A Coupled Markov Chain Approach to Credit Risk Modeling111Research partly supported by the Austrian National Bank Jubiläumsfond Research Grant 12306.

Abstract

We propose a Markov chain model for credit rating changes. We do not use any distributional assumptions on the asset values of the rated companies but directly model the rating transitions process. The parameters of the model are estimated by a maximum likelihood approach using historical rating transitions and heuristic global optimization techniques.

We benchmark the model against a GLMM model in the context of bond portfolio risk management. The proposed model yields stronger dependencies and higher risks than the GLMM model. As a result, the risk optimal portfolios are more conservative than the decisions resulting from the benchmark model.

1 Introduction

In this paper, we present a coupled Markov chain (CMC) model which builds on the approach in Kaniovski and Pflug (2007). The aim of the model is to come up with a statistical description of the joint probabilities of credit rating changes of companies, which does not depend on distributional assumptions of the joint distribution of the asset values of the companies. We assume the that the individual rating transitions follow Markov processes and model the dependency between rating migrations of different companies by coupling the corresponding Markov chains. The advantage of being able to describe the dependencies of the credit quality of multiple debtors is that risk management on a portfolio level can be based on such a model. Therefore, we assess the quality of the model in the context of a stylized bond portfolio optimization problem and compare the portfolio decisions based on the proposed coupled Markov model with the decisions based on a GLMM model from the literature. The results show that the proposed model yields more conservative decisions then the GLMM model.

A major advantage of the proposed model over Kaniovski and Pflug (2007) is that it lends itself to statistical estimation of the parameters. More specifically, we derive the likelihood function of the model and develop methods for finding solutions to the maximum likelihood problem – a task which is complicated by the fact that the likelihood function is non-convex and computationally expensive to evaluate.

Although agency ratings have been criticized for their sluggish response to fast evolving events (see Altman (1998); Crosbie and Bohn (2002); Lando and Skødeberg (2002); Nickell et al. (2000)), many models use credit ratings as a basis for assessing credit risk. The credit rating of a company condenses a range of qualitative and quantitative assessments of the credit worthiness of a company and therefore is a signal for the credit quality of the debtor, which is consistent over time as well as among different debtors. Furthermore, rating based valuations are of increasing importance since pending new banking regulations use ratings as an important input for calculating capital requirements for banks (see Basel Committee on Banking and Supervision (2004)).

The most commonly used rating based method for modeling credit risk is the CreditMetrics approach. The main idea behind CreditMetrics is similar to the one in this paper: the current rating of a company influences the default probability in the next period. The difference, however, to the proposed approach is the copula used to specify the joint behavior of the rating processes for different companies. In the CreditMetrics approach, a Gaussian copula is used for this purpose. There exist a range of models describing the joint default behavior of companies in the literature: for excellent surveys and model classifications see for example Crouhy et al. (2000); Duffie and Singleton (2003); Frey and McNeil (2003); Frydman and Schuermann (2008); Gordy (2000) or McNeil et al. (2005).

In McNeil and Wendin (2006, 2007), the authors propose a generalized linear mixed model (GLMM) for rating transitions which is estimated using Bayesian techniques. The model describes systematic risk factors as a combination of fixed and random effects and also allows for serial correlations in the unobserved risk factors and hence for so called rating momentum on a macroeconomic scale.

Stefanescu et al. (2009) propose a model for continuous credit worthiness variables, which are translated to discrete ratings by identifying a rating class with an interval of the credit worthiness score. The continuous credit worthiness variables are allowed to depend on obligor specific as well as macroeconomic factors, whereby the latter are used for modeling dependencies in rating transitions of different obligors.

In Korolkiewicz and Elliott (2008) credit quality is modeled by a hidden Markov model. The published credit ratings are considered to be noisy signals that give an indication of the true credit worthiness.

Models for credit quality based on ratings are also frequently used in the pricing and risk management literature, see for example Jarrow et al. (1997); Kijima (1998); Kijima and Komoribayashi (1998).

Note that there is some empirical evidence hinting to the fact that the Markov assumption of credit ratings does not always hold (see Altman (1998); Lando and Skødeberg (2002); Nickell et al. (2000)). The reasons for this might be contagion effects (cf. Giesecke and Weber (2006)) or long range dependencies in macroeconomic variables. Nevertheless, we do not consider more complicated models as the Markov assumption does not seem to be too wrong as shown in Kiefer and Larson (2007) and is implicit in most credit risk models.

This paper is structured as follows: Section 2 is devoted to a discussion of the coupled Markov chain model. In Section 3, we discuss a maximum likelihood approach which is subsequently used to estimate the parameters of the model from empirical data in Section 4. In Section 5, we compare the proposed model to a model by McNeil and Wendin (2006) and discuss the differences of two models in a risk management context. Section 6 concludes the paper.

2 The Model

The model is based on the ideas presented in Kaniovski and Pflug (2007). For sake of clarity, we postpone the discussion of the differences to the aforementioned paper to the end of this section.

We model joint rating transitions of companies in different rating classes belonging to different industry sectors, such that

-

1.

migrations of companies having the same credit rating are dependent;

-

2.

evolution of companies through credit ratings are dependent;

-

3.

every individual migration is governed by a Markovian matrix, which is the same for all the companies.

In line with Kaniovski and Pflug (2007), we assume that the rating migration process of each company is Markov with identical rating transition matrix and that these processes are coupled in such a way that they are statistically dependent because of their dependence on common systematic factors.

We start by considering a diversified portfolio consisting of debt obligations of different firms . The debtors are non-homogeneous in their credit ratings and belong to different industry sectors. Assume that there are non-default rating classes. The ratings are numbered in a descending order so that corresponds to the highest credit quality, while is next to the default class. For example, in terms of the rating scheme of Standard and Poor’s (S&P) we have, , , , , , , , , and with .

A company is fully characterized by its rating at time as well as its industry sector . Denote by the number of different industry sectors in the model, i.e. for all . Note that the sectoral classification can be replaced by any arbitrary discrete classification scheme without structurally changing the model. Possible alternative classifications could, for example, include size or geographic origin of the company.

Let be the probability that a company in rating class at the beginning of a time period ends up in rating class at the end of the period. In particular, is the probability that a debtor who is currently rated with -th credit rating defaults within the next period. The transition matrix can be estimated using one of the various techniques proposed in literature and is also reported by the rating agencies themselves. Since we are mainly concerned with the coupling of the rating processes, we assume the matrix to be known.

We suppose the evolution of the portfolio is modeled by a multi-dimensional random process . indicates the rating of company at the end of period , whereby period is the timespan between time points and . The marginals are modeled as dependent discrete-time Markov chains with state space , transition probability matrix , and absorbing state .

Similar to the classical one factor Gaussian model, the starting point of the specification of the dependencies between the rating processes of individual companies is the decomposition of risk factors in an idiosyncratic and a systematic factor. We split the rating movement of company at time in two components: a systematic component and an idiosyncratic component . Both components take values in with transition probabilities depending on . The non-trivial joint distribution of the vector is used to model dependency between the rating migration processes.

The rating of company at time is given by

| (1) |

The mixing between the idiosyncratic and the systematic component is achieved via a Bernoulli variable depending on the rating class of company at time , , as well as the industry sector of company . We define

| (2) |

and .

While the variables and are independent of all the other variables, the variables are independent of and , but have a non-trivial dependency structure within a given time period. The marginal distribution of and is dependent on the current rating class of the company and the transition matrix . In particular, we define

| (3) |

To model the dependencies between the components of the random vector , we divide the transition of in two parts: its tendency (i.e. up or down) and the magnitude of the change. To be more specific, let be a vector of Bernoulli variables, where determines whether a non-deteriorating move takes place for all companies with at time , i.e.

| (4) |

The probability of success of is given by

Observe that there are not but only tendency variables per time period . This renders the variables dependent via their dependance on and the non-trivial joint distribution of the same. Conditioned on the tendency, the magnitude of the change for a company with follows the distribution

| (5) |

and

| (6) |

Given the tendencies, the distribution of the magnitude is completely determined by the marginal distribution of the rating transitions, i.e. the matrix . Note that unconditional distribution of with is

| (7) |

i.e. identical to the distribution of .

The decomposition of a rating move in a tendency and a magnitude is useful since the tendency part can be used to model the dependencies between different debtors via the joint distribution of , which we do not restrict in our model. Finally, variables are modeled independent of one another.

Since depends only on the variables , and and these variables in turn only depend on and , is a Markov chain, i.e.

| (8) |

where and .

The model in (1) differs from the model presented in Kaniovski and Pflug (2007) (the KP model) in two aspects: in the specification of the dependencies and in the way parameter estimates are obtained. We start with discussing the former: the KP model reads

| (9) |

Note that at every point in time , there are only different variables and not of them like in the formulation proposed in (1). This implies that all companies with rating class , whose rating move is determined by the systematic risk factors (i.e. ) move exactly to the same rating class in period . Since this seems to be a strong assumption, we allow that companies are affected by the common risk factors to various degrees: while the direction remains same for all the companies in a specific rating class, the magnitude of the effect of the common risk factors is allowed to vary. This additional degree of freedom makes the filtering problem posed by the estimation of the model parameters easier since the definition of a common move gets wider and therefore the identification of these moves by the estimation procedure is easier (see Section 4). Furthermore, we only have to estimate the corresponding tendencies and not the magnitudes of the common move, which might vary between companies.

Note that the KP model assumes stronger dependencies between companies in the same rating class than model (1). To see this, let and be two companies in sectors and respectively. In (9), due to the independence properties of and for , we have

| (10) | |||||

| (11) | |||||

| (12) | |||||

| (13) | |||||

| (14) |

Similarly, we get

| (15) |

for model (1). Note that the two above expressions coincide as long as , i.e. the companies belong to different rating classes at time . However, if , we trivially have for the KP model while for (1)

| (16) |

with the exact value depending on the unconditional transition probabilities .

As mentioned above, the second difference is the estimation of model parameters: In Kaniovski and Pflug (2007) pairwise correlations between the tendency variables are assumed to be known and the joint distribution of these variables is found by an optimization approach. The probabilities in are manually tuned for small models to demonstrate the models flexibility and expressiveness. However, to use the model in practice, numerically tractable estimation routines are needed to obtain realistic parameter estimates for and . We therefore adopt a maximum likelihood approach to estimate the parameters of the model as discussed in the next section.

3 Maximum Likelihood Approach to Parameter Estimation

In this section, we introduce an approach to estimate the parameters of model (1), where is assumed to be known. For a model instance with non-default rating classes and industry sectors, there are unknown parameters in and degrees of freedom for the specification of the joint distribution .

Given a set of realizations of the rating process for firms of the dimensional process for a period of time steps, we estimate the parameters and the joint probability mass function for . Since we model rating transitions as coupled Markov chains, provides us with realizations of the process (1), but only with (hidden) joint realizations of . It follows that we can analyze every time step separately, but have to take into consideration the joint behavior of moves within each step. In the following, we derive the likelihood function by conditioning.

Because of the Markov property, the likelihood of given and is

| (17) |

The fact that is independent of yields and therefore, by the law of total probability, we have

| (18) |

where and .

To calculate the above sum, we divide the companies into groups. Let be the number of companies in sector which move from class to class in period . We start by analyzing these subgroups and fix , , and with and . We calculate the probability that the companies move from to as a function of the parameters to be estimated. Since , the only possibility for a deterioration to happen is that for all the corresponding companies. Therefore, the joint probability for these moves is

Now consider the case that and . In this case, the corresponding companies could move from either by a realization of (if ) or by a realization of (if ). Since all the combinations have to be considered, the probability is

| (19) |

where we abbreviate by . A similar logic applies for the case .

Splitting up all the moves in period according to industry sector and rating class, we get by the above argument

| (20) |

with

| (21) |

where . The likelihood function (17) can consequently be written as

| (22) | |||||

| (23) |

The above function is clearly non-convex in and , and since it consists of mix of sums and products, this problem can not be resolved by a logarithmic transform. Maximizing the likelihood for given data in the parameters and amounts to solving the following constrained optimization problem

| (28) |

where is the log likelihood function of the model. Note that the constraints in (28) imply that for all with and therefore,

It turns out that the evaluation of the likelihood is computationally expensive and numerically unstable because of the terms , which tend to get very small for high values of . To obtain a numerically and computationally more tractable version of the (28), we define

| (29) |

and derive a concentrated version of by replacing by . We now define

| (30) |

and replace by in (28). The concentrated likelihood is numerically more tractable and computationally less expensive than the original one, while yielding the same parameter estimates as the original formulation (see A for a proof).

4 Data Description & Parameter Estimation

4.1 Particle Swarm Algorithm

Since problem (28) is non-convex and the number of parameters to be estimated is too large to employ standard non-convex solvers, we use heuristic global optimization techniques. In particular, we employ a particle swarm algorithm, as described in Hochreiter and Wozabal (2009), to find a local optimum of (28). The main idea of the algorithm is that finitely many particles move in the feasible region of the problem. In each iteration of the algorithm, the objective value, corresponding to the position of the particle in the feasible region, is evaluated and the particle moves on. Each particle knows its best position till then (in terms of the likelihood function) and every particle knows the best position ever seen by any particle. The velocity of a particle changes in such a way that it is drawn to and to a random degree. Eventually, all the particles will end up close to one another and near to a local optimum of the problem.

In the following, we give a brief description of the algorithm, which follows the ideas in Kennedy and Eberhart (1995).

-

1.

Choose a convergence threshold and .

-

2.

Generate random samples for from the feasible region of (28). Each sample is the starting point of a particle. Set and for all .

-

3.

Set and .

-

4.

For all particles

-

(a)

First compute a velocity for the -th particle

(31) where , , are fixed constants, and are component-wise uniformly distributed random matrices of appropriate dimension and is the Hadamard (pointwise) matrix multiplication. The new position of the particle is

-

(b)

If then .

-

(a)

-

5.

If for some , then . Set .

-

6.

If or terminate the algorithm, otherwise go to 4.

Note that in step 4(a) of the above algorithm, a particle may leave the feasible region by violating the constraints on or . In this case, the particle bounces off the border and completes its move in the modified direction. For details on sampling from the feasible region as well as on the bouncing of the particles, we refer to Hochreiter and Wozabal (2009).

In our setting the PSA consistently reaches its final state after approximately 50 iterations. After this stage does not improve any further and the variance stays constant. Since it is hard to interpret the absolute values of , a meaningful bound for can not be found. We therefore exclusively used the criterion to terminate the loop.

The algorithm was implemented in MATLAB 2008a. For our calculations, we set and , which leads to a runtime of several minutes.

4.2 Data & Estimates

The estimation is based on yearly historical rating data for 10166 companies from all over the world as quoted by Standard & Poor’s over a time horizon of years ( - ). The data set comprises of observations of rating transitions between the S&P rating classes from AAA to D (not all the companies are rated over the whole time horizon). To reduce the number of parameters to be estimate, the rating classes are clubbed in the following way: , , , and , i.e. . Additionally, we incorporate information on industry sectors by distinguishing between industries according to the SIC classification scheme. Table 1 gives an overview of the composition of the sample used for fitting the model.

| Rating Class | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Sector (Number) | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Mining & Constr. (1) | 117 | 344 | 550 | 1078 | 924 | 710 | 84 | 16 | 0 | 40 |

| Manufacturing (2) | 194 | 777 | 2613 | 2953 | 2697 | 2749 | 208 | 30 | 0 | 135 |

| Tech. & Utility (3) | 258 | 1371 | 3914 | 3778 | 1448 | 1494 | 200 | 27 | 3 | 174 |

| Trade (4) | 22 | 148 | 572 | 871 | 777 | 837 | 45 | 1 | 0 | 38 |

| Finance (5) | 2617 | 9856 | 15317 | 12250 | 5806 | 2617 | 466 | 4 | 3 | 212 |

| Services (6) | 10 | 129 | 437 | 807 | 949 | 1171 | 87 | 3 | 0 | 40 |

We estimate the matrix of transition probabilities by simple counting as

| (32) |

Note that in the data set there are transitions from every non-default rating class to every other rating class, and therefore no problems associated with estimated probabilities being arise. The aggregation of the rating classes into a reduced set of classes was chosen after comparing several possible groupings. The current partition strikes a balance between parsimony and expressive power of the model.

The choices above leave us with parameters to be estimated. The estimated matrix can be found in Table 2, while the joint probability function for the can be found in Table 3. Along with the estimates of the elements of and , we provide standard deviations obtained by running the particle swarm algorithm times with different randomly sampled starting particles. As can be seen by the generally low values for the standard deviations, the algorithm is stable and converges to more or less the same solution in every run.

However, note that the reported standard deviations, measure the noise associated with the random nature of the particle swarm algorithm. In particular, the estimates are not based on asymptotic theory for maximum likelihood estimation. Hence, the standard deviations can be interpreted as a measure of stability of the stochastic solution algorithm applied to solve problem (28) but cannot be used for hypothesis testing.

| Rating Class | ||||

|---|---|---|---|---|

| Sector | 1 | 2 | 3 | 4 |

| 1 | 0.1974 (0.0008) | 0.0000 (0.0000) | 0.3745 (0.0023) | 1.0000 (0.0001) |

| 2 | 0.0793 (0.0007) | 0.0000 (0.0000) | 0.3205 (0.0015) | 1.0000 (0.0002) |

| 3 | 0.0168 (0.0005) | 0.0000 (0.0000) | 0.0000 (0.0002) | 1.0000 (0.0007) |

| 4 | 0.0000 (0.0001) | 0.0000 (0.0000) | 0.4943 (0.0035) | 1.0000 (0.0002) |

| 5 | 0.1469 (0.0004) | 0.0428 (0.0001) | 0.5068 (0.0013) | 1.0000 (0.0000) |

| 6 | 0.3127 (0.0032) | 0.0000 (0.0000) | 0.4514 (0.0021) | 1.0000 (0.0001) |

| Rating Class | Rating Class | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | Probability | 1 | 2 | 3 | 4 | Probability |

| 0 | 0 | 0 | 0 | 0.0000 (0.0000) | 0 | 0 | 0 | 1 | 0.0000 (0.0000) |

| 1 | 0 | 0 | 0 | 0.0000 (0.0000) | 1 | 0 | 0 | 1 | 0.0000 (0.0000) |

| 0 | 1 | 0 | 0 | 0.0000 (0.0016) | 0 | 1 | 0 | 1 | 0.0000 (0.0007) |

| 1 | 1 | 0 | 0 | 0.0397 (0.0035) | 1 | 1 | 0 | 1 | 0.0000 (0.0030) |

| 0 | 0 | 1 | 0 | 0.0000 (0.0000) | 0 | 0 | 1 | 1 | 0.0000 (0.0000) |

| 1 | 0 | 1 | 0 | 0.0000 (0.0000) | 1 | 0 | 1 | 1 | 0.0360 (0.0000) |

| 0 | 1 | 1 | 0 | 0.0000 (0.0043) | 0 | 1 | 1 | 1 | 0.0809 (0.0043) |

| 1 | 1 | 1 | 0 | 0.1733 (0.0063) | 1 | 1 | 1 | 1 | 0.6701 (0.0062) |

To test the validity of our modeling, we estimated the parameters of the model for the data set restricted to the transitions of the US companies in our sample. The results prove to be quite stable: All but one estimated parameter of the restricted model shows an absolute deviation less than 0.02 from the respective values for the full data set. The average absolute deviation is well under 0.01. This can be seen as evidence that the partitioning of companies according to industry sector is more meaningful than the partitioning into geographical subgroups.

Looking at the estimated values for , we note that for all the entries corresponding to the lowest rating class. This implies that companies next to default are mainly influenced by idiosyncratic factors and not by the economic environment. Another interesting finding is that companies belonging to the industry sector Transportation, Technology and Utility show a strong dependency on common economic factors, since for all . In general, rating classes and seem to be more affected by common moves than the classes and .

The estimate of the joint probability mass function of the tendency variables reveal that most combinations of up and down moves are assigned probability zero and that by far the most probable outcome is a non-deteriorating move for all the rating classes. Another entry with positive probability corresponds to the event that the investment grade assets (i.e. the first two classes) make a non-deteriorating move while companies in the other classes face a downward trend. This seems to be a plausible scenario in economically difficult times. A similar interpretation fits to the entry . However, slightly surprising there are two entries with positive probabilities which correspond to a downgrading of the highest and the second highest rating class, while the other classes are not downgraded.

In practice, one might want to restrict the number of parameters of the model by introducing tighter constraints on, for example, the entries of the matrix . As suggested by a referee, we exemplify this by testing whether the plausible restrictions for all , and lead to a more compact model without losing too much of the statistical quality. Examining the entries in does not suggest that the restriction is justified. Fitting the model with the abovementioned restriction reveals that the Bayesian information criterion (BIC) for the restricted model is 43777 while the BIC for the original model is 43401. Hence, the original model is preferable. This is confirmed by a likelihood ratio test, which rejects the restricted model for every reasonable level of significance.

5 Model Comparison

5.1 A Benchmark Model

To assess the quality of the CMC model, we compare it with a model proposed in McNeil and Wendin (2006) adapted to our setting. The aforementioned paper discusses GLMM models with latent factors. Debtors are split into buckets , which in our case consist of , i.e. all the combinations of industry sectors and ratings classes. The distribution of rating migrations for debtor in rating class and industry sector at time is modeled as

| (33) |

where are vectors in with increasing components, i.e. ( refers to the j-th component of the i-th vector). Furthermore, are random latent systematic factors used for modeling the dependency in rating transitions between debtors of different industrial sectors, while are factor loadings, which make this dependency rating class specific. Finally, the function is an arbitrary strictly increasing function which we choose as the logit link function, i.e. . It is assumed that conditional on the latent factors the rating transitions of the companies are independent.

Inspecting the model, it can be seen that the joint distribution of credit migrations depends on the current ratings as well as the sectoral information. In this sense, the model is similar to the model proposed in this paper. Except for the lack of an autoregressive component in the latent factors, (33) resembles model proposed in section 4.5 in McNeil and Wendin (2006). In this paper, we did not include a autoregressive term because we are dealing with yearly data as opposed to McNeil and Wendin (2006) who analyze quarterly transitions. As a result, there are too few time periods to estimate the parameters of the autoregressive process in a reliable manner: numerical experiments show that inclusions of an autoregressive term dramatically decreases the quality of the estimates. Furthermore, it turns out that estimated autocorrelation is close to zero – an observation which is plausible when considering yearly data.

To obtain the joint distribution of the rating transitions, we define the migration counts , where is the number of debtors from industry class with rating at time which are in rating class at the beginning of period . We further define as the overall number of debtors in rating class and industry sector at the beginning of period .

Based on (33), the joint distribution of the migrations in period is given by the following multinomial distribution

| (34) |

where with and

| (35) |

with for all .

Following McNeil and Wendin (2006), we estimate the model parameters by an application of the Gibbs sampler. To do this, we assign prior distributions to the parameters and unobserved variables in the model. In specific, we assign the independent normal prior to the variables , the vague prior to , an ordered Gaussian prior with covariance matrix to the vector (where is chosen large so as to ensure an non-informative prior), and finally the normal prior to . To ensure identifiability of the model, we fix the sign of to be .

When estimating the parameters of the model (33), we also implicitly estimate the unconditional transition probabilities, i.e. the matrix . However, the CMC model takes the matrix as an input. Thus, to ensure a fair comparison of the two models, we restrict the parameters for in such a way that the unconditional transition probabilities equal given the parameters and .

To fit the model, we iteratively sample from the full conditional distributions of the parameters. Samples from the full conditional distributions are generated using the ARMS algorithm, see Gilks (1992). For the numerical studies, we simulated iterations of the Gibbs sampler after an initial burn-in phase of iterations.444The estimation is implemented in R using the arms() method in the HI package for sampling from the full conditionals. One run of the Gibbs sampler takes several hours to complete. For a more detailed introduction into the topic of Gibbs sampling see Robert and Casella (2004) or in the context of the discussed models McNeil and Wendin (2006); Huang and Yu (2010). The results of the estimation along with standard deviations are reported in Table 4 and Table 5.555Note that, as opposed to the Markov Chain model, the standard deviations can be used to make inferential statements on the true values of the parameters.

| 0 | 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|---|

| 1 | 2.5460 | 6.9421 | 8.6172 | 9.7158 | ||

| (0) | (0.0233) | (0.0289) | (0.0289) | (0.0297) | (0) | |

| 2 | -3.8586 | 3.3129 | 6.1926 | 6.7005 | ||

| (0) | (0.0060) | (0.0059) | (0.0059) | (0.0064) | (0) | |

| 3 | -5.9054 | -2.5644 | 3.5128 | 4.5164 | ||

| (0) | (0.0621) | (0.0453) | (0.0453) | (0.0593) | (0) | |

| 4 | -6.3538 | -4.8364 | -1.6294 | 1.4457 | ||

| (0) | (0.0577) | (0.0562) | (0.0562) | (0.0286) | (0) | |

| 0.5284 (0.0537) | 1 (0) | 0.4389 (0.0497) | 1.6220 (0.1036) | 1.3698 (0.1353) |

5.2 Comparing Investment Decisions

To compare the two models, we set up a portfolio optimization framework, which uses the rating transition process as input. More specifically, we are interested in the risk minimal allocation of capital among a pre-specified set of corporate bonds. For this purpose, we represent the uncertainty about rating transitions of the companies as scenarios. The scenarios are sampled either from the GLMM model (33) or the CMC model (1) with the parameters as fitted in the last sections.

We base our analysis on 10,000 scenarios from each of the two models for a risk free rate of . To translate the simulated rating transitions into scenarios for losses, we implement a mark-to-market approach. Consider a scenario of rating transitions for years of company , i.e. is a realization of the Markov chain model in (33) or (1), where is the non-stochastic state of the world at the time the investment decision is taken. Assume, without loss of generality, that the price of each bond is and all bonds are sold at par at the beginning of the planning horizon and mature at time . Setting , the discounted loss of a corresponding bond for company in sector for scenario is equal to (cf. Gupton et al. (1997))

| (36) | ||||

where is the indicator function of the set , is the yield of a bond in rating class and industry sector with maturity at time 0, and finally are the forward zero rates of a bond for a company in rating class , sector and time to maturity years. The forward zero curves are calculated at the risk horizon of 1 year from the yields . To estimate the year yields of bonds in different sectors depending on the rating classes, we average over bond spreads as quoted on the 1/4/2008 by Markit Financial Information Services and add the risk free rate. For parsimony, we assumed that coupons are paid yearly and that the first coupon is paid even if the borrower defaults within the first year.

We start our analysis by evaluating the risk return profile of bonds in different sector/rating class combinations. A summary of this analysis can be found in Table 6.

| Rating | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Sectors | 1 | 2 | 3 | 4 | |||||

| CMC | 1 | -0.0407/ | -0.0024 | -0.0399/ | 0.1951 | -0.0351/ | 1.0000 | -0.0728/ | 1.0000 |

| 2 | -0.0414/ | -0.0111 | -0.0403/ | 0.2175 | -0.0429/ | 1.0000 | 0.0991/ | 1.0000 | |

| 3 | -0.0404/ | -0.0088 | -0.0397/ | 0.2254 | -0.0504/ | 1.0000 | 0.0721/ | 1.0000 | |

| 4 | -0.0401/ | -0.0044 | -0.0393/ | 0.2318 | -0.0431/ | 1.0000 | 0.1494/ | 1.0000 | |

| 5 | -0.0497/ | 0.0001 | -0.0437/ | 0.4211 | -0.1776/ | 1.0000 | -0.0710/ | 1.0000 | |

| 6 | -0.0392/ | 0.0148 | -0.0386/ | 0.2701 | -0.0516/ | 1.0000 | -0.1408/ | 1.0000 | |

| Rating | |||||||||

| Sectors | 1 | 2 | 3 | 4 | |||||

| Gibbs | 1 | -0.0407/ | -0.0093 | -0.0384/ | 0.2440 | -0.0491/ | 1.0000 | -0.0820/ | 1.0000 |

| 2 | -0.0414/ | -0.0081 | -0.0394/ | 0.1991 | -0.0582/ | 1.0000 | 0.0866/ | 1.0000 | |

| 3 | -0.0402/ | -0.0013 | -0.0385/ | 0.2206 | -0.0584/ | 1.0000 | 0.0648/ | 1.0000 | |

| 4 | -0.0400/ | 0.0014 | -0.0385/ | 0.2203 | -0.0609/ | 1.0000 | 0.1391/ | 1.0000 | |

| 5 | -0.0497/ | -0.0047 | -0.0406/ | 0.3768 | -0.1954/ | 1.0000 | -0.0800/ | 1.0000 | |

| 6 | -0.0392/ | 0.0076 | -0.0372/ | 0.2683 | -0.0676/ | 1.0000 | -0.1448/ | 1.0000 | |

Since the GLMM model is calibrated to have the same marginal transition probabilities, the results of the model from McNeil and Wendin (2006) are very similar to the respective figures for the CMC model. It turns out that the expected discounted losses as well as the risks in different industry sectors are quite different, with the financial sector (sector 5) emerging as the most attractive, except for companies in rating class .

To compare the implications of the two models in the context of risk management, we set up a simple scenario based asset allocation model. An optimal decision consists of a set of non-negative portfolio weights , where represents the percentage of the available capital invested into asset . Adopting the scenario based approach, we solve the following problem using the Conditional Value-at-Risk (CVaR) in the objective function

| (37) |

where is the inner product and is the vector consisting of all ones. The random variable describes the discounted losses of the individual bonds, as calculated in (36) from the rating transition scenarios. We use finitely many equally probable scenarios to represent . Notice that we use the variables , and to ensure that we get reasonable portfolio decisions, i.e. weights which are bounded from above and below, and this in turn makes the above problem a mixed integer problem.

The Conditional Value-at-Risk at level (CVaRα) of a random variable is defined as

| (38) |

where is the cumulative distribution function of and is its left inverse. In our case, the random variable is the portfolio loss and correspondingly is the average loss in the % of the worst scenarios.

Our choice of CVaR as a risk measure is motivated by its favorable theoretical properties. Since CVaR is a convex risk measure it leads to sensible decisions from an economic point of view, favoring diversification over concentration - a property that for example the Value-at-Risk lacks, see Pflug (2000). Moreover, CVaR being piecewise linear in the finite scenario setting, makes problem (37) numerically tractable, see Rockafellar and Uryasev (2000). Lastly, the fact that CVaR is closely related to the Value-at-Risk (VaR), which plays an important role in the Basel accord. In fact, it is easy to see that CVaR is an upper bound for VaR, making portfolios which have favorable CVaR-characteristics also attractive from a VaR perspective.666It can even be shown that the Conditional Value-at-Risk is the best conservative approximation of the Value-at-Risk from the class of law invariant convex risk measures, which are continuous from above (see Föllmer and Schied (2004), Theorem 4.61)

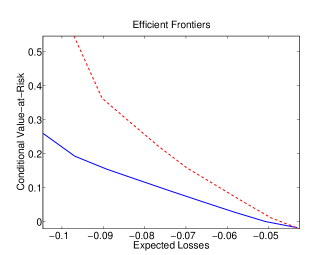

To obtain numerical results, we set up a hypothetical asset universe with one representative bond for each combination of sector and rating. Without loss of generality, we assume that the maturity of all the bonds equals years and set as discussed above. Furthermore, we set , for all and . To compare how well risks can be hedged for both the models, we solve problem (37) for varying levels of , spanning the whole range of feasible choices for . The resulting efficient frontier is depicted in Figure 1. Clearly, the scenarios generated by the GLMM model (33) allow for lower risks than the scenarios generated by the CMC models for most of the values of . This is an indication that the scenarios produced by the CMC model exhibit a higher correlation then the results from the GLMM model. Consequently, it is not possible to diversify risks to the same degree as in the GLMM model.

To compare the portfolio decisions produced by the two models, we set , i.e. equal to the risk free rate. The results are reported in Table 7. Interestingly, when using the scenarios from the GLMM model, only assets in the highest rating class are chosen, while the CMC scenarios lead to a more uniform utilization of asset classes with a significant share of the capital in the more risky rating classes. This might be due to the non trivial correlation structure of the variables .

| Sector | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Rating | 1 | 2 | 3 | 4 | 5 | 6 | ||||||

| 1 | 0. | 2 | 0. | 2 | 0. | 2 | 0. | 17 | 0. | 0539 | 0. | 0393 |

| 0. | 2 | 0. | 2 | 0. | 2 | 0. | 19 | 0. | 2 | 0. | 01 | |

| 2 | 0. | 0155 | 0. | 0165 | 0. | 0151 | 0. | 0114 | 0. | 0145 | 0. | 0108 |

| 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | |

| 3 | 0. | 01 | 0. | 0108 | 0. | 0105 | 0. | 0 | 0. | 0118 | 0. | 01 |

| 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | |

| 4 | 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 |

| 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | 0. | 0 | |

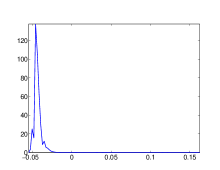

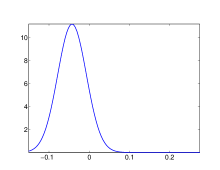

The return distributions of the optimal portfolios for are depicted in Figure 2. It can be seen that the loss distribution of the optimal portfolio for the GLMM model is much more concentrated and therefore less risky. The return distribution for the CMC model on the other hand has a long right tail and a significant part of the distribution is above 0, i.e. corresponds to losses. This confirms the observation made above that the scenarios representing extreme losses simulated from the CMC model are harder to hedge against. This in turn is another indication to the fact that there are stronger joint migrations in this model.

6 Conclusion

In this paper, we present a coupled Markov chain model for credit rating transitions based on Kaniovski and Pflug (2007). As opposed to the original formulation, our modification lends itself to a maximum likelihood estimation. We derive the likelihood of the model and obtain estimates of the model parameters by solving a simplified but equivalent non-convex optimization problem by heuristic global optimization techniques.

Subsequently, we generate a set of scenarios for joint rating transitions for a set of hypothetical companies and use these to compare the proposed model to a benchmark model from the literature. We find that for the model presented in this paper, there is a stronger dependency between the moves of single debtors. This in turn leads to more conservative portfolio decisions, since extreme risk can not be hedged to the same degree as in the benchmark model.

The flexibility of the approach as well as the computational tractability of large problem instances make the outlined methods interesting for practitioners.

Acknowledgements

The authors want to thank an anonymous referee for careful proofreading and many useful suggestions, which lead to a significant improvement of the paper.

Appendix A Justification of the Modified Likelihood Function

Since

| (39) |

and are fixed parameters not affected by the decision variables and , it is possible to concentrate out the terms without changing the optimizer of problem (28). In detail:

| (40) | |||||

| (41) | |||||

| (42) | |||||

| (43) | |||||

| (44) |

However, the last term does not depend on the decision variables but only on the data, i.e. is a constant in the optimization problem which can be omitted without changing the optimal solution.

References

- Altman [1998] Edward I. Altman. The importance and subtlety of credit rating migration. Journal of Banking & Finance, 22(10-11):1231 – 1247, 1998. ISSN 0378-4266. doi: DOI:10.1016/S0378-4266(98)00066-1.

- Basel Committee on Banking and Supervision [2004] Basel Committee on Banking and Supervision. International convergence of capital measurement and capital standards: A revised framework. Technical report, 2004.

- Crosbie and Bohn [2002] P. Crosbie and J. Bohn. Modelling default risk. Technical report, KMV Working Paper, 2002.

- Crouhy et al. [2000] Michel Crouhy, Dan Galai, and Robert Mark. A comparative analysis of current credit risk models. Journal of Banking & Finance, 24(1-2):59 – 117, 2000. ISSN 0378-4266. doi: DOI:10.1016/S0378-4266(99)00053-9.

- Duffie and Singleton [2003] Darrell Duffie and Kenneth J. Singleton. Credit Risk: Pricing, Measurement, and Management. Princeton University Press, 2003.

- Föllmer and Schied [2004] Hans Föllmer and Alexander Schied. Stochastic finance, volume 27 of de Gruyter Studies in Mathematics. Walter de Gruyter & Co., Berlin, extended edition, 2004. An introduction in discrete time.

- Frey and McNeil [2003] R. Frey and A. J. McNeil. Dependent defaults in models of portfolio credit risk. Journal of Risk, 6(1):59–92, 2003.

- Frydman and Schuermann [2008] Halina Frydman and Til Schuermann. Credit rating dynamics and markov mixture models. Journal of Banking & Finance, 32(6):1062 – 1075, 2008. ISSN 0378-4266. doi: DOI:10.1016/j.jbankfin.2007.09.013.

- Giesecke and Weber [2006] K. Giesecke and S. Weber. Credit contagion and aggregate losses. Journal of Economic Dynamics and Control, 30(5):741 – 767, 2006.

- Gilks [1992] W.R. Gilks. Derivative-free adaptive rejection sampling for Gibbs sampling, volume 4 of Bayesian statistics, pages 641 –49. Oxford University Press, Oxford, 1992.

- Gordy [2000] Michael B. Gordy. A comparative anatomy of credit risk models. Journal of Banking & Finance, 24(1-2):119–149, January 2000.

- Gupton et al. [1997] G.M. Gupton, C.C. Finger, and M. Bhatia. Creditmetrics–technical document. Technical report, J.P. Morgan & Co., New York, 1997.

- Hochreiter and Wozabal [2009] R. Hochreiter and D. Wozabal. Evolutionary approaches for estimating a coupled markov chain model for credit portfolio risk management. In Applications of Evolutionary Computing, EvoWorkshops 2009, volume 5484 of Lecture Notes in Computer Science, pages 193–202. Springer, 2009.

- Huang and Yu [2010] S.J. Huang and J. Yu. Bayesian analysis of structural credit risk models with microstructure noises. Journal of Economic Dynamics and Control, 34(11):2259 – 2272, 2010.

- Jarrow et al. [1997] Robert Jarrow, David Lando, and Stuart Turnbull. A markov model for the term structure of credit risk spreads. Review of Financial Studies, 10(2):481–523, 1997.

- Kaniovski and Pflug [2007] Y. M. Kaniovski and G. Ch. Pflug. Risk assessment for credit portfolios: A coupled markov chain model. Journal of Banking & Finance, 31(8):2303–2323, 2007.

- Kennedy and Eberhart [1995] J. Kennedy and R. Eberhart. Particle swarm optimization. In IEEE International Conference on Neural Networks, volume 4, pages 1942–1948. IEEE Computer Society, 1995. doi: 10.1109/ICNN.1995.488968.

- Kiefer and Larson [2007] Nicholas M. Kiefer and C. Erik Larson. A simulation estimator for testing the time homogeneity of credit rating transitions. Journal of Empirical Finance, 14(5):818 – 835, 2007.

- Kijima [1998] Masaaki Kijima. Monotonicities in a markov chain model for valuing corporate bonds subject to credit risk. Mathematical Finance, 8(3):229–247, 1998.

- Kijima and Komoribayashi [1998] Masaaki Kijima and Katsuya Komoribayashi. A markov chain model for valuing credit risk derivatives. Journal of Derivatives, 6(1):97–108, 1998.

- Korolkiewicz and Elliott [2008] M.W. Korolkiewicz and R.J. Elliott. A hidden markov model of credit quality. Journal of Economic Dynamics and Control, 32(12):3807 – 3819, 2008.

- Lando and Skødeberg [2002] David Lando and Torben M. Skødeberg. Analyzing rating transitions and rating drift with continuous observations. Journal of Banking & Finance, 26(2-3):423 – 444, 2002. ISSN 0378-4266. doi: DOI:10.1016/S0378-4266(01)00228-X.

- McNeil et al. [2005] A. J. McNeil, R. Frey, and P. Embrechts. Quantitative risk management. Princeton Series in Finance. Princeton University Press, 2005.

- McNeil and Wendin [2006] A.J. McNeil and J.P. Wendin. Dependent credit migrations. Journal of Credit Risk, 2(3):87–114, 2006.

- McNeil and Wendin [2007] A.J. McNeil and J.P. Wendin. Bayesian inference for generalized linear mixed models of portfolio credit risk. Journal of Empirical Finance, 14(2):131–149, 2007.

- Nickell et al. [2000] Pamela Nickell, William Perraudin, and Simone Varotto. Stability of rating transitions. Journal of Banking & Finance, 24(1-2):203 – 227, 2000. ISSN 0378-4266. doi: DOI:10.1016/S0378-4266(99)00057-6.

- Pflug [2000] G. Ch. Pflug. Some remarks on the Value-at-Risk and the Conditional Value-at-Risk. In Probabilistic constrained optimization, volume 49 of Nonconvex Optimization and its Applications, pages 272–281. Kluwer, 2000.

- Robert and Casella [2004] Christian P. Robert and George Casella. Monte Carlo statistical methods. Springer Texts in Statistics. Springer-Verlag, New York, second edition, 2004.

- Rockafellar and Uryasev [2000] R. T. Rockafellar and S. Uryasev. Optimization of Conditional Value-at-Risk. The Journal of Risk, 2(3):21–41, 2000.

- Stefanescu et al. [2009] Catalina Stefanescu, Radu Tunaru, and Stuart Turnbull. The credit rating process and estimation of transition probabilities: A bayesian approach. Journal of Empirical Finance, 16(2):216–234, 2009.