A new extrapolation method for weak approximation schemes with applications

Abstract.

We review Fujiwara’s scheme, a sixth order weak approximation scheme for the numerical approximation of SDEs, and embed it into a general method to construct weak approximation schemes of order for . Those schemes cannot be seen as cubature schemes, but rather as universal ways how to extrapolate from a lower order weak approximation scheme, namely the Ninomiya-Victoir scheme, for higher orders.

Key words and phrases:

weak approximation schemes, high order, cubature methods, extrapolation, Ninimiya-Victoir scheme, Fujiwara scheme. MSC 2000: Primary: 65H35; Secondary: 65C301. Introduction

The Ninomiya-Victoir scheme for the weak approximation of solutions of stochastic differential equations can be described in the following framework: let be a probability space and let be a -dimensional standard Brownian motion. Define and . We consider stochastic differential equations driven by the Brownian motion

| (1) |

where is in , and stands for Stratonovich integral. We associate for later use the following simple stochastic differential equations to equation (1)

| (2) |

Let and be the associated heat semigroups on such that for , and for . Notice here that the equation associated to the index is a pure drift equation, the semigroup a transport semigroup. Denote furthermore by

the generator of the diffusion process (1), two ordered products of (semi-)flows with generators and and the average of the two ordered products . Then we have the well-known short time asymptotics, formulated in the language of -norms (see Definition 4)

as , leading – by iteration – to the Ninomiya-Victoir scheme. Indeed, when we define -fold iteration of the operator

we obtain a scheme of weak approximation order , i.e.,

Let us define formally weak approximations of for a some fixed, finite of weak approximation order .

Definition 1 (scheme of weak approximation order ).

A family of linear operators on , continuous with respect to the supremum norm topology, is called a scheme of weak approximation order if there exists and some number such that

| (3) |

for all and for all .

Notice that the operator is only supposed to be linear and continuous with respect to the supremum norm topology on the set of -function, but not necessarily of sub-Markovian type. This means in particular that classical (Romberg-)extrapolations belong to this class.

In [5] T. Fujiwara constructs a sixth order scheme for smooth functions which consists of a linear combination of the previously described Ninomiya-Victoir scheme. Through the linear combination T. Fujiwara can “extrapolate” the weak approximation order to . In this paper, we define generalized Fujiwara schemes of order including the scheme in [5] by refining Fujiwara’s technique to prove the convergence order and construct versions of weak approximation order for . We finally obtain the following Theorem 4, whose proof can be found in Section 4, notations can be found in the subsequent sections:

Let be a generalized Fujiwara scheme of order , then

for is a scheme of weak approximation of order , where a choice of is given by

that means

for test functions .

The remainder of the article is organized as follows: in Section 2 we introduce all algebraic prerequisities, in Section 3 we show the main algebraic result of this article, which is then applied in Section 4 to prove the existence of generalized Fujiwara schemes. In Section 5 we provide an implementation result, where the results can be compared to [10]. The appendix is devoted to an original proof of Fujiwara’s basic algebraic result.

2. Algebraic prerequisites and their relation to weak approximation

Let be a set whose elements are . We call an alphabet and letters. A word in alphabet is a finite sequence of letters. Let be a empty word and a set of words including . If we impose a total ordering on , then together with word concatenation and lexicographic ordering becomes an ordered unital semigroup. Let be a set of noncommutative polynomials on over i.e. a set of –linear combinations of elements of and let be a set of noncommutative series of elements of with coefficients in , i.e. a set of functions with well ordered support. Using componentwise addition and multiplication, which is induced by word concatenation, makes a –algebra (see [4] for more details). The degree of a monomial is a number of letters contained in the monomial and the degree of a noncommutative polynomial and a noncommutative series are the maximum degree of monomials contained in them. Let and be the set of homogeneous polynomials of the degree and the set of polynomials of the degree less or equal to respectively. Define and in the same manner. Since every has a well ordered support, we can define and and it is easy to see that and are double sided ideals in algebra . Let and be the natural surjective maps from onto and respectively.

Since every subset of has a least element regarding lexicographical ordering, we have . The set is countable, therefore taking metric topology in makes with induced product topology into a Polish space. Hence, we can consider its Borel -algebra , –valued random variables and expectations, and other notions as usual.

For we define the exponential map

and for with vanishing constant term, we define the logarithm,

It is easy to check that

| (4) | ||||

| (5) |

on the respective domains. For define

Let us make the substitution, which is the heart of the transfer from algebra to numerical schemes, formally correct. Let be another alphabet including and set in the same manner. For all define an algebra homomorphism by setting

| (6) | ||||

| (7) |

for all .

Define next an algebra homomorphism by setting

| (8) |

Let . Clearly, and is a –subalgebra of . The homomorphism can then be uniquely extended to an –algebra homomorphism .

The algebra of non-commutative words plays a major role in the analysis of weak approximation schemes due to the following well-known asymptotic expansion theorem, which allows to approximate the truncated exponential series in by other simpler expressions.

Theorem 1.

For all function , and , it holds that

| (9) |

as .

Proof.

See [6]. ∎

Hence we can, e.g., express the generator of the diffusion process (1) by

in particular we obtain the following crucial asymptotic formulas,

as and again due to Theorem 1.

To be more precise on the goal of our paper, Theorem 1 also means that if we approximated by linear combinations of up to a certain degree within the algebra such that the remainder term is of order , then could be approximated by linear combinations of in a weak sense of order .

Notice that the letters correspond to squares of vector fields under , hence one has to work out the correspondence to exponentials of first order terms, too. The next lemma shows how to relate thoes linear semi-flows of PDEs to non-linear flows of ODEs up to a certain degree , namely by replacing the normal random variable by a random variable taking finitely many values and sharing moments up to order . This finally means that we can approximate by convex combinations of exponentials of first degree terms, i.e. leading to weak approximation schemes.

Lemma 1.

For all we have that

| (10) |

holds true. This formula also holds true under the homomorphism , i.e.,

for test functions and .

Proof.

Proof by applying the Fourier transform of Brownian motion and classical subordination results. ∎

3. How to approximate by ?

An alternative proof of this result can be found in the appendix:

Lemma 2 ( [5] Lemma 2.1).

We have

| (11) |

Proposition 1 ([5] Proposition 2.2).

There exists such that for all ,

holds.

Corollary 1.

Let be a linear combination of for some . If there exists such that , then .

Proof.

For all , holds. Hence, the case is clear. Suppose and . Since for some and since for all , it follows . According to Proposition 1

for some . Since , we have

for all . Then

which proves the corollary. ∎

Set

Corollary 2.

| (12) |

holds.

Corollary 3.

For all ,

| (13) |

4. Generalized Fujiwara scheme and its property

Definition 2 (Generalized Fujiwara scheme).

A family of series,

| (14) |

is called a generalized Fujiwara scheme of order if

holds.

A straightforward calculation involving induction gives the following connection concerning the powers of series in . Notice that we split the product into telescoping summands, where one, two up to terms of the form appear.

Proposition 2.

For and , we have

In particular for ,

holds true.

Lemma 3.

For , if and , then .

Proof.

By the assumption, monomials with the lowest degree contained in and are of the degree and . Then, monomial with the lowest degree contained in has the degree . Hence . ∎

Corollary 4.

For , if and , then .

Corollary 5.

For , if , then .

Theorem 2.

If a series,

| (15) |

is a -th order generalized Fujiwara scheme, then for all ,

| (16) |

holds true.

Proof.

Definition 3.

A generalized power series is an element of if for every , there exists a uniform bound for all the coefficients of the terms of with degree , which satisfies as .

Theorem 3.

If is an -th order generalized Fujiwara scheme, then

where for , and .

Proof.

Let . The case is trivial. Let be an -th order generalized Fujiwara scheme. Note that . Then by Proposition 2, we have,

Set

For set

and for define

In particular the summand can be written as

| (18) |

Let , be as in Proposition 1. By Theorem 2,

thus . Also it holds that

By Corollary 2, for all , holds. Thus, by Corollary 5, Corollary 4 and Proposition 1

| (19) |

holds, hence . Moreover,

Let with property for . By using similar arguments as in the proof of Theorem 2, we get

and

for all . We conclude, that .

It remains to prove that .

First, let us observe for . Choose . As above we can write

The coefficient of the power of the term of degree is of the form , where is the coefficient of of the same degree. Hence, the coefficient of the term of degree of

is a finite sum, namely

where and the number of summands do not depend on , and , . Let us denote . Thus, the coefficient of a term of degree of

has the following upper bound

Since the number of terms of

is finite and their number does not depend on , there exists a uniform bound for all of the coefficients, which proves our assertion for .

Let us observe the . As above

Since is a convex combination of products of all its coefficients are positive and the sum of all coefficients at the terms which are derived from by permutation of ’s is exactly the coefficient at the term of the in the (commutative) power series algebra, generated by , with coefficients in and the same goes for the coefficients of the power and the coefficients of the commutative series . The rest of the argument goes as in the case of , which gives us the upper bound of the coefficients at the terms of

∎

Now we are able – by means of our homomorphisms and to transfer the algebraic results into the realm of weak approximation schemes.

Definition 4.

Let and let . Define

Remark 1.

The function is a norm on .

Definition 5.

Let denote the space of bounded linear operators on . We can regard as a normed space with the operator norm.

Proposition 3 ([6]).

Fix a . The following assertions hold:

-

(1)

The family is a uniformly bounded subset of .

-

(2)

Let be the geneartor of the diffusion process (1) and let . Then, for we have

We are now able to formulate weak approximation schemes of order by means of our algebraic preparations. Recall therefore the definitions

of the building blocks of Ninomiya-Victoir schemes.

Theorem 4.

Let be a generalized Fujiwara scheme of order , then

for is a scheme of weak approximation of order , where a choice of is given by

that means

for test functions .

Proof.

Due to asymptotic formulas

and

where the constants in the Landau symbol depend on the derivatives of order at most . Therefore we can simply copy the proof of Theorem 3 by first replacing with and by . In the appearing sums we have to use the previous asymptotic formulas, namely

where the order behavior of the middle part has been shown in Theorem 3 and the order behavior of the other two summands follows from the previous asymptotic formulas. Apparently each term in , which is approximated due to the asymptotic formulas, increases the number of derivatives necessary to do the estimation by , which leads to the formula for . ∎

Example 1.

The case apparently corresponds to a version of the original Ninomiya-Victoir scheme.

Example 2.

The case corresponds to a scheme already presented in [5]. One can choose and and and .

Example 3.

The case corresponds to Fujiwara’s originally presented scheme, which in our language reads like follows. Notice that we do not need the full strength of our previous proof, which is built on Theorem 2.

For all mutually different numbers , we can construct -th order generalized Fujiwara scheme with a form:

5. Implementation of a –th order generalized Fujiwara scheme

A scheme for approximation of expectation of order six was first introduced by Fujiwara [5]. In previous sections we theoretically constructed schemes for approximation of expectation of order for arbitrary . In this section we show how to construct a practical scheme with approximating flow of vector fileds , which drive the SDE (1), by some suitable integration schemes. The usual choice for the integration schemes are Runge-Kutta methods. In our concrete example from mathematical finance we will use a seventh-order nine-stage explicit Runge-Kutta method with a very good stability, given by M.Tanaka et al. (see [11], [12] and [13]). Higer order Runge-Kutta mehod often lose stability with respect to rounding error, truncated error and piling error. In addition, these effect decrease order of approximating error. Since in a concrete application of the algorithm, e.g. in mathematical finance, some of the ODEs can be very close to being stiff, the stability of the Runge–Kutta algorithm is of high importance. We show a relation between convergence order of weak approximation scheme and -th order Runge-Kutta method. In addition we construct a concrete algorithm of a -th order generalized Fujiwara scheme and analyze its computational cost and its approximating error. At the end we present a concrete numerical experiment. Tanaka’s result is presented in the Appendix since we could not find any of his papers written in English.

The results of this section can be compared to those from [10].

5.1. Runge-Kutta method

For , the map represents the flow driven by the vector field starting at , i.e. the solution of the ordinary differential equation:

| (20) | ||||

Definition 6 ( stage explicit Runge–Kutta method of order for autonomous systems).

A stage explicit Runge–Kutta method of order for autonomous systems is determined by a lower triangular matrix and a row such that the following hold:

-

•

Let , and let for all . Given the vector as an approximation to , where satisfies the equation (20), the approximation to is computed by evaluating, for ,

where are given by

and then evaluating

-

•

The Taylor expansion of as a function of around should coincide with the Taylor expansion of up to (including) the term at the power .

Remark 2.

Usually Runge–Kutta methods are studied for general non-autonomous systems. In these cases the method is uniquely identified by a triplet , and , where and are as above and is a suitable column vector.

The next theorem shows that we need at least -th order Runge-Kutta method for -rd order generalized Fujiwara scheme.

Theorem 5.

For all , and , there exists such that

where and .

Proof.

The first inequality follows from the definition of -th order Runge-Kutta method and Taylor’s theorem. Set . By the definition of Runge-Kutta method and Taylor’s theorem again, we have,

Note that for all , holds. Thus the conclusion is true. ∎

The next theorem shows that if we do not urge to have computational cost, 4th order Runge-Kutta method is enough for sixth order scheme.

Theorem 6.

For , for all , for all , and for all , there exists such that

holds where .

Proof.

∎

5.2. Recipe for –th order generalized Fujiwara scheme

In the following subsection we will provide the pseudocode for implementation of the -th order generalized Fujiwara scheme with fixed coefficients . Let be as in the section 4 and let the function return the solution of the ODE (20) at time with initial condition .

Remark 3.

Usually in modern computers memory size is no longer an issue. From this perspective it seems sensible to generate all needed random variables in advance. Namely, the random variables for various ’s do not have to be independent, therefore we can reduce its number by reusing them, and there exist efficient algorithms which speed up the process of their generation if we do it in one batch instead of step by step as it is written in Algorithm 2.

5.3. Computational cost

Theorem 7.

Let be as above, such that is sufficiently small. Furthermore, assume that each step of the method needs operations, i.e. additions, multiplications and function evaluations, that operations are needed to generate a (pseudo or quasi) Bernoulli random variable and that operations are needed to generate a standard -dimensional normally distributed (pseudo or quasi) random variable. Then the computational cost of Algorithm 1 is .

Proof.

Let us denote the computational cost of the Algorithm 2 by . A straightforward calculation shows that the computational cost of the Algorithm 1 is equal to .

For fixed in Algorithm 2 we have operations. Hence, for fixed there are operations. It follows that . ∎

Remark 4.

The error of the algorithm consists of discretization part, i.e. the error due to numerical solution of ODEs and the error which comes from the scheme, and of the convergence error which comes from the Monte Carlo or quasi Monte Carlo simulation.

Theorem 8.

For such that is sufficiently small. The approximation error of Algorithm 1 is .

Remark 5.

One should take great care when choosing a suitable subdivision of the interval, since the coefficient of the discretisation error directly depends on function and vector fields , thus, although bounded, the coefficient can get fairly large in some cases. Moreover, the convergence error of the Monte Carlo simulation is directly proportional to the sqare root of variance of . As in the case of discretisation error this should be taken into account, since, although constant, the variance can be large comparing to the size of error we would like to achieve.

5.4. Numerical example

For our numerical example we have chosen the genearlized Fujiwara scheme of order with , and , i.e. the scheme that first appeared in [5], and the generalized Fujiwara scheme of order with the choice of parameters , , and .

In order to compare the algorithm to the basic Ninomiya-Victoir scheme we consider an Asian call option written on an asset whose price process follows the Heston stochastic volatility model. Let be the price process of an asset following the Heston model:

| (21) | ||||

where , is a two-dimensional standard Brownian motion, and are some positive coefficients satisfying to ensure that the volatility does not reach zero. The payoff of the Asian call option on this asset with maturity and strike is , where

| (22) |

Hence, the price of this option becomes where is an appropriate discount factor on which we do not focus in this experiment. As in [9] take , , , , , , and .

Up to the error of the magnitude we have

obtained from [8]. Let . SDEs (21) and (22) can be transformed in the Stratonovich form since :

where

| (23) | ||||

Taking our choice of into consideration we get exact solutions of ODEs of the type (20) driven by vector fields and (see [9] for more details):

| (24) | ||||

According to the proof of Theorem 5 we need a Runge–Kutta method of order at least to approximate the solution for generalized Fujiwara scheme of order and a Runge–Kutta method of order at least for a generalized Fujiwara scheme of order if we want a linear algorithm. If we allow quadratic computational cost for the the generalized Fujiwara scheme of the weak order , it is sufficient to use a Runge–Kutta method of order . In our example we used stage -th order Runge–Kutta method from [11], defined by the Butcher’s tableau presented in the Appendix.

The pseudorandom numbers in MC were generated by the Mersenne twister algorithm. The QMC was performed using Sobol sequence, generated by the library SobolSeq51.dll provided by Broda (see [1]). Both MC and QMC integration were performed using sample paths.

The use of exact solutions of ODEs driven by vector fields and reduces the computational cost of the algorithm by , where designates the order of weak generalized Fujiwara scheme divided by , denotes the number of MC/QMC sample paths, is the number of subdivision points and is the number of operations required for solving ODE’s driven by or , if we compare it to the results of Theorem 7.

| Method / | ||||

|---|---|---|---|---|

| NV | 0.00208536744970740 | 0.00095536839891733 | 0.00055694952858933 | |

| GF (order 6) MC | 0.00006154245956983 | 0.00003651735446759 | 0.00003522768790512 | |

| GF (order 6) QMC | 0.00005526280089 | 0.0000105789197729 | 0.0000040357269938 | 0.0000028986604713 |

| GF (order 8) MC | 0.00004536485526115 | 0.00003694928288030 | 0.000055051968504230 | |

| GF (order 8) QMC | 0.0000178413262662 | 0.0000013695959963 | 0.0000010913411477 |

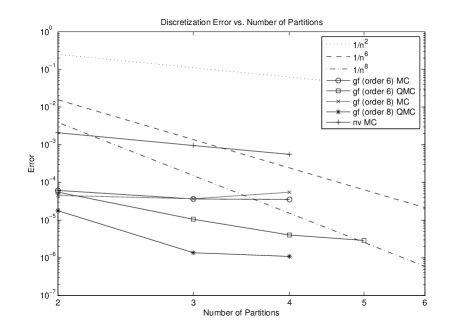

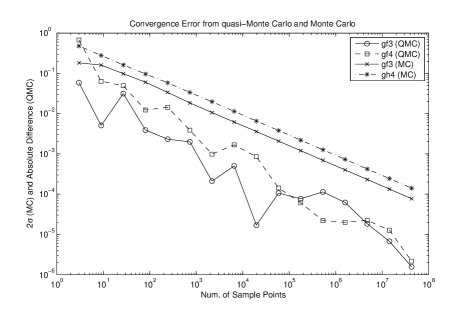

The graph in Fig. 1 clearly shows that the new extrapolation method reduces the order of the discretization error in comparison to the original Ninomiya-Victoir algorithm for several magnitudes. In the MC case the discretization error almost immediatly converges to the integration error (see Fig 1 and Fig. 2). Also in the QMC case the discretization error is soon (for small ) overshadowed by the integration error caused by QMC integration (see Fig. 2), the weak order of the extrapolated algorithms can still be observed from the slope of curves in the graph in Fig. 1.

Acknowledgements

The research was done while first and third authors were guests at the Research Unit of Financial and Actuarial Mathematics at the Vienna University of Technology. The research of the third author was supported by AMaMeF exchange grant No. 2080. A part of the research of the second and the third author was kindly supported by Vienna WWTF project “Mathematik und Kreditrisiken”. The second author was kindly supported by means of the START prize project Y 328.

References

- [1] British-Russian Offshore Development Agency (BRODA), http://www.broda.co.uk/.

- [2] Butcher, J. C., The Numerical Analysis of Ordinary Differential Equations, John Wiley & Sons, Chichester–New York–Brisbane–Toronto–Singapore, 1987.

- [3] Butcher, J. C., Numerical Methods for Ordinary Differential Equations, John Wiley & Sons, Chichester, 2003.

- [4] Cohn, P. M., Skew fields. Theory of general division rings, Encyclopedia of Mathematics and its Applications 57, Cambridge University Press, Cambridge, 1995.

- [5] Takehiro Fujiwara, Sixth order methods of Kusuoka approximation, UTMS 2006-7.

- [6] Nobuyuki Ikeda and Shinzo Watanabe, Stochastic Differential Equations and Diffusion Processes, Second Edition, Elsevier,1989.

- [7] Arturo Kohatsu-Higa , Weak approximations. A Malliavin calculus approach, Math. Comp., 70(2001), 135-172.

- [8] Mariko Ninomiya and Syoiti Ninomiya, A new weak approximation scheme of stochastic differential equations and the Runge–Kutta mathod, arXiv:0709.2434v3.

- [9] Syoiti Ninomiya and Nicolas Victoir, Weak approximation of stochastic differential equations and application to derivative pricing, Appl. Math. Finance 15, no. 1-2 (2008), 107–121. arXiv:math/0605361.

- [10] Mariko Ninomiya and Syoiti Ninomiya, A new higher-order weak approximation scheme for stochastic differential equations and the Runge-Kutta method. Finance Stoch. 13 (2009), no. 3, 415–443.

- [11] Tanaka, M., Kasahara, E., Muramatsu, S. and Yamashita, S., On a Solution of the Order Conditions for the Nine-Stage Seventh-Order Explicit Runge-Kutta Method(in Japanese), Information Processing Society of Japan, Vol. 33, No. 12(1992) 1506-1511.

- [12] Tanaka, M., Muramatsu, S. and Yamashita, S., On the Optimization of Some Nine-Stage Seventh-Order Runge-Kutta Method(in Japanese), Information Processing Society of Japan, Vol. 33, No. 12(1992) 1512-1526.

- [13] Tanaka, M., Yamashita, S., Kubo, E. and Nozaki, Y., On Seventh-order Nine-stage Explicit Runge-Kutta Methods with Extended Region of Stability(in Japanese), Information Processing Society of Japan, Vol. 34, No. 1(1993) 52-61.

- [14] V. S. Varadarajan, Lie groups, Lie algebras, and their representations, Springer–Verlag, New York, 1984.

6. Appendix

We give our original proof of Lemma 2.

Definition 7.

Let be a Lie algebra. For define and by the following recursion formula

where are coefficients defined in [14, 2.15.9]

For more details about see [14, Sec. 2.15].

Lemma 4.

| (25) |

Proof.

For the assertion is clear.

Suppose we have for all . By recursion we obtain

Using the induction hypothesis and bilinearity of Lie brackets, the above equation transforms into

which proves the assertion. ∎

Let denote .

Proof of Lemma 2.

The case is trivial. Next we consider the case . Using Baker–Campbell–Hausdorff formula to expand and and applying (25) proves the formula (11). By applying Baker–Campbell–Hausdorff formula to the definition of we get

Suppose that for all , we have

Using Lemma 4, the induction hypothesis and the BCH-formula on gives us

Thus, it is sufficient to show that for all and we have

| (26) |

Note that the equality in (26) holds trivially for .

Since is a homogeneous polynomial of degree , the assertion is clear for and all . It is easy to see that for we have

| (27) |

Let now for all and , then we have

Using (27), the induction hypothesis and the bilinearity of Lie brackets the above expression transforms into

Thus,

which is the desired result. ∎