On The Existence Of Consistent Price Systems

Abstract.

We formulate a sufficient condition for the existence of a consistent price system (CPS), which is weaker than the conditional full support condition (CFS). We use the new condition to show the existence of CPSs for certain processes that fail to have the CFS property. In particular this condition gives sufficient conditions, under which a continuous function of a process with CFS admits a CPS, while the CFS property might be lost.

Key words and phrases:

Consistent price systems, No-arbitrage, Transaction costs, Conditional Full Support, Stability under Composition with Continuous Functions.1. Introduction

In markets with proportional transaction costs, a consistent price system (CPS) plays the role of a martingale measure in both hedging and absence of arbitrage problems, as highlighted by the recent results of Guasoni, Rásonyi, and Schachermayer (see [3, Theorem 1.3] and [4, Theorem 1.11]). Therefore it is crucial to study the existence of CPSs. Recall that a strictly positive adapted stochastic process defined on a filtered probability space that satisfies the usual conditions (i.e., the filtration is right continuous, and contains all of the null sets of ) admits an -CPS for if there exists an equivalent probability measure and a -martingale such that

Originally, the concept of CPS is due to Jouini and Kallal [5]. See [8] for further details.

In [3], Guasoni, Rásonyi, and Schachermayer introduced an important condition, conditional full support (CFS), for continuous stochastic processes and showed that CFS implies the existence of CPSs. (See equation (13), below, for the definition of CFS.) They proved that fractional Brownian motion (fBm) and certain continuous Markov processes possess the CFS property. Motivated by this result, in the subsequent papers [1, 2, 6, 7] several other processes were shown to possess the CFS property.

In Section 2 of this note, we give weaker sufficient conditions for the existence of CPSs. As an application of these results, in Section 3, we study the existence of the CPSs for transformed processes of the form , where is a continuous function and is a continuous process with CFS. Moreover, based on these results, we construct examples of processes that do not have CFS, and yet admit a CPSs.

2. Criteria for the existence of consistent price systems

Let us first recall the definition of random walk with retirement, introduced in [3]. To this end, let be a discrete-time filtered probability space such that and .

Definition 1.

A random walk with retirement is a -adapted process such that and

where and is a -adapted process in with the following properties:

-

(R1)

for all on for all ;

-

(R2)

on for all and , with the convention that ;

-

(R3)

.

Any random walk with retirement admits an equivalent probability measure , under which it is a uniformly integrable martingale [3, Lemma 2.6]. This fact will be used in our argument, below.

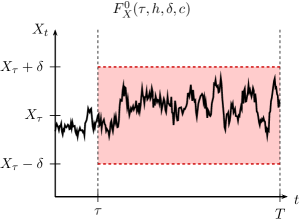

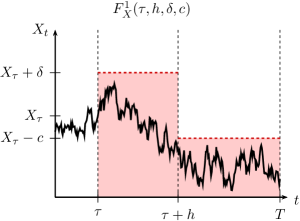

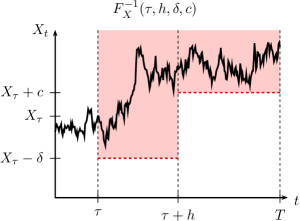

To state our main results, let be a continuous process adapted to the filtration . Moreover, for any , , , and any stopping time with values in , let

| (1) | ||||

The event is indeed independent of and , but we add these arguments for consistency with and . Roughly speaking, these three events correspond to staying in a tube, moving down, and moving up, respectively, after the stopping time —see Figure 1 for an illustration.

Theorem 1.

Let be a continuous process adapted to filtration . If there exists such that for any and stopping time with values in , and ,

| (2) |

then admits an -CPS with .

Proof.

As in proof of Theorem 1.2 of [3], we set up a CPS for using a random walk with retirement associated with . We divide the proof into three steps.

Step 1. Define

| (3) |

and

| (6) |

for all . Moreover, set

| (7) |

By construction, for all and is adapted to the filtration , given by .

Step 2. We will check that satisfies the conditions of a random walk with retirement on the filtered probability space , with . To show this, we need to check (R1)–(R3) in Definition 1. Clearly, condition (R1) is satisfied, and (R3) is a consequence of the continuity of . Therefore, we only need to check that

| (8) |

for all . This is equivalent to showing that for any with

and ,

Let be such that . Let and . Denote

Note that is a stopping time and its values are in . By the assumption of the theorem, we have

for any . Note that with , and therefore, the events

have positive probability, which, in turn, implies for any . Since , the result follows.

Step 3. Since is a random walk with retirement, thanks to Lemma 2.6 of [3], there exists an equivalent probability measure such that is a uniformly integrable martingale. Let . For each , set . Observe that , and that on the set for all . Thus the following holds

| (9) |

We write . Note that each of , , and takes values in on the set . Therefore, from (9), we have

Since , we conclude that

| (10) |

Therefore is an -CPS for , with . ∎

Remark 1.

If is adapted to a sub-filtration of and (2) holds with respect to for , then it also holds with respect to the smaller filtration for .

The condition (2) in Theorem 1 needs, of course, to be checked for a very wide class of stopping times. Depending on the process , direct verification of (2) might be a difficult task. To overcome this difficulty, we establish the following variant of Theorem 1 with a sufficient condition that involves only deterministic times.

Theorem 2.

Let be a continuous process adapted to filtration . If there exists such that for any , , , , and ,

| (11) |

then admits an -CPS for any .

Proof.

By Theorem 1, it suffices to show that (11) holds whenever is replaced with any stopping time that assumes values in . We use a strategy that is similar to the proof of Lemma 2.9 of [3] and assume, contrapositively, that there is , stopping time with values in , , and such that

| (12) |

for some . We will consider here only the case . When , it suffices to invoke Lemma 2.2 of [6], whereas the case is completely analogous to .

For brevity, let us write . By (12) and the definition of conditional expectation, we have . The continuity of the paths of implies that , where

Since , there is such that . Let us consider the stopping time

where , , that clearly satisfies on and on . Note that and on , and that . Hence, on ,

Moreover, on ,

We have thus shown that , where

Furthermore, and . Finally, we have

whence on , and the assertion follows. ∎

Let us briefly compare the criteria above to the conditional full support property, mentioned in the introduction. Recall that a continuous process has conditional full support (CFS) if

| (13) |

where denotes the space of continuous functions with and “supp” denotes the support (the smallest closed set of probability one). Actually, the CFS property holds if and only if (13) is satisfied also when is replaced with an arbitrary stopping time [3, Lemma 2.9].

The sufficient conditions for the existence of an -CPS for arbitrarily small established in Theorems 1 and 2 are weaker than CFS. In particular, they are local in the sense that they do not require that remains -close to, e.g., a continuous function with arbitrarily large maximum with positive conditional probability, like CFS does. This is illustrated by the following consequence of Theorem 2.

Corollary 1.

Let be a continuous process adapted to filtration . If there exists such that for any and continuous, monotone function with ,

| (14) |

then admits an -CPS for any .

3. Application to transformed processes

As an application of the results above, we study the existence of CPSs for processes of the form , where is a continuous surjection and is a process with CFS.

Proposition 1.

Assume that is continuous process with CFS. Let and be a continuous function that satisfies either of the following:

Then

| (16) |

for any , any stopping time with values in , and any .

Proof.

We will show the result for continuous functions that satisfy condition (a). The proof for any that satisfies condition (b) is similar and will be omitted.

Let and be an -stopping time with values in . In order to prove (16), we need to show that for any with . Fix any with . Let be such that the event

has positive probability. Note that . Since is uniformly continuous on , there exists such that , whenever and .

(i) Proof that : Note that

for any , and by our assumption, we have that . Therefore, , which implies .

(ii) Proof that : Let be such that for all . By our assumption on , we have that a.s. Therefore, . Observe that on ,

Therefore, if , then , which implies that

As a result, . If, on the other hand, , then since , we have . Therefore, on ,

Moreover, on , we have that

This implies that

which in turn implies that

Now, since on , it follows that

We conclude that from which the result follows since .

(iii) Proof that : The proof is similar to part (ii). ∎

The properties (a) and (b) above essentially mean “nearly increasing” and “nearly decreasing” respectively, and they would reduce to monotonicity for . In fact, for this particular case the following holds true.

Corollary 2.

If is a continuous process with CFS and is a monotone, continuous surjection, then admits an -CPS for any .

Proof.

Assume is non-decreasing and satisfies the first two conditions of (a) in Proposition 1. Then it also satisfies the third condition of (a) for any . Therefore, by Proposition 1, (16) holds for any and . Thus, from Theorem 1, we conclude that admits -CPS for any . The proof for the case of non-increasing function follows similarly. ∎

It is worth noting that unless the continuous functions are strictly monotonous in the above corollary, does not have CFS in general. The next corollary covers cases when the continuous function is not monotonous.

Corollary 3.

Let be a continuous process with CFS. If is a continuous function that satisfies the first two conditions in either (a) or (b) in Proposition 1, then for any we can find a small enough such that satisfies

| (17) |

for any , any stopping time with values in , and any . In particular,

Remark 2.

It is clear that the surjectivity of is not a necessary condition for the existence of CPSs for . In particular, if is a bijection, where and has CFS, then the results of [6] can be used to construct CPSs for . However, when is not bijective and assumes the value or , it appears to be an open problem whether can have a CPS.

The next example is to illustrate how Corollary 3 can be applied.

Example 1.

Consider the process

where is a fractional Brownian motion with Hurst parameter . The function satisfies the first two conditions in (a) of Proposition 1. Also,

Therefore, for any the process admits an CPS whenever .

The following is an important example where has CFS and does not, while admits CPSs.

Example 2.

First, let us recall an implication of the CFS property: If has a CFS, then

| (18) |

for any valued stopping time , and any with , and any and . (As mentioned before, this follows from Lemma 2.9 of [3].)

Now, let be a standard Brownian motion. For , consider , where

Let us prove that does not have the CFS property for any . Let

On the set the paths of the process are non-negative, whereas on we have that . Therefore, if we let , then we have

Thus, does not have the CFS property for any .

Finally, it is worth stressing that without transaction costs, does admit arbitrage opportunities. It follows from the CFS property of Brownian motion that the simple short strategy , where

is an arbitrage.

Acknowledgements

We are grateful to the anonymous referee for his/her comments which helped us improve our paper. We would like to express our thanks to Paolo Guasoni for his helpful comments. E. Bayraktar is supported in part by the National Science Foundation under a Career grant, DMS-DMS-0955463, and in part by the Susan M. Smith Professorship. M. S. Pakkanen acknowledges support from CREATES, funded by the Danish National Research Foundation, and from the Aarhus University Research Foundation regarding the project “Stochastic and Econometric Analysis of Commodity Markets”.

References

- [1] Alexander Cherny. Brownian moving averages have conditional full support. Ann. Appl. Probab., 18(5):1825–1830, 2008.

- [2] Dario Gasbarra, Tommi Sottinen, and Harry van Zanten. Conditional full support of Gaussian processes with stationary increments. Journal of Applied Probability, 48(2):561–568, 2011.

- [3] Paolo Guasoni, Miklós Rásonyi, and Walter Schachermayer. Consistent price systems and face-lifting pricing under transaction costs. Ann. Appl. Probab., 18(2):491–520, 2008.

- [4] Paolo Guasoni, Miklos Rasonyi, and Walter Schachermayer. The fundamental theorem of asset pricing for continuous processes under small transaction costs. Annals of Finance, 6:157–191, 2010.

- [5] Elyes Jouini and Hédi Kallal. Martingales and arbitrage in securities markets with transaction costs. J. Econom. Theory, 66(1):178–197, 1995.

- [6] Florian Maris, Eric Mbakop, and Hasanjan Sayit. Consistent price systems for bounded processes. Communications on Stochastic Analysis, 6 (4):633–645, 2011.

- [7] Mikko S. Pakkanen. Stochastic integrals and conditional full support. Journal of Applied Probability, 47 (3):650–667, 2010.

- [8] Walter Schachermayer. The fundamental theorem of asset pricing under proportional transaction costs in finite discrete time. Math. Finance, 14(1):19–48, 2004.