and considered the square root of the absolute log differences, that is , where is the exchange rate at time . A plot of the transformed data is given in Figure 7. The test statistic based on the entire data set gave the value , which corresponds to the p-value . Thus suggests there is evidence to reject the null of second order stationarity. To locate the regions of nonstationarity the data is partioned into segments of half length, quarter length and eighth length and the test was performed on each of these segments. The results are given in Table 1. Studying Table 1 and the p-values, there is evidence to suggest that for most periods there is no evidence to reject the null of stationarity. However, over the blocks June 2002 - November 2004, and August 2008 - October 2009, the data seems to be second order nonstationary. This information can be used to fit a model with time-varying parameters to the data.

| Jan’00 | Mar’01 | Jun’02 | Sep’03 | Nov’04 | Feb’06 | May’07 | Aug’08 |

7 Conclusions

In this article we have considered a test for second order stationarity. The test is based on the property that the DFT of a second order stationary time series is close to uncorrelated. The sampling properties of the test statistic under the null are derived under the assumption that the time series statisfies a short memory, representation. However, empirical evidence suggest that similar sampling properties also hold in the case of both stationary long memory and nonlinear time series too. For this general case, it may be possible to use some of the theory developed in ? (?), however, this is beyond the scope of the current paper and is future work.

Acknowledgements

The authors are grateful to Professor Manfred Deistler for several interesting discussions. This work has been partially supported by the NSF grant DMS-0806096.

Appendix A Appendix

In this appendix we prove the results from the main section.

For short hand, when it is clear that plays a role, we use the notation , , and .

A.1 Some results on DFTs and Fourier coefficients

In the sections below, under various assumptions of the dependence of , we will show asymptotic normality and obtain the mean and variance of . In the case that is a short memory, stationary time series, then it is relatively straightforward to evaluate the variance of , since are close to uncorrelated random variables. However, in the nonstationary case this no longer holds and we have to use some results in Fourier analysis to derive . To do this we start by studying the general random variable

where . We will show that under certain conditions on , can be written as the weighted average of . Expanding we see that can be written as

Without any smoothness assumptions on , it is not clear whether the inner sum of the above converges to zero as , and if the variance of converges to zero. However, let us suppose that . In this case, the DFT of , , is an approximation of the Fourier coefficient (the error in this approximation is discussed below). Noting that the Fourier coefficients as , we have

Now under relatively weak conditions on the Fourier coefficients, , is almost surely finite (and second order stationary if were stationary). Hence can be considered a weighted average of , where the weights in this case are random but almost surely finite. We now justify some of the approximations discussed above and state some well know results in Fourier analysis. An interesting overview of results in Fourier analysis is given in ? (?).

The following theorem is well known, see for example, ? (?), Theorem 6.2, for the proof.

Theorem A.1

Suppose that is a periodic function with period . We shall assume that either (a) or (b) and is piecewise montone function. Let

Therefore for all , we have in case (a) and in case (b) , where is constant independent of and .

Moreover .

We now apply the above result to our setup. We will use Lemma A.1, below, to prove the asymptotic normality result in Section A.4.

Lemma A.1

Suppose Assumption 3.1 or Assumption 4.1 is satisfied. And let be the spectral density of the stationary linear time series or the integrated spectral density of the locally stationary time series. Let

| (18) | |||||

| (19) |

Under the stated assumptions we have either has a bounded second derivative (under Assumption 3.1(iv-a) or Assumption 4.1) or that has a bounded first derivative and is piecewise monotone (under Assumption 3.1(iv-b)). Therefore, and .

PROOF. The above is a straightforward application of Theorem A.1.

Lemma A.2

Suppose Assumption 4.1 is satisfied. Define the th order cumulant spectra as

and the Fourier transform

| (20) |

-

(i)

If Assumption 4.1(iv)(a) holds, then and

(21) -

(ii)

If Assumption 4.1(iv)(b) holds, then , is a piecewise monotone function in and

(22)

We note that the constant is independent of the function and .

PROOF. To ease notation we only prove (ii), the proof of (i) is similar. We note that

Now under Assumption 4.1, and are bounded function, hence we see from the above that is bounded. Moreover, by using Theorem A.1 we have (21). The proof of (ii) is similar, and we omit the details.

We observe that in the stationary case , then for .

In the following lemma we consider the error in approximation of the DFT with the Fourier coefficient.

Lemma A.3

A.2 Proof of Theorems 3.1 and 4.1

The follow result is due to ? (?), Lemma 6.2, and is a generalisation of ? (?), Theorem 4.3.2, for locally stationary time series.

Lemma A.4 (Paparoditis (2009), Lemma 6.2)

Corollary A.1

The following well known result represents moments in terms of cumulants.

Lemma A.5

Let us suppose that . Then we have

| (24) |

where is a partition of and the sum is done over all partitions of .

We use the above lemmas below.

Lemma A.6

PROOF. To simplify notation in the proof we let . By expanding the expectation in (i) we have

| (25) | |||||

To prove the result we first represent the above moments in terms of

cumulants using Lemma A.5.

We observe that many of the terms will cancel, however those

that do remain will involve at least one cumulant which has

elements belong to the set

and

the set , since these

can only arise the cumulant expansion of

.

Now by a careful analysis of all cumulants involving elements from both

these two sets we observe that the largest cumulant terms are

and

(the rest are of a lower order). Therefore

recalling

that and using

Corollary A.1 gives

where is a finite constant independent of and .

The proof of (ii) is similar to the proof of (i), hence we omit the details. We note that if we were to show asymptotic normality of , then (ii) would immediately follow from this.

We now prove (iii). By definition of , using Lemmas A.4 and A.1, under Assumption 3.1(i) we have

Using a similar proof we can show that under Assumption 3.1(iv-a) or Assumption 4.1 we have . Thus proving (iii).

The proof of (iv) uses Lemma A.4 and Corollary A.1 and is straightforward, hence we omit the details.

Lemma A.7

PROOF. The proofs of (26) and (27) are very similar. Most of the time we will be obtaining the bounds under Assumption 4.1, however in a few places the bounds under Assumption 3.1 can be better than those under Assumption 4.1. In this case we will obtain the bounds under each of the Assumptions (separately).

To prove both (26) and (27) we first note that by the mean value theorem evaluated to the second order we have , where lies between and . Applying this to the difference we have the expansion

where

We consider the terms and separately. We first obtain a bound for . Observe that , where

hence we will obtain the bounds and . Expanding and using Lemma A.6(i) and that is bounded away from zero gives

| (28) |

Expanding gives

| (29) | |||||

The bounds for differ slightly, depending on the assumption. Under Assumption 3.1, by using ? (?), Theorem 4.3.2, it can be shown that (since ). Moreover, by using Lemma A.6(iii) we have . Therefore under Assumption 3.1 we have

| (30) |

Therefore, under Assumption 3.1, using (28) and (30) gives and

| (31) |

On the other hand, under Assumption 4.1 we do not have that , instead we substitute Lemma A.6(iv) into (29) and obtain

| (32) |

Therefore, under Assumption 4.1, using (28) and (32) gives and

| (33) |

We now obtain a bound for . Since the spectral density is bounded away from zero and (see ( ?), Lemma 6.1(ii)), we have , where

To obtain a bound for we use that , where

Using Cauchy-Schwarz inequality, Lemma A.6(ii,iv) we have

We now obtain a bound for . Using Lemma A.6(iii,iv) we have

A.3 The variance and expectation of the covariance

A.3.1 Under the null

It is straightforward to show, under Assumption 3.1, that . We now obtain the asymptotic variance of the under the null of stationarity. We mention that the following two lemmas apply to nonlinear time series too.

The following lemma immediately follows from ( ?), Theorem 4.3.2. We use this result to obtain the asymptotic variance of , below.

Lemma A.8

Let be a stationary time series where we denote the second and fourth order cumulants as and . Suppose and . Then we have

| (35) | |||||

Lemma A.9

Suppose the assumptions in Lemma A.8 hold. Then we have

| (38) | |||||

Furthermore if the tri-spectra is Lipschitz continuous we have

| (41) | |||||

and for all , .

PROOF. To prove the result we use that and , and evaluate , and . Expanding gives

where . Substituting (35) into the above it is easy to show that for we have and for we have

The same method gives us a similar bound for . Similarly it can be shown that unless we have . Also, for we have Altogether this gives us (38).

We now obtain (41) by using (38) and replacing the sum with an integral. By using that the spectral density and tri-spectra and are Lipschitz continuous we can replace the summand above with an integral to give

A similar result can be obtained for . Substituting the above into (38) gives (41).

Lemma A.10

Suppose Assumption 3.1 holds. Then the spectral density and the phase function , satisfy and .

PROOF. The fact that follows immediately from Assumption 3.1(i). To prove that we recall that . Differentiating with respect to and using the chain rule gives

Under Assumption 3.1(i,iii) we have , and . Therefore . Thus giving the required result.

PROOF of Lemma 3.1 We use Lemma A.9 to prove the result. We note that Assumption 3.1 satisfy the assumptions in Lemma A.9. Therefore we have the identity in (38). However in the case that the time series is linear this expression can be simplified. It is well know that for a linear time series the tri-spectra can be written in terms of the transfer function that is

Now we recall that for a linear time series hence substituting this into the ratio in (38) gives

Substituting the above into (38) gives

Finally we note that due to Lemma A.10, the phase is Lipschitz continuous, hence is Lipschitz continuous, and we can replace the summand in the above with an integral to give

This completes the proof.

A.3.2 The alternative of local stationarity

We now consider some of the moment properties of under the assumption of local stationarity.

PROOF. Expanding in terms of cumulants gives

finally substituting Corollary A.1 into the above gives the result.

PROOF of Lemma 4.1 equations (13) and (14) We first prove (13). We note that from the definition of in (1) and under Assumption 4.1 we have

| (43) |

We now obtain . We observe that

Now we substitute (42) into the above to give

We observe from the above that the covariance terms dominate the fourth order cumulant term. Moreover, by using Lemma A.2 we have , which gives . This together with (43) gives (13).

We now prove (14). Using Lemma A.4 for gives

| (44) |

Now by using replacing sum with integral and

using Lemma A.3 (noting

and

) gives

| (45) |

thus we have (14).

To prove (15) in Lemma 4.1, we evaluate the limiting variance of under the alternative of local stationarity.

Lemma A.12

A.4 Asymptotic normality

In this section we prove asymptotic normality of . Since the locally stationary linear time series model includes the stationary time series model as a special case we show asymptotic normality of the more general locally stationary model. We start by approximating with a random variable which only involves current innovations . We make this approximation in order to use the martingale central limit theorem to prove asymptotic normality of . In this section, we will make frequent appeals to Lemma A.1.

Using that the locally stationary time series model satisfies (11) we have can write as

where is the DFT defined in (18).

We now partition into terms which involve ‘present’ and ‘past’ innovation, that is

| (47) |

where

In the following lemma we obtain a bound for the remainder . Later we will show asymptotic normality of .

Lemma A.13

PROOF. We first observe that , where

We first show that . By the Minkowski’s inequality we have

It can be shown that

Substituting this into the bound for , under Assumption 4.1 and using Lemma A.1 we have

Using a similar method we can show that and . Thus we obtain the result.

Therefore the above lemma shows that .

Remark A.1

Now it is worth noting that in the case that is a stationary linear time series, then has an interesting form. That is, it is straightforward to show (using ( ?), Theorem 6.2.1) that

where .

We use the martingale central limit theorem to show asymptotic normality of , which will imply asymptotic normality of . To do this we rewrite as the sum of martingale differences

and

We now show that the coefficients in the martingale differences are absolutely summable.

Lemma A.14

Suppose Assumption 4.1 holds. Then we have

PROOF. To prove the result we note that under Assumption 4.1 and using Lemma A.1 we have

which gives the required result.

In the theorem below we show asymptotic normality of . To accommodate both the stationary and nonstationary case we will let the asymptotic variance of be and specify its value later.

Theorem A.2

Suppose Assumption 4.1 holds. Furthermore suppose that as . Then we have

PROOF. We use the martingale central limit theorem to prove the result. We will show asymptotic normality of . However, using the same method it straightforward to show asymptotic normality for all linear combinations of and and thus by the Cramer-Wold device to show asymptotic normality of the random vector . Let . To apply the martingale central limit theorem we need to verify that the variance of is finite (which is assumed), Lindeberg’s condition is satisfied and (see ( ?), Theorem 3.2). To verify Lindeberg’s condition, we require that for all ,

, where is the identity function and . By using Hölder and Markov inequalities, we obtain a bound for the following

| (49) |

Now by using Lemma A.14 we have , therefore

Since

is a positive random variable, the above result implies

.

Substituting this into (49) gives

as .

Finally we need to show that

| (50) |

Under the stated assumptions, we have as . Therefore it remains to show

which will give us (50). We will show that . To do this we note that and

| (51) |

Now by using the Cauchy Schwartz inequality and conditional expectation arguments for we have

We now show that . Let , then it is clear that for all , . Therefore, we have which gives

Expanding in terms of and using , it can be shown that as , and

Substituting the above into (A.4) we have , hence we have shown (50), and the conditions of the martingale central limit theorem are satisfied, giving the required result.

References

- Adak Adak, S. (1998). Time depedendent spectral analysis of a time series. J. American Statistical Association, 93, 1488-1501.

- Andreou and Ghysels Andreou, E., and Ghysels, E. (2008). Structural breaks in financial time series. In T. G. Anderson, R. A. Davis, J.-P. Kreiss, and T. Mikosch (Eds.), Handbook of financial time series (p. 839-866). Berlin: Springer.

- Berkes et al. Berkes, I., Gombay, E., and Horváth, L. (2009). Testing for changes in the covariance structure of linear processes. J. Statistical Planning and Inference, 139, 2044-2063.

- Briggs and Henson Briggs, W., and Henson, V. E. (1997). The DFT: An owner’s manual for the discrete fourier transform. SIAM.

- Brillinger Brillinger, D. (1981). Time series, data analysis and theory. San Francisco: SIAM.

- Brillinger and Rosenblatt Brillinger, D., and Rosenblatt, M. (1967). Asymptotic theory of estimates of k-th order spectra. Proceedings of the National Academy of Sciences, USA, 57, 206-210.

- Brockwell and Davis Brockwell, P. J., and Davis, R. A. (1987). Time series: Theory and methods. New York: Springer.

- Chen and Deo Chen, W., and Deo, R. (2004). A generalized Portmanteau goodness of fit test for time series. Econometric Theory, 20, 382-416.

- Cho and Fryzlewicz Cho, H., and Fryzlewicz, P. (2009). Multiscale and multilevel technique for consistent segmentation of nonstationary time series. Preprint.

- Dahlhaus Dahlhaus, R. (1997). Fitting time series models to nonstationary processes. Ann. Statist., 16, 1-37.

- Dahlhaus and Polonik Dahlhaus, R., and Polonik, W. (2006). Nonparametric quasi-maximum likelihood estimation for gaussian locally stationary processes. Ann. Stat., 34, 2790-2824.

- Giraitis and Leipus Giraitis, L., and Leipus, R. (1992). Testing and estimating in the change point problem of the spectral density. Lithuanian Mathematical Journal, 32, 15-29.

- Hall and Heyde Hall, P., and Heyde, C. (1980). Martingale Limit Theory and its Application. New York: Academic Press.

- Kokoszka and Mikosch Kokoszka, P., and Mikosch, T. (2000). The periodogram at the fourier frequencies. Stochastic processes and their applications, 86, 49-79.

- Loretan and Philips Loretan, M., and Philips, P. C. B. (1994). Testing the covariance stationarity of heavy tailed time series. J. Empirical Finance, 1, 211-248.

- Nason and Sachs Nason, G., and Sachs, R. von. (1999). Wavelets in time series analysis. Phil. Trans. R. Soc. Lond. A, 2511-2526, 357.

- Nason et al. Nason, G., Sachs, R. von, and Kroisandt, G. (2000). Wavelet processes and adaptive estimation of the evolutionary wavelet spectrum. J. Royal Statistical Society (B), 62, 271-292.

- Ozaki and Tong Ozaki, T., and Tong, H. (1975). On the fitting of non-stationary models in time series. In Proceedings of the 8th Hawaii Internation Conference on System Science (p. 224-226). Western Periodical Company.

- Paparoditis Paparoditis, E. (2009). Testing temporal constancy of the spectral structure of a time series. To appear in Bernoulli.

- Picard Picard, D. (1985). Testing and estimating change points in time series. Advances in time series analysis, 17, 841-867.

- Priestley Priestley, M. B. (1981). Spectral analysis and time series. London: Academic Press.

- Priestley and Subba Rao Priestley, M. B., and Subba Rao, T. (1969). A test for non-stationarity of a time series. J. Roy. Stat. (B), 31, 140-149.

- Robinson Robinson, P. (1989). Nonparametric estimation of time-varying parameters. In P. Hackl (Ed.), Statistical analysis and Forecasting of Economic Structural Change (p. 253-264). Berlin: Springer.

- Sachs and Neumann Sachs, R. von, and Neumann, M. H. (1999). A wavelet-based test for stationarity. Journal of Time Series Analysis, 21, 597-613.

- Subba Rao Subba Rao, T. (1970). The fitting of non-stationary time-series models with time-dependent parameters. J. R. Statist. Soc. B, 32, 312-22.